Sell idea on GER40After receiving multiple breakthroughs listening to The mental game of trading

I’m starting to realize that the more I document the more I’m able to resolve

When we resolve, we recognize patterns

And when recognize patterns were able to stop the downward spiral

I noticed when I get frustrated, I tend to throw my rules out of the window

But before this, I felt really calm. I was able to clean and get things done.

I sat down in front of my computer and started to realize that we made a massive move to the downside

I drew a fib from high to low and noticed that we’re getting close to the 38% pull back

On the overall move on the daily timeframe till the upside

So we’re catching a piece of the pull back and we’re also going to be waiting for confirmation for the big move up

Tracking his key not just on my trading journal but publishing these ideas

DE40 trade ideas

Bearish drop?DAX40 (DE40) is reacting off the pivot which acts as a pullback resistance and could drop to the overlap support.

Pivot: 23,758.06

1st Support: 23,381.73

1st Resistance: 24,078.12

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

Bearish drop off pullback resistance?GER40 has reacted off the resistance level which is a pullback resistance that lines up with the 38.2% Fibonacci retracement and could drop from this level to our take profit.

Entry: 23,897.39

Why we like it:

There is a pullback resistance level that lines up with the 38.2% Fibonacci retracement.

Stop loss: 24,321.37

Why we like it:

There is a pullback resistance level that aligns with the 78.6% Fibonacci retracement.

Take profit: 23,138.29

Why we like it:

There is a pullback support level.

Enjoying your TradingView experience? Review us!

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Everest Fortune Group’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Everest Fortune Group.

GER 30 BUY OPPOTUNITYI am in a buy on GER30. I intend to add more position when the market breaks and retests the "BUYERS ZONE".

DAX INTRADAY at pivotal level Trend Overview:

The DAX Index remains in a bullish trend, supported by a series of higher highs and higher lows. The broader structure continues to favour the upside, although recent intraday price action suggests a sideways consolidation, signalling a potential pause within the prevailing uptrend.

Key Support and Resistance Levels:

Support: 23680 (key pivot), followed by 23445 and 23200

Resistance: 24570 (initial), then 24770 and 25000

Technical Outlook:

A pullback toward the 23680 support—which aligns with the prior consolidation zone—could offer a buying opportunity if price action confirms a bullish reversal from that level.

A sustained break above 24570 would likely accelerate bullish momentum, targeting 24770 and 25000 over the medium term.

Conversely, a daily close below 23680 would invalidate the bullish bias, exposing the index to a deeper retracement toward 23445 and potentially 23200.

Conclusion:

While the broader DAX trend remains bullish, traders should watch for price behavior around the 23680 level. A bounce could resume the uptrend toward 25000, but a confirmed breakdown would shift the short-term bias to bearish, signaling a deeper correction.

This communication is for informational purposes only and should not be viewed as any form of recommendation as to a particular course of action or as investment advice. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Opinions, estimates and assumptions expressed herein are made as of the date of this communication and are subject to change without notice. This communication has been prepared based upon information, including market prices, data and other information, believed to be reliable; however, Trade Nation does not warrant its completeness or accuracy. All market prices and market data contained in or attached to this communication are indicative and subject to change without notice.

DAX: Move Up Expected! Long!

My dear friends,

Today we will analyse DAX together☺️

The market is at an inflection zone and price has now reached an area around 23.976.69 where previous reversals or breakouts have occurred.And a price reaction that we are seeing on multiple timeframes here could signal the next move up so we can enter on confirmation, and target the next key level of 24.050.29. Stop-loss is recommended beyond the inflection zone.

❤️Sending you lots of Love and Hugs❤️

GER 40 (DAX) LONG TRADE IDEAGER40 (DAX) – Long Trade Idea

Timeframes:

Quarterly Bias: Bullish

Entry Execution: 1HR–4HR

Market Narrative:

The Quarterly outlook on GER40 remains bullish, and recent price action has confirmed alignment with this narrative:

Sell-side liquidity has been swept.

A clear bullish market structure shift has occurred.

Price is now likely to retest a Bullish Breaker Block near 23,995—an ideal area to look for long entries.

This setup presents a high-probability continuation move to the upside, targeting premium-side inefficiencies and liquidity.

Entry Zone:

🟢 Buy Zone: 23,995

Retest of the Bullish Breaker Block

Look for:

A bullish FVG or displacement candle on 1HR/4HR

BOS (Break of Structure) confirmation on lower timeframes

Entry after internal liquidity sweep (e.g., stop run below previous low)

Stop Loss:

🔴 SL: 23,900

Below Bullish Breaker and recent structure low

Invalidation point of the bullish thesis

Take Profit Levels:

TP1 – 24,265

🎯 Return to previous structural high & imbalance fill

TP2 – 24,360

🎯 Extended move into premium + likely liquidity draw above highs

Risk Management:

📊 Risk: 1% per trade

Maintain position sizing discipline

Use partial profits at TP1 and trail stop to breakeven or structure for TP2

Confluences:

Quarterly bullish bias remains intact

Sell-side liquidity sweep provides fuel for a bullish move

Market structure shift confirms smart money accumulation

Bullish Breaker Block in discounted territory presents a key entry opportunity

Price likely to seek buy-side liquidity in premium

Execution Plan:

Wait for price to return to 23,995 zone

Watch for confirmation on 15min–1HR:

Internal liquidity sweep

Bullish BOS or FVG

Entry on bullish displacement

Manage trade dynamically based on market behavior at TP1

The calm before the storm for Germany to 25,113W Formation formed on Germany and the price rallied up super well.

3/4s to the take profit, but then the inevitable consolidation phase kicked in and we've been waiting for the next breakout for when it breaks above the box.

So all other elements and conditions stay the same, we just need to be patient and let it run it's course.

Price>20 and 200

Target 25,113

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

DAX INTRADAY corrective pullback, Key level to watch 23680Trend Overview:

The DAX Index remains in a bullish trend, supported by a series of higher highs and higher lows. The broader structure continues to favour the upside, although recent intraday price action suggests a sideways consolidation, signalling a potential pause within the prevailing uptrend.

Key Support and Resistance Levels:

Support: 23680 (key pivot), followed by 23445 and 23200

Resistance: 24570 (initial), then 24770 and 25000

Technical Outlook:

A pullback toward the 23680 support—which aligns with the prior consolidation zone—could offer a buying opportunity if price action confirms a bullish reversal from that level.

A sustained break above 24570 would likely accelerate bullish momentum, targeting 24770 and 25000 over the medium term.

Conversely, a daily close below 23680 would invalidate the bullish bias, exposing the index to a deeper retracement toward 23445 and potentially 23200.

Conclusion:

While the broader DAX trend remains bullish, traders should watch for price behavior around the 23680 level. A bounce could resume the uptrend toward 25000, but a confirmed breakdown would shift the short-term bias to bearish, signaling a deeper correction.

This communication is for informational purposes only and should not be viewed as any form of recommendation as to a particular course of action or as investment advice. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Opinions, estimates and assumptions expressed herein are made as of the date of this communication and are subject to change without notice. This communication has been prepared based upon information, including market prices, data and other information, believed to be reliable; however, Trade Nation does not warrant its completeness or accuracy. All market prices and market data contained in or attached to this communication are indicative and subject to change without notice.

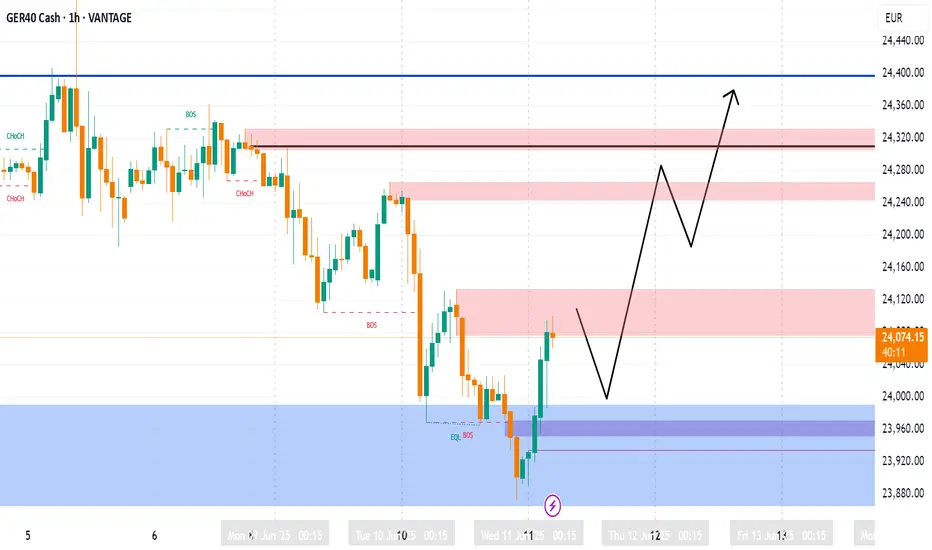

Bullish bounce off pullback support?GER40 has bounced off the support level which is a pullback support that aligns with the 50% Fibonacci retracement and could rise from this level to our take profit.

Entry: 24,101.42

Why we like it:

There is a pullback support level that lines up with the 50% Fibonacci retracement.

Stop loss: 23,934.55

Why we like it:

There is a pullback support level that is slightly above the 78.6% Fibonacci retracement.

Take profit: 24,396.66

Why we like it:

There is a pullback resistance level.

Enjoying your TradingView experience? Review us!

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Everest Fortune Group’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Everest Fortune Group.

Technical Weekly AnalysisStart your week by identifying the key price levels and trends.

The SpreadEx Research team has analysed the most popular markets, including stocks, indices, commodities & forex.

--------------------------------------------------------------------------------------------------------------

Analysis

Germany 40 remains in a bullish trend and is currently in an impulsive phase, trading at 24,202, slightly above its VWAP of 24,031. The RSI at 61.1 suggests steady buying interest. Support is at 23,641, with resistance at 24,422.

UK 100 continues in a bullish trend, trading at 8,833, above its VWAP of 8,760, indicating underlying strength. The RSI at 63.9 supports ongoing momentum. Support is at 8,679, with resistance at 8,850.

Wall Street remains in a bullish trend and is currently in an impulsive phase, trading at 42,806, above its VWAP of 42,235. The RSI of 61.8 indicates sustained buying strength. Support is at 41,513, with resistance at 42,857.

Brent Crude is in a neutral consolidation phase, trading at 6,628, slightly above its VWAP of 6,464, indicating tight price action. The RSI at 58.4 suggests a balanced market outlook. Support is at 6,268, with resistance at 6,640.

Gold remains in a neutral consolidation phase, trading at 3,320, marginally above its VWAP of 3,310, indicating cautious market interest. The RSI at 51.4 points to a neutral stance. Support is at 3,231, with resistance at 3,396.

EUR/USD is in a bullish trend but in a consolidation phase, trading at 1.1434, slightly above its VWAP of 1.1347. The RSI at 58.5 indicates steady buying interest. Support is at 1.1208, with resistance at 1.1486.

GBP/USD is in a bullish impulsive phase, trading at 1.3573, above its VWAP of 1.3481, confirming ongoing strength. The RSI at 62.3 shows solid bullish momentum. Support is at 1.3328, with resistance at 1.3636.

USD/JPY is currently in a neutral consolidation phase, trading at 144.04, matching its VWAP of 144.00. The RSI at 49.3 points to a neutral tone. Support is at 142.24, with resistance at 145.61.

New Week New Trades with Pinex CaptialWe have built a strong zone on the Dax where we can expect a reaction downwards if we pay attention to the current topics in the world and we still have the cap that we would like to fill I think this week is the right time for it we are getting weaker and weaker at the ATH so if you want to long watch your money ^^ Cheers

Drop followed by riseDax is currently ranging and may drop towards the 24,000 due to failing to settle above 24,300 and continue upwards. If price action manages to go beyond 24,3k zone, the indice will probably be bullish until the bulls run out of steam. If price remains under the 24,300 zone, a bearish lens is favourable.

2 TRAPS - 2H chartHere you can see - looked for sells after bull traps.

Then look for buys after bear traps….

Hope you can see the potential - and if you use this indicator in conjunction with the other one we have fo ryou guys that confirm buy and sell entries as per previous examples.

You should have no excuse in doing well.

Longs - after TRAPHere is the last example for the week….

You can see that you can go on any timeframe to find potential bias for what moves can be up next.

Here on 45min chart we had b bear trap warning…. Meaning after this we need to find BUY trades only.

And look what move came from that….

DE40 – Buy the Dip Near Support & EMA ConfluenceTrade Idea

Type: Buy Limit

Entry: 24,171

Target: 24,555

Stop Loss: 24,039

Duration: Intraday

Expires: 06/06/2025 07:00

Technical Overview

Intraday dips continue to attract buyers, reinforcing the strength of the ongoing uptrend.

Price action is consolidating near all-time highs, with former resistance at 24,170 now acting as support.

The 20-period 4H EMA sits at 24,162, reinforcing this level as a dynamic support zone.

With no technical signs of exhaustion, the strategy is to buy into weakness, aiming for a breakout continuation toward 24,555.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

DAXINTRADAY bullish breakout supported at 23680Trend Overview:

The DAX Index remains in a bullish trend, supported by a series of higher highs and higher lows. The broader structure continues to favor the upside, although recent intraday price action suggests a sideways consolidation, signaling a potential pause within the prevailing uptrend.

Key Support and Resistance Levels:

Support: 23680 (key pivot), followed by 23445 and 23200

Resistance: 24570 (initial), then 24770 and 25000

Technical Outlook:

A pullback toward the 23680 support—which aligns with the prior consolidation zone—could offer a buying opportunity if price action confirms a bullish reversal from that level.

A sustained break above 24570 would likely accelerate bullish momentum, targeting 24770 and 25000 over the medium term.

Conversely, a daily close below 23680 would invalidate the bullish bias, exposing the index to a deeper retracement toward 23445 and potentially 23200.

Conclusion:

While the broader DAX trend remains bullish, traders should watch for price behavior around the 23680 level. A bounce could resume the uptrend toward 25000, but a confirmed breakdown would shift the short-term bias to bearish, signaling a deeper correction.

This communication is for informational purposes only and should not be viewed as any form of recommendation as to a particular course of action or as investment advice. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Opinions, estimates and assumptions expressed herein are made as of the date of this communication and are subject to change without notice. This communication has been prepared based upon information, including market prices, data and other information, believed to be reliable; however, Trade Nation does not warrant its completeness or accuracy. All market prices and market data contained in or attached to this communication are indicative and subject to change without notice.

DAX H4 | Bullish uptrend to extend higher?The DAX (GER30) is falling towards a swing-low support and could potentially bounce off this level to climb higher.

Buy entry is at 23,765.39 which is a swing-low support.

Stop loss is at 23,200.00 which is a level that lies underneath an overlap support.

Take profit is at 24,732.86 which is a resistance that aligns with the 127.2% Fibonacci extension.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Stratos Markets Limited (tradu.com ):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 63% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Europe Ltd (tradu.com ):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 63% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Global LLC (tradu.com ):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to Tradu (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of Tradu and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of Tradu or any form of personal or investment advice. Tradu neither endorses nor guarantees offerings of third-party speakers, nor is Tradu responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

DAX: Bulls Are Winning! Long!

My dear friends,

Today we will analyse DAX together☺️

The price is near a wide key level

and the pair is approaching a significant decision level of 24,262.29 Therefore, a strong bullish reaction here could determine the next move up.We will watch for a confirmation candle, and then target the next key level of 24,423.36.Recommend Stop-loss is beyond the current level.

❤️Sending you lots of Love and Hugs❤️

GER40 Trading Plan: Ride the Wave or Get Trapped?🚨 DE40 Heist Alert: The Bullish Breakout Robbery Plan (Swing & Scalp Strategy) 🚨

🌟 Hi! Hola! Ola! Bonjour! Hallo! Marhaba! 🌟

Attention Money Makers & Market Robbers! 🤑💰💸

Based on the 🔥Thief Trading Style🔥, here’s our master plan to loot the DE40 / GER40 "Germany40" Index. Follow the strategy on the chart—focusing on LONG entries—and escape near the high-risk Red Zone. This area is overbought, consolidating, and a potential reversal trap where bears lurk. 🏆 Take profits fast—you’ve earned it! 💪

🎯 Heist Entries:

📈 Entry 1: "The Breakout Heist!" – Wait for Resistance (24200) to break, then strike! Bullish profits await.

📈 Entry 2: "Big Players’ Pullback!" – Jump in at 23300+ for a safer steal.

🔔 Pro Tip: Set a chart alert to catch the breakout instantly!

🛑 Stop Loss Rules:

*"Yo, listen! 🗣️ If you’re entering with a buy-stop, DON’T set your SL until AFTER the breakout. Place it at the nearest swing low (4H timeframe) or wherever your risk allows—but remember, rebels risk more! 🔥"*

🏴☠️ Target: 24,800

🧲 Scalpers: Only play LONG! Use trailing SL to lock in profits. Big wallets? Go all in. Small stacks? Join the swing heist!

📊 Market Pulse:

The DE40 is neutral but primed for bullish momentum. Watch:

Fundamentals (COT, Macro, Geopolitics)

Sentiment & Intermarket Trends

Positioning & Future Targets

📌 Check our bioo linkks for deep analysis! 🔗🌍

⚠️ Trading Alert:

News = Volatility! Protect your loot:

Avoid new trades during major news

Use trailing stops to secure profits

💥 Boost This Heist!

Hit 👍 & 🔄 to strengthen our robbery crew! Let’s dominate the market daily with the Thief Trading Style. 🚀💵

Stay tuned—another heist drops soon! 🎯🐱👤

DAX INTRADAY Bullish sideways consolidation Trend Overview:

The DAX Index remains in a bullish trend, supported by a series of higher highs and higher lows. The broader structure continues to favor the upside, although recent intraday price action suggests a sideways consolidation, signaling a potential pause within the prevailing uptrend.

Key Support and Resistance Levels:

Support: 23680 (key pivot), followed by 23445 and 23200

Resistance: 24570 (initial), then 24770 and 25000

Technical Outlook:

A pullback toward the 23680 support—which aligns with the prior consolidation zone—could offer a buying opportunity if price action confirms a bullish reversal from that level.

A sustained break above 24570 would likely accelerate bullish momentum, targeting 24770 and 25000 over the medium term.

Conversely, a daily close below 23680 would invalidate the bullish bias, exposing the index to a deeper retracement toward 23445 and potentially 23200.

Conclusion:

While the broader DAX trend remains bullish, traders should watch for price behavior around the 23680 level. A bounce could resume the uptrend toward 25000, but a confirmed breakdown would shift the short-term bias to bearish, signaling a deeper correction.

This communication is for informational purposes only and should not be viewed as any form of recommendation as to a particular course of action or as investment advice. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Opinions, estimates and assumptions expressed herein are made as of the date of this communication and are subject to change without notice. This communication has been prepared based upon information, including market prices, data and other information, believed to be reliable; however, Trade Nation does not warrant its completeness or accuracy. All market prices and market data contained in or attached to this communication are indicative and subject to change without notice.