GBPNZD: Forecast & Trading Plan

The price of GBPNZD will most likely collapse soon enough, due to the supply beginning to exceed demand which we can see by looking at the chart of the pair.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

❤️ Please, support our work with like & comment! ❤️

GBPNZD trade ideas

GBPNZD Bullish Triangle Breakout,with bullish pennant set upThe GBPNZD 2H chart illustrates a bullish pennant formation following a strong upward move. Price is consolidating within the triangle and is expected to break upward, continuing the bullish trend. A breakout above the triangle suggests a potential rally toward the 2.30086 target, with 2.25443 acting as the stop loss level for risk management.

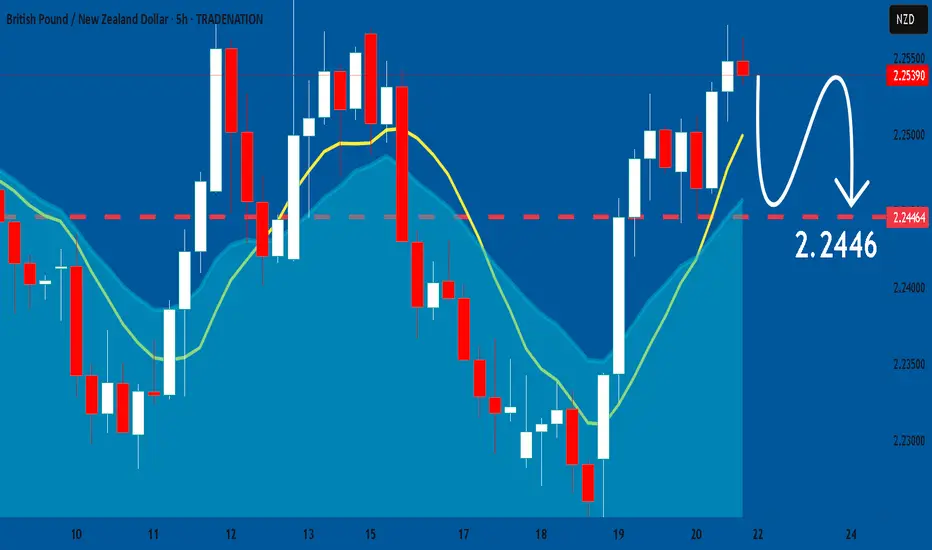

GBPNZD: Potential Reversal From The Resistance ZoneGBPNZD: Potential Reversal From The Resistance Zone

GBPNZD tested an area that was also tested earlier at the beginning of March 2025

From the chart, we can see that this zone has stopped the price several times on the past.

The chances are that GBPNZD may start a bearish wave from the same zone again despite that the market has frozen for all instruments lately.

The Geopolitical situation looks more stable, which can help all currencies regain direction.

NZD is already oversold too much so it can take advantage of this moment.

Key target areas: 2.2500; 2.2380 and 2.2280

You may find more details in the chart!

Thank you and Good Luck!

❤️PS: Please support with a like or comment if you find this analysis useful for your trading day❤️

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

GBPNZD Buy✅ 1. Inverse Head and Shoulders Pattern:

You have a well-defined Left Shoulder → Head → Right Shoulder structure. This is a classic bullish reversal pattern indicating the end of the downtrend and suggesting that price is now more likely to move upwards.

✅ 2. Trendline Support:

The price is following and respecting an ascending trendline, confirming that bullish momentum is gaining strength. This trendline gives you a defined area of support and a low-risk entry point.

✅ 3. Break and Retest:

The price appears to have broken a key resistance level (now acting as support), making the entry more favorable for a long position.

✅ 4. Strong Momentum:

The chart confirms a shift from lower highs and lower lows to higher highs and higher lows (a trend reversal), aligning with a long position.

✅ 5. Clear Risk Management:

With the entry, stop loss, and 50% take-profit point clearly marked, you have defined risk/reward, making this a disciplined and structured trade.

Long GNGN has rejected the recent value area high. From the candlestick, project that price will reach to the recent high level.

GBPNZD BUY IDEAAccording to the Daily Chart, we're currently in an uptrend. Price broke a major resistance level, 2.25511, yesterday and continued without a retest. I'm looking at a retest of the broken resistance for continued buys.

GBP-NZD Long From Demand Ahead! Buy!

Hello,Traders!

GBP-NZD is making a bearish

Correction but will soon

Retest a wide demand area

Around 2.2539 from where

We will be expecting a

Local rebound a move up

Buy!

Comment and subscribe to help us grow!

Check out other forecasts below too!

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

GBPNZDprice is reaching main support/OB area, price will likely reverse either HH or just for downtrend correction because price is still downtrend.. all htf showing reversal on bearish side but price is still in uptrend on htf so this is just idea for correction... use proper risk

GBPNZD BUY BIAS • Supply Zone (Red Box):

Price tapped into a clearly defined supply area around 2.27000–2.27474, indicating potential for bearish reversal.

• Rejection Candles:

Bearish rejection formed at the top of the zone with clear upper wicks, suggesting selling pressure.

• 200 EMA (Curved Line):

Price rallied into the supply from below the EMA, increasing the probability of a mean reversion move.

• Risk/Reward Box:

A short trade is shown with:

• Entry: Just under 2.27000

• Stop Loss: -2.27474

• Target: 2.22349, aligning with previous structure and EMA

2024/06/23 - GBPNZD - Golden swingDaily Horizontal SR Daily Diagonal SR Golden Swing

Divergence on m30

Gbpnzd Bullish Trading Idea

GBPNZD is following a strong Bullish Channel — the pair has been consistently making Higher Highs (HH) and Higher Lows (HL).

Currently, the price is around 2.2210, showing bullish momentum. We're expecting the next Higher High to reach 2.3249+.

🚨 Watch for a breakout and hold above 2.221 for potential long entry!

💰 Great opportunity for swing traders & intraday scalpers!

GBPNZD: Market Sentiment & Forecast

Looking at the chart of GBPNZD right now we are seeing some interesting price action on the lower timeframes. Thus a local move down seems to be quite likely.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

❤️ Please, support our work with like & comment! ❤️

Potential Bullish Shark Pattern on #GBPNZDI have just spotted a potential bullish shark pattern on GBPNZD., We have gotten a structure shift on H1.

As usual, I will discuss more on this analysis with a video and attach the link as a comment to this write-up.

GBPNZD BUY OR SELL IDEAHope y'all caught the 300 pips buy move last week. Mehn, that was fast. Well, price is a major resistance and is currently retracing. The question is whether price action is retracing for a further move upwards or a fall back to the support level at 2.2233?

The chart pattern is showing a falling wedge. A break of resistance 2.25 and retest would be confirmation for an entry for buys, or a break of the 61.8 & 50 fib zone/formation of lower highs and lower lows would be confirmation for a sell entry. The market always gives a signal, so we watch once the market opens

GBPNZD: Partials Secured on Sell – Watching PRC for LongCaught the move off the descending trendline and 1H supply zone on GBPNZD. Original TP was set for 3R, but I took early partials around +60 pips to lock in some profit and reduce risk. SL was moved to breakeven — price retraced and took me out risk-free.

Now watching the PRC level (previous resistance turned support) for a trend continuation buy setup. Waiting for confirmation before entering long again.

Approach: Trend-based setup with key zones

Tools: EMA 9/20/50, PRC Zones, Trendlines

Style: Risk-managed swing entry with partial profits

Timeframe: 1H

GBP_NZD RISKY SHORT|

✅GBP_NZD is going up now

But a strong resistance level is ahead at 2.2591

Thus I am expecting a pullback

And a move down towards the target of 2.2524

SHORT🔥

✅Like and subscribe to never miss a new idea!✅

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

GBPNZD BEARISH SETUPGBPNZD is bearish setup.

Take entry with instant.

After take profit 1 hit then trade breakeven.

GBP-NZD Will Go Down! Sell!

Hello,Traders!

GBP-NZD will soon hit

A horizontal resistance

Of 2.2556 and as its a

Strong key level we will

Be expecting a local

Pullback and a move down

Sell!

Comment and subscribe to help us grow!

Check out other forecasts below too!

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

GBP/NZD – Sell Now from Daily Trendline Rejection + 1H Supply ZoGBP/NZD is a sell now as price reacts sharply to a confluence of technical resistance:

• Daily descending trendline rejection

• Clean touch of a key supply zone around 2.2520

• 1H shows signs of exhaustion and rejection with wicks and slowing momentum

• EMAs are flattening on lower timeframes, hinting at a potential shift

This setup offers high-probability short entries with clear structure to target.

🔻 Sell Now

🎯 TP1: 2.2410 (local support)

🎯 TP2: 2.2330 (liquidity zone)

🛑 SL: Above 2.2550 (trendline break invalidates)

Watch for 1H bearish continuation patterns. A clean daily close above 2.2550 invalidates this setup.

GBPNZD Sellers In Panic! BUY!

My dear subscribers,

My technical analysis for GBPNZD is below:

The price is coiling around a solid key level - 2.2314

Bias - Bullish

Technical Indicators: Pivot Points Lowanticipates a potential price reversal.

Super trend shows a clear buy, giving a perfect indicators' convergence.

Goal - 2.2402

About Used Indicators:

By the very nature of the supertrend indicator, it offers firm support and resistance levels for traders to enter and exit trades. Additionally, it also provides signals for setting stop losses

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

———————————

WISH YOU ALL LUCK

GBPNZD BUY IDEAPrice is currently at a major support area, which hasn't been broken since March. Examining the area for signals for the beginning of an uptrend.

GBPNZD: Will Keep Growing! Here is Why:

Our strategy, polished by years of trial and error has helped us identify what seems to be a great trading opportunity and we are here to share it with you as the time is ripe for us to buy GBPNZD.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

❤️ Please, support our work with like & comment! ❤️

GBPNZD - Looking To Sell Pullbacks In The Short TermH1 - Strong bearish move.

No opposite signs.

Currently it looks like a pullback is happening.

Expecting bearish continuation until the two Fibonacci resistance zones hold.

If you enjoy this idea, don’t forget to LIKE 👍, FOLLOW ✅, SHARE 🙌, and COMMENT ✍! Drop your thoughts and charts below to keep the discussion going. Your support helps keep this content free and reach more people! 🚀

--------------------------------------------------------------------------------------------------------------------