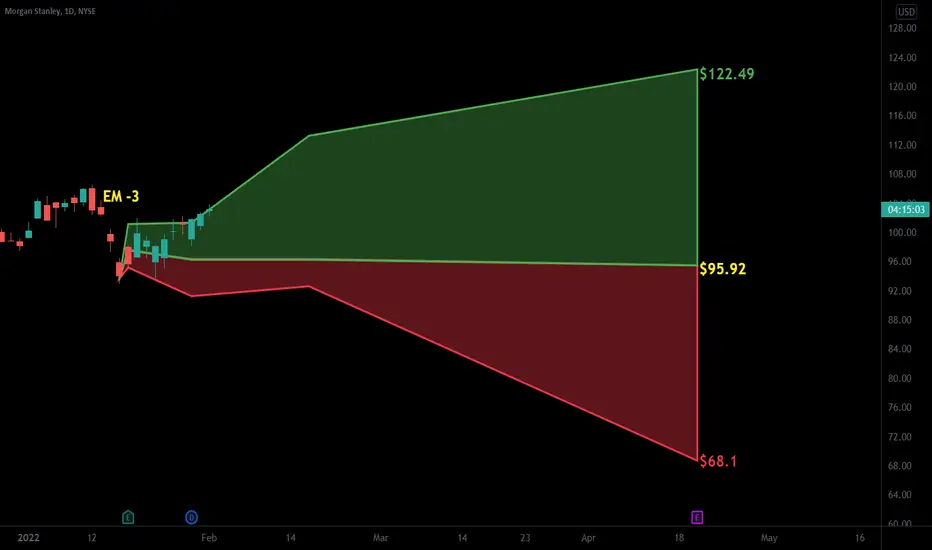

$MS with a Bullish outlook following its earnings #Stocks The PEAD projected a Bullish outlook for $MS after a Positive over reaction following its earnings release placing the stock in drift B with an expected accuracy of 60%.

DWD trade ideas

Rest on MondayWhen you're cognitively relaxed, you're likely to be in a good mood, so you like what you see, you trust

what you hear, you trust your intuition, and you feel comfortable and familiar. At this point, your thoughts

may also be relatively random and superficial. When you're nervous, you're more likely to be alert,

suspicious, put more energy into your hand, feel cramped, make fewer mistakes, but your intuition and

creativity are lower than usual

Thinking Fast and Slow

Relax ~

Morgan Stanley (US: MS) - Revival of the bull?100.77-101Morgan Stanley rebounded earlier on 8th March. Since then, prices had a strong consecutive up run especially for the past two days. Short-term target is at US$100.77-US$101.00 region. But we could buy at the lower immediate support at 86.45-87.00 region

MSHello everyone, to you expect the price to hesitate between the following numbers in relation to the bearish trend

90.82

86.99

75.85

70.07

But if it bounces off the trend line, we find it at the levels shown on the chart

Possible scenario for Morgan Stanleyif bear market gets really red I see this thing dropping 23% by april 1. Don't take my word for it. Also let me know if it looks like my, april 1, 70 strike puts will hit.

Morgan StanleyMorgan Stanley Daily..

The price may return for the second time to test the previous low of $82, after touching the current resistance level.

* Technical analysis and not a direct recommendation..

Morgan Stanley bounce coming. This analysis is based simply on the pattern and the RSI. RSI says oversold, pattern indicates clearly it's at/near the bottom of the trend and will rebound back upwards. Will it make it to the top trend line? Probably not. I'd bail well before that. This is a short term play with a tight stop loss outside of the lower trend line.

MORGAN STANLEY setting up for buyMorgan stanley is setting up for another buy opportunity.

Good luck @everyone

MS on WatchMS looks poised to break out from a long term consolidation. Looking for a quick move to 108. Trade would be very rate dependent. If yields fall or the yield spread tightens bank stocks will drop. I like this in and above the green box. No longer interested below the green box. Targets are the fib extensions above.

Buys setting up on Morgan stanleyHi Everyone,

Look for buys from the bottom. Also look at zero crossover for you to confirm entries.

Good luck

MSDaily Report

MS looking great for a breakout. If it can breakout of the 105 resistance level then the immediate target would be $111. If it fails to break it can find support at 102. I would be looking for a breakout on the RSI because sometime it can show a breakout ahead of time.

$MS with a Bullish outlook following its earnings #Stocks The PEAD projected a Bullish outlook for $MS after a Positive Under reaction following its earnings release placing the stock in drift A with an expected accuracy of 33.33%.

If you would like to see the Drift for another stock please message us. Also click on the Like Button if this was useful and follow us or join us.

MS - Double BottomPrice has twice bounced off support at around $93-$94 forming a double bottom pattern. This generally signifies the end of the prior downtrend and the beginning of a new uptrend so it looks like a good time to go long. Price has also just broken past resistance at $96, relatively easily, and there is a bullish crossover on MACD. Despite the strong technicals, this is a risky time in the market, especially with FOMC coming up in 2 days, so I would keep any position light. PT#1 is at $101.50 and PT#2 is at $106.50. Place a stop loss right under $94.

10x Any Trading Account - Using MathTLDR: It's not as hard to 10x an account as it may seem. By using math, we can exponentially grow our account while also exponentially making it easier to grow (and also continue to minimize our risk).

So, I am planning on growing an account from 3k - 30k. This is no easy task, but I am going to break down why it's not as hard as you think. Math!

As the account grows, hitting 10% of the original amount each day will get exponentially easier. Here's an example

Day 1 : 3k to trade with means each daily profit goal is ~ $450 (Thats 3 trades of 25% profit using reasonable risk management. I'm going to break that down later, why this isn't actually as difficult as it it may seem to do consistently) Hint: 0dte

Day 2 : We now have $3,450 in the account. Adjusting the trading plan risk management to the new account size, this means the profit goal for today is now ~ $518. (see where this is going)

Day 8 : By now, the account is $7,854 and the profit goal the previous day was $1032. By following the same trading plan and carrying it over as the account grows, the profit compounds.

Now, this is great, but it could be better. To further reduce risk, instead of increasing the profit target with a larger buying power, we can instead play with the trading plan to make our chances of success even higher. Lets take a look at the variables affecting the profit in a trade, and we'll come back to this idea in the future. (edited)

In every trade, there are 3 main factors that affect how much cash you acquire. These are:

The total % of your account used in each trade

The dollar amount you use in each trade

The % of profit you attain from those two figures

The total amount of the account we use in each trade, the less % we have to make in each trade. (10% on a 500 play is 50 - Alternatively, 5% on a 1000 play is also 50.) This allows us to trade even in markets where this isn't much volatility. We can shorten the time we are in a trade, and the movement required on the chart, to hit our goal. (edited)

Also, there's one huge factor I am relying on. As the account grows, hitting 10% of the original amount each day will get exponentially easier. Here's an example > Day 1: 3k to trade with means each daily profit goal is ~ $450 (Thats 3 trades of 25% profit using reasonable risk management. I'm going to break that down later, why this isn't actually as difficult as it it may seem to do consistently) Hint: 0dte > > Day 2: We now have $3,450 in the account. Adjusting the trading plan risk management to the new account size, this means the profit goal for today is now ~ $518. (see where this is going) > > Day 8: By now, the account is $7,854 and the profit goal the previous day was $1032. By following the same trading plan and carrying it over as the account grows, the profit compounds. Now, this is great, but it could be better. To further reduce risk, instead of increasing the profit target with a larger buying power, we can instead play with the trading plan to make our chances of success even higher. Lets take a look at the variables affecting the profit in a trade, and we'll come back to this idea in the future. (edited)

So back to our little example. Instead of increasing the goal each day, it would be wiser to adjust our trading plan to allow for more attempts (using less % of total BP per trade) or for higher success rate (5% profit per trade instead of 25%). This means that as our account grows, the effort will go down as success probability rate increases - exponentially.

This is where it all comes together. By day 10 of making $450 per day, we would have $7,500 in the account. We would effectively be doubling the amount of trades we can make (10% of the account per trade instead of 20%) and cutting the %gains needed per trade (from 25% to 20%).

We can now afford to lose more often, as we have more buying power. Because we can afford to lose more often, we can also afford to tighten our stops losses, minimizing the risk per trade. Also, we now have much more opportunity to slip into more trades, as our %gains needed decreases each day.

(As another method, this can be played with to your liking and manipulated differently depending on how you feel that day, once you get comfortable enough with your trading plan. So maybe you don't have to trade every day, and you take advantage of the compounding profit effect in the later stages. Say maybe, 5x into the 10x challenge. (15k out of a 3k - 30k challenge.)

This is also how the "rich get richer". As your capital grows from initial investment, it becomes easier and easier to make profits in comparison to that initial investment.

MORGAN STANLEY - BREAKOUT OR GOOD BUY OPPORTUNITYMorgan Stanley is expected to report earnings on 01/19/2022 before the market open. The report will be for the fiscal Quarter ending Dec 2021.

Better than expected results may give strong support to the bulls and send the price back into the channel. On the other hand, if the results do not satisfy the investors this will be a good signal for the bears to step in.

Morgan Stanley is the third-largest investment bank behind Goldman Sachs and JPMorgan Chase. In terms of revenue, it is the largest wealth management firm in the U.S. Morgan Stanley ranks behind only Goldman Sachs in the equity capital markets.

Risk Disclosure: Trading Foreign Exchange (Forex) and Contracts of Difference (CFD's) carries a high level of risk. By registering and signing up, any client affirms their understanding of their own personal accountability for all transactions performed within their account and recognizes the risks associated with trading on such markets and on such sites. Furthermore, one understands that the company carries zero influence over transactions, markets, and trading signals, therefore, cannot be held liable nor guarantee any profits or losses.

MS: Long Bullish Weekly Signal Alert$MS stock coming out of a weekly retracement and having a weekly squeeze. Trend and Pattern indicates the stock ready to breakout on a weekly time frame provided the Indexes consolidate and turn bullish here.

$MSStrong Relative strength.

making highs with volume

Need to cross $105

A small pull back to Moving average will be good

Resistance ZoneThe five time confirmed resistance zone seems to be corrective today and may be not broken immediately. The momentum seems to be slowing.

Morgan StanleyHello Traders,

welcome to this free and educational analysis.

I am going to explain where I think this asset is going to go over the next few days and weeks and where I would look for trading opportunities.

If you have any questions or suggestions which asset I should analyse tomorrow, please leave a comment below.

I will personally reply to every single comment!

If you enjoyed this analysis, I would definitely appreciate it, if you smash that like button and maybe consider following my channel.

Thank you for watching and I will see you tomorrow!