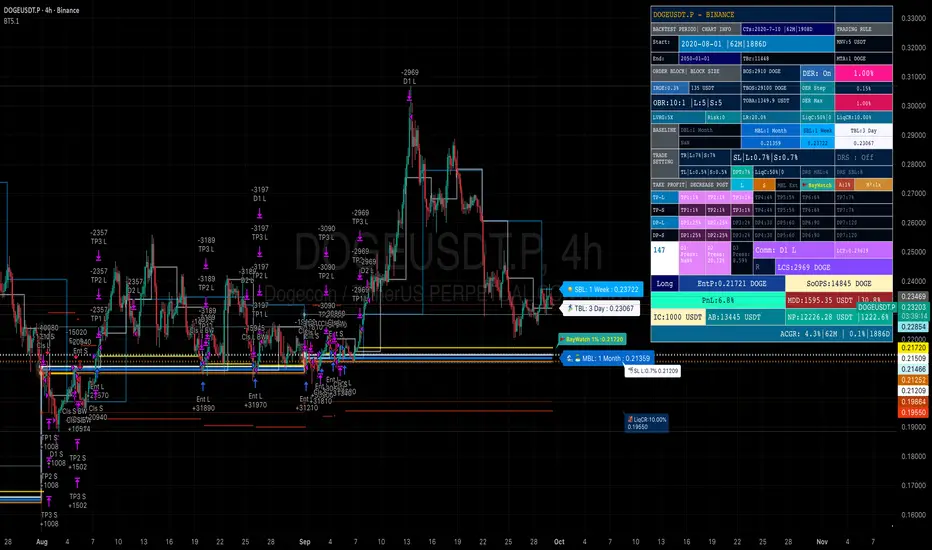

Baseline TrendBaseline Trend Strategy Overview

Baseline Trend is a crypto-only trading strategy built on straightforward price-based logic: market direction is determined solely by the price’s position relative to a selected baseline open price. No technical indicators like RSI, MACD, or volume are used—this approach is purely focused on price action and position size manipulation.

This strategy is a genuine concept, developed from my own market analysis and logical theory, refined through extensive observation of crypto market behaviour.

While the strategy offers structure and adaptability, it’s important to recognise that no single trading system or indicator fits all market conditions. This tool is meant to support decision-making, not replace it—encouraging traders to stay flexible, informed, and in control of their risk.

Important Usage Note:

This system is intended for crypto markets only.

– When used as an indicator guide, it can be applied to both spot and futures markets.

– However, when used with web-hook automation, it is designed only for futures contracts.

Ensure compatibility with your trading setup before using automation features.

Core Logic: The Baseline

The strategy revolves around the concept of a “Baseline”, with three types available:

Main Baseline: Defines the primary trend direction. If the price is above, go long; if below, go short.

Second Baseline and Third Baseline: Used to measure buying/selling pressure and are key to certain take-profit logic options.

Baselines are customisable to different timeframes—Year, Month, Week, and more—based on available input settings. Structurally, the Main Baseline is the highest-level trend reference, followed by the Second, then Third.

Users can mix and match these baselines across timeframes to backtest crypto symbols and understand behaviour patterns, particularly when used with standard candlestick charts.

Entry & Exit Logic

Entry Signal: Triggered when price crosses over/under a defined distance (percentage) from the Main Baseline. This distance is the Trade Line, calculated based on the close price.

Exit Signal / Stop Loss: If price moves un-favorable and crosses over/under the Stop Loss Line (a defined distance from the Main Baseline), the open position will be force-closed according to user-defined settings.

LiqC (Liquidation Cut)

LiqC is a secondary stop-loss that activates when a leveraged position’s loss equals or exceeds the user-defined liquidation threshold. It forcefully closes the position to help prevent full liquidation before stop-loss, providing an extra layer of protection.

This LiqC is directly tied to the leverage level set by the user. Please ensure you understand how leverage affects liquidation risk, as different broker exchanges may use different liquidation ratio models. Using incorrect assumptions or mismatched leverage values may result in unexpected behaviour.

Position Sizing & Block Units

This strategy features a block-based position sizing system designed for flexibility and precision in trade management:

Block Range: Customisable from 1 to 10 blocks

Risk Allocation: Controlled through a user-defined ROE (Risk of Equity) value

For example, setting an ROE of 0.1% with 10 blocks allocates a total of 1% of account equity to the position. This structure supports both conservative and aggressive risk approaches, depending on user preference.

Block sizes are automatically calculated in alignment with exchange requirements, using Minimum Notional Value (MNV) and Minimum Trade Amount (MTA). These values are dynamically calculated based on the live market price, and scaled relative to the trader’s balance and selected risk percentage. This ensures accurate sizing with built-in adaptability for any account level and current market conditions.

Scalping Meets Trend Holding

This system blends short-term scalping with longer-term trend holding, offering a flexible and adaptive trading style.

Example:

Enter 10 blocks → take quick profits on 5 blocks → let the remaining 5 ride the trend.

This dual-layered approach allows traders to secure early gains while staying positioned for larger market moves. Think of it as:

5 Blocks to Protect: Capture quick wins and manage exposure.

5 Blocks to Pursue: Let profits run by following the broader trend.

By combining both protection and pursuit, the strategy supports risk control without sacrificing the potential for extended returns.

Flexible Take-Profit Logic

The strategy supports multiple, customisable take-profit mechanisms:

TP1–4 (Profit Percentage)

Triggers take profit of 1 block unit when unrealised gains reach defined percentage thresholds (TP1, TP2, TP3, TP4).

Buying/Selling Pressure-Based Take Profit

D1 – Pressure 1

Measures pressure between Second and Third Baselines.

If the distance between them exceeds a user-defined DPT (Decrease Post Threshold) and the price moves far enough from the Third Baseline, D1 activates to take profit or scale out one block.

D2 – Pressure 2

Measures pressure between the Main and Second Baselines.

Works similarly to D1, using a separate distance and pressure trigger.

Note: Both D1 and D2 deactivate in reversal or even trend conditions.

D3–5: High-High / Low-Low Logic

Based on bar index tracking after position entry:

For Long Positions: If after D3 bars the price doesn't exceed the previous bar's high, the system executes a take profit or scale-out.

For Short Positions: If the price doesn't drop below the previous low, the same logic applies.

This approach adds time-based and momentum-aware exit flexibility.

Leverage & Liquidation Risk

When backtesting with leverage enabled, the system checks whether historical candles exceed the liquidation range, calculated based on the average entry price and the leverage input. If the Liquidation Risk Count exceeds 1, profit and loss accuracy may be affected. Traders are encouraged to monitor this count closely to ensure realistic backtesting results.

Since the system cannot directly control or sync with your broker exchange’s actual leverage setting, it’s important to manually match the system’s leverage input with your broker’s configured leverage.

For example: If the system leverage input is set to 10, your exchange leverage setting must also be set to 10. Any mismatch will lead to inaccurate liquidation risk and PnL calculations.

Backtesting and Customisation

All TP1–4 and D1–5 functions are fully optional and customisable. Users are encouraged to backtest different crypto symbols to observe how price behaviour aligns with baseline structures and pressure metrics.

Each of the TP1–4 and D1–5 triggers is designed to execute only once per open position, ensuring controlled and predictable behaviour within each trade cycle.

Since backtesting is based on available historical bar data, please note that data availability varies depending on your TradingView subscription plan. For more reliable insights, it’s recommended to backtest across multiple time ranges, not just the full dataset, to assess the stability and consistency of the strategy’s performance over time.

Additionally, the time frame resolution interval in TradingView is customisable. For best results, use commonly supported time frames such as 30 minutes, 1 hour, 4 hours, 1 day, or 1 week. While the system is designed to support a broad range of intervals, non-standard resolutions may still cause calculation errors.

Currently, the system supports the following resolution ranges:

Intraday: from 1 minute to 720 minutes

(e.g., 60 minutes = 1 hour, 240 minutes = 4 hours, 720 minutes = 12 hours)

Daily: from 1 day to 6 days

Weekly: from 1 week to 3 weeks

Monthly: from 1 month to 4 months

Although the script is built to adapt to various resolutions, users should still monitor output behaviour closely, especially when testing less common or edge-case time frames.

System Usage Notice:

This system can be used as a standalone trading indicator or integrated with an exchange that supports web-hook signal execution. If you choose to automate trades via web-hook, please ensure you fully understand how to configure the setup properly. Web-hook integration methods vary between exchanges, and incorrect setup may lead to unintended trades. Users are responsible for ensuring proper configuration and monitoring of their automation.

Note on Lower Time Frame Usage

When using lower time frames (e.g., 1-minute charts) as the trading time frame, please be aware that available historical data may be limited depending on your subscription plan. This can affect the depth and reliability of backtesting, making it harder to establish a trustworthy probability model for a symbol’s behaviour over time.

Additionally, when pairing a high-level Main Baseline (MBL) time line (such as "1 Month") with low time frame resolutions (like 1-minute), you may encounter order execution limits or calculation overloads during backtesting. This is due to the large number of historical bars required, which can strain the system's capacity.

That said, if a user intentionally chooses to work with lower time frames, that decision is fully respected—but it should be done with awareness and at the user’s own risk.

Things to Be Aware Of (Web-hook Usage Only)

The following points apply if you're using web-hook automation to send signals from the system to an exchange:

Alert Signal Reliability

During extreme market volatility, some broker exchanges may fail to respond to web-hook signals due to traffic overload. While rare, this has occurred in the past and should be considered when relying on automation.

Alert Expiration (TradingView)

If you're on a Basic plan, TradingView alerts are only active for a limited time—typically around 1.5 months. Once expired, signals will no longer be sent out.

To keep your system active, reset the alert before expiration. For uninterrupted alerts, consider upgrading to a Premium plan, which supports permanent alert activation.

TradingView Alert Maintenance

TradingView may occasionally perform system maintenance, during which alerts may temporarily stop functioning. It’s recommended to monitor TradingView’s status if you’re relying on real-time automation.

Repainting

As of the current version, no repainting behaviour has been observed. Signal stability and consistency have been maintained across real-time and historical bars.

Order Execution Type and Fill Logic

All signals use Limit orders by default, except for MBL Exit and Fallback execution, which use Market orders.

Since Limit orders are not guaranteed to fill, the system includes logic to cancel unfilled orders and resend them. If necessary, a Fallback Market order is used to avoid conflict with new incoming trades.

This has only happened once, and is considered rare, but users should always monitor execution status to ensure accuracy and alignment with system behaviour.

Feedback

If you encounter any errors, bugs, or unexpected behaviour while using the system, please don’t hesitate to let me know. Your input is invaluable for helping improve the strategy in future updates.

Likewise, if you have any suggestions or ideas for enhancing the system—whether it’s a new feature, adjustment, or usability improvement—please feel free to share. Together, we can continue refining the tool to make it more robust and beneficial for everyone.

Disclaimer

All trading involves risk, particularly in the crypto market where conditions can be highly volatile. Past performance does not guarantee future outcomes, and market behaviour may evolve over time. This strategy is offered as a tool to support trading decisions and should not be considered financial or investment advice. Each user is responsible for their own actions and accepts full responsibility for any results that may arise from using this system.

Algorithmictrading

TrendR - Algo v6

Overview

The TrendR Algorithm is a sophisticated trend-following trading strategy implemented in Pine Script for TradingView. This professional-grade algorithm combines advanced trend detection, comprehensive risk management, and intelligent market condition filtering to deliver consistent trading performance across various market conditions.

Core Algorithm Architecture

Volatility-Adaptive Band System

The algorithm incorporates a sophisticated volatility measurement system that adapts to changing market conditions.

Intelligent Trend State Management

The TrendR algorithm features a sophisticated trend state tracking system with hysteresis to prevent false signals.

Advanced Risk Management System

Professional 1:3 Risk-Reward Framework

The algorithm implements a comprehensive risk management system designed for professional trading.

Customizable Risk-Reward Ratios : Default 1:3 ratio with user adjustment from 1:1 to 1:10

Percentage-Based Stop Loss : Configurable stop loss distance as a percentage of entry price (default: 2%)

Dual Take Profit Methods :

- Risk-reward ratio based calculation (recommended for consistent risk management)

- Fixed percentage take profit for advanced users requiring specific targets

Automatic Order Management : Seamless integration with TradingView's strategy engine for precise execution

Position Management Features

Entry Price Tracking : Precise entry price recording for accurate SL/TP calculations

Dynamic Level Updates : Real-time calculation and display of stop loss and take profit levels

Position Size Control : Configurable position sizing based on account equity percentage (default: 1%)

Commission and Slippage : Built-in consideration for realistic trading costs (0.1% commission, 3 ticks slippage)

Risk Management Calculations

The system employs sophisticated mathematical models for risk calculation:

Stop Loss Distance : Calculated as percentage of entry price for consistent risk exposure

Take Profit Distance : Dynamically calculated based on stop loss distance multiplied by risk-reward ratio

Position Sizing : Maintains consistent risk per trade through percentage-based allocation

Risk-Adjusted Returns : Optimizes for risk-adjusted performance rather than absolute returns

Entry and Exit Management

Automatic Position Closure : Intelligently closes opposing positions before entering new trades

Risk Management Integration : Automatically places stop loss and take profit orders upon entry

Order Sequencing : Ensures proper order execution sequence to prevent position conflicts

Alert System : Comprehensive alert notifications for entry, exit, and risk management events

Signal Quality Enhancement

The algorithm incorporates multiple layers of signal filtering:

Volatility Filtering : Adjusts signal sensitivity based on current market volatility

Trend Strength Assessment : Evaluates trend momentum before signal generation

False Signal Reduction : Employs hysteresis mechanism to prevent whipsaw trades

Market Condition Awareness : Adapts signal generation to current market regime

Visual Enhancement System

Chart Visualization Features

The TrendR algorithm provides extensive visual feedback for enhanced trading decision-making:

Trend Line Plotting : Dynamic trend lines with color-coded direction indication

Basis Line Display : Central reference line showing the calculated trend basis

Support/Resistance Levels : Visual representation of dynamic support and resistance levels

Risk Management Levels : Clear display of stop loss and take profit levels with color coding

Color-Coded Market States

Bullish Trend : Green coloring system for upward trend conditions

Bearish Trend : Red coloring system for downward trend conditions

Gradient Background : Intensity-based background coloring showing trend strength progression

Bar Coloring : Optional candlestick coloring based on current trend direction

Information Display System

Signal Labels : Clear entry point markers with integrated risk management information

Risk Management Table : Real-time display of current position parameters and risk metrics

Dynamic Updates : Live updating of all visual elements as market conditions evolve

Performance Metrics : Visual representation of strategy performance statistics

Risk Management Configuration

Enable/Disable Toggle : Complete control over risk management system activation

Risk-Reward Ratio : Customizable from 1:1 to 1:10 with 0.1 increments (default: 1:3)

Stop Loss Percentage : Adjustable from 0.1% to 10% with 0.1% increments (default: 2%)

Take Profit Method : Choice between ratio-based or fixed percentage calculation

Fixed Take Profit : Alternative percentage-based take profit (range: 0.1%-20%, default: 6%)

Visualization Controls

Color Customization : User-defined colors for bullish and bearish market conditions

Display Toggles : Individual control over bars, background, signals, and risk levels

Chart Elements : Selective display of various algorithm components

Information Table : Configurable display of real-time strategy metrics

Alert and Notification System

Comprehensive Alert Framework

The TrendR algorithm provides multiple alert types for different trading scenarios:

Entry Signals : Immediate notifications for long and short entry opportunities

Risk Management Alerts : Specific alerts for positions with active risk management

Position Risk Alerts : Advanced warnings when positions approach stop loss levels

Strategy Alerts : Dynamic alerts with real-time risk management data integration

Alert Message Architecture

Static Alerts : Consistent alert messages for basic signal notifications (compatible with Pine Script requirements)

Dynamic Strategy Alerts : Real-time data including entry prices, SL/TP levels, and risk ratios

Risk Event Alerts : Specialized notifications for stop loss and take profit activations

Market Condition Alerts : Notifications for significant market regime changes

Performance Characteristics

Optimal Market Conditions

The TrendR algorithm demonstrates exceptional performance in:

Trending Markets : Clear directional moves with sustained momentum and defined trend channels

Medium to Long-term Timeframes : Reduced noise environment with clearer trend identification

Volatile Assets : Benefits from volatility-adaptive band system and dynamic risk management

Liquid Markets : Optimal execution environment with minimal slippage impact

Algorithm Strengths

Trend Following Excellence : Captures major market moves with minimal lag through advanced EMA system

Risk Management Integration : Professional-grade position protection with customizable parameters

Market Adaptability : Automatically adjusts to changing market volatility conditions

Visual Clarity : Comprehensive chart visualization system for enhanced decision support

Customization Flexibility : Extensive parameter adjustment capabilities for different trading styles

Performance Metrics

Win Rate Optimization : Designed to maximize risk-adjusted returns rather than win percentage

Drawdown Control : Risk management system limits maximum position risk exposure

Profit Factor Enhancement : 1:3 risk-reward ratio improves overall profit factor

Consistency : Standardized risk per trade creates predictable performance patterns

Implementation Details

Technical Specifications

Platform : TradingView Pine Script v6 with full strategy functionality

Strategy Type : Overlay strategy with integrated risk management system

Position Sizing : Percentage of equity based with configurable allocation

Commission Model : Percentage-based commission structure with realistic slippage modeling

Execution Model : Market orders with automatic stop loss and take profit placement

Backtesting Framework

Date Range Control : Configurable start and end dates for comprehensive historical testing

Performance Metrics : Detailed strategy performance analysis with risk-adjusted metrics

Risk Analytics : Comprehensive risk measurement including maximum drawdown and Sharpe ratio

Trade Analysis : Individual trade performance tracking with entry/exit analysis

Code Architecture

The implementation follows professional software development principles:

Modular Design : Separate functions for trend calculation, risk management, and visualization

Single Responsibility : Each function handles a specific aspect of the algorithm

Clean Code Structure : Well-organized sections with comprehensive commenting

Error Handling : Robust handling of edge cases and market conditions

Implementation

Cumulative Intraday Volume with Long/Short LabelsThis indicator calculates a running total of volume for each trading day, then shows on the price chart when that total crosses levels you choose. Every day at 6:00 PM Eastern Time, the total goes back to zero so it always reflects only the current day’s activity. From that moment on, each time a new candle appears the indicator looks at whether the candle closed higher than it opened or lower. If it closed higher, the candle’s volume is added to the running total; if it closed lower, the same volume amount is subtracted. As a result, the total becomes positive when buyers have dominated so far today and negative when sellers have dominated.

Because futures markets close at 6 PM ET, the running total resets exactly then, mirroring the way most intraday traders think in terms of a single session. Throughout the day, you will see this running total move up or down according to whether more volume is happening on green or red candles. Once the total goes above a number you specify (for example, one hundred thousand contracts), the indicator will place a small “Long” label at that candle on the main price chart to let you know buying pressure has reached that level. Similarly, once the total goes below a negative number you choose (for example, minus one hundred thousand), a “Short” label will appear at that candle to signal that selling pressure has reached your chosen threshold. You can set these threshold numbers to whatever makes sense for your trading style or the market you follow.

Because raw volume alone never turns negative, this design uses candle direction as a sign. Green candles (where the close is higher than the open) add volume, and red candles (where the close is lower than the open) subtract volume. Summing those signed volume values tells you in a single number whether buying or selling has been stronger so far today. That number resets every evening, so it does not carry over any buying or selling from previous sessions.

Once you have this indicator on your chart, you simply watch the “summed volume” line as it moves throughout the day. If it climbs past your long threshold, you know buyers are firmly in control and a long entry might make sense. If it falls past your short threshold, you know sellers are firmly in control and a short entry might make sense. In quieter markets or times of low volume, you might use a smaller threshold so that even modest buying or selling pressure will trigger a label. During very active periods, a larger threshold will prevent too many signals when volume spikes frequently.

This approach is straightforward but can be surprisingly powerful. It does not rely on complex formulas or hidden statistical measures. Instead, it simply adds and subtracts daily volume based on candle color, then alerts you when that total reaches levels you care about. Over several years of historical testing, this formula has shown an ability to highlight moments when intraday sentiment shifts decisively from buyers to sellers or vice versa. Because the indicator resets every day at 6 PM, it always reflects only today’s sentiment and remains easy to interpret without carrying over past data. You can use it on any intraday timeframe, but it works especially well on five-minute or fifteen-minute charts for futures contracts.

If you want a clear gauge of whether buyers or sellers are dominating in real time, and you prefer a rule-based method rather than a complex model, this indicator gives you exactly that. It shows net buying or selling pressure at a glance, resets each session like most intraday traders do, and marks the moments when that pressure crosses the levels you decide are important. By combining a daily reset with signed volume, you get a single number that tells you precisely what the crowd is doing at any given moment, without any of the guesswork or hidden calculations that more complicated indicators often carry.

Altcoins DCA ScalperIntroduction

The Altcoins DCA Scalper is a Pine Strategy Script designed to automate Altcoins trading through 3Commas integration. It implements a Dollar-Cost Averaging (DCA) strategy that expands upon 3Commas' standard DCA capabilities, helping to manage risk while trading both long and short positions automatically.

This tool aims to assist both beginners exploring automated trading and experienced 3Commas users seeking dynamic DCA automation. The script is specifically designed for the 1-minute timeframe , where it has shown a good balance between performance and risk management. Complete setup typically takes less than 10 minutes, with a detailed guide making configuration straightforward for users of all experience levels.

------------------------------

🔶 What is DCA?

------------------------------

Dollar-cost averaging (DCA) refers to the practice of gradually increasing your position size at lower prices when trading long, or at higher prices when trading short, to achieve a better average entry price if the market moves against the initial entry . Instead of investing all capital at once, which could result in a significant drawdown if the price moves unfavorably, DCA spreads entries across different price levels to help manage potential drawdowns as they occur.

In this script, DCA is implemented through a system that:

🔹 Triggers safety orders only when/if needed (if take profit isn't reached quickly)

🔹 Dynamically adjusts order sizing based on market volatility

🔹 Automatically reduces take profit targets after each DCA order to increase the likelihood of a positive outcome

🔹 Can handle drawdowns depending on market volatility and settings

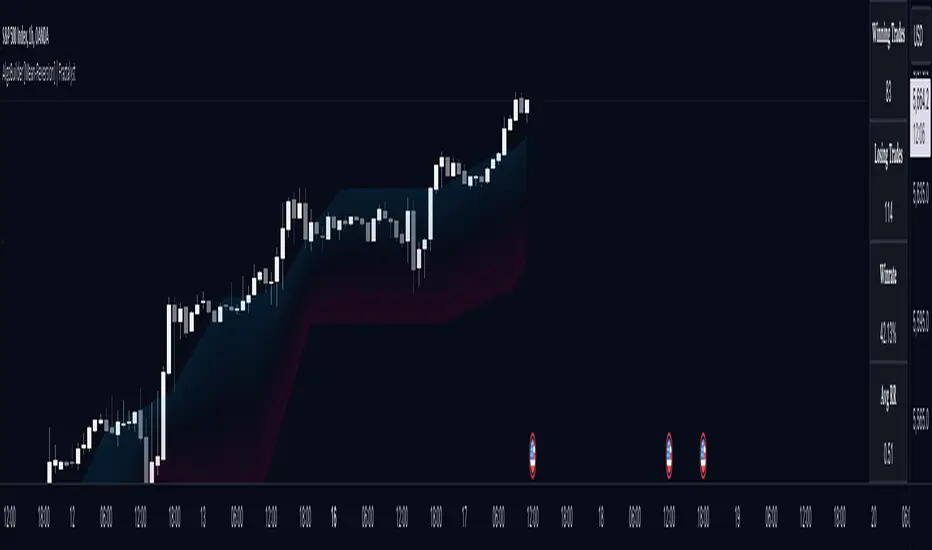

The images below illustrate two scenarios: one where an entry reaches the take profit directly, without activating DCA orders, and another where DCA is utilized, with the order closing positively after two DCA orders.

Case 1: Order closes in profit after entry

Case 2: Order closes in profit after 2 DCA orders (dynamically placed based on trend and volatility)

This DCA implementation aims to enhance standard 3Commas DCA by adding market-adaptive features while maintaining risk management principles.

------------------------------

🔶 Could this strategy script benefit you?

------------------------------

This script may be helpful if you are:

✅ Looking to automate your trading through 3Commas integration while maintaining full control of your assets

✅ Wanting to enhance 3Commas' standard DCA with market-adaptive features that consider:

Multi-timeframe trend analysis

Real-time volatility assessment

Dynamic safety order sizing and timing

✅ Seeking to minimize chart monitoring through full automation of:

Entry and exit decisions

Safety order management

Risk controls

✅ Interested in comprehensive performance tracking with:

Real-time position metrics

Detailed backtesting capabilities

Risk/reward analysis

Backtesting Metrics (script performance over the backtesting period - which is approx. 15 days on the 1min timeframe with the TradingView Pro Plan):

Current/Open Deal Metrics (the deal is currently under DCA, and waiting for further actions to close):

✅ Looking for trading automation that remains easy to set up and use

Note: While this script provides trading automation, successful trading requires proper education, risk management, and regular performance monitoring. No automated tool can guarantee trading success or profits.

------------------------------

🔶 How it Works

------------------------------

The Altcoins DCA Scalper provides trading automation through:

Market Analysis

* Multi-timeframe trend analysis (1m to 1d) for market direction and entry validation

* Volatility assessment (1h, 4h, 24h) benchmarked against TOTAL3 (excluding Top10 Altcoins and Stablecoins)

* Real-time adjustment of DCA parameters based on:

* Current volatility class (low/medium/high) vs. overall Altcoins market

* Market trend strength

* Price action dynamics

Trading Execution

* Position opening aligned with detected market trends

* "Beast Mode" base order sizing that increases position size during strong trends

* Dynamic take-profit targets that automatically reduce after each safety order to increase the likelihood of positive exits

* Dynamic DCA with safety orders that can:

* Adapt timing based on volatility

* Scale order sizes based on market conditions

* Handle 30-50% drawdowns depending on volatility class

* Execute up to 6 safety orders per position

Risk Management

* Emergency exits during extreme market events:

* "Black Swan" protection for long positions

* "God-Candle" protection for short positions

* Configurable stop-loss with volatility-based placement

* Trend-switch management with automated position reversal

* Position aging controls to prevent capital lock-up

* Leveraged trading protection with a pre-liquidation exit system

Integration & Automation

* Quick setup with two 3Commas bots (typically under 10 minutes)

* Fully automated signal generation and execution through 3Commas

* Detailed performance tracking including:

* Real-time position metrics

* DCA depth analysis

* Win rate and ROE calculations

* Pre-configured settings optimized for most pairs

* Multiple customization options for experienced users

Note: While this strategy employs automation and risk management, trading always carries the risk of loss. No system can guarantee profits, and market conditions significantly impact performance. Always do your own research and monitor your positions closely.

------------------------------

How to Use

------------------------------

Setting up the Altcoins DCA Scalper is quick and facilitated by the User Interface:

1️⃣ 3Commas/TradingView Setup

* Create two 3Commas accounts if using the FREE plan:

* One account for Long Bot

* One account for Short Bot

* This split allows full functionality while staying within 3Commas' free tier limits

* You do not need two separate accounts if you have a Paid 3Commas subscription

* While a free TradingView account works with the script, it limits you to one trading pair and a 4-day backtesting history. A paid TradingView subscription removes these limitations (such as the "Essential" plan).

2️⃣ Bot Configuration

* Create one Long and one Short DCA Bot in 3Commas

* Follow the setup guide available in the script itself for hassle-free configuration

* Copy Bot IDs and Email Token for script connection

* No complex settings needed - the script manages all DCA parameters by itself

3️⃣ Script Implementation

* Apply the script to your TradingView charts

* Use the built-in backtesting to analyze performance on different pairs

* Focus on USDT.P futures pairs with good volatility

4️⃣ Trading Activation

* Create TradingView alerts for each trading pair you want to activate

* Example: Set an alert for BINANCE: XRPUSDT.P following the in-script guide

* The script automatically manages all aspects:

* Entry and exit decisions

* DCA execution

* Risk management

* Position monitoring

Capital Requirements

* Important: Ensure sufficient capital to cover all activated pairs

* Consider volatility class when allocating capital to specific pairs

Once setup is complete, the script operates fully automatically while you maintain complete control of your funds through 3Commas and your exchange.

Note: While the setup is straightforward, always start with a small number of pairs and monitor performance before expanding. Trade responsibly and never risk more than you can afford to lose.

------------------------------

Explaining the Settings

------------------------------

The Altcoins DCA Scalper offers mulitple customization options during the setup process. All settings include detailed tooltips and default values.

Core Settings Sections:

1️⃣ 3Commas Connection

* Bot IDs and Email Token configuration

* Leverage settings (1x to 5x supported)

* Detailed 3Commas bot setup guide included

* Automatic bot control configuration

2️⃣ Trading Parameters

* Capital allocation per trade

* Timeframe verification

* Alert system setup

* Backtesting period control

* Performance tracking preferences

3️⃣ Advanced Features

🔹 Risk Management Suite

* Emergency exit controls (to strengthen protection against extraordinary market events)

* Customizable stop-loss system

* Trend-based exit management

* Position aging controls

* Liquidation protection features

* Advanced DCA controls

🔹 Performance Analytics

* Real-time position monitoring

* Comprehensive backtesting metrics

* DCA depth analysis

* Win rate calculations

* Capital efficiency tracking

🔹 Technical Optimizations

* Exchange minimum order adjustment

* Trading pair name override capability

* System stability controls

* Error handling mechanisms

🔹 Interface Customization

* Theme selection

* Chart overlay options

* Warning display preferences

* Performance metrics visibility

All settings come pre-configured but can be fully customized based on your trading preferences and risk tolerance. The script includes tooltips and setup guides for each option.

Note: While default settings may be tested, market conditions vary and all trading involves risk. Monitor performance and adjust settings according to your risk management requirements.

------------------------------

Frequently Asked Questions

------------------------------

Here are some common questions you may have, and our answers:

❓ Is this tool only for experts? I'm new to algo trading, can I use it?

No, the Altcoins DCA Scalper could be used by both beginners and experienced traders. The setup process is guided, and the algorithm handles all the calculations in the background.

❓ I'm not familiar with 3Commas. Is that a problem?

While the script is designed to work with 3Commas, a step-by-step guide is provided within the script to help you set up your 3Commas accounts and bots, if needed.

❓ Do I need to constantly monitor the script after it's set up?

No, after the initial setup and configuration, the script operates autonomously. It handles all aspects of trading including entries, exits, DCA management, and risk controls. However, we recommend:

* Checking performance metrics daily

* Reviewing position statistics weekly

* Adjusting pair selection monthly based on performance

* Monitoring overall market conditions that might require adjustments

❓ Can I use it with leverage?

Yes, the script is designed to work with leverage up to 5x on perpetual futures pairs (USDT.P). It includes specific features for leveraged trading:

* Dynamic safety order placement based on distance to liquidation

* Pre-liquidation exit system to minimize exchange fees

* Adjustable take-profit targets optimized for leveraged positions

* Emergency exit system for extreme market movements

* Optional risk controls specific to leverage:

* Automatic exit in the liquidation danger zone

* Position size scaling based on leverage level

* Safety order adjustments for different leverage settings

While leverage can amplify returns, it also increases risk. We recommend starting with lower leverage (2x), or no leverage at all, until familiar with the script's operation.

❓ Does this script guarantee profits?

No, no script or trading strategy can guarantee profits. The Altcoins DCA Scalper provides a framework for implementing an automated DCA strategy, but your success will depend on many different factors and conditions.

❓ Do I need to understand the complex algorithms used in the script?

No, it’s not necessary. The logic is handled by the script, and you do not need to understand every detail to use it effectively. However, a basic knowledge of DCA concepts will be beneficial.

❓ Can I use this script with spot or leveraged trades?

The script is optimized for USDT.P pairs (perpetual futures) with leverage up to 5x. This allows:

* Automatic long/short position management

* Increased capital utilization

* Full DCA functionality without holding the underlying assets

* Enhanced risk management features specific to futures

While spot trading is possible, it requires holding underlying assets for shorts and doesn't access the script's full capabilities.

❓What timeframe should I use?

This script is optimized for the 1-minute timeframe , which is the recommended setting for the best balance between performance, capital efficiency, and risk. While we recommend using the tool on the 1 minute TF, it would work on other timeframes too.

❓ What happens if my internet/computer goes down?

Since the script sends signals from Tradingview to 3Commas (which executes trades on your exchange), your positions and DCA management continue to function even if your TradingView chart is closed or your computer is off. The script only needs to be active to generate new signals.

❓ How are the DCA parameters determined?

The script dynamically adjusts DCA parameters based on:

* The pair's volatility class (compared to the overall altcoin market)

* Current market conditions and volatility

* Position direction (long/short)

* Leverage settings

* Number of safety orders already executed

This allows for adaptive/dynamic DCA compared to static or %-based parameters.

❓ What exchanges are supported?

The script works with any exchange supported by 3Commas for futures trading (approximately 15 different crypto Exchanges). However, it's optimized for Binance Futures (USDT.P pairs) due to its high liquidity and for consistency.

❓ What happens during extreme market conditions?

The script includes some (optional) protective measures that can be activated:

* Emergency exits during sharp and abnormal market moves

* Automatic adjustment of DCA parameters during high volatility

* Position closure on significant trend changes

* Special handling of aged positions

These features aim to protect capital during unusual market conditions.

❓How many pairs can I trade simultaneously?

This depends on your total capital. As a general indication, define the number of pairs to activate based on:

* Total available capital

* Desired position size per pair

* Risk tolerance

* Pairs' volatility class

------------------------------

Final Thoughts

------------------------------

We believe that your trading performance will greatly depend on your selection of appropriate trading pairs for this script (high volatility), and your commitment to regularly monitoring its performance and adjust the settings, rather than on the script alone.

------------------------------

⚠️ Risk Disclaimer

------------------------------

Remember that trading involves risk, and most day traders experience losses. This script is for educational and informational purposes only. Past performance does not guarantee future results. This is not financial advice, and you should always do your own research (DYOR). Trade responsibly with capital you can afford to lose.

The Altcoins DCA Scalper is an independent tool and is not endorsed, connected, or validated by TradingView.

3Commas is a third-party service, and TradingView is not responsible for the 3Commas integration or the performance of 3Commas bots. You are solely responsible for the security and management of your 3Commas account. Do not share your 3Commas access credentials (like login information, Bots-ID, Email Token) with anyone. The Author of the script has no access to such information, and nobody (but you) should.

QuantBuilder | FractalystWhat's the strategy's purpose and functionality?

QuantBuilder is designed for both traders and investors who want to utilize mathematical techniques to develop profitable strategies through backtesting on historical data.

The primary goal is to develop profitable quantitive strategies that not only outperform the underlying asset in terms of returns but also minimize drawdown.

For instance, consider Bitcoin (BTC), which has experienced significant volatility, averaging an estimated 200% annual return over the past decade, with maximum drawdowns exceeding -80%. By employing this strategy with diverse entry and exit techniques, users can potentially seek to enhance their Compound Annual Growth Rate (CAGR) while managing risk to maintain a lower maximum drawdown.

While this strategy employs quantitative techniques, including mathematical methods such as probabilities and positive expected values, it demonstrates exceptional efficacy across all markets. It particularly excels in futures, indices, stocks, cryptocurrencies, and commodities, leveraging their inherent trending behaviors for optimized performance.

In both trending and consolidating market conditions, QuantBuilder employs a combination of multi-timeframe probabilities, expected values, directional biases, moving averages and diverse entry models to identify and capitalize on bullish market movements.

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

1. Trading:

- Designed for traders looking to capitalize on bullish markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for both swing and intraday trading with a focus on probabilities and risk per trade approach.

2. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully/partially investing in the asset during bullish conditions.

How does the strategy identify market structure? What are the underlying calculations?

The strategy utilizes an efficient logic with for loops to pinpoint the first swing candle featuring a pivot of 2, establishing the point at which the break of structure begins.

What entry criteria are used in this script? What are the underlying calculations?

The script utilizes two entry models: BreakOut and fractal.

Underlying Calculations:

Breakout: The script assigns the most recent swing high to a variable. When the price closes above this level and all other conditions are met, the script executes a breakout entry (conservative approach).

Fractal: The script identifies a swing low with a period of 2. Once this condition is met, the script executes the trade (aggressive approach).

How does the script calculate probabilities? What are the underlying calculations?

The script calculates probabilities by monitoring price interactions with liquidity levels. Here’s how the underlying calculations work:

Tracking Price Hits: The script counts the number of times the price taps into each liquidity side after the EQM level is activated. This data is stored in an array for further analysis.

Sample Size Consideration: The total number of price interactions serves as the sample size for calculating probabilities.

Probability Calculation: For each liquidity side, the script calculates the probability by taking the average of the recorded hits. This allows for a dynamic assessment of the likelihood that a particular side will be hit next, based on historical performance.

Dynamic Adjustment: As new price data comes in, the probabilities are recalculated, providing real-time aduptive insights into market behavior.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

How does the script calculate expected values? What are the underlying calculations?

The script calculates expected values by leveraging the probabilities of winning and losing trades, along with their respective returns. The process involves the following steps:

This quantitative methodology provides a robust framework for assessing the expected performance of trading strategies based on historical data and backtesting results.

How is the contextual bias calculated? What are the underlying calculations?

The contextual bias in the QuantBuilder script is calculated through a structured approach that assesses market structure based on swing highs and lows. Here’s how it works:

Identification of Swing Points: The script identifies significant swing points using a defined pivot logic, focusing on the first swing high and swing low. This helps establish critical levels for determining market structure.

Break of Structure (BOS) Assessment:

Bullish BOS: The script recognizes a bullish break of structure when a candle closes above the first swing high, followed by at least one swing low.

Bearish BOS: Conversely, a bearish break of structure is identified when a candle closes below the first swing low, followed by at least one swing high.

Bias Assignment: Based on the identified break of structure, the script assigns directional biases:

A bullish bias is assigned if a bullish BOS is confirmed.

A bearish bias is assigned if a bearish BOS is confirmed.

Quantitative Evaluation: Each identified bias is quantitatively evaluated, allowing the script to assign numerical values representing the strength of each bias. This quantification aids in assessing the reliability of market sentiment across multiple timeframes.

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

- Initial Stop-loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14)

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

- Trailing Stop-Loss:

One of the key elements of this strategy is its ability to detect structural liquidity and structural invalidation levels across multiple timeframes to trail the stop-loss once the trade is in running profits.

By utilizing this approach, the strategy allows enough room for price to run.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

What tables are available in this script?

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Total Commission: Displays the cumulative commissions incurred from all trades executed within the selected backtesting window. This value is derived by summing the commission fees for each trade on your chart.

Average Commission: Represents the average commission per trade, calculated by dividing the Total Commission by the total number of closed trades. This metric is crucial for assessing the impact of trading costs on overall profitability.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month and year.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- UI Table: A user-friendly table that allows users to view and save the selected strategy parameters from user inputs. This table enables easy access to key settings and configurations, providing a straightforward solution for saving strategy parameters by simply taking a screenshot with Alt + S or ⌥ + S.

User-input styles and customizations:

To facilitate studying historical data, all conditions and filters can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

How to Use This Quantitive Strategy Builder to Create a Profitable Edge and System?

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker/prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 200 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

What makes this strategy original?

QuantBuilder stands out due to its unique combination of quantitative techniques and innovative algorithms that leverage historical data for real-time trading decisions. Unlike most algorithmic strategies that work based on predefined rules, this strategy adapts to real-time market probabilities and expected values, enhancing its reliability. Key features include:

Mathematical Framework: The strategy integrates advanced mathematical concepts, such as probabilities and expected values, to assess trade viability and optimize decision-making.

Multi-Timeframe Analysis: By utilizing multi-timeframe probabilities, QuantBuilder provides a comprehensive view of market conditions, enhancing the accuracy of entry and exit points.

Dynamic Market Structure Identification: The script employs a systematic approach to identify market structure changes, utilizing a blend of swing highs and lows to detect contextual/direction bias of the market.

Built-in Trailing Stop Loss: The strategy features a dynamic trailing stop loss based on multi-timeframe analysis of market structure. This allows traders to lock in profits while adapting to changing market conditions, ensuring that exits are executed at optimal levels without prematurely closing positions.

Robust Performance Metrics: With detailed performance tables and visualizations, users can easily evaluate strategy effectiveness and adjust parameters based on historical performance.

Adaptability: The strategy is designed to work across various markets and timeframes, making it versatile for different trading styles and objectives.

Suitability for Investors and Traders: QuantBuilder is ideal for both investors and traders looking to rely on mathematically proven data to create profitable strategies, ensuring that decisions are grounded in quantitative analysis.

These original elements combine to create a powerful tool that can help both traders and investors to build and refine profitable strategies based on algorithmic quantitative analysis.

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

BE-NSE-Distributed Straddle Intraday Trading StrategyHerewith publishing the script (not the Indicator!) for the benift of Option Traders. I call this a script as this doesn't perform any kind of analysis of candle data and provide general BUY | SELL information. This Script is based on the TRUE VALUES concept which is nothing but LTP.

Idea Behind this Script:

As an option seller i need the lower risk option premium to trade. so that, time can work in our favor. basic question which we get at the first is which option to choose out of many available.

If traders feel the question is apt then this script is for them.

Logic Behind this script:

Upon Market Open, script in the BACKEND ( Under the hood ) deployes 60 possible combinations of STRADDLES for sampling, and continue to monitor the LTP movements and compares it against opposite pairs. lets say out of 30 Straddle options one of the Straddle it picked is ATM CE VS ATM PE. for 1 rs move in underlying how much impact is happening in CE VS PE.

This simple anlysis is done at every 30 seconds. once the Analysis is complete it picks 4 options 2 on the CALL side and 2 on the PUT side, which script feels the movement of prices are smooth. SMOOTH refers that time decay that can work in our favor..

Calculations behid the script:

lets say BNF LTP is 52000 at 9:20 AM, and one of the pair script took for sampling was ATM CE vs PE which are having the LTP of 100 each.

At 9:35 AM, BNF is trading at 52075, and ATM CE is reading the LTP of 122 and ATM PUT is reading the LTP of 70. ideally LTP of Call should be around 135 and Put should be around 65 considering the usual delta of 0.48 . Net Money Index for this Pair Sample is 8

Call Side => 100 - 122 = -22

Put Side => 100 - 70 = 30

Money Index => 30 - 22 = 8 for 15 Min

This Money index is calculated across choosen samples and the Option strikes is provided as an output which has mere possiblity of working in Options Seller's favor.

How to Read the Output:

For the choosen strikes from the time of Entry (Suggested Entry time by script) till the current time, the bottom pane plots the Money index as columns. Green Columns indicate that how much option premium eroded due to time decay. Red Columns indicate that how much Option premium increased during the time.

Note: Script dynamically calculate the strikes and suggests in realtime.

WARNING or a Humble Request:

For those who don't understand the word "Repaint" how it works in Pine Script. plz don't consider using this script. For those who wish to understand I have kept the Observer mode in the settings which shall guide you on why the Money Index shown on the chart when the MARKET IS CLOSED is different than when the MARKET IS OPEN (Realtime).

Disclaimer:

I have tested the script only in BNF and not sure if this works on Nifty, FinNifty or others. you may still try and plz do provide the feedback for improvising the script.

----- BreathEasy --------

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

AlgoBuilder [Mean-Reversion] | FractalystWhat's the strategy's purpose and functionality?

This strategy is designed for both traders and investors looking to rely and trade based on historical and backtested data using automation.

The main goal is to build profitable mean-reversion strategies that outperform the underlying asset in terms of returns while minimizing drawdown.

For example, as for a benchmark, if the S&P 500 (SPX) has achieved an estimated 10% annual return with a maximum drawdown of -57% over the past 20 years, using this strategy with different entry and exit techniques, users can potentially seek ways to achieve a higher Compound Annual Growth Rate (CAGR) while maintaining a lower maximum drawdown.

Although the strategy can be applied to all markets and timeframes, it is most effective on stocks, indices, future markets, cryptocurrencies, and commodities and JPY currency pairs given their trending behaviors.

In trending market conditions, the strategy employs a combination of moving averages and diverse entry models to identify and capitalize on upward market movements. It integrates market structure-based moving averages and bands mechanisms across different timeframes and provides exit techniques, including percentage-based and risk-reward (RR) based take profit levels.

Additionally, the strategy has also a feature that includes a built-in probability function for traders who want to implement probabilities right into their trading strategies.

Performance summary, weekly, and monthly tables enable quick visualization of performance metrics like net profit, maximum drawdown, profit factor, average trade, average risk-reward ratio (RR), and more.

This aids optimization to meet specific goals and risk tolerance levels effectively.

-----

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

Trading:

1. Trading:

- Designed for traders looking to capitalize on bullish trending markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for active trading with a focus on mean-reversion and risk per trade approach.

◓: Mode | %: Risk percentage per trade

3. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully investing in the asset during bullish conditions.

- ◓: Mode | %: Risk not applied (In investing mode, the strategy uses 10% of equity to buy the asset)

-----

What's is FRMA? How does the triple bands work? What are the underlying calculations?

Middle Band (FRMA):

The middle band is the core of the FRMA system. It represents the Fractalyst Moving Average, calculated by identifying the most recent external swing highs and lows in the market structure.

By determining these external swing pivot points, which act as significant highs and lows within the market range, the FRMA provides a unique moving average that adapts to market structure changes.

Upper Band:

The upper band shows the average price of the most recent external swing highs.

External swing highs are identified as the highest points between pivot points in the market structure.

This band helps traders identify potential overbought conditions when prices approach or exceed this upper band.

Lower Band:

The lower band shows the average price of the most recent external swing lows.

External swing lows are identified as the lowest points between pivot points in the market structure.

The script utilizes this band to identify potential oversold conditions, triggering entry signals as prices approach or drop below the lower band.

Adjustments Based on User Inputs:

Users can adjust how the upper and lower bands are calculated based on their preferences:

Upper/Lower: This method calculates the average bands using the prices of external swing highs and lows identified in the market.

Percentage Deviation from FRMA: Alternatively, users can opt to calculate the bands based on a percentage deviation from the middle FRMA. This approach provides flexibility to adjust the width of the bands relative to market conditions and volatility.

-----

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

This comparison filter can be turned on (>) or off.

For example, you can set the filter so that MA#1 > MA#2, meaning the first moving average must be above the second one before the script looks for entry conditions. This adds an extra layer of trend confirmation, ensuring that trades are only taken in more favorable market conditions.

⍺: MA Period | Σ: MA Timeframe

-----

What entry modes are used in this strategy? What are the underlying calculations?

The strategy by default uses two different techniques for the entry criteria with user-adjustable left and right bars: Breakout and Fractal.

1. Breakout Entries :

- The strategy looks for pivot high points with a default period of 3.

- It stores the most recent high level in a variable.

- When the price crosses above this most recent level, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot high left bars period | ◨: Pivot high right bars period

2. Fractal Entries :

- The strategy looks for pivot low points with a default period of 3.

- When a pivot low is detected, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot low left bars period | ◨: Pivot low right bars period

2. Hunt Entries :

- The strategy identifies a candle that wicks through the lower FRMA band.

- It waits for the next candle to close above the low of the wick candle.

- When this condition is met and the bar is closed, the strategy takes the buy entry.

By utilizing these entry modes, the strategy aims to capitalize on bullish price movements while ensuring that the necessary conditions are met to validate the entry points.

-----

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

Initial Stop-Loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14).

Example - ATR (14) * 2

⍺: ATR period | Σ: ATR Multiplier

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

Example - ADR (20) * 2

⍺: ADR period | Σ: ADR Multiplier

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

Application in Strategy (ATR/ADR):

- The strategy calculates the current bar's ADR/ATR with a user-defined period.

- It then multiplies the ADR/ATR by a user-defined multiplier to determine the initial stop-loss level.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

-----

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

Example:

If the entry price is $100, the initial risk is $10, and the RR ratio is 2, the break-even level is $100 + ($10 * 2) = $120.

FRMA Based:

Moves the stop-loss to break-even when the price hits the FRMA level at which the entry was taken.

Calculation:

Break-even level = FRMA level at the entry

Example:

If the FRMA level at entry is $102, the break-even level is set to $102 when the price reaches $102.

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

When Both Percentage (%) Based and RR Based Take Profit Levels Are Off:

The script will adjust the take profit level to the higher FRMA band set within user inputs.

Calculation: