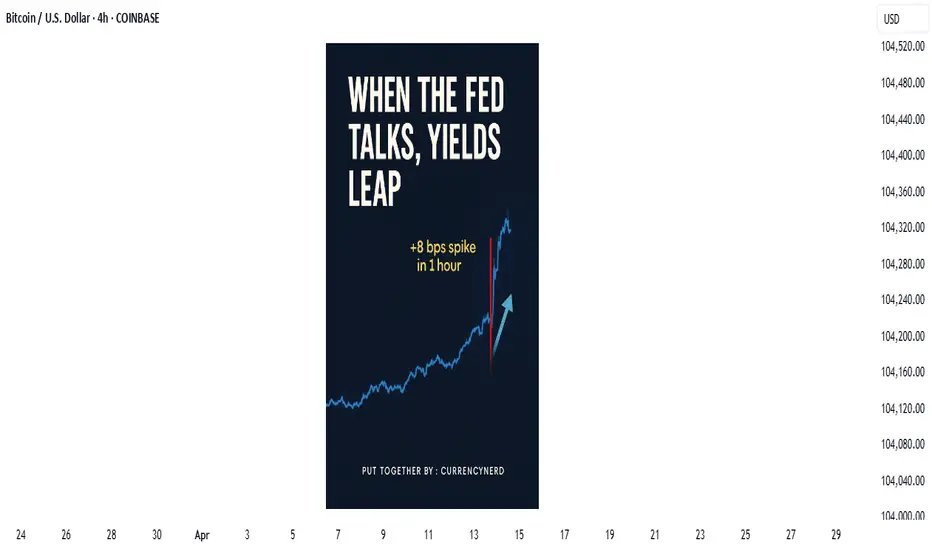

when Jerome says spike, the markets asks how low/high"Watch what they do, but also how they say it."

In the high-stakes world of central banking, few things move markets like the subtle wording of a Fed statement, But beyond the headlines and soundbites, one market absorbs this information faster—and with greater clarity—than almost any other: the bond market.

💬 What Is "Fed Speak"?

"Fed speak" refers to the nuanced and often deliberately vague language used by U.S. Federal Reserve officials when communicating policy expectations. It includes:

FOMC statements

Dot plot projections

Press conferences

Individual speeches from Fed officials

nerdy tip: the Fed aims to influence expectations without committing to specific outcomes, maintaining flexibility while steering market psychology.

📈 The Bond Market as a Decoder

The bond market, particularly the U.S. Treasury market, is where real-time interpretation of Fed policy plays out. Here's how it typically reacts:

1. Short-Term Yields (2Y, 3M) = Fed Expectation Barometer

These are the most sensitive to near-term interest rate expectations. If the Fed sounds hawkish (more rate hikes), short-term yields jump. If dovish (hinting cuts), they fall. At the May 7, 2025 FOMC meeting, the 2-year Treasury yield (US02Y) experienced a modest but clear reaction:

Just before the release, yields were hovering around 3.79%.

In the first hour following the 2:00 PM ET (20:00 UTC+2) statement, the yield ticked up by approximately +8 basis points, temporarily reaching about 3.87%.

Later that day, it eased back to around 3.79%, ending the day roughly unchanged—a sharp, immediate spike followed by a reversion.

2. Long-Term Yields (10Y, 30Y) = Growth + Inflation Expectations

Longer-dated yields reflect how the market sees the economy unfolding over time. After a Fed speech:

Rising long-term yields = stronger growth/inflation expected

Falling yields = fears of recession, disinflation, or policy over-tightening

3. The Yield Curve = Market's Policy Verdict

One of the best tools to read the bond market's verdict is the yield curve—specifically, the spread between 10Y and 2Y yields.

Steepening curve → Market thinks growth is picking up (Fed may be behind the curve)

Flattening or Inversion → Market believes the Fed is too aggressive, risking a slowdown or recession

📉 Example: After Jerome Powell’s hawkish Jackson Hole speech in 2022, the 2Y-10Y spread inverted deeply—markets were pricing in recession risks despite a strong Fed tone.

🧠 Why Traders Must Watch Bonds After Fed Speak

🪙 FX Traders:

Higher yields = stronger USD (carry trade advantage)

Falling yields = weaker USD (lower return for holding)

📈 Equity Traders:

Rising yields = pressure on tech/growth stocks (higher discount rates)

Falling yields = relief rally in risk assets

📊 Macro Traders:

The MOVE Index (bond volatility) often spikes around FOMC events

Forward guidance shifts = big rotation opportunities (e.g., bonds > gold > dollar)

(BONUS NERDY TIP) 🔍 How to Analyze Fed Speak Through Bonds

✅ Step 1: Watch the 2Y Yield

First responder to new rate expectations.

✅ Step 2: Check the Fed Funds Futures

Compare market pricing pre- and post-statement.

✅ Step 3: Look at Yield Curve Movement

Steepening or inversion? That’s the market’s macro take.

✅ Step 4: Track TLT or 10Y Yield on Your Chart

Bond ETFs or Treasury yields reveal sentiment instantly.

🧭 Final Nerdy Thought : Bonds React First, Talk Later

When the Fed speaks, don't just read the words. Read the yields. The bond market is often the first to interpret what the Fed really means—and the first to price in what comes next.

So next FOMC meeting, instead of watching only Powell’s facial expressions or CNBC pundits, open a chart of the 2Y and 10Y. That’s where the smart money’s listening.

put together by : @currencynerd as Pako Phutietsile

courtesy of : @TradingView

Federalreserve

Decoding Fed Rate Changes via Federal Funds Futures Index◉ What Are Federal Funds Futures?

● Definition: Federal Funds Futures are financial contracts traded on the Chicago Mercantile Exchange (CME) that allow market participants to bet on or hedge against future changes in the federal funds rate (the interest rate at which banks lend to each other overnight).

● Purpose: These futures reflect the market's expectations of where the Fed will set interest rates in the future.

◉ How Federal Funds Futures Work?

● Pricing: The price of a federal funds futures contract is calculated as 100 minus the expected average federal funds rate for the contract month.

➖ Example: If the futures price is 95.00, it implies an expected federal funds rate of 5.00% (100 - 95 = 5).

● Contract Expiry: Each contract represents the market's expectation of the average federal funds rate for a specific month.

◉ Why Use Federal Funds Futures?

● Predict Fed Policy: Traders and investors use these futures to gauge the likelihood of the Fed raising, cutting, or holding interest rates.

● Hedge Risk: Institutions use them to protect against potential losses caused by interest rate changes.

● Market Sentiment: They provide insight into what the broader market expects from the Fed.

◉ Steps to Analyze Fed Policy Using Federal Funds Futures

● Step 1: Check Current Federal Funds Futures Prices

Look up the prices of federal funds futures contracts for the months you're interested in. These are available on financial platforms like Bloomberg, Reuters, or the CME Group website.

● Step 2: Calculate the Implied Federal Funds Rate

Implied Federal Funds Rate = 100 - Futures Price.

➖ Example: If the futures price for March is 95.5, the implied rate is 4.5% (100 - 95.5 = 4.5).

● Step 3: Compare Implied Rates to the Current Rate

If the implied rate is higher than the current federal funds rate, the market expects the Fed to raise rates. If it's lower, the market expects a rate cut.

● Step 4: Estimate the Probability of Rate Changes

By comparing the implied rates of contracts expiring before and after an FOMC meeting, you can estimate the probability of a rate change.

➖ Example: If the implied rate for March is 4.75% and the current rate is 4.5%, the market is pricing in a 25 basis point (0.25%) hike.

● Step 5: Monitor Changes Over Time

Track how futures prices change over time. Shifts in prices indicate changes in market expectations. For example, if futures prices drop (implying higher rates), it suggests the market is anticipating a more hawkish Fed.

◉ Practical Applications

● Trading: Traders use federal funds futures to speculate on interest rate movements.

● Economic Forecasting: Economists use them to predict the Fed's monetary policy and its impact on the economy.

● Investment Strategy: Investors adjust their portfolios based on expected rate changes (e.g., shifting from bonds to equities if rates are expected to rise).

◉ Limitations of Federal Funds Futures

● Market Sentiment: Futures prices reflect market expectations, which can be influenced by sentiment and may not always accurately predict Fed actions.

● External Shocks: Unexpected events (e.g., geopolitical crisis, pandemics) can disrupt rate expectations.

● Liquidity: Less liquid contracts (further out in time) may not accurately reflect expectations.

◉ Example Analysis

Let’s assume:

➖ Current federal funds rate: 4.5%

➖ March federal funds futures price: 95.5

● Step 1: Calculate the implied rate:

100 − 95.5 = 4.5%.

● Step 2: Compare to the current rate:

The implied rate (4.5%) is equal to the current rate (4.5%), suggesting the market expects no change in rates by March.

● Step 3:

If the futures price drops to 95.25, the implied rate becomes 4.75%, indicating the market now expects a 25 basis point rate hike..

◉ Why This Matters?

● For Traders: Federal funds futures provide a direct way to bet on or hedge against interest rate changes.

● For Investors: Understanding rate expectations helps in making informed decisions about asset allocation.

● For Economists: These futures offer valuable insights into market expectations of monetary policy.

◉ Conclusion

Federal funds futures are a powerful tool for analyzing and predicting the Fed's interest rate decisions. By understanding how to interpret these futures, traders, investors, and economists can gain valuable insights into market expectations and make more informed decisions. However, it's important to consider their limitations and use them in conjunction with other economic indicators for a comprehensive analysis.

Interest Rate Strategies: Trade Smarter with Fed Rate DecisionsInterest Rate Strategies: Trade Smarter with Fed Rate Decisions

Trading interest rates may seem straightforward at first: buy when cuts end and sell when they fall. However, this approach often defies expectations, as determining when rate cuts truly end isn't as simple as pointing to a rate pause following a cut. While today’s Federal Reserve rate decisions are made during scheduled (and unscheduled emergency) Federal Open Market Committee (FOMC) meetings, this wasn’t always the case. Before the 1990s, the Fed often made changes outside of meetings. The shift to exclusively deciding rates during FOMC meetings was implemented to provide greater transparency and predictability for markets.

Topics Covered:

How Are Interest Rates Traded?

Three Interest Rate Trading Strategies.

Key Insights from Backtesting Interest Rate Trading Strategies.

Interest Rate Trading Indicator (Backtest For Yourself).

█ How Are Interest Rates Traded?

This strategy focuses on trading around Federal Reserve interest rate decisions, including hikes (increases), cuts (decreases), and pauses. These decisions are believed by many to have both short- and long-term effects on the market.

Key Strategy Concepts Backtested:

Buy on Rate Pauses or Increases: Go long (buy) when the Fed pauses or raises interest rates, typically signaling market stability or optimism.

Sell on Rate Decreases: Go short (sell) or close longs when the Fed cuts rates, often indicating economic concerns or slowing growth.

Buy on Specific Rate Decreases: Enter trades when the Fed implements specific rate cuts, such as 50 basis points (bps) which represents 0.5%, and analyze market reactions over different time horizons.

█ Strategy: Long during Pauses and Increases, Short during Decreases

This section examines the effectiveness of going long on rate pauses or increases and shorting during decreases. This strategy performed well between 2001 and 2009, but underperformed after 2009 and before 2001 compared to holding positions. The main challenge is the unpredictability of future rate changes. If you could foresee rate trends over two years, decision-making would be easier, but that’s rarely the case, making this strategy less reliable in certain periods.

2001-2009

Trade Result: 67.02%

Holding Result: -31.19%

2019-2021

Trade Result: 19.28%

Holding Result: 25.22%

1971-Present

Trade Result: 444.13%

Holding Result: 5694.12%

█ Strategy: Long 50bps Rate Cuts

This section evaluates trading around 50 basis point (bps) rate cuts, which is a 0.5% decrease. Large cuts usually respond to economic stress, and market reactions can vary. While these cuts signal aggressive economic stimulation by the Fed, short-term responses are often unpredictable. The strategy tends to perform better over longer timeframes, as markets absorb the effects.

1971-Present

Trade Duration: 10 trading days — Average Return: -0.19%

Trade Duration: 50 trading days — Average Return: 2.41%

Trade Duration: 100 trading days — Average Return: 2.46%

Trade Duration: 250 trading days — Average Return: 11.4%

2001-Present

Trade Duration: 10 trading days — Average Return: -2.12%

Trade Duration: 50 trading days — Average Return: -1.84%

Trade Duration: 100 trading days — Average Return: -3.72%

Trade Duration: 250 trading days — Average Return: 1.72%

2009-Present

Trade Duration: 10 trading days — Average Return: -15.79%

Trade Duration: 50 trading days — Average Return: -6.11%

Trade Duration: 100 trading days — Average Return: 7.07%

Trade Duration: 250 trading days — Average Return: 29.92%

█ Strategy: Long Any Rate Cuts

This section reviews the performance of buying after any rate cut, not just large ones. Rate cuts usually signal economic easing and often improve market conditions in the long run. However, the size of the cut and its context greatly influence how the market reacts over different timeframes.

1971-Present

Trade Duration: 10 trading days — Average Return: 0.33%

Trade Duration: 50 trading days — Average Return: 2.65%

Trade Duration: 100 trading days — Average Return: 4.38%

Trade Duration: 250 trading days — Average Return: 8.4%

2001-Present

Trade Duration: 10 trading days — Average Return: -1.12%

Trade Duration: 50 trading days — Average Return: -0.69%

Trade Duration: 100 trading days — Average Return: -1.59%

Trade Duration: 250 trading days — Average Return: 0.22%

2009-Present

Trade Duration: 10 trading days — Average Return: -3.38%

Trade Duration: 50 trading days — Average Return: 3.26%

Trade Duration: 100 trading days — Average Return: 12.55%

Trade Duration: 250 trading days — Average Return: 12.54%

█ Key Insights from Backtesting Interest Rate Trading Strategies

The first assumption I wanted to test was whether you should sell when rate cuts begin and buy when they end. The results were inconclusive, mainly due to the difficulty of predicting when rate cuts will stop. A rate pause might suggest cuts are over, but that’s often not the case, as shown below.

One key finding is that the best time to be fully invested is when rates fall below 1.25% or 1.00%, as this has historically led to stronger market performance. But this can be subject to change.

█ Interest Rate Trading Indicator (Backtest For Yourself)

Indicator Used For Backtesting (select chart below to open):

The 'Interest Rate Trading (Manually Added Rate Decisions) ' indicator analyzes U.S. interest rate decisions to determine trade entries and exits based on user-defined criteria, such as rate increases, decreases, pauses, aggressive changes, and more. It visually marks key decision dates, including both rate changes and pauses, offering valuable insights for trading based on interest rate trends. Historical time periods are highlighted for additional context. The indicator also allows users to compare the performance of an interest rate trading strategy versus a holding strategy.

Does the Market Rally When the Fed Begins to Cut Rates?The relationship between rate cuts and the stock market, as illustrated in the provided graph, shows that major market declines often occur after the Federal Reserve pivots to lower interest rates. This pattern is evident in historical instances where the Fed's rate cuts were followed by significant drops in the S&P 500. Several factors contribute to this phenomenon, which are crucial for investors to understand.

Economic Weakness:

Rate cuts typically respond to economic slowdown or anticipated recession.

Each instance of the Fed pivoting to lower rates (1969, 1973, 1981, 2000, 2007, 2019) corresponds to significant market declines soon after.

Rate cuts signal concerns about economic health, causing investors to lose confidence, as reflected in the graph.

Delayed Impact:

Rate cuts do not immediately stimulate the economy; it takes time for their effects to propagate.

The graph shows that the majority of the market decline occurs after the Fed's pivot, indicating that initial rate cuts were insufficient to halt the downturn.

During this lag period, the market may continue to decline as economic data reflects ongoing weakness.

Investor Sentiment:

Rate cuts can trigger fear among investors, who interpret the move as an indication of severe economic issues.

The graph shows substantial percentage drops in the S&P 500 following each pivot, demonstrating how negative sentiment can exacerbate declines.

The fear of a worsening economy leads to a sell-off in stocks, contributing to further market drops.

Credit Conditions:

During economic stress, banks may tighten lending standards, reducing the effectiveness of rate cuts.

Post-rate cut periods in the graph align with times of economic stress, where credit conditions likely tightened.

Businesses and consumers may not be able to take advantage of lower borrowing costs, limiting economic recovery and impacting the market negatively.

Historical examples such as the crises in 2000 and 2007 highlight substantial market drops after rate cuts, as seen in the graph. In both cases, the rate cuts responded to bursting bubbles (tech bubble in 2000, housing bubble in 2007), and the economic fallout was too severe for rate cuts to provide immediate relief. The graph underscores that while rate cuts aim to stimulate the economy, they often follow significant economic downturns. Investors should be cautious, recognizing that initial market reactions to rate cuts can be negative due to perceived economic weakness, delayed policy impact, and deteriorating sentiment.

Exploring the Weekly OptionsCME: E-Mini Nasdaq 100 Weekly Options ($Q1D-$Q5D)

When I first started trading two decades ago, I was overwhelmed by the amount of data that was available. I had a hard time correlating how data relates to price movement. While observing the stock market, I have one question in particular: why does the market often moves drastically immediately after the release of a major report?

Over time, I learnt that these reports provide insight into how the economy works. New data validates our assumptions about the future. Take the United States as an example:

• Consumers drive the U.S. economy;

• Consumers need jobs to be able to buy things and keep the economy going;

• The ebb and flow between the degree of joblessness and full employment drive economic activity up or down;

• How easy or difficult for households and businesses to get credit affects consumption, jobs, and investment.

The following reports have an outsized impact on global financial markets:

• The Nonfarm Payroll Report, released by the Bureau of Labor Statistics (BLS);

• The Consumer Price Index, also published by the BLS;

• Personal Income and Outlays, by the Bureau of Economic Analysis (BEA);

• Gross Domestic Product (GDP), also by the BEA;

• Federal Open Market Committee (FOMC) meeting, this is where the Federal Reserve sets the Fed Funds interest rates, ten times a year;

• Interest rate actions by other central banks, including European Central Bank, the Bank of England, the Bank of Japan, and the People’s Bank of China.

Binary Outcomes: Ideal Setting for Options Trading

For these highly anticipated reports, investors usually reach a consensus on the expected impact of the new data prior to its release. Market price tends to price in such investor expectations.

The next FOMC meeting is on September 20th. According to CME Group’s FedWatch tool, the futures market currently expects a 94% probability that the Fed would keep the Fed Funds rate unchanged at the 5.25%-5.50% range.

The September contract of CME Fed Funds Futures (ZQU3) is last settled at 94.665. This implies a Fed Funds rate of 5.335%, right in the middle of the target range.

When new data is released, investors focus less on the actual data, but more on how it compares to the consensus. Because the prevailing price already reflected market expectation, new data serves to either confirm or dispute it. We could use a range of -1 to +1 to categorize these outcomes:

• Well Below Expectations, -1;

• Meet Expectations, 0;

• Well Above Expectations, +1.

The sign of the outcome does not necessarily correspond to a positive or negative price movement. It differs by the type of data and the respective financial instrument.

We could further simplify the results into binary outcomes:

• Within Expectation: 0, where actual data approximates previous expectation;

• Beyond Expectation: 1, either below or above expectation by a pre-defined margin.

Both human and computer think in binary terms: Light switch On or Off, Price goes Up or Down, Risk turns On or Off. In derivatives market, we could buy a Call Options if we expect the price to go up, and a Put Options if we think the price will decline.

Weekly Options for Event-Driven Strategies

The FOMC meeting is the most significant event that affects global markets. Market may stay calm if the Fed keeps rate unchanged (within expectation). However, if the Fed raises rate unexpectedly, you could hear investors screaming all around the world!

To trade the Fed decision, investors could form different strategies using a wild variety of instruments, such as stock market indexes, Treasury bonds, forex futures, gold, WTI crude oil, and even bitcoin. Today, we focus on the Nasdaq 100 index. Here are some alternatives to consider:

• Nasdaq 100 ETF: many asset managers offer them, including Invesco, iShares and ProShares. From a trader’s perspective, ETFs offer no leverage. A $100K exposure requires $100K upfront investment. If the market moves up 1%, you also gain 1%, minus the fees.

• Nasdaq 100 Futures: CME Micro Nasdaq 100 ($MNQ) has a notional value of 2 times the index, valuing it at $31025, given the Nasdaq’s last close at 15512.5. Each contract requires initial margin of $1680. The futures contract is embedded with an 18.5-to-1 leverage.

• Nasdaq 100 Options: As the nearby September contract expires on the 3rd Friday, or the 15th, ahead of the FOMC meeting date, we could not use it for our strategy. Instead, we could apply it with the December contract ($NQU3). On September 1st, the 15800-strike Call is quoted $541.50, and the 15400-strike Put is quoted $535.

• Weekly Options: On September 1st, the 15800-strike Call to expire in one week is quoted $14.25, while the 15400-strike Put to expire in one week is quoted $54.50.

Premiums for the standard American-style Options are expensive. They come with quarterly contracts and quarterly expirations. While our target date is September 20th, we have to use the December contract and acquire 3-1/2-month worth of time value.

Weekly options, on the other hand, offer more precise trading and risk management with more expirations. Investors pay low premium to get the exposure they need and avoid the unnecessary and costly time value.

For E-Mini Nasdaq 100, the weekly options that expire on Wednesday, September 20th will be listed on the prior Thursday, September 14th. If an investor forms an opinion about the FOMC decision, he could implement it with a weekly call or put next week.

Nasdaq Weekly Options are deliverable contracts. If an investor owns a call and it expires in the money, he will settle the contract with a long position in E-Mini Nasdaq 100 futures. Likewise, if he owns an in-the-money put, he will get a short futures position.

If the market moves in favor of an investor’s expectation, the potential payoff could be significant due to the leverage in weekly options. If the investor is incorrect, he could lose money, up to the amount of the entire premium. However, the low-premium nature in weekly options helps contain such loss at a tolerable level.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trading set-ups and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

The Powell meme bomb & pivotThe fed and Powell have tried everything to dismiss inflation . First ignoring it then saying transitory then changing the perimeters as to how it's calculated. Even Sleepy Joe then chimed in at one point by saying hotdogs are actually cheaper for your red white and blue lies.

How about awards... Let's give Ben Bernanke the noble economics prize during this all of this insanity! How about an Oscar to a president? (Sean Penn to Zelensky) yeah why not??

Giving Bernanke an award like "Noble Economics" is like calling Dahmer chef of the year!

What the heck is going on? People are so broke they can't even pay attention! Has reality become the twilight zone? or was it always?

Who are these people that rule us? Can they really be this incompetent? If so why is there no accountability?

Now to Powell and gang. Last year they were caught for insider trading, what was their punishment? They were forced to sell their stock, at record gains mind you. Really... that's a punishment now? No one even batted an eye.

The west has become a bunch of zombie filled degenerate nations with it's citizens consuming filth at record pace even Usain Bolt would be envious of.

For this charade to keep going, you need to print more zombie snacks (dollars) there is no other way. I do believe the market is pricing in an inevitable Fed pivot at the moment which could turn out to be a sell the news moment next year at some point (not Financial advice).

Psychological warfare. The Psy-op being played has been ramped up to new levels the past couple years and it is being reflected in the market due to technology with access to investing now easier than ever with a device sitting in your pocket, just add a little emotion with degenerative news and voila.

The Pivot will eventually come, but will be the long term effects of it? Anyone can assume but simple 101 Noble Bernanke economics will tell you it ain't good. Anyway, this is my rant for the day.

Actually, I have a question. What effect do SEC (crypto) rulings have past American borders?

Here is my opinion, (crypto specifically) They have no jurisdiction past American borders so the effect is limited if any. In my opinion these negative rulings will only stifle any American innovation and growth of the sector. It actually just opens doors for other countries to take advantage of it as crypto is global. Please give me your thoughts on this down bellow.

Special Guest Appearance George Carlin

Thanks

WeAreSat0shi

Stay Blessed!

SOFR: Farewell to LIBORCME: SOFR ( CME:SR31! )

On June 30th, SEC Chairman Gary Gensler posted a 3-minute short video on Twitter. In this educational piece titled RIP LIBOR, he explains what the London Interbank Offered Rate (LIBOR) is, and why its passing away is actually a good thing for consumers.

As CFTC Chairman in 2009-2014 and SEC Chairman since 2021, Mr. Gensler oversaw the investigation of the 2012 LIBOR scandal and its replacement by the Secured Overnight Financing Rate (SOFR) in 2021 as the benchmark interest rate for US dollar.

Eurodollar and LIBOR

Offshore Dollar, the US currency deposited in banks outside of the United States, is commonly known as Eurodollar. Traditionally, offshore dollars were traded mainly among European banks. The name sticks to these days and applies to funds in non-European banks as well.

A key advantage of trading Eurodollar is the fact that it is subject to fewer regulations by the Fed, being outside of the US jurisdiction. London is the largest trading hub for Eurodollar.

The London Interbank Offered Rate came into being in the 1970s as a reference interest rate in the Eurodollar markets. By 1986, the British Bankers' Association (BBA) began publishing the US Dollar LIBOR daily. The BBA Libor was calculated based on interest rates reported by 17 member banks who together represented the bulk of Eurodollar transactions. Libor has been widely used as a reference rate for many financial instruments, including:

• Forward rate agreements

• Interest rate futures, e.g., CME Eurodollar futures

• Interest rate swaps and swaptions

• Interest rate options, Interest rate cap and floor

• Floating rate notes and Floating rate certificates of deposit

• Syndicated loans

• Variable rate mortgages and Term loans

• Range accrual notes and Step-up callable notes

• Target redemption notes and Hybrid perpetual notes

• Collateralized mortgage obligations and Collateralized debt obligations

How important was Libor? It is a reference rate in the documentation by private trade association International Swaps and Derivatives Association (ISDA), which sets global market standard for OTC derivative transactions.

In 2008, 60% of prime adjustable-rate mortgages and nearly all subprime mortgages were indexed to the USD Libor in the US. Furthermore, American cities borrowed 75% of their money through financial products that were linked to the Libor.

Libor has been the indispensable global benchmark for pricing everything from credit card debt to mortgages, auto loans, corporate loans, and complex derivatives.

CME Eurodollar Futures

In 1981, the Chicago Mercantile Exchange launched Eurodollar futures, the first ever cash-settled futures contract. It quickly became the most liquid contract by CME. At its peak, over 1,500 traders and clerks worked at the Eurodollar pit on CME trading floor.

Not to be confused with the Euro currency, Eurodollar futures contracts are derivatives on the interest rate paid on a notional or "face value" of $1,000,000 time deposit at a bank outside of the United. It uses the 3-month USD Libor rate as its settlement index. The late Fred D. Arditti, CME economist, is credited as the brain behind Eurodollar futures.

Eurodollar futures are priced as a Money Market instrument. The CME IMM index is used to convert a coupon-bearing instrument such as bank deposit, into a discounted instrument that does not make regular interest payments.

For instance, a futures price of 95.00 implies an interest rate of 100.00 - 95.00, or 5%. The settlement price of a Eurodollar futures contract is defined to be 100.00 minus the official BBA fixing of 3-month Libor on the day the contract is settled.

The 2012 LIBOR Scandal

The LIBOR Scandal was a highly publicized scheme in which bankers at major financial institutions colluded with each other to manipulate the Libor rate. As the scandal came to light in 2012, investigators found that the banks had been submitting false information about their borrowing costs to manipulate the Libor rate. This allowed the banks to profit from trades based on the artificially low or high rates.

A dozen big banks were implicated in the scandal. It led to lawsuits and regulatory actions. After the rate-fixing scandal, LIBOR's validity as a credible benchmark was over. As a result, regulators decided that Libor would be phased out and replaced.

If you want to learn more about the LIBOR scandal, feel free to check out the 2017 bestseller by David Enrich: “The Spider Network: The Wild Story of a Math Genius, a Gang of Backstabbing Bankers, and One of the Greatest Scams in Financial History”.

What is the SOFR

In 2017, the Federal Reserve assembled the Alternative Reference Rate Committee to select a Libor replacement. The committee chose the Secured Overnight Financing Rate as the new benchmark for dollar-denominated contracts.

The daily SOFR is based on transactions in the Treasury repurchase market, where firms offer overnight or short-term loans to banks collateralized by their bond assets ,similar to pawn shops.

Unlike LIBOR, there’s extensive trading in the Treasury repo market, estimated at $4.8 trillion in June 2023. This theoretically makes it a more accurate indicator of borrowing costs. Moreover, SOFR is based on data from observable transactions rather than on estimated borrowing rates, as was the case with LIBOR.

The Federal Reserve Bank of New York began publishing the SOFR in April 2018. By 2021, SOFR has replaced most of the LIBOR-linked contracts. The LIBOR committee officially folded up on June 30, 2023. Chairman Gensler apparently chose this day to post his RIP LIBOR video to mark the end of an era.

The difference between Fed Funds Rate and SOFR

Fed Funds Rate is set by the Fed’s FOMC meeting, and SOFR is published by the NY Fed. However, they are very different.

• Fed Funds Rate is considered a risk-free interest rate, and only member banks have access to this ultra-low rate through the Fed’s discount window.

• SOFR is a commercial interest rate where banks charge each other. The NY Fed publishes the rate based on transactions in the US Treasury repurchase market.

SOFR is similar to LIBOR because they are both commercial interest rate benchmarks. On the other hand, Fed Funds Rate is a policy rate set by the US central bank.

CME SOFR Futures and Options

CME Group launched the 3-month SOFR futures and options contracts in May 2018. The contracts were based on the SOFR Index, published daily by the New York Fed.

SOFR futures contracts are notional at $2,500 x contract-grade International Monetary Market (IMM) Index, where the IMM Index = 100 minus SOFR. At a 5.215 IMM, for example, each contract has a notional value of $13,037.50. CME requires a $550 margin per contract. An interest rate move by a minimum tick of 0.25 basis point would result in a gain or loss of $6.25.

At the beginning, SOFR contracts traded side-by-side with the Eurodollar contracts. By 2021, Eurodollar liquidity has transitioned to SOFR contracts. By April 2023, All Eurodollar contracts were delisted, and the transition was completed.

For all intended purposes, you could think of the SOFR futures as the same as the legacy Eurodollar contracts, with the only notable exception being the settlement index switched from LIBOR to SOFR.

On June 30th, the daily trading volume and Open Interest of SOFR contracts were 4,443,245 and 9,310,433 contracts, respectively. On the same date, CME Group total volume and OI were 23,769,103 and 104,221,083, respectively.

On the latest trade day, SOFR accounts for 18.7% of CME Group’s trade volume and 8.9% of its total open interest. Indeed, SOFR has successfully replaced Eurodollar as new No. 1 contract at CME and is arguably the most liquid derivatives contract in the world.

Where We Are at the SOFR Market

On June 30th, the JUN SOFR contract (SR3M3) expired and settled at 94.785. This translates to the JUN SOFR rate of 5.215 (100-94.785).

SEP 2023 (SR3U3) is now the new lead contract. It settled at 94.595 and implied a forward SOFR rate at 5.405 (100-94.595). This shows that the futures market expects a rate increase in the next Fed meeting.

Like Eurodollar futures, rising futures price will confer to declining SOFR rate, as rate is equal to 100 minus futures price. Similarly, a decline in futures price equates to a rising SOFR rate.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trading set-ups and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

USDebtCeilingCrisis.ComLet’s make some noise for the 11th hour party people. Bipartisan talks between US President Biden and House Republicans over the debt ceiling crisis have finally come to a resolution. Well, in theory at least since there is the small matter of Congress having to vote on it later this week. US lawmakers might balk at the idea that this is an 11th hour deal since the much touted ‘hard deadline’ of the 1st of June has now moved to the 5th of June. Any chances we could see that pushed forward by a few more days in the event of further brinkmanship during the Congressional vote on the deal?

Make no mistake. Regardless of the real hard deadline before the US technically defaults on its public debt, this will have been an 11th hour deal. The thing with 11th hour deals whether they’re related to business, divorce settlements, ransom/hostage negotiations or drug deals is that they tend to be equally bad for both parties but at least everyone walks away equally disappointed. A deal as critical as the one needed to tackle the debt ceiling crisis should have been done and dusted well before this game of chicken ended in both parties swerving just before the head on collision.

The US debt ceiling issue is a bubble. The limit has been lifted 78 times since 1960 and is quite the magician’s trick. Raising the limit each time a ceiling is reached and then kicking the issue into the long grass until the next time negotiations need to take place is dangerous enough but the way in which this current deal has been tentatively reached has created micro tears in this bubble and only time will tell if the bubble bursts at some point in the not- too-distant future. Even a smooth run through Congress later this week will be short-term relief for markets as the possibility of a crash depends on the extent of any liquidity leaving the system and where exactly that liquidity drain comes from as soon as the US Treasury turns on the T-bill tap to full blast after a confirmed deal.

These are exciting times for FX traders as we trade the bull runs, the bear runs and the crashes. Keep yourself educated and informed at all times. And remember that whenever you go to the market, be careful out there.

BluetonaFX

Decoding the Structure of the Federal Reserve System 🏦

If you've ever wondered how the U.S. monetary system functions and who runs the show, keep reading. In this article, we will break down the structure of the Federal Reserve System and help you understand how it operates.

🏦 The Federal Reserve System, often referred to as the Fed, is the central banking system of the United States. It was created in 1913 by the Federal Reserve Act and is an independent entity within the government. The Fed has a three-part structure, including the Board of Governors, the Federal Reserve Banks, and the Federal Open Market Committee (FOMC).

1️⃣ Board of Governors:

The Board of Governors is the governing body of the Federal Reserve System. It consists of seven members appointed by the President and confirmed by the Senate for 14-year non-renewable terms. One person is designated by the President as Chair and another as Vice-Chair. The Board's main function is to set monetary policy, supervise and regulate banking institutions, and maintain the stability of the financial system.

2️⃣Federal Reserve Banks:

There are 12 Federal Reserve Banks located throughout the United States. Each Federal Reserve Bank serves a specific geographic district and is responsible for carrying out the policies set forth by the Board of Governors. The Federal Reserve Banks are overseen by a board of nine directors, six of whom are appointed by banks in the district, and three by the Board of Governors.

In addition to overseeing the banking system, the Federal Reserve Banks also provide services to financial institutions and the U.S. Treasury. These services include processing and clearing checks, storing currency, and distributing new currency.

3️⃣Federal Open Market Committee:

The FOMC is the most powerful body within the Federal Reserve System. It is responsible for setting monetary policy, specifically the target for the federal funds rate, which is the interest rate that banks charge each other for overnight loans. The FOMC is made up of the seven members of the Board of Governors and five of the 12 Federal Reserve Bank presidents.

The FOMC meets eight times a year to analyze economic data and determine appropriate policy decisions. Their decisions impact not only the banking system but also the overall economy. For example, if the FOMC decides to raise interest rates, it will become more expensive to borrow money, affecting everything from mortgages to credit card payments.

Conclusion:

The Federal Reserve System is a complex organization that plays a critical role in the U.S. economy. Its structure is designed to ensure checks and balances across its three branches so that no one entity has too much power. While the Board of Governors sets policy and oversees the entire system, the Federal Reserve Banks carry out those policies and provide essential services to the financial system. The FOMC, on the other hand, is responsible for setting monetary policy, affecting the interest rates that impact our daily lives.

Understanding the Federal Reserve System is essential for anyone wanting to understand the U.S. economy. Knowing how the Fed operates can help individuals and businesses make informed decisions about their finances. With this knowledge, you can better navigate the ups and downs of the economy and protect your hard-earned money.

❤️Please, support my work with like, thank you!❤️

FED Interest Rates and it's mechanism BINANCE:BTCUSDT

In the United States, the federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis. Reserve balances are amounts held at the Federal Reserve to maintain depository institutions' reserve requirements. Institutions with surplus balances in their accounts lend those balances to institutions in need of larger balances. The federal funds rate is an important benchmark in financial markets.

The effective federal funds rate (EFFR) is calculated as the effective median interest rate of overnight federal funds transactions during the previous business day. It is published daily by the Federal Reserve Bank of New York.

The federal funds target range is determined by a meeting of the members of the Federal Open Market Committee (FOMC) which normally occurs eight times a year about seven weeks apart. The committee may also hold additional meetings and implement target rate changes outside of its normal schedule.

The Federal Reserve uses open market operations to bring the effective rate into the target range. The target range is chosen in part to influence the money supply in the U.S. economy

Financial institutions are obligated by law to hold liquid assets that can be used to cover sustained net cash outflows. Among these assets are the deposits that the institutions maintain, directly or indirectly, with a Federal Reserve Bank. An institution that is below its required liquidity can address this temporarily by borrowing from institutions that have Federal Reserve deposits in excess of the requirement. The interest rate that a borrowing bank pays to a lending bank to borrow the funds is negotiated between the two banks, and the weighted average of this rate across all such transactions is the effective federal funds rate.

The Federal Open Market Committee regularly sets a target range for the federal funds rate according to its policy goals and the economic conditions of the United States. It directs the Federal Reserve Banks to influence the rate toward that range with open market operations or adjustments to their own deposit interest rates. Although this is commonly referred to as "setting interest rates," the effect is not immediate and depends on the banks' response to money market conditions. Separately, the Federal Reserve lends directly to institutions through its discount window, at a rate that is usually higher than the federal funds rate.

Future contracts in the federal funds rate trade on the Chicago Board of Trade (CBOT), and the financial press refer to these contracts when estimating the probabilities of upcoming FOMC actions.

When the FOMC wishes to reduce interest rates they will increase the supply of money by buying government securities. When additional supply is added and everything else remains constant, the price of borrowed funds – the federal funds rate – falls. Conversely, when the Committee wishes to increase the federal funds rate, they will instruct the Desk Manager to sell government securities, thereby taking the money they earn on the proceeds of those sales out of circulation and reducing the money supply. When supply is taken away and everything else remains constant, the interest rate will normally rise.

The Federal Reserve has responded to a potential slow-down by lowering the target federal funds rate during recessions and other periods of lower growth. In fact, the Committee's lowering has recently predated recessions, in order to stimulate the economy and cushion the fall. Reducing the federal funds rate makes money cheaper, allowing an influx of credit into the economy through all types of loans.

THE MOST USEFUL TRADING SITES ...and how to utilize themIn this post, I will share the some of the most useful trading sites that are available to you and how you are able to utilize them to your advantage whether it's for fundamentals, charting, analysis, performance tracking, news events or just to follow your favorite professionals and their ideas & education that they share publicly.

First and foremost, if you haven't made this your PRIMARY trading platform, I want to encourage you to use and SUBSCRIBE to TRADINGVIEW

As we all evolve as traders, I'm sure we can all relate to one thing in common which is hard work and dedication. Trading is one of the hardest professions out there and without hard work, practice and dedication, we know that 90% of traders fail to make it in this industry. TRADINGVIEW gives you all the resources you need to be able to become one of the 10% as it enables you to become a content creator, it gives you a community to research ideas, you're able to watch livestreams, catch news flows, back test & analyze your own strategies and most importantly of all, you have direct support team to help guide you by sharing their own personal trading experiences, publicly as well as privately. Whether your choice of market is Forex, Stocks, Crypto, Bonds, Futures, Commodities or Yields, TRADINGVIEW has all the tools to be able get you well on your journey to become a professional trader.

See Figure 1: Subscriptions

WWW.MYFXBOOK.COM

MYFXBOOK has a variety of different tools to use ranging anywhere from position size calculators, COT data (Commitment of traders), Broker spreads/quotes/volumes, news flows, correlations and most importantly, account linked performance analysis. You may be a full time trader or a part time trader with a 9-5 job, either way analyzing your entries, exits, RR ratio, drawdowns etc. are necessary to find what works and what doesn't. Trading is about probabilities and if you're not making money in 25 trades, you need to reanalyze and change your approach. Myfxbook.com allows you to link your trading platform to breakdown your performance, ultimately being your own coach to find the approach that suits you the best.

See Figure 2: Performance Stats

WWW.TRADINGECONOMICS.COM

As many different crises happen throughout the world (especially the most recent ones within the last few years), understanding how the Federal Reserve operates to manage monetary policy is key to get an edge in your positions in the forex market. TRADINGECONOMICS gives you all the accurate information needed to be able to forecast and research throughout 196 countries like, economic indicators, exchange rates, stock market indexes, government bond yields and commodity prices. Micro and Macro economics are a big part of how this world operates and having access to all the most important information that drives the Feds decisions due to the economy being split between these two realms are valuable as they could be bridged together for more accurate forecasting.

See Figure 3: Inflation Rates/GDP Growth (By Country)

WWW.FOREXLIVE.COM

FOREXLIVE has many different helpful resources to keep you up to date in the market no matter what time zone or trading session you take part in. As our lives are busy with family, day jobs, business endeavors or simply being in different time zones, you may not be able to watch all sessions play out and in fact, taking a break from the screen is healthy for your mind and emotions. The great thing about FOREXLIVE is that you are able to read Session Wraps to keep you up to date with a summary after each session (Asian, European, U.S) completes. Psychology is a big part of why a trader either succeeds or fails which balancing your time on and off the markets are important to detach your emotions from your positions. Set a plan for how many times you will scan the charts a day and fill that in between time with activities like exercising, reading, chores, spending time with your family, going for a walk and much more.

See Figure 4: Session Wraps

WWW.INVESTOPEDIA.COM

INVESTOPEDIA was founded in 1999 headquartered in the heart of New York city U.S. This website provides comparisons of financial products, reviews, ratings, comparisons of different financial products and most importantly, it is a financial dictionary. With the broad range of information provided, it gives readers the confidence to manage every aspect of their financial life. Whether you're learning about money and investing for the first time or are looking to improve your knowledge and skills, anyone from an experienced investor, a business owner, a professional, an advisor, INVESTOPEDIA has all the information to build your skills.

See Figure 5: 4 Basic Things to Know About Bonds/Key Takeaways

WWW.INVESTING.COM

INVESTING.COM is a well known site that offers real-time market quotes, information about stocks, futures, options, analysis, commodities and most importantly an economic calendar. Keeping an eye out for the high impact news events will help you adapt and control the volatility during those peak hours. Another helpful aspect of this site is knowing what will drive the market mood for each upcoming week. The top 5 most important fundamental areas to watch for are explained and broken down to help your forecast and analysis so you can prepare your trade setups accordingly. Applying fundamental analysis along with technical analysis will help you become a better trader as when the high impact news events hit, markets get volatile which could cause a running profit turn into an absolute loss. Knowing when to be in or out of the market is valuable so you don't go into a draw down phase.

See Figure 6: Economic Calendar

As I only have mentioned a small number of sites that you are able to access, we all know there are so many other ones available out there, paid and free.

Researching and spending the time to read to broaden your knowledge in the financial world will only help you grow as a trader and essentially improve your trading results.

Check out some more free sites:

www.fxstreet.com

www.dailyfx.com

www.forexfactory.com

www.babypips.com

Please share the site that most helps you in by leaving it in the comment section. I would love to see the variety of ones available.

** If you felt this was helpful in anyway, please support by hitting the LIKE button and FOLLOW me for more educational and analysis ideas **

I appreciate all the feedback!

Thanks

Trade Safe

The Fed rate or Why everyone is watching the US economy?The Fed or the Federal Reserve System is a kind of analogue of the central bank in the United States. It is an independent body and receives powers from the US Congress. Its independence lies in the fact that all decisions on monetary policy do not have to be approved by the authorities and even the president. We can say that the Fed does not belong to anyone, because. after agreement with the Senate, the main positions are appointed by the President of the United States, but the owners are private individuals.

The functions of the Fed are the same as those of the central bank: issuing money, controlling private banks, changing the key rate, and other important decisions for the US economy, which affects the economy of the whole world. Let's analyze them in more detail:

maintaining a balance between the financial and social spheres;

protecting the interests of participants in banking operations;

dollar issue;

control of the internal financial market;

acting as a depository for large organizations;

supporting the functioning of payments within the country and between countries;

maintaining liquidity.

And now let's take a look at the questions about the impact of the Fed's actions on the crypto economy in order, so that you have a general picture of what is happening.

1. Why do many investors and traders in stocks and cryptocurrencies constantly follow the news from the US, especially the speeches of the head of the Fed?

One of the Fed's main tools, through which they influence the US economy, is to raise or lower the key rate. The Fed sets the percentage rate at which loans are issued to banks. This, in turn, affects other market segments, and the effect is different for each.

This has a direct impact on the bond market: the higher the rate, the higher the yield.

However, the effect on the stock market is completely opposite, because the reduction in the rate is followed by an adjustment in other lending rates. At a low rate, companies' businesses can grow faster. Due to this, stock quotes of many companies also increase due to the increase in their capitalization. Consumer and business confidence is on the rise, the real estate market is rebounding, and corporate earnings are rising, which in turn has a positive effect on share prices.

As the interest on loans decreases, the interest on deposits also decreases. There is more money in the financial system, which encourages people to look for more profitable areas of investment.

Yes, just a second. We feel that you may get confused or never understand what it is and why everything works the way it does. Let's explain with a very simple example.

The Fed rate is the percentage at which the main bank lends to other banks. If it falls, then other banks can take out a loan at a low interest rate and also issue loans with a small interest rate for organizations and individuals, including mortgages and credit cards. The decline in market interest rates encourages people to take out loans and buy various goods, invest in real estate and invest. The interest on deposits is falling, it is becoming less profitable to keep money on deposits, and people are looking for more attractive ways to invest - these are, first of all, stocks. Due to increased demand, the price of stocks and indices rises. And if the main indices grow, such as the NASDAQ, S&P500 or the Dow Jones industrial index, then Bitcoin grows, and other cryptocurrencies follow it.

At the same time, if the Fed rate rises, then people pull their savings out of riskier types of investment into more stable ones (deposits / deposits). Thus, the capitalization of the stock and cryptocurrency markets is falling, followed by a price drop. As you have noticed, everything in the world of economics is interconnected, and it is extremely difficult to explain all its principles in one article. We just want to bring you to the relationship between the Fed rate and the cryptocurrency market.

And here comes the next question!

2. Why is Bitcoin most of the time correlated with major stock market indices?

Everything is a little easier here. Previously, Bitcoin was something incomprehensible to most - an uninteresting technology and hype. But as blockchain technologies are introduced into everyday life (mass adoption), Bitcoin has turned into a risky, but quite common asset of the market. Because of this, relatively recently, “old” money has entered this market. People who used to earn only in the stock market and large companies entered the market. Large investors have developed strategies for trading and investing. Thus, for them, Bitcoin has become a financial instrument, just more risky. From that moment on, there was a high correlation with the stock market.

In conclusion, one of the important questions.

3. How do the US and the US dollar affect the entire world economy?

In the past, there was a situation when world trade and its institutions, as well as the world banking system, became pegged to the US dollar, central bank reserves began to accumulate mainly in dollars, and a financial market was formed with tools that allow you to effectively

place these reserves in dollar form. Simply put, most of the world uses the dollar, which is why it is the main reserve currency of the world. US hegemony, which influences the whole world, has been developing since 1944.

Let's summarize step by step to consolidate the information:

The American dollar and the US economy affect the entire world market, the first - because it has historically happened, and the second - because it is the largest in the world.

If the rate rises, then after it interest on loans and deposits rises. It becomes more profitable to invest in bonds and keep deposits in banks. Companies and people are shifting funds from risky stocks and cryptocurrencies to more stable types of investment: precious metals, government. bonds or simply withdraw to fiat.

If the rate falls, then after it interest on loans and deposits goes down. Companies and people are becoming more willing to take out credit, thereby increasing the financial system. Companies are developing business and increasing capitalization, people are starting to invest in more profitable instruments such as stocks and cryptocurrencies.

CPI & Inflation Rate USHello everyone! Let's take a look on what happened yesterday on the US financial market and understand the impact of CPI and inflation rate.

The Consumer Price Index (CPI) and inflation news from the United States can have a significant impact on financial markets and the value of the U.S. dollar. The CPI measures the change in the price of a basket of goods and services consumed by households, and inflation is the rate at which the general level of prices for goods and services is rising.

When the CPI and inflation numbers are higher than expected , it can indicate that the economy is growing, which can boost stock prices, lead to higher interest rates, and appreciate the dollar. This is because as the economy grows, companies will see increased demand for their products and services, which can lead to higher profits and stock prices. Higher interest rates can also attract more investors to bonds, which can lead to higher bond prices. Additionally, a strong economy can lead to increased demand for U.S. goods and services, and increased foreign investment in the U.S. economy. As a result, the demand for dollars increases, which can lead to an increase in the value of the dollar.

On the other hand, if the CPI and inflation numbers are lower than expected , it can indicate that the economy is slowing down , which can lead to lower stock prices, lower interest rates and depreciation of the dollar. This is because as the economy slows down, companies will see decreased demand for their products and services, which can lead to lower profits and stock prices. Lower interest rates can also lead to less investors in bonds, which can lead to lower bond prices. Additionally, a weak economy can lead to decreased demand for U.S. goods and services, and decreased foreign investment in the U.S. economy. As a result, the demand for dollars decreases, which can lead to a decrease in the value of the dollar.

It's important to note that the Federal Reserve uses inflation as an indicator to change the monetary policy, as they use interest rates as a tool to control inflation. Typically if inflation is too high, the Fed will increase interest rates to slow down the economy and curb inflation, and if inflation is too low, the Fed will decrease interest rates to stimulate the economy. These monetary policy decisions can also have an impact on the value of the dollar, as when the Fed raises interest rates, it can make the U.S. a more attractive place to invest, which can lead to an appreciation of the dollar. Conversely, when the Fed lowers interest rates, it can make the U.S. a less attractive place to invest, which can lead to a depreciation of the dollar.

How to Adjust Your Stock Chart for Inflation, Dividends, and TaxUsing a pretty simple formula involving CPI , we can adjust the stock chart to show real returns instead of nominal returns. Real returns represent a more accurate picture of the return of the stock over time. In addition, we can easily adjust returns for dividends and estimated taxes.

impact of two important following news on DXYTwo important factors that been driving Dollar prices in last several month as we all know is Federal Funds Rate and Inflation data like CPI.

In this week we have both of them coming out on Tuesday and Wednesday, now we want to see how it can affect the market.

Price usually tend to be at important resistive or supportive areas at the time of important news hit the market and as we can see now price is at supporting area and at the Daily low which probably will remain here until the news hit the market so we can expect of low volatility movement on USD and other major crosses, But what will happen when the news releases?

As we know CPI balance is curving to downside and shows that inflation is cooling down and as we see the prediction of tomorrow CPI news we can see that the market expect this trend to continue. Now here is the tricky part, if CPI data put out like prediction or lower than the prediction this means that fed has the inflation under control which makes trader to believe that federal reserve would not need to raise prices very aggressively like before and as a result we may see a risk on environment in the market which can lead Dollar prices to come lower, but on the other hand SPX, TLT, EUR,JPY and also commodity currencies like AUD,NZD to take benefit from the situation.

But if CPI data comes out higher than expectation then we can argue that federal reserve do not have inflation under control so it needs to continue hiking prices like before and this situation may lead to higher prices for Dollar and lower prices for all the other assets that we covered above.

Also if the second scenario take place tomorrow we can expect USYIELD to continue going higher which have negative effect on US treasury bond and very bad effect on SPX index.

Put CPI analysis apart the other important news that can shake prices real hard is federal reserve which going to hit the market on Wednesday. On that time we can see that what exactly is in the mind of federal reserve and how they are going to impact the economy. In overall, if they raise rate same or below the expectation its going to be very good for risky assets since it shows that we are getting close to end of rate hiking cycle but if federal reserve going for raising rate higher than expectation then it will have a very good impact on Dollar but bad impact on risky assets.

Inflation Slowing, but Still a Concern for the Federal ReserveInflation in the United States, as measured by the consumer price index (CPI), is expected to have slowed again in November. This is due in part to a weaker economy, which has reduced inflation pressures. However, the expected 0.3% increase in the CPI is not enough to ease concerns at the Federal Reserve or prevent the central bank from raising interest rates even higher to slow the economy.

Gas prices have fallen since the summer, reversing the spike in spring that sent inflation to a 40-year high. As a result, the cost of living has risen more slowly in the past four months. If the forecast is accurate, the annual rate of inflation would taper off to 7.3% from 7.7% in October and a peak of 9.1% in June.

The core rate of inflation, which excludes food and gas, is also forecast to rise 0.3% in November. This is still higher than the monthly gains that were the norm before the pandemic. The yearly rate of core inflation may fall slightly to 6.1% from 6.3% in the previous month. The rate peaked at 6.6% in November.

The increase in the cost of goods, excluding energy, has relaxed to 5% in October from 12.4% in February. However, the increase in the price of services continues to accelerate. The cost of services, excluding energy, has risen 6.8% in the past year. This is due in part to the increasing cost of labor, which is the biggest expense for most service-oriented businesses.

Rents have jumped 7.5% in the past year, marking the biggest surge since 1982. Rents are starting to decrease as the economy slows, but the Fed and Wall Street are watching for clear evidence of a reversal. Even if rents and home prices level off, the change may not immediately show up in the CPI report.

FOMC Meeting Next Week: Bank of America Expects 50bp Rate Hike The Federal Open Market Committee (FOMC) is set to meet next week, and investors are eagerly anticipating the outcome of the meeting. Bank of America Global Research has discussed its expectations for the meeting, saying that it expects the Fed to raise its target range for the federal funds rate by 50bp in December to 4.25-4.5%.

According to Bank of America, the Fed has telegraphed this move over the last few weeks through its communications. However, the more important question is where the Fed will go next. Bank of America expects the median forecast for 2023 to move up by 50bp to 5.125%, which is consistent with its terminal rate. The bank also expects the dot plot to show 100bp of cuts each in 2024 and 2025.

In addition, Bank of America expects the macro projections in the Statement of Economic Projections (SEP) to be revised to show lower GDP growth and inflation than in September, and higher unemployment.

At the press conference following the FOMC meeting, Bank of America expects Chair Powell to push back against easing in financial conditions and remind investors that a slower pace of hikes does not mean a lower terminal rate. The bank believes that Powell will stress that the Fed's job is far from done.

Overall, Bank of America expects the FOMC meeting next week to be consistent with the Fed's previous communications and for there to be no major surprises or shifts in policy.

Some Jargon Explained

The Dot Plot

The dot plot, also known as the Summary of Economic Projections (SEP), is a visual representation of Federal Reserve policymakers' individual forecasts for where they think key interest rates will be in the coming years. The dot plot shows the central tendency, or the middle of the range, of the individual forecasts for the federal funds rate.

Each participant in the FOMC meeting provides their own individual forecast for the federal funds rate at the end of each calendar year, as well as over the longer run. These forecasts are then plotted on a chart, with the dots representing the individual forecasts and the lines connecting the dots indicating the median of the group's forecasts.

The dot plot is released four times per year, along with the FOMC's policy statement, and provides insight into the collective thinking of FOMC members about the future path of interest rates. It is an important tool for investors to gauge the future direction of monetary policy.

The Terminal Rate

The terminal rate, also known as the long-run federal funds rate or the equilibrium real interest rate, is the interest rate that the Federal Reserve believes is consistent with the long-run health of the economy. It represents the level of the federal funds rate that is neither expansionary nor contractionary and is expected to prevail in the long run, once the economy has reached its full employment and price stability goals.

The terminal rate is not a fixed number, and can change over time depending on a variety of factors such as changes in the underlying productivity and demographic trends of the economy. The Federal Reserve uses the terminal rate as a reference point when setting its short-term interest rate targets.

In general, the terminal rate is expected to be lower than the current federal funds rate, as the Fed typically raises interest rates in the short run to prevent the economy from overheating and then lowers them in the long run to support economic growth. This means that the terminal rate can provide important information about the future direction of monetary policy.

How the Fed's Rate Hikes Affect the Market (or Not)In this post, I'll be demonstrating how the Fed's rate hikes affect the equity market (or how they don't), through historical examples and analyses of market psychology. This is an issue that has been going on for a while, and one that has caught the attention of all market participants. Yes, tapering and rate hikes aren’t necessarily good news, but I don’t think that 1) they necessarily indicate the beginning of a bear market/recession, and 2) the Fed is as powerful and influential as we think they are.

This is not financial advice. This is for educational purposes only.

Introduction

- There’s a myth, a misconception in the market that the Fed allegedly rescues falling markets with rate cuts and easing measures, and vice versa for when the market is overheated.

- This myth began in 1987 during Black Monday, when Alan Greenspan’s Fed cut rates after the crash, creating an impression that the Fed was directly responding to the stock market.

- This is when the (mis)belief that the Fed would put a floor under a a falling market stuck.

- Nevertheless, if we analyze the data, it actually demonstrates that the Fed stood pat for most corrections, and cutting cycles typically arrive during bear markets, just as coincidence.

Historical Cases

- There are only two occasions in history where the Fed’s cutting cycles corresponded with market lowpoints.

- The first is the aforementioned Black Monday of 1987, and even for this case.

- If we take a look at the situation back then, it’s not so much that the Fed made international moves that contributed to history, but rather that the bear market started amid a global liquidity crisis.

- With excess liquidity, the rates should have been flat, or down, but that wasn’t the case.

- Thus, the Fed’s rate cuts were vital to unfreezing credit and ensuring banks and clearing houses would have access to liquidity they needed, while the market was under severe stress.

- The second occasion was the rate cut in 1998, when stocks were reacting to the collapse of Long-Term Capital Management (LTCM).

- There was fear in the market that this collapse would lead to a domino effect, ending in a banking meltdown.

- Generally, when people fear a banking contagion, liquidity in interbank funding markets dry up.

- The Fed’s action to cut rates during this time helped keep money moving, and ensured that banks met their regulatory obligations.

Market Psychology

- In order to understand the recent discussion revolving around the importance of the Fed’s actions, we need to understand human nature.

- People love finding narrative threads and grand explanations because we’re biologically wired to make sense of the world that way.

- They confuse correlation and causation, and zero in on evidence that supports their view and shuns whatever suggests otherwise.

- But it’s important to remember that in most cases, a fact that everyone knows, tends to be closer to myth than reality, and even if it weren’t a myth, the fact that everyone knows it does not give us an edge in the market.

Summary

Market shocks are caused by surprises. News about a pandemic or cyber attack that catches investors off guard is much riskier than macro events that are predictable and can be anticipated. Given that the markets are efficient (which I believe they are), it's rational to assume that news about the Fed's rate hikes, and people reaction to it are already priced in. While short term volatility is definitely expected, I believe that the likelihood of this event becoming a trigger for a multi-year recession is extremely unlikely.

If you like this educational post, please make sure to like, and follow for more quality content!

If you have any questions or comments, feel free to comment below! :)

Impact of Fed Unchanged Interest Rate and Gold PricesHere I tried to show the movement of the day when Fed announces its unchanged Interest Rate decisions during the last 6 times. As you can see, the gold prices had been quite volatile during the last Fed decision on June the 16th and shed 1.45%. Since then, the yellow metal has not been able to overcome the loss and is in the downward trend.

Please note that this is shared for educational and informational purposes only and is not intended for financial decisions.

If you like the idea, please like and comment :)

The Link Between Inflation, Rising Bond Yield, & Market Sell-offAggravated by Jerome Powell's speech at the Wall Street Journal Jobs Summit, the tech-led sell-off continues, causing the Dow Jones Industrial Average to fall by 1.11%, S&P 500 by 1.34%, and Nasdaq Composite by 2.11%. On that note, the 10-year Treasury yield also popped to 1.541% during Jerome Powell's speech, later closing at that level for the day.

But how, specifically, did Jerome Powell cause the market to sell-off yesterday? Let's find out.

Prior to Jerome Powell's speech, there were already a substantial amount of tension surrounding the bond market and concerns regarding inflation.

A key event occurring recently that brought a great deal of attention to the acceleration of rising bond yields were the sudden spike in 10-year Treasury yield back in 2/25/21 from 1.38% to 1.54% - temporarily jumping as high as 1.6%, when an auction of US$62 billion 7-year notes was met with weak demand. This rattled the stock market because investors were not ready for the velocity of the 10-year Treasury yield surge. Instead, they were expecting for yields to gradually inch higher throughout the year.

In an effort to pinpoint the exact reason for the surge, many conclusions were drawn. One of which relates to inflation concerns. Over the course of the pandemic, trillions in fiscal relief has been delivered, of which an addition $1.9 trillion in fiscal package is expected to come from the Biden Administration. With so much money printed and nowhere to flow yet due to economic lockdown as a result of the pandemic, investors fear that once the economy reopens again, pent-up demand will drive people to go on vacation and spend in masses, injecting all the printed money over the course of the pandemic into the economy all at once, driving inflation up at a rate that has not been seen since the 2008 Financial Crisis. Due to this belief of a looming inflation, it makes bond that are purchased currently potentially worthless because of possible subpar yield. As a result, people flock away from bonds at the moment because they are expecting that yields will rise going forward in order to compensate for inflation risk. Thus, yields are continuously being driven up.

However, with the sudden spike in yield, it creates uncertainty around whether we will be seeing an acceleration of rising bond yields and possibly indicate that inflation could be around the corner. The possibility of this scenario is further amplified by vaccination efforts contributing to a recovering U.S. economy, and the incoming $1.9 trillion fiscal package that could further inflate the economy going forward while pushing the economy further into the recovery.

Taking all of this into account, let's go back to Jerome Powell's speech.

Having understood all of these, investors were looking at Jerome Powell to see whether he would give any indication on how he plan to control the acceleration of the rising bond yield, perhaps through an adjustment of the Fed's asset purchase program, where they will step up on the purchasing of long-term bonds to drive down long-term interest rates, or even extending the Supplementary Leverage Ratio that will be expiring on 3/31/21, so that banks can further help with the purchase of long-term bonds.

However, in his speech, Jerome Powell said nothing of the sort, in which the market took as a signal that yields could rise further, triggering the sell-off even further, and driving the 10-year Treasury yield further up to a level that matches the initial 10-year Treasury yield spike back in 2/25/21. In fact, Jerome Powell made supposedly positive remarks stating that he expects the rise in inflation as the economy recovers to only be temporary, that he does not expect the move up in price to be long-lasting nor does he expect it to be enough to change the Fed's accommodative monetary policy, among others. With the market sell-off and surge in yield during his speech, it is clear that the market neither believes his words nor views it positively.

To conclude, we are now in a very volatile situation where stocks no longer just goes up. We cannot control the direction of the market, but what we can control is how we deal with this situation emotionally and monetarily. Don't get too hung up on the short-term bearishness of the current market condition because if you zoom out your chart, in the grand scheme of things, this is just a tiny bleep. As such, if you believe that we will eventually recover from this market sell-off, use this as an opportunity to buy into your favorite companies at a huge discount.

Invest safe.

This is not investment advice so please do your own due diligence!

Support this idea with likes and share your thoughts below.