Our opinion on the current state of SAPPI(SAP)Sappi (SAP) manufactures paper, dissolving wood pulp (DWP), and paper pulp internationally and supplies products in 150 countries. DWP is used to manufacture clothing, packaging products, and many other applications. DWP, specialty, and packaging products were seen as the profit generator in the future, but until recently, the price of DWP had fallen sharply. Then in 2021, the price of DWP began to rise as demand from China surged. It is directly linked to the level of consumer spending, and it is well-diversified geographically, selling products in 150 countries.

The company said that the civil unrest in July 2021 had cut its profit by R220m. The company has had problems with the backlogs at Durban port and rising energy costs. On 13th April 2022, the company reported that the excessive flooding in the Natal province had caused it to close three of its mills. The company claimed $28m (about R430m) from insurers. On 21st April 2022, the company said that there had been no material damage and that operations had resumed, but 23,000 tons of production was lost, and 45,000 tons of inventory was damaged.

In an update on the quarter to 1st March 2023, the company reported HEPS down 67%. The company said, "Sappi delivered an EBITDA excluding special items of US$167 million against a backdrop of a challenging global economy and significantly weaker paper and pulp markets." In an update on the nine months to 30th June 2023, the company reported sales down 18% and headline earnings per share (HEPS) down 43%. The company's net asset value (NAV) was up 6% at 446c per share. The company said, "The Group faced persistent challenges in the global economy and encountered ongoing weakness in paper and pulp markets, leading to a reduction in EBITDA to US$106 million for the quarter ended June 2023."

In its results for the year to 30th September 2023, the company reported sales down 20% and HEPS down 62% in US dollars. The company's net asset value (NAV) was 5% higher at 438c per share. The company said, "The widespread disruption caused by ongoing geopolitical instability, weak global economic growth, rising interest rates, and an underperforming Chinese economy negatively impacted markets for our products."

In an update on the 3 months to 31st December 2023, the company reported sales down 23% and a headline loss per share of 22c (US) compared with a profit of 34c in the previous period. The company said, "Profitability was negatively impacted by approximately US$45 million due to the lower production volumes associated with the planned maintenance shutdowns at the Saiccor, Ngodwana and Cloquet mills offset somewhat by a US$26 million positive plantation fair value price adjustment."

In an update on the second quarter ending on 31st March 2024, the company reported sales down 6% and HEPS down 58%. The company's net asset value (NAV) dropped 13% to 387c per share. The company said, "Operating performance for the second quarter was slightly ahead of expectations with the group delivering EBITDA(2) excluding special items of US$183 million, which was 10% above the prior year."

In an update on the 3 months to 30th June 2024, the company reported sales up 3% and net asset value (NAV) down 9% at 405c (US) per share. The company said, "Operating performance for the third quarter was substantially above last year with the group delivering EBITDA(2) excluding special items of US$151 million."

Technically, the share has been in an upward trend since August 2023 but has become volatile in recent weeks. It is essentially a commodity share and hence somewhat risky.

SAP trade ideas

Our opinion on the current state of SAPPI(SAP)Sappi (SAP) is an international manufacturer specializing in paper, dissolving wood pulp (DWP), and paper pulp. The company supplies products to over 150 countries. DWP, a primary component used for clothing and packaging products, is crucial to Sappi's future profitability, although its price fluctuated sharply until demand from China surged in 2021. Civil unrest in July 2021 caused a loss of R220 million in profit, and additional challenges included Durban port backlogs and rising energy costs. In April 2022, severe flooding in Natal led to the temporary closure of three mills, a loss of 23,000 tons of production, and damage to 45,000 tons of inventory. Sappi filed a $28 million insurance claim and resumed operations shortly after.

The company has faced significant challenges recently. In its quarterly update to March 1, 2023, Sappi's HEPS dropped by 67%, citing weak global economic conditions and a decline in paper and pulp markets. By June 30, 2023, sales had fallen 18%, and HEPS was down 43%. The company's net asset value (NAV) had increased by 6% to 446 cents per share. Sappi's EBITDA for that quarter was US$106 million.

In the annual report ending on September 30, 2023, Sappi revealed a 20% decrease in sales and a 62% drop in HEPS (in USD), while the NAV increased by 5% to 438 cents per share. This decrease was attributed to global economic instability and challenges in key markets. An update to December 31, 2023, highlighted a further 23% drop in sales and a 22-cent (USD) headline loss per share, contrasting with a profit of 34 cents the previous year. Production was significantly affected by planned maintenance at major mills.

By March 31, 2024, sales were down 6%, and HEPS decreased by 58%. The company's NAV dropped 13% to 387 cents per share. Despite these figures, operating performance exceeded expectations, delivering a 10% increase in EBITDA to US$183 million.

Sappi's share price has been on an upward trend since August 2023, reaching 5325 cents after being included in the Winning Shares List (WSL) at 4729 cents on March 7, 2024. While the company remains in an upward trajectory, it's still a commodity share, which introduces some risk due to market volatility.

UPDATE SAPPI Target reached at R56.60 - Omwards and UpwardsSAPPI has performed great since it broke above the Symmetrical Triangle,.

The analysis was done in February, it broke above the Apex and since then has rushed to its first target at R56.60.

No ways, is this worth a punt to the short side. We can now expect some sideways chop, possible pattern form and then will provide another buy signal.

What is the opposite of Timber!!!! ?

$JSESAP - Sappi: Now I'm Convinced In The BreakoutSee link below for previous analysis.

I am now convinced in the breakout due to

1-Increase in volume after breakout.

2-Clear price continuation above the resistance trendline.

Buy the dips.

SAPPI - Broken its downtrendSappi has traded strongly recently and has now managed to break the yellow downward trend line. . As such, we could possibly see a retest of the yellow band before moving higher or, price could continue moving upwards in this relatively strong move. Initial target on this move would be around 58.18 and stop loss would be placed on a close below 40.80 or, on a close below the blue upward TL.

$JSESAP - Sappi: Not Yet Convinced It's A BreakoutSee link below for previous analysis

The stock has made a minor breakout from the upper resistance trendline and is currently using it as support.

I am not convinced by this breakout due to:

1-Low volume breakout

2-Weak price momentum after breakout

It's still early days but I will sit on my hands under I get more bullish evidence.

SAP: further gains after a correction?A price action above 4300 supports a bullish trend direction.

Further bullish confirmation for a break above 4700.

The target price is set at 5000.

The stop-loss price is set at 4200.

Remains above the confluence of 200-day and 200-week simple moving averages, supporting a bullish long-term trend.

Our opinion on the current state of SAPSappi (SAP) is a global leader in the manufacturing of paper, dissolving wood pulp (DWP), and paper pulp, supplying products to over 150 countries. DWP, crucial for manufacturing clothing, packaging products, and various other applications, was identified as a future profit generator for Sappi. However, the price of DWP experienced a significant drop until 2021 when it began to rise due to increased demand from China, reflecting its direct link to consumer spending patterns. Sappi's operations are geographically diversified, with its products sold in 150 countries. The company reported a loss of R220m in profit due to civil unrest in July 2021, alongside challenges such as backlogs at Durban port and escalating energy costs.

On 13th April 2022, Sappi announced the closure of three of its mills due to excessive flooding in Natal province, leading to a claim of $28m (approximately R430m) from insurers. By 21st April 2022, the company resumed operations, reporting no material damage but a significant loss of production and inventory damage.

For the quarter ending on 1st March 2023, Sappi reported a 67% decrease in headline earnings per share (HEPS), attributing the decline to a challenging global economy and weaker paper and pulp markets, resulting in an EBITDA of US$167 million. The nine-month update to 30th June 2023 showed an 18% decrease in sales and a 43% decrease in HEPS, with a 6% increase in net asset value (NAV) per share to 446c. The company cited ongoing global economic challenges and market weaknesses as factors reducing its EBITDA to US$106 million for the quarter ended June 2023.

Yearly results to 30th September 2023 indicated a 20% decline in sales and a 62% decrease in HEPS in US dollars, with a slight 5% increase in NAV to 438c per share. Sappi pointed to disruptions caused by geopolitical instability, weak global economic growth, rising interest rates, and a struggling Chinese economy as the reasons for the negative impact on its product markets. The most recent update for the three months to 31st December 2023 showed a 23% decrease in sales and a headline loss per share of 22c (US), contrasting with a profit in the previous period. The company noted that profitability was adversely affected by lower production volumes due to planned maintenance shutdowns, partially offset by a positive plantation fair value price adjustment.

Technically, Sappi's share price experienced a significant decline after forming a "triple top" between mid-2017 and September 2018, reaching a cycle bottom in March 2020 before trending upwards. The company's stock is considered a commodity share, which introduces a certain level of risk to its investors.

SAPPI looking shap! Target potential to R56.76Symmetrical Triangle seems to have formed on Sappi.

Now on the contrary of a Symmetrical Triangle being a Continuation pattern, it is possible for a reversal to take place in this instance.

We have the converging of the trendlines where the price has reached an apex. Strong buy divergences and price action to the up.

It's a bit premature to BUY just yet but I anticipate a breakour to the upside.

Then full steam ahead.

Other peripheral indicators confirm upside:

7>21>200

RSI>50 (Buy divergence)

Target R56.76

Our opinion on the current state of SAPSappi (SAP) manufactures paper, dissolving wood pulp (DWP) and paper pulp internationally and supplies products in 150 countries. DWP is used to manufacture clothing, packaging products and many other applications. DWP, specialty and packaging products were seen as the profit generator in the future, but until recently, the price of DWP had fallen sharply. Then in 2021 the price of DWP began to rise as demand from China surged. It is directly linked to the level of consumer spending, and it is well diversified geographically, selling products in 150 countries. The company said that the civil unrest in July 2021 had cut its profit by R220m. The company has had problems with the backlogs at Durban port and rising energy costs. On 13th April 2022, the company reported that the excessive flooding in the Natal province had caused it to close three of its mills. The company claimed $28m (about R430m) from insurers. On 21st April 2022, the company said that there had been no material damage and that operations had resumed, but 23000 tons of production was lost, and 45000 tons of inventory was damaged. In an update on the quarter to 1st March 2023 the company reported HEPS down 67%. The company said, "Sappi delivered an EBITDA excluding special items of US$167 million against a backdrop of a challenging global economy and significantly weaker paper and pulp markets". In an update on the nine months to 30th June 2023 the company reported sales down 18% and headline earnings per share (HEPS) down 43%. The company's net asset value (NAV) was up 6% at 446c per share. The company said, "The Group faced persistent challenges in the global economy and encountered ongoing weakness in paper and pulp markets, leading to a reduction in EBITDA to US$106 million for the quarter ended June 2023". In its results for the year to 30th September 2023 the company reported sales down 20% and HEPS down 62% in US dollars. The company's net asset value (NAV) was 5% higher at 438c per share. The company said, "The widespread disruption caused by ongoing geopolitical instability, weak global economic growth, rising interest rates, and an underperforming Chinese economy negatively impacted markets for our products". Technically, the share has been trending down since May 2022. It is essentially a commodity share and hence somewhat risky.

$JSESAP - Sappi Ltd: Forming A Wedge PatternSee link below for previous analysis.

Sappi has found the going tough since peaking at 6348, shedding over 40% of its value.

This bear trend looks to be forming a falling wedge pattern.

Price is still contained within this pattern so I will sit on my hands until we get a clear breakout, hopefully on higher than average volume.

SAPPI - ObservationThe stock seems to have formed a short-term top (hourly double top).

RSI reached overbought territory and unless bulls can close back above R47.50, a pullback to the rising 20ema is likely.

A Double Top is a bearish pattern that forms after an asset reaches a high price twice with a decline between the two highs. It’s confirmed once the asset’s price falls below a support level equal to the low between the two highs. The pattern includes a prior trend, first peak, valley, and second peak. The second top usually occurs with low volume and will be slightly below the first peak. This pattern signals a medium or long-term trend change in an asset class.

SappiAn extract from today's research. For more research insights, including trade ideas, get in touch today.

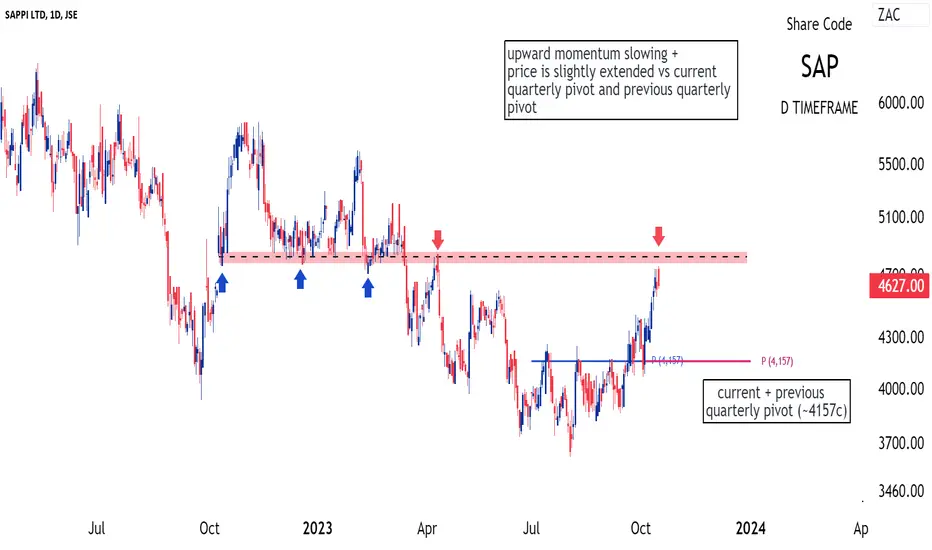

Over a 2-day period, the share has shifted one level lower, from high bullish momentum to strong. This possibly reflects a slowdown in upward momentum. Also over a 3-day period, sellers have controlled the range between 4685c and 4937c. It's possible that the share develops a minor pullback, potentially into the rising 8 and 21-EMA range before continuing it's trend higher.

In the Green: Bullish Indicators and the Quest for 56In the Green: Bullish Indicators and the Quest for 56

Sappi (JSE: SAP)

1. Price Formation: The price has broken out from a Reverse Cup and Handle price formation on a daily chart.

2. Moving Averages: The 7-day moving average (MA) is above the 21-day MA, which is a positive sign indicating short-term bullish momentum.

3. 200-day Moving Average is below the Price.

4. Thus, Mas 7>21>200

5. Relative Strength Index (RSI): The RSI is > than 50, indicating bullish momentum and potential further upward movement.

6. Price Target: 56

Sappi – the company

Sappi (JSE: SAP) is a global company that specializes in producing paper, pulp, and specialty products. They are one of the world's leading producers of dissolving wood pulp, which is used in the textile and pharmaceutical industries.

Sappi was established in south Africa in 1936 to produce paper.

Sappi has manufacturing operations on three continents, with ten production facilities in Western Europe, four in North America, and five in Southern Africa. The company has over 12,800 employees spread across over 35 countries.

The annual production capacity of Sappi includes:

• Approximately 5.7 million tons per year of paper

• Approximately 2.6 million tons per year of paper pulp

• Approximately 1.4 million tons per year of dissolving pulp

SAP: break major resistance?A price action above 4000 supports a bullish trend direction.

Starting to counter-test some major resistance (now support).

The target price is set at 4400.

The stop-loss price is set at 3900.

It will appear that the 200-week acted as some major support.

Remains a risky trade.

TIMBER! For Sappi to R20.00 due to Short Formed MShort Formed M Formation is evident.

This is a normal Double Top but the second one has a lower high than the previous.

This indicates even stronger selling pressure for the company.

With it broken below the neckline, the next price level it can go to is at least R20.000

Other indicators confirm:

21>7 (Bearish)

Price<200 - Bearish

RSI<50 (Lower highs)

Target R20.00

ABOUT THE COMPANY

Sappi Limited, originally known as South African Pulp and Paper Industries, is a multinational company specializing in wood pulp, paper, and paper-related products.

Inception:

Sappi was founded in 1936 and started operations as a pulp and paper company.

Headquarters:

The company is headquartered in Johannesburg, South Africa.

Global Presence:

Sappi operates manufacturing operations across three continents: North America, Europe, and Southern Africa.

Stock Listing:

The company is listed on the Johannesburg Stock Exchange, with secondary listings on the New York and London stock exchanges.

Primary Business:

Sappi is one of the world's largest manufacturers of dissolving wood pulp, a material used in a wide variety of products, including textiles, and packaging materials.

Paper Production:

The company is a leading global producer of printing and writing papers.

Product Range:

Beyond pulp and paper, Sappi also produces packaging and specialty papers, casting and release papers, and biomaterials.

Employment:

Sappi employs over 12,000 people globally.

$JSESAP - Sappi Ltd: Bullish Outlook Invalidated, Now What?The market is indeed fickle.

The last update on Sappi on 17.05.2023 maintained the bullish outlook as price held above 3937.

I was surprised by the market reaction to a very poor interim results report and the very gloomy fundamental outlook.

Well, it looks like the market has had second thoughts and corrected itself.

The stock has broken below 3937 thus invalidating the bullish outlook.

The question is, what now?

The bearish technical structure looks complex from the 6348 peak.

From 6348 to 3937, the move is in three waves ABC could be labelled as a higher degree (A) or (W).

The sell-off from 5835 looks to be developing another complex, extended structure which i can only label tentatively for now.

I will maintain a bearish stance below 4595 and update the labels as price unfolds.

$JSESAP - SAPPI: Bulls Defend 3937 But I Am Still TentativeOn 2023.05.11 Sappi released second quarter & interim results for the period ended March 2023.

The results were bad and the outlook was gloomy.

Salient results half-year:

Sales (13%)

EBITDA excluding special items (21%)

Profit for the period (17%)

The share rallied from 3968 to 4595, up almost 16% over the next three trading days.

The share has pulled back providing buying opportunities for those bullish on the stock.

Looking at the bigger structure from an Elliott Wave perspective:

*from 3937 to 5835, the view that the rally is wave 1 is still valid.

*from 5835 to 3968, this three wave move is a zigzag pattern with wave ((c)) unfolding as an ending diagonal.

If this is the complete correction, 3968 must hold and should be used as a stop-loss level.

Sappi is a volatile stock and the fundamentals do not look too good in the short-medium-term but the technicals are still valid for a bullish outlook.

TARGET REACHED: Sappi struck through the first price of R40.60Symmetrical Triangle formed on Sappi, the price broke below the apex and the price chose the bias of down.

We had other indicators showing bearishness such us.

200>21>7 - Bearish

RSI<50- Bearish

Target reached at R40.60

The trend is still down and we will need the next formation to form before we decide what to do next.

I'll keep you updated.

ABOUT

Sappi Limited was founded in 1936 and is headquartered in Johannesburg, South Africa.

Sappi's name is derived from its original name, South African Pulp and Paper Industries Limited. (Also think of SAP from a tree I guess).

The company was founded in South Africa in 1936 as a state-owned enterprise and was later privatized in the 1990s. The name Sappi was adopted in 1997 when the company underwent a rebranding exercise as part of its global expansion strategy.

The company is listed on the Johannesburg Stock Exchange (JSE) and the New York Stock Exchange (NYSE) under the ticker symbol "SPP".

Sappi is a leading global producer of dissolving wood pulp, paper pulp, and paper-based solutions.

The company has operations in North America, Europe, and Southern Africa, with customers in over 150 countries.

Sappi produces a range of products, including graphic papers, packaging and speciality papers, and pulp.

In 2020, Sappi launched a new product range called Sappi Verve, which is a compostable barrier paper designed for use in food packaging.

SAPPI - Bouncing on Support - JSESAPSappi is bouncing nicely off a rising trendline

R46.50 is the next level to clear to target the R50 level.

TRADE UPDATE Sappi breakdown with a markup before drop to R40.60Symmetrical Triangle formed on Sappi.

Broke below and has been coming down nicely.

200>21>7 - Bearish

RSI<50- Bearish

We recently had a markup phase which is where the orders are being filled from the recent drop. We need to retest the high (resistance) and price should come down. If it breaks above, it will be wise to place a stop loss and lock in profits as the trend will have turned up.

Right now, still bearish with a target to R40.60

Update: Sappi - target hitLast week Tuesday I published a short on Sappi at 4817c, with a target of 4380c, which was hit 2 days later. Today the share hit it's lowest level since September with a low of 4244c.

Original idea attached.

The majority of my research insights are published for clients and occasionally highlighted on this platform. To become a regular recipient of my research, including trade ideas, get in touch with me today for a brief discussion.

SAPPI On the way to target R42.39 Symmetrical Triangle formed and price broke below.

200>21>7 - Bearish

RSI<30 - Bearish

Since then it's been swimming to the price target of R42.39.

We can just wait until the trade plays out.