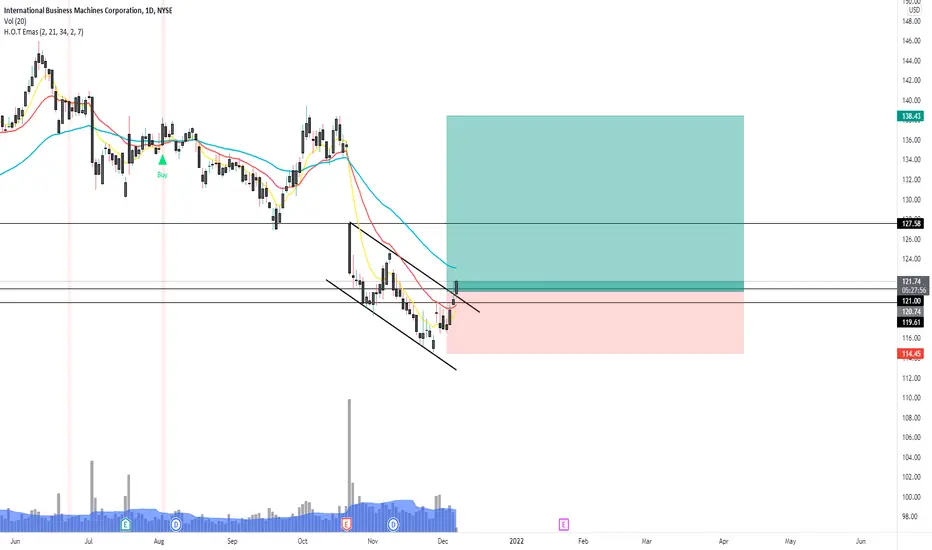

$IBM bounce? potential target $300 (4/5)Conviction: 4/5

need to break above descending resistance line for confirmation.

depending on speed of ascent, upper channel points to $300 target

General Thesis

bounced off long-term channel support since 1984-ish recently in 2020

also seems to continue channel since 1999

bounced off short term channel since 2020 lows

weekly RSI about neutral

Growth

Gross margins (50%) is pretty steady, near historical highs

Revenue growth (0.33%) is super low, but recent highs

Value

P/FCF below average (25th percentile)

P/S about average

Fundamentals & Balance Sheet

low debt to asset (<1)

Potential Risks

entry for Weekly RSI is not ideal, could be lower

IBM trade ideas

IBM LongZone confirmation entry

Demand Zone below Support zone

Entry 126

Stop 123

Target 133, 145

Risk management is much more important than a good entry point.

I am not a PRO trader.

In my trading plan, the Max Risk of each short term trade should be less than 1% of an account.

IBM - careful SELLIBM is within a defined regression channel, and the top is around $ 129-130.

The stochastic RSI is on high side, and the RSI is high based on historical performance.

I feel selling near top of channel $ 128-130 with tight stop $ 135, which means we would be trading within the GAP. The GAP down previously suggest we may trade below that for the coming weeks.

The over picture is we should re-test lower $ 116.

Wait the selling moment for IBMIBM's stock is on my target to sell.

Firsrly, it is under EMA200. The RSI form a trading divergence on my extreme bought area.

But won't directly sell it now. I want to wait the bearish candlestick on a daily timeframe exactly on the next day. EMA200 curve will be my maximum stop loss if I execute selling.

IBMI watched this ticker for 2 weeks now. I expected the reversal on the weekly channel which was confirmed. I am bullish on this and I believe we are seeing money flowing into this ticker. We have a gap on the Daily to fill but it appears we rejected it last week. I am watching for continuation and if it fails, I expected a retest of the weekly channel.

$IBM... wonder what @allstarcharts 💫 thinks of this name? 🤔👇The old-school tech company starting to test the gap. Can't ignore the smiley face and the green finish on Friday with the market red!

IBM USA Sun Storm Investment Trading Desk & NexGen Wealth Management Service Present's: SSITD & NexGen Portfolio of the Week Series

Focus: Worldwide

By Sun Storm Investment Research & NexGen Wealth Management Service

A Profit & Solutions Strategy & Research

Trading | Investment | Stocks | ETF | Mutual Funds | Crypto | Bonds | Options | Dividend | Futures |

USA | Canada | UK | Germany | France | Italy | Rest of Europe | Mexico | India

Disclaimer: Sun Storm Investment and NexGen are not registered financial advisors, so please do your own research before trading & investing anything. This is information is for only research purposes not for actual trading & investing decision.

#debadipb #profitsolutions

IBM double topLook at this clean rejection to form a nice double top. I'll be looking to enter into puts if resistance levels hold.

IBM bottomed?Great R:R on the chart.

Looks like it found a bottom and its ready to move.

There is a gap on the upside that could get filled as well.

IBM Idea - Restoring TrendlineCurrently price is sitting just under a major trendline that can be drawn

Similarities can be drawn between a dip in the early movement of IBM and one that has occurred recently

Post this dip, the price rose and retook the trendline

I expect this to be the case again

Weekly Chart

IBM 4h wolfe wave bullish 11/29A Wolfe Wave is a chart pattern composed of five wave patterns in price that imply an underlying equilibrium price. Investors who use this system time their trades based upon the resistance and support lines indicated by the pattern.

$IBM coming into support for swing into 2022 Idea : Swing Long $IBM from support levels into next earnings (~3 months).

Rationale : The last two quarters earnings were great for IBM and price increased both times, last year around this time we had a big gap down after earnings , and ran up into the next earnings which had another gap down and then ran up. I anticipate there is seasonally in their revenue recognition and with the gap down this past earnings , I expect price to rebound going into early next year before Q1 earnings . IBM is an establish IT player making big moves in AI and 5G with over 50% institutional ownership. This swing may take a few months but I think the set-up is solid.

Entry : I have an alert set at 124.19, but my buy zone is highlighted in green on the chart and I will add at the white line shown.

Exit : Sell when the gap closes before next earnings (do-not hold into next earnings ).

Good luck!

$IBM with a Bearish outlook following its earnings #Stocks The PEAD projected a Bearish outlook for $IBM after a Negative Under reaction following its earnings release placing the stock in drift D with an expected accuracy of 81.82%.

If you would like to see the Drift for another stock please message us. Also click on the Like Button if this was useful and follow us or join us.

IBM an opportunityfor long-term investors???IBM :125

Market cap: 112 B

P/E:23

Dividend Yield: 5.21%

Currently trading at the bottom of a bullish regression channel (-3,+3).

In the past, it touched this level and each time bounced back +50%..!

The fundamental fair value estimation is 142-172 USD/share which is very likely to happen in the next trading year.

However, in the past 5 years, IBM showed that it could easily slip to 90-100 USD/share and no matter how good this company is, The price pattern says there will be better opportunities to buy IBM in the next few months!

Best,

Moshkelgosha

DISCLAIMER

I’m not a certified financial planner/advisor nor a certified financial analyst nor an economist nor a CPA nor an accountant nor a lawyer. I’m not a finance professional through formal education. The contents on this site are for informational purposes only and do not constitute financial, accounting, or legal advice. I can’t promise that the information shared on my posts is appropriate for you or anyone else. By using this site, you agree to hold me harmless from any ramifications, financial or otherwise, that occur to you as a result of acting on information found on this site.

IBM Wedge breakout My idea is for long term holders.

Technical - IBM price has broken out of a downward sloping wedge pattern which is usually a bullish pattern.

Fundamental - the hybrid cloud product will be a boon for the company.

IBM | Fundamental Analysis | Must Read...IBM shares fell nearly 10 percent to a seven-month low on Oct. 21 after the tech behemoth released a weak Q3 report.

IBM's revenues rose just 0.3 percent from a year earlier to $17.6 billion, $190 million less than forecasts. But excluding divestitures and foreign exchange rates, the company's revenues were down 0.2%.

Excluding the impending Kyndryl spin-off, IBM's revenue was up 2.5% in the period. Excluding divested businesses and foreign exchange rates, "excluding Kyndryl" earnings were up 1.9%.

IBM's GAAP earnings, which include Kyndryl spin-off expenses, fell 34% to $1.25 per share. Non-GAAP earnings, which exclude those expenses, still fell 2% to $2.52 per share, but beat forecasts by one penny.

IBM's performance was unimpressive, but it was in line with the outlook the company presented at an investor briefing in early October. Did investors exaggerate IBM's disappointing third-quarter report and create a new buying opportunity?

As in previous quarters, IBM reported third-quarter earnings in five main segments: cloud and cognitive software, global business services, global technology services, systems, and global finance.

IBM's cloud and cognitive software revenues grew thanks to double-digit growth in its cloud-related business, which offset low growth in its applications business and lower revenues in its transaction processing business.

The global business services segment profited from strong demand for cloud services, consulting, application management, and global technology services.

However, the Global Technology Services division weakened again, as weak growth in cloud services could not offset the continued decline in the Managed Infrastructure Services segment, which will be taken out by the Kyndryl spin-off.

The company's systems division struggled because of cyclically declining sales of IBM Z and Power systems, and financing revenues declined amid lower demand for financing services and slow sales of used equipment.

Once again, IBM's strengths failed to offset vulnerabilities, and investors were left attempting to find positives in lackluster reporting segments. However, this may all change as the "old" IBM ceases to exist.

After IBM spins off from Kyndryl next week, it will present four new reporting segments: consulting (29% of continuing operations revenue in 2020), software (42%), infrastructure (25%), and finance (2%).

IBM thinks these four segments will make it easier for investors to track the expansion of its faster-growing businesses.

IBM expects the software segment, which includes Red Hat and other hybrid cloud and artificial intelligence services, to be a major growth driver.

It also probably anticipates a streamlined consulting segment to better stand up to faster IT services and consulting companies, such as Accenture and Globant.

IBM's infrastructure business, which includes the legacy systems business as well as other hardware products and services, is likely to remain underperforming. However, IBM's earnings outlook suggests that the company will focus on streamlining its business and cutting costs to improve margins.

IBM believes that after the Kyndryl spin-off, it will deliver "sustained mid-single-digit revenue growth" from 2022 to 2024.

The company believes this growth to be driven by the expansion of hybrid cloud and AI services that can be integrated with public cloud platforms such as Amazon Web Services (AWS) and Microsoft Azure.

IBM probably realizes that it is too late to catch up with AWS and Azure in the public cloud market, but it can still use its large enterprise customer base and Red Hat's open-source software to develop services for the hybrid cloud, which sits between private clouds and public cloud services.

IBM investors will get Kyndryl stock next month. If they keep both shares, they will initially receive a combined dividend equivalent to IBM's current dividend, but then both companies may reduce their payouts.

It would seem that IBM investors should sell their Kyndryl stock immediately since the latter would likely have difficulty keeping up with companies like Accenture, but hold onto their shares of a "renewed" IBM to see if its plans to get out of the crisis work.

Nevertheless, today is not a good time to buy IBM stock. Right now, the stock may seem cheap at 12 times forward earnings, but the company still faces stiff competition from Amazon and Microsoft, which are expanding their public clouds in a hybrid market, and an unstable infrastructure business could derail growth in its software and consulting business.

Investors should wait for IBM to complete its spin-off and for results to improve for a few quarters before believing that the tipping point has arrived. Until then, they should buy other blue-chip stocks, not Big Blue.

IBM dip buy comingIBM, leading up to previous earnings, formed a bearish divergence and gapped down. IBM has not been this oversold (RSI) since this time last year, and indicators show a strong bullish momentum. Hour timeframes shows that dip buying has started.

IBM analysistoday 10/21/2021 IBM's Results has been published less than the consensus and this made an impulsive bearish movement down to the historical zone mentioned in red color in the graphic , not only that , but also the 360 MA overlapped the zone and reacted as a support for the price

IBM post earnings Look for the dip buy around 130.50 - 130.80

seems were in a bear channel , possible breakout next earnings

IBM : CMP 142 Time to buy IBM...Completing Correction on Monthly Timeframe....IBM Is in Correction from 2012 .... Expected to complete this correction in next 3-6 months.... Short Term Traders can buy this target for 205 and longterm investor for target 400 in next 3 years....115 sl

Buying begets more buyingIBM price is quietly climbing higher. Years of price breakdown have finally led to a 2021 price breakout as highlighted by the green circle. My analysis shows some serious buying potential at these prices.

Fundamentally, businesses are being forced to migrate operations onto the cloud in order to survive and IBMs hybrid alternative is set to be an attractive option.