US Technology Stock Sector. The Underpressured PathThe recent reduction of tariffs under former President Trump's administration, while intended to ease trade tensions, has had several negative impacts on the U.S. technology sector, particularly in 2025.

Increased Costs and Supply Chain Disruptions

Despite some tariff reductions, the overall tariff environment remains highly volatile and complex. Many tariffs on tech products, especially those involving China, remain elevated-up on Chinese-made smartphones and other electronics. This has significantly increased manufacturing costs for U.S. tech companies reliant on global supply chains, particularly those sourcing components or assembling products in China, Vietnam, and other Asian countries.

The tariffs have disrupted supply chains, forcing companies to reconsider production locations and logistics. Many firms are shifting production away from China to countries like India or Vietnam to mitigate tariff impacts, but this transition is costly and slow. Reshoring semiconductor manufacturing to the U.S. is challenging due to high labor costs and lack of skilled workforce, which means higher prices for end products like AI-enabled PCs and servers are expected.

Suppressed Consumer Demand and Market Uncertainty

Higher tariffs translate to increased retail prices for consumer electronics, reducing demand. For example, smartphone prices have risen, leading to weaker consumer sentiment and slower sales growth. This is particularly harmful in a sector where rapid innovation and high sales volume are critical for profitability and investment in new technologies.

The uncertainty caused by fluctuating tariff policies has also led to delayed purchasing decisions by enterprises and consumers. Companies are hesitant to invest in new hardware or AI infrastructure due to unclear future costs and potential further tariff changes. This delay threatens technology roadmaps and weakens the U.S. tech sector's competitiveness globally.

Impact on Innovation and Investment

Tariffs have broader implications beyond immediate cost increases. By fragmenting markets and increasing operational costs, they reduce incentives for innovation. Companies face pressure to duplicate investments or abandon certain markets, which slows technological progress and reduces the U.S.'s ability to maintain leadership in emerging fields like AI and advanced semiconductors.

The increased costs and uncertainty have also dampened investment in U.S. tech infrastructure. Although some companies like TSMC and Apple have announced U.S. manufacturing investments to offset tariff impacts, these efforts are insufficient to counterbalance the negative effects fully. The long lead times and capital intensity of building semiconductor fabs mean that reshoring will not provide a quick fix.

Economic and Strategic Risks

The tariffs contribute to broader economic risks, including potential recession, inflation, and job losses in the tech sector and related industries. CEOs across sectors have expressed concerns about the tariffs leading to economic downturns, higher prices, and layoffs. The tech sector, being highly globalized and interconnected, is particularly vulnerable to these macroeconomic shocks.

Moreover, the tariffs strain U.S.-China relations, a critical factor in global tech supply chains and innovation ecosystems. Retaliatory tariffs from China and other countries further complicate market access for U.S. tech firms, reducing their export opportunities and competitiveness.

Conclusion

In summary, the recent tariff reductions under Trump's policy have not fully alleviated the negative impacts on the U.S. technology sector. Elevated tariffs continue to raise manufacturing costs, disrupt supply chains, and suppress consumer demand. The resulting uncertainty delays investments and innovation, while economic risks and strained international relations further threaten the sector's growth and global standing. These factors collectively undermine the competitiveness and future prospects of the U.S. tech industry.

Technical challenge

The main technical graph for US Technology Sector Futures CME_MINI:XAK1! (cost-adjusted modification) still remains under key resistance of 52-week SMA, which indicates on further possible bearish pressure.

--

Best wishes

@PandorraResearch Team

XAK1! trade ideas

US Technology Sector Futures. The Heartbreak HotelPresident Donald Trump's tariffs on imported tech goods, targeting China, the EU, Canada, and Mexico, are reshaping the U.S. technology sector through higher costs, supply chain disruptions, and retaliatory trade risks. While intended to boost domestic manufacturing and reduce trade deficits, these measures are creating immediate economic strain across critical industries. Below is an analysis of their key negative impacts:

Rising Consumer Prices and Hardware Costs

The 25% tariff on EU semiconductors, 10% levy on Chinese goods, and 25% duties on Canadian/Mexican imports are projected to add $50 billion in new costs to North American tech supply chains. This directly affects consumer electronics:

Smartphones and laptops. Apple’s iPhone production in China exposes it to 10% tariffs, likely forcing U.S. price hikes.

Semiconductors. The U.S. relies on China and Taiwan for 80% of 20-45nm chips and 70% of 50-180nm chips, with tariffs disrupting access to essential components.

Cloud/AI infrastructure. Steel and aluminum tariffs (25%) increase data center construction costs, potentially raising prices for AWS, Google Cloud, and Microsoft Azure services.

Experts warn companies may pass 60-100% of tariff costs to consumers rather than absorb profit losses.

Supply Chain Disruptions and North American Integration

The tariffs jeopardize tightly integrated North American production networks:

Cross-border dependencies. Components often cross U.S.-Mexico or U.S.-Canada borders multiple times during manufacturing. Christine McDaniel of the Mercatus Center notes this integration means tariffs “hurt the pricing power of the U.S.” by inflating domestic costs.

Critical material shortages. Canada supplies nickel and cobalt for batteries, while Mexico handles assembly for firms like Foxconn. Tariffs risk delays and renegotiations with suppliers.

Retaliatory measures. The EU may respond with fines or trade barriers against U.S. tech giants like Apple and Google, escalating tensions.

Sector-Specific Challenges

Semiconductors and Hardware

Chip shortages. With limited domestic foundry capacity, tariffs on EU semiconductors threaten AI development and device manufacturing.

Networking equipment. Proposed 10% tariffs on Chinese-made routers and modems could disrupt cloud providers reliant on these components.

Data Centers and AI

Construction delays. Steel/aluminum tariffs increase costs for server racks and cooling systems, potentially delaying $80 billion in planned U.S. data center investments.

AI infrastructure. Projects like the $500 billion Stargate initiative face higher expenses for imported components, slowing AI adoption.

Macroeconomic Risks

Trade deficit growth. Despite tariffs aiming to reduce the $1 trillion U.S. goods trade deficit, S&P Global warns retaliatory Chinese tariffs could worsen imbalances.

Job losses. Economic modeling suggests tariffs may cost 125,000+ U.S. tech jobs through reduced consumer spending and IT budget cuts.

Innovation slowdown. While firms like TSMC and Intel accelerate U.S. fab construction, short-term supply chain reallocations divert R&D funding.

Corporate Responses and Limitations

Some companies are attempting mitigation strategies:

Stockpiling. NVIDIA and AMD are urging partners to increase pre-tariff production.

Domestic shifts. Apple plans $500 billion in U.S. manufacturing, while TSMC pledged $160 billion for stateside fabs.

However, these efforts face scalability issues. Building advanced chip foundries takes 3-5 years, leaving gaps in critical components. Meanwhile, 65% of IT firms report difficulty finding tariff-free alternatives for Chinese inputs.

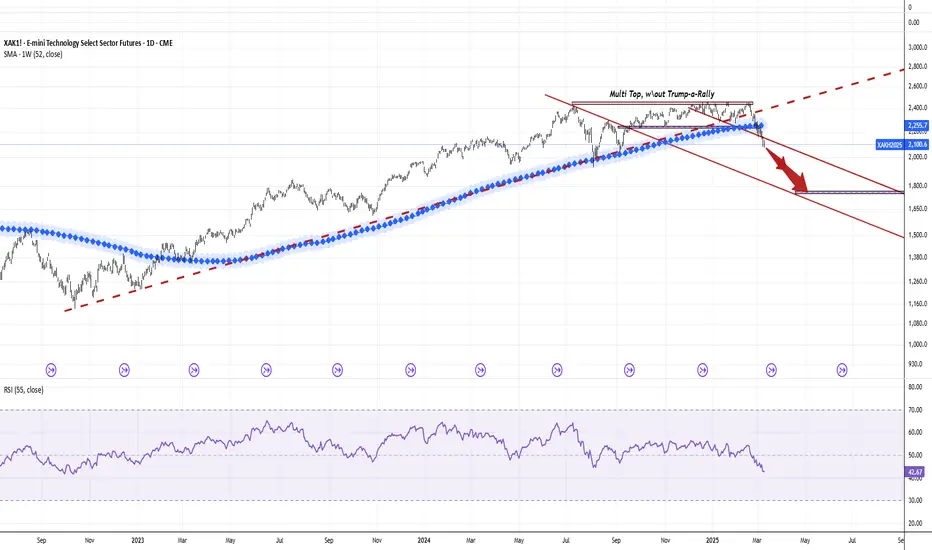

Technical challenge

The main technical graph for US Technology Select Sector Futures CME_MINI:XAK1! (CME Group mode of AMEX:XLK - SPDR Select Sector Fund - S&P500 Technology ETF) indicates on further Bearish market in development since major support of 52-week SMA has been broken already, with possible upcoming Bearish cascade effects in the future.

It is also important to note the almost complete absence of a Trump-a-rally in the 2024 holiday quarter, which contributed to the formation of a multi-resistance top.

Conclusion

While the tariffs aim to strengthen U.S. tech autonomy, their immediate effects—higher prices, supply instability, and strained international relations—outweigh potential long-term benefits. With global IT spending still projected to grow 9% in 2025, the sector’s resilience is being tested by policy-driven headwinds that threaten America’s competitive edge in semiconductors, AI, and consumer electronics.

Investing in S&P500 Technology Sector Futures / ETFs seeks to provide precise exposure to companies from technology hardware, storage and peripherals; software; communications equipment; semiconductors and semiconductor equipment; IT services; and electronic equipment, instruments and components industries; allows investors to take strategic or tactical positions at a more targeted level than traditional wide style based investing.

S&P500 Technology Sector Futures / ETFs are designed for investing at a more targeted Technology level, since nearly 50 percent of holdings weight just a five well-known names:

Name Weight

APPLE INC NASDAQ:AAPL 15.61%

MICROSOFT CORP 12.83%

NVIDIA CORP NASDAQ:NVDA 11.91%

BROADCOM INC NASDAQ:AVGO 5.18%

SALESFORCE INC NYSE:CRM 3.11%

--

Best 'Heartbreaking' wishes,

@PandorraResearch Team 😎

The Implications of Nasdaq 100 RebalancingCME: Micro Nasdaq 100 Futures ( CME_MINI:MNQ1! ), E-Mini S&P Technology Select Sector Futures ( CME_MINI:XAK1! )

The Nasdaq 100 index tracks the 100 largest non-financial stocks listed on the Nasdaq stock exchange. Since its inception over 38 years ago, it has become the world’s preeminent large-cap growth index.

So far in 2023, Nasdaq 100 has surged 42%, far outpacing the 18.7% gain from the S&P 500 and the 6.4% return by the Dow Jones Industrial Average. This big rally has prompted the Nasdaq to implement an index "Special Rebalance". What’s going on here?

Nasdaq-100: Market-cap weighted Index with a Twist

In the world of stock market indices, the two most common construction methodologies are equal-weighted and market-cap-weighted. The Nasdaq 100 is market-cap weighted, meaning the weight of each component is based on its market cap as a percentage of the aggregate market cap of the index. The higher the market cap, the bigger the weight.

Nasdaq performs regular quarterly weight adjustments in March, June, September, and December. To prevent the index from becoming too top-heavy and unbalanced, Nasdaq imposes weight limits in its Nasdaq Index Weight Adjustment Guidelines.

• No security weight may exceed 14% of the index.

• If the aggregate weight of the five largest market capitalizations is more than 40%, they will be adjusted to 38.5%.

• No security outside the largest five market cap companies may have a final index weight exceeding 4.4%.

The list below shows index weight as of June 30th, the last quarterly adjustment, and the most recent market cap as of July 21st, for the top ten companies in Nasdaq 100:

• No. 1, Microsoft (MSFT): market cap $2,556bn, index weight 12.92%

• No. 2, Apple (AAPL): $3,019bn (12.57%)

• No. 3, Nvidia (NVDA): $1,094bn (6.94%)

• No. 4, Amazon (AMZN): $1,334bn (6.85%)

• No. 5, Tesla (TSLA): $830bn (4.25%)

• No. 6, Meta (META): $756bn (4.22%)

• No. 7, Alphabet Class A (GOOGL): $1,560bn (3.71%)

• No. 8, Alphabet Class C (GOOGL): $1,599bn (3.64%)

• No. 9, Broadcom (AVGO): $373bn (2.40%)

• No. 10, PepsiCo (PEP): $263bn (1.70%)

• Top-5: market cap $8,833bn, index weight: 43.53%

• Top-10: market cap $13,384bn, index weight: 59.20%

• Nasdaq 100 (^NDX): aggregate market cap $25,990bn

The Top-5 has already breached the 40% mark and will be brought down to 38.5% in the “Special Rebalance” to address the concerns of over-concentration:

“A Special Rebalance may be conducted at any time based on the weighting restrictions described in the Index Rebalance Procedure if it is determined to be necessary to maintain the integrity of the Index.”

How will this Rebalancing Impact Investors?

According to the Nasdaq, over $500 billion in exchange traded funds (ETF) are tied to the Nasdaq-100, including Invesco QQQ ETF, iShares Nasdaq-100 UCITS ETF and ProShares UltraPro QQQ, just to name a few. If each fund tracks the Nasdaq 100 closely and responds to the rebalancing immediately, the Top-5 stocks in the portfolio will be reduced by 5% (from 43.5% to 38.5%). This would create short-term selling pressure in tens of billions of dollars.

To put the figures in context: although the Top-5 companies have an aggregate market cap of nearly $9 trillion, they have a modest daily float. Based on my calculation, the average daily transaction value over the past three months was only $77 billion, less than 1% of their market valuation, with 337 million shares changing hands.

Leading up to the rebalancing, we are seeing larger trade volume and higher volatility:

• On July 21st, Microsoft had a trade volume of 69.3 million shares, vs. its 3-month average volume of 29.3 million shares;

• Nvidia: trade volume 96.2m vs. 3-mo average 49.3m

• Alphabet: trade volume 55.5m vs. 3-mo average 26.4m

• Amazon: trade volume 69.5m vs. 3-mo average 63.6m

Since peaking at 15,932 on July 19th, Nasdaq 100 has trended down in the last three trading sessions, currently trading at 15,455 on the morning of July 24th.

Arbitrage Opportunity between Technology Indexes

The Nasdaq 100 rebalancing is a unique issue with the Nasdaq 100 index. It has nothing to do with the fundamentals of these companies and has no impact on other Tech sector stock indexes which also include the same component companies.

The S&P Technology Select Sector (XAK) has over 90% correlation with Nasdaq 100 (MNQ) historically. The former includes Apple, Microsoft and Nvidia, but not Alphabet or Amazon.

In the past five years, XAK outperformed MNQ by 40%. In the past five trading days, MNQ underperformed XAK by 1%, likely due to the impact of the Nasdaq-100 rebalancing.

In the long run, Nasdaq 100 rebalance will dilute the impact of the largest stocks in the index. Strong growth in Big Tech will be fully represented in XAK but capped in MNQ. This, in my opinion, would result in a widening spread between XAK and MNQ.

XAK futures contract is based on $100 x S&P Select Sector Technology Index. At 1,786.6, each XAK contract has a notional value of $178,660 on July 21st. CME requires an initial margin of $9,500.

MNQ contract is based on $2 x Nasdaq 100 Index. At 15,555, each MNQ has a notional value of $31,110. CME requires an initial margin of $1,680.

Based on the relative notional values, someone bullish on the spread could establish a trade with 1 long XAK and 6 short MNQ.

Using the last five days as an example:

• If XAK increases by 1%, the long end of the trade would show a gain of $1,787 (17.9 x 100). If, during the same period, MNQ is flat, the short end would have no gain or loss. This spread combination would have a net gain of $1,787.

• Using initial margins of $19,580 as a cost base, this equates to a one-week return of +9.1%.

For comparison, if a trader invests in a Nasdaq 100 ETF and the index gains 1%, the return would also be 1%. Trading in futures comes with a leverage that would supercharge the gain if you were on the right direction.

The spread trade would loss money if MNQ has a stronger performance than XAK.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trading set-ups and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Disinflation – Fact or Fiction?CME: S&P Technology Select Sector ( CME_MINI:XAK1! )

The U.S. consumer price index (CPI) rose 0.5% in January and +6.4% year over year, reported the Bureau of Labor Statistics (BLS) on Tuesday. Excluding food and energy, Core CPI increased 0.4% monthly and 5.6% yearly.

Economists surveyed by Dow Jones expected the headline CPI to grow 0.4% monthly and 6.2% yearly. Expectations for core CPI changes were 0.3% and 5.5%, respectively.

On Tuesday, US stocks fell at open in response to the hotter-than-expected CPI report. But major indexes recovered somewhat at the close of the day. The Dow Jones Industrial Average slipped 156 points, or -0.46%, after initially losing over 300 points. The S&P 500 was flat at 4,136 (-0.03%), and the Nasdaq 100 gained 68 points to 11,960.

US Treasury yields ticked higher. 2-year yield went up 94 ticks to 4.628%, while 10-year yield lifted 36 points to 3.755%. Bond investors widely expected the Federal Reserve to raise rates by 25 basis points to the 4.75%-5.00% range in March.

Mega Trend in US Inflation

While we usually focus on the percentage changes in inflation, CPI data are constructed as indexes, each using 1982-84 price data as a baseline at 100. January CPI reading of 299.170 is 0.8% above December of 296.797. It is up 6.4% from 281.148 in January 2022 (Data in this section is from Table 1 in the January CPI release).

Interpretation: Today, the average price of goods and services in the U.S. is about 3 times as high as the price level from nearly four decades ago. This translates into a compound annual growth rate (CAGR) of 2.93% for the past 38 years.

Insights: Long-run inflation rate is almost one percentage point higher than the Fed policy target. With less restrictive monetary policy on one hand, but more expansive fiscal policy on the other, the 2% goal appears to be far fetching. Barring a major recession, I expect the US inflation to stay above its 3% historical average in the foreseeable future.

In the past four decades, cost of many consumer goods tripled in price, including Food (+219%), Energy (+183) and Core CPI (+202%). But there are noticeable outliners:

• Tobacco and smoking products, +1289%

• Motor vehicle insurance, +559%

• Medical care services, +502%

• New vehicle, +77%

• Apparel, +28%

January CPI Readings

Before diving into the data, we should know that when BLS releases CPI data in February, it readjusts the weighting to account for the latest changes in the cost of living. For 2023, CPI weights are updated annually based on a single calendar year of consumer expenditure data. This reflects a change from prior practice of updating weights biennially.

The changes of weighting by product and service category in the January report:

CPI Category Old Weight New Weight Change

Housing 46.40% 44.40% +2.0%

Entertainment 5.70% 5.40% +0.3%

Food 14.50% 14.40% +0.1%

Clothing 2.50% 2.50% 0.0%

Other 2.60% 2.70% -0.1%

Medical 7.70% 8.10% -0.4%

Education 5.20% 5.80% -0.6%

Transport 15.30% 16.70% -1.4%

Rising shelter costs accounted for nearly half the monthly price increase. The component accounts for more than one-third of the index and rose 0.7% on the month and was up 7.9% from a year ago. Energy also was a significant contributor, up 2% month over month (M/M) and 8.7% annually, while food costs rose 0.5% M/M and 10.1% annually.

Food: Up 0.5% M/M in January from 0.1% in December. Annualized inflation is 10.1%.

Energy: Up 2.0% M/M in January from -3.1% in December. Annualized gain is 8.7%, of which, gasoline (+1.9%), diesel (+27.7%), electricity (+11.9%), and natural gas (+26.7%).

Shelter: Up 0.7% M/M in January from 0.8% in December. Up 7.9% Y/Y.

Transportation: Up 0.9% M/M in January from 0.6% in December. Up 14.6% Y/Y.

While the headline CPI ticks down from 6.5% to 6.4% on an annualized basis, January price increase of 0.5% is significantly higher than the December reading of +0.1%.

Overall inflation level is undoubtedly on the way down, but price increases from food, shelter and transportation are very sticky and don’t normally go down once moving up.

Is disinflation a fact or fiction? I think we are somewhere in between, in the Twilight Zone.

The US Stock Market Narratives

In the past three years, the stock market narratives have changed several times:

• After the initial pandemic hit in March 2020, US stocks staged a very impressive bull run. Growth drivers were US companies innovating with new products and services and catering for “work-from-home” employees and “play-at-home” consumers.

• 2022 started with a major geopolitical crisis, pushing stocks sharply down. Fed rate hikes from March 2022 dragged major stock indexes into bear market territory.

• Since inflation peaked in July and the Core CPI reading confirmed it in October 2022, US stock market began to rebound, centering on the notion of “Fed Pivot”.

More recently, investors are caught by conflicting economic data.

• Unemployment at 50-year low vs. Big Techs pushing rounds of massive lay-offs;

• Lower inflation rate vs. “Eggflation” and “Shrinkflation” that consumers experience;

• Whether the Fed is hawkish or dovish depends on the next dataset.

While investors try to make sense of all these, stock market moves sideways. The 30-day returns for Dow and the S&P are -0.83% and +3.20%, respectively.

Are we at the beginning of a new bull market? Or is it a bear relief, a temporary rebound from a bear market? To make an assessment, you need to know how many more rate hikes could be (pick a number between 1 and 4), and what the terminal rate would be (5.0%, 5.25%, 5.5%, 5.75%, or 6.0%)? I have no idea.

When uncertainty becomes the dominant narrative, it’s time to explore opportunities that promise more certainties.

AI - New Engine for Economic Growth

One visible exception is Nasdaq 100, which gained 8.9% in the past month. S&P Technology Select Sector Index (XAK) had an even higher return at 9.5%.

Most Big Tech companies were vastly overstaffed during the pandemic years. With stock prices cutting by two thirds or more, they are forced to live within their cash flow. Cutting off unprofitable divisions and laying off redundant staff help them survive in leaner years.

This is certainly very painful for the tech workers and their families. To investors, Big Tech may have transformed itself from lofty Growth Stock to reasonably priced Value Stock. For Nasdaq 100, its trailing 12-month price/earnings ratio was 34 one year ago. It is 23.63 as of February 10th, according to Birinyi Associates.

Technological breakthroughs have always powered the US economy to growth for the long run. Personal computers in the 1980s, Internet for the 1990s, smart phones and mobile internet in the 2000s, and electric vehicles in the 2010s, just to name a few.

In my opinion, Artificial Intelligence will be our economic growth engine in 2023. While AI is nothing new, the viral success of ChatGPT has sensationally changed the game. Its popularity among mainstream consumers helps form strong support for all publicly traded companies in the AI sector, not just for OpenAI and its parent Microsoft.

While writing this report, I asked ChatGPT one question: “Please show me the top-10 publicly traded stocks in the AI field.” Below is his/her/its answer:

1. Alphabet Inc. (GOOGL) - Google's parent company, which has been investing heavily in AI technology and applications.

2. NVIDIA Corporation (NVDA) - A leading company in graphics processing units (GPUs), which are commonly used in AI training and inferencing.

3. International Business Machines Corporation (IBM) - A company that has been developing AI technologies for several years and has a range of products and services, including the Watson AI platform.

4. Microsoft Corporation (MSFT) - Microsoft has invested heavily in AI technologies, and its Azure platform provides a range of AI tools and services.

5. Amazon.com, Inc. (AMZN) - Amazon's AI capabilities are used in a variety of products and services, including the Alexa voice assistant and its recommendation algorithms.

6. Baidu, Inc. (BIDU) - A Chinese company that has been investing heavily in AI technologies, including natural language processing and autonomous driving.

7. Alibaba Group Holding Limited (BABA) - A Chinese company that has also invested heavily in AI technologies and has been developing AI applications for e-commerce, logistics, and finance.

8. Intel Corporation (INTC) - A company that has been developing hardware specifically for AI, including custom processors and FPGA chips.

9. Twilio Inc. (TWLO) - A company that provides cloud-based communication services and has been investing in AI technologies to improve its services.

10. Advanced Micro Devices, Inc. (AMD) - A company that develops CPUs and GPUs for AI applications and has been investing heavily in machine learning and other AI technologies.

This is very impressive. ChatGPT not only gives me a list of the companies, but also highlights each company’s involvement in the AI field.

Since ChatGPT doesn’t have data beyond 2021, we come back to our trusty TradingView to pull out 1-year return charts. What a brutal year! Only Microsoft manages to gain 5.3%. The rest in the list had negative returns from -10% to 40%. Twilio is the loss leader, yielding -66.8% in the last 12 months.

This drives home the two major risks in new technology investing:

Firstly, at an early stage, you have no idea which technology will win out at the end. Is it direct current (DC) or alternative current (AC)? Airship or Aircraft? VHS or Betamax? Cable TV or satellite TV? And TDMA or GSM for cellular signal?

Secondly, you do not know which company will become a leader in a winner-take-all market. If you go back in time and invest in the new automobile industry in 1908, you have a 99% chance of losing money, unless you luckily picked Ford, General Motors, or Chrysler out of the 253 publicly traded automakers.

Likewise, if you invested in mobile phone companies in early 2000, you likely picked Motorola, Blackberry, Ericsson, or Nokia. However, when an outsider Apple launch a breakthrough product, iPhone 1 in 2007, it knocked out all leading cellphone markers and became the ultimate winner. Right now, I predict that most electric vehicle makers will go out of business in five years, except for Tesla, and maybe BYD.

The Case for S&P Technology Select Sector Index

Consistently picking winners in emerging technologies is extremely difficult. Even the smartest stock picker could not beat the market. Take Cathy Wood’s Ark Innovation ETF (ARKK) as an example, its cumulative returns comparing to the Nasdaq 100 were:

• 1-year: -42.8% vs. -12.4%;

• 5-year: -2.1% vs. +85.1%;

• Since Inception (8-year): +100.3% vs. +203.5%.

Diversification is a very powerful concept in investing, notably in times of uncertainty. Concentrating on stock picking, many active managers tend to cloud objective assessment with their own conviction and lose sight of potential market leaders amid emerging mega trends. Passive investment via index futures focusing on the high-tech sector allows us to express our conviction and capture emerging trends.

XAK is one of the 11 sector indexes in the S&P 500. Its top holdings are Apple (AAPL), Microsoft (MSFT), Nvidia (NVDA), Visa (V), Mastercard (MA), Broadcom (AVGO), Cisco (CSCO), and Adobe (ADBE).

My research shows that S&P Technology Select Sector (XAK) outperformed many Big Tech stocks and ETFs in both short-term and long-term. According to Fact Sheet published by S&P, as of January 31st, the annualized historical returns are -15.22% (1Y), 13.82% (3Y), 16.22% (5Y) and 18.48% (10Y). Total returns since inception are 6,425.9%.

You may invest in one of the technology sector ETFs, such as SPDR XLK, iShare IYW, and Vanguard VGT. But CME E-Mini S&P Technology Select Sector Index Futures (XAK) has distinguished features over ETFs.

Firstly, XAK has five quarterly contracts to choose from: March, June, September, December and March 2024. This allows us to evaluate strategies focusing on expected future value of the index, up to 1 year ahead.

Secondly, you could place either Long or Short position, allowing both bullish and bearish strategies to implement.

Thirdly, initial margin of placing 1 contract is approximately 35% of the notional value. This built-in leverage could enhance the returns if market moves in the right direction.

Finally, by holding a long position on the quarterly futures contract and rolling it each quarter, investors could replicate the strategy of holding the stocks or the ETFs.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trade set-ups and express my market views. If you have futures in your trading portfolio, check out on CME Group data plans in TradingView that suit your trading needs www.tradingview.com

Tech sector below Cosmic Gravity supportE-mini technology sector futures price recently broke below Cosmic Gravity "Support Channel"(😎) and failing to break back above this level dropped back down (🧐). A next possible long entry position is now at "S6 Line".