KO: Buy ideaBuy idea on KO as you can see on the chart because we have the breakout with force the vwap and the resistance line by a big green candle.

KO trade ideas

KO short ideaas you see on chart we can built short setup because stoch rsi overbought and this stock still in downtrend.

Coca-Cola: Keep Going! In the short term, KO should still climb higher with the current blue wave (y). After the high, we expect another downward move, but ultimately, the resistance at $63.76 should be exceeded again. It is important for the support at $57.93 to hold for our scenario to remain valid.

Anticipating a reversal hereDaily chart bounce of the 50 ma has occured. Price is respecting the overall bullish channel. Waiting for a breakout of the short term channel. Also a positive change in the macd. That along with a candle close above the short term resistance.

LONG TERM OUTLOOK ON DIVIDNED LEGENDBased on the current structure off the bottom of the Covid 19 correction, it appears we have a clean wave 1 and 2, and we are possibly in the beginning stages of wave three, with weekly RSI and MACD supporting the theory. That said, looks like price is currently in wave 1 of 3, which we would like to see target the .618 extension, but with the greater market in a tight spot, momentum doesn't support it, hence the current wave 3 target being the 1.382 extension. Once we have more information regarding wave 1 of 3, we can clean up the forecast. That said, this looks like a viable option for dividend investors and leaps contracts.

$KO Nice Weekly BreakoutNice years long consolidation resolving on the weekly chart for $KO. This name pretty much only goes up over the years but is not explosive like some of our other favorite names. Buy shares or buy a lot of time on the options contracts and let this one ride till the end of the year and beyond if you have a longer-term investment horizon. Kind of a no brainer.

LETS BUY THIS SHARE (KO)I think KO will go up and hit 64.30 based on elliot analysis.

so you can enter at current price ( 62.80 ) and stop loss would be 61.50.

R/R is almost 1 and possibility of hitting tp is about 70 percent.

good luck.

The 3 Step System You Can Use For Technical AnalysisThe rocket booster strategy may take you time to understand

but i want you to look at the chart above what do you see?

--

You will notice the following 3 steps:

-The price is above the 50 MA

-The price is above the 200 MA

-The price has gapped above the both MA's

--

This is how the parabolic system can be used with the rocket booster strategy for short-term trading

--

But you need to remember that in short-term trading you

always have to take profits

--

If you want to invest then I would suggest you study

fundamental analysis

because this is not what I write about

My goal is to teach Technical analysis for short-term trading only.

If you got value from this rocket boost this content to learn more.

--

Disclaimer: Trading is risky you will lose money whether you like it or not because of this you need to learn risk management

KO: Sell ideaSell idea on KO as you see on the chart after the breakout with force the vwap by a big red candle follow by a large red volume!.Thanks!

Barclays projects Coca-Cola shares to climb 16%. Idea 18/04/24Shares of The Coca-Cola Company have hovered around the same trading level for the last two and a half years, but analysts at Barclays now predict a potential surge of approximately 16% in the coming months, with a target price of 68 USD in sight. This optimistic forecast is rooted in anticipated growth within the global carbonated drinks market, where Coca-Cola is a major player. The expected market expansion is projected to fuel increases in Coca-Cola's sales.

Additionally, Coca-Cola's long-standing status as a dividend aristocrat – known for consistently paying and increasing dividends for over 25 consecutive years – further bolsters confidence in the company's financial stability and growth prospects.

Analysing Coca-Cola Co. (NYSE: KO) stock for potential trading opportunities:

In the Daily (D1) timeframe, the stock has established a 57.95 USD support level and a resistance at 59.40 USD. Having broken out of its previous trading channel, it has entered a downtrend and is currently testing the trend line. If the support level is breached, a fall to 56.40 USD could be imminent.

However, if the stock can break through the resistance at 59.40 USD, it presents a buying opportunity with a short-term target of 62.50 USD. For investors with a medium-term outlook, holding a position with a target of up to 66.40 USD may be worthwhile.

—

Ideas and other content presented on this page should not be considered as guidance for trading or an investment advice. RoboMarkets bears no responsibility for trading results based on trading opinions described in these analytical reviews.

The material presented and the information contained herein is for information purposes only and in no way should be considered as the provision of investment advice for the purposes of Investment Firms Law L. 87(I)/2017 of the Republic of Cyprus or any other form of personal advice or recommendation, which relates to certain types of transactions with certain types of financial instruments.

Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69.88% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

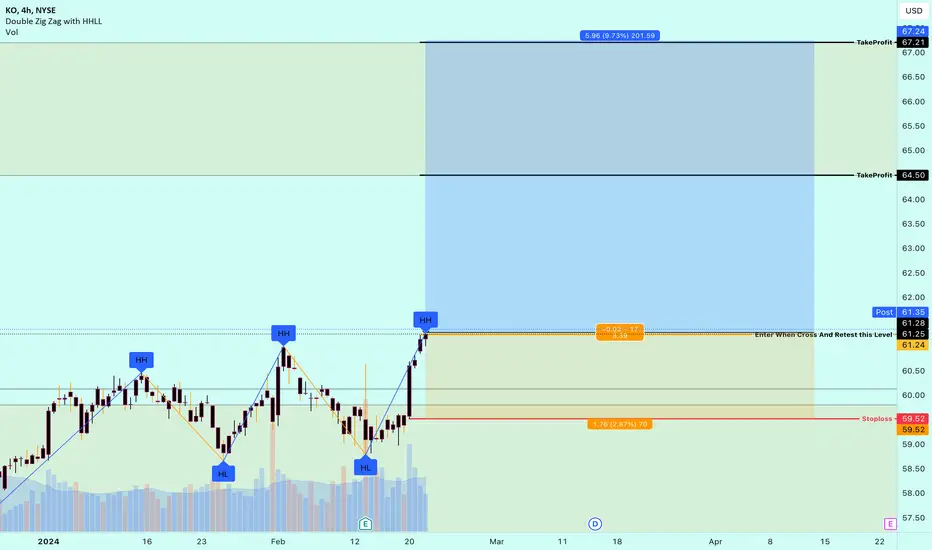

KO potential buy setupReasons for bullish bias:

- Entry at HH breakout

- Basic DOW

Here are the recommended trading levels:

Entry Level(CMP): 61.18

Stop Loss Level: 59.54

Take Profit Level 1: 62.82

Take Profit Level 2: Open

🥤 Coca-Cola (KO): Strong Performance and Positive Momentum! 📈📊 Analysis:

Coca-Cola NYSE:KO

Strong Performance: Reported a 12% increase in organic sales in 2023.

Guidance: Management's guidance indicates continued positive momentum into 2024.

Restructuring Success: Restructuring efforts led to rising revenue and net income.

Diversification: Expansion into energy drinks and sparkling water diversifies product portfolio for future growth.

📈 Bullish Sentiment:

Entry Range: Suggested entry above the $53.00-$54.00 range.

Upside Target: Target set at $75.00-$77.00, reflecting confidence in KO's ability to navigate challenges and capitalize on opportunities.

🌐 Note: Monitor KO's performance and execution of diversification strategy for sustained growth! 📊💹 #KO #BullishSentiment #PositiveMomentum 🥤📈

COCA-COLA $KO - Feb. 20th, 2024COCA-COLA COMPANY NYSE:KO - Feb. 20th, 2024

BUY/LONG ZONE (GREEN): $60.10 - $63.00

DO NOT TRADE/DNT ZONE (WHITE): $58.85 - $60.10

SELL/SHORT ZONE (RED): $56.65 - $58.85

Weekly: Bullish

Daily: Bullish

4H: Bullish

Currently holding a long position in NYSE:KO , price just broke above my next bullish target so I decided to chart some new target and support levels.

I quickly labeled what I had previously looked at to enter my long position. Shown is the first bullish zone I looked at, a second zone that was broken to the upside, supported and broken structure, and most recently a range between 58.85 - 59.85, lasting from Dec 29th, 2023 - Feb 1st, 2024. Price had a strong break above this range and then shortly after fell back into the range zone, which became the new DNT area I have drawn. Today, there was strong bullish momentum that broke out of the zone around 60. Price targets to the upside are drawn up to 63.

This is what I would personally look at before entering trades, everything is subject to change on a daily basis and as I analyze different timeframes and ideas.

ENTERTAINMENT PURPOSES ONLY, NOT FINANCIAL ADVICE!

Coca-Cola: Analyzing Diverging Performance and Investment OpportCoca-Cola: Analyzing Diverging Performance and Investment Opportunities

In the world of investments, Coca-Cola's recent stock returns present a notable contrast to its business performance. Despite positive operating trends reported for fiscal 2023, Coke's stock lags behind, raising questions about potential opportunities for investors. Let's explore this divergence and assess whether investing in Coke presents a chance for market-beating returns.

While Coke's organic sales saw a 12% increase in 2023, driven mainly by higher prices, sales volume growth slowed to just 2%. This deceleration hints at weakening consumer demand for soda, a trend likely to persist into 2024. Despite projections for a modest 6-7% growth this year, Coke faces challenges in a sluggish industry, with rival PepsiCo forecasting similar struggles.

However, Coke's strategic initiatives are promising. Cost reductions, increased prices, and a focus on non-core beverages like sparkling waters and energy drinks fueled a 16% rise in non-GAAP earnings in 2023. Operating profit margins soared to 29%, surpassing PepsiCo's results. CFO John Murphy's optimism about further margin expansion adds to the positive outlook.

Moreover, Coke's cash returns are robust. Generating $10 billion in free cash flow in 2023, the company returned nearly the same amount to investors through stock buybacks and dividends. With a dividend payment track record spanning over 60 years, Coke offers steady dividend growth despite short-term cash flow dips.

Interestingly, Coke's stock is attractively priced compared to historical metrics and peers like PepsiCo. Despite short-term sales concerns, gaining exposure to Coke's stability and long-term potential makes it a compelling addition to investors' portfolios.

In conclusion, while short-term challenges may dampen Coke's stock performance in 2024, its solid fundamentals and attractive valuation make it a worthy consideration for investors seeking stable returns in the long run.

Is Coke going flat? Might be a good time to sell...NYSE:KO

Analysis is based on simplified Smart Money Trading Concepts.

Coke has been printing Weekly bearish order flow since August of 2022.

Recent price action( past ~134 days) on the Weekly time frame has had a Bullish pullback with what I anticipate a continuation or return to Bearish order flow between the 70.5% - 89% fibo zones. This would be supply overtaking demand to continue the weekly Bearish Structure also known as order flow.

Trade Idea Point of Invalidation: Any break AND close above $64.99

------------------------------------------------------------------------------------------------------

Reward to Risk ratios could vary between 3:1 up to greater than 5:1 depending on the instrument you are trading and the level that you enter in at.

The round trip time from entry to exit is between 6-11 months.

If you are Shorting the Underlying stock :

4 positions between the 70.5% pullback($61.03) and the 89% pullback($63.51) would be ideal.

Exits:

1st = $51.55

2nd = $47.92

**Split your positions between the 2 suggested exits**

------------------------------------------------------------------------------------------------------

If you are trading stock options:

NO less than a 6 month expiration!

Suggestion:

16 Aug 2024 -- Buy $57.50 Puts (out of the money)

or

17 Jan 2025 -- Buy $57.50 Puts (out of the money)

Exits:

Underlying stock price

1st = $51.55

2nd = $47.92

If you need an options calculator, I suggest using: www.optionsprofitcalculator.com

------------------------------------------------------------------------------------------------------

If you are interested in a FREE course on how I analyze the markets, let me know in the comments.

THERE IS NO CHARGE FOR AWESOMENESS

KO Rally Mode: Your Chance to Buy and Prosper!"## Coca-Cola Co (NYSE: KO) - Short Fundamentals & Recent News (as of February 21, 2024)

**Fundamentals:**

* **Market Cap:** $263.8 Billion

* **Current Price:** $61.24 (as of February 21, 2024, 4:00 PM EST)

* **Dividend Yield:** 2.94%

* **P/E Ratio:** 24.06

* **EPS:** $2.54

* **52-Week Range:** $51.55 - $64.99

**Recent News:**

* **Q4 2023 Earnings Beat:** Coca-Cola reported strong Q4 2023 earnings, beating analyst expectations on both revenue and EPS. The company is benefiting from strong pricing power and global demand for its products.

* **Stock Price Increase:** Following the positive earnings report, KO's stock price has increased by over 2% year-to-date.

* **New Product Launches:** Coca-Cola is continuously launching new products, such as its recently released Starlight zero-sugar soda.

* **Sustainability Efforts:** The company is investing in sustainability initiatives, such as reducing its water usage and plastic footprint.

**Disclaimer:**

I am not a financial advisor and this information should not be considered financial advice. Please do your own research before making any investment decisions.

Coca-Cola's Winning FormulaA Tale of Pricing Power and Consumer Demand

Coca-Cola (NYSE: NYSE:KO ) emerges as a clear victor, showcasing its prowess through stellar fourth-quarter results that surpassed Wall Street's expectations. The iconic beverage giant's ability to navigate through challenges and capitalize on opportunities underscores its resilience and strategic foresight.

At the heart of Coca-Cola's (NYSE: NYSE:KO ) success lies its adept management of pricing strategies. Despite raising prices consistently over several quarters, the company continues to witness robust demand, particularly for its flagship Coca-Cola (NYSE: NYSE:KO ) brand. This phenomenon speaks volumes about the unwavering loyalty of consumers who prioritize their favorite beverages, even in the face of economic fluctuations.

Contrastingly, Coca-Cola's rival PepsiCo faced a setback, experiencing a decline in sales for the first time in 14 quarters. The stark difference in performance between the two industry behemoths underscores Coca-Cola's superiority in pricing power and consumer appeal.

A key driver of Coca-Cola's (NYSE: NYSE:KO ) impressive performance is its ability to strike a delicate balance between price increases and consumer satisfaction. By leveraging higher product prices alongside strong demand, the company not only boosts its revenue but also maintains consumer trust and loyalty.

The fourth-quarter results paint a compelling picture of Coca-Cola's (NYSE: NYSE:KO ) resilience and adaptability. Despite concerns over potential saturation of price hikes, the company remains optimistic about its future growth trajectory. While forecasting a modest organic revenue growth for fiscal 2024, Coca-Cola's projections still outshine its competitors, notably PepsiCo.

Analysts, too, express confidence in Coca-Cola's prospects, with Wedbush analyst Gerald Pascarelli highlighting the company's better-than-expected organic revenue forecast. This sentiment is echoed by investors, as evidenced by the uptick in Coca-Cola's stock price following the earnings announcement.

Coca-Cola's (NYSE: NYSE:KO ) ability to capitalize on easing input costs further solidifies its position in the market. With an operating margin of 21%, up from 20.5% the previous year, the company demonstrates its efficiency and profitability.

Looking ahead, Coca-Cola (NYSE: NYSE:KO ) remains committed to delivering shareholder value, with annual adjusted profit expected to grow between 4% and 5%. While this projection aligns with market estimates, it underscores the company's consistency and reliability in delivering steady returns.

In conclusion, Coca-Cola's (NYSE: NYSE:KO ) fourth-quarter performance serves as a testament to its enduring strength and resilience in the face of challenges. Through effective pricing strategies, robust consumer demand, and strategic foresight, the company continues to outshine its competitors and chart a course towards sustained growth and success in the dynamic beverage industry.

KO going bull directionCoka-Cola is looking to make a bull move. It bounced three times off similar support lines and looking to retest previous highs. The set up looks very good.

KO @ $59.15Do you notice that the 50 EMA is about to Cross the 200 EMA?

If you look at the chart what do you see?

--

What is the Rocket booster strategy?

--

Because you can only see this if you understand the

rocket booster strategy.

--

Rocket Booster Strategy:

This is when the price is above the 50 EMA & The 200 EMA.

--

If this strategy is confusing you, then learn also about

candle stick patterns

--

NYSE:KO is looking like a good buy.

--

When you combine this strategy with candle stick patterns you will

see a whole New World.

--

Rocket boost this content to learn more.

--

Disclaimer: Please do not buy or sell anything i recommend to you these

are just ideas am sharing with you do your own research before you buy or sell anything

trading is risky and you will lose money.

Also, learn risk management strategies to improve your trading skills. Take this as a warning!

WARren BuffetSome of these days tha crackers gon 2 crack n his family gon2 b wanting some liquid coming out of coke, u know, since this dudes METArial purchases were what they were.

9.2%...

Supply

Demand?

Coca-Cola: Navigating Challenges and Anticipating Growth in 2024Coca-Cola: Navigating Challenges and Anticipating Growth in 2024

Investors in Coca-Cola faced a challenging year in 2023 as the beverage giant's shares declined, ranking it as the sixth-worst-performing stock in the Dow Jones Industrial Average despite a 22% rally in the S&P 500. However, the outlook for 2024 holds promise, supported by compelling factors that indicate a potential turnaround.

Factors Driving Optimism:

Emphasis on Volume:

Despite the challenging market conditions, Coca-Cola strategically emphasized volume growth alongside price adjustments. The company's balanced approach led to an 11% surge in organic revenue in the last quarter of 2023. Market share gains in on-the-go beverages and substantial growth in core segments contributed to this positive momentum.

Cash Returns:

Shareholders can anticipate enhanced returns as Coca-Cola raised its earnings outlook, projecting an 8% increase for the entire 2023 year. The potential for even higher gains exists if cost inflation continues to moderate. A forthcoming dividend increase, a consistent practice by Coca-Cola, adds to the appeal for investors seeking direct cash inflows.

Attractive Yield:

Despite recent underperformance, Coca-Cola offers an attractive yield of 3.1%, outpacing competitors like Procter & Gamble and PepsiCo. This, combined with potential capital appreciation, positions Coca-Cola as an appealing choice for income-seeking investors.

Price Check and Dogs of the Dow:

Coca-Cola emerges as a compelling candidate within the "Dogs of the Dow" strategy, presenting an opportunity for a rebound after its underperformance in the previous year. With a relatively affordable price, currently trading at 5.7 times annual sales, Coca-Cola offers potential advantages over its competitors, including higher income, swifter growth, and superior profit margins.

Conclusion:

As Coca-Cola investors enter 2024, the strategic emphasis on volume growth, anticipated cash returns, an attractive yield, and a favorable price point contribute to a more optimistic outlook. While challenges in the previous year impacted the stock's performance, the resilience of Coca-Cola's business model and its commitment to shareholder returns position it well for potential superior returns in the coming year and beyond.

Our preference

LONG positions Above 57.47 with targets at 63.26 & 64.00 in extension.

Triple Bottom ReversalReversal continuation to the upside

Triple Bottom Pattern Reversal

Look to ride the wave up

Buy or Long

risk reward 3 to 1