EMA Cross + RSI Pullback Strategy with 1H ConfirmationThis strategy combines an ema9 and ema21 cross on the 15min timeframe with a short retest of the RSI 50-line (or close to the RSI 50-line) on the candle before the cross, on the cross, or one or two candles after the cross.

The script uses higher time frame confirmation on the 1 hour. It gives only a buy signal on the 15 minute if on the 1 hour the ema21 is above the ema 50. It gives only a sell signal on the 15 minute if on the 1 hour the ema21 is below the ema50.

It is still in the testing phase. So please backtest this strategy before putting money in the game. I combine my trading with the ATR stoploss finder set on 0.8 (instead of 1.5 default) and aim for RR 1:2 or better.

Please feel free to comment (nicely and polite) ;)

Exponential Moving Average (EMA)

The Most Powerful TQQQ EMA Crossover Trend Trading StrategyTQQQ EMA Crossover Strategy Indicator

Meta Title: TQQQ EMA Crossover Strategy - Enhance Your Trading with Effective Signals

Meta Description: Discover the TQQQ EMA Crossover Strategy, designed to optimize trading decisions with fast and slow EMA crossovers. Learn how to effectively use this powerful indicator for better trading results.

Key Features

The TQQQ EMA Crossover Strategy is a powerful trading tool that utilizes Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. Key features of this indicator include:

**Fast and Slow EMAs:** The strategy incorporates two EMAs, allowing traders to capture short-term trends while filtering out market noise.

**Entry and Exit Signals:** Automated signals for entering and exiting trades based on EMA crossovers, enhancing decision-making efficiency.

**Customizable Parameters:** Users can adjust the lengths of the EMAs, as well as take profit and stop loss multipliers, tailoring the strategy to their trading style.

**Visual Indicators:** Clear visual plots of the EMAs and exit points on the chart for easy interpretation.

How It Works

The TQQQ EMA Crossover Strategy operates by calculating two EMAs: a fast EMA (default length of 20) and a slow EMA (default length of 50). The core concept is based on the crossover of these two moving averages:

- When the fast EMA crosses above the slow EMA, it generates a *buy signal*, indicating a potential upward trend.

- Conversely, when the fast EMA crosses below the slow EMA, it produces a *sell signal*, suggesting a potential downward trend.

This method allows traders to capitalize on momentum shifts in the market, providing timely signals for trade execution.

Trading Ideas and Insights

Traders can leverage the TQQQ EMA Crossover Strategy in various market conditions. Here are some insights:

**Scalping Opportunities:** The strategy is particularly effective for scalping in volatile markets, allowing traders to make quick profits on small price movements.

**Swing Trading:** Longer-term traders can use this strategy to identify significant trend reversals and capitalize on larger price swings.

**Risk Management:** By incorporating customizable stop loss and take profit levels, traders can manage their risk effectively while maximizing potential returns.

How Multiple Indicators Work Together

While this strategy primarily relies on EMAs, it can be enhanced by integrating additional indicators such as:

- **Relative Strength Index (RSI):** To confirm overbought or oversold conditions before entering trades.

- **Volume Indicators:** To validate breakout signals, ensuring that price movements are supported by sufficient trading volume.

Combining these indicators provides a more comprehensive view of market dynamics, increasing the reliability of trade signals generated by the EMA crossover.

Unique Aspects

What sets this indicator apart is its simplicity combined with effectiveness. The reliance on EMAs allows for smoother signals compared to traditional moving averages, reducing false signals often associated with choppy price action. Additionally, the ability to customize parameters ensures that traders can adapt the strategy to fit their unique trading styles and risk tolerance.

How to Use

To effectively utilize the TQQQ EMA Crossover Strategy:

1. **Add the Indicator:** Load the script onto your TradingView chart.

2. **Set Parameters:** Adjust the fast and slow EMA lengths according to your trading preferences.

3. **Monitor Signals:** Watch for crossover points; enter trades based on buy/sell signals generated by the indicator.

4. **Implement Risk Management:** Set your stop loss and take profit levels using the provided multipliers.

Regularly review your trading performance and adjust parameters as necessary to optimize results.

Customization

The TQQQ EMA Crossover Strategy allows for extensive customization:

- **EMA Lengths:** Change the default lengths of both fast and slow EMAs to suit different time frames or market conditions.

- **Take Profit/Stop Loss Multipliers:** Adjust these values to align with your risk management strategy. For instance, increasing the take profit multiplier may yield larger gains but could also increase exposure to market fluctuations.

This flexibility makes it suitable for various trading styles, from aggressive scalpers to conservative swing traders.

Conclusion

The TQQQ EMA Crossover Strategy is an effective tool for traders seeking an edge in their trading endeavors. By utilizing fast and slow EMAs, this indicator provides clear entry and exit signals while allowing for customization to fit individual trading strategies. Whether you are a scalper looking for quick profits or a swing trader aiming for larger moves, this indicator offers valuable insights into market trends.

Incorporate it into your TradingView toolkit today and elevate your trading performance!

Triple EMA Crossover StrategyTriple EMA Crossover Strategy

Overview

The Triple EMA Crossover Strategy is a trend-following trading system that utilizes three Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. This strategy is based on the principle that when shorter-term prices cross above longer-term prices, it can indicate a bullish trend, and conversely when they cross below, it can signal a bearish trend.

Components

Exponential Moving Averages (EMAs):

Short EMA: A fast-moving average that reacts quickly to price changes (commonly set to 9 periods).

Medium EMA: A medium-term average that smooths out price data and helps confirm trends (commonly set to 21 periods).

Long EMA: A slow-moving average that helps identify the overall trend direction (commonly set to 55 periods).

Trading Signals:

Buy Signal: A long entry is triggered when:

The Short EMA (9) crosses above the Medium EMA (21).

The Medium EMA (21) is above the Long EMA (55).

Sell Signal: A short entry is signaled when:

The Short EMA (9) crosses below the Medium EMA (21).

The Medium EMA (21) is below the Long EMA (55).

Stop Loss and Take Profit:

Stop Loss: Implement a predefined percentage or ATR-based stop loss to limit potential losses.

Take Profit: Set a target based on a risk-to-reward ratio that reflects your trading strategy's goals.

Advantages

Trend Identification: The EMA crossover system allows traders to identify the current trend dynamically, focusing on upward or downward price movements.

Simplicity: The strategy is straightforward, making it accessible for both new and experienced traders.

Flexibility: This method can be applied across multiple timeframes and asset classes, making it versatile for various trading styles.

Disadvantages

Lagging Indicator: Moving averages are lagging indicators, meaning signals may come later than the actual price movement, which can lead to missed opportunities.

Whipsaw Effect: In ranging markets, the strategy may produce false signals leading to potential losses.

Dont make me crossStrategy Overview

This trading strategy utilizes Exponential Moving Averages (EMAs) to generate buy and sell signals based on the crossover of two EMAs, which are shifted downwards by 50 points. The strategy aims to identify potential market reversals and trends based on these crossovers.

Components of the Strategy

Exponential Moving Averages (EMAs):

Short EMA: This is calculated over a shorter period (default is 9 periods) and is more responsive to recent price changes.

Long EMA: This is calculated over a longer period (default is 21 periods) and provides a smoother view of the price trend.

Both EMAs are adjusted by a fixed shift amount of -50 points.

Input Parameters:

Short EMA Length: The period used to calculate the short-term EMA. This can be adjusted based on the trader's preference or market conditions.

Long EMA Length: The period used for the long-term EMA, also adjustable.

Shift Amount: A fixed value (default -50) that is subtracted from both EMAs to shift their values downwards. This is useful for visual adjustments or specific strategy requirements.

Plotting:

The adjusted EMAs are plotted on the price chart. The short EMA is displayed in blue, and the long EMA is displayed in red. This visual representation helps traders identify the crossover points easily.

Signal Generation:

Buy Signal: A buy signal is generated when the short EMA crosses above the long EMA. This is interpreted as a bullish signal, indicating potential upward price movement.

Sell Signal: A sell signal occurs when the short EMA crosses below the long EMA, indicating potential downward price movement.

Trade Execution:

When a buy signal is triggered, the strategy enters a long position.

Conversely, when a sell signal is triggered, the strategy enters a short position.

Trading Logic

Market Conditions: The strategy is most effective in trending markets. During sideways or choppy market conditions, it may generate false signals.

Risk Management: While this script does not include explicit risk management features (like stop-loss or take-profit), traders should consider implementing these to manage their risk effectively.

Customization

Traders can customize the EMA lengths and the shift amount based on their analysis and preferences.

The strategy can also be enhanced with additional indicators, such as volume or volatility measures, to filter signals further.

Use Cases

This strategy can be applied to various timeframes, such as intraday, daily, or weekly charts, depending on the trader's style.

It is suitable for both novice and experienced traders, offering a straightforward approach to trading based on technical analysis.

Summary

The EMA Crossover Strategy with a -50 shift is a straightforward technical analysis approach that capitalizes on the momentum generated by the crossover of short and long-term EMAs. By shifting the EMAs downwards, the strategy can help traders visualize potential entry and exit points more clearly, although it's important to consider additional risk management and market context for effective trading.

Exponantial Spread StrategyIt is strongly recommended to evaluate the strategy's performance on long time frames such as 1D or 4H.

This strategy calculates a custom moving average by the formula EMA+(TEMA-DEMA)*G,

G being the gain parameter. The main idea behind that is since TEMA is much more adaptive than DEMA their spread give us momentum, and incorporating this with a gain allows us to calculate a very responsive but yet not noisy moving average.

We calculate 4 MAs like described with gains 0,1,2,3 from less adaptive (normal EMA) to most adaptive. When they align in terms of position and the price is above the original MA we enter a long position, and do partial exits at each crossunder weighted by how adaptive ma is, the more adaptive the less weight, we do a full stop when the price crossed below under the original MA or the position aligment changed.

Overnight Positioning w EMA - Strategy [presentTrading]I've recently started researching Market Timing strategies, and it’s proving to be quite an interesting area of study. The idea of predicting optimal times to enter and exit the market, based on historical data and various indicators, brings a dynamic edge to trading. Additionally, it is integrated with the 3commas bot for automated trade execution.

I'm still working on it. Welcome to share your point of view.

█ Introduction and How it is Different

The "Overnight Positioning with EMA " is designed to capitalize on market inefficiencies during the overnight trading period. This strategy takes a position shortly before the market closes and exits shortly after it opens the following day. What sets this strategy apart is the integration of an optional Exponential Moving Average (EMA) filter, which ensures that trades are aligned with the underlying trend. The strategy provides flexibility by allowing users to select between different global market sessions, such as the US, Asia, and Europe.

It is integrated with the 3commas bot for automated trade execution and has a built-in mechanism to avoid holding positions over the weekend by force-closing positions on Fridays before the market closes.

BTCUSD 20 mins Performance

█ Strategy, How it Works: Detailed Explanation

The core logic of this strategy is simple: enter trades before market close and exit them after market open, taking advantage of potential price movements during the overnight period. Here’s how it works in more detail:

🔶 Market Timing

The strategy determines the local market open and close times based on the selected market (US, Asia, Europe) and adjusts entry and exit points accordingly. The entry is triggered a specific number of minutes before market close, and the exit is triggered a specific number of minutes after market open.

🔶 EMA Filter

The strategy includes an optional EMA filter to help ensure that trades are taken in the direction of the prevailing trend. The EMA is calculated over a user-defined timeframe and length. The entry is only allowed if the closing price is above the EMA (for long positions), which helps to filter out trades that might go against the trend.

The EMA formula:

```

EMA(t) = +

```

Where:

- EMA(t) is the current EMA value

- Close(t) is the current closing price

- n is the length of the EMA

- EMA(t-1) is the previous period's EMA value

🔶 Entry Logic

The strategy monitors the market time in the selected timezone. Once the current time reaches the defined entry period (e.g., 20 minutes before market close), and the EMA condition is satisfied, a long position is entered.

- Entry time calculation:

```

entryTime = marketCloseTime - entryMinutesBeforeClose * 60 * 1000

```

🔶 Exit Logic

Exits are triggered based on a specified time after the market opens. The strategy checks if the current time is within the defined exit period (e.g., 20 minutes after market open) and closes any open long positions.

- Exit time calculation:

exitTime = marketOpenTime + exitMinutesAfterOpen * 60 * 1000

🔶 Force Close on Fridays

To avoid the risk of holding positions over the weekend, the strategy force-closes any open positions 5 minutes before the market close on Fridays.

- Force close logic:

isFriday = (dayofweek(currentTime, marketTimezone) == dayofweek.friday)

█ Trade Direction

This strategy is designed exclusively for long trades. It enters a long position before market close and exits the position after market open. There is no shorting involved in this strategy, and it focuses on capturing upward momentum during the overnight session.

█ Usage

This strategy is suitable for traders who want to take advantage of price movements that occur during the overnight period without holding positions for extended periods. It automates entry and exit times, ensuring that trades are placed at the appropriate times based on the market session selected by the user. The 3commas bot integration also allows for automated execution, making it ideal for traders who wish to set it and forget it. The strategy is flexible enough to work across various global markets, depending on the trader's preference.

█ Default Settings

1. entryMinutesBeforeClose (Default = 20 minutes):

This setting determines how many minutes before the market close the strategy will enter a long position. A shorter duration could mean missing out on potential movements, while a longer duration could expose the position to greater price fluctuations before the market closes.

2. exitMinutesAfterOpen (Default = 20 minutes):

This setting controls how many minutes after the market opens the position will be exited. A shorter exit time minimizes exposure to market volatility at the open, while a longer exit time could capture more of the overnight price movement.

3. emaLength (Default = 100):

The length of the EMA affects how the strategy filters trades. A shorter EMA (e.g., 50) reacts more quickly to price changes, allowing more frequent entries, while a longer EMA (e.g., 200) smooths out price action and only allows entries when there is a stronger underlying trend.

The effect of using a longer EMA (e.g., 200) would be:

```

EMA(t) = +

```

4. emaTimeframe (Default = 240):

This is the timeframe used for calculating the EMA. A higher timeframe (e.g., 360) would base entries on longer-term trends, while a shorter timeframe (e.g., 60) would respond more quickly to price movements, potentially allowing more frequent trades.

5. useEMA (Default = true):

This toggle enables or disables the EMA filter. When enabled, trades are only taken when the price is above the EMA. Disabling the EMA allows the strategy to enter trades without any trend validation, which could increase the number of trades but also increase risk.

6. Market Selection (Default = US):

This setting determines which global market's open and close times the strategy will use. The selection of the market affects the timing of entries and exits and should be chosen based on the user's preference or geographic focus.

Crypto Volatility Bitcoin Correlation Strategy Description:

The Crypto Volatility Bitcoin Correlation Strategy is designed to leverage market volatility specifically in Bitcoin (BTC) using a combination of volatility indicators and trend-following techniques. This strategy utilizes the VIXFix (a volatility indicator adapted for crypto markets) and the BVOL7D (Bitcoin 7-Day Volatility Index from BitMEX) to identify periods of high volatility, while confirming trends with the Exponential Moving Average (EMA). These components work together to offer a comprehensive system that traders can use to enter positions when volatility and trends are aligned in their favor.

Key Features:

VIXFix (Volatility Index for Crypto Markets): This indicator measures the highest price of Bitcoin over a set period and compares it with the current low price to gauge market volatility. A rise in VIXFix indicates increasing market volatility, signaling that large price movements could occur.

BVOL7D (Bitcoin 7-Day Volatility Index): This volatility index, provided by BitMEX, measures the volatility of Bitcoin over the past 7 days. It helps traders monitor the recent volatility trend in the market, particularly useful when making short-term trading decisions.

Exponential Moving Average (EMA): The 50-period EMA acts as a trend indicator. When the price is above the EMA, it suggests the market is in an uptrend, and when the price is below the EMA, it suggests a downtrend.

How It Works:

Long Entry: A long position is triggered when both the VIXFix and BVOL7D indicators are rising, signaling increased volatility, and the price is above the 50-period EMA, confirming that the market is trending upward.

Exit: The strategy exits the position when the price crosses below the 50-period EMA, which signals a potential weakening of the uptrend and a decrease in volatility.

This strategy ensures that traders only enter positions when the volatility aligns with a clear trend, minimizing the risk of entering trades during periods of market uncertainty.

Testing and Timeframe:

This strategy has been tested on Bitcoin using the daily timeframe, which provides a longer-term perspective on market trends and volatility. However, users can adjust the timeframe according to their trading preferences. It is crucial to note that this strategy does not include comprehensive risk management, aside from the exit condition when the price crosses below the EMA. Users are strongly advised to implement their own risk management techniques, such as setting appropriate stop-loss levels, to safeguard their positions during high volatility periods.

Utility:

The Crypto Volatility Bitcoin Correlation Strategy is particularly well-suited for traders who aim to capitalize on the high volatility often seen in the Bitcoin market. By combining volatility measurements (VIXFix and BVOL7D) with a trend-following mechanism (EMA), this strategy helps identify optimal moments for entering and exiting trades. This approach ensures that traders participate in potentially profitable market moves while minimizing exposure during times of uncertainty.

Use Cases:

Volatility-Based Entries: Traders looking to take advantage of market volatility spikes will find this strategy useful for timing entry points during market swings.

Trend Confirmation: By using the EMA as a confirmation tool, traders can avoid entering trades that go against the trend, which can result in significant losses during volatile market conditions.

Risk Management: While the strategy exits when price falls below the EMA, it is important to recognize that this is not a full risk management system. Traders should use caution and integrate additional risk measures, such as stop-losses and position sizing, to better manage potential losses.

How to Use:

Step 1: Monitor the VIXFix and BVOL7D indicators. When both are rising and the Bitcoin price is above the EMA, the strategy will trigger a long entry, indicating that the market is experiencing increased volatility with a confirmed uptrend.

Step 2: Exit the position when the price drops below the 50-period EMA, signaling that the trend may be reversing or weakening, reducing the likelihood of continued upward price movement.

This strategy is open-source and is intended to help traders navigate volatile market conditions, particularly in Bitcoin, using proven indicators for volatility and trend confirmation.

Risk Disclaimer:

This strategy has been tested on the daily timeframe of Bitcoin, but users should be aware that it does not include built-in risk management except for the below-EMA exit condition. Users should be extremely cautious when using this strategy and are encouraged to implement their own risk management, such as using stop-losses, position sizing, and setting appropriate limits. Trading involves significant risk, and this strategy does not guarantee profits or prevent losses. Past performance is not indicative of future results. Always test any strategy in a demo environment before applying it to live markets.

Flexible Moving Average StrategyThis strategy offers flexibility to choose between SMA and EMA, and allows users to set the review frequency to Daily, Weekly, or Monthly. It adapts to different market conditions by providing full control over the length and timeframe of the Moving Average.

### Key Features:

- **Moving Average Method**: Select between SMA and EMA.

- **Review Frequency**: Choose Daily, Weekly, or Monthly review periods.

- **Customizable**: Set the Moving Average length and timeframe.

- **Entry/Exit Rules**:

- **Enter Long**: When the close price is above the Moving Average at the end of the period.

- **Exit**: When the close price falls below the Moving Average.

### Parameters:

- **Review Frequency**: Daily, Weekly, Monthly

- **Moving Average Method**: SMA or EMA

- **Length & Timeframe**: Fully adjustable

This strategy suits traders who prefer a flexible, trend-following approach based on long-term price movements.

PVT Crossover Strategy**Release Notes**

**Strategy Name**: PVT Crossover Strategy

**Purpose**: This strategy aims to capture entry and exit points in the market using the Price-Volume Trend (PVT) and its Exponential Moving Average (EMA). It specifically uses the crossover of PVT with its EMA as signals to identify changes in market trends.

**Uniqueness and Usefulness**

**Uniqueness**: This strategy is unique in its use of the PVT indicator, which combines price changes with trading volume to track trends. The filtering with EMA reduces noise and provides more accurate signals compared to other indicators.

**Usefulness**: This strategy is effective for traders looking to detect trend changes early. The signals based on PVT and its EMA crossover work particularly well in markets where volume fluctuations are significant.

**Entry Conditions**

**Long Entry**:

- **Condition**: A crossover occurs where PVT crosses above its EMA.

- **Signal**: A buy signal is generated, indicating a potential uptrend.

**Short Entry**:

- **Condition**: A crossunder occurs where PVT crosses below its EMA.

- **Signal**: A sell signal is generated, indicating a potential downtrend.

**Exit Conditions**

**Exit Strategy**:

- The strategy does not explicitly program exit conditions beyond the entry signals, but traders are encouraged to close positions manually based on signals or apply their own risk management strategy.

**Risk Management**

This strategy does not include default risk management rules, so traders should implement their own. Consider using trailing stops or fixed stop losses to manage risk.

**Account Size**: ¥100,000

**Commissions and Slippage**: 94 pips per trade for commissions and 1 pip for slippage

**Risk per Trade**: 10% of account equity

**Configurable Options**

**Configurable Options**:

- **EMA Length**: The length of the EMA used to calculate the EMA of PVT (default is 20).

- **Signal Display Control**: The option to turn the display of signals on or off.

**Adequate Sample Size**

To ensure the robustness and reliability of this strategy, it is recommended to backtest it with a sufficiently long period of historical data, especially across different market conditions.

**Credits**

**Acknowledgments**:

This strategy is based on the concept of the PVT indicator and its application in strategy design, drawing on contributions from technical analysis and the trading community.

**Clean Chart Description**

**Chart Appearance**:

This strategy is designed to maintain a clean and simple chart by turning off the plot of PVT, its EMA, and entry signals. This reduces clutter and allows for more effective trend analysis.

**Addressing the House Rule Violations**

**Omissions and Unrealistic Claims**

**Clarification**:

This strategy does not make unrealistic or unsupported claims about its performance, and all signals are for educational purposes only, not guaranteeing future results. It is important to understand that past performance does not guarantee future outcomes.

Negroni Opening Range StrategyStrategy Summary:

This tool can be used to help identify breakouts from a range during a time-zone of your choosing. It plots a pre-market range, an opening range, it also includes moving average levels that can be used as confluence, as well as plotting previous day SESSION highs and lows.

There are several options on how you wish to close out the trades, all described in more detail below.

Back-testing Inputs:

You define your timezone.

You define how many trades to open on any given day.

You decide to go: long only, short only, or long & short (CAREFUL: "Long & Short" can open trades that effectively closes-out existing ones, for better AND worse!)

You define between which times the strategy will open trades.

You define when it closes any open trades (preventing overnight trades, or leaving trades open into US data times!!).

This hopefully helps make back-testing reflect YOUR trading hours.

NOTE: Renko or Heikin-Ashi charts

For ALL strategies, don’t use Renko or Heikin-Ashi charts unless you know EXACTLY the implications.

Specific to my strategy, using a renko chart can make this 85-90% profitable (I wish it was!!) Although they can be useful, renko charts don’t always capture real wicks, so the renko chart may show your trade up-only but your broker (who is not using renko!!) will have likely stopped you out on a wick somewhere along the line.

NOTE: TradingView ‘Deep backtesting’

For ALL strategies, be cynical of all backtesting (e.g. repainting issues etc) as well as ‘Deep backtesting’ results.

Specific to this strategy, the default settings here SHOULD BE OK, but unfortunately at the time of writing, we can’t see on the chart what exactly ‘deep backtesting’ is calculating. In the past I have noted a number of trades that were not closed at the end of the day, despite my ‘end of day’ trade closing being enabled, so there were big winners and losers that would not have materialized otherwise. As I say, this seems ok at these settings but just always be cynical!!

Opening Range Inputs

You define a pre-market range (example: 08:00 - 09:00).

You define an opening range (example: 09:00 - 09:30).

The strategy will give an update at the close of the opening range to let you know if the opening range has broken out the pre-market range (OR Breakout), or if it has remained inside (OR Inside). The label appears at the end of the opening range NOT at the bar that ‘broke-out’.

This is just a visual cue for you, it has no bearing on what the strategy will do.

The strategy default will trade off the pre-market range, but you can untick this if you prefer to trade off the opening range.

Opening Trades:

Strategy goes long when the bar (CLOSE) crosses-over the ‘pre-market’ high (not the ‘opening range’ high); and the time is within your trading session, and you have not maxed out your number of trades for the day!

Strategy goes short when the bar (CLOSE) crosses-under the ‘pre-market’ low (not the ‘opening range low); and the time is within your trading session, and you have not maxed out your number of trades for the day!

Remember, you can untick this if you prefer to trade off the opening range instead.

NOTES:

Using momentum indicators can help (RSI and MACD): especially to trade range plays in failed breakouts, when momentum shifts… but the strategy won’t do this for you!

Using an anchored vwap at the session open can also provide nice confluence, as well as take-profit levels at the upper/lower of 3x standard deviation.

CLOSING TRADES:

You have 6 take-profit (TP) options:

1) Full TP: uses ATR Multiplier - Full TP at the ATR parameters as defined in inputs.

2) Take Partial profits: ATR Multiplier - Takes partial profits based on parameters as defined in inputs (i.e close 40% of original trade at TP1, close another 40% of original trade at TP2, then the remainder at Full TP as set in option 1.).

3) Full TP: Trailing Stop - Applies a Trailing Stop at the number of points, as defined in inputs.

4) Full TP: MA cross - Takes profit when price crosses ‘Trend MA’ as defined in inputs.

5) Scalp: Points - closes at a set number of points, as defined in inputs.

6) Full TP: PMKT Multiplier - places a SL at opposite pre-market Hi/Low (we go long at a break-out of the pre-market high, 50% would place a SL at the pre-market range mid-point; 100% would place a SL at the pre-market low)'. This takes profit at the input set in option 1).

MACD with 1D Stochastic Confirmation Reversal StrategyOverview

The MACD with 1D Stochastic Confirmation Reversal Strategy utilizes MACD indicator in conjunction with 1 day timeframe Stochastic indicators to obtain the high probability short-term trend reversal signals. The main idea is to wait until MACD line crosses up it’s signal line, at the same time Stochastic indicator on 1D time frame shall show the uptrend (will be discussed in methodology) and not to be in the oversold territory. Strategy works on time frames from 30 min to 4 hours and opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Higher time frame confirmation: Strategy utilizes 1D Stochastic to establish the major trend and confirm the local reversals with the higher probability.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

MACD line of MACD indicator shall cross over the signal line of MACD indicator.

1D time frame Stochastic’s K line shall be above the D line.

1D time frame Stochastic’s K line value shall be below 80 (not overbought)

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with EMA. If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 3.25, value multiplied by ATR to be subtracted from position entry price to setup stop loss)

ATR Trailing Profit Activation Level (by default = 4.25, value multiplied by ATR to be added to position entry price to setup trailing profit activation level)

Trailing EMA Length (by default = 20, period for EMA, when price reached trailing profit activation level EMA will stop out of position if price closes below it)

User can choose the optimal parameters during backtesting on certain price chart, in our example we use default settings.

Justification of Methodology

This strategy leverages 2 time frames analysis to have the high probability reversal setups on lower time frame in the direction of the 1D time frame trend. That’s why it’s recommended to use this strategy on 30 min – 4 hours time frames.

To have an approximation of 1D time frame trend strategy utilizes classical Stochastic indicator. The Stochastic Indicator is a momentum oscillator that compares a security's closing price to its price range over a specific period. It's used to identify overbought and oversold conditions. The indicator ranges from 0 to 100, with readings above 80 indicating overbought conditions and readings below 20 indicating oversold conditions.

It consists of two lines:

%K: The main line, calculated using the formula (CurrentClose−LowestLow)/(HighestHigh−LowestLow)×100 . Highest and lowest price taken for 14 periods.

%D: A smoothed moving average of %K, often used as a signal line.

Strategy logic assumes that on 1D time frame it’s uptrend in %K line is above the %D line. Moreover, we can consider long trade only in %K line is below 80. It means that in overbought state the long trade will not be opened due to higher probability of pullback or even major trend reversal. If these conditions are met we are going to our working (lower) time frame.

On the chosen time frame, we remind you that for correct work of this strategy you shall use 30min – 4h time frames, MACD line shall cross over it’s signal line. The MACD (Moving Average Convergence Divergence) is a popular momentum and trend-following indicator used in technical analysis. It helps traders identify changes in the strength, direction, momentum, and duration of a trend in a stock's price.

The MACD consists of three components:

MACD Line: This is the difference between a short-term Exponential Moving Average (EMA) and a long-term EMA, typically calculated as: MACD Line=12-period EMA−26-period

Signal Line: This is a 9-period EMA of the MACD Line, which helps to identify buy or sell signals. When the MACD Line crosses above the Signal Line, it can be a bullish signal (suggesting a buy); when it crosses below, it can be a bearish signal (suggesting a sell).

Histogram: The histogram shows the difference between the MACD Line and the Signal Line, visually representing the momentum of the trend. Positive histogram values indicate increasing bullish momentum, while negative values indicate increasing bearish momentum.

In our script we are interested in only MACD and signal lines. When MACD line crosses signal line there is a high chance that short-term trend reversed to the upside. We use this strategy on 45 min time frame.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.08.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -4.79%

Maximum Single Profit: +20.14%

Net Profit: +2361.33 USDT (+44.72%)

Total Trades: 123 (44.72% win rate)

Profit Factor: 1.623

Maximum Accumulated Loss: 695.80 USDT (-5.48%)

Average Profit per Trade: 19.20 USDT (+0.59%)

Average Trade Duration: 30 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe between 30 min and 4 hours and chart (optimal performance observed on 45 min BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

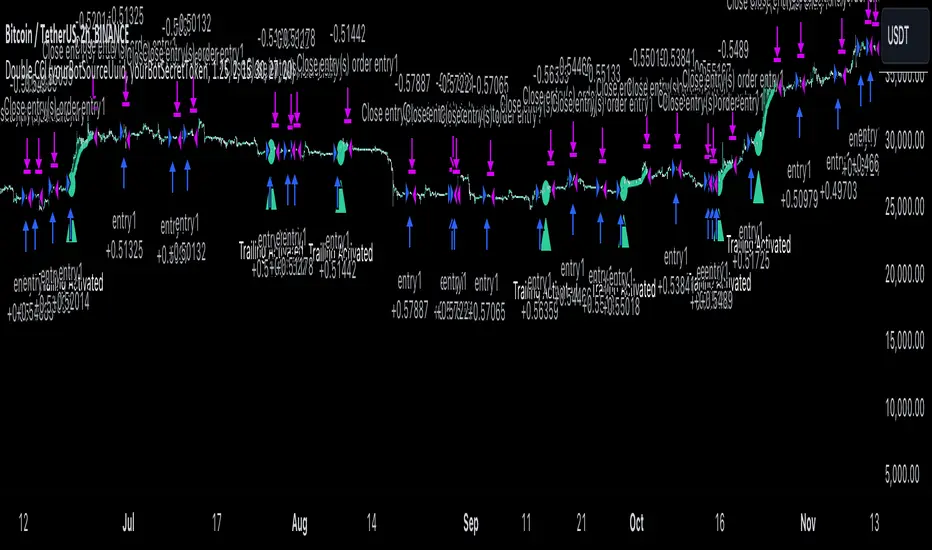

Double CCI Confirmed Hull Moving Average Reversal StrategyOverview

The Double CCI Confirmed Hull Moving Average Strategy utilizes hull moving average (HMA) in conjunction with two commodity channel index (CCI) indicators: the slow and fast to increase the probability of entering when the short and mid-term uptrend confirmed. The main idea is to wait until the price breaks the HMA while both CCI are showing that the uptrend has likely been already started. Moreover, strategy uses exponential moving average (EMA) to trail the price when it reaches the specific level. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Double trade setup confirmation: Strategy utilizes two different period CCI indicators to confirm the breakouts of HMA.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

Short-term period CCI indicator shall be above 0.

Long-term period CCI indicator shall be above 0.

Price shall cross the HMA and candle close above it with the same candle

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with EMA. If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

CCI Fast Length (by default = 25, used for calculation short term period CCI

CCI Slow Length (by default = 50, used for calculation long term period CCI)

Hull MA Length (by default = 34, period of HMA, which shall be broken to open trade)

Trailing EMA Length (by default = 20)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is CCI and HMA.

The Commodity Channel Index (CCI) is a momentum-based technical indicator used in trading to measure a security's price relative to its average price over a given period. Developed by Donald Lambert in 1980, the CCI is primarily used to identify cyclical trends in a security, helping traders to spot potential buying or selling opportunities.

The CCI formula is:

CCI = (Typical Price − SMA) / (0.015 × Mean Deviation)

Typical Price (TP): This is calculated as the average of the high, low, and closing prices for the period.

Simple Moving Average (SMA): This is the average of the Typical Prices over a specific number of periods.

Mean Deviation: This is the average of the absolute differences between the Typical Price and the SMA.

The result is a value that typically fluctuates between +100 and -100, though it is not bounded and can go higher or lower depending on the price movement.

The Hull Moving Average (HMA) is a type of moving average that was developed by Alan Hull to improve upon the traditional moving averages by reducing lag while maintaining smoothness. The goal of the HMA is to create an indicator that is both quick to respond to price changes and less prone to whipsaws (false signals).

How the Hull Moving Average is Calculated?

The Hull Moving Average is calculated using the following steps:

Weighted Moving Average (WMA): The HMA starts by calculating the Weighted Moving Average (WMA) of the price data over a period square root of n (sqrt(n))

Speed Adjustment: A WMA is then calculated for half of the period n/2, and this is multiplied by 2 to give more weight to recent prices.

Lag Reduction: The WMA of the full period n is subtracted from the doubled n/2 WMA.

Final Smoothing: To smooth the result and reduce noise, a WMA is calculated for the square root of the period n.

The formula can be represented as:

HMA(n) = WMA(WMA(n/2) × 2 − WMA(n), sqrt(n))

The Weighted Moving Average (WMA) is a type of moving average that gives more weight to recent data points, making it more responsive to recent price changes than a Simple Moving Average (SMA). In a WMA, each data point within the selected period is multiplied by a weight, with the most recent data receiving the highest weight. The sum of these weighted values is then divided by the sum of the weights to produce the WMA.

This strategy leverages HMA of user given period as a critical level which shall be broken to say that probability of trend change to the upside increased. HMA reacts faster than EMA or SMA to the price change, that’s why it increases chances to enter new trade earlier. Long-term period CCI helps to have an approximation of mid-term trend. If it’s above 0 the probability of uptrend increases. Short-period CCI allows to have an approximation of short-term trend reversal from down to uptrend. This approach increases chances to have a long trade setup in the direction of mid-term trend when the short-term trend starts to reverse.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements. It’s also important to make a note, that script uses HMA to enter the trade, but for trailing it leverages EMA. It’s used because EMA has no such fast reaction to price move which increases probability not to be stopped out from any significant uptrend move.

Backtest Results

Operating window: Date range of backtests is 2022.07.01 - 2024.08.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 100%

Maximum Single Position Loss: -4.67%

Maximum Single Profit: +19.66%

Net Profit: +14897.94 USDT (+148.98%)

Total Trades: 104 (36.54% win rate)

Profit Factor: 2.312

Maximum Accumulated Loss: 1302.66 USDT (-9.58%)

Average Profit per Trade: 143.25 USDT (+0.96%)

Average Trade Duration: 34 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 2h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Moving Average Crossover Swing StrategyMoving Average Crossover Swing Strategy

**Overview:**

The basic concept of this strategy is to generate a signal when a faster/shorter length moving average crosses over (for Longs) or crosses under (for Shorts) a medium/longer length moving average. All of which are customizable. This strategy can work on any timeframe, however the daily is the timeframe used for the default settings and screenshots, as it was designed to be a multi-day swing strategy. Once a signal has been confirmed with a candle close, based on user options, the strategy will enter the trade on the open of the next candle.

The crossover strategy is nothing new to trading, but what can make this strategy unique and helpful, is the addition of further confirmation points, ATR based stop loss and take profit targets, optional early exit criteria, customizable to your needs and style, and just about everything visual can be toggled on/off. This strategy is based on a Trend (MA) indicator and a Momentum (MACD) indicator. While a Volume-based indicator is not shown here, one could consider using their favorite from that category to further compliment the signal idea.

It should be noted that depending on the time frame, direction(s) chosen, the signal options, confirmation options, and exit options selected, that a ticker may not produce more than 100 trades on the back test. Depending on your style and frequency, one could consider adjusting options and/or testing multiple tickers. It should also be noted that this strategy simply tests the underlying stock prices, not options contracts. And of course, testing this strategy against historical data does not assume that the same results will occur in future price action.

Shoutout given to Ripster's Clouds Indicator as pieces of that code were taken and modified to create both the Cloud visualization effects, and the Moving Average Pair Plots that are implemented in this strategy.

BASIC DEFAULTS

All can be changed as normal

Initial capital = 10,000

Order Sizing = 25% of equity (use the "Inputs" tab to modify this)

Pyramiding = 0

Commission = 0.65 USD per order

Price Verification = 1 tick

Slippage = 1 tick

RISK MANAGMENT

You will notice two different percentage options and ATR multipliers. This strategy will adjust position sizing by not exceeding either one of those % values based on the ATR (Average True Range) of the symbol and the multipliers selected, should the stock hit the stop loss price.

For Example, lets assume these values are true:

Account size = $10,000,

Max Risk = 1% of account size

Max Position Size = 25% of the account size

Stock Price = 23.45

ATR = 3.5

ATR Stop Loss Multiplier = 1.4

Then the formulas would be:

ACCT_SIZE * MaxRisk_% = 10000 * .01 = $100 (MaxCashRisk)

-----

MaxCashRisk / (ATR * ATR_SL_MULTIPLIER) = 100 / (3.5 * 1.4) = 20.4 Shares based on Max Cash Risk

-----

(ACCT_SIZE * MaxEquity_%) / STOCK_PRICE = (10000 * .25) / 23.45 = 106.61 Shares based on Max Equity Allocation

The minimum value of each of those options is then used, which in this case would be to purchase 20 shares so as not to exceed the max dollar risk should the stock reach the stop loss target. Likewise, if the ATR were to be much lower, say 0.48 cents, and all else the same, then the strategy would purchase the 106 shares based on Max Equity Allocation because the Max Cash Risk would require 149.25 shares.

MOVING AVERAGE OPTIONS

Select between and change the length & type of up to 5 pairs (10 total) of moving averages

The "Show Cloud-x" option will display a fill color between the "a" and "b" pairs

All moving averages lines can be toggled on/off in the "Style" tab, as well as adjusting their colors.

Visualization features do not affect calculations, meaning you could have all or nothing on the chart and the strategy will still produce results

SIGNAL CHOICES

Choose the fast/shorter length MA and the medium/longer length MA to determine the entry signal

CONFIRMATION OPTIONS

Both of these have customizable values and can be toggled on/off

A candle close over a slower/much longer length moving average

An additional cross-over (cross-under for Shorts) on the MACD indicator using default MACD values. While the MACD indicator is not necessary to have on the chart, it can help to add that for visualization. The calculations will perform whether the indicator is on the chart or not.

EARLY EXIT CRITERIA

Both can be toggled on/off with customizable values

MA Cross Exit will exit the trade early if the select moving averages cross-under (for longs) or cross-over (for shorts), indicating a potential reversal.

Max Bars in Trades will act as a last-resort exit by simply calculating the amount of full bars the trade has been open, and exiting on the opening of the next bar. For example: the default value is 8 bars, so after 8 full bars in the trade, if no other exit has been triggered (Stop Loss, Take Profit, or MA Cross(if enabled)), then the trade will exit at the opening of the 9th bar.

Finally, there is a table displaying the amount of trades taken for each side, and the amount & percent of both early exits. This table can be turned off in the "Style" tab

ADDITIONAL PLOTS

MACD (Moving Average Convergence/Divergence):

- The MACD is an optional confirmation indicator for this strategy.

- Plotting the indicator is not necessary for the strategy to work, but it can be helpful to visually see the status and position of the MACD if this feature is enabled in the strategy

- This helps to identify if there is also momentum behind the entry signal

Strategy SEMA SDI WebhookPurpose of the Code:

The strategy utilizes Exponential Moving Averages (EMA) and Smoothed Directional Indicators (SDI) to generate buy and sell signals. It includes features like leverage, take profit, stop loss, and trailing stops. The strategy is intended for backtesting and automating trades based on the specified indicators and conditions.

Key Components and Functionalities:

1.Strategy Settings:

Overlay: The strategy will overlay on the price chart.

Slippage: Set to 1.

Commission Value: Set to 0.035.

Default Quantity Type: Percent of equity.

Default Quantity Value: 50% of equity.

Initial Capital: Set to 1000 units.

Calculation on Order Fills: Enabled.

Process Orders on Close: Enabled.

2.Date and Time Filters:

Inputs for enabling/disabling start and end dates.

Filters to execute strategy only within specified date range.

3.Leverage and Quantity:

Leverage: Adjustable leverage input (default 3).

USD Percentage: Adjustable percentage of equity to use for trades (default 50%).

Initial Capital: Calculated based on leverage and percentage of equity.

4.Take Profit, Stop Loss, and Trailing Stop:

Inputs for enabling/disabling take profit, stop loss, and trailing stop.

Adjustable parameters for take profit percentage (default 25%), stop loss percentage (default 4.8%), and trailing stop percentage (default 1.9%).

Calculations for take profit, stop loss, trailing price, and maximum profit tracking.

5.EMA Calculations:

Fast and slow EMAs.

Smoothed versions of the fast and slow EMAs.

6.SDI Calculations:

Directional movement calculation for positive and negative directional indicators.

Difference between the positive and negative directional indicators, smoothed.

7.Buy/Sell Conditions:

Long (Buy) Condition: Positive DI is greater than negative DI, and fast EMA is greater than slow EMA.

Short (Sell) Condition: Negative DI is greater than positive DI, and fast EMA is less than slow EMA.

8.Strategy Execution:

If buy conditions are met, close any short positions and enter a long position.

If sell conditions are met, close any long positions and enter a short position.

Exit conditions for long and short positions based on take profit, stop loss, and trailing stop levels.

Close all positions if outside the specified date range.

Usage:

This strategy is used to automate trading based on the specified conditions involving EMAs and SDI. It allows backtesting to evaluate performance based on historical data. The strategy includes risk management through take profit, stop loss, and trailing stops to protect gains and limit losses. Traders can customize the parameters to fit their specific trading preferences and risk tolerance. Differently, it can perform leverage analysis and use it as a template.

By using this strategy, traders can systematically execute trades based on technical indicators, helping to remove emotional bias and improve consistency in trading decisions.

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Smoothed Heiken Ashi Strategy Long OnlyThis is a trend-following approach that uses a modified version of Heiken Ashi candles with additional smoothing. Here are the key components and features:

1. Heiken Ashi Modification: The strategy starts by calculating Heiken Ashi candles, which are known for better trend visualization. However, it modifies the traditional Heiken Ashi by using Exponential Moving Averages (EMAs) of the open, high, low, and close prices.

2. Double Smoothing: The strategy applies two layers of smoothing. First, it uses EMAs to calculate the Heiken Ashi values. Then, it applies another EMA to the Heiken Ashi open and close prices. This double smoothing aims to reduce noise and provide clearer trend signals.

3. Long-Only Approach: As the name suggests, this strategy only takes long positions. It doesn't short the market during downtrends but instead exits existing long positions when the sell signal is triggered.

4. Entry and Exit Conditions:

- Entry (Buy): When the smoothed Heiken Ashi candle color changes from red to green (indicating a potential start of an uptrend).

- Exit (Sell): When the smoothed Heiken Ashi candle color changes from green to red (indicating a potential end of an uptrend).

5. Position Sizing: The strategy uses a percentage of equity for position sizing, defaulting to 100% of available equity per trade. This should be tailored to each persons unique approach. Responsible trading would use less than 5% for each trade. The starting capital used is a responsible and conservative $1000, reflecting the average trader.

This strategy aims to provide a smooth, trend-following approach that may be particularly useful in markets with clear, sustained trends. However, it may lag in choppy or ranging markets due to its heavy smoothing. As with any strategy, it's important to thoroughly backtest and forward test before using it with real capital, and to consider using it in conjunction with other analysis tools and risk management techniques.

This has been created mainly to provide data to judge what time frame is most profitable for any single asset, as the volatility of each asset is different. This can bee seen using it on AUXUSD, which has a higher profitable result on the daily time frame, whereas other currencies need a higher or lower time frame. The user can toggle between each time frame and watch for the higher profit results within the strategy tester window.

Other smoothed Heiken Ashi indicators also do not provide buy and sell signals, and only show the change in color to dictate a change in trend. By adding buy and sell signals after the close of the candle in which the candle changes color, alerts can be programmed, which helps this be a more hands off protocol to experiment with. Other smoothed Heiken Ashi indicators do not allow for alarms to be set.

This is a unique HODL strategy which helps identify a change in trend, without the noise of day to day volatility. By switching to a line chart, it removes the candles altogether to avoid even more noise. The goal is to HODL a coin while the color is bullish in an uptrend, but once the indicator gives a sell signal, to sell the holdings back to a stable coin and let the chart ride down. Once the chart gives the next buy signal, use that same capital to buy back into the asset. In essence this removes potential losses, and helps buy back in cheaper, gaining more quantitity fo the asset, and therefore reducing your average initial buy in price.

Most HODL strategies ride the price up, miss selling at the top, then riding the price back down in anticipation that it will go back up to sell. This strategy will not hit the absolute tops, but it will greatly reduce potential losses.

Versatile Moving Average StrategyVersatile Moving Average Strategy (VMAS)

Overview:

The Versatile Moving Average Strategy (VMAS) is designed to provide traders with a flexible approach to trend-following, utilizing multiple types of moving averages. This strategy allows for customization in choosing the moving average type and length, catering to various market conditions and trading styles.

Key Features:

- Multiple Moving Average Types: Choose from SMA, EMA, SMMA (RMA), WMA, VWMA, HULL, LSMA, and ALMA to best suit your trading needs.

- Customizable Inputs: Adjust the moving average length, source of price data, and stop-loss source to fine-tune the strategy.

- Target Percent: Set the percentage difference between successive profit targets to manage your risk and rewards effectively.

- Position Management: Enable or disable long and short positions, allowing for versatility in different market conditions.

- Commission and Slippage: The strategy includes realistic commission settings to ensure accurate backtesting results.

Strategy Logic:

1. Moving Average Calculation: The selected moving average is calculated based on user-defined parameters.

2. Entry Conditions:

- A long position is entered when the entry source crosses over the moving average, if long positions are enabled.

- A short position is entered when the entry source crosses under the moving average, if short positions are enabled.

3. Stop-Loss: Positions are closed if the stop-loss source crosses the moving average in the opposite direction.

4. Profit Targets: Multiple profit targets are defined, with each target set at an incremental percentage above (for long positions) or below (for short positions) the entry price.

Default Properties:

- Account Size: $10000

- Commission: 0.01% per trade

- Risk Management: Positions are sized to risk 80% of the equity per trade, because we get very tight stoploss when position is open.

- Sample Size: Backtesting has been conducted to ensure a sufficient sample size of trades, ideally more than 100 trades.

How to Use:

1. Configure Inputs: Set your preferred moving average type, length, and other input parameters.

2. Enable Positions: Choose whether to enable long, short, or both types of positions.

3. Backtest and Analyze: Run backtests with realistic settings and analyze the results to ensure the strategy aligns with your trading goals.

4. Deploy and Monitor: Once satisfied with the backtesting results, deploy the strategy in a live environment and monitor its performance.

This strategy is suitable for traders looking to leverage moving averages in a versatile and customizable manner. Adjust the parameters to match your trading style and market conditions for optimal results.

Note: Ensure the strategy settings used for publication are the same as those described here. Always conduct thorough backtesting before deploying any strategy in a live trading environment.

Price Based Z-Trend - Strategy [presentTrading]█ Introduction and How it is Different

Z-score: a statistical measurement of a score's relationship to the mean in a group of scores.

Simple but effective approach.

The "Price Based Z-Trend - Strategy " leverages the Z-score, a statistical measure that gauges the deviation of a price from its moving average, normalized against its standard deviation. This strategy stands out due to its simplicity and effectiveness, particularly in markets where price movements often revert to a mean. Unlike more complex systems that might rely on a multitude of indicators, the Z-Trend strategy focuses on clear, statistically significant price movements, making it ideal for traders who prefer a streamlined, data-driven approach.

BTCUSD 6h LS Performance

█ Strategy, How It Works: Detailed Explanation

🔶 Calculation of the Z-score

"Z-score is a statistical measurement that describes a value's relationship to the mean of a group of values. Z-score is measured in terms of standard deviations from the mean. If a Z-score is 0, it indicates that the data point's score is identical to the mean score. A Z-score of 1.0 would indicate a value that is one standard deviation from the mean. Z-scores may be positive or negative, with a positive value indicating the score is above the mean and a negative score indicating it is below the mean."

The Z-score is central to this strategy. It is calculated by taking the difference between the current price and the Exponential Moving Average (EMA) of the price over a user-defined length, then dividing this by the standard deviation of the price over the same length:

z = (x - μ) /σ

Local

🔶 Trading Signals

Trading signals are generated based on the Z-score crossing predefined thresholds:

- Long Entry: When the Z-score crosses above the positive threshold.

- Long Exit: When the Z-score falls below the negative threshold.

- Short Entry: When the Z-score falls below the negative threshold.

- Short Exit: When the Z-score rises above the positive threshold.

█ Trade Direction

The strategy allows users to select their preferred trading direction through an input option.

█ Usage

To use this strategy effectively, traders should first configure the Z-score thresholds according to their risk tolerance and market volatility. It's also crucial to adjust the length for the EMA and standard deviation calculations based on historical performance and the expected "noise" in price data.

The strategy is designed to be flexible, allowing traders to refine settings to better capture profitable opportunities in specific market conditions.

█ Default Settings

- Trade Direction: Both

- Standard Deviation Length: 100

- Average Length: 100

- Threshold for Z-score: 1.0

- Bar Color Indicator: Enabled

These settings offer a balanced starting point but can be customized to suit various trading styles and market environments. The strategy's parameters are designed to be adjusted as traders gain experience and refine their approach based on ongoing market analysis.

Z-score is a must-learn approach for every algorithmic trader.

Bitcoin Momentum StrategyThis is a very simple long-only strategy I've used since December 2022 to manage my Bitcoin position.

I'm sharing it as an open-source script for other traders to learn from the code and adapt it to their liking if they find the system concept interesting.

General Overview

Always do your own research and backtesting - this script is not intended to be traded blindly (no script should be) and I've done limited testing on other markets beyond Ethereum and BTC, it's just a template to tweak and play with and make into one's own.

The results shown in the strategy tester are from Bitcoin's inception so as to get a large sample size of trades, and potential returns have diminished significantly as BTC has grown to become a mega cap asset, but the script includes a date filter for backtesting and it has still performed solidly in recent years (speaking from personal experience using it myself - DYOR with the date filter).

The main advantage of this system in my opinion is in limiting the max drawdown significantly versus buy & hodl. Theoretically much better returns can be made by just holding, but that's also a good way to lose 70%+ of your capital in the inevitable bear markets (also speaking from experience).

In saying all of that, the future is fundamentally unknowable and past results in no way guarantee future performance.

System Concept:

Capture as much Bitcoin upside volatility as possible while side-stepping downside volatility as quickly as possible.

The system uses a simple but clever momentum-style trailing stop technique I learned from one of my trading mentors who uses this approach on momentum/trend-following stock market systems.

Basically, the system "ratchets" up the stop-loss to be much tighter during high bearish volatility to protect open profits from downside moves, but loosens the stop loss during sustained bullish momentum to let the position ride.

It is invested most of the time, unless BTC is trading below its 20-week EMA in which case it stays in cash/USDT to avoid holding through bear markets. It only trades one position (no pyramiding) and does not trade short, but can easily be tweaked to do whatever you like if you know what you're doing in Pine.

Default parameters:

HTF: Weekly Chart

EMA: 20-Period

ATR: 5-period

Bar Lookback: 7

Entry Rule #1:

Bitcoin's current price must be trading above its higher-timeframe EMA (Weekly 20 EMA).

Entry Rule #2:

Bitcoin must not be in 'caution' condition (no large bearish volatility swings recently).

Enter at next bar's open if conditions are met and we are not already involved in a trade.

"Caution" Condition:

Defined as true if BTC's recent 7-bar swing high minus current bar's low is > 1.5x ATR, or Daily close < Daily 20-EMA.

Trailing Stop:

Stop is trailed 1 ATR from recent swing high, or 20% of ATR if in caution condition (ie. 0.2 ATR).

Exit on next bar open upon a close below stop loss.

I typically use a limit order to open & exit trades as close to the open price as possible to reduce slippage, but the strategy script uses market orders.

I've never had any issues getting filled on limit orders close to the market price with BTC on the Daily timeframe, but if the exchange has relatively low slippage I've found market orders work fine too without much impact on the results particularly since BTC has consistently remained above $20k and highly liquid.

Cost of Trading:

The script uses no leverage and a default total round-trip commission of 0.3% which is what I pay on my exchange based on their tier structure, but this can vary widely from exchange to exchange and higher commission fees will have a significantly negative impact on realized gains so make sure to always input the correct theoretical commission cost when backtesting any script.

Static slippage is difficult to estimate in the strategy tester given the wide range of prices & liquidity BTC has experienced over the years and it largely depends on position size, I set it to 150 points per buy or sell as BTC is currently very liquid on the exchange I trade and I use limit orders where possible to enter/exit positions as close as possible to the market's open price as it significantly limits my slippage.

But again, this can vary a lot from exchange to exchange (for better or worse) and if BTC volatility is high at the time of execution this can have a negative impact on slippage and therefore real performance, so make sure to adjust it according to your exchange's tendencies.

Tax considerations should also be made based on short-term trade frequency if crypto profits are treated as a CGT event in your region.

Summary:

A simple, but effective and fairly robust system that achieves the goals I set for it.

From my preliminary testing it appears it may also work on altcoins but it might need a bit of tweaking/loosening with the trailing stop distance as the default parameters are designed to work with Bitcoin which obviously behaves very differently to smaller cap assets.

Good luck out there!

Trend Deviation strategy - BTC [IkkeOmar]Intro:

This is an example if anyone needs a push to get started with making strategies in pine script. This is an example on BTC, obviously it isn't a good strategy, and I wouldn't share my own good strategies because of alpha decay.

This strategy integrates several technical indicators to determine market trends and potential trade setups. These indicators include:

Directional Movement Index (DMI)

Bollinger Bands (BB)

Schaff Trend Cycle (STC)

Moving Average Convergence Divergence (MACD)

Momentum Indicator

Aroon Indicator

Supertrend Indicator

Relative Strength Index (RSI)

Exponential Moving Average (EMA)

Volume Weighted Average Price (VWAP)

It's crucial for you guys to understand the strengths and weaknesses of each indicator and identify synergies between them to improve the strategy's effectiveness.

Indicator Settings:

DMI (Directional Movement Index):

Length: This parameter determines the number of bars used in calculating the DMI. A higher length may provide smoother results but might lag behind the actual price action.

Bollinger Bands:

Length: This parameter specifies the number of bars used to calculate the moving average for the Bollinger Bands. A longer length results in a smoother average but might lag behind the price action.

Multiplier: The multiplier determines the width of the Bollinger Bands. It scales the standard deviation of the price data. A higher multiplier leads to wider bands, indicating increased volatility, while a lower multiplier results in narrower bands, suggesting decreased volatility.

Schaff Trend Cycle (STC):

Length: This parameter defines the length of the STC calculation. A longer length may result in smoother but slower-moving signals.

Fast Length: Specifies the length of the fast moving average component in the STC calculation.

Slow Length: Specifies the length of the slow moving average component in the STC calculation.

MACD (Moving Average Convergence Divergence):

Fast Length: Determines the number of bars used to calculate the fast EMA (Exponential Moving Average) in the MACD.

Slow Length: Specifies the number of bars used to calculate the slow EMA in the MACD.

Signal Length: Defines the number of bars used to calculate the signal line, which is typically an EMA of the MACD line.

Momentum Indicator:

Length: This parameter sets the number of bars over which momentum is calculated. A longer length may provide smoother momentum readings but might lag behind significant price changes.

Aroon Indicator:

Length: Specifies the number of bars over which the Aroon indicator calculates its values. A longer length may result in smoother Aroon readings but might lag behind significant market movements.

Supertrend Indicator:

Trendline Length: Determines the length of the period used in the Supertrend calculation. A longer length results in a smoother trendline but might lag behind recent price changes.

Trendline Factor: Specifies the multiplier used in calculating the trendline. It affects the sensitivity of the indicator to price changes.

RSI (Relative Strength Index):

Length: This parameter sets the number of bars over which RSI calculates its values. A longer length may result in smoother RSI readings but might lag behind significant price changes.

EMA (Exponential Moving Average):

Fast EMA: Specifies the number of bars used to calculate the fast EMA. A shorter period results in a more responsive EMA to recent price changes.

Slow EMA: Determines the number of bars used to calculate the slow EMA. A longer period results in a smoother EMA but might lag behind recent price changes.

VWAP (Volume Weighted Average Price):

Default settings are typically used for VWAP calculations, which consider the volume traded at each price level over a specific period. This indicator provides insights into the average price weighted by trading volume.

backtest range and rules:

You can specify the start date for backtesting purposes.

You can can select the desired trade direction: Long, Short, or Both.

Entry and Exit Conditions:

LONG:

DMI Cross Up: The Directional Movement Index (DMI) indicates a bullish trend when the positive directional movement (+DI) crosses above the negative directional movement (-DI).

Bollinger Bands (BB): The price is below the upper Bollinger Band, indicating a potential reversal from the upper band.

Momentum Indicator: Momentum is positive, suggesting increasing buying pressure.

MACD (Moving Average Convergence Divergence): The MACD line is above the signal line, indicating bullish momentum.

Supertrend Indicator: The Supertrend indicator signals an uptrend.

Schaff Trend Cycle (STC): The STC indicates a bullish trend.

Aroon Indicator: The Aroon indicator signals a bullish trend or crossover.

When all these conditions are met simultaneously, the strategy considers it a favorable opportunity to enter a long trade.

SHORT:

DMI Cross Down: The Directional Movement Index (DMI) indicates a bearish trend when the negative directional movement (-DI) crosses above the positive directional movement (+DI).

Bollinger Bands (BB): The price is above the lower Bollinger Band, suggesting a potential reversal from the lower band.

Momentum Indicator: Momentum is negative, indicating increasing selling pressure.

MACD (Moving Average Convergence Divergence): The MACD line is below the signal line, signaling bearish momentum.

Supertrend Indicator: The Supertrend indicator signals a downtrend.

Schaff Trend Cycle (STC): The STC indicates a bearish trend.

Aroon Indicator: The Aroon indicator signals a bearish trend or crossover.

When all these conditions align, the strategy considers it an opportune moment to enter a short trade.

Disclaimer:

THIS ISN'T AN OPTIMAL STRATEGY AT ALL! It was just an old project from when I started learning pine script!

The backtest doesn't promise the same results in the future, always do both in-sample and out-of-sample testing when backtesting a strategy. And make sure you forward test it as well before implementing it!