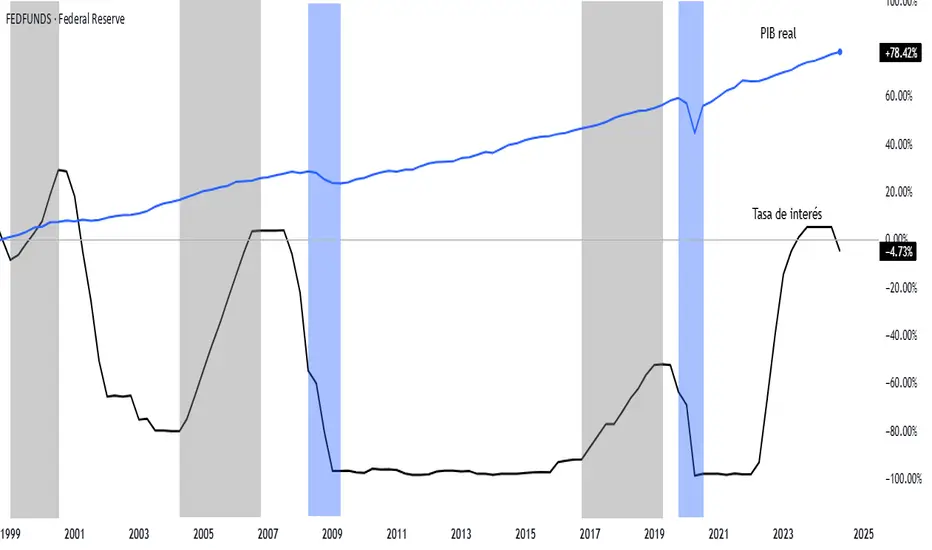

Real GDP vs FED FUNDS RATEReal GDP and the Federal Funds Rate are closely intertwined in the context of economic policy and performance. The Federal Funds Rate, set by the Federal Reserve, is a key tool used to influence economic activity. When the Fed raises the Federal Funds Rate, borrowing costs increase for consumers and businesses, which can slow down spending, investment, and overall economic growth, potentially leading to a moderation in Real GDP growth. Conversely, when the Fed lowers the Federal Funds Rate, it aims to stimulate the economy by making borrowing cheaper, encouraging spending and investment, which can boost Real GDP growth. However, this relationship is not always straightforward, as other factors like inflation, global economic conditions, and fiscal policy also play significant roles. For instance, during periods of economic recovery, low rates may support GDP growth, but if inflation rises too quickly, the Fed may raise rates to cool the economy, even if it risks slowing Real GDP expansion. Thus, the interplay between Real GDP and the Federal Funds Rate reflects the delicate balance the Fed seeks to maintain between fostering growth and controlling inflation.

GDPC1 trade ideas

US Debt Exploding Relative To Real GDPUS debt has risen more than 90% since 2016, with no meaningful increase in economic growth inflation-adjusted (Real terms) meaning we pay more for goods and services showing a higher nominal GDP.

As you can see in the chart the economy used to grow faster than debt and even outpaced debt in 70s, 80s and 90's.

As I have shown before on tradingview, The annual US Gov't spending as a percentage of annual GDP is now 45% and it has been even higher.

My question to you is this. next recession when Real GDP falls and politicians tell you we have to increase deficits and spending to "stimulate" the economy. How much higher will the debt go relative to real GDP?

Reduce risk in portfolios without hampering returns Asset allocation is ultimately about balancing returns with risks. While it is relatively easy to reduce risk in a portfolio, it is harder to do so without diminishing its return potential. Diversification, that is, adding uncorrelated assets to the portfolio, is one of the main tools available to investors to lower such risk, but it often comes at the cost of returns. The 60/40 portfolio, a mix between 60% equities and 40% fixed income, is the bedrock of asset allocation for many investors.

Adding fixed income to equities does lower volatility and improve the Sharpe ratio, in line with Markowitz’s findings in this Nobel Prize-winning work and due to the historically negative correlation between equities and investment-grade fixed income. However, it is also true that a 60/40 portfolio has tended to deliver lower returns than a 100% equity portfolio.

Does it mean that investors have to choose between higher returns with increased volatility or lower returns with decreased volatility?

Cliff Asness’ thought experiment: the levered 60/40

As with any problem, the solutions usually require out-of-the-box thinking. In our case, it requires to start thinking about leverage. Cliff Asness, co-founder of AQR Capital, provided such a solution in December 1996 when serving as Goldman Sachs Asset Management’s director of quantitative research with his paper ‘Why Not 100% Equities: A Diversified Portfolio Provides More Expected Return per Unit of Risk’.

In his paper, Asness argues that investors can achieve competitive returns while managing risk more effectively by diversifying their portfolios with a combination of equities and bonds and using leverage. Asness designs the ‘Levered 60/40’ portfolio which leverages a 60/40 portfolio so that the volatility of the leveraged portfolio is equal to those of equities. The applied leverage is, therefore 155%. The borrowing rate used for leveraging his 60/40 portfolio is proxied by the one-month t-bill rate.

In his original paper, Asness finds that, over the period 1926 to 1993, the Levered 60/40 portfolio returns 11.1% on average per year with 20% volatility. Equities, in contrast, return only 10.3% with the same volatility. For reference, the 60/40 portfolio (unleveraged) returns 8.9% with 12.9% volatility.

We extended the Asness analysis to the most recent period. We observe that over this longer period, the results still hold true. The Levered 60/40 delivers higher returns than equities with similar volatility. The Sharpe ratio of the Levered 60/40 benefits from the diversification and is improved, compared to equities, with no cost to returns themselves.

Leveraging the 60/40 around the world, a successful extension

In Figure 2, we extend the analyses to other regions to test the robustness of such results. While the history is not as deep, Figure 2 shows similar results. Across all the tested regions, the returns and Sharpe ratio of the Levered 60/40 portfolio exceeds those of the equities alone. At the same time, the volatility is identical, and the max drawdown is reduced.

Note that we do not use a 155% leverage in all those analyses; we use the relevant leverage to match the volatility of the equities in the region. Having said that, the leverage remains very similar across regions as it oscillates between 160% for global equities and 170% for Japanese equities.

The theory behind the Levered 60/40

From a theoretical point of view, the idea of focusing on the most efficient portfolio possible and leveraging it to create the most suited investment for a given investor is well anchored in financial theory. When he introduced the Modern Portfolio Theory (MPT) in 1952, Harry Markowitz had already outlined the concept through the Capital Allocation Line (Markowitz, March 1952).

The efficient frontier for a mix of 2 assets: US equities and US high investment-grade bonds. Note that each portfolio on the efficient frontier is the most efficient for a given level of volatility, assuming no leverage. All portfolios on the efficient frontier are not equal and have, in fact, different Sharpe ratios. Along this efficient frontier, there is a portfolio with the highest Sharpe ratio of all, called the ‘Tangential Portfolio’. This most efficient of all the efficient portfolios happens to be found where the Capital Allocation Line touches the efficient frontier. The Capital Allocation Line is the line that is tangential to the efficient frontier and crosses the Y axis (the 0% volatility axis) at a return level equal to the risk-free rate.

When it comes to building the most efficient portfolio for a given level of volatility, investors have two choices. Without leverage, they can pick the portfolio with the highest return for that volatility level on the efficient frontier. If investors look for strategies with a volatility level equal to equities, equities are the most efficient portfolio. Considering potential leverage, the answer is quite different. With leverage, an investor can pick the portfolio with the relevant volatility level (in this case, the equity volatility) on the Capital Allocation Line. Portfolios on this line happen to have a Sharpe ratio equal to the Sharpe ratio of the Tangential portfolio (that is, the best Sharpe ratio of all the portfolio combinations without leverage) but with any level of volatility that may be required. We called the Leveraged Tangency Portfolio the portfolio on the Capital Allocation Line with the same volatility as the equity portfolio. This portfolio is a ‘more efficient portfolio’. The return is improved by almost 2% for the same volatility, leading the Sharpe ratio to jump from 0.27 to 0.45.

Key Takeaways

“Diversification is the only free lunch in Finance”, whether a real or fake H. Markowitz’s quote, epitomises the philosophy that underpins the 60/40 portfolio. It is also one of the main lessons from Markowitz's Nobel prize-winning work. Having said that, the second lesson has not been heeded as well: leveraging a good portfolio can make an even better portfolio. Overall, by leveraging a traditional 60/40 portfolio, an idea that, at WisdomTree, we call ‘Efficient Core’, investors could potentially receive a similar level of volatility present in a portfolio 100% allocated to equities but with the better Sharpe ratio of a 60/40 portfolio.

Possible examples of where such Efficient Core portfolios may be used widely in multi-asset portfolios include:

An equity replacement

A core equity solution designed to replace existing core equity exposures. By offering return enhancement, improved risk management and diversification potential compared to a 100% equity portfolio, Efficient Core can also be used to complement existing equity exposures.

A capital efficiency tool

By delivering equity and bond exposure in a capital-efficient manner, Efficient Core can help free up space in the portfolio for alternatives and diversifiers. In line with the illustrations above, allocating 10% of a portfolio to this idea, investors would aim to get 9% exposure to US equities and 6% exposure to US Treasuries. This could allow investors to divest 6% from existing fixed income exposures and consider alternative assets (such as broad commodities, gold, carbon or other assets). In this scenario it could potentially be achieved without losing the diversifying benefits of their fixed income exposure.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

GDP is Bad and You Should Feel BadThe GDP number of 2.7% growth is being propped up by net exports, while consumption is at a cycle low. This is horrible for earnings expectations and risk assets. Net exports were at a low in prior quarters, making the economy look worse off than it was. Now the economy is actually worse off than it is and the metric is instead making it look better. This is why the NBER doesn't use "two quarters of negative GDP" to date recessions. There are too many false signals.

Don't fall for the GDP meme. The pain is coming.