Short GLD until $162Short GLD till we hit 162, then long!

Seeing more down side in gold for the next week or so.

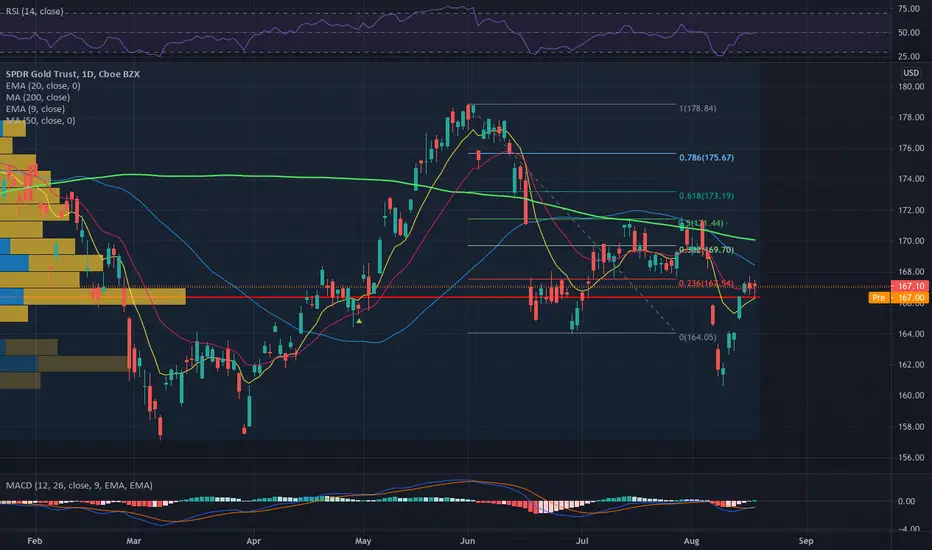

GLD trade ideas

SLV - ready to move up?I think so. This is the gold to silver ratio. When silver outperforms gold this ration goes down. SLV has taken it on the chin this year and over the next few months I expect the pattern to resolve itself to the downside similar to the 2010-2012 period (look left). Indicators look ripe for a roll. Typically silver makes a new all time high within a year or less of gold reaching a new high and that did not happened with silver this time around with gold's new all time high last August. I haven't written a silver note in a long time. I think we are looking at a back up the truck opportunity. My observation.

GLD BullishCurrent price for GLD is near the POC Line (YTD) and the MACD is crossing over. The most recent daily candle tested the .23 fibonacci level and closed just under it.

Given the uncertainty with covid, the markets being at all time highs and inflation I cannot think of a reason why gold should not rally from these levels.

Targeting $178.84 in the short term and a possible all time high later this year or early '22.

BUY OPPORTUNITY GLD is a fund that reflects the price of gold . It has a direct correlation with the underlying. When the price of gold increases, that of the fund increases, while when the price of gold decreases, the price of the fund decreases.

It is a highly protective asset that helps diversify portfolio risk. It has a long-term bullish statistical bias and is particularly tempting to place in a portfolio. By statistically analyzing the history of gold prices (1970 - today) we can consider ourselves in a position of extreme advantage at this time. Analyzing the past crises from 1974 (from the point of maximum to their minimum) to date, 6 major crashes are found for the gold market. The smallest reversal was 35% at the end of 1987, while the largest decrease in value was recorded starting from 1980, losing more than 70%, with an average drawndown of -47.5%. The ratio of drawdown to recovery period is around 1.5. Means that on average gold takes around 1.5 times the time it takes to recover value compared to the time it takes to lose it. Analyzing the declines that did not affect the trend reversal, we can see that in over 50 years of history, the declines that did not lead to trend reversals have had decreases in value that have never exceeded 30%. The price of gold has lost only about - 17% from its maximums, so for the moment we are well above the average level of historical reversal (-30%). Although the quantitative analysis in the past has an indicator of a probable trend reversal of the instrument in the future, the decrease in price from the maximums does not confirm the same direction (the price did not exceed -30% from the maximum reached in 2020), considering the situation extra ordinary (and still uncertain) for the world economy and the probability of new lockdowns, finding ourselves on a discount level of approximately -17% of the asset, I will proceed accordingly. Insertion of the asset class in the core department, finding the discount level interesting. Given past trends and the present period, gold will be positively affected in the event of continued uncertainty in the future economy. If the price should fall below the -30% level from the 2020 highs, we will proceed to close the position on the asset. Going up now considering the discount on prices brings us to an advantageous situation as it allows us to decrease the risk of our operation.

If we assume that we are close to a minimum level and that the long-term is characterized by a strong upward statistical bias, combined with the fact that the global economic situation is still far from an official recovery and that the Fed will have to wait a little longer before raising rates, positioning on $GLD is an excellent medium / long term opportunity for part of the core structure of my portfolio.

Let's analyze the data:

- Standard Deviation 10Y = 0.99%

- Standard Deviation 5Y = 0.85%

- Standard Deviation 3Y = 0.90%

The riskiness of the product decreased by about 10% from 2010 to today.

- 5Y yield = + 5.54%

- 3Y yield = + 12%

- YTD yield = - 1%

3Y Expected Return: + 30%

Max loss (with hedging): 5.60%

Max portfolio loss (in the event that the outcome of this core transaction does not go according to estimates):

% of equity to be dedicated to this operation: 10% of the total portfolio + 5% for any hedging = 15% of the total portfolio

Risk - Return = 1: 5.35

Over time, three different situations can arise:

A) Closing the long trade at a loss and closing the hedging in profit, then:

- Potential loss% on the portfolio: - 0.57%

B) Closing of the hedging at a loss and profit of the long operation, then:

- Potential gain% on the portfolio: + 2.37%

C) There is no need for the hedging strategy and the instrument meets expectations, then:

- Potential gain% on the portfolio: + 3%

Remember that this is my market vision and should not be interpreted in any way as an investment advice!

Scaredy Cat GOLD - No Need to PanicSmall Caps with revenue growth and profits now are the bees knees. Who needs gold when the #cannabisreform legislation is getting written....

#cannabisboom2021 & beyond. JOBS & Justice!

$GNLN

#thegem

#MSOgang

Gold needs to hold support or a gap to fill$GLD gold needs to hold 164.18 support, if we break there's a gap to fill down to 158.24. Trading at the bottom of that wedge so there is strong support here. Remember inflation data, Consumer Pricing Index on Wednesday 8/11/21

Trade Idea: GLD March 18th 140/September 17th 165 LCD*... long call diagonal.

Comments: Here, I'm preliminarily pricing out a bullish assumption GLD setup, buying the back month 90 delta and selling the front month at-the-money call. I'd prefer to deploy this at that obvious support level at 160, which has resulted in some buying interest previously. If that occurs, I'd have to tweak the strikes slightly, selling an at-the-money 160, for example, and then buying whatever the 90 delta strike in the back month.

The Metrics:

Buying Power Effect: 22.79 ($2279)

Max Profit: The Width of the Diagonal Spread (25.00) Minus the Debit Paid (22.79) = 2.21 ($221)

ROC %-Age as a Function of Buying Power Effect: 2.21/22.79 = 9.7%

Break Even: The Long Call Strike (140) + the Debit Paid (22.79) = 162.79 versus a spot price of 164.64

Trade Management:

Take profit on the setup's approach of max (which would be 25.00).

Otherwise, roll out the short call to a strike at or above your break even of 164.64 to reduce setup cost basis.

Variations:

Preliminarily, I'm pricing out the setup with a fairly long-dated back month. To get in with less buying power effect, look to buy a shorter duration back month 90 delta, with the trade-off being that you'll have less time to reduce cost basis via the short call in the event that gold prices keep on going down. To look for more profit potential, sell a less monied call (e.g., the 30 delta) to give the trade more room to the upside.

Gold is Looking Much StrongerAMEX:GLD

This looks like it could be setting up for a longer term trend. There is a lot of space ahead of us while the longer term bulls won out on the last important retest. Bearing in mind this is on a 2 day chart.

GLD daily C&H$GLD giant C&H with eyes on inflation and personal spending data tomorrow. Above 173.73 is a big deal but to hold above is even bigger.

Inflation surprise + no Fed policy change = GoldGold has jumped above its exponential moving averages on both the daily and weekly charts after inflation numbers came in red-hot yesterday and today. Despite the hot inflation numbers, Federal Reserve chairman Jay Powell signaled this morning that the Fed will stay the course on easy monetary policy and still expects inflation to be temporary. That means that more inflation surprises could lay ahead, and traders may look to inflation hedges like TIPS, crypto, and gold. All three popped today, with the iShares TIPS bond ETF making a new all-time high.

Gold's got potentially a lot of upside in the horizontal channel here. Note that August tends to be seasonally the strongest month for gold, perhaps because traders rotate to the relative safety of gold as a hedge against the weakest months of the year for stocks (August and September). I also like gold miners right now, with the P/E on GDX at about 17 and the P/FCF at just over 8 making this a relatively inexpensive sector.

I will say as a caveat that this is not a high-conviction trade for me, so I'm not going in very heavy. I've been a little underwhelmed by the intraday price action lately, with lots of strong opens and weak closes. But given the news headlines and the seasonality here, I've decided it's worth taking a position.

GLD: Correction incoming! ↘️↘️↘️The GLD price has reached its ideal mark at around $171.43. Now, we expect the price to drop all the way down to levels around $162.15. Ending the correction there, the GLD can then look forward to gain upward momentum.

Enjoy your weekend!

GLD vs SPY Gold vs SPYTo me, looks like a swing failure low. As long as this low holds it could be bullish for gold. With this talk of inflation, who knows.

Closing (IRA): GLD September 17th 150/July 23rd 166... long call diagonal for a 15.43/contract credit.

Comments: Money, taking, running on this (which was pretty much my original intention if I got the move). My cost basis was 13.88, (See Post Below), so my profit is the difference between what I closed it for (15.43) minus my cost basis (13.88) or 1.55 ($155)/contract. 1.55/13.88 = 11.2% ROC. Naturally, there could be continuation, but the most I can make out of this diagonal is the width of the spread (16.00), and I'm not sure I want to hang out another 17 days (the duration of the front month), since it's been flopping back and forth across that 166 mark for a bit (which is where I'd need price to finish above to realize max).

GLD LongGold is still accumulating and might go a little deeper before the next up rise move. But it's ok for a long-term holding.

90% BUY / 100% HOLD

Estimated PO $200 area

GLD bottoming out herehello everyone please leave a like and follow if you enjoy my ideas :) if you have been trading for a while you know every dip provided in gold and silver is a free money dip buy for the patient traders. we will see some upside soon in my opinion! please leave a like and follow if you enjoy my ideas <3

Rolling (IRA): GLD July 16th 166 to July 23rd 166... for a .36/contract credit.

Comments: Here, just rolling the short option leg of my GLD diagonal (See Post Below) while price is right at the short call strike to bring in a little bit more credit, reduce cost basis further, and improve my break even a smidge. I originally filled this for 14.24 (See Post Below), so my cost basis is now 14.24 - .36 or 13.88 and my break even 150 (the long call strike) + 13.88 or 163.88. Max profit potential now the width of the spread (16) minus my cost basis of 13.88 or 2.12.

Precious Metals Shift with the Winds of InflationGold and Silver drop as the Dollar rises. This has happened as investors have begun to shift expectations in the wake of the latest FOMC meeting. It's also happening at a time when producers, in all sectors, seem to be ramping up supply to meet consumer demand. Are gold and silver going through seasonal demand or is this yet another point of evidence that inflation may be about to diminish.

Inverse Head & Shoulders on Gold#Gold (GLD) busy forming an inverse head and shoulders pattern. GLD also finds itself in EXTREME OVERSOLD according to its 14-day RSI. A recovery in GLD could target $178. Little bit worried about negative momentum, but will monitor closely.

GLD ForcastThis most likely course for gold to take over the next week. I believe GLD will fill the gap, test TL, and then be rejected and break down lower. Scalping up to TL, and then Short will be the positions i will be looking to take. I dont believe that Gold will be a safe bet in the event that we see a 5-10% correction in the overall market.