Top 5 Weekly Trade Ideas #1 - INTC Bull FlagINTC is set to gap up and open near the top end of its bull flag. If it can open above and stay above I'll look for longs for a move up to $26.40. Ideally we'd get a retest of the flag before moving higher, but that may never happen.

There's also a lot more upside potential if it takes out $26.40 as well. I'd consider this invalid if it can't remain above the top end of the bull flag.

ITLC34 trade ideas

Will America's Tech Sovereignty Rise or Fall on a Silicon Chip?In the high-stakes chess game of global technological supremacy, Intel emerges as America's potential knight—a critical piece poised to reshape the semiconductor landscape. The battleground is not just silicon and circuits, but national security, economic resilience, and the future of technological innovation. As geopolitical tensions simmer and supply chain vulnerabilities become increasingly apparent, Intel stands at the crossroads of a transformative strategy that could determine whether the United States maintains its technological edge or surrenders ground to international competitors.

The CHIPS and Science Act represents more than a financial investment; it is a bold declaration of technological independence. With billions of dollars earmarked to support domestic semiconductor production, the United States is making an unprecedented bet on Intel's ability to leapfrog current manufacturing limitations. The company's ambitious 18A process, slated for 2025, symbolizes more than a technological milestone—it represents a potential renaissance of American technological leadership, challenging the current dominance of Asian semiconductor manufacturers and positioning the United States as a critical player in the global tech ecosystem.

Behind this narrative lies a profound challenge: can Intel transform from a traditional chip manufacturer into a strategic national asset? The potential partnership discussions with tech giants like Apple and Nvidia, and the looming geopolitical risks of over-reliance on foreign chip production, underscore a moment of critical transformation. Intel is no longer just a technology company—it has become a potential linchpin in America's strategy to maintain technological sovereignty, with the power to redefine global semiconductor production and secure the nation's strategic technological infrastructure.

(Daytrading setup) Intel break out trendline beforemarketTrend: Up

setup: break out trendline in multi timeframe

open m1 chart we can entry like this

i will small entry when open then take tp whenever see the profit

Back to the TopWe had built a bottom, then exceeded the range and reverted to the top pf the range again now. I consider this as a buy signal.

Intel Corporation- NEXT BULL RUN IS COMINGIntel’s stock is currently consolidating near the $30 support level, historically a strong price floor. A potential breakout above its 50-day moving average could signal the beginning of a bullish trend, with sentiment improving as the tech sector recovers

INTC - Short Term Bear MoveThe curved dotted line being touched by price right now is being tested to create this new curved up channel

If the green circle breaks to the upside this idea is good and the bulls are firmly in charge

Bullish on this Weekly timeframe

Intel ValueWith Trump becoming president and Chinese US trade relations sure to to get heated, can't but help thinking that the abandoned chipmaker Intel still has a part to play in the future of chip production. Looking at $30 range retracement, options market currently is pricing $30 as fair value for a year from now, itm looks like best value on premium priced $30, although deep itm has slight discounts down to $28. Main thing is all premium even deep itm will not discount this stock as it is surely to rise over the next 12 months. Long itm leap calls $25c

INTC: Channel playHello,

INTC likes to play in channels, a possible channel play is outlined here.

If you can catch the right channel, it's about 10% every swing.

Happy trading

NASDAQ:INTC

INTC about to breakout 26 to 28 stretched.INTC is forming a symmetrical triangle, indicating a period of consolidation as the price action narrows into the triangle's apex. This pattern suggests indecision in the market, with the potential for a significant breakout in either direction. The resolution of this triangle is likely to set the tone for the next move, however I have taken a bullish position. The price action is nearing the triangle’s apex, suggesting a breakout is likely within the next 3–5 trading sessions.

Watch for a volume spike to confirm the direction of the breakout. For a bullish breakout, take partial profits at $25.50, then hold for the full target of $25.89 to 28.00.

Entry Strategy:

Enter a long position if the price breaks and closes above $24.54 with strong volume.

This would indicate a bullish continuation, with the price likely to target higher resistance levels.

Profit Target Calculation:

Triangle Height:

Measured from $24.54 (upper resistance) to $23.19 (lower support), giving a height of $1.35.

Breakout Target:

Bullish Target: Add $1.35 to the breakout point ($24.54) → $25.89.

Bearish Target: Subtract $1.35 from the breakdown point ($23.66) → $22.31.

Stop-Loss Placement:

For a bullish breakout, place a stop-loss below the lower trendline at $24.19.

For a bearish breakdown, place a stop-loss above the upper trendline at $24.54.

I have already taken a position for 11/22/24 25C @0.28

INTCif 25 hold, going to 30

an upward trend in the prices of an industry's stocks or the overall rise in broad market indices, characterized by high investor confidence

Intel - Still Got Another +15% From Here!Intel ( NASDAQ:INTC ) is perfectly respecting structure:

Click chart above to see the detailed analysis👆🏻

For more than two decades, Intel has not been trading in any clear trend. We saw a lot of swings towards the upside which were eventually always followed by corrections, making Intel a very easy to trade stock. After the current retest of support, a move higher will eventually follow.

Levels to watch: $20, $27

Keep your long term vision,

Philip (BasicTrading)

INTEL at $25 from $19 Low Hello Testosterone traders,

Election is finally over!

Intel stock has hit the $25 level coming from the low of $19.

Recently, Intel was kicked out of the SP 500 and replaced with Nvidia.

Intel liquidity sweep incomingDip beyond still on track.

Market makers giving a faulse bottom impression.

Could be wrong but could be the sweetest buy.

NO MONEY IN THE GAME.

NOT FINANCIAL ADVICE!!!

BullishIntel’s stock recently broke out of a bullish flag pattern, indicating a potential uptrend with a target around $25. However, performance struggles and past volatility may impact this rally.

N/b just a speculative analysis

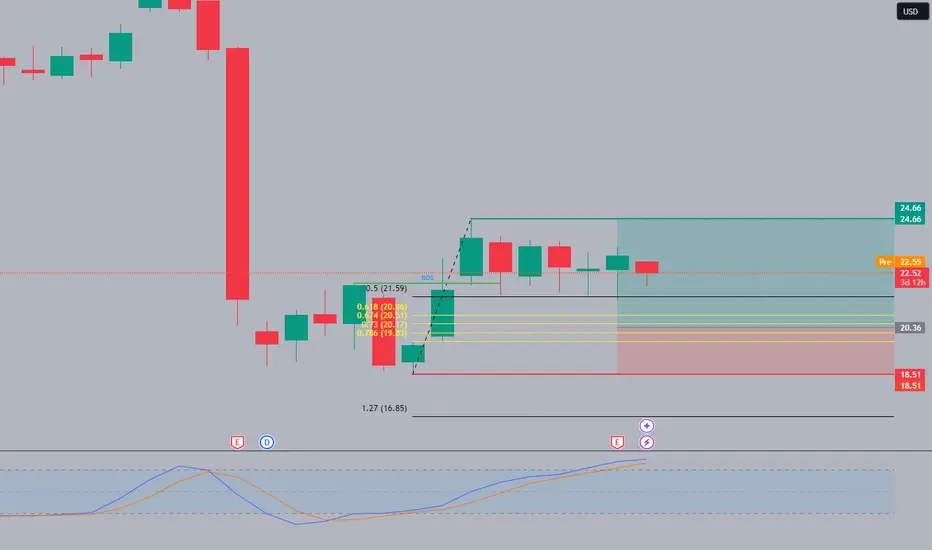

Long from oversold conditionsLimit buy orders waiting on yellow numbers marked. I also took a small position off of the 0.5. The market is very oversold, and one look at the fundamentals tells you why that is. However there is potential for a buy out. Should this happen you would expect a short term push upwards. The technicals look really good to me and meet my conditions. The conditions are, liquidity sweep, break of structure, FVG created, entry on return to the fib areas marked. Additionally, currently the stock is correcting very nicely. Weekly momentum is overbought suggesting we could expect a deeper move down in the coming weeks, whilst monthly momentum is oversold. Lets see what happens !

Intel in Trouble or Ready for Redemption?There is growing potential for QUALCOMM Incorporated to acquire Intel.

I now believe that this development has advanced enough to warrant a fresh look at the stock

Qualcomm recently approached Intel about a takeover. According to WSJ , Qualcomm has expressed interest in acquiring Intel, which, if realized, would mark one of the most significant deals in recent history

Initially, this seemed like a long shot, with limited details emerging from the report. However, QCOM has continued to pursue the idea. Also QCOM has been in contact with Chinese antitrust regulators over the past month about this potential deal and is waiting until after the US presidential election to decide on making a formal offer. Since the election is just less than a month away, I believe this acquisition is becoming more of a possibility that investors should factor into their assessment of INTC. If a deal goes through, it’s likely that the acquisition will come at a premium to the current stock price, creating an opportunity for significant short term gains for investors

There is always a chance that no deal will occur. In that case, potential investors should evaluate whether the stock is worth holding as a long-term investment. My outlook here is not optimistic, and I’ll delve into INTC's competitive position, as indicated by its latest inventory data, in the next section

Given these two potential scenarios, I am upgrading my rating from "Sell" to "Hold." In summary, the possibility of QCOM acquiring INTC introduces a major upside catalyst that I hadn’t accounted for in my previous analysis. This potential acquisition helps offset some of the concerns about INTC as a standalone company.

Unlike many financial metrics that can be interpreted in different ways, inventory levels are more straightforward. He also explained that inventory trends can provide early indicators of business cycles. For cyclical industries, rising inventories can signal overproduction as demand wanes, while shrinking inventories can indicate strong demand

As shown in INTC’s most recent balance sheet, its inventory levels have generally been on the rise. For instance, in December 2014, inventory was valued at $ 4.273 billion, while the most recent figures show an increase to $ 11.244 billion. In some cases, rising inventory can signal business growth with increasing demand and production capacity, which was true for Intel in the early part of the last decade.

When inventory growth exceeds the pace of business growth, it becomes a red flag. In this scenario, rising inventory suggests weakened competitiveness and declining market position—an issue that Intel currently faces, in my opinion. The following chart helps illustrate this point, showing a comparison of days of inventory outstanding (DIO) for Intel and NVIDIA over the last five years, from 2020 to 2024. DIO is a measure of how many days it takes a company to sell its inventory

Given Intel's inventory buildup and declining competitive edge, I find its current valuation multiples hard to justify. Specifically, the chart highlights a comparison of price-to-earnings (P/E) ratios between Intel, NVIDIA, and AMD. Focusing on non-GAAP earnings estimates for fiscal years FY1 through FY3, Intel is currently trading with the highest P/E ratio for FY1 at 87.7 almost twice the multiple of NVIDIA and AMD, which are at 46.29 and 46.25, respectively

That said, the outlook changes somewhat when considering the years further ahead. For instance, in FY2, NVIDIA’s expected P/E ratio rises to the highest at 32.77, compared to Intel's 20.02 and AMD's 29.02. However, I want to emphasize the substantial uncertainty in Intel's earnings forecasts. As shown in the next chart, the consensus estimates for Intel's earnings per share (EPS) in FY 2024 range from a low of $0.15 to a high of $0.31 (a more than twofold variation) and from a low of $0.65 to a high of $2.1 (an almost fourfold variation). Given such uncertainty, I believe investors should be cautious about relying too heavily on forward P/E ratios too far into the future.

Both Intel and NVIDIA have experienced significant fluctuations in DIO over the years. Notably, both companies saw a spike in 2023 due to the COVID pandemic, which disrupted global supply chains. As the disruption faded, both firms saw a recovery (ie, a reduction in DIO). the difference in recovery is striking. Intel's DIO peaked at over 150 days in 2023 and has since decreased to 125 days a modest reduction but still above its historical average of 114 days. In contrast, NVIDIA's DIO surged to over 200 days but has rapidly dropped to 76 days, which is not only below its four-year average of 97.9 days but also near its lowest level in four years.

I expect Intel to face increasing competitive pressure as rivals like NVIDIA and AMD roll out their next-generation chips, particularly NVIDIA’s Blackwell chips. I recommend potential investors keep a close eye on inventory data, as it can signal changes in competitive dynamics for the reasons discussed here.

In addition to inventory issues and valuation risks, Intel faces a few other specific challenges. A significant portion of Intel’s current product lineup is concentrated in certain segments, such as PCs, which I believe are nearing market saturation plus a large share of Intel’s revenue comes from China. Given the ongoing trade tensions between the US and China, this heavy reliance on China poses a considerable geopolitical risk. These factors may limit Intel’s ability to adapt to technological advancements and shifting geopolitical conditions

The potential for a QUALCOMM acquisition has emerged as a new major upside catalyst. While my outlook on Intel’s business remains pessimistic based on the latest inventory data, the acquisition possibility partially offsets these negatives, leading me to upgrade my rating from Sell to Hold or if you are risk taker like Me, load the dip

Intel (INTC): Patience is key while the market is rangingNothing significant has changed on NASDAQ:INTC since our last analysis. It appears that Intel may have found a bottom at the 88.2% Fibonacci level, but the stock has remained in a range since then. Unless the resistance level above is reclaimed, we wouldn’t be surprised to see continued ranging behavior.

Even Intel’s latest earnings report didn’t create much movement. Despite posting a considerable net loss due to impairment and restructuring charges, Intel projected fourth-quarter revenue above estimates. As one of the largest producers of PC chips, Intel has recently benefited from renewed demand for PCs, driven by on-device AI features and a fresh Windows update cycle. These factors allowed Intel to exceed Wall Street’s low expectations, but not enough to break the current range.

We’ll continue to monitor NASDAQ:INTC , but as it stands, trying to long it into the overhead resistance doesn’t make sense from our perspective. Patience is often the best strategy in such uncertain market conditions.

INTC 6h Bear ABCDThe bullish 5-0 harmonic broke down to stop loss. A bearish AB=CD harmonic is stronger, and will take price back sharply to recent lows before bullish reversal can continue.

Will Intel play catch-up?CAPITALCOM:INTC has vastly underperformed its peers for a long time, but there might be signs the stock will start to move in the right direction. There has been a lot going on with the company this last week, maybe the chart will show some improvement.

Price has broken resistance recently and closed above on Monday this week. It has since started building momentum, with indicators showing strength. MACD is rising, and On-balance-volume is confirming the uptrend. My first target would be for price to fill the gap created on Aug 2 when price dropped a whopping 25%. Once reached, we might see a slight pullback, however this should be temporary. Next speed bump might occur around $35.50 - $36.00 but that would be a 50% jump from the price today and will be more long term I believe, unless rumors of a takeover (or a massive investment) of the company becomes more solid. One more trigger one might want to wait for is the shorter EMA (i.e. 21) crossing the longer (i.e. 50).

Intel CorporationHello community.

Daily chart.

Accumulation zone plotted on the chart.

Simple moving average 200 periods oriented downwards.

Nice gap above the price.

Slight tendency to go back up, but it is timid.

End of the decline?

Make your opinion, before placing an order.

► Thank you for boosting, commenting, subscribing!

INTC buyingThere is a positive bullish wedge pattern and there is also a divergence between the price indicator and the MACD.

INTC likely to pumpAs intel searches for a catalyst to extend this initial pivot I believe earnings may provide this. With the stock recently trading as low as .6 price to book, I believe it remains undervalued. Remember there is a right price for any stock that makes money or is about to make money. My short term target is the 20 week moving average around 25$. I still believe the stock is valued at 28-32$ based on assets and cash flows combined.

INTC REVERSAL ?INTC in reversal area for now, or we succeed or fail!

If you are in the trade you must make space for the SL, because it could not do immediate reversal (enter range then reverse).

I will keep watching of how it's going, generally talking it's looking good.

If you haven't bought it yet, I would suggest to wait a bit more to get more confirmation regrading the reversal

SL BELOW 20.5

TARGET 29

* will update if there is any change in sentiment of the structure

* for any question drop them below, and HIT THE FOLLOW BUTTON