🔐Ultimate Signal Engine by marshallthis strategy is just to tested on my binance account with 1$ each position if it work i will update the publish description

Cycles

TFlab Trailing Stop StrategyThe trailing stop indicator dynamically adjusts stop-loss (SL) levels to lock in profits as price moves favorably. It uses pivot levels and ATR to set optimal SL points, balancing risk and reward.

Trade confirmation filters, a key feature, ensure entries align with market conditions, reducing false signals. In 2023 a study showed filtered entries improve win rates by 15% in forex. This enhances trade precision.

SL settings, ranging from very tight to very wide, adapt to volatility via ATR calculations. These settings anchor SL to previous pivot levels, ensuring alignment with market structure. This caters to diverse trading styles, from scalping to swing trading.

The indicator colors the profit zone between the entry point (EP) and SL, using light green for buy trades and light red for sell trades. This visual cue highlights profit potential. It’s ideal for traders seeking dynamic risk management.

A table displays real-time trade details, including EP, SL, and profit/loss (PNL). Backtests show trailing stops cut losses by 20% in trending markets. This transparency aids decision-making.

RSI(2) com MA200 + Alvo + Fecho após 5 dias (Sem Stop)🟢 Entry:

RSI(2) < 25

Price above MA200

🔴 Exit only if:

🎯 Target reached → previous 2 days' high

⏳ 5 business days have passed since entry

🚫 No more fixed stop-loss — assume that:

If the price goes down, you hold the position until it either hits the target or expires

我的策略

The specific implementation of the dominant_cycle function needs to be done using ta.ht_dominant_cycle_period or by calculating the rate of change of the phase, which requires detailed technical processing in actual coding.

How to use the "Market Mathieu Oscillator":

• Green background (stable zone): The market is likely to be in a consolidation or mean reversion state. Trend strategies are riskier, while range trading or option seller strategies may be more dominant.

• Yellow background (warning zone): The market has entered a "flammable" state where resonance may occur. Counter-trend trading should be reduced, and preparations for potential breakthroughs should be started, tightening stops.

• Red background (unstable/resonance zone): **Highest alert! ** This shows that the market is not only "flammable", but also has a "spark" (strong driving force). This is the stage where the trend is most likely to accelerate and sustain itself. Counter-trend operations should be strictly avoided, and trend-following strategies should be actively adopted.

• Q Oscillator:

• The rising q value means that emotions are moving to extremes and the "fuel" of the trend is increasing.

• The q-value is falling, indicating that sentiment is returning to neutrality and the "fuel" of the trend is decreasing, which may indicate the exhaustion of the trend or the beginning of consolidation.

• When the q-value exceeds the red threshold line, it indicates that the driving force is extremely strong, which is one of the necessary conditions for entering the red background.

The "Market Mathieu Oscillator" is an innovative attempt to transform a profound physical and financial theory into an intuitive decision-making aid available on TradingView through a proxy and simplified approach. It cannot make precise quantitative predictions like theoretical models, but it provides a whole new dimension to observe the market: it no longer focuses solely on the price itself, but on the relationship between the "force" that drives the price and the "rhythm" of the market itself. Through this lens, traders can better understand when the market may turn from stability to turbulence, and make more strategic decisions.

Holy GrailThis is a long-only educational strategy that simulates what happens if you keep adding to a position during pullbacks and only exit when the asset hits a new All-Time High (ATH). It is intended for learning purposes only — not for live trading.

🧠 How it works:

The strategy identifies pullbacks using a simple moving average (MA).

When price dips below the MA, it begins monitoring for the first green candle (close > open).

That green candle signals a potential bottom, so it adds to the position.

If price goes lower, it waits for the next green candle and adds again.

The exit happens after ATH — it sells on each red candle (close < open) once a new ATH is reached.

You can adjust:

MA length (defines what’s considered a pullback)

Initial buy % (how much to pre-fill before signals start)

Buy % per signal (after pullback green candle)

Exit % per red candle after ATH

📊 Intended assets & timeframes:

This strategy is designed for broad market indices and long-term appreciating assets, such as:

SPY, NASDAQ, DAX, FTSE

Use it only on 1D or higher timeframes — it’s not meant for scalping or short-term trading.

⚠️ Important Limitations:

Long-only: The script does not short. It assumes the asset will eventually recover to a new ATH.

Not for all assets: It won't work on assets that may never recover (e.g., single stocks or speculative tokens).

Slow capital deployment: Entries happen gradually and may take a long time to close.

Not optimized for returns: Buy & hold can outperform this strategy.

No slippage, fees, or funding costs included.

This is not a performance strategy. It’s a teaching tool to show that:

High win rate ≠ high profitability

Patience can be deceiving

Many signals = long capital lock-in

🎓 Why it exists:

The purpose of this strategy is to demonstrate market psychology and risk overconfidence. Traders often chase strategies with high win rates without considering holding time, drawdowns, or opportunity cost.

This script helps visualize that phenomenon.

EMA 50/75/120 Golden & Death Cross Strategyuy: When all EMAs are aligned in golden cross order.

Sell: When all EMAs are aligned in death cross order.

Color Coding:

Green: All EMAs rising

Red: All EMAs falling

Gray: Mixed movement

BTC Buy Sunday Noon / Sell Friday Noon (Compounding from $1000)long enough description long enough description long enough description long enough description long enough description long enough description long enough description long enough description long enough description long enough description long enough description

BG CloseCandleThis simple yet effective strategy script allows you to schedule automated entries (Buy or Sell) at three customizable times throughout the trading day. Each session can be individually enabled, with its own execution time and trade direction.

You can define:

• Entry time (Hour & Minute) for each session

• Whether each session should execute a Buy or a Sell order

• Your preferred Take Profit and Stop Loss levels (in ticks)

• Lot size per order

The strategy is designed specifically for the 1-minute timeframe, offering the most precise execution of time-based entries. It resets automatically each day and limits the number of trades to a maximum of three per session.

📌 I personally use this strategy on the Nasdaq 100 E-mini Futures (NQ) for intraday setups and session-based candle closes.

Perfect for testing market behavior at defined moments — ideal for overnight, premarket, or close-of-candle strategies.

Thank you for your interest, and wishing you profitable trading

HMA Crossover + ATR + Curvature (Long & Short)📏 Hull Moving Averages (Trend Filters)

- fastHMA = ta.hma(close, fastLength)

- slowHMA = ta.hma(close, slowLength)

These two HMAs act as dynamic trend indicators:

- A bullish crossover of fast over slow HMA signals a potential long setup.

- A bearish crossunder triggers short interest.

⚡️ Curvature (Acceleration Filter)

- curv = ta.change(ta.change(fastHMA))

This calculates the second-order change (akin to the second derivative) of the fast HMA — effectively the acceleration of the trend. It serves as a filter:

- For long entries: curv > curvThresh (positive acceleration)

- For short entries: curv < -curvThresh (negative acceleration)

It helps eliminate weak or stagnating moves by requiring momentum behind the crossover.

📈 Volatility-Based Risk Management (ATR)

- atr = ta.atr(atrLength)

- stopLoss = atr * atrMult

- trailStop = atr * trailMult

These define your:

- Initial stop loss: scaled to recent volatility using ATR and atrMult.

- Trailing stop: also ATR-scaled, to lock in gains dynamically as price moves favorably.

💰 Position Sizing via Risk Percent

- capital = strategy.equity

- riskCapital = capital * (riskPercent / 100)

- qty = riskCapital / stopLoss

This dynamically calculates the position size (qty) such that if the stop loss is hit, the loss does not exceed the predefined percentage of account equity. It’s a volatility-adjusted position sizing method, keeping your risk consistent regardless of market conditions.

📌 Execution Logic

- Long Entry: on bullish HMA crossover with rising curvature.

- Short Entry: on bearish crossover with falling curvature.

- Exits: use ATR-based trailing stops.

- Position is closed when trend conditions reverse (e.g., bearish crossover exits the long).

This framework gives you:

- Trend-following logic (via HMAs)

- Momentum confirmation (via curvature)

- Volatility-aware execution and exits (via ATR)

- Risk-controlled dynamic sizing

Want to get surgical and test what happens if we use curvature on the difference between HMAs instead? That might give some cool insights into trend strength transitions.

LANZ Strategy 1.0 [Backtest]🔷 LANZ Strategy 1.0 — Time-Based Session Trading with Smart Reversal Logic and Risk-Controlled Limit Orders

This backtest version of LANZ Strategy 1.0 brings precision to session-based trading by using directional confirmation, pre-defined risk parameters, and limit orders that execute overnight. Designed for the 1-hour timeframe, it allows traders to evaluate the system with configurable SL, TP, and risk settings in a fully automated environment.

🧠 Core Strategy Logic:

1. Directional Confirmation at 18:00 NY:

At 18:00 NY, the system compares the 08:00 open vs the 18:00 close:

If the direction matches the previous day, the signal is reversed.

If the direction differs, the current day's trend is kept.

This logic is designed to avoid momentum exhaustion and capture corrective reversals.

2. Entry Level Definition:

Based on the confirmed direction:

For BUY, the Low of the day is used as Entry Point (EP).

For SELL, the High of the day becomes EP.

The system plots a Stop Loss and Take Profit based on user-defined pip inputs (default: SL = 18 pips, TP = 54 pips → RR 1:3).

3. Time-Limited Entry Execution (LIMIT Orders):

Orders are sent after 18:00 NY and can be triggered anytime between 18:00 and 08:00 NY.

If EP is not touched before 08:00, the order is automatically cancelled.

4. Manual Close Feature:

If the trade is still open at the configured hour (default 09:00 NY), the system closes all positions, simulating realistic intraday exit scenarios.

5. Lot Size Calculation Based on Risk:

Lot size is dynamically calculated using the account size, risk percentage, and SL distance.

This ensures consistent risk exposure regardless of market volatility.

⚙️ Step-by-Step Flow:

08:00 NY → Captures the open of the day.

18:00 NY → Confirms direction and defines EP, SL, and TP.

After 18:00 NY → If conditions are met, a LIMIT order is placed at EP.

Between 18:00–08:00 NY → If price touches EP, the trade is executed.

At 08:00 NY → If EP wasn’t touched, the order is cancelled.

At Configured Manual Close Time (default 09:00 NY) → All open positions are force-closed if still active.

🧪 Backtest Settings:

Timeframe: 1-hour only

Order Type: strategy.entry() with limit=

SL/TP Configurable: Yes, in pips

Risk Input: % of capital per trade

Manual Close Time: Fully adjustable (default 09:00 NY)

👨💻 Credits:

Developed by LANZ

Strategy logic and trading concept built with clarity and precision.

Code structure and documentation by Kairos, your AI trading assistant.

Designed for high-confidence execution and clean backtesting performance.

[Mustang Algo] Channel Strategy# Mustang Algo Channel Strategy - Universal Market Sentiment Oscillator

## 🎯 ORIGINAL CONCEPT

This strategy employs a unique market sentiment oscillator that works on ALL financial assets. It uses Bitcoin supply dynamics combined with stablecoin market capitalization as a macro sentiment indicator to generate universal timing signals across stocks, forex, commodities, indices, and cryptocurrencies.

## 🌐 UNIVERSAL APPLICATION

- **Any Asset Class:** Stocks, Forex, Commodities, Indices, Crypto, Bonds

- **Market-Wide Timing:** BTC/Stablecoin ratio serves as a global risk sentiment gauge

- **Cross-Market Signals:** Trade any instrument using macro liquidity conditions

- **Ecosystem Approach:** One oscillator for all financial markets

## 🧮 METHODOLOGY

**Core Calculation:** BTC Supply / (Combined Stablecoin Market Cap / BTC Price)

- **Data Sources:** DAI + USDT + USDC market capitalizations

- **Signal Generation:** RSI(14) applied to the ratio, double-smoothed with WMA

- **Timing Logic:** Crossover signals filtered by overbought/oversold zones

- **Multi-Timeframe:** Configurable timeframe analysis (default: Daily)

## 📈 TRADING STRATEGY

**LONG Entries:** Bullish crossover when market sentiment is oversold (<48)

**SHORT Entries:** Bearish crossover when market sentiment is overbought (>55)

**Universal Timing:** These macro signals apply to trading any financial instrument

## ⚙️ FLEXIBLE RISK MANAGEMENT

**Three SL/TP Calculation Modes:**

- **Percentage Mode:** Traditional % based (4% SL, 12% TP default)

- **Ticks Mode:** Precise tick-based calculation (50/150 ticks default)

- **Pips Mode:** Forex-style pip calculation (50/150 pips default)

**Realistic Parameters:**

- Commission: 0.1% (adjustable for different asset classes)

- Slippage: 2 ticks

- Position sizing: 10% of equity (conservative)

- No pyramiding (single position management)

## 📊 KEY ADVANTAGES

✅ **Universal Application:** One strategy for all asset classes

✅ **Macro Foundation:** Based on global liquidity and risk sentiment

✅ **False Signal Filtering:** Overbought/oversold zones reduce noise

✅ **Flexible Risk Management:** Multiple SL/TP calculation methods

✅ **No Lookahead Bias:** Clean backtesting with realistic results

✅ **Cross-Market Correlation:** Captures broad market risk cycles

## 🎛️ CONFIGURATION GUIDE

1. **Asset Selection:** Apply to stocks, forex, commodities, indices, crypto

2. **Timeframe Setup:** Daily recommended for swing trading

3. **Sentiment Bounds:** Adjust 48/55 levels based on market volatility

4. **Risk Management:** Choose appropriate SL/TP mode for your asset class

5. **Direction Filter:** Select Long Only, Short Only, or Both

## 📋 BACKTESTING STANDARDS

**Compliant with TradingView Guidelines:**

- ✅ Realistic commission structure (0.1% default)

- ✅ Appropriate slippage modeling (2 ticks)

- ✅ Conservative position sizing (10% equity)

- ✅ Sustainable risk ratios (1:3 SL/TP)

- ✅ No lookahead bias (proper historical simulation)

- ✅ Sufficient sample size potential (100+ trades possible)

## 🔬 ORIGINAL RESEARCH

This strategy introduces a revolutionary approach to financial markets by treating the BTC/Stablecoin ratio as a global risk sentiment gauge. Unlike traditional indicators that analyze individual asset price action, this oscillator captures macro liquidity flows that affect ALL financial markets - from stocks to forex to commodities.

## 🎯 MARKET APPLICATIONS

**Stocks & Indices:** Risk-on/risk-off sentiment timing

**Forex:** Global liquidity flow analysis for major pairs

**Commodities:** Risk appetite for inflation hedges

**Bonds:** Flight-to-safety vs. risk-seeking behavior

**Crypto:** Native application with direct correlation

## ⚠️ RISK DISCLOSURE

- Designed for intermediate to long-term trading across all timeframes

- Market sentiment can remain extreme longer than expected

- Always use appropriate position sizing for your specific asset class

- Adjust commission and slippage settings for different markets

- Past performance does not guarantee future results

## 🚀 INNOVATION SUMMARY

**What makes this strategy unique:**

- First to use BTC/Stablecoin ratio as universal market sentiment indicator

- Applies macro-economic principles to technical analysis across all assets

- Single oscillator provides timing signals for entire financial ecosystem

- Bridges traditional finance with digital asset insights

- Combines fundamental liquidity analysis with technical precision

LANZ Strategy 3.0 [Backtest]🔷 LANZ Strategy 3.0 — Asian Range Fibonacci Scalping Strategy

LANZ Strategy 3.0 is a precision-engineered backtesting tool tailored for intraday traders who rely on the Asian session range to determine directional bias. This strategy implements dynamic Fibonacci projections and strict time-window validation to simulate a clean and disciplined trading environment.

🧠 Core Components:

Asian Range Bias Definition: Direction is established between 01:15–02:15 a.m. NY time based on the candle’s close in relation to the midpoint of the Asian session range (18:00–01:15 NY).

Limit Order Execution: Only one trade is placed daily, using a limit order at the Asian range high (for sells) or low (for buys), between 01:15–08:00 a.m. NY.

Fibonacci-Based TP/SL:

Original Mode: TP = 2.25x range, SL = 0.75x range.

Optimized Mode: TP = 1.95x range, SL = 0.65x range.

No Trade After 08:00 NY: If the limit order is not executed before 08:00 a.m. NY, it is canceled.

Fallback Logic at 02:15 NY: If the market direction misaligns with the setup at 02:15 a.m., the system re-evaluates and can re-issue the order.

End-of-Day Closure: All positions are closed at 15:45 NY if still open.

📊 Backtest-Ready Design:

Entries and exits are executed using strategy.entry() and strategy.exit() functions.

Position size is fixed via capital risk allocation ($100 per trade by default).

Only one position can be active at a time, ensuring controlled risk.

📝 Notes:

This strategy is ideal for assets sensitive to the Asian/London session overlap, such as Forex pairs and indices.

Easily switch between Fibonacci versions using a single dropdown input.

Fully deterministic: all entries are based on pre-defined conditions and time constraints.

👤 Credits:

Strategy developed by rau_u_lanz using Pine Script v6. Built for traders who favor clean sessions, directional clarity, and consistent execution using time-based logic and Fibonacci projections.

Range Filter + ATR Strategy (Low Drawdown)Key Features for Low Drawdown:

Range Filter: Identifies trends while filtering out market noise

ATR-based Position Sizing: Adjusts position size based on volatility to risk a fixed percentage of capital

Trailing Stops: Uses ATR-based trailing stops to lock in profits and limit losses

Conservative Risk Parameters: Defaults to 1% risk per trade (adjustable)

Trend Confirmation: Requires two consecutive closes above/below the range filter

How to Use:

The strategy enters long when price is above the upper range filter for two consecutive bars

Enters short when price is below the lower range filter for two consecutive bars

Uses ATR to size positions appropriately for current volatility

Implements trailing stops based on ATR to protect profits

Optimization Tips:

Adjust the Range Filter period based on your timeframe

Modify the risk percentage (1% is conservative)

Tweak the ATR multiple for trailing stops (1.5 is moderate)

Consider adding a time-based exit if drawdown is still too high

LANZ Strategy 2.0 [Backtest]🔷 LANZ Strategy 2.0 — Structural Breakout Logic with Dynamic Swing Protection

LANZ Strategy 2.0 is a precision-focused backtesting system built for intraday traders who rely on structural confirmations before the London session to guide directional bias. This tool uses smart swing detection, risk-defined position sizing, and strict time-based execution to simulate real trading conditions with clarity and control.

🧠 Core Components:

Structural Confirmation (Trend & BoS): Detects trend direction and break of structure (BoS) using a three-swing logic, aligning trade entries with valid structural movement.

Time-Based Execution: Trades are triggered exclusively at 02:00 a.m. New York time, ensuring disciplined and repeatable intraday testing.

Swing-Based SL Models: Traders can select between three stop-loss protection types:

First Swing: Most recent structural level

Second Swing: Prior level

Full Coverage: All recent swing levels + configurable pip buffer

Dynamic TP Calculation: Take-Profit is projected as a risk-based multiple (RR), fully adjustable via input.

Capital-Based Risk Management: Risk is defined as a percentage of a fixed account size (e.g., $100 per trade from $10,000), and lot size is automatically calculated based on SL distance.

Fallback Entry Logic: If structural breakout is present but trend is not confirmed, a secondary entry is triggered.

End-of-Session Management: Any open trades are automatically closed at 11:45 a.m. NY time, with optional manual labeling or review.

📊 Visual Features (Optional in Indicator Version):

(Note: Visuals apply to the indicator version of LANZ 2.0, not this backtest script)

Swing level labels (1st, 2nd) and dynamic SL/TP lines.

Real-time session coloring for clarity: Pre-London, Entry Window, and NY Close.

Outcome labels: +RR, -RR, or net % at close.

Auto-cleanup of previous drawings for a clean chart per session.

⚙️ How It Works:

Detects last trend and BoS using swing logic before 02:00 a.m. NY.

At 02:00 a.m., evaluates directional bias and executes BUY or SELL if confirmed.

Applies selected SL logic (1st, 2nd, or full swing protection).

Sets TP based on the RR multiplier.

Closes the trade either on SL, TP, or at 11:45 a.m. NY manually.

🔔 Alerts:

Time-of-day alert at 02:00 a.m. NY to monitor execution.

Can be extended to cover SL/TP triggers or new BoS events.

📝 Notes:

Designed for backtesting precision and discretionary decision-making.

Ideal for Forex pairs, indices, or assets active during the London session.

Fully customizable: session timing, swing logic, SL buffer, and RR.

👤 Credits:

Strategy built by @rau_u_lanz using Pine Script v6, combining structural logic, capital-based risk control, and London-session timing in a backtest-ready framework for traders who demand accuracy and structure.

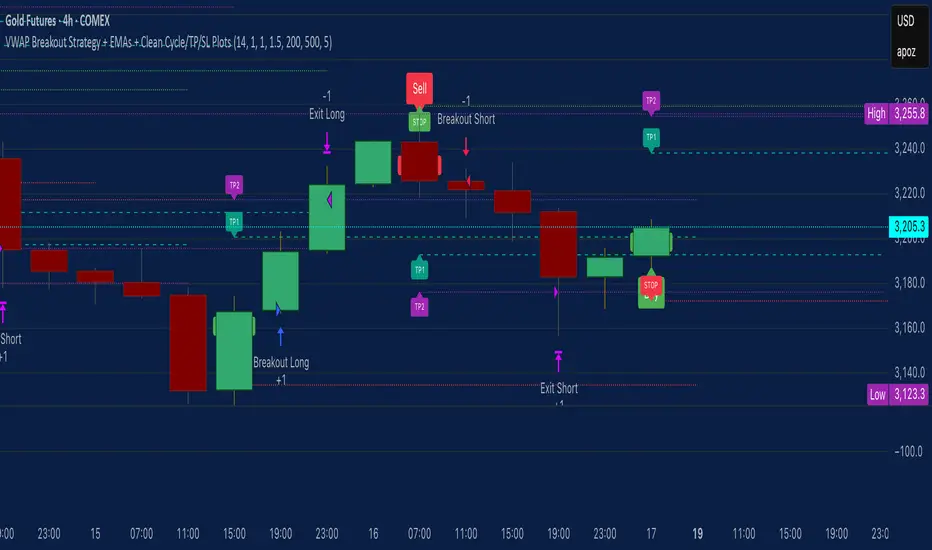

VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL PlotsHere’s a quick user-guide to get you up and running with your “VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL Plots” script in TradingView:

⸻

1. Installing the Script

1. Open TradingView, go to Pine Editor (bottom panel).

2. Paste in your full Pine-v6 code and hit Add to chart.

3. Save it (“Save as…”): give it a memorable name (e.g. “VWAP Breakout+EMAs”).

⸻

2. Configuring Your Inputs

Once it’s on the chart, click the ⚙️ Settings icon to tune:

Setting Default What it does

ATR Length 14 Period for average true range (volatility measure)

ATR Multiplier for Stop 1.5 How many ATRs away your stop-loss sits

TP1 / TP2 Multipliers (ATR) 1.0 / 2.0 Distance of TP1 and TP2 in ATR multiples

Show VWAP / EMAs On Toggles the blue VWAP line & EMAs (100/34/5)

Full Cycle Range Points 200 Height of the shaded “cycle zone”

Pivot Lookback 5 How many bars back to detect a pivot low

Round Number Step 500 Spacing of your dotted horizontal lines

Show TP/SL Labels On Toggles all the “ENTRY”, “TP1”, “TP2”, “STOP” tags

Feel free to adjust ATR multipliers and cycle-zone size based on the instrument’s typical range.

⸻

3. Reading the Signals

• Long Entry:

• Trigger: price crosses above VWAP

• You’ll see a green “Buy” tag at the low of the signal bar, plus an “ENTRY (Long)” label at the close.

• Stop is plotted as a red dashed line below (ATR × 1.5), and TP1/TP2 as teal and purple lines above.

• Short Entry:

• Trigger: price crosses below VWAP

• A red “Sell” tag appears at the high, with “ENTRY (Short)” at the close.

• Stop is the green line above; TP1/TP2 are dashed teal/purple lines below.

⸻

4. Full Cycle Zone

Whenever a new pivot low is detected (using your Pivot Lookback), the script deletes the old box and draws a shaded yellow rectangle from that low up by “Full Cycle Range Points.”

• Use this to visualize the “maximum expected swing” from your pivot.

• You can quickly see whether price is still traveling within a normal cycle or has overstretched.

⸻

5. Round-Number Levels

With Show Round Number Levels enabled, you’ll always get horizontal dotted lines at the nearest multiples of your “Round Number Step” (e.g. every 500 points).

• These often act as psychological support/resistance.

• Handy to see confluence with VWAP or cycle-zone edges.

⸻

6. Tips & Best-Practices

• Timeframes: Apply on any intraday chart (5 min, 15 min, H1…), but match your ATR length & cycle-points to the timeframe’s typical range.

• Backtest first: Use the Strategy Tester tab to review performance, tweak ATR multipliers or cycle size, then optimize.

• Combine with context: Don’t trade VWAP breakouts blindly—look for confluence (e.g. support/resistance zones, higher-timeframe trend).

• Label clutter: If too many labels build up, you can toggle Show TP/SL Labels off and rely just on the lines.

⸻

That’s it! Once you’ve added it to your chart and dialed in the inputs, your entries, exits, cycle ranges, and key levels will all be plotted automatically. Feel free to experiment with the ATR multipliers and cycle-zone size until it fits your instrument’s personality. Happy trading!

Rawstocks 15 Minute ModelRawstocks 15-Minute Model

The Rawstocks 15-Minute Model is a precision intraday trading strategy designed for the US stock market (9:30 AM - 4:00 PM ET), optimized for the 15-minute timeframe. It combines institutional order flow concepts with Fibonacci retracements to identify high-probability reversal setups while enforcing strict risk management and session-based rules.

Key Features

Time-Based Execution

Trading Hours: 9:30 AM - 4:00 PM ET (no new entries after 4:00 PM)

Force Close: All positions auto-exit at 4:30 PM ET (prevents overnight risk)

Entry Logic

Order Block + Fib Confluence:

Identifies institutional order blocks (previous swing highs/lows)

Requires price pullback to 61.8% or 79% Fibonacci level

Liquidity Confirmation:

Waits for stop runs (liquidity sweeps) before reversal entries

Exit Rules

Stop Loss: 1x ATR (14) from entry

Take Profit: 2:1 Risk-Reward (adjustable)

Visual Signals

Green Triangle: Valid long setup (pullback to bullish OB + Fib)

Red Triangle: Valid short setup (pullback to bearish OB + Fib)

Blue/Purple Background: Highlights active trading vs. close period

How It Works

Identify the Setup

Wait for a strong impulse move (break of structure)

Mark the order block (institutional zone)

Confirm Pullback

Price must retrace to 61.8% or 79% Fib level

Must occur within trading hours (9:30 AM - 4:00 PM)

Enter on Confirmation

Long: Break of pullback candle high (stop below recent swing low)

Short: Break of pullback candle low (stop above recent swing high)

Manage the Trade

Trail stop or exit at 2R (risk-to-reward)

All positions close at 4:30 PM sharp

Gaussian Channel StrategyGaussian Channel Strategy — User Guide

1. Concept

This strategy builds trades around the Gaussian Channel. Based on Pine Script v4 indicator originally published by Donovan Wall. With rework to v6 Pine Script and adding entry and exit functions.

The channel consists of three dynamic lines:

Line Formula Purpose

Filter (middle) N-pole Gaussian filter applied to price Market "equilibrium"

High Band Filter + (Filtered TR × mult) Dynamic upper envelope

Low Band Filter − (Filtered TR × mult) Dynamic lower envelope

A position is opened when price crosses a user-selected line in a user-selected direction.

When the smoothed True Range (Filtered TR) becomes negative, the raw bands can flip (High drops below Low).

The strategy automatically reorders them so the upper band is always above the lower band.

Visual colors still flip, but signals stay correct.

2. Entry Logic

Choose a signal line for longs and/or shorts: Filter, Upper band, or Lower band.

Choose a cross direction (Cross Up or Cross Down).

A signal remains valid for Lookback bars after the actual cross, as long as price is still on the required side of the line.

When the opposite signal appears, the current position is closed or reversed depending on Reverse on opposite.

3. Parameters

Group Setting Meaning

Source & Filter Source Price series used (close, hlc3, etc.)

Poles (N) Number of Gaussian filter poles (1-9). More poles ⇒ smoother but laggier

Sampling Period Main period length of the channel

Filtered TR Multiplier Width of the bands in fractions of smoothed True Range

Reduced Lag Mode Adds a lag-compensation term (faster but noisier)

Fast Response Mode Blends 1-pole & N-pole outputs for quicker turns

Signals Long → signal line / Short → signal line Which line generates signals

Long when price / Short when price Direction of the cross

Lookback bars for late entry Bars after the cross that still allow an entry

Trading Enable LONG/SHORT-side trades Turn each side on/off

On opposite signal: reverse True: reverse -- False: flat

Misc Start trading date Ignores signals before this timestamp (back-test focus)

4. Quick Start

Add the strategy to a chart. Default: hlc3, N = 4, Period = 144.

Select your signal lines & directions.

Example: trend trading – Long: Filter + Cross Up, Short: Filter + Cross Down.

Disable either side if you want long-only or short-only.

Tune Lookback (e.g. 3) to catch gaps and strong impulses.

Run Strategy Tester, optimise period / multiplier / stops (add strategy.exit blocks if needed).

When satisfied, connect alerts via TradingView webhooks or use the builtin broker panel.

5. Notes

Commission & slippage are not preset – adjust them in Properties → Commission & Slippage.

Works on any market and timeframe, but you should retune Sampling Period and Multiplier for each symbol.

No stop-loss / take-profit is included by default – feel free to add with strategy.exit.

Start trading date lets you back-test only recent history (e.g. last two years).

6. Disclaimer

This script is for educational purposes only and does not constitute investment advice.

Use entirely at your own risk. Back-test thoroughly and apply sound risk management before trading real capital.

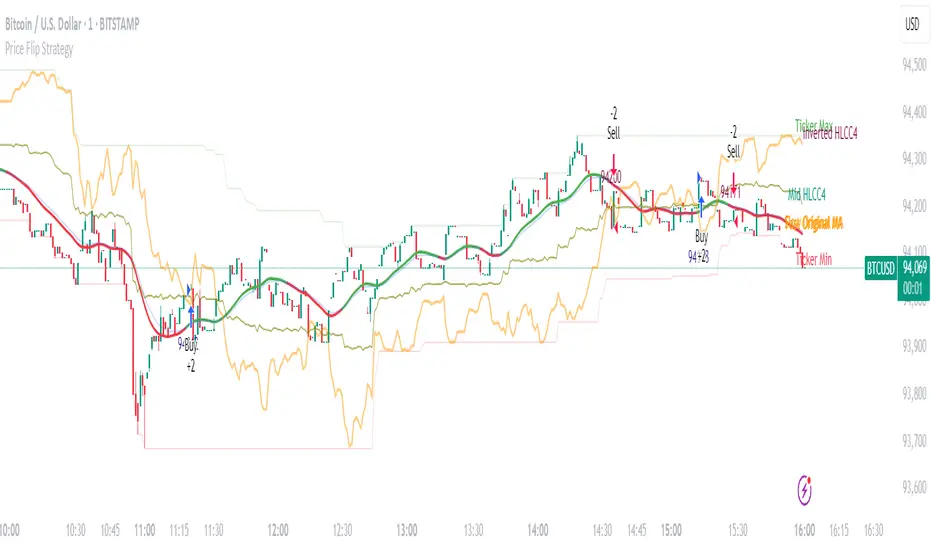

Price Flip StrategyPrice Flip Strategy with User-Defined Ticker Max/Max

This strategy leverages an inverted price calculation based on user-defined maximum and minimum price levels over customizable lookback periods. It generates buy and sell signals by comparing the previous bar's original price to the inverted price, within a specified date range. The script plots key metrics, including ticker max/min, original and inverted prices, moving averages, and HLCC4 averages, with customizable visibility toggles and labels for easy analysis.

Key Features:

Customizable Inputs: Set lookback periods for ticker max/min, moving average length, and date range for signal generation.

Inverted Price Logic: Calculates an inverted price using ticker max/min to identify trading opportunities.

Flexible Visualization: Toggle visibility for plots (e.g., ticker max/min, prices, moving averages, HLCC4 averages) and last-bar labels with user-defined colors and sizes.

Trading Signals: Generates buy signals when the previous original price exceeds the inverted price, and sell signals when it falls below, with alerts for real-time notifications.

Labeling: Displays values on the last bar for all plotted metrics, aiding in quick reference.

How to Use:

Add to Chart: Apply the script to a TradingView chart via the Pine Editor.

Configure Settings:

Date Range: Set the start and end dates to define the active trading period.

Ticker Levels: Adjust the lookback periods for calculating ticker max and min (e.g., 100 bars for max, 100 for min).

Moving Averages: Set the length for exponential moving averages (default: 20 bars).

Plots and Labels: Enable/disable specific plots (e.g., Inverted Price, Original HLCC4) and customize label colors/sizes for clarity.

Interpret Signals:

Buy Signal: Triggered when the previous close price is above the inverted price; marked with an upward label.

Sell Signal: Triggered when the previous close price is below the inverted price; marked with a downward label.

Set Alerts: Use the built-in alert conditions to receive notifications for buy/sell signals.

Analyze Plots: Review plotted lines (e.g., ticker max/min, HLCC4 averages) and last-bar labels to assess price behavior.

Tips:

Use in trending markets by enabling ticker max for uptrends or ticker min for downtrends, as indicated in tooltips.

Adjust the label offset to prevent overlapping text on the last bar.

Test the strategy on a demo account to optimize lookback periods and moving average settings for your asset.

Disclaimer: This script is for educational purposes and should be tested thoroughly before use in live trading. Past performance is not indicative of future results.

Vinicius Setup ATR

Description:

This script is a strategy based on the Supertrend indicator combined with volume analysis, candle strength, and RSI. Its goal is to identify potential entry points for buy and sell trades based on technical criteria, without promising profitability or guaranteed results.

Script Components:

Supertrend: Used as the main trend compass. When the trend is positive (direction = 1), buy signals are considered; when negative (direction = -1), sell signals are considered.

Volume: Entries are only validated if the volume is above the average of the last 20 candles, adjusted with a 1.2 multiplier.

Candle Body: The candle body must be larger than a certain percentage of the ATR, ensuring sufficient strength and volatility.

RSI: Used as a filter to avoid trades in extreme overbought or oversold zones.

Support and Resistance: Identified based on simple pivots (5 periods before and after).

Customizable Parameters:

ATR Length and Multiplier: Controls the sensitivity of the Supertrend.

RSI Period: Adjusts the relative strength filter.

Minimum Volume and Candle Body: Settings to validate entry signals.

Entry Conditions:

Buy: Positive trend + strong candle + high volume + RSI below 70.

Sell: Negative trend + strong candle + high volume + RSI above 30.

Exit Conditions:

The trade is closed upon the appearance of an opposite signal.

Notes:

This is a technical system with no profit guarantees.

It is recommended to test with realistic capital values and parameters suited to your risk management.

The script is not optimized for specific profitability, but rather to support study and the construction of setups with objective criteria.

EMA 34 Crossover with Break Even Stop LossEMA 34 Crossover with Break Even Stop Loss Strategy

This trading strategy is based on the 34-period Exponential Moving Average (EMA) and aims to enter long positions when the price crosses above the EMA 34. The strategy is designed to manage risk effectively with a dynamic stop loss and take-profit mechanism.

Key Features:

EMA 34 Crossover:

The strategy generates a long entry signal when the closing price of the current bar crosses above the 34-period EMA, with the condition that the previous closing price was below the EMA. This crossover indicates a potential upward trend.

Risk Management:

Upon entering a trade, the strategy sets a stop loss at the low of the previous bar. This helps in controlling the downside risk.

A take profit level is set at a 10:1 risk-to-reward ratio, meaning the potential profit is ten times the amount risked on the trade.

Break-even Stop Loss:

As the price moves in favor of the trade and reaches a 3:1 risk-to-reward ratio, the strategy moves the stop loss to the entry price (break-even). This ensures that no loss will be incurred if the market reverses, effectively protecting profits.

Exit Conditions:

The strategy exits the trade when either the stop loss is hit (if the price drops below the stop loss level) or the take profit target is reached (if the price rises to the take profit level).

If the price reaches the break-even level (entry price), the stop loss is adjusted to lock in profits and prevent any loss.

Visualization:

The stop loss and take profit levels are plotted on the chart for easy visualization, helping traders track the status of their trade.

Trade Management Summary:

Long Entry: When price crosses above the 34-period EMA.

Stop Loss: Set to the low of the previous candle.

Take Profit: Set to a 10:1 risk-to-reward ratio.

Break-even: Stop loss is moved to entry price when a 3:1 risk-to-reward ratio is reached.

Exit: The trade is closed either when the stop loss or take profit levels are hit.

This strategy is designed to minimize losses by employing a dynamic stop loss and to maximize gains by setting a favorable risk-to-reward ratio, making it suitable for traders who prefer a structured, automated approach to risk management and trend-following.

LUX CLARA - EMA + VWAP (No ATR Filter) - v6EMA STRAT SHOUT OUTOUTLIERSSSSS

Overview:

an intraday strategy built around two core principles:

Trend Confirmation using the 50 EMA (Exponential Moving Average) in relation to the VWAP (Volume-Weighted Average Price).

Entry Signals triggered by the 8 EMA crossing the 50 EMA in the direction of that confirmed trend.

Key Logic:

Bullish Trend if the 50 EMA is above VWAP. Only long entries are allowed when the 8 EMA crosses above the 50 EMA during that bullish phase.

Bearish Trend if the 50 EMA is below VWAP. Only short entries are allowed when the 8 EMA crosses below the 50 EMA during that bearish phase.

Intraday Focus: Trades are restricted to a user-defined session window (default 7:30 AM–11:30 AM), aligning entries/exits with peak intraday liquidity.

Exit Rule: Positions close automatically when the 8 EMA crosses back in the opposite direction of the entry.

Why It Works:

EMA + VWAP helps detect both immediate momentum (EMAs) and overall institutional bias (VWAP).

By confining trades to a set intraday window, the strategy aims to capture morning volatility while avoiding choppy afternoon or overnight sessions.

Customization:

Users can adjust EMA lengths, session times, or incorporate stops/targets for additional risk management.

It can be tested on various symbols and intraday timeframes to gauge performance and robustness.

Enhanced Range Filter Strategy with ATR TP/SLBuilt by Omotola

## **Enhanced Range Filter Strategy: A Comprehensive Overview**

### **1. Introduction**

The **Enhanced Range Filter Strategy** is a powerful technical trading system designed to identify high-probability trading opportunities while filtering out market noise. It utilizes **range-based trend filtering**, **momentum confirmation**, and **volatility-based risk management** to generate precise entry and exit signals. This strategy is particularly useful for traders who aim to capitalize on trend-following setups while avoiding choppy, ranging market conditions.

---

### **2. Key Components of the Strategy**

#### **A. Range Filter (Trend Determination)**

- The **Range Filter** smooths price fluctuations and helps identify clear trends.

- It calculates an **adjusted price range** based on a **sampling period** and a **multiplier**, ensuring a dynamic trend-following approach.

- **Uptrends:** When the current price is above the range filter and the trend is strengthening.

- **Downtrends:** When the price falls below the range filter and momentum confirms the move.

#### **B. RSI (Relative Strength Index) as Momentum Confirmation**

- RSI is used to **filter out weak trades** and prevent entries during overbought/oversold conditions.

- **Buy Signals:** RSI is above a certain threshold (e.g., 50) in an uptrend.

- **Sell Signals:** RSI is below a certain threshold (e.g., 50) in a downtrend.

#### **C. ADX (Average Directional Index) for Trend Strength Confirmation**

- ADX ensures that trades are only taken when the trend has **sufficient strength**.

- Avoids trading in low-volatility, ranging markets.

- **Threshold (e.g., 25):** Only trade when ADX is above this value, indicating a strong trend.

#### **D. ATR (Average True Range) for Risk Management**

- **Stop Loss (SL):** Placed **one ATR below** (for long trades) or **one ATR above** (for short trades).

- **Take Profit (TP):** Set at a **3:1 reward-to-risk ratio**, using ATR to determine realistic price targets.

- Ensures volatility-adjusted risk management.

---

### **3. Entry and Exit Conditions**

#### **📈 Buy (Long) Entry Conditions:**

1. **Price is above the Range Filter** → Indicates an uptrend.

2. **Upward trend strength is positive** (confirmed via trend counter).

3. **RSI is above the buy threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **📉 Sell (Short) Entry Conditions:**

1. **Price is below the Range Filter** → Indicates a downtrend.

2. **Downward trend strength is positive** (confirmed via trend counter).

3. **RSI is below the sell threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **🚪 Exit Conditions:**

- **Stop Loss (SL):**

- **Long Trades:** 1 ATR below entry price.

- **Short Trades:** 1 ATR above entry price.

- **Take Profit (TP):**

- Set at **3x the risk distance** to achieve a favorable risk-reward ratio.

- **Ranging Market Exit:**

- If ADX falls below the threshold, indicating a weakening trend.

---

### **4. Visualization & Alerts**

- **Colored range filter line** changes based on trend direction.

- **Buy and Sell signals** appear as labels on the chart.

- **Stop Loss and Take Profit levels** are plotted as dashed lines.

- **Gray background highlights ranging markets** where trading is avoided.

- **Alerts trigger on Buy, Sell, and Ranging Market conditions** for automation.

---

### **5. Advantages of the Enhanced Range Filter Strategy**

✅ **Trend-Following with Noise Reduction** → Helps avoid false signals by filtering out weak trends.

✅ **Momentum Confirmation with RSI & ADX** → Ensures that only strong, valid trades are executed.

✅ **Volatility-Based Risk Management** → ATR ensures adaptive stop loss and take profit placements.

✅ **Works on Multiple Timeframes** → Effective for day trading, swing trading, and scalping.

✅ **Visually Intuitive** → Clearly displays trade signals, SL/TP levels, and trend conditions.

---

### **6. Who Should Use This Strategy?**

✔ **Trend Traders** who want to enter trades with momentum confirmation.

✔ **Swing Traders** looking for medium-term opportunities with a solid risk-reward ratio.

✔ **Scalpers** who need precise entries and exits to minimize false signals.

✔ **Algorithmic Traders** using alerts for automated execution.

---

### **7. Conclusion**

The **Enhanced Range Filter Strategy** is a powerful trading tool that combines **trend-following techniques, momentum indicators, and risk management** into a structured, rule-based system. By leveraging **Range Filters, RSI, ADX, and ATR**, traders can improve trade accuracy, manage risk effectively, and filter out unfavorable market conditions.

This strategy is **ideal for traders looking for a systematic, disciplined approach** to capturing trends while **avoiding market noise and false breakouts**. 🚀