Recession indicator #2 Just realized that measuring the spread between TVC:US02Y and FRED:FEDFUNDS gives you a pretty accurate heads up of looming recessions. We might be in one from a few months now.

US10Y trade ideas

US 10Y TREASURY: rollercoaster, againMarket movements in a previous period are clearly showing how high uncertainty is currently among market participants. The US Treasuries for one more time took the downtrend during the previous week, clearly testing the 4,2% level with 10Y US benchmark, but Fridays better than expected jobs report, was a trigger for a move back toward the higher grounds. The lowest weekly level of 10Y yields was 4,13% on Thursday, however, the rest of the trading week the market was looking at the upside. The strong move up, brought the 10Y yields toward the level of 4,30% where yields have closed the trading week.

The volatility might continue also during the week ahead. The FOMC meeting is scheduled for May 6-7th, while on Wednesday will be the interest rate decision day, and also Fed Chair Powell's address to the public. As per current market expectations, as posted by the CME Group FedWatch Tool, the Fed could leave interest rates unchanged at this meeting, considering stronger than expected jobs data posted during this week. In addition, the market is expecting that the Fed will not change interest rates until their meeting in July. At the same time, analysts are noting that it is too early to see the reflection of trade tariffs in real economy, concretely in jobs data, in which sense, they are taking precaution with current strong jobs data. In this sense, the Fed Chair Powell's speech, after the FOMC meeting will be closely watched by markets, for a standing of Fed on the current state of the US economy as well as their view on tariffs repercussions in the future period.

US10Y - April ReviewWhenever we are faced with a market that is consolidating, it's best to lower your leverage and aim for low hanging fruits.

Gun to my head, I would like to see a bullish draw to 4.440% but after that price is met, anything goes!

10Y Note Auction & Why Markets did %10 Movement with Last Data?Hello Traders tomorrow we have 10-Year Note Auction data and I wanted to prepare a nice little information for you about this topic because the data released last month showed an immediate 10% increase and from what I saw, many people had no idea what was happening.

📌 What is the 10-Year Note Auction?

The U.S. government regularly issues 10-year Treasury notes to finance its budget. The auction result reflects investor demand and long-term interest rate expectations. The yield (interest rate) that results from the auction is a key benchmark for financial markets globally.

🔄 Connection to U.S. Stocks and EUR/USD

🟢 If Demand Is Strong (Yields Stay Low):

Investors are eager to buy U.S. debt, pushing prices up and yields down.

This indicates confidence in the U.S. economy and little concern about inflation or rate hikes.

Stock markets generally react positively.

🔴 If Demand Is Weak (Yields Rise):

Investors require higher returns, possibly due to inflation fears or policy tightening expectations.

This pushes yields up, increasing borrowing costs and reducing the attractiveness of risk assets.

Stocks typically decline, and the dollar strengthens.

💱 Effect on EUR/USD

🟢 If Yields Rise:

U.S. dollar becomes more attractive due to higher returns.

Investors buy USD to invest in Treasuries.

EUR/USD typically falls.

🔴 If Yields Fall:

Lower yields reduce the appeal of the dollar.

Investors may move capital elsewhere.

EUR/USD tends to rise.

🗓️ Latest 10-Year Treasury Auction – April 9, 2025

Auction Size: $39 billion

High Yield: 4.435%

Expected (WI) Yield: 4.465%

Outcome: Strong demand – yield came in lower than expected.

📊 Post-Auction Market Reactions

🔹 10Y Treasury Yield:

Before auction: ~4.466%

After auction: Dropped to ~4.38%

➝ Reflects strong investor demand and confidence in long-term stability.

🔹 S&P 500 Index:

Lower yields reduce borrowing costs and support equity valuations.

Investors often shift toward riskier assets like stocks when yields fall.

The S&P 500 responded positively after the auction.

🔹 EUR/USD:

Falling yields reduce the dollar's relative appeal.

This may push EUR/USD higher, depending on other macroeconomic influences (like ECB policy or geopolitical risks).

✅ Conclusion

The April 9, 2025, 10-year Treasury auction showed strong demand with a yield lower than market expectations. This led to a drop in yields, a positive reaction in U.S. stock markets, and potential downward pressure on the dollar, which may support EUR/USD.

US10YA bond is essentially a loan made by an investor to a borrower, which can be a government or a corporation. It is a fixed-income financial instrument where the borrower agrees to pay back the principal amount (face value) on a specified maturity date and usually makes periodic interest payments called coupons to the bondholder.

What Is a Government Bond?

A government bond is a type of bond issued by a national government to raise funds. When you buy a government bond, you are lending money to the government in exchange for regular interest payments and the return of the bond’s face value at maturity. These bonds are often considered low-risk because they are backed by the government’s credit and taxing power.

Why Do Governments Offer Bonds?

Governments issue bonds primarily to:

Finance Fiscal Deficits: Bonds help cover budget shortfalls without immediately raising taxes or cutting spending.

Fund Public Projects: Money raised can be used for infrastructure, schools, hospitals, and other public services.

Manage Debt: Governments use bonds to refinance maturing debt or restructure their debt profile.

Control Monetary Policy: Central banks may buy or sell government bonds to influence money supply and interest rates.

Develop Financial Markets: Issuing bonds establishes benchmark yields that help price other financial instruments and deepen capital markets

Provide Investment Opportunities: Bonds offer a relatively safe investment option, encouraging savings and investment within the economy.

Summary

Aspect Explanation

Bond A loan from an investor to a borrower with interest payments

Government Bond Debt security issued by a government to fund spending

Why Issued To finance deficits, fund projects, manage debt, and control monetary policy

Risk Level Generally low risk due to government backing

Investor Benefit Periodic interest (coupon) and principal repayment at maturity

In short, government bonds are a crucial tool for governments to raise capital sustainably while providing investors with a relatively safe income stream.

Difference Between Bond Yield and Bond Price and Their Effect on the US Dollar

Bond Price vs. Bond Yield: The Inverse Relationship

Bond Price is the current market value or price investors pay to buy a bond. It can be above (premium), below (discount), or equal to the bond’s face (par) value.

Bond Yield is the return an investor earns on a bond, expressed as a percentage. It reflects the income from coupon payments relative to the bond’s current price, and can be calculated as the current yield or yield to maturity.

Key point: Bond price and bond yield move in opposite directions.

When bond prices rise, yields fall because the fixed coupon payments represent a smaller return relative to the higher price paid.

When bond prices fall, yields rise to compensate investors for the lower price paid for the same fixed coupon payments.

Why This Happens

If interest rates in the market increase, new bonds offer higher coupon rates. Existing bonds with lower coupons become less attractive, so their prices drop to increase their effective yield to match market rates. Conversely, if interest rates fall, existing bonds with higher coupons become more valuable, pushing their prices up and yields down.

How Bond Yields and Prices Affect the US Dollar

Higher US Treasury Yields (rising yields due to falling bond prices) tend to strengthen the US dollar. This is because higher yields attract foreign investors seeking better returns on US debt, increasing demand for USD to buy Treasuries.

Conversely, falling yields (rising bond prices) make US assets less attractive, potentially weakening the USD as capital flows out or seek higher returns elsewhere.

The US Dollar Index (DXY) often moves in tandem with US Treasury yields because both reflect investor sentiment about US economic strength, inflation expectations, and Federal Reserve policy.

When the Fed raises interest rates, bond yields typically rise, boosting the USD. When the Fed cuts rates, yields fall, putting downward pressure on the USD.

In essence: When bond prices fall and yields rise, the US dollar tends to strengthen due to increased demand for higher-yielding US assets. Conversely, rising bond prices and falling yields usually weaken the dollar.

$US10Y making new lows. 4% upcoming. 3.5% target low.TVC:US10Y is going through a volatile period. After ‘Liberation Day’ the standard deviation if the movements in the TVC:US10Y has gone up significantly affecting the Equity and Bond indexes. This has been volatility story for the last 1-2 months. Now we are touching the midpoint of the downward sloping parallel channel which lies at 4.1 %. On the medium term the downward sloping channel indicates we can touch the Midpoint of 4.0 %.

The downward spiral in the rates will continue for the foreseeable future because the Fed will decrease rates, and this will put pressure on the $US10Y. In the long term the rates will touch 3.5% by end of the year.

Verdict: TVC:US10Y to 4% in near term and 3.5% by Dec 2025. Short $US10Y.

Macro Bullish Rates?An over simplification? I hope so.

The narrative fits too close for me. Needless to say, it's worth keeping an eye on.

If we manage to keep interest rates low for a while but inflation creeps in again (not due to high demand but because of monetary inflation) I can see the debt spiral scenario playing out in full force. This is a chilling thought, not something my generation has been exposed to and I believe it could have a very different impact to the population than the previous cycle. The difference being of course, the inflation not being demand driven but monetary debasement driven. To me this practically means a more impoverished population that is already struggling and those holding assets will further increase their portion of the pie.

There are a lot of unknows for me, as I basically know nothing about this. These are just my back of napkin thoughts. Me, trying to make sense of the world we live in because I know you can't look to anyone for the answer. Why? Frankly, I have learned that 98% of us don't know anything.

Ps - I am still not taking the deflationary narrative play off the table. Population decline, low interest rates and using robots to increase GDP etc. But either way all I can see is a exponential increase in debt creation. What other option is there? Both scenarios can't possibly lead to the same outcome, can they?

10 Yr Bond Yield breaks downtrend & then falls back into it!10 Yr Bond yields seem to have topped after that massive 1 week run. That was an impressive run! TVC:TNX

Even though the downtrend was broken, the 10Yr Yield put in a LOWER high.

We can also see that the recent uptrend was violated, back in a down trend.

Short term interest rates look worse!

US10Y - Higher Probability Times Are to Come Soon!Throughout this month, its been nothing but indecision in the markets and it does not look like anything will change anytime soon!

With the reciprocal tariffs running rampant throughout the economy, investors and traders cannot make up their mind whether they want to be a buyer or seller.

Best thing to do is sit on your hands and be patient as market conditions like this have the power of ripping your face off!

US 10Y TREASURY: NFP and jobs data ahead There has been another pullback in the 10Y US Treasury yields during the previous week. It comes as a result of investors' anticipation that the trade war between the US and China might soon be finalized. However, this sentiment is again based on mixed signals coming from the US Administration during the previous week. What will be the final result, no one actually knows, not even the US Administration, as per some analysts. The US President is still putting pressures on Fed Chair Powell to lower interest rates, which he noted on several occasions in interviews.

Anyway, the data show that the 10Y US yields started the previous week around 4,42% and dropped during the rest of the week to the Fridays level of 4,25%. Certainly, as long as the US Administration is using the push-and-pull strategy regarding trade tariffs, the market volatility will continue. And it is not only the US Treasury bond market, but also prices of equities and gold. As per technical analysis, the 4,2% level is the supporting level for the 10Y yields, which will be tested again in the week ahead. Still, it should be considered that the US NFP and jobs data will be released, where Friday is again day to closely watch, as it might bring for one more time a surprisingly volatile trading day.

Rates - Trend to Continue UpWhile rates soften after a recent surge, the 10 month moving average will likely continue to rise over time. Paring back on rate sensitive stocks seems like a good idea going forward.

Interest Rates don't seem to want to slow downWe believed that interest rates were going higher in Early April/Late March.

The Bullish Engulfing formation was a sign that higher interest rates were coming TVC:TNX

The 10 Yr Yield Downtrend was broken, it retraced some, we posted that it was likely consolidating, & seems to want to go a little higher.

Central Banks worldwide are lowering rates while the US is raising them.

---

Please see our profile for more info... We do post a lot.

US 10Y TREASURY: just a short correctionTariffs continue to be the major market concern, considering its potential impact on inflation, and at the last distance - the decision of the Fed to cut interest rates during the course of this year. The US Administration continues to urge the Fed to cut interest rates, noting that this is the right moment for such a move, while Fed Chair Powell refuses to comment. However, during the previous week, Powell publicly noted that the US economy might be hurt with tariffs in terms of higher inflation. This was not something that the markets were happy to hear, as it meant the possibility of even no rate cuts during the course of this year. The US Treasury yields reacted to this comment from Powell, bringing back volatility to the bond market.

The 10Y US Treasury benchmark started the week around 4,48%, and was traded toward the downside during the course of the week. The lowest weekly level was achieved on Wednesday, at 4,27%, but the reversal came on Thursday, when yields reverted back toward the 4,33%. Analysts are still cautious to bring their revised forecast for the US economy. Firstly, because the tariffs are so uncertain, and change almost on a daily basis, where it is extremely hard to bring into the light forecast of their impact on the US economy. However, as long as the US Administration uses tariffs narrative, the volatility on the market will continue.

10-Year Treasury Yield: Final Move Before Collapse?

The 10-year US Treasury Yield, once the benchmark of global confidence, is now exhibiting signs of a macro top. Since its 2020 low of 0.333%, it surged to 5.00% in October 2023, marking the end of the 40-year bond bull market. It now trades around 4.20%—a key Fibonacci confluence zone and the March 2025 breakout retest area.

A breakdown below 3.95%–3.82% could trigger a cascade to:

3.30%

3.16%

2.85% and 2.63%

This would imply disinflation, economic contraction, or systemic bond market stress.

The consequence? Institutional investors are diversifying out of bonds—once considered the safest asset class—and looking for alternative long-duration stores of value.

Gold has always been the traditional hedge. But now, with Bitcoin's price stabilizing and institutional credibility growing, it's being seriously considered as a digital parallel to gold.

US10Y - 90 Day Halt On Tariffs Rattles The Market!Extreme levels of volatility has ensued after the news was released that tariffs will be held for 90 days.

When will we see the return of the norm?

US 10Y TREASURY: to be or not to be – recessionMarket uncertainty continues to be supported with tariffs-narrative induced by US Administration and other world governments. The tariffs-war intensified between the US and China, bringing them to the level of absurdity. The fear of stagflation is for one more time active on financial markets. The 10Y Treasury yields ended one more week at higher grounds. They started the week around 3,87% and ended it at 4,49%. The highest weekly level was reached on Friday, at the level of 4,58%. As analysts involved in a matter noted, the highest sellers of US Treasuries were China and Japan.

The tariffs-war is currently disrupting the market. This sentiment does not have anything to do with current macro data and anticipation on future monetary policy. It has to do with a perception of investors regarding future effects of currently imposed tariffs, which are changeable on a daily basis. The sentiment is the one that is supporting extreme volatilities, as markets face it for the last few weeks now. In the future period, this will all settle down, and the market will find its equilibrium level. It is just a game of nerves at this moment.

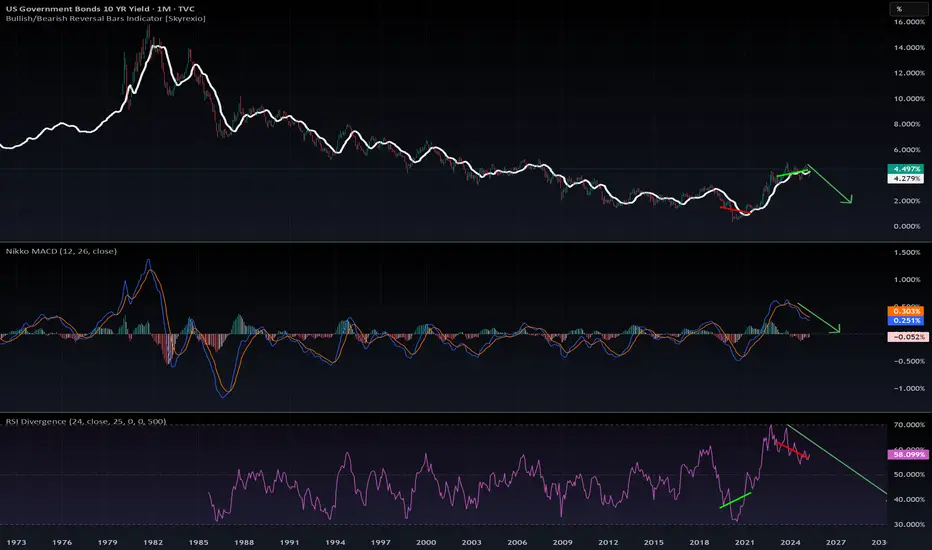

10YR Bond Yields: Panic on LTF, Calm on HTF📉 10YR Bond Yields: Panic on LTF, Calm on HTF

Yes, the recent spike in the 10-Year Yield is causing some short-term panic. But if you zoom out to the monthly timeframe, the bigger picture looks far more constructive.

🔍 Here’s what the chart says:

The MACD and RSI on the monthly are both pointing down.

Yields touched 4.5%, historically a key recession threshold.

We’re now seeing a MACD bearish crossover and a clear bearish divergence—classic signs of a trend reversal.

💡 What does this mean?

If no new fear or shock hits the market, yields are likely headed down, potentially toward the 2% range in the coming months. This would naturally ease pressure on equities and crypto.

📉 Conclusion:

This recent spike in yields seems to be transitional, not structural.

The chart suggests that the top is in, and the market is correcting from an overextended zone.

The Fed might not even need to intervene—the bond market is likely to correct on its own.

Stay calm. Stay rational. Always zoom out.

#10YearYield #BondMarket #MacroAnalysis #InterestRates #RecessionWatch #MarketPanic #MACD #TechnicalAnalysis #FederalReserve #CryptoMarkets #StockMarketInsights #StayCalmZoomOut #DYOR

10Y Bond Yield Long (Bond Short): Another recession signal?Take note that I do have a bias on when analyzing the bond yield. But the counts are valid nonetheless, except that another leg down is also valid (as briefly mentioned). Take this as a part 2 to the multi-assets analysis that I made on 11th April.

The 10 Year: When Should We Worry?All over the media eyes are on yields but what exactly do the different potential rates of the 10-year yield mean in terms of debt servicing for the United States? I made this chart to visualize the danger points.

I am not saying I think we will get there I just wanted to know myself and help others to understand what each pain point can mean to the United States economy.

PPI Misses Across the Board — Rate Cut Setup StrengthensFresh inflation data just gave the market a clear signal: the Fed has room to cut sooner than expected.

PPI Snapshot (Actual vs. Forecast):

PPI MoM: -0.4% vs. 0.2% ✅

Core PPI MoM: -0.1% vs. 0.3% ✅

PPI YoY: 2.7% vs. 3.3% ✅

Core PPI YoY: 3.3% vs. 3.6% ✅

PPI ex Food/Energy/Trade YoY: 3.4% vs. 3.5% ✅

🧠 Prices aren’t just slowing — they’re contracting. Combined with soft CPI, this disinflation confirms a Fed-friendly trend and clears the way for policy easing.

🧨 The Twist: 10-Year Yield Spiked

Despite stocks falling, the 10-year yield moved up — a rare divergence in risk-off environments.

This likely reflects three key forces:

Hedge funds facing margin calls, forced to liquidate bond positions.

Political actors unloading treasuries amid U.S. fiscal tensions.

A potential counter-strike to Trump’s efforts to push yields down via market stress.

💡 Ironically, this may help the Fed. Rising yields tighten financial conditions on their own, giving Powell more space to act without risking an inflation resurgence.

🧭 Sector Playbook (Macro-Aligned)

Tech and Growth — Overweight. These sectors thrive on falling rates and an easing narrative.

Bonds — Accumulate. Yield spike could offer a prime entry point before a Fed pivot.

Crypto — Risk-On. Disinflation + volatility = breakout fuel.

Energy and Defense — Hold. May underperform in a growth-led rally (Besides nuclear).

Defensives — Underweight. Safety trade could unwind as liquidity improves.

Small Caps — Speculative. Could bounce hard if liquidity rotation begins.

⚠️ Final Thought

Markets are digesting short-term chaos, but underneath it all, the macro signals are aligning. Even without a "golden tweet," the inflation data is giving Powell the green light.

If the Fed wants to cut — the data is here. The only thing missing is confirmation from Powell’s tone.

#Disinflation #FedCut #YieldSpike #MacroUpdate #CPI #BondMarket #TradingViewIdeas #MarketOutlook #SectorRotation

Double top in equities in 2025 as per 2006-2007 fractal1. This fractal follows the 2006-2007 cycle using US10Y (leading indicator).

2. The orange lines denote a peak in SPY. In this case, a second top in equities this cycle is expected in late Q4 2025, or early 2026 (latest).

3. The bottom in equities appear to be circa Q4 2026, or Q1 2027. Qualitatively, this could point to the house flipping blue.

4. Interestingly, this chart expects a short-term spike in US10Y before its eventual descent to just under 3% by 2027. We may have already seeing this spike in April 2025 ala tariffs.

5. Technical recession is pretty much already on its way. 2026 will not be kind.

6. AMEX:GLD and US Treasury Bonds ( NASDAQ:TLT AMEX:TMF ) will likely be fantastic safe havens.

7. BTC is tethered to SPY, so watch the cycle closely. Liquidate your alt portfolio by 2026.

8. DXY is expected to perform poorly with targets of 95, 85 and 75.

9. We want China to do well but avoid China like the plague.

US yeilds in a corrective rebound In analysis from a few weeks back, we talked about bearish USD and presented a bearish outlook. Since then dollar fall nicely and one of the reason are also lower US yields.

Looking at US yeilds I see bearish impulsive price action down from 4.8%, which could keep the US dollar in a downtrend. What we’ve seen so far is a strong rebound from 3.8%, as shown on the updated 4-hour chart. This rebound suggests that yields are stepping into a correction now, which could unfold as an A-B-C structure. So, it looks like we could see a bit more upside in the near term before US yields turn back to the downside. At the same time, this could mean the US dollar may find some support soon or remain in consolidation a bit longer.

GH