BMC1! trade ideas

Price Gap Examples - Bitcoin FuturesSharing for educational purposes only.

█ Three Types of Gaps

There are three general types of gaps:

Breakaway Gap

Runaway (or Measuring) Gap

Exhaustion Gap

█ 1 — The Breakaway Gap

The breakaway gap usually occurs:

At the completion of an important price pattern.

At the beginning of a significant market move

Examples:

After a market completes a major basing pattern, the breaking of resistance often involves a breakaway gap.

Breaking major trendlines signaling a reversal of trend may also involve this type of gap

Key Characteristics:

Heavy volume often accompanies breakaway gaps.

They are typically not filled (or only partially filled).

In an uptrend, upside gaps act as support areas on subsequent corrections.

A close below the gap is a sign of weakness.

█ 2 — The Runaway or Measuring Gap

The runaway gap forms:

Midway through a trend (uptrend or downtrend).

Indicates the market is moving effortlessly, usually on moderate volume.

Key Characteristics:

In an uptrend, it signals strength.

In a downtrend, it signals weakness.

Acts as support or resistance during subsequent corrections.

Why "Measuring" Gap?

It often occurs at the halfway point of a trend.

By measuring the distance the trend has already traveled, the probable extent of the remaining move can be estimated by doubling the amount already achieved.

█ 3 — The Exhaustion Gap

The exhaustion gap appears:

Near the end of a market move.

Key Characteristics:

Occurs after objectives have been achieved and other gap types (breakaway and runaway) have been identified.

In an uptrend, prices leap forward in a final push but quickly fade.

Within a couple of days or a week, prices turn lower.

█ Conclusion

By understanding the types of gaps and their characteristics, traders can better interpret market signals and anticipate potential trends or reversals.

█ Source:

Murphy, John J. Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance, 1999. Chapter 4, "Price Gaps," pp. 94-98.

$BTC Top Target, $2M by February 2026Using my scandinavian quant I have come to the mathematical conclusion that this chart shows the exact top by time and price.

good luck and have fun fellow comrades

dynamic support buying areaas we can see the overall trend is an uptrend, with buyers in control. The market has reached our support where it might buy, to enter this trade it's best to wait for a breakout above the dynamic support(blue lines) then enter using H1(bullish candlestick confirmation)

Chart Pattern Analysis Of Bitcoin.

K1 and K2 is a bearish harami pattern,

But unfortunately, K3 close upon K2 immediately.

Perhaps it is a valid break up, after all it is a bull market.

And K4 will keep climbing up to test 115-128K area.

On the other hand,

It is also possible that a large scale consolidation started from K1 earlier,

And K3 is just a fake up candle.

If that is a fact,

K4 will likely fall to test 90-95K area.

It will be a good place to buy then.

BTC CME Regression Trend Re-visiting an old chart, I put in a regression trend channel on March 11 2024, before the halving. BTC has just come back to the bottom part of that channel. Should retest bottom, then middle, another test, then test the top , in theory. nothing about the next 6 months is known. watch the liquidity cycle. Gonna get crazy, be safe, hardware wallets everyone!

Where from here? my thoughts are $225K, but..., ladder out at fibs, the 61.8's

Bitcoin’s Shooting Star: RSI Divergence Sparks CautionWe’re seeing a potential shooting star pattern forming on Bitcoin’s daily chart, combined with RSI divergence. Despite BTC hitting a new high, the RSI hasn’t confirmed it, hinting at fading upside momentum. While these signals are concerning, I’m waiting on further confirmation. Ideally, a bearish candle should follow the shooting star—something we don’t have yet. A break and close below the 20-day moving average near 93,823 should be enough to trigger a deeper correction. Until that happens, extreme caution is advised.

Disclaimer:

The information posted on Trading View is for informative purposes and is not intended to constitute advice in any form, including but not limited to investment, accounting, tax, legal or regulatory advice. The information therefore has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient. Opinions expressed are our current opinions as of the date appearing on Trading View only. All illustrations, forecasts or hypothetical data are for illustrative purposes only. The Society of Technical Analysts Ltd does not make representation that the information provided is appropriate for use in all jurisdictions or by all Investors or other potential Investors. Parties are therefore responsible for compliance with applicable local laws and regulations. The Society of Technical Analysts will not be held liable for any loss or damage resulting directly or indirectly from the use of any information on this site.

The Top is In. Bitcoin, while revolutionary in its inception, faces significant hurdles that challenge its viability as a practical medium of exchange. The cornerstone of this argument lies in the inherent limitations of its transaction processing speed. The Bitcoin network's distributed ledger requires approximately 10 minutes to compute and record each transaction, rendering it impractical for everyday commerce.

This prolonged confirmation time poses a substantial obstacle to Bitcoin's adoption in real-world transactions. In an era where instant gratification is the norm, waiting 10 minutes or more for a simple purchase is not only inconvenient but also commercially unviable. This fundamental flaw undermines Bitcoin's utility as a currency for daily transactions.

Furthermore, if Bitcoin cannot function effectively as a means of exchange, one must question its true value proposition. The current fervor surrounding Bitcoin may be likened to a speculative mania, divorced from practical utility. Historical patterns suggest that such manias often follow Fibonacci ratios in their price movements. We may be witnessing the culmination of a third wave increase, potentially followed by a significant correction.

This correction could see Bitcoin's value plummet to $50,000 or even lower. While it's premature to predict Bitcoin's demise, its current trajectory raises serious concerns about its long-term sustainability as both a currency and an investment vehicle.

In conclusion, the 10-minute transaction confirmation time is not merely an inconvenience; it's a critical flaw that undermines Bitcoin's fundamental purpose. This limitation, coupled with the speculative nature of its current valuation, casts a shadow over Bitcoin's future prospects in the world of finance and commerce.

Again this is my opinion and my perspective, you should do your own due diligence and think on your own two feet about this.

I did predict Bitcoin at $100 by the way.......

You don't have to believe in BitcoinBut all signs point to it reaching $100k. Saylor still has money to print. He will buy the dip. Sellers will be exhausted.

BEARS are salivtingEveryone should be well into profit taking. It would only make sense that all the new people and attention is prime to be used as exit liquidity. I been in the game since 2017 and i got that feeling again the rug is about to get pulled. Dont get stuck sitting in a bear market for years when you should be taking profits to begin with. Discipline and survive. Dont get greedy or youll be rekt

Possible Buying areasgood day traders, I've decided to share my First analysis on futures and these are the possible buying areas I see, between the dynamic trendline or the major low. It's best to wait for a bullish confirmation between these two areas before entering to increase your probability of winning, don't forget proper risk management

CME Bitcoin futures chart look bearishCME #btc #bitcoin futures price has made bearish double top and distribution seems has just started. Bearish continuation may be expected, beware.

Bitcoin tends to falter the day after ThanksgivingThe 124k target remains in play overall, but for now I suspect the shakeout from its 100k milestone has more to offer bears. And while bitcoin prices are showing a nice breakout from a flag pattern on the 1-hour chart, bulls should take note that today (the day after Thanksgiving) tends to be a bearish day on average. And that could make any moves towards 100k tempting for bears to fade into over the near term.

MS

Bear market first two quarters of 2025 expecting BTC to be bearish just a pull back to the monthly order block then skyrocket again looking at price range from 65k-70k

Strong Buy on Micro BTC 15 min timeframe (Futures)Above the 50 and 300 EMA

Entered on a pullback from my indicator

Targeting 200 ticks

~One to two Risk : Reward ratio

Will the CME gap get filled?

BTC is looking for a liquidity void, and the CME gap looks perfect for it, but will it get filled?

i'm still bullish long term

BTC CME Chart - Mind the Gap!Currently there exists a gap of around 3000 USD between roughly 80.000 USD and 77.000 USD. This gap is around 20-22 % from the last top and also marks a zone between two fibonacci lines (0.283 from the last lowest low and the 0.382 line from the low before that).

My educated guess is that we get a relatively 'normal' traceback to that zone. To fill the gap and to build up momentum for another rise in the bitcoin price.

Note that pullbacks of 20 percent are quite normal, although the range in Dollars can get larger and larger as we go higher and higher.

Please like if you share my opinion.

Btc1!/UsdtCME:BTC1!

Simple to understand market going to fill this gap soon i am not moving my Spot position when market give a opportunity then i am going to buy some spot bags...

Disclaimer : Not Financial Advice

BTC Huge Gap!!! We going back to 75k?Hey guys!

Congrats all with BTC ATH and recent profits, I was not commenting the situation, because it was pretty clear, and we all know what was happening.

But also, as we know, even in the bull cycle have to be corrections and consolidations.

So here at the futures chart, we can see a huge gap around the healthy correction possible zone (max to 30%). Also, we have RSI oversold for sure and descending volumes.

Plus, in December there were no promises about decreasing US Interest rate, so possibly December can end up in this correction phase.

What's your thoughts about when and how much we could go? Let's chat in the comments =)

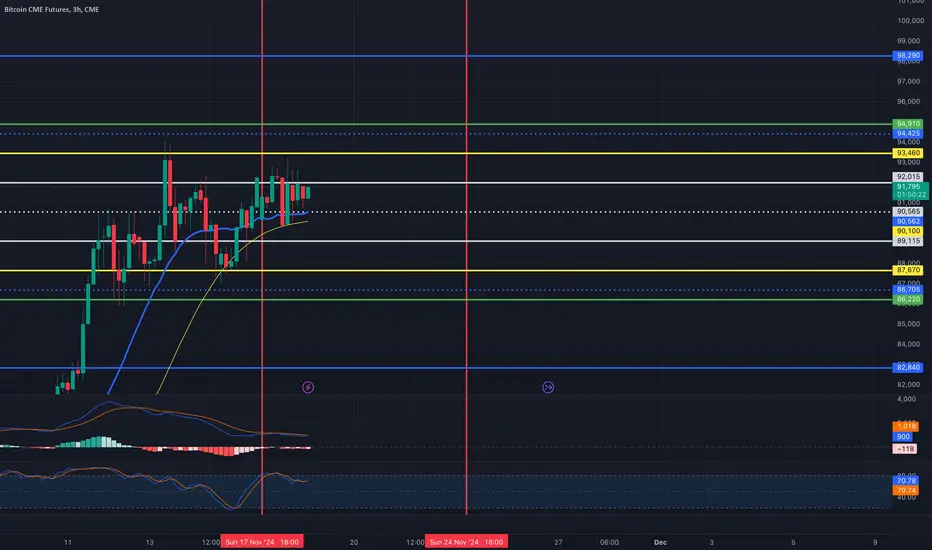

BTC1! WEEK OF 11/18/24BTC1! WEEK OF 11/18/24

To maintain simplicity, once the price moves beyond the WHITE range, monitor for a potential retest of the breached level.

Be prepared to initiate long or short positions targeting the YELLOW ranges.While prices may surpass the YELLOW range targets, these levels provide a robust framework for securing profits. 🎯🫡

*These levels are derived from comprehensive backtesting and research, demonstrating over 90% accuracy. This statistical foundation suggests that price movements are likely to exceed initial estimates.*