USDX trade ideas

$DXY - First signs of recovery, but no confirmation yet.To find confirmation, I would like to see a clean break of the blue Line on 1d or 3d chart and a bullish MacD cross.`

US dollar, a potential bullish divergence to watchThe US Federal Reserve (FED) recently updated its economic projections against a backdrop of growing uncertainty. It is now openly concerned about a scenario of stagflation, a combination of weak growth, persistent inflation and rising unemployment. This concern stems in particular from the as yet unquantified impact of the new tariffs imposed by the Trump administration, as well as rising geopolitical tensions, particularly in the Middle East.

Gloomy forecasts, but monetary policy still flexible

At its last meeting, the FED kept its key rate in the 4.25% - 4.5% range, while publishing gloomy forecasts for the US economy. By the end of 2025, it anticipates PCE inflation at around 3%, unemployment at 4.5% and moderate growth. Despite this worrying picture, the central bank is still planning two rate cuts this year, demonstrating its determination to support economic activity.

Nevertheless, this monetary stance is the subject of debate within the committee: ten members support the cuts, while seven believe that rates should remain unchanged. Jerome Powell, Chairman of the FED, advocates caution, insisting on the need to observe the evolution of economic data before acting, particularly in view of the delayed effects of tariffs.

The FED is faced with a dilemma: it must curb inflation without destroying growth. Its diagnosis of stagflation is harsh, but perhaps too pessimistic if inflation figures remain under control. A rate cut in September is still conceivable, but will largely depend on the evolution of geopolitical tensions and international trade in the weeks ahead.

Below, you can see the table with the latest update of the FED's macroeconomic projections

US dollar (DXY), a potential bullish technical divergence to be monitored

The FED's confirmed intransigence is having an impact on the foreign exchange market. While the US dollar has been the weakest Forex currency since the beginning of the year, it has been stabilizing for several weeks now. If the FED maintains its current wait-and-see stance on a resumption of Fed funds rate cuts, the US dollar could be close to a low point on the Forex market.

At present, there are no resistance breaches to suggest this, but a potential bullish technical divergence has appeared on the weekly timeframe. In the past, this signal was a precursor to a future rebound in the US dollar against a basket of major Forex currencies.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

DXY OUTLOOK - SWING SETUPThe dollar has been on a six-month decline, but I anticipate a recovery. This is primarily due to the current economic climate, geopolitical landscape, and the dollar's traditional role as a safe-haven currency during periods of significant uncertainty

"May fortune attend thee, and thy trade prosper." .......L2Earned

Politics is a show. Live watching the Federal Reserve Chair Jerome Powell News Conference

(FOMC Conference)

and at the same time,

Dollar just swept liquidity,

Hit EQ,

Filled 1hrFV Array,

Sent to buyside.

This is crazy.

Its all a game. Its not real.

Bullish bounce?US Dollar Index (DXY) is reacting off the pivot and could rise to the 1st resistance.

Pivot: 98.48

1st Support: 98.09

1st Resistance: 99.25

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

DXY: Bulls Are Winning! Long!

My dear friends,

Today we will analyse DXY together☺️

The recent price action suggests a shift in mid-term momentum. A break above the current local range around 98. 059 will confirm the new direction upwards with the target being the next key level of 98.148 and a reconvened placement of a stop-loss beyond the range.

❤️Sending you lots of Love and Hugs❤️

Dollar In Fifth Wave-Reversal In Trend May Not Be Far Away.The Fed will announce its latest policy decision later, and expectations are that Powell will keep rates on hold, especially after last week's slightly higher inflation print and still solid US jobs data. We can see some stabilization in the US dollar ahead of this event, but we have to keep an eye on geopolitical tensions in the Middle East, which coudl also play a key role in driving safe haven flows.

Meanwhile, the stock market continues to trade sideways, and I don't expect any major breakouts or strong moves ahead of the Fed. Also, tomorrow is a holiday in the US, so that could contribute to slower market conditions into the end of the week, unless, of course, the situation in the Middle East gets worse.

Looking at the DXY waves structure, I see athree-wave move from the most recent lows, so the fourth wave I highlighted a few days ago could now be approaching completion near this week’s key resistance around the 99 level. That’s definitely a level to watch for a potential fresh, but possibly final sell-off toward new lows around 97, maybe even 96.

That’s where the DXY could stabilize, as ending diagonal pattern signals that we are likely in the late stages of wave five, meaning this bearish cycle could soon come to an end.

dxy 1hr chart analaysis The current bullish trend in the DXY is likely to face a strong rejection around the 99.55–99.65 zone. Unless there is major news that significantly shifts the market direction — such as a surprise policy announcement like the tariffs introduced during Trump's era — the dollar index is not expected to break above that level. That zone could act as a major turning point, and a bearish reversal is likely to emerge from there

DXY 2H Analysis – June 18, 2025Pair : dxy ,,💲

Is the bullish move fading out? 📉

Price reacting near upper trendline resistance 🔵

Potential correction or final push before deeper drop ❗

Wave count suggests i–ii–iii–iv completed; wave v setup expected 🔁

Watch the reaction in the highlighted zone 📦

Either short continuation or a bullish trap loading 🧠

📌 Strategy: Elliott Wave + Trendline Confluence

📅 Stay sharp. Events approaching 📰

📈 Trade with a plan, not hope.

🔔 Follow @Greenfireforex for more real-time setups and ideas.

USXUSD LOTD SetLOTD Set

Looking for Unemployment Claims / FOMC Delivery Higher on USXUSD.

Nice buildup of Asia Highs below draw.

Let's see.

Dollar - Coming back into Consolidation (Short Term Bullish)Been following dollar with videos for over a month and we have been in sync from the highs highlited in the video. We hit our target last week and now looking for a short term bullish run on stops at 94.40s

Give us a follow. Support the channel. Videos are regular

Skeptic | DXY Crash Alert: Epic Bearish Triggers Unleashed!heyy, traders, what’s good? It’s Skeptic ! 😎 Let’s dive into a full-on breakdown of DXY—the Dollar Index is making waves, and I’m hyped to unpack it. The 98.801 level looks busted with a pullback in play, and I’m expecting more action. Stick with me to the end as we rip through Daily and 4-Hour timeframes to catch the vibe and nail those triggers! 🚖

Daily Timeframe: The Big Picture

So, US inflation data came in softer than expected recently, but DXY still dumped. You might be like, “Wait, shouldn’t lower inflation juice up the dollar?” Nah, here’s the deal: markets move on expectations, not just news. When something grows in the markets, it’s ‘cause traders are betting it’ll keep growing—and vice versa. For DXY, traders are sniffing out a US economic slowdown and expecting the Federal Reserve to cut rates soon, which could spark higher inflation later. That’s the double-whammy driving DXY’s drop, despite the tame inflation numbers. This is the biggest secret in markets—nobody talks about it, but it’s what I learned in econ class and see every day: markets run on expectations. 📚

Major Trend: Per Dow Theory, we’re in a bearish trend as long as we’re below 98.801 .

Game Plan: While under this level, hunt longs on USD pairs like EUR/USD. If we break above 98.801, chill and let the market reform before jumping in.

4-Hour Timeframe: Long & Short Triggers

Now, let’s get to the 4-hour chart for the real action—our long and short triggers:

Short Trigger: A break below support at 98.017 could keep the bearish vibe rolling. RSI hitting oversold would be a dope confirmation. 😤

Long Trigger: Since the major trend is bearish, longs are against the flow, so keep risk tight and take profits quick. The trigger is a break above 98.801, but the main long trigger is smashing through 99.244. So, 99.244 is your go-to for longs. 💪

Pro Tip: Shorts align with the trend, so they’re safer, but longs need extra caution—small positions, tight stops, and don’t get greedy!

Final Vibe Check

That’s the DXY lowdown, fam! Markets are tricky, but if you stick to reasoning over hype, you’ll stay ahead. No FOMO, no hype, just reason —that’s how we roll at Skeptic Lab. Wanna dive deeper into risk management or another pair? Let me know! 🙌

💬 Let’s Talk!

If this analysis got you pumped, smash that boost—it means a ton! 😊 Got a pair or setup you want me to tackle next? Drop it in the comments. Thanks for vibing with me—keep trading sharp! ✌️

DXY bullish here, sell XXXUSD! Do miss this trade plsAs per my previous post on dxy, I'm looking for higher prices now. I dont know the news or war or tariff or rate cut that will push it up. I'm just reporting what I'm seeing on the charts, most times, it doesn't lie. Just when everyone was bullish back in Jan, 2025. I turned bearish, now I'm telling you that we go up slowly or range.

This means you have to sell EURUSD, GBPUSD etc

TP1 @ 98.9

TP2 @ 99.4

Enjoy

Follow me and turn on notification so you'll see my trades on time and enter them on time

DXY June 18 2025We believe that Trump's tariffs and the downward trend in U.S. interest rates will continue to put pressure on the dollar, leading to further depreciation.

Monthly Target: 95.445-101.977

Bearish reversal?US Dollar Index (DXY) has reacted off the pivot and could drop to the 1st support.

Pivot: 98.89

1st Support: 98.29

1st Resistance: 99.60

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

DXYThe DXY has faced severe sell off due to President Trump's policy and idea of how the dollar should be controlled/managed. Though it has fallen, a pullback will happen soon. I will be using the DXY as a good guide for all the USD/XXX or XXX/USD pairs. You as a trader can take what you can from this.

These 4HR FVG'S seem like a very good place where you can do one of two things. First you may be able to manage and hold a trade throughout the whole pullback. Another option is take complete profits instead of partials and enter in at good prices with this pullback in mind for bias.

$DXYAs tensions rise in the Middle East, the dollar remains a safe haven.

We could see a temporary bullish run on the dollar as capital seeks safety.

But for me, Bitcoin was the first signal that smart money is shifting into alternative assets like Gold, Silver, and beyond.

Stay alert. The market speaks before the news does.

DXY OVERVIEW AND ANALYSIS - SELLOFF AT FOMC PRESS CONFERENCE 🟣DXY🟣 H4 CHART

As we witness the unfolding of a conflict in the Middle East this week I expect the commodities of OIL and GOLD to raise more after a pullback that will offer buy entries.

On my view the DXY index will pullback to the previous broken support now resistance in the 99.200 - 99.340 area and selloff to the weekly targets 97.500 and 96.800.

FOMC on Wednesday should catalyse this move and I expect the pullback to take place between the first days of the week

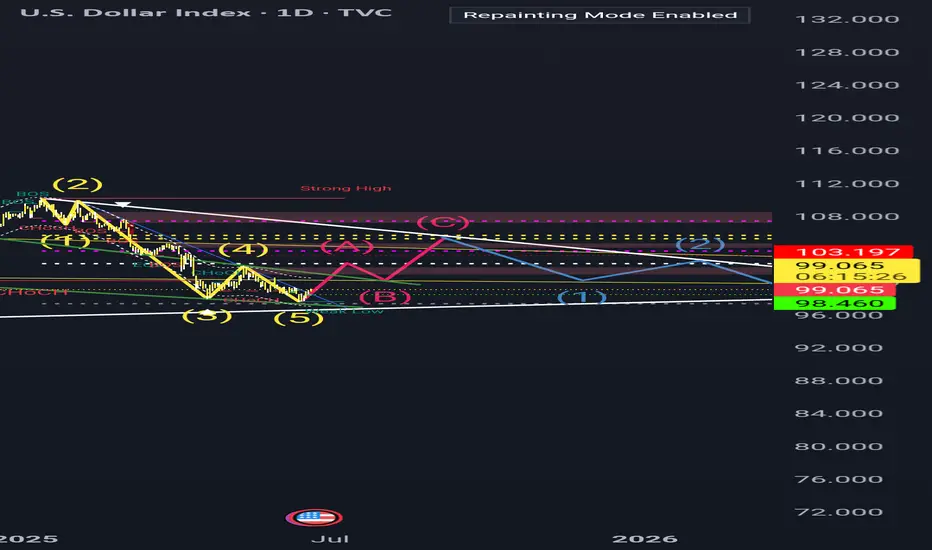

DXY Long term targetI think the IV wave is finished. now in 1-2 year dxy next target will be around 120. probably in 1 year.

Dollar consolidating - Still long term bearishLets see if the Daily Volume imbalance can hold price lower here. If it breaks higher then the clean highs will be a target for a sweep then return lower again. FOMC Tomorrow!! Stay safe

DXY: US dollar To Drop Further Around 95?The US dollar has been steadily declining since the new president was elected in the USA. This decline has been accompanied by the ongoing trade wars. Numerous economic indicators have supported this trend, and we anticipate further depreciation in the coming days or weeks. Before trading, it’s essential to conduct your own analysis and gain a comprehensive understanding of the market.

We wish you the best of success in trading. Good luck and trade safely.

Like and comment for more, and as always, happy trading!

Team Setupsfx_