[Prakash Pipes ltd] CMP 490Date:26-12-2024

Time: 12:12PM

CMP: 490

Report by : Mujadid Saad

Evaluation of Prakash Pipes Ltd for Long-Term Investment

1. Financial Health

• Revenue Growth: Sales grew at a 14% CAGR over 5 years, with steady increases in operating profit margins (from 11% to 17%).

• Net Profit Margin: Improved consistently, with a 26% CAGR in net profit over 5 years.

• Debt-to-Equity Ratio: Low at 0.14, indicating manageable leverage.

• Return on Equity (ROE): Strong at 27.8%, showcasing efficient profit generation from equity.

• Free Cash Flow: Positive and growing, with ₹120 Cr from operations in FY 2024.

• EPS Growth: EPS has shown consistent growth, reaching ₹41.05 in FY 2024.

• Dividend Payout: Modest at 5%, retaining profits for growth.

2. Market Position

• Market Share: Positioned well in the plastics and packaging segment, with diversified products (PVC pipes and packaging).

• Competitive Positioning: A P/E ratio of 11.8 (below the industry median of 34.8) suggests potential undervaluation compared to peers.

• Customer Loyalty and Innovation: Stable growth indicates customer trust and consistent demand for its products.

3. Management and Governance

• Leadership Track Record: No major red flags; steady performance post-demerger from Prakash Industries.

• Corporate Governance: Promoter holding stable at 44.41%, signaling confidence in the company.

• Controversies: No significant litigation or ethical concerns reported.

4. Industry Trends

• Growth Outlook: Packaging and construction industries (key end-users of PVC pipes) are poised for steady growth.

• Emerging Trends: ESG compliance and recycling initiatives could enhance long-term prospects.

• Macroeconomic Factors: Inflation and raw material price volatility could impact margins, but the company's cost efficiency is a mitigating factor.

5. Risk Analysis

• Market Volatility: Stock price fluctuates in sync with market sentiment but shows resilience with positive long-term returns.

• Operational Inefficiencies: Managed well, with improving operating margins.

• Geopolitical Factors: Limited exposure due to domestic focus.

6. Valuation

• P/E Ratio: At 11.8, the stock is undervalued compared to the industry median of 34.8.

• P/B Ratio: Moderate at 2.82, with consistent book value growth.

• Industry Benchmark: Strong fundamentals make it attractive relative to peers like Astral and Supreme Industries.

7. Performance Metrics

• ROI and ROA: High returns on investment and assets due to operational efficiency.

• CAGR: Stock price CAGR of 49% over 5 years reflects investor confidence.

• Notable Achievements: Delivered strong profit growth while maintaining a healthy balance sheet.

Investment Decision: YES

Justification:

1. Strong financial health with consistent revenue and profit growth.

2. Attractive valuation metrics (low P/E and strong ROE) compared to peers.

3. Positive industry outlook, with resilience to macroeconomic pressures.

4. Efficient management and sound corporate governance.

5. Low leverage and strong free cash flow support long-term stability.

Additional Considerations:

• Monitor raw material price trends and their impact on margins.

• Assess ESG compliance and initiatives for long-term sustainability.

• Review quarterly performance to ensure consistency in key metrics.

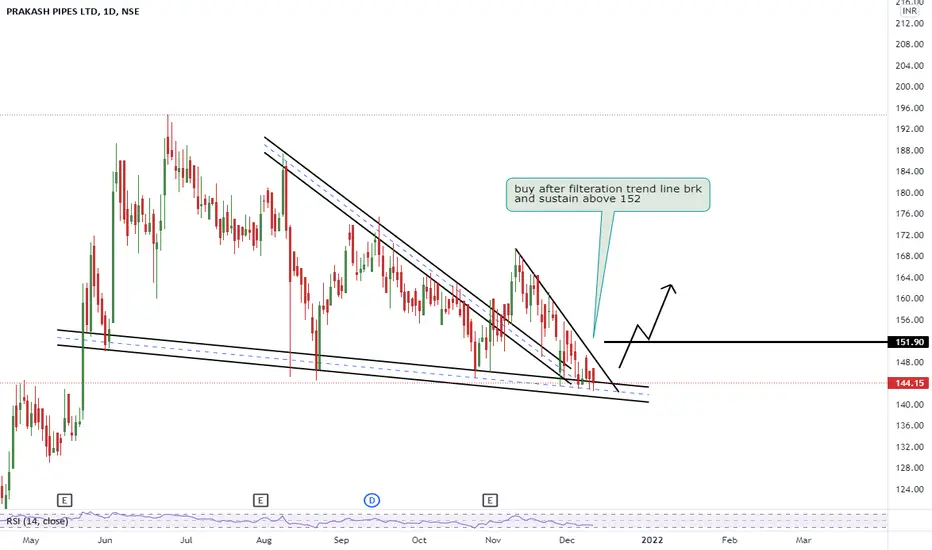

PPL trade ideas

Prakash Pipes - Fib RetracementWith steady sales, profit, dividend, increasing fii buy, this looks to be an attractive buy for a swing trade

PPL - Prakash Pipes Ltd - Uptrend - Long1. Double Bottom at Demand Zone

2. 50 EMA support

3. Volume Spike

4. ADX - shows Trend Strength buildup

Bullish View on Prakash PipesTargets towards 250/300

I just follow Fib levels.

I am not the best analyst like the other social media experts. I am just a beginner and self investor. Please DYOR

Prakash pipe looks goodPPL Has given very strong breakout.

Now waiting for a retest entry.

Keep on watchlist.

Prakash Pipes Strong Bullish momentumWeekly timeframe has broken out of a 2 year long consolidation period, it shows a flag and pole pattern breakout at Weekly R1.

Also note that the consolidation and bounce that has happened is at Fib 38.2%, hence expect strong bullish momentum to continue.

Hence looking for huge upside potential in the Mid to Long term, for a short term can look for the black lines marked in the weekly timeframe.

Demand levels marked in the 75 min time frame.

Prakash Pipes can Pull Out a good jumpPPL CMP: 171

Prakash Pipes is one of the largest PVC pipes and fittings manufacturer in India. The company products are Agri pipes, plumbing pipes, casing pipes and garden pipes etc. In 2018-19 the company entered flexible packing division & furthermore expanded it to provide complete packaging solutions to FMCG companies manufacturing laminates and pouches for snacks, soaps, shampoo etc.

Prakash pipes CMP is 171. The Negative aspects of the company is high promoter pledge. The Positive aspects of the company are improving annual net profits, no debt & improving cash from operating activity.

Entry can be taken at closing above 175. Final entry at 185. Target of the call will be 199. Long term target is 209. Stop loss of the call should be maintained at closing below 155.

Fibonacci Levels - Multiple Support LevelsFibo retracement levels acted as support level at multiple price points

Disc : Not holding and not a buy or sell recommendation

prakash pipes breakoutcan enter in pull back.

low debt, price lower than book value by 1.5 times, intrinsic value 205

warning : earnings / revenues not growing steadily

for education purposes

PPL 1DNSE:PPL

Please note that we are not a SEBI Registered Investor Adviser/PMS/ Broking House.

All the contents over here are for educational purposes only and are not investment advice or recommendations

offered to any person(s) with respect to the purchase or sale of the stocks / futures and options.

You are also requested to apply your prudence and consult your advisers in case you choose to act on

any such content available as WE claims no responsibilities for any of your actions or any outcome of

such action

PPL 1DNSE:PPL

Please note that we are not a SEBI Registered Investor Adviser/PMS/ Broking House.

All the contents over here are for educational purposes only and are not investment advice or recommendations

offered to any person(s) with respect to the purchase or sale of the stocks / futures and options.

You are also requested to apply your prudence and consult your advisers in case you choose to act on

any such content available as WE claims no responsibilities for any of your actions or any outcome of

such action

PPL 1DNSE:PPL

Please note that we are not a SEBI Registered Investor Adviser/PMS/ Broking House.

All the contents over here are for educational purposes only and are not investment advice or recommendations

offered to any person(s) with respect to the purchase or sale of the stocks / futures and options.

You are also requested to apply your prudence and consult your advisers in case you choose to act on

any such content available as WE claims no responsibilities for any of your actions or any outcome of

such action

NSE:PPL LongNSE:PPL

#PPL broken the resistance and closed above the level, Sustainability will give good positive momemtum.

Good above : 160 with SL 145

⭐ Pipes are buzzing | Amazing pattern to trade on A very good breakout from this channel :)

Quite tradable with proper risk management

Prakash PipesPrakash Pipes....giving Rectangle Breakout. Looks good to add each dip for good gains.

Also recently have good results. They even recently added cvc pipes in their portfolio which will give good profit in coming times.

PPL at all time high with highest volumeAt ATH with highest volume, maybe consolidation, but could be good bet on breakout above 121 on weekly closing basis

PPLPPL gave a good volume breakout. Entry, SL, Target updated on chart.

These idea's are not my recommendation. Do your own analysis before making any trade based on this idea.