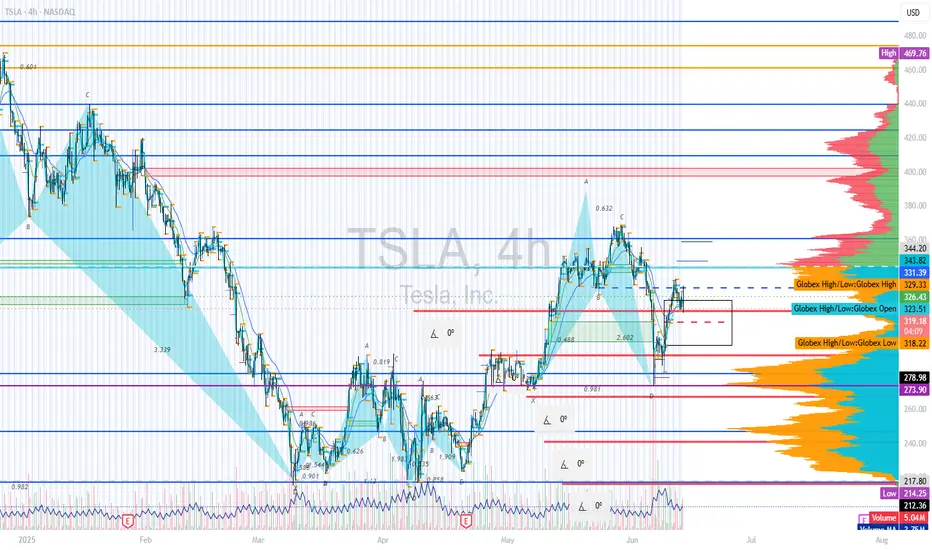

Key Support at $313.3 Holds Potential for TSLA UpsideTesla tested the order block with an average price of $325.00 in yesterday's trading session. The critical support for TSLA is at $313.3, and if this level holds, the price can target $367.71.

TSLA34 trade ideas

TESLA..(TSLA) 30M TIME FRAME..Tesla (TSLA) on a 30-minute timeframe using Ichimoku Cloud along with trendlines and breakout levels.

There are two target levels indicated:

---

🔵 Immediate Target Point (Breakout Target):

Price Level: ~$350

This seems to be the first breakout target if price breaks above the current resistance zone.

Based on the measured move from the ascending triangle or trendline breakout.

---

🔵 Extended Target Point (Full Target):

Price Level: ~$375–$380

This is the higher target possibly based on a full breakout move from the bottom of the triangle pattern to the top projection.

---

🟢 Current Price: ~$327.55 (at the time of the screenshot)

🧠 Suggested Trade Plan (if you’re trading this setup):

Entry: Above breakout level (possibly ~$335–$340)

First TP: $350

Second TP: $375–$380

Stop Loss: Below trendline or recent support (~$320 or slightly lower)

Let me know if you want a risk-reward analysis or SL/TP calculator based on your entry.

TSLA PRICE ACTION JUNE 25 2025This is the price action for Tesla. I have discussed all the levels. I have given a trade today & have discussed it thoroughly.

If you have any doubts, then feel free to Dm me or leave a comment below

NOTE:DO NOT BUY CALLS

TSLA shortPart of a larger analysis, at the moment Tsla rejected 332 B pivot and imo retesting possible b.o. area. missed gap up open, retest of highs sent 305p strike. looking to close at 310-305 tgt zone. n.f.a. g.l.h.f

AoO Series No.3Wed - Monitoring the FVA reaction. The last swing high on the D is the last line of defence of the bearish FVG. If we run that high, there is no resistance left and we enter an area of opportunity.

Monitoring on the 4H and 1H early signs of respect of the FVA.

TSLA : Up trend is becoming weakNASDAQ:TSLA is in Up trend. But the uptrend is becoming weak. Bullish momentum may become weak here. It has pull backed from the down trend line. So It may enter in sideways trend. Down trend line may act as resistance and up trend line may act as support.

Will the Robotaxi euphoria continue to push TSLA higher?NASDAQ:TSLA pushing higher the last few days thanks to the start robotaxis. Will this rally continue? the answer is yes until the LIS gets broken.

LIS is at 311, any break below will give a retrace. If you are long, get out and get back in when the next LIS gets broken on the upside. This is efficient investing. Don't waste time doing HODL.

LIS is evolving over time, I will keep you updated on it.

This is really simple trading based on important levels. Keep following my post, so you can see it by yourself.

TSLA Intraday Reversal Setup | Smart Money Buy Zone HitTesla just tapped into a deep discount + strong demand confluence with SMC confirmation.

📍 Buy Zone: $311–$324

📍 Target Zone: $372.16 – $374.16 (liquidity above weak high)

📍 Midpoint (EQ/TP1): $336.23 – $345

Trade Thesis:

BOS confirmed after internal CHoCH

Price swept lows into premium discount zone

Volume spike + divergence near key Fibonacci (0.236–0.382)

Bullish intent visible if PA reclaims 336.23 (EQ)

🎯 Targeting ~15%+ intraday swing from reaccumulation. Ideal for scalpers with asymmetric R/R profiles.

🧠 Wait for confirmation – this is where Smart Money steps in.

⚠️ Not financial advice. Educational content only.

#TSLA #Tesla #SmartMoneyConcepts #SMC #LiquiditySweep #Equilibrium #Fibonacci #DayTrading #Scalping #VolumeProfile #WaverVanir #TradingView #IntradayEdge

TSLA: GEX Points to Bounce Setup. Is This the Dip to Load Calls?📊 GEX-Based Options Suggestion

Gamma Exposure (GEX) data paints a bullish opportunity if TSLA holds the critical support zones:

* ✅ Key GEX Levels:

* $338: Near current price, minor GEX flip zone.

* $345–$350: Strong upward magnets (3rd Call Wall + GEX build-up).

* $359: Gamma Wall + Highest Net Positive GEX — market makers may pin price near this into end of week if bulls hold.

* 🛡️ Below Support:

* $330: Light PUT defense.

* $320: Major Put Support (-67.5%) — strong bounce zone if downside accelerates.

🔔 Option Trade Idea Based on GEX:

With TSLA near the $338 zone and GEX showing stacked resistance above + positive net exposure, a high-risk/reward call entry is forming.

* Play: Buy 345C or 350C expiring 06/28 or 07/05

* Trigger: Only if price holds $335+ and shows strength with volume bounce

* Target: $345 → $350 → potential pin near $359 (Gamma Wall)

* Stop: Close under $332 invalidates the bounce setup

🧠 Trading Setup – 1H Chart (Second Image)

From the second image, we analyze price action and structure to validate the GEX idea:

📉 Market Structure:

* Price is pulling back into a prior demand zone from $335–$338.

* Trendline support + Fair Value Gap zone + SMC CHoCH aligning at this base.

* Multiple bullish CHoCHs suggest potential reaccumulation if support holds.

🎯 Trading Plan Based on Price Action:

Bullish Case (Base Holds):

* Entry: $335–$338 zone (bounce off trendline and demand zone)

* Target: $345 (GEX level) → $348 → $350

* Stop-Loss: $331

High confluence with GEX option play. Use volume spike for confirmation.

Bearish Breakdown Scenario:

* Trigger: Loss of $331 + trendline break

* Target: $325 → $320 (strong PUT wall support)

* Put Options: 325P or 320P if breakdown triggers with momentum

⚠️ Summary:

TSLA is entering a decision zone — GEX shows bullish opportunity if $335 support holds, with upside targets toward $350–$359. But if price breaks under $330, expect a flush toward PUT support.

Patience is key — let price confirm the bounce or the break.

This setup is for educational purposes only. Trade with discipline and use stops. Always do your own research.

Technical Analysis – TSLAChart Summary:

Current Price: ~$349.21

Local Top: ~$357.53 (100% Fib extension)

Bearish Rejection: Notable wick + retrace from 0.886–1.0 zone

Probable Pullback Zone: 343.00–338.50 (Fibonacci 0.618–0.5 retracement)

Major Support Levels:

$334.50 – Prior key horizontal + Fib confluence

$311.62 – Historical demand zone

Projection:

Intraday double-leg correction toward $338–$343

Possible bounce and continuation toward the golden target zone:

$366.47 (1.236 Fib)

$374.16–$380.95 (1.618 zone)

🌍 Macro Alignment

Bullish backdrop:

Tech sector leading broader rally

Tesla’s robotaxi and AI narrative lifting sentiment

Oil down → margin relief for EV production

Catalysts this week: Powell testimony, PCE inflation

📈 Trading Plan

Type Direction Entry Target(s) Stop Loss Confidence

Intraday Bearish $352–$353 rejection zone $343 → $338.5 Above $357.5 🔶 Medium

Swing (Buy the dip) Bullish $338–$334 zone $366.47 → $374.16 Below $330 🟢 Strong

📌 Suggested Strategy

Scalp short if rejection at $353.2–$357.5 confirms with bearish candle on volume.

Add long exposure if price consolidates or reverses from the $338–$334.5 support area.

Monitor Powell’s remarks – Any dovish tilt could accelerate tech upside.

TSLA sentiment remains strong, but intraday shakeouts are expected.

✍️ Summary Signal

“TSLA remains bullish on a swing basis, but intraday looks set for a Fibonacci pullback to $338–$334. Buy dips if structure holds. Macro backdrop (robotaxi + Fed pause) supports continuation to $366–$374.”

Tesla, Inc. (TSLA) Boosted by Energy StorageTesla, Inc. (TSLA) is a global leader in electric vehicles, clean energy solutions, and battery technology. The company designs and manufactures EVs, solar products, and energy storage systems that help drive the transition to sustainable energy. Tesla’s growth is fueled by rising EV adoption, battery innovations, and expansion into new markets with its cutting-edge technologies.

On the chart, a confirmation bar with increasing volume signals strong buying interest. The price has moved into the momentum zone by breaking above the .236 Fibonacci level. A trailing stop can be set just below this level using the Fibonacci snap tool to protect gains as momentum continues.

Launch of Robotaxi Service Boosts Tesla Share Price by Over 8%Launch of Robotaxi Service Boosts Tesla (TSLA) Share Price by Over 8%

As previously announced by Elon Musk, Tesla has launched its robotaxi service in Austin, Texas. The cost of a ride is $4.20.

The service is not yet fully operational. It is more of an extended testing phase, as access is currently by invitation only, and a Tesla employee may be present in the back seat.

Nevertheless, the market responded positively — Tesla (TSLA) shares rose by more than 8% (comparing the closing prices of daily candlesticks).

Technical Analysis of TSLA Share Price Chart

In our 11 June publication, we:

→ identified an ascending channel;

→ highlighted the May support level (marked with an arrow), suggesting it could act as resistance following a bearish breakout.

Since then:

→ the channel has remained relevant;

→ the aforementioned level acted as resistance but was broken by the bulls yesterday.

As a result, the TSLA share price has reached the median of the current ascending channel, where it may find equilibrium and form a consolidation zone once the initial positive reaction to the robotaxi launch subsides.

It is also worth noting the stock’s resilience following Elon Musk’s controversy with President Trump — the price has already risen more than 28% from the June low, indicating the potential for a scenario in which resistance at $365 is tested.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

TSLA long scenario

TSLA long scenario

1.. important Registance ( $370 )

if break midpoint ( $370 ) next TP $457

2. i expect some correction near $ 330

it will be one more buy chance

-----------------------------------------

based on price action

harmonic theory

Bearish Elliot Triangle Wave $250 targetObserving Tesla Chart, I noticed a bearish 4hr Elliot Wave A-E. The flow is also bearish and lines up with the bear sentiment. Looking for a bearish Apex Breakout..

TSLA Breaking Out! Is This Just the Beginning or a Trap? Jun 24 🔥Price Action Overview:

TSLA had a powerful move, jumping +8.23% to $348.68. It cleared key resistance and now consolidates near $349–350. Volume surged, but we’re seeing a bull flag structure with some internal weakness forming.

🧠 Smart Money Market Structure (15-min Chart)

* CHoCH occurred before the breakout, showing smart money accumulation.

* Break of Structure (BOS) confirms bullish intent.

* Price is now ranging in a supply zone, rejecting upper levels with signs of compression.

* Consolidation wedge suggests a possible breakout or fakeout setup.

🔮 Gamma Exposure (GEX) Breakdown (1h Chart)

* Current Price: $348.68

* Gamma Resistance (Call Wall):

* $357.53 → 1st resistance

* $365.00 → heavy resistance

* $367.5 → Extreme Call Wall / GEXY8

* Gamma Support:

* $340 → strong support

* $320 → HVL (High Volume Level) and PUT defense

* $315 / 312.5 → 2nd PUT Wall (if breakdown)

Interpretation:

Price is trapped between GEX compression levels. A breakout above $350 could trigger a gamma squeeze toward $357–360+. A breakdown below $340 targets $320 fast.

📈 Indicators Snapshot

* Volume: High on the breakout, but tapering off during consolidation.

* RSI/MACD (not shown): Likely cooling off — favoring a pullback or re-accumulation.

* CHoCH & OB Zones: Indicate smart money watching $340-$345 for support retest.

⚖️ Scalping vs Swing Outlook

✅ Bullish Case

* Break above $350 → Watch $357.50 and $365 targets.

* Above $367 = gamma squeeze zone unlocked.

Entry: Break and hold $350

Target: $357.50, then $365

Stop: Below $345

⚠️ Bearish Case

* Break below $340 → Flush to $320 and possibly $315

* GEX puts will dominate under $320

Entry: Break and hold below $340

Target: $320, $315

Stop: Above $345

🧭 Trade Strategy Summary

* ⚔️ Inflection Zone: $340–$350 = Decision zone

* 🚀 Watch for gamma squeeze if $350+ holds

* 🛑 Breakdown below $340 flips bias bearish

* 🔄 Volume confirmation is key

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk carefully.

A Bullish Long-Term Outlook Tesla continues to present a compelling case for long-term investors, underpinned by its innovation-led growth trajectory and emerging dominance in autonomous mobility. Technically, recent market structure reveals an imbalance within a quarterly bullish breaker, suggesting further price expansion. If macroeconomic conditions remain favorable, the next algorithmic target zones fall between $594 and $690, signaling potential upside.

On the fundamental front, Tesla’s recent moves—particularly its rollout of the robotaxi network—have ignited fresh investor optimism. Analysts now estimate that autonomous driving could account for a substantial portion of Tesla’s future valuation, with some long-range forecasts placing the stock above $2,000 within the next several years.

While short-term pressures such as softening EV demand and regulatory barriers persist, Tesla’s consistent execution on AI-driven mobility may unlock new valuation territory.

Tesla: Robotaxi Hype and Breakout WatchNASDAQ:TSLA surged nearly +10% today, driven by growing anticipation around the upcoming robotaxi unveiling on August 8.

Investors are positioning early, speculating this innovation could open new revenue streams for Tesla and redefine mobility.

📊 Technical Setup:

• Price broke out of local resistance near $330

• Approaching major resistance at $370–371 (Bollinger Band + prior support)

• If $370 is broken and held, the stock could enter a new trading range: $370–$440

• RSI and Stochastic are heating up, but no signs of reversal yet

⚙️ Robotaxi Catalyst:

• Elon Musk confirmed the Robotaxi event set for August 8

• Analysts speculate this could boost valuation through AI and self-driving revenue potential

• Option volume and retail interest are rising fast

📌 Levels to watch:

• Breakout level: $370

• Target: $440

• Support zone: $330

• Invalidation: Close below $310

👀 Watch for pre-event momentum. A break above $370 could trigger a squeeze.

Tesla Rolls Out Much-Awaited Robotaxis. Buy or Sell the Stock?They’re here. After years of tweets, teasers, and timelines that aged like unrefrigerated dairy, Tesla NASDAQ:TSLA officially launched its long-awaited robotaxi service in Austin, Texas.

The self-driving revolution, we were told, would arrive like a lightning bolt. Instead, it quietly rolled up to the curb with a safety monitor riding shotgun.

On Sunday, ( as promised ) a small, highly curated fleet of Teslas — fully driverless, but not entirely unsupervised — began picking up paying passengers in an isolated section of Austin. CEO Elon Musk, as usual, led the cheer squad, declaring victory on X.

“Super congratulations to the Tesla AI software and chip design teams on a successful robotaxi launch!! Both the AI chip and software teams were built from scratch within Tesla.”

Investors, naturally, perked up. Tesla shares edged higher by more than 5% Monday morning as Wall Street tried to figure out whether this was the long-awaited catalyst for another rally… or just another “sell-the-news” moment that fizzles as quickly as the hype fades.

🔔 The Soft Launch Heard Around The Internet

Let’s not get carried away. This wasn’t a citywide revolution. Tesla’s launch was extremely limited — more of a PR exercise than a true market rollout. Only a handful of Teslas were involved, operating in a tightly controlled, geofenced area.

The riders? Carefully selected influencers, many of whom were more excited to film TikToks than analyze technical driving capability. In other words, this wasn’t exactly New York City rush-hour stress testing.

The rides cost a flat fee of $4.20, because, of course they did. And while the cars drove themselves, safety monitors sat in the front passenger seats — a very human reminder that the project is still very much in beta mode.

The bigger question for investors: Does this prove Tesla’s technology is ready for prime time? Or is it simply an appetizer served years before the main course?

📈 The Market Reaction: Buy the Rumor, Sell the Launch?

Here’s where things get tricky for traders.

The stock market, as always, is forward-looking. Tesla stock didn’t just wake up bullish on Monday because of a few rides in Austin — it’s been rallying for months because of the promise of robotaxis.

Since Tesla’s big October 10 robotaxi event — where Musk laid out plans to launch a self-driving cab service in 2025 — shares have climbed roughly 35%. Much of that gain is already baked into expectations for Tesla finally delivering on what Musk has been promising since at least 2016.

Now that the product is technically “live,” even in tiny demo form, some traders are wondering: is this the start of an even bigger rally?

The answer probably depends on how fast Tesla can scale. And that’s where reality gets stickier.

🤔 The Scaling Problem: A Long Road Ahead

As exciting as Sunday’s launch may have been for influencers and Tesla superfans, it’s not exactly proof of scalability. Deploying 10 carefully monitored cars in a tiny slice of Austin is one thing; blanketing entire metro areas, or states, or countries is another beast entirely.

Tesla’s AI software may be improving, and its in-house chip design gives it some vertical integration advantages. But scaling fully autonomous fleets will require navigating a minefield of regulatory, safety, and logistical challenges — not to mention stiff competition.

Alphabet’s Waymo is already operating robotaxi services in Phoenix, San Francisco, and Los Angeles, with years of public road testing under its belt. Cruise (General Motors) ran its own driverless service before recently pausing operations after high-profile safety incidents. The technology arms race is fierce — and far from settled.

Industry experts continue to caution that mass-market robotaxis may take years — if not decades — to fully materialize. And while Tesla loves to move fast and break things, cities, regulators, and insurance companies tend to prefer a bit more caution when thousands of driverless vehicles are involved.

📝 What’s Actually Priced Into Tesla Stock?

Here’s where this gets existential for Tesla bulls.

A huge chunk of Tesla’s market valuation — some would argue most of it — now rests on the idea that it isn’t just a car company. It’s an AI company. A software company. A robotics company. A future robotaxi empire. If those narratives start to weaken, so does the multiple.

Tesla remains dominant in EV production and it still benefits from profit margins (about half of the profits coming from selling regulatory credits to other carmakers). But even Musk himself has made clear that Tesla’s long-term valuation depends heavily on successfully delivering robotaxis and humanoid robots.

If Sunday’s soft launch is the start of something truly scalable, then maybe the valuation holds up. If it stalls — either due to regulatory hurdles, technological ceilings, or public skepticism — the market may need to reevaluate just how much of Tesla’s price reflects reality versus dreams.

👀 Bottom Line: Revolutionary or Just Another Test Ride?

So, should you buy or sell Tesla after its long-awaited robotaxi debut?

That depends on how you frame this moment. The bulls see a trillion-dollar industry being born, with Tesla perfectly positioned. The bears see a carefully staged PR event masking how far away true autonomy still is.

For now, Tesla gets credit for being bold — even if it’s bold enough to roll out a very small, very managed test.

But markets eventually ask: “What’s next?” And unless Tesla can quickly scale from 10 cars in Austin to fully functioning fleets in major cities, a victory lap here could feel a little premature.

As always with Tesla: the story is thrilling, the stock is volatile, and the future is still very much under construction.

And with its earnings just around the corner — you’re following the earnings calendar , right? — things might just be getting exciting.

Off to you : Which side are on? The bullish traders looking to add to their long positions or the bearish sellers who’ve been calling “overvalued” for years? Share your thoughts in the comments!

TSLA ready to head higherTSLA at the 200 SMA coming out of a sell off.... After the RoboTaxi debut, may get positive momentum to go higher ...

Bullish Setup Suggests Rally Towards $350 Zone

- T1 = $340.00

- T2 = $350.00

Stop Levels:

- S1 = $315.00

- S2 = $310.00

**Wisdom of Professional Traders:**

This analysis synthesizes insights from thousands of professional traders and market experts, leveraging collective intelligence to identify high-probability trade setups. The wisdom of crowds principle suggests that aggregated market perspectives from experienced professionals often outperform individual forecasts, reducing cognitive biases and highlighting consensus opportunities in Tesla.

**Key Insights:**

Tesla continues to receive robust interest as macroeconomic conditions favor growth-oriented companies, particularly in the electric vehicle sector. The recent earnings showed signs of stabilization in gross margins, thanks to operational efficiency and cost reductions. Similarly, the company's megapack energy storage segment is gaining traction, which provides an ancillary growth avenue outside its core vehicle business. Technical indicators suggest strong momentum, with Tesla's Relative Strength Index (RSI) approaching bullish levels while trading volume supports the ongoing price recovery.

Furthermore, global EV adoption continues to rise, with increased government support for sustainable energy initiatives securing Tesla's place as a leading player. Supply chain constrictions, previously a concern, are relaxing, providing tailwinds for smoother production cycles.

**Recent Performance:**

Tesla's stock has gained over 8% in the past two weeks, recovering from its support levels around $305. The recent breakout above $320 signals renewed buying interest, accompanied by increased institutional participation. Short-term volatility has brought manageable dips, but overall momentum indicates bullish consolidation towards higher highs in its near-term trading range.

**Expert Analysis:**

Market strategists highlight Tesla’s ability to outperform its competitors due to vertical integration, advanced battery technologies, and scaling of operational efficiencies. Technical analysts note Tesla hovering near an ascending triangle formation with breakout potential above $330. Analysts also observe robust support around $310, which acts as a safety net for downside risks. Moving averages, especially the 50-day and 200-day lines, are converging as they indicate sustained bullish sentiment.

**News Impact:**

Recent news regarding expanded production facilities in Europe and positive developments in autonomous driving technology have fueled optimism among investors. Further bolstering sentiment is CEO Elon Musk’s strategic focus on prioritizing volumes over short-term profit metrics—a move widely seen as prudent given the current competitive landscape in EV markets.

**Trading Recommendation:**

Tesla is primed for upside momentum and presents an attractive long opportunity for traders targeting $340 and $350 next price zones. Its technical and fundamental outlook support the bullish case as macroeconomic tailwinds and company-specific factors align for higher valuations. Focus on maintaining risk discipline by exiting trades if stops at $315 or $310 are breached. For patient investors, Tesla is likely to remain a candidate for continued capital appreciation.

TSLA: Anyone knows this powerful pattern?TSLA:

Anyone knows this powerful pattern?

The crowd gets lost in colorful indicators, forgetting that the market speaks clearly through just price and volume.

.

US STOCKS- WALL STREET DREAM- LET'S THE MARKET SPEAK!

Quick View: $TSLA

- Bullish Box on the daily chart supported by the ema50d and strong ema 21d and 9d. No volume on this box.

- Almost the same pattern on the hourly

$TSLA Short Trade – Breakdown in the Making “When pressure buil⚡🔻 💣📉

Tesla ( NASDAQ:TSLA ) is coiling tighter than ever inside this symmetrical triangle — but this isn’t strength… it’s stress.

With lower highs stacking and bulls running out of breath, the breakdown could hit like a spark in a lithium mine. ⚠️🔋

Is this just technicals? Or is the market doubting the Elon engine again? 🚗🧠

📌 Trade Setup:

Entry: $322.17

Target: $308.07

Stop-loss: $327.52

From breakout darling to breakdown candidate — Tesla’s chart is whispering a warning.

Will it hold… or will gravity take over? 🧲

#TSLA #ShortSetup #BearishChart #TeslaTrade #TradingViewSetup #ChartBreakdown #TechnicalAnalysis #OptionsPlay #ProfittoPath