A Grim Picture of InflationFed Funds Futures (ZQ) CBOT:ZQ1! , 2-Yr Yield (2YY) CBOT_MINI:2YY1! , 10-Yr Yield (10Y) CBOT_MINI:10Y1!

This is the third report in the series “Year of the Rabbit: Short-tailed Trading”.

US Consumer Price Index (CPI) declined 0.1% in December 2022 on a seasonally adjusted basis, after increasing 0.1% in November, the U.S. Bureau of Labor Statistics reported on Thursday, January 12th. Over the last 12 months, the headline CPI increased 6.5%. The inflation index for all items less food and energy rose 0.3% in December, after rising 0.2% in November. The Core CPI increased 5.7% year-over-year.

December is the only month in 2022 when aggregate price falls below prior-month level. The headline CPI is now 0.5% lower than a year ago on an annualized basis.

Cooling inflation is welcoming news to consumers, businesses, and investors. It also gives the US Federal Reserve more flexibility to moderate its hawkish monetary policy.

Inflation by Category Data Paints a Different Picture

The December CPI data was a “one-man show”. Gasoline price declined 9.4% in one month, bringing its annual change to -1.5%. After an all-time high record of $5/gallon reached in June, we ended 2022 with lower gasoline price year-over-year.

If you think we are getting relief in energy cost, nothing could be further from the truth.

• Fuel oil dropped 16.6% in December, but it is up 41.5% for the year

• Electricity price went up 1% in December and +14.3% for the year

• Pipelined natural gas were up 3% monthly and +19.3% yearly

Americans are getting bigger utility bills to light up the room and heat the house this winter.

Other essential items:

• Food cost +0.3% in December and +10.4% Y/Y in 2022

• Shelter cost +0.8% monthly and +7.5% annually

• New cars cost 5.9% more but used cars are 8.8% cheaper in 2022

Inflation is certainly on the way down, but it is sticky. Many product and service items essential to household living and business operation are far from under control.

Interest Rate Outlook for 2023

After the release of new CPI data, market consensus centers on a modest 25-basis-point increase on February 1st., which would bring the Fed Funds rate up to 4.50-4.75%. I also expect another 25-bp raise on March 22nd, setting the so-called terminal rate at 4.75-5.00% for the rest of 2023. This is my baseline forecast for 2023.

The previous section shows that inflation is still uncomfortably high for food, housing, and energy to power the home, as well as for new vehicle. The Fed’s job for fighting inflation is far from over. I do not expect any rate cuts to occur in foreseeable future.

When it comes to central bank monetary policy, there is a lagging period before it works its way through the economy. The response lag could be anywhere from 6 to 12 months. By my estimate, it takes about 7 months in this rate-hike cycle.

The Fed initiated the first increase in March, but inflation did not peak until June at 9.1%. Monthly CPI was unchanged the following month. However, the slowdown was solely due to a sharp decline in gasoline price, not attributable to the Fed.

Core CPI topped 6.6% in September, then subsequently moved lower to 6.3%, 6.0% and 5.7% in the fourth quarter. October was the first month when core inflation reverses its rising path. This is where I mark the start of inflation response to monetary tightening.

Once the Fed reaches its terminal rate, the force of inertia would carry the policy impact on inflation for several more months. That’s why the Fed is likely to keep the rate unchanged for the remainder of 2023, measuring the policy effect.

Fixed Income Investment Opportunities

On “The Real Cost of Fed Rate Hikes”, published on July 25th, I spelled out the impact of interest rate increases to households, corporations, Federal and local governments.

With the risk-free rate expected to reach 5%, all borrowing cost will go up further, even after they rose significantly last year. As the economy slows down, those with high debt loads may not make it through this downturn.

If you plan on investing in bonds, default risk should be on the very top of your mind. Consider safe play: Avoid any issuer with a high debt-to-equity ratio. Corporate high-yield, municipal bonds, and securities backed by adjustable-rate mortgages and credit card balance fit this bill.

JPMorgan Chase took notice. On Friday the 13th, JPM NYSE:JPM posted revenue that beat expectations, but the biggest US bank warned it was setting aside more money to cover credit losses because of a “mild recession” is its “central case.” The bank posted a $2.3 billion provision for credit losses in Q4, a 49% increase from the 3rd quarter.

For relatively safe investment options, bank certificates of deposits (Jumbo CD) and high-quality corporate bonds (rated A or above) offer yields from 4.50% to 6.0%. They could beat inflation in the coming years.

Spread Trade Opportunities

We have been in a negative yield-curve environment since July. In my opinion, slower rate hikes weaken the force that drives short-term yield rising faster than long-term ones. Once the Fed actions are over, mean reversion could occur so long as we do not fall into a deep recession.

A Refresher: Yield curve plots the interest rates on government bonds with different maturity dates, notably 3-month Treasury Bills, 2-year and 10-year Treasury Notes, 15-year and 30-year Treasury Bonds.

Bond investors expect to be paid more for locking up their money for a long stretch, so interest rates on long-term debt are normally higher than those on short-term. Plotted out on a chart, the various yields for bonds create an upward sloping line.

Sometimes short-term rates rise above long-term ones. That negative relationship is called yield curve inversion. An inversion has preceded every U.S. recession for the past half century, so it’s seen as a leading indicator of economic downturn.

On January 12th, 2-year T-note is quoted at 4.20% in cash market, while the 10-year T-note is priced at 3.61%. This measures the 10Y-2Y yield spread at 59 basis points.

The negative yield curve could become less inverted, then change to a flat yield curve in the coming months. It could reverse back to an upward sloping normal yield curve in 2024. Here are my reasoning:

• Easy money created by record government spending kept the borrowing cost low. This was a main reason why longer-term yields rise less than short-term ones.

• The new Republican-controlled Congress would stall the approval of big-ticket expenditure bills. Closing the flood gate could bring the borrowing cost back up.

• After the depletion of low-cost capital, lenders will have no choice but to raise the long-term lending rate above the short-term deposit rate.

CBOT Micro Yield Futures offer a way to express your view on future yield direction. You could also observe how the expected yield spread changes between 10Y and 2Y.

On January 12th, February Micro 10Y Yield Futures (10YG3) was settled at 3.446. February Micro 2Y Yield Futures (2YYG3) was settled at 4.081. The 10Y-2Y spread is -63.5 basis points.

Micro Yield Futures are notional at 1,000 index point, with each point equal to 1/10 of 1 basis point and value at $1. For example, if the 10Y-2Y spread narrows to -40 basis points, your position would gain $235 (= (-40+63.5) x 10) if you long the spread.

To trade Micro Yield futures, margins are $375 for 10Y and 2YY. A long spread can be constructed by a Long 10Y and a Short 2YY positions.

Happy trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trade set-ups and express my market views. If you have futures in your trading portfolio, check out on CME Group data plans in TradingView that suit your trading needs www.tradingview.com

ZQ1! trade ideas

30 day federal funds interest rates ... 30 day federal funds interest rates ... analysis of COT Futures Only - Percent of Open Interest and OBV, volume of effective federal funds ...

Fed vs. Inflation 4:6CME: SOFR Futures ( CME:SR31! ), E-Micro S&P 500 ( CME_MINI:MES1! )

While football fans are fervently following the 2022 World Cup, we analogize the Federal Reserve’s year-long battle with surging inflation to a football match. In this game, the Core CPI had an early advantage over the Fed Funds Rate, at 6.00% vs. 0.25% in January. The Fed mounted decisive offense, raising rates to 4.00% and bringing the deficit down to 2 points. But make no mistake – we are still trailing in the game. The Fed would not accept defeat. With stoppage time and overtime, the fight against inflation could drag on well into 2023.

When could the Fed declare victory? Its stated goal is to keep inflation at 2%. Most of us think this is unrealistic. In my opinion, the Fed needs to bring Core CPI below the Fed Funds rate at a bare minimum.

The Fed has been known to be data-driven. Unless there is conclusive data showing the inflation is on the way down and the economy is cooling, the Fed is unlikely to end its monetary tightening policy.

The talk of Fed Pivot is very misleading. Slowing the pace of rate hikes doesn’t mean an overhaul of monetary policy. The Fed simply needs time to collect more data and evaluate if previous rate hikes are working.

A lot depends on how quickly Core CPI comes down. It peaked at 6.6% in September and lowered to 6.3% in October. But one data point doesn’t make a trend.

• In 2022, Core CPI ranges from 5.9% to 6.6%.

• In 2021, it was between 1.3% and 5.5%.

• The last time Core CPI fell below 4% was in May 2021.

• Before 2022, it was 40 years ago (August 1982) when Core CPI went above 6.0%.

In the past 1-1/2 years, Core CPI ran up very quickly and then stabilized at a very high level. Any projection of 4% Core CPI is not supported by data. I don’t see Fed would take such hypothesis into consideration.

Statistically speaking, bringing Core CPI down below Fed Funds rate could only be achieved by raising rates. The BLS will release November CPI data on December 13th, and the next FOMC meeting is scheduled on December 13th-14th. The Fed would have the most recent inflation data available in voting for its December rate decision.

Short-term: Fed Pivot Trade

Current market expectation is for the Fed to break its consecutive 75-point hikes. Any rate increase below 75 bp would give a big boost to market morale. Expect the stock market to rally, and the US dollar and bond yield to retreat.

CPI data release and Fed decision are the “one-two-punch” ideal for short-term event driven strategies. There are good candidates I like for potential trade setup, from a risk-reward standpoint:

• Call Options for CME E-Micro S&P 500 Futures (MES)

• Call Options for E-Micro NASDAQ 100 (MNQ)

• Call Options for CME Euro FX (M6E)

• Call Options for CME 30-day Fed Funds Futures (ZQ)

• Call Options for Three-Month SOFR Futures (SR3)

For a rate increase below 75 bp, stock market is expected to rally, so it is bullish for MES and MNQ. US dollar will pull back, so it is bullish for Euro/USD exchange rate.

Short-term interest rate futures are quoted as discounted instrument, 100 – Rate. Lowered expected interest rates translate into higher futures prices. Therefore, it is also bullish for ZQ and SR3.

Medium-term: Recession

The world runs on credit. Fed monetary tightening policies have made it more costly for businesses and households to obtain credit. The run-up in cost happened very quickly and the impacts are profound. Below are comparisons of interest rates between December 2021 and November 2022, taken from various sources:

• 30-year-fixed mortgage: from 3.646% to 7.296%

• 60-month auto loan rate: from 3.85% to 5.29%

• Average credit card rate: from 14.91% to 19.20%

• AAA corporate bond rate: from 2.06% to 4.64%

• BBB corporate bond rate: from 2.53% to 5.88%

• SBA loan rate: from 6%-8% to 11.5%-13.5%

Even if the Fed stops raising rates now, financing costs are not likely to return to previous levels. The unwinding of Fed policy takes time. There is no indication that the Fed would lower rates after the terminal rate is reached. More likely than not, businesses and households would bear high interest cost well into 2024.

While Core CPI excludes food and energy, their impacts are felt everywhere. Take diesel as an example, the national retail average price is $5.228/gallon on November 27th, according to the American Automobile Association (AAA).

• This is 58.8 cents (-10.1%) below its all-time high of $5.816 set on June 19th. However, it is still 69.7% higher than a year ago.

• Comparing to gasoline, at $3.555/gallon, it is $1.461 or 29.1% below its record high of $5.016. But it is a modest increase of 4.7% year over year.

Diesel price is a tax on all products requiring highway transportation. Fed rate hikes are not likely to lower diesel production cost. In addition, higher wages, higher rents, and higher borrowing cost would stick, long after the Fed stop hiking rates.

In my view, the US could not avoid a recession in 2023. Weakening corporate profit and elevated unemployment will eventually take a toll on stock prices.

We have witnessed a strong Black Friday sales season. But worrisome signs emerge that US consumers are increasingly constrained by their budget. According to a CNBC report, Walmart is the most visited shopping destination. Higher priced Bloomingdale and Nordstrom reported a lull in sales earlier this month.

The downgrade from premium department stores to discount stores is a leading indicator, a classic economic example that inferior products thrive during a recession.

Another warning sign, “Buy Now Pay Later” payments increased by 78% compared with the past week, according to the CNBC report. Consumers still want to get the great deals for holidays, but they need help with financing.

If the market rallies after the November CPI data and December FOMC decision, it’s a good time to set up a 3–6-month trade shorting the stock market. Investor sentiment has significant impacts in the short term. But fundamental factors will win over in the medium/long term. If inflation fails to decline materially, the Fed will stay on its tightening course.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trade set-ups and express my market views. If you have futures in your trading portfolio, check out on CME Group data plans in TradingView that suit your trading needs www.tradingview.com

Terminal rates - How FX traders can benefit on TradingViewOne of the more watched interest rate settings in markets is the so-called ‘terminal’ interest rate – the point in the interest rate futures curve that reflects the highest point of future rate expectations – said differently, where the market feels a central bank could take its key policy rate by a specific date.

For those who really want to understand fed funds futures far better, this research piece from the St. Louis Fed is good - files.stlouisfed.org

As an FX trader, I am not too concerned as to the exact pricing in the rates market, a basis point here or there is no great issue - I loosely want to know what is priced by way of future expectations. This lends itself to more fundamental, tactical or thematic trading strategies and obviously day traders won’t pay too close attention, although, it’s worth considering that when rates are on the move you do see higher intraday volatility and that is a factor they have to operate in – where one of the core considerations for any day trader is ‘environment recognition’ and the assessment of whether we’re seeing in a trending or mean reversion (convergence) day.

We also see terminal pricing correlated with FX and equity markets – certain if we look at the relationship between fed funds futures April contract and USDJPY we can see the correlation.

Some will just use the US 2-year Treasury, as this is the point on the US Treasury curve that is most sensitive to rate pricing. The good thing about the fed fund's future though is we can see quantitatively the degree of rate hikes being priced for a set date.

Using the logic expressed in the St Louis Fed research piece we can see that the market sees the highest level where the Fed hike rates is March – subsequently, this is priced off the April contract, and currently, this sits at 4.90%.

Using 4.9% as our yardstick, interest rate traders would make a call if the expected fed funds effective rate was either priced too high, or indeed too low and could push above 5% - if new economic data emerged that suggested the Fed needed to go even harder on hiking than what is priced, and the terminal rate moves above 5% then the USD will find a new leg higher. Conversely, if the market started to trade this down to say 4.70% to 4.5% then the USD will find sellers – and notably USDJPY is the cleanest expression of interest rate differentials.

For TradingView users we can use this code in the finder box - (100-ZQJ2023). I put these codes into a watchlist and add a section' for heightened display. Again, this tells me where the peak pricing/expectations are in the interest rate curve. You can see the corresponding codes needed for each contract.

Terminal rates matter – if we're to see this trending lower, most likely in 2023, then it may be one of the clear release valves the equity market needs – for those looking for the Fed to pivot – the terminal rate will be one way to visualise it

Interest Rate Jargons and Fed Funds TrajectoryCBOT:ZQ1!

We are in a rising interest rate environment. But wait, which rate are you talking about?

All eyes are on the Federal Reserve. But could you really borrow money at the Fed Funds rate? If not, why is it a big deal? Most of us deal with different types of interest rates, such as those for bank deposit, mortgage loan, home equity loan, auto loan, credit card debt, student loan and business loan.

How are these rates determined? How are they related to the Fed Funds rate? Before you take out a loan or make an investment, it’s a good idea to gain some understanding of these questions. Our discussions mainly focus on US dollar interest rates.

Breaking Down an Interest Rate

According to Bankrate.com, the national average of 30-year fixed mortgage rate on October 8th is 6.89%. How is this rate calculated?

While all lenders employ elaborate methods to price an interest rate, I would like to introduce a simple formular to break down the rate into different components.

R(e) = R(rf) + D(p) + R(p) + L(p) , where:

• R(e) is the effective interest rate

• R(rf) is the risk-free interest rate

• D(p) is a duration premium

• R(p) is the risk premium

• L(p) is the liquidity premium

Risk-free Interest Rate

Generally, we consider short-term U.S. government debts to carry zero default risk. Target Fed Funds rate is currently in the range of 3.00%-3.25%.

Duration Premium

US treasury debts have different durations, or the number of days till their maturity.

* Treasury bills (T-bills) are discount instruments maturing in one year or less from their issue date. T-bills are issued for terms of 4, 8, 13, 26, and 52 weeks.

* Treasury notes (T-notes) are interest-bearing securities that have a maturity between 1 and 10 years. T-notes are issued in 2, 3, 5, 7, and 10-year maturities.

* Treasury bonds (T-bonds) are long-term treasury securities issued with a 30-year maturity. Outstanding T-bonds have terms from 10 to 30 years.

While all Treasury instruments are free of default risk, longer-term notes and bonds carry a duration premium. The longer the term, the higher the rate.

We are in an inverted yield curve environment. US Treasuries are quoted and priced in yields. On October 7th, 2-Year T-Note is quoted at 4.312% while 10-Year T-note at 3.888%. The easiest explanation is that investors expect a recession on the horizon and interest rates to fall in the future.

Risk Premium

When a lender evaluates the default risk of a loan, they examine the borrower’s Character, Capacity, Capital, Collateral, and Conditions . These are called the “5 Cs” of credit.

In mortgage lending, 5Cs generally refer to the credit history, income, down payment, value of the house, and current housing market conditions, respectively.

The bigger the risk premium, the higher the interest rate. A subprime borrower with a 600 FICO score would pay higher rate than one with an 800 FICO. Someone who could put up a 25% down payment would get a lower rate than those with 10% down only.

In a booming housing market, a bank is willing to accept a lower risk premium. In the event of the borrower default, it could resell the house and likely get paid back in full.

Liquidity Premium

In the old days, when you got a 30-year mortgage from a savings-and-loans, it had to carry it on the book for the entire term. Since the loan was so illiquid, the lender had to charge a high premium to compensate for all the risks it took.

With the invention of the mortgage-backed securities (MBS), lenders could package hundreds of loans into MBS. As they recoup most of the capital quickly, they could make more loans and generate more fees. Readers who are interested in the history of MBS may check out Michael Lewis’ classic, Liar’s Poker: Rising through the Wreckage on Wall Street.

Mortgage loan applicants may find that Federal Housing Administration (FHA) loans carry a lower rate. If your loan meets FHA’s requirements, it would be guaranteed by the government agency. Therefore, it carries a lower risk for the lender. Additionally, FHA-conformed loans can be easily packaged into MBS, enhancing their liquidity.

The Importance of Reference Rates

When a lender prices an interest rate, it usually employs one or more reference rates. If you carry a credit card balance, you may notice that interest charges vary monthly.

Look up the Customer Agreement with the credit card issuer, you would likely find them defining the Annual Percentage Rate (APR) as “prime rate + xx%”.

Typically, the mark-up portion on the right is fixed for contract terms. However, prime rate is usually defined as “Fed Funds + x%” and may be updated monthly or weekly.

If your credit card says APR = prime rate + 12% and Prime Rate = Fed Funds + 3%, you will be paying 18.25% (= 3.25+3.00+12.00) on outstanding balance, accrued daily. If the Fed raises rate by 75 bp next month, you will find the APR jumping to 19%.

Most lenders use reference rates. With Fed Funds being the root of rate calculation, every Fed rate decision would cause a repricing of the entire credit market. Fed Funds rate is the most important interest rate benchmark in the world. This is why we call it the “Mother of All Reference Rates”.

If you do not wish to iterate rate calculations step-by-step, other references may provide easy solutions. For example, a small-town savings-and-loans could set its deposit rate at the Secured Overnight Financing Rate (SOFR) CME:SR11! , and mortgage rates at 5 basis points over the national average rates published by Mortgage Bankers Association.

Rate Trajectory Projected by Fed Funds Futures

CME 30-day Fed Funds Futures ( CBOT:ZQ1! ) are directly linked to Fed Funds rates. Keeping up with T-bill market conventions, they are quoted like a discount instrument, 100 – R. Interest rate of 3.25% will be converted to a market quote of 96.75 (=100 – 3.25). If you ever wonder why, this is because short-term rate products do not make periodic coupon payments. Instead, you buy at a discount and get the par value back at maturity.

ZQ has monthly contracts going out for five years, with good liquidity for the first 1-1/2 years. It is a reliable measure of what investors think the Fed Funds rates would be in the future. Based on ZQ settlement prices as of October 7th, we get forward Fed Funds Rates implied by the futures market as follows:

• OCT 2022: 3.080%

• NOV 2022: 3.755% (+67.5 bp)

• DEC 2022: 4.110% (+35.5 bp)

• MAR 2023: 4.610% (+55.0 bp)

• JUN 2023: 4.635% (+2.5 bp)

• SEP 2023: 4.580% (-5.5 bp)

• DEC 2023: 4.435% (-14.5 bp)

• FEB 2024: 4.365% (-7.0 bp)

The above quotes show where futures market expects rate hikes to end in Mid-2023. They also expect Fed Fund rate to go down immediately afterwards.

Last Wednesday, in an interview with Bloomberg TV, San Francisco Federal Reserve Bank President Mary Daly called out such projections as inaccurate. She said that the Fed would like the rate to be restrictive enough (4.5%?) and to stay there for a while until inflation is back to the 2% policy target.

Mispricing in the outer months may be a good trading opportunity. Just remember, if you think the implied rate in December 2023 is too low, you would short ZQ futures. This is because of the 100 – R pricing convention. A bigger R would result in a smaller 100 – R.

Financial market is extremely volatile this year. Getting an information edge increases your odds of success in managing risk. I suggest leveraging real-time market data for a better gauge of market situation. TradingView users already have access to delayed data. A Pro user could upgrade to real-time CME market data for only $4 a month, a huge discount at the time of high inflation.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

Ahead of the Sept 22, 2022 FOMCAs I have been watching less and less crypto YT'rs, I have been drawn to bonds and bond data analysts as they seem to have a better understanding of overall market economic shifts and since I haven't published anything in a while, I wanted to get a brief heads up.

Just a quick look at of the target rate probability ahead of the 21st of Sept, 2022 Fed meeting. Currently expected earnings show 82.0% as of today:

www.cmegroup.com

-------------------------------

FED RESERVE BONDS 101

-------------------------------

For those unfamiliar with how Fed Funds Futures works here is a brief description, obvious if if this is all familiar knowledge you can skip smartee

The Federal Reverse Bank of NY (FRBNY) gathers funds daily of participating banks and broker dealers using a volume weighted average using the daily calculating the (E)ffective (F)ed (F)unds (R)ate (EFFR) as report by the Federal Reserve Bank of NY of participating banks and broker dealers.

ZQ charts typically track the 30-Day Fed Funds Futures Contracts. The contracts unit size is $5,000,000 per contract, contracts are listed monthly, extended 36 months or 3 years of yield curve

Fed Funds Futures are traded in IMM index terms as a price rather than a rate, the price is calculated in these terms:

100 - (IMPLIED RATE) = (FED FUNDS PRICE)

For example, with the implied price of 4.4% as expected by April or sooner

100 - 4.4% = 95.600

If is important to remember that the (F)ederal (O)pen (M)arket (C)ommitee, (FOMC) is backwards looking and sets each contract rate during each FOMC meeting obviously, the first fed futures contract rates to be affected by a rate change would be the next deferred contract month and not the contract month in which the meeting takes place, that is why investors are looking into April 2023 yield expectations as the market tends to price in future market behavior.

Obviously there are more than mechanics involved in calculating expectations besides FOMC reports such as other inflation expectations, and employment statistics, etc.

=^..^=

Effective Fed Fuds 2023 - Powell's War on You

Growth, Employment, Inflation - aka what's left of the Economy.

1. Employment - seeking roughly a reduction of 12 Million Jobs.

2. Growth - reduction of 50% for S&P 500 from Highs.

3. Inflation - Leads until Rate Lag breaks everything.

_________________________________________________________________________________

Capital Stocks

Powell - Bonds are going to see a Yield Curve Inversion, larger than usual. There is no single

condition, what is the term premium on Longer Rates is what matters most.

Powell - Housing will see a significant correction, we want the housing market back on a

sustainable path.

Powell - Equities are overvalued, period, the end. We're committed to "Price Stability"

Powell - The US should not return to a Gold Standard - Digital Currency is the path.

Powell - We flooded the System with Money (Digitally) by buying Bonds now we are selling them.

_________________________________________________________________________________

Forward Rates are indicating he is very serious.

I've warned about this for well over a year now - safe to say its come to pass.

Weak service PMI - Fed Fund Futures exploding higherFed Fund Futures exploding higher -> major dovish signal (higher price = less hikes).

Fed Fund Futures - Controlled YCCWhois buying all this MBS Junk that Fred and Wilma need to sell?

No One... absolutely not a soul.

In fact, Fred has to buy some, yeah right, it's not working out.

Balance sheet reduction (QT) remains the key metric to observe

as Fred, Wilma, and Dino went Bam Bam on the Bid recently.

Truly a modern stone-age family, this house of Flinstone.

If I recall correctly Fred was assigned with making rubble...

_______________________________________________________

The Quarry will have many landslides.

Eh, Stevie?

This is why....the market is green today, as the decline in rate hike expectations is a supportive factor.

Most of the retreat is attributable to recent dovish comments (e.g. Bostic), which were suggesting a temporary pause in the fall and Ackman rightfully so trashed this as a big mistake yesterday. Expect this trend to reverse as soon as supply issue blow up again as we move into summer.

Fed Funds futures disconnected from realityThe fed fund futures seem to be disconnected from reality and in my opinion the primary driver of the markets right now.

On their last meeting the Fed signaled a target rate of 1.75-2% by end of the year so over the 6 remaining meetings an average .25 rate hike per meeting. Economists think this will be a bit higher with 2x .5 hikes and 4x .25 hikes. As of today the Fed Funds futures for June were pricing in a .5 hike then a 86% chance of a .75 hike and 14% change of a 1.00 hike. last week before the June contracts were pricing in a 9% chance of .5 and 91% chance of .75. This is an extremely rapid chance in expectations with no real fundamental basis.

Historically the Fed and economists forecasts estimate almost always too high. Seeing the erratic nonsensical movements in these prices leads me to believe the market is just trading on momentum and a very one sided trade. With the next FOMC May 4th we should hopefully see some return to reality with the fed funds rate and expectations to substantially drop regardless if they do a .25 or .5 hike. Either this meeting or next I expect a complete 180 reversal in sentiment.

Rate hike expectation....go vertical ahead of the FOMC meeting. US-Natgas with highest level since 2008. Not so "transitory"..

Out of controlThe "peak inflation narrative" saw a resurgence yesterday, after 10Y yields dropped by over 10 bps intraday, but well..today's Philly Fed Index put an end to such ideas (input costs highest since 1979). FFR futures now price in 2.57% for the end of the year.

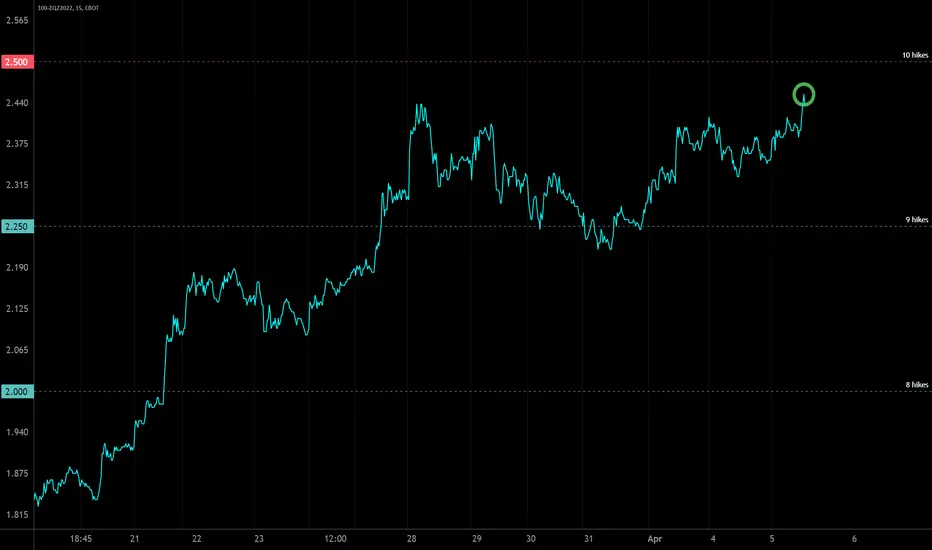

FFR Futures....(December contracts) are making new lows (chart is inverted) pointing to almost 10 hikes for the year now.

This is why....markets are selling off. Rate hike expectations are exploding, suggesting that the Fed is still way behind the curve.

The other aspect is the dangerous geopolitical situation that is still highly underestimated by markets (Ukraine/Yemen).

That escalated quicklyFuture now officially price in eight rate hikes for the year, but the stock market still refuses to capitulate.

Bostic sees 6 hikes and now and has less....confidence in an aggressive hike path. Fed funds rate futures have other ideas meanwhile..

Good morning!

Fed Rates vs SPYThe rates and market usually trend up and down with each other. Now with rates being so low for so long, the market needs to come down to meet the rates. How long far down will it go to reach the rates? Hard to say.

Fed rates VS marketIn the past fed rates have gone up to pace the market. Now they're rising to meet the falling market. Where will the market meet the fed?

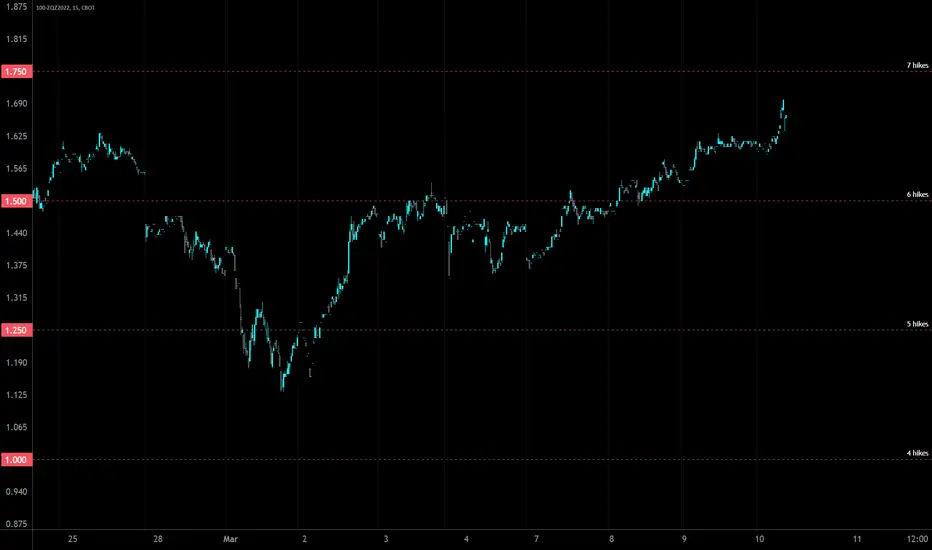

A war....possibly military involvement from China, and now 7 hikes fully priced in! Good luck with that.

Rate hike probabilities....are moving towards seven hikes again. Traders will be disappointed if they bet on support from the monetary authorities.

Markets are pricing out....a 50 basis points in March.

This is one of the main reasons the equities have found some support and are drifting higher. According to the CME Fed watch tool, there is only a 12.4% probability, that the Fed will hike by 50 basis points.

The chart depicts the inverted April federal fund rate future contract.