Want to join the fun ride to zero?Hello,

This is our time to shine my bear bros! I waited for this moment my whole life! I constantly wait for the moment to make money while others suffer.

If you have been in this game for more than 6 months you know that Credit Suisse is a losing story.

No one wants to buy this dead bank. And even people "on its side" have targets way below where the price is right now.

UBS made claims about possibly buying CS in the future, which would provide a lot of liquidity (from noobs throwing their money into the fire).

As usual casuals are all long, 99% of IG clients are long. Humans are broken, I think they are part of a different species than mine.

And what is the best way to make quick profits? Short selling a stock that has fallen by 90%, if your broker and regulator will allow you to.

This pos is going to zero and there is nothing these 🤡 can do to stop it. History will repeat itself with mindless monkeys trying to "save the stock market" and to "save" a "reputable" bank. It's a lot of fun to see stupid people make the same mistake, but if these stupid people actually would let us make money from their mistakes then it would be even more fun. The more they try to "save" steaming piles of 💩, the more slow and painful it will be as well as harder to bounce back from.

This will at least be a lesson. A lesson to have several brokers (which I do) because they typically have the regulator pressuring them to protect "rEtAiL tRaDeRs" eager to buy shares such as this "thing" and lose everything they have. I have to be 1 in 100 that actually has a brain and wants to sell but that's barred too (otherwise the creatures will get angry and blame me for their losses). I'll update this idea if I am able to short sell 😁.

It could go up a few hundred percent sure, and a lottery ticket could go up a few million percents too. I'd never buy this, not without some sort of uptrend or new high first, and even then I'd just be in short term hoping for suckers to follow.

Definitely a great stock to short sell. It will still be overpriced at 1 cent.

CS trade ideas

Downtrend Credit Suisse Group Monthly1.1. Downtrend Credit Suisse Group Monthly. Shows the fall in the last years

Credit Suisse: Heading to Bankrupcy? Is this stock really heading to bankrupcy? Maybe. It looks like that's the case from a technical analysis perspective. The stock's price has been dropping consistently over the years dating all the way back to 2014. As of today, on Tuesday April 18, 2023, the stock's price is at $0.92 ....less than a dollar. This is the first time the stock has dipped below $1. News on Yahoo finance reveals a plan by another investment company called UBS Group to acquire Credit Suisse Group. Earnings announcements show that net income has gone in the negatives in 2022. Before 2022, CS stock was producing positive earnings reports.

go up or dieIn my personal opinion, if Credit Suisse does not grow from these areas, it will lose all hope

This trading setup is risky but has an attractive risk to reward.

$CS Credit Suisse to have big day tomorrow? #CreditSuisseAt the bottom of a channel.. looks quite possibly that we could see a large bounce there. It is quite literally the only bank stock that I've seen that looks good to me.

This trading strategy WILL make you TONS of MONEY!Hello, guys!

Today I share a strategy I discovered in 2017 when doing comprehensive Fibonacci research!

Everything in this world starts from 0, so we also use that rule in markets!

Hope you find this educational and stay sharp!!

CS Credit Suisse Group to $0.27 on Monday??UBS Group AG has made an offer to acquire Credit Suisse for as much as $1 billion.

The Swiss government is planning to change the country's laws to bypass the need for a shareholder vote on the deal, as they seek to restore confidence in the banking sector following Credit Suisse's outflow of 10 billion Swiss francs in just one week.

The proposed agreement, which is an all-share deal between Switzerland's two largest banks, is expected to be signed as early as Sunday evening.

The deal is priced at a fraction of Credit Suisse's closing price on Friday.

According to insiders, the offer was made on Sunday morning at a price of 0.25 Swiss francs ($0.27) per share, payable in UBS stock.

On Friday, Credit Suisse's shares closed at $2.01 Swiss francs.

I think we are about to see more bidders and the price go up from $0.27.

Looking forward to read your opinion about it.

It can't go bankrupt, and these are good times to enterA 167-year-old bank that they will not allow to fail because Switzerland will stand behind it

Credit Suisse Price Channel PainI don't love the idea of making grandiose predictions; I prefer to see everything in ranges of probability.

That being said, the few simple tools I have added to this chart seem to have rather negative implications.

There may be other price levels that are noteworthy, but I see the psychological levels of $10 and $3 having importance here.

$6.50 as a previous ATL.

$2 Psychological Support Level currently bearing the brunt of the weight.

The wick of the current candle falls below to the current ATL of $1.76.

I have marked a vague price channel towards the end.

End result is a possible price channel to $0.

To me, this doesn't look great.

Take everything anyone says with a grain of salt.

DYOR/DYOC.

Commentary welcome; I don't mind being wrong, especially in this case.

Credit Suisse trend linesNew to this.

But it seems to me $CS should hold at around $1.81. The midline is in the $2.50ish range.

Maximum Pain in The Future CS Credit SuisseBanks restructure the debt of stressed corporations every day, not out of philanthropy but out of enlightened self-interest.

But the problem was that, now that we had accepted the EU–IMF bailout, we were no longer dealing with banks but with politicians who had lied to their parliaments to convince them to relieve the banks of Greece’s debt and take it on themselves.

A debt restructuring would require them to go back to their parliaments and confess their earlier sin, something they would never do voluntarily, fearful of the repercussions.

Credit Suisse is A Mess, This won't be good R-R for a reversal until late 2023. There are hundreds of significantly better opportunities available

CS mean reversionCS is approaching some important areas in terms of trend.

Given it's failure to fail amidst the FUD of insolvency, restructuring, etc, the fundamental probability of some kind of mean reversion to major MAs is increasing.

Walking outside of the yellow down trend line would be a bullish signal for a mean reversion to occur.

Continuing along the path of the green down trend line would signal we should continue to wait for more shoes to drop.

Currently sitting at a triple top on the hourly, and hitting resistance at the yellow trend line on the weekly. A break higher should signal a move to the 5's near term, and open up the door for a longer term move to the 200ma weekly around 9.

Looking at this with a long bias

Fwiw, I would want to keep any profits as shares given the dividend history on this.

Keeping an eye out on $CSLooks to be coming out of a decades length descending wedge. could see some upside soon.

Growth potential for CSGrowth potential for Credit Suisse, that is currently trading at the lowest ever reached.

CS quite likely hit bottom and is slowly crawling out of the hole.

Mismanagement hit the company in the recent years and the recent (few days ago) reshuffle at the top of its Investment Banking division is yet another step for the company to seek a way out of the current situation.

Two important levels are to be monitored in my opinion.

3.40 and 3.80 are two levels to keep in mind as strong resistances to break in order to see a real bull run.

*** This Content is for educational and informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. ***

All I Want For Christmas Is the TruthToday's research note is rather pointed and short. The function of these notes is to provide a little depth and context for an event or environment in the world, primarily focused on Financial markets, and there is a particular subsection of shoddy securities regulations that deserves a moment of reflection. Credit Suisse is a Foreign Private Issuer on the New York Stock Exchange - NYSE, which means it follows a special rule set. This alternative ruleset isn't as game-breaking as any number of the core errors built into the system, regulators asleep at the wheel, or even accounting firms counting on consulting fees; this ruleset just turns the water that much more opaque. Key highlights are reduced financial reports, alternative accounting methods on those financial reports, and an ability to significantly delay market impacting information. Chinese companies filing as ADRs received similar benefits and committed enough fraud to force the SEC to drastically increase reporting requirements. Investors still do not know the whole story of two impactful events from the last few years afflicting Credit Suisse, nor the extent to their cooperation with US Federal authorities in investigations to rival banks. This analyst cannot and will not argue whether Credit Suisse's glass is half empty or half full, only that whatever is in the glass isn't clear.

Credit Suisse can report in US GAAP, non-US GAAP, or International Financial Reporting Standards- of which it only needs to report semiannual unaudited financial statements from the first two quarters. Saving Credit Suisse from all this paperwork will surely help keep them in one lean mean-flailing machine, as they are also not required to disclose material nonpublic information in a timely manner. On top of that, insiders may sell and short sell shares as they please under the guidance, prudence, and regulation by the internal compliance officer - except their audit post-Archegos showed there was no real compliance structure. The other major benefits include Governance exemptions, especially in Compensation disclosures. The biggest one of these is the SEC Proxy Rule Exemption which allows Credit Suisse to make all disclosures and reports in proxy statements under the rules of it's Sovereign, the Swiss National Bank- SNB.

Then there is Rule 12g3-2b. This exemption allows for a FPI to not register a class of securities under some minor qualifiers, one being it's primary listing exchange is outside the US. Late 2021, the Bank of New York Melon issued a new bankruptcy-proof share class, information that was vital to have under their current financial strain. Should recent reports on Qatar's plan to gut and split Credit Suisse be accurate, it would be vital to know major changes and qualify capital raises. If investors expect this information to at least be reported quarterly, again, it does not.

Finally, Credit Suisse serves the interests and at the behest of the SNB, and Swiss government. Credit Suisse exists to service Swiss money and Swiss business interests, to connect foreign investors to Swiss bank accounts, and Swiss bank accounts to foreign markets. Failure to perform adequately in any of these functions will drive more investors away, which the public markets only know due to other financial institutions reporting over $90 Billion in withdrawals from Credit Suisse in October, which never recovered. Cutting the Timberrrr jokes, whatever is happening in and to Credit Suisse will be murky at best. Leave the presents under the tree, give me the financials to unwrap Christmas day.

Author's Note:

I don't intend on writing on Credit Suisse for a while, this is in response to a significant number of questions on investing for a bounce. Credit Suisse is at All-Time-Lows, from previous All-Time-Lows. Whenever those brand new lows stop and how low it goes is anyone's guess, but it is a guess. Too many smart people keep getting this environment wrong to count on any smart guesses, I say stick to what you see - and can see. Good luck, Merry Christmas, Happy Hanukkah, and if I don't see you, have an amazing New Year.

Selected References:

www.perkinscoie.com

www.credit-suisse.com

www.law.cornell.edu

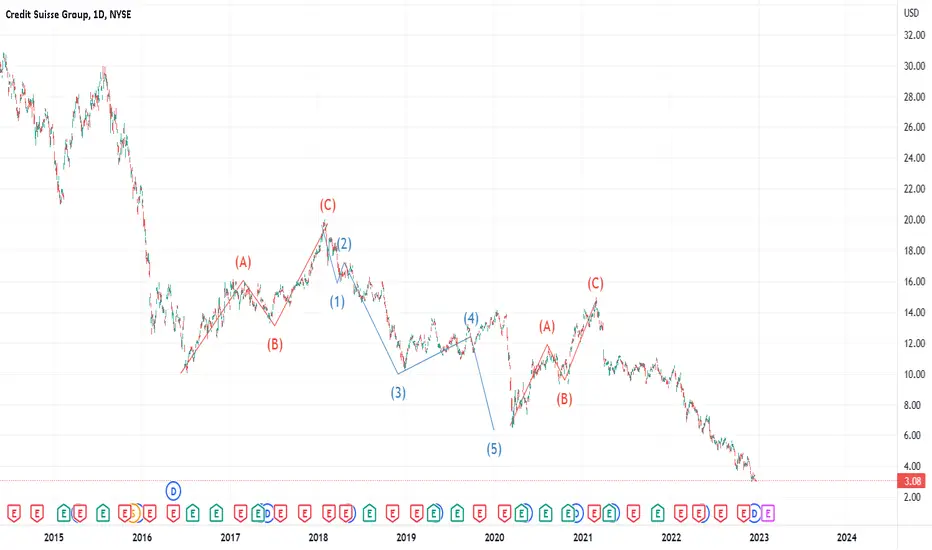

CS elliot waves all the way down. We drew attention to the CS Elliot formation when we were at 11. Now we're at 3 and the EWs have been very consistent all the way down.

No bueno for CS.

nothing like a safe swiss bankwhat do you think folks know about this penny stock, maybe we should pay attention

this can not be goodlehman 2.0 counterparties etc, member '08? one of europes biggest banks, whats up with that?

CS | I Might Be A Buyer | BounceCredit Suisse Group AG, together with its subsidiaries, provides various financial services in Switzerland, Europe, the Middle East, Africa, the Americas, and Asia Pacific. The company offers wealth management solutions, including investment advice and discretionary asset management services; risk management solutions, such as managed investment products; and wealth planning, succession planning, and trust services. It also provides financing and lending solutions, including consumer credit and real estate mortgage lending, real asset lending relating to ship, and aviation financing for UHNWI; standard and structured hedging, and lombard lending solutions, as well as collateral trading services; and investment banking solutions, such as global securities sales, trading and execution, capital raising, and advisory services. In addition, the company offers banking solutions, such as payments, accounts, debit and credit cards, and product bundles; asset management products; equity and debt underwriting, and advisory services; cash equities, equity derivatives, and convertibles, as well as prime services; and fixed income products, such as credit, securitized, macro, emerging markets, financing, structured credit, and other products. Further, it provides HOLT, a framework for assessing the performance of approximately 20,000 companies; and equity and fixed income research services. The company serves private and institutional clients; ultra-high-net-worth individuals, high-net-worth individuals, and affluent and retail clients; corporate clients, small and medium-sized enterprises, external asset managers, financial institutions, and commodity traders; and pension funds, hedge funds, governments, foundations and endowments, corporations, entrepreneurs, private individuals, financial sponsors, and sovereign clients. As of December 31, 2021, it operated through a network of 311 offices and branches. The company was founded in 1856 and is based in Zurich, Switzerland.

The Bank Run ComethEquations have two-sides, and solutions involve balance. Perhaps there is no country greater known for keeping a balance than Switzerland. In fact, Switzerland has maintained it's strength through several "world orders" by maintaining balance on the financial equation - not by keeping balanced finances, but by serving both sides. It is common history that Switzerland's Bank for International Settlements (BIS) serviced Nazi Germany's economy, granting them the financial fortitude to carry a war against the world. Switzerland has long stood by an ethos of "a world that banks together, stays together", sheltering it's institutions against countless historical attempts to engrain ethics or be held accountable for the downstream effects of those they help. Tangential to every step of Credit Suisse's story, and this analyst's interpretation, has been the approval and motions of the SNB. Pre-COVID, SNB requested CS to strengthen it's balance sheet. Failing this direction, SNB next pushed CS to merge with an ally to rebuild the international banking arm to preserve Swiss interests. On the back of those proclamations: Greensill, Archegos, Russian Oligarchical financing, #SuisseSecrets, CET1 requirements breach, a recent bank run, and... more?

Credit Suisse revealed their most recent restructuring plan on October 27th, 2022 headlining with Cost and Staff cuts, a $4 billion capital raise via equity dilution, and a nascent restart of the First Boston Investment Bank. All this will bring on a new investor with just under 10% ownership of the Swiss bank - the Saudi National Bank (SaNB). Switzerland has been integral to the history of the world since it's birth in 1291, playing critical roles long before the Americas were discovered by a European power, long before the notion of the Petrodollar and Bretton Woods. Now, as sovereign rivalries reshape the global economy, centered on the United States-Saudi leaders mutual hostility, Switzerland finds itself in a uniquely-Swiss position. There is a historical platitude for making UBS the Western bank, CS the Eastern. Switzerland would maintain their position as the neutral facilitator of global financial matters, eschewing notions of ethics for a platform of stability. While many governments might be quick to take sides for diplomatic favours and intranational positioning, Switzerland alone can service the inelastic needs for all sides to maintain a balance, maintaining the equation for global growth and unity.

But can Credit Suisse maintain a balance without losing more legs? Taking on a Middle Eastern sovereign as a major shareholder is a repeat of CS's GFC restructuring, a plan that saw Qatar taking massive stakes in convertible bonds leading to equity dilutions. However, the GFC-periods rise in oil prices was far from political-endeavors for national profits; a hyperinflationary risk environment led to hyperinflationary asset appreciation across the board, oil as well. The current rise in oil prices is a direct confrontation between US and OPEC leaders - specifically Saudi Arabia (minus the chaos from Putin's moronic war*). The ability for a single organization to maintain bridges between Western and Middle Eastern financial interests might be difficult, but separating them between two arms of the same sovereign state might provide cover. Which makes the First Boston move the oddity of the plan - perhaps even the impossibility. Renaming the investment branch as a new investment bank is one way to obscure losses, but First Boston has a ring to it that assumes Western positioning, positioning that will involve Saudi money. First Boston is to be Headquartered in NYC. With recent moves by the US government to limit and block Chinese investments in specific technological sectors, the question of moves against Saudi interests is not a silent one. Especially with NOPEC, the No Oil Producing and Exporting Cartels Act, a bill making it's way through the US senate that would allow charges to be brought into US courts against OPEC nations. Blurring the lines of whose money goes where is one thing, doing it in an environment of direct financial confrontation is requiring more finesse than an organization that just recently announced it had a bank run might be capable of.

Enter the bank run. Last week Credit Suisse announced investor withdrawals pushing below their minimum CET1 requirement, a simple metric to prevent banks from taking on too much leverage compared to liquid and valuable assets. Credit Suisse has one of the higher minimums at 11.4%, but CET1 is hardly the metric of stability to be called on. The actual requirements of Capital Equity Tier 1 is loose; Capital Equity Tier 1 includes volatile equity holdings and swaps that are not guaranteed or protected by any sovereign. Q3 2021, Credit Suisse sat at 14.4% CET1, Q2 2022 was 13.5%, and Q3 2022 was 12.6%. Which means in early October, as Credit Default Swaps moved to GFC#1 highs and equity to lows, major investors withdrew at least ~$2 billion dollars. Credit Suisse claims that they did not need SNB-aid, but someone in Switzerland activated Federal Reserve dollar swaps to a tune of $10-11 billion through the SNB. UBS released a report saying it could have been an arbitrage opportunity, as the Federal Reserve's interest rate is ~.25%, and SNB is giving .45% interest for dollar liquidity - an arbitrage opportunity specifically designed to exist to give financial institutions deniability and liabilities - or rather assets (banks sure do like to flip the names). Bank runs are considered old, maybe even ancient. Fall of 2021 led to some "bank run" behaviours in China when the collapse of Evergrande reverberated across financial institutions and many citizens attempted withdrawals. The pictures and videos were clear as long lines of customers stood outside of their bank, and more stood outside the offices of their favoured real estate investment vehicle company. One of the biggest arguments against a financial crash and bank run in 2022, is that this couldn't happen in 2022 - banks would be able to give endless amounts of capital to customers to move to other banks and just write them off as liabilities and take a loan from their courterparts - an act that is playing out similarly to Credit Suisse as just about every major bank in the world is filling in their accounts with loans. When the BIS added CET1 requirements post-GFC, the ideaology was that it forced banks to control risk-on behaviour and limit leverage, preventing even the possibility of bank runs. But if there was anything positive from the recent Senate oversight committee on the banks, it was that JP Morgan et al are quite worried about these CET1 requirements. The idea was sound, the regulations too loose, and now the tool to prevent is looking like the tool to affect. Depending on how much investors did withdraw, as Credit Suisse was only ~$1.5 billion from their threshold as of latest quarterly reports, another bank run could happen as investors digest a restructuring plan promising weak profits 3 years in the future against a backdrop of continued legal troubles, major geopolitical contentions, and whatever stupid risky loans Credit Suisse has made that hasn't collapsed yet. Because yet is coming.

And then there was the restructuring plan. Credit Suisse will tap Apollo and friends to handle the Securitized Product arm, rename the Investment Bank arm, and try desperately to hold onto wealth management while reducing "non-core businesses". Apollo and friends will control business operations of the securitized product arm and feed these assets back into the Wealth management and Investment Banking arms of Credit Suisse, the same Securitized product arm that securitized Russian oligarch's yachts, faxed the paperwork to all their rich clientele to woo investors, subpoenaed for information and details on said paperwork, and then asked their clientele to destroy all paperwork. The idea is that this isn't going to end, but Credit Suisse will have maximum plausible deniability as they no longer "know" the details of securitized products, just interest and fees. The Non-Core Unit they are winding down? It is leveraged 132x, makes up Residual Prime lending, European Investment bank lending, Emerging Markets lending, and presence in selected countries**. The billions of dollars Credit Suisse has of CET1 is ubiquitous across the Bank, these are the same billions of dollars needed to maintain Leverage ratios of 168X in Wealth Management, 241x in the core Swiss Bank, 3x in Asset Management, 184x in Investment Bank, 32x in Corporate Center, 85x in Securitized Products, and 132x in the Non-core unit. This means that Credit Suisse has to completely restructure and shed massive capital arms without taking on major losses, again. All of this just to squeeze out sub-10% return on tangible equity (the most intangible returns possible), meanwhile almost every banking competitor is above that now and without as massive losses coming into this quarter.

This analyst's fascination with Credit Suisse is mechanical. How does a bank run happen in modern financial infrastructure with modern financial regulations? How does it start? How does it end? How does it spread? Bank runs are an unhealthy event, but part of a healthy cycle of degradative turnover. In the human body, old and dead cells are continuously removed so that new and healthier cells can take their place. Credit Suisse failed their basic role of creating healthy and stable economic growth, they failed their basic role of making money, and they failed their basic role of assuming safe risk. Archegos and Greensill were multi-billion dollar loans with limited possible profits, but extremely outsized risks. Even if Credit Suisse didn’t know what Archegos was buying (which would be impossible since they were a prime brokerage and thus the point of contact), loaning tens of billions of dollars for Public Equity market portfolios on derivative holdings is… dumb. Greensill's business worked by premonition; Greensill would loan massive amounts of money to specific businesses in their sector on the assumption business would grow and they would make *billions* in interest fees. All of this with Greensill booking and billing companies that it never interacted with, and never formed contracts. It shouldn't take too competent a risk management team to dissect these business plans and point out the stupid, but Credit Suisse's were not up to the task. Similar to investors leaving CS, major employees are too. Part of this is good, some of these high up employees failed their basic roles and responsibilities, so watching them move to their competitors is an oddity. But now CS is expected to restructure while maintaining, continuing to find and invest in profitable wealth and investment vehicles, without any of their staff. Staff who are also being fired to the tune of 9000 bankers this year.

Still, banks can’t just fail. Banks are connected to each other directly and indirectly, through third party counter-risk groups. Credit Suisse makes a loan to company X for $5 billion over 10 years. Credit Suisse goes to counter-risk party A to hedge this loan, i.e. if X fails to pay, A pays out. It doesn't cover everything, but on paper it changes a $5 billion liability into a neutral bet, books are even-weighted and no one is concerned. Counter-risk party A plays counter-risk to several banks on many loans. The recent work by Ellul and Kim on "Counterparty Choice, Bank Interconnectedness, and Bank Risk-Taking" published by the Office of Financial Research using confidential risk agreements by US banks illustrates this perfectly***. In fact, their work illustrates that banks aren't just more likely to use the same counterparties for risk, but they are also selling Credit Default Swaps on these counterparties, almost as if they are sure they will fail. Which means they are completely unhedged. Either Credit Suisse survives, or more will fall.

*Putin's moronic war - this author feels comfortable with this description, as Russia, the sovereign country, is much less so. Sure, Putin drove a massive rise in energy prices that benefitted Russia's energy exports, but led to a destruction in international wealth, value, and respect that will take decades to recover from. Furthermore, Russia has seen so much loss in combat personnel that it will take generations to recover. Yes, he has slaughtered thousands and thousands of Ukrainian citizens and soldiers, raised hell in Western markets and economies, but has brought more pain upon his own nation than any other - making this a stupid and moronic war.

**TBD, likely to grow to… all.

*** www.financialresearch.gov READ THIS! Using confidential information given to federal regulators, Ellul and Kim perfectly show how banks have engaged in the riskiest behaviours by selling default debt on their counterparties and by overloading the same counterparties. If bad loans default, the hedging banks do will be negated.

Selected References

www.credit-suisse.com

www.finews.com

www.congress.gov

www.financialresearch.gov

too big to fail: swiss editionthe fed has quietly halted bottom line reductions of the balance sheet, markets should rally leading into the holiday season and then tank once again. CS is heavily exposed to growth and tech sector. I expect that sector to relief pump and help repair their failing balance sheet in the short term. Gets a bit shakier depending on if there is sufficient time and liquidity for them to reposition before an anticipated downturn in Q1 2023 or so.

Credit Suisse, classic chart?Classic buy the rumor sell the news chart

Volume that is increasing in this last deep

The only green stock in my watchlist on Friday

Parabolic bounce to 76 fibs.My attention is drawn to this because people are talking about it. I'm not one for the fundies but I do always notice if people are speaking about a lot of bad news in something and then in the days after everyone is talking about then shock rally in it. When I see these things, I always look for 76 retracements.