TSLA Short Setup – Fading the July 7 Gap FillTSLA Short Setup – Fading the July 7 Gap Fill 📉

This short idea on TSLA builds off a key gap fill from Monday, July 7 , combined with a strong local volume profile and risk-reward alignment on the 15-minute chart.

Entry: $312.76

Stop Loss: $314.81 (above gap resistance and local high)

Target: $299.89 (gap base and volume shelf)

RR: ~6.3R

Why I'm shorting here:

TSLA has just filled the July 7 gap , which often acts as a technical resistance zone on retest.

Price stalled right as it completed the fill — with visible hesitation and selling pressure stepping in.

VRVP shows low liquidity above, suggesting diminished reward for upside continuation.

Below, there's a clean volume shelf around $294–$300 that could attract price if weakness confirms.

Trade Logic:

This is a classic fade-the-gap-fill setup, targeting the lower edge of the volume cluster for a potential bounce or reversal zone.

As always: size accordingly, stick to the stop, and don’t chase if the entry’s already gone.

Thoughts? Anyone else watching this gap level?

TL0 trade ideas

TSLA, Long, 1D✅ TSLA has just broken out of a clear symmetrical triangle pattern, signaling a potential bullish continuation.

Yesterday’s daily candle was a white Marubozu, indicating strong buying pressure and clear dominance by the bulls.

LONG 📈

✅ Like and subscribe to never miss a new technical analysis! ✅

TSLA eyes on $294: Key Support for bulls to hold or face $253TSLA oscillating all over the place thanks to Musk moves.

Currently testing a key support zone $293.96-294.32.

Loss of this floor opens the Golden Genesis at $253.57

See "Related Publications" for previous charts ------------>>>>>>

Tesla (TSLA) 1-hour chartTesla (TSLA) 1-hour chart im provided, here are the key bullish target points indicated by the chart analysis:

📈 Bullish Target Points (Upside Levels):

First Target Point:

🔹 Around $338.00 – $340.00

This level is marked as the initial breakout target, likely based on recent price structure and resistance zone.

Second Target Point (Extended Target):

🔹 Around $362.00 – $364.00

This is the higher target zone, representing a potential move if bullish momentum continues strongly. Likely aligning with a measured move or previous highs.

🧠 Context:

Price has broken out of a descending triangle/wedge pattern, a bullish signal.

It's also moving above the Ichimoku cloud, showing short-term bullish trend continuation.

Holding above the breakout level (around $305–$308) is critical to maintain upward momentum.

Triangle Pattern in TSLALooking at 4H-1D Chart, there is a triangle pattern emerging which may target 400 area. Good luck.

Tesla Flashes Bullish Reversal: Engulfing Candle and Volume PoinLet’s reassess TSLA now that we have this new candle (a big move +4.73%) in context. This changes things substantially, so I’ll reapply candlestick techniques, assess trend health, box positioning, and momentum.

Candlestick Analysis

The new candle:

Large white body (+4.7%) closing at $309.87. Engulfing prior 2 candles’ real bodies → this is a Bullish Engulfing Pattern. Occurs near the 50% retracement ($290) zone (previous support). Volume expanded vs prior days → adds validity. Bullish engulfing after a down leg is an early reversal signal.

Context:

This happens after weeks of indecision candles (spinning tops / dojis) → classic “coiling” behavior before expansion.

Trend Health & Momentum

MACD: Still below zero but histogram bars turning less negative → momentum starting to shift.

RSI: Up to ~47.6, breaking out of its down channel. A move >50 would confirm momentum pivot.

Box Dynamics

TSLA just punched through the upper edge of Box 2 ($300) with conviction.

Now entering “no man’s land” between Box 2 ($300–$360) and Box 1 ($360–$465).

For a sustained breakout it must close above $306–310 range for 2-3 days. Ideally see follow-through with a test of $328 (78.6% Fib).

Tactical Breakdown

✅ Breakout case (higher probability now):

Bullish Engulfing + volume expansion at support zone.

Closing above $306-310 increases odds of a run toward $328 (78.6%) and possibly $360.

❌ Reversal back down (lower probability):

Only if TSLA immediately rejects $310 and falls back below $300 in the next 1–2 sessions.

This price action looks like accumulation showing its hand. Large white candle suggests buyers absorbing supply at prior resistance.

Breakout above $306 confirmed if follow-through continues. Odds for a reversal lower just dropped sharply after today’s engulfing.

TSLA racing to break thru resistancearea 1: 340

area 2: 360

will be tuned into earnings to see if the jig is jiggin July 23rd.

Elon is busy. so let's see what's the dealio.

****280 is a key level

**300 needs to hold for these attempts

Why TSLA will Crash based On Copper TarrifsHere’s why that bearish outlook is gaining traction:

Copper costs are surging: Tesla uses over 180 pounds of copper per vehicle. With prices spiking 13% in a single day and a 50% tariff looming, production costs are rising fast.

Analysts are cutting price targets: UBS, JPMorgan, and Bank of America have all lowered their forecasts for Tesla, citing margin pressure and weakening demand3.

Brand sentiment is shaky: Tesla’s recent delivery miss and political controversies around Elon Musk have added to investor unease.

Tariff ripple effects: The broader trade war is expected to disrupt supply chains and inflate costs across the EV sector5.

That said, some analysts still see long-term upside if Tesla can pivot quickly—especially with its AI and autonomous driving ambitions. But for now, the market is reacting to the immediate risks.

Overall Enter Short for Gains of 3-5 percent.

Tesla (TSLA) Market UpdateTesla NASDAQ:TSLA shares dropped nearly 7% after Elon Musk dismissed analyst Dan Ives' suggestion to scale back his political activities. Musk also proposed a new pay package, raising concerns among investors about potential distractions from Tesla’s core business.

📊 Upcoming Catalyst:

Tesla is set to report its Q2 earnings on July 23, with investors eagerly awaiting updates on the company’s financial performance and the newly launched robo-taxi service in Austin, Texas.

⚠️ Sentiment:

Recent bearish headlines include:

Concerns over potential Robotaxi issues

The ongoing Trump/Elon Musk political drama

📈 Trading Opportunity (Long Setup):

Despite the negative sentiment, this dip could offer a solid long entry opportunity:

Entry Zone: $275–$270

Take Profit Targets:

TP1: $315

TP2: $335

Stop Loss: Close below $265

TSLA Long Idea — Buying the Support After News-Driven DipNASDAQ:TSLA price has stabilized near the key $290–291 support zone, a level that has previously triggered rebounds. This presents a solid entry opportunity with limited downside risk.

Context: The recent drop was triggered by headlines involving the U.S. President and Elon Musk. If this was mainly speculative noise, now could be the best time to buy, as the market absorbs the news and finds technical support.

Technical Setup:

• Strong support at $290–291 holding firm.

• Stochastic is in the oversold zone and starting to turn upward.

• Bollinger Bands tightening — breakout likely.

• Target: $307.45 (+4.57%)

• Stop-loss: $289.09 (−1.68%)

• Risk/Reward Ratio: 2.72

Expected move by July 9, 2025. With strong technical signals and fading news impact, this setup offers a favorable risk/reward for bulls looking to ride a rebound.

Long TESLATrading Fam,

Today my indicator has signaled a BUY on $TSLA. The technicals align. M pattern looks to have completed at strong support (RED TL) and is bouncing upwards inside of a solid liquidity block. Buyers are stepping in. I'm in at $315 and will shoot for $430 (probably taking some profit along the way). My SL is currently $241 but will trail as we enter profit.

Best,

Stew

TESLA (TSLA) ARE WE HEADING TO 336? Morning Folks

It appears we are trying to break the highs of 304 and if we are successful a nice range up to 327-336 makes sense. However be careful if sink back down under 289 which then can see levels of 259 getting hit.

What are your thoughts on Tesla? Put in the comments section below

Kris Mindbloome Exchange

Trade Smarter Live Better

TSLA: Buy ideaBuy idea on TSLA as you can see on the chart after the breakout with force the resistance line by the buyers.

TSLA BUY 253.8Recently, TSLA has maintained a volatile operation. Currently, we can pay attention to the area around 253.8 below, which is a potential buying position for a bullish Gartley pattern. At the same time, this position is within the previous demand area.

TSLA Caught in Tug-of-War-TA for July 10TSLA Caught in Tug-of-War: Key Gamma & Price Action Setups Unfolding ⚠️

🔍 GEX (Gamma Exposure) Analysis:

Tesla’s options market is highly polarized heading into the week.

* Gamma Walls: Strong Call Wall near $304–$310, showing potential upside magnet if bulls regain control. Above this, the $317.5–$320 zone could trigger a gamma squeeze.

* Put Walls: The $288–$285 zone represents a heavily defended downside, marked by high negative NET GEX and multiple put walls.

* Current GEX Bias: Negative gamma regime persists, increasing potential for volatile moves and sharp directionality.

* IVX is elevated at 61.1, with IVR 17.4, suggesting the options market is pricing in moderate near-term volatility.

📈 Options Trade Ideas:

* Bullish Setup: Consider July 12/July 19 300c–310c debit spread if price confirms reclaim of $300, targeting a gamma squeeze toward $317.5–$320.

* Bearish Setup: If price breaks below $288, buy 285p–275p vertical or 295p straight puts, expecting continuation toward $280 and below.

🕒 1H Price Action Outlook:

Tesla remains stuck in a tight consolidation wedge, showing a battle between supply at $300–304 and demand near $288–290.

* Structure: Market formed a bullish BOS earlier this week but failed to extend higher. The latest CHoCH + rejection from $300 zone suggests sellers are still active.

* Range: Coiling inside a triangle formation with tightening price action. A breakout or breakdown is imminent.

* Demand Zone: The green liquidity block around $284–$288 has held firm so far.

* Trendlines: Price is being compressed between a descending trendline (supply) and ascending trendline (demand), signaling a make-or-break moment.

🎯 Intraday Trade Plan:

* Bullish Case:

* Entry: Above $300 with volume

* Target: $304 → $310 → $317

* Stop: Below $294

* Bearish Case:

* Entry: Breakdown below $288

* Target: $284 → $280

* Stop: Above $295

💭 Final Thoughts:

TSLA is in a pressure cooker. A breakout above $300 opens the door to gamma-driven upside, but continued compression or a loss of $288 support could trigger a fast liquidation. Monitor volume closely — this wedge is near resolution.

This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk responsibly.

Important Volatility Period: Around August 21

Hello, traders.

If you "Follow", you can always get the latest information quickly.

Have a nice day today.

-------------------------------------

(TSLA 1D chart)

The medium-term trend is maintaining an uptrend.

However, if the price falls below the M-Signal indicator on the 1M chart and maintains, there is a possibility of a downtrend, so caution is required.

The support zone is

1st: 222.15-235.59

2nd: 172.16

Around the 1st and 2nd above.

The 268.07-311.48 zone is an important support and resistance zone.

If the price is maintained above this zone, there is a high possibility that a full-scale upward trend will continue.

However, since a resistance zone is formed in the 347.21-382.40 zone, we need to look at how this zone is broken upward.

-

When it falls to the 172.16-234.59 zone, we need to find a time to buy.

If not, we need to buy when it shows support in the 268.07-311.48 zone.

It would be better to buy at a lower price, but since the investment period will inevitably be longer, I think it is better to buy when an upward trend is detected.

-

The important volatility period is around August 21st, but before that, we need to check the movement around July 25th.

If it falls below 268.07 after August 21st, it could lead to further decline.

If it rises above 311.48 and maintains the price during the movement around July 25th, it could lead to further increase and it seems likely to create a trend after the volatility period around August 21st.

-

Thank you for reading to the end.

I hope you have a successful trade.

--------------------------------------------------

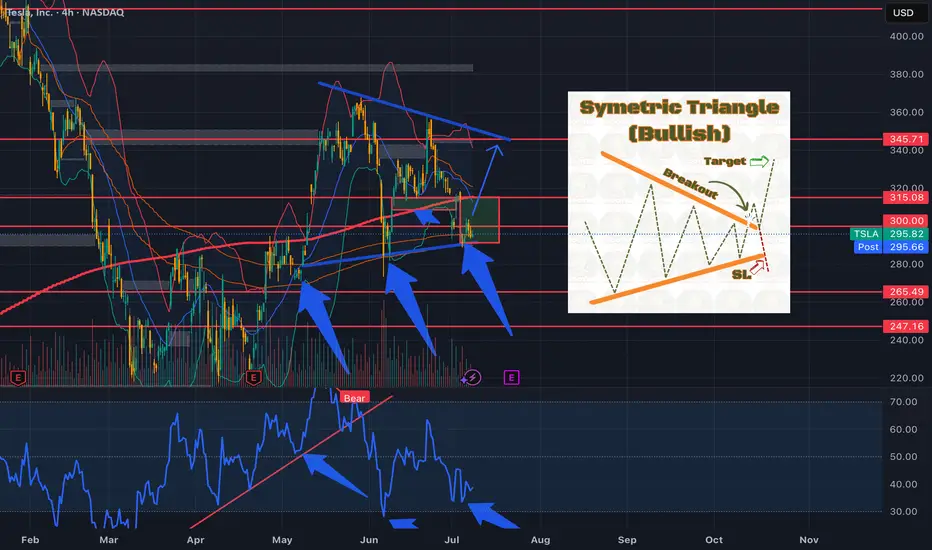

TSLA....Symetric Triangle....Earnings Rally?Could we see the bulls step in and leads us into earnings?

Break of rising trendline TSLA – 4H 🧠

Bias: Bearish

Entry: Below 300.00

🎯 Targets: 273.67 – 253.87

❌ Invalidation: Above 315.01

Break of rising trendline signals bearish momentum. Downside continuation anticipated.

#TSLA #Stocks #NASDAQ #PriceAction #TradingView #piporia

Tsla below 288 ?I see an H&S pattern forming if we break below 288 we could see it drop to 280 ish imo. Can play out this week. Lets see

Tesla Share Price at Key Technical LevelTesla’s share price has returned to a well-established upward trendline. The key question now is: will this trendline act as support and trigger a bounce, or will it be breached, attracting further selling pressure and pushing the price lower?

We’d love to hear your thoughts — will the bulls defend this level, or are the bears gaining ground?

$TSLA: Battleground stock. There’re better way to make money. In this bull market where almost all the stocks are working, NASDAQ:TSLA seems to be still in the penalty box. When NASDAQ:NVDA , NASDAQ:MSFT are at ATH and most of the Mag7 are near to the ATH. NASDAQ:TSLA is still 33% below its ATH of 484 $. And the price action is not particularly bullish. This week NASDAQ:AVGO crossed NASDAQ:TSLA with a larger Market Cap cos. May be NASDAQ:AVGO should replace NASDAQ:TSLA in MAG7. A food for thought.

With such poor price action and the price stuck within the 0.618 and 0.382 Fib retracement levels the stock has not looked bullish recently. IN this recent market reversal all the speculative sectors like Quantum, Space stocks and Drone stocks are working, NASDAQ:TSLA is still searching for direction. In my opinion NASDAQ:TSLA has a great future with a visionary leader, but it might end up being a good company but not a good stock. With controversy surrounding the leadership it has become a battle ground stock. There are many large cap liquid stocks where the positive momentum is working. Until the stock breaks out of this consolidating pattern it’s better to make money somewhere else.

Verdict: Stay on sidelines for NASDAQ:TSLA stock. Accumulate if you need to. Buy it above 400 $ once momentum is back.

TSLA at Critical Compression – Will 300 Break or Reject Again?🔍 Options Sentiment (GEX) Insight:

TSLA is currently sitting just below the $300 call wall — a key resistance level with 71.83% call gamma. This makes $300 a battleground where dealers are likely to defend against upward movement unless there's a significant catalyst or volume thrust. The highest positive call gamma is stacked at $320, making that the next magnet level if $300 is breached with strength.

Below, the $290 level is critical, hosting a major PUT wall and high-volume liquidity (HVL). A break below could trigger acceleration toward $285–$280, where the strongest negative NET GEX exists — signaling potential dealer hedging flows in favor of downside momentum.

Options Trade Ideas:

* Bullish Scenario (Breakout):

* Buy CALL if TSLA breaks and holds above $300, targeting the $310–$317.5 range.

* Ideal setup: Use 310c or 315c, 1–2 weeks out, looking for gamma squeeze.

* Bearish Scenario (Breakdown):

* Buy PUT if TSLA breaks and holds below $290, targeting $285 → $280.

* Ideal contracts: 280p or 285p, especially if IV remains low (IVR is at 21.3).

* Be cautious of chop inside the $290–$300 zone — it's gamma neutral.

📈 1-Hour Technical Structure:

TSLA is trading inside a descending wedge with a bullish CHoCH (Change of Character) confirming near the lower boundary of the wedge. There is a visible bullish OB (order block) between $288–$290, which acted as support in the last two sessions.

* Trendline Resistance from recent highs still caps upward movement unless $300 is reclaimed decisively.

* A strong bullish breakout above $300 could flip the structure fully bullish and initiate trend continuation toward $320.

* Failure to hold $290 could invalidate the CHoCH and confirm a BOS (Break of Structure) back to the downside.

Intraday Trade Scenarios:

* Scalp Long:

* Entry: $297.50 (if holds and reclaims above $300)

* Target: $307 / $310

* Stop: $293.94 (below last swing)

* Scalp Short:

* Entry: Break below $288.77

* Target: $285 → $280

* Stop: $293.94

Final Thoughts:

TSLA is consolidating near a major decision zone. $300 remains the trigger level for a directional move, and option flows suggest an explosive resolution if either side breaks. Stay nimble, wait for confirmation, and trade with clear invalidation in mind.

This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk appropriately.