$INTC with a Neutral outlook following its earnings #Stocks The PEAD projected a Neutral outlook for $INTC after a Negative over reaction following its earnings release placing the stock in drift C with an expected accuracy of 75%.

INTC trade ideas

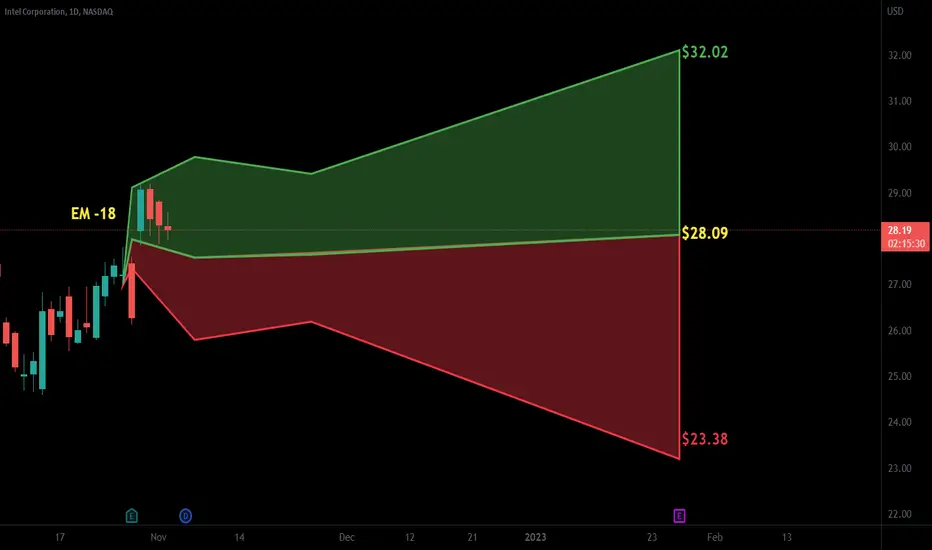

INTC - Drop not over yetIntel´s 50+% drop may be soon over, but I believe that we should still have one leg down.

It is very common for corrections to finish with RSI Divergence, and we still don´t see it in this chart.

I´ll be bullish once price breaks the channel and stays above gray support.

Trading Idea 005: IntelMarket Conditions:

- trend reversal

- bullish sentiment in the market

Key Level and Lines:

- $30.38 resistance

Trading Ideas:

- go long after a consolidation below the resistance

- a false breakout and bearish sentiment in the market = trade opportunity for shorting.

Intel $INTC ShortEarnings prospects not looking good. Will probably come in line to slightly miss due to inflation and supply chain problems. Look for a pull back to 22 area then a DCB. FOMC on Jan31, MSFT earnings miss, and current economic environment points to a lower price in the short term.

Intel gets some help from Uncle Sam?Chart shows AMD's market cap rising above Intel just when the bill is pass helping Intel...

INTC Intel Corporation Double Bottom Chart PatternINTC chart looks seems to have a textbook Double Bottom!

Looking at the INTC Intel Corporation options chain ahead of earnings , I would buy the $30 strike price Calls with

2023-1-27 expiration date for about

$1.29 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

[INTC] INTEL BUY SETUPlooking for a bounce. first target ~69-70$.

then it could expand or fall again.

Idea about intelIntel prepare itself for pullish movement .

so take care of the support shown here in the graph and wait for the takeprofit .

if our ideas seem good for you boost our channel .

INTC - D Chart- Falling wedge formed

- Cup has been formed waiting for handle and trend continuation.

- Major resistance has reached

Intel Corp. (INTC)Intel has generated $3.25 earnings per share over the last year ($3.25 diluted earnings per share) and currently has a price-to-earnings ratio of 9.0. Earnings for Intel are expected to decrease by -2.56% in the coming year, from $1.95 to $1.90 per share. Intel will be looking to display strength as it nears its next earnings release on Jan 26. The company is expected to report EPS of $0.20; most recent consensus estimate is calling for quarterly revenue of $14.5 billion.

INTC - Price Targets & Stop Loss📈 What’s up investors! 📉

Welcome back to another one of

💡“Mike’s Ideas”.💡

I post as I find signals… these signals are based on the personal rules I have built and follow in order to make up what I call the “SST Strategy”. Follow for more ideas in the future!!

I have 4 levels marked and colour coded on the Chart.

These levels are:

⚪ White = Entry Point

🔴 Red = Stop Loss

🟢 Green = 1.2:1 Risk Reward Ratio

🟡 Yellow = 1.5:1 Risk Reward Ratio

🔵 Blue = 2:1 Risk Reward Ratio

👀 So what are we looking at today…!!!

🚨( INTC ) Intel Corporation🚨

Intel Corporation engages in the design, manufacture, and sale of computer products and technologies worldwide. The company operates through CCG, DCG, IOTG, Mobileye, NSG, PSG, and All Other segments. It offers platform products, such as central processing units and chipsets, and system-on-chip and multichip packages; and non-platform or adjacent products, including accelerators, boards and systems, connectivity products, graphics, and memory and storage products. The company also provides high-performance compute solutions for targeted verticals and embedded applications for retail, industrial, and healthcare markets; and solutions for assisted and autonomous driving comprising compute platforms, computer vision and machine learning-based sensing, mapping and localization, driving policy, and active sensors. In addition, it offers workload-optimized platforms and related products for cloud service providers, enterprise and government, and communications service providers. The company serves original equipment manufacturers, original design manufacturers, and cloud service providers. Intel Corporation has a strategic partnership with MILA to develop and apply advances in artificial intelligence methods for enhancing the search in the space of drugs. The company was incorporated in 1968 and is headquartered in Santa Clara, California.

Looks very strongPrice is oversold in the weekly timeframe and has already bounced off twice the strong support with lots of volume the two times. Is very early to tell if is forming a double bottom, but it looks that market doesn't want the price to go lower under the support. This a long term holding, maybe a couple of years but the risk reward is too good to ignore it. On the other hand, check my previous post lines below on AVGO, another chip maker.

DONT SWIM AGAINST THE CURRENTTHIS IS INSANE - Technically speaking the market in general is in a downtrend. a recession or correction. it should not matter. what is insane is am taking a Long trade on such a downtrend market. As any trading Guru would say " dont swim against the Current " dont trade against the trend. But I did. well I make exceptions. let me explain.

The Long-term(M) is in a downtrend. the price is coming strongly overselling into a fresh DZ. I set my ENTR at 27.xx with STP-LOSS below the DZ; small risk with plenty room for profit to run. my risk to reward ratio adds up. I always calculate my estimates Rs (risk) before I calculate my estimated Rw (Reward)

When price enters the DZ: there are three possible outcomes;

- Trend Reversal - The DZ will hold & trend changes. Big win & small Loss

- Correction - The DZ will hold for sometime, giving small win and small Loss

- Breakthrough - The DZ does not hold at all, giving a small loss; I am OK taking that small loss; it is within my trade plan

What I was looking for was a correction, happy to take this small Long profit in such a downtrend market. to do this type of trade & swim against the current one much be very vigilant; tight STP loss is key.

What I did here, price entered the DZ, the correction began; I covered 1/2 of my position; I took $3 of each share, & let the rest (other 1/2) run; sadly but predictably, the correction lost momentum in a heavily bearish market. I readjusted my STP LOSS to exit trade at breaking even.

Fast In Fast Out ShortCandle is stuck in the cloud. Snatch a couple of short bucks for the next few days.

INTC Headed LowerBumping up against resistance at the .328 fib resistance level, Expect next leg down to test the -0.236 fib around 20.

Bullish Spike on Intel (INTC)This morning's 10am scan yielded bullish price action spikes on both AMD and INTC. I like the level that Intel NASDAQ:INTC is holding to for a swing trade. The first target will be a retest of this week's high.

In the longer term after a very long bearish trend the chip makers have begun to turn. It is somewhat "late" in the turn from October but there are now confirmed signs of a possible reversal. Daily chart:

INTEL is only up from hereindicators show a likely bottom here,

computers aren't going anywhere and INTEL is still the leader in chip manufacturing despite their issues loosing the patent lawsuit.

INTEL in for a major comeback.

RSI and MACD bottomed out,

dropping lower to 14$ possible but unlikely, most likely this is bottom and only up from here

INTL - Higher Highs Ahead?Coming in from a Bullish Market standpoint, Intel may be setting up for a big rally. Following the A-B-C correction, INTL would move into a wave 3, pushing for much higher prices.

INTC daily wave 2 of uptrendINTC daily wave 2 of uptrend probably I'm already in you can move your entry above next day candle if it closes above today's doji and completes morning star reversal.

$INTC with a Bullish outlook following its earnings #Stocks The PEAD projected a Bullish outlook for $INTC after a Negative over reaction following its earnings release placing the stock in drift A with an expected accuracy of 66.67%.

That's Why I am Keep saying "INTC" is very interesting right now

As What I posted on Oct 26th, I think INTC is very interesting right now, and INTC's earning proved what I was saying.

As reported, "Intel shares rose as much as 7% in after-hours trading Thursday even though the semiconductor giant gave a revenue outlook that suggested sales are slowing down heading into the end of the year. Intel (INTC) said that for its current, fiscal fourth, quarter it expects to earn $0.20 a share, excluding one-time items, on revenue of between $14B and $15B. That outlook suggests that Intel's (INTC) sales could fall as much as 31% from the fourth quarter of 2021.The company also lowered its full-year revenue estimate to a range of $63B to $64B, from an earlier forecast of $65B to $68B in sales. While its forecasts left something to be desired, Intel (INTC) reported third-quarter earnings that surpassed Wall Street's expectations. Intel said that it earned $0.59 a share, excluding one-time items, on revenue of $15.3B for the quarter ending September 30. Analysts had earlier forecast that Intel (INTC) would earn $0.33 a share on $15.3B in revenue. During the year-ago period, Intel (INTC) earned $1.45 a share on revenue of $18.1B. It was a rough quarter for Intel , as sales in its main business areas declined from a year ago. For its main business areas, Intel's client computing group, which includes sales of chips and technology for consumers and businesses, turned in revenue of $8.1B, down 17% from the third quarter in 2021, and data center sales of $4.2B, which fell 27%. Chief Executive Pat Gelsinger said in a statement that "despite worsening economic conditions," Intel "made significant progress with our product and process execution" during the quarter."

The market is already celebrating the results (up 7%), but I see this as an oversold bounce that will fix itself. Mobileye Global Inc. has raised very little cash for the company and won't change trajectory of things. Look lower for a buy point and be prepared to say farewell to that fat yield!

HOLD INTC if you can!

The investments and idea published may not be suitable for all investors. If you have any doubts as to the merits of an investment, you should seek advice from independent financial advisor or other professionals to determine what may be best for your individual needs. We do not and cannot guarantee that your use of our APP and/or any of its features will generate profits. All opinions, news, reviews, research, analysis, prices, or other information contained on or provided via this site are provided on an “as is” basis as general market commentary and/or expressions of opinion only. Information may not be complete, accurate or up to date and may not be suitable for every individual, nor be a suitable basis for an investment decision. No representation, warranty, undertaking, assurance or guarantee (express or implied) is made or given as to the availability, adequacy, accuracy, completeness, reasonableness or appropriateness of any of the information or opinions provided or expressed on or through this site. There is no obligation to notify you of any corrections or modifications.

Buying Intel..?Intel Corporation - 30d expiry - We look to Buy a break of 28.02 (stop at 25.88)

We are trading at oversold extremes.

In our opinion this stock is undervalued.

Price action has posted a Doji candle and signals a possible reversal of the recent trend.

The RSI is trending higher.

Bullish divergence is expected to support prices.

We need to see a break of bespoke resistance (at 28.00) to confirm the positive outlook.

Our profit targets will be 33.69 and 36.69

Resistance: 27.00 / 28.00 / 30.00

Support: 25.50 / 24.50 / 23.00

Disclaimer – Saxo Bank Group.

Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis , like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis , as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.