The confidence that the worst is overAlthough stocks fooled around all day yesterday until they were bought off, high-yield bonds rose, breaking further and further from the lows.

This once again underlines our thesis that the demand for government bonds is caused not only by the desire of investors to escape from risk (as some people think), but by the confidence that the worst is over.

Because inflation will also decline, and the Fed's position will gradually soften.

Otherwise, only 10-year government bonds would rise (making the curve flat), and high-yield bonds would not rise.

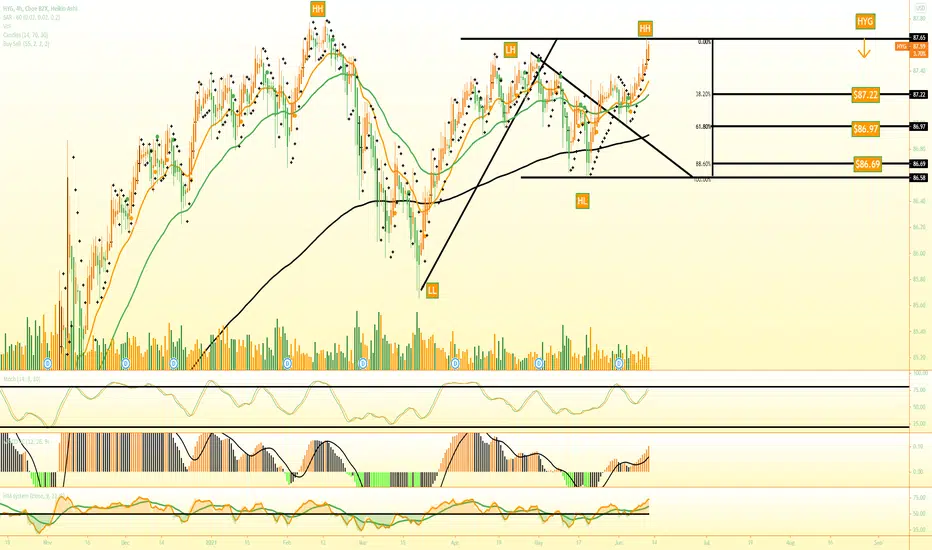

HYG trade ideas

Junk bonds, very good indicator for a liquidity crisis - 1929.2I wanna just short everything that moves. junk bonds look like 1929 free fall, when they break first support gonna be ugly.

Fed is gonna squeeze us to our knees. if everything so good why junk bonds not mooning lmao.

Implode quick (vix 80) to start recovery sooner. bruh this recession can be spotted by blind man.

xoxo

First look at BONDS!!! Then you'll understand equities! Bond yields often broadcast a pulse on global economic and geopolitical events long before the equities markets! Most market observers are already keeping 10yr Tsy yields on their radar, and of course the 3mth Bills/10yr Tsy spread as the key indicator of curve 'steepness' or 'inversion'. But especially as the Fed starts unloading bonds from its balance sheet, another metric to have front and center on the radar is 'credit spreads'. The chart of the High Yield ETF (HYG) vs the Investment Grade ETF (LQD) is a rough measure, for sure, but noteworthy nonetheless. It's noteworthy that credit spreads have already widened, with the spread on this ETF differential already back to 2019 levels! Ever since the start of Covid when the Fed all but assured the market that they'd underwrite corporate credits in order to avoid Covid-induced defaults, credit spreads have come crashing in, with some companies boasting the title 'zombies' given that they had no cashflow to sustain their debt load! Well, now with the Fed in 'kill inflation and tighten financial conditions' mode, credit matters once again! This is not to say that a credit crisis is over the horizon, but it does suggest that 'risk pricing' is returning to asset pricing! And the more that we see that in bond markets, one can be pretty certain that we'll continue to see it in equity markets.

High Yield related to Investment Grade break out?HYG / LQD weekly chart shows a breakout above the March 2020 former broken support which was tested as resistance in March 2021 and could even be called a cup and handle.

High Yield is commanded from this bonds because they are considered higher risk.

So with all the geopolitical and rising rates concerns, this seems contrary and signals that we may be in a risk-on environment.

This by itself is considered risk-on but needs to be taken in context.

It's definitely worth considering though.

The market participants driving this price movement is not afraid to put their money on higher risk bonds and the bond market is not something to ignore.

HYG/LQD ratioWith credit conditions starting to deteriorate currently,(mostly in Europe) high yielding debt will definitely be most negatively affected, especially after the first rate hikes from the Fed. Another great opportunity here to go short. The structure shows clearly a developing Wyckoff distribution similar to the one of Bitocin just before it crashed to 30k last May.

Risk Proxy Turns BullishIt's only Wednesday, but the weekly perspective on this ratio of high yield "junk" bonds to government treasuries is currently painting "Go" conditions. Often used as a proxy for overall market risk, the ratio trends higher when investor demand for high yield bonds is greater than their demand for government treasuries. The concept then is a rising ratio shows risk appetite, and a falling ratio suggests defensive positioning.

Notice that even through the Sept-Oct rally, GoNoGo Trend remained in neutral amber conditions ahead of the "risk off" conditions through Q4 and the start of 2022. As this ratio breaks out into a fresh "Go" trend, we could correlate more bullish conditions to risk assets in the equity and commodity spaces as well.

Looking to the lower panel we can see GoNoGo Oscillator broke through the zero line into positive territory the week of Dec 27, 2021, retested the objective neutral levels of all blended momentum indicators, found support, and has rallied positive again on heavy volume (the line is dark blue on heavy volume, aqua on light volume).

GoNoGo charts paint conditions in real-time, so this final weekly bar is still forming with two days of trading data yet to be factored in, but the weight of the evidence points to the upside.

Better Charts. Better Decisions. GoNoGo Charts.

Different Types of Risk On / Off IndicatorsJNK/TLT is equal to HYG/TLT

IWM/SPY

IWM/QQQ

BTCUSD is a newer one. Time will tell if it holds up.

"Risk on" means risk on 'outperforms' risk off.

It does not mean risk on goes up and risk off goes down. They can move in the same direction.

HYG IS NEARING A I.T. LOW HYG is now in the last wave within this decline or correction . this is the last neg for the markets. for this down leg . and we are now ready to see the mark go from BEAR PHASE target date jan 27 plus or minus 1 day . We now rally I will post . DO NOT BE SHORT

Credit markets signal danger if HYG continues below 84HYG can be used as a proxy to indicate health of U.S. credit markets, which is an economic backbone. Since my recent post about macro indicators, HYG has fallen further. You can see on chart that every move below 84.00 corresponds with a market downturn. So if January stock market declines happened as HYG kept going below 86 and 85, you can imagine greater market declines if HYG keeps falling. IF, keyword.

Further, this fits with the Fed statement that asset purchases will be reduced. Less systemic liquidity will drop markets. Junk bonds are seeming less attractive. Corporate credit tightens when Fed reduces liquidity. Applied to consumer credit, the nonstop loan and credit offers flooding mailboxes in 2020 have stopped (okay, greatly reduced).

I will be buying March expiry puts if HYG breaks 84.

hyg and jnk bonds are in dangerous spot with inflation + sellingInflation cpi near 7%, future potential rate hikes, FED reducing future purchases. Why would ne money be excited to jump in and buy up riskier paper at rates near 4-5% and stocks in a bear market? At what interest rate and risk premium are junk bonds attractive?

HYG Round TopScaling in for a short position.

If it fails, cut immediately and move on.

What're your thoughts?

HYGthe levy is soon to break, markets to follow ,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,

HYG Death Cross... Caution WarrantedHYG put in a Death Cross last week and this week, on November 22nd, HYG lost the October 11th low with SPY selling off heavy into the close. We may backtest the October 11th low but this is a potential negative indicator for equity risk on. Equities tend follow lockstep with high yield, or so they have with every major selloff since 2007-2008. This is something to keep an eye on over the next week or so, especially after Thanksgiving.

YTD Bond Performance Bond performance across USTY short and long term, US HY, US IG and EM sovereign and Corp.

Finding markets bottomsFinding markets bottoms, adding the new lows and new highs for better see the internal condition of the market

junk bonds undesired while treasuries catching bid, hyg over tltwith higher inflation and possible shrinking forward guidance, are corporate junk grade bonds less desirable now? maybe the market doesnt top out or pull back, but cpi over 5% while junk bonds yield mid 4% starts to sound less attractive for the risk, doesnt it?

HYG vs SPY - on Watch

HYG ETF, index composed of U.S. dollar-denominated, high yield corporate bonds. Versus SPY ETF.

HYG at triplet resistance, Wedge fractal characteristics, 50ma Week, potential break.

HYG High yield corporate bond ETF 1/0.1HYG High yield corporate bond ETF 1/0.1

Price levels chart - daily

Junk bonds topping out = Bearish leading indicatorThis is a monthly chart of the high yield corporate bonds ETF - aka "junk bonds". Notice that it is right at the a multi-year trend line. I expect this to start to go down given the multi-year resistance line. Yet one more canary pointing to a market top.

Negative Rate Cut? Powell Wants a Correction $SPYThe markets are at a crucial spot and Powell is due for a decision soon... The chance of negative rates is low but definitely not out of the picture and if that happens, TLT will pump and HYG/IWM will dump (yes SPY too). Timing will be hard but the pressure is certainly building and is confirmed on the technical side of things.

$TLT tested a crucial level at $148.9 this last week which could signal weakness in the equity/bond market as well as the Dollar. Either A) things will spin out of control regarding Delta variant and TLT will breakout or we could see this melt-up continue for roughly 4-5 more months before seeing IWM and the rest of the market make its correction. If TLT were to fall the market could also very likely follow to the downside, this environment is choppy.

On the other hand, we watch IWM as it typically can signal weakness in the market via smaller cap companies. If the markets do correct, puts on IWM/HYG will pay beautifully. I'll give this 6 - 8 month then pop, otherwise my short position will get stopped and we could just continue to melt up until the next election. Also whether Crypto has it's one or two top cycle will play a part in all this as money will either transfer away or to the Crypto market (& possibly away from other markets).

It should go as followed If markets do correct to the downside:

1) TLT will breakout and possibly melt quickly as done in 2020 or flash crash. SPY/ETFs could see a gap down then trend up to retest as resistance

2) SPY will begin its bleed, IWM HYG leads the way to the downside.

3) Metals and Cryptos seem like they could move in sync. Cryptos might even lead the way. The one question I ask is if people sell out of both Cryptos and Stocks, where does their money go? Will this create the largest spending era or send us into a depression? Share your thoughts below

DCJ | Melt-Up or Short