XAUUSD Correlation IndicatorXAUUSD Correlation Indicator

Questo indicatore per TradingView calcola e visualizza la correlazione tra il prezzo di XAUUSD (oro) e una serie di altri asset finanziari, tra cui valute (EURUSD, AUDUSD, NZDUSD, GBPUSD), metalli preziosi (platino, argento), indici azionari (SPX500, DJI, NASDAQ) e il dollaro statunitense (DXY).

L'indicatore offre:

1. Correlazione: Calcola la correlazione tra XAUUSD e gli altri asset su un periodo personalizzabile, dove un numero superiore allo 0 indica una correlazione positiva ed un numero inferiore allo 0 indica una correlazione negativa.

2. Variazione percentuale: Mostra la variazione percentuale dei prezzi degli asset rispetto all'apertura.

3. Visualizzazione personalizzabile: Permette di ordinare i dati in base alla correlazione o alla variazione percentuale.

4. Tabella interattiva: I risultati sono visualizzati in una tabella colorata, con opzioni per personalizzare i colori di sfondo, testo e bordi.

Ideale per trader e analisti che vogliono monitorare le relazioni tra l'oro e altri mercati in tempo reale, questo strumento aiuta a identificare opportunità di trading basate su correlazioni e tendenze di mercato.

Fundamental Analysis

EZ_Algo Copyright label

This script overlays a fully adjustable watermark on your chart, featuring:

A bold Main Title (e.g., your brand or name) and Subtitle (e.g., a tagline or ID).

Optional extras like a copyright notice, logo symbol, warning message, and chart info (symbol, timeframe, timestamp, or close price).

A subtle repeating overlay pattern to deter theft.

Flexible positioning, sizing, and color options to match your vib

e

It’s built for traders who want to protect their charts and make them stand out, all in a few clicks.

How to Use It

Add to Chart: Click "Add to Chart" and watch the default watermark appear (e.g., "EZ ALGO" at the top).

Customize It:

Main Title: Set your brand (e.g., "EZ ALGO") under "Main Title". Tweak color, size, and alignment.

Subtitle: Add a tagline (e.g., "Algo Trading") and trader ID (e.g., "@EZ_Algo

") with matching style options.

Text Opacity: Adjust "Text Opacity" in "Appearance" to control title and subtitle transparency (0 = solid, 100 = invisible).

Chart Info: Toggle "Show Chart Info" to display symbol and timestamp, or add "Show Close Price" for extra data.

Extras: Enable "Show Copyright" for a © notice, "Show Logo" for a symbol (e.g., ★), or "Show Warning" to shout "DO NOT COPY".

Overlay Pattern: Turn on "Show Overlay Pattern" to repeat a phrase (e.g., "EZ Algo") across the chart.

Positioning: Pick vertical/horizontal spots (top, middle, bottom; left, center, right) or try "Randomize Main Position" for a surprise placement.

Appearance: Set a "Background Color" and "Background Opacity" for the watermark’s backdrop.

Cell Size: Adjust "Cell Width (%)" and "Cell Height (%)" to resize the watermark (0 = auto-fit).

Apply & Share: Hit "OK" to save settings, then screenshot or share your branded chart with confidence!

Tips

Use a semi-transparent background (e.g., 50 opacity) to keep the chart readable.

Experiment with "Randomize Main Position" for a dynamic look.

Pair a bold logo with a faint overlay pattern for max branding power.

Credits

Inspired by @KristaKT

thanks for the great ideas!

Enjoy marking your charts with flair and protection! Questions? Drop a comment below.

Enhanced HHLL Time Confirmation with EMAStrong recommendation , remove the green and red circle , or leave it how it is ;)

To be used on 1 minute chart MSTR , Stock

other time frames are good , ;)

How to Use

HHLL Signals: Look for green triangles (buy) below bars or red triangles (sell) above bars to identify confirmed HH/LL setups with trend alignment.

EMA Signals: Watch for lime circles (buy) below bars or maroon circles (sell) above bars when price crosses the EMA 400 in a trending market.

Trend Context: Use the EMA 400 as a dynamic support/resistance level and the SMA trend filter to gauge market direction.

Enable alerts to get notified of signals in real-time.

Best Practices

Adjust the Lookback Period and Confirmation Minutes to suit your timeframe (e.g., shorter for scalping, longer for swing trading).

Combine with other indicators (e.g., volume, RSI) for additional confirmation.

Test on your preferred market and timeframe to optimize settings.

Indicator Description: Enhanced HHLL Time Confirmation with EMA

Overview

The "Enhanced HHLL Time Confirmation with EMA" is a versatile trading indicator designed to identify key reversal and continuation signals based on Higher Highs (HH), Lower Lows (LL), and a 400-period Exponential Moving Average (EMA). It incorporates time-based confirmation and trend filters to reduce noise and improve signal reliability. This indicator is ideal for traders looking to spot trend shifts or confirm momentum with a combination of price structure and moving average crossovers.

Key Features

Higher High / Lower Low Detection:

Identifies HH and LL based on a customizable lookback period (default: 30 bars).

Signals are confirmed only after a user-defined time period (in minutes, default: 60) has passed since the last HH or LL, ensuring stability.

Trend Filter:

Uses a fast (10-period) and slow (30-period) Simple Moving Average (SMA) crossover to confirm bullish or bearish trends.

Buy signals require a bullish trend (Fast SMA > Slow SMA), and sell signals require a bearish trend (Fast SMA < Slow SMA).

EMA 400 Integration:

Plots a 400-period EMA (customizable) as a long-term trend reference.

Generates additional buy/sell signals when price crosses above (buy) or below (sell) the EMA 400, filtered by trend direction.

Visualizations:

Optional dashed lines for HH and LL levels (toggleable).

Debug markers (diamonds) to visualize HH/LL detection points.

Distinct signal shapes: triangles for HHLL signals (green/red) and circles for EMA signals (lime/maroon).

Alerts:

Built-in alert conditions for HHLL Buy/Sell and EMA Buy/Sell signals, making it easy to stay informed of key events.

Input Parameters

Lookback Period (default: 30): Number of bars to look back for HH/LL detection.

Confirmation Minutes (default: 60): Time (in minutes) required to confirm HH/LL signals.

High/Low Source: Select the price source for HH (default: high) and LL (default: low).

Show HH/LL Lines (default: true): Toggle visibility of HH/LL dashed lines.

Show Debug Markers (default: true): Toggle HH/LL detection markers.

EMA Period (default: 400): Adjust the EMA length.

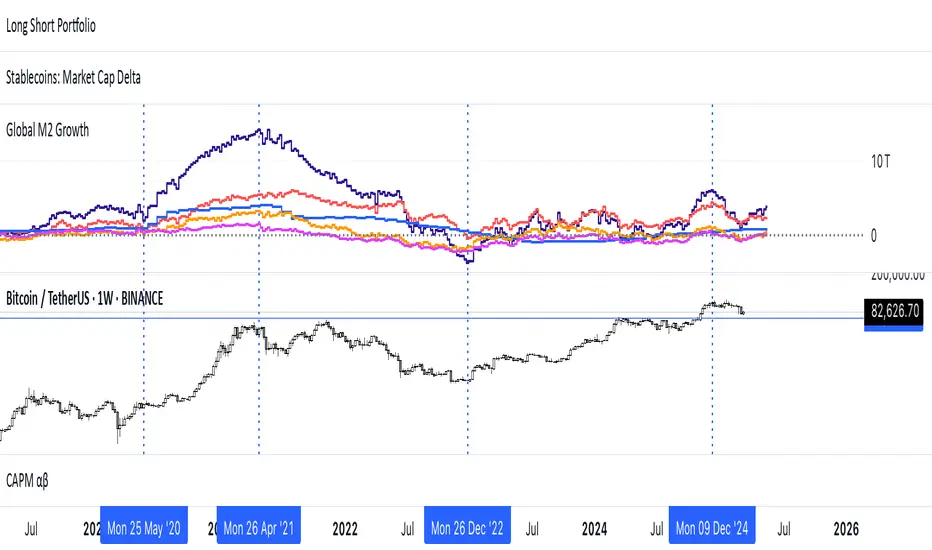

Global M2 Money Supply (USD) GrowthThe Global M2 Growth indicator evaluates the total liquid money supply, including cash, checking deposits, and assets that can be easily converted to cash. It reflects changes in global liquidity by tracking year-on-year (YoY) changes in the Global M2 money supply rather than its absolute value. This approach highlights the velocity of liquidity expansion or contraction, offering a clearer understanding of its correlation with asset performance, such as Bitcoin.

How It Works

When the Global M2 money supply expands, it reflects an increase in available liquidity. This often leads to an influx of capital into higher-yielding and riskier assets like Bitcoin, equities, and commodities. Conversely, when M2 contracts, liquidity tightens, leading to declines in the values of these assets.

An essential insight is that Bitcoin's price is not immediately affected by changes in M2. Research shows a lag of approximately 56-60 days (around two months) between liquidity changes and Bitcoin's price movements. Shifting the liquidity data forward by this period improves the correlation between Global M2 and Bitcoin performance.

How to Use

Track Global M2 YoY Change: Focus on liquidity's yearly change to identify trends. Rapid increases in liquidity often signify favorable conditions for Bitcoin and other risk assets to rise, while contractions often predict price declines or consolidation phases.

Account for the Lag Effect: Incorporate the two-month lag into your analysis to predict Bitcoin's potential moves more accurately. For instance, a recent resurgence in liquidity growth could signal a Bitcoin rally within the next two months.

Use as a Macro Indicator: Monitor liquidity trends alongside other economic indicators and asset performance metrics to build a more comprehensive investment framework.

By tracking these dynamics, traders and investors can better anticipate Bitcoin's trajectory and make informed decisions.

Binance Leveraged Liquidations ApproximationBinance Leveraged Liquidations Approximation (BLLA)

The Binance Leveraged Liquidations Approximation (BLLA) indicator is a tool designed to estimate liquidation levels for leveraged trading on Binance. It calculates the approximate prices at which liquidations could occur for long and short positions, based on the entry price and leverage levels selected by the user.

Key Features:

Liquidation Level Calculation:

Estimates liquidation prices for multiple leverage levels (e.g., 20x, 10x, 5x, etc.).

Supports both long and short positions.

Customization:

Allows the user to manually input the entry price or automatically calculate it as the midpoint between the low and high of a defined period.

Leverage levels are configurable, enabling the indicator to adapt to different trading strategies.

Clear Visualization:

Displays liquidation levels directly on the chart, with labels indicating the corresponding leverage.

Uses distinct colors for long positions (yellow) and short positions (blue).

Recommended Use:

Risk Management: Helps identify liquidation levels to adjust stop-loss orders and manage risk in leveraged trading.

Market Analysis: Provides a quick overview of key levels where significant price movements might occur due to mass liquidations.

Settings:

Entry Price: Enter manually or leave at 0.0 to calculate automatically.

Leverage: Configure desired leverage levels (e.g., 20x, 10x, 5x, etc.).

Transparency and Display: Adjust the transparency of the lines and the number of bars displayed.

Quick Instructions:

Add the indicator to your chart.

Enter the entry price or leave it at 0.0 to calculate automatically.

Configure leverage levels according to your strategy.

Observe liquidation levels on the chart and use them to manage your risk.

Note:

This indicator is an approximation and does not guarantee absolute accuracy of liquidation levels, as these may vary depending on market conditions and exchange policies.

Quantitative Easing and Tightening PeriodsQuantitative Easing (QE) and Quantitative Tightening (QT) periods based on historical events from the Federal Reserve:

Quantitative Easing (QE) Periods:

QE1:

Start: November 25, 2008

End: March 31, 2010

Description: The Federal Reserve initiated QE1 in response to the financial crisis, purchasing mortgage-backed securities and Treasuries.

QE2:

Start: November 3, 2010

End: June 29, 2011

Description: QE2 involved the purchase of $600 billion in U.S. Treasury bonds to further stimulate the economy.

QE3:

Start: September 13, 2012

End: October 29, 2014

Description: QE3 was an open-ended bond-buying program with monthly purchases of $85 billion in Treasuries and mortgage-backed securities.

QE4 (COVID-19 Pandemic Response):

Start: March 15, 2020

End: March 10, 2022

Description: The Federal Reserve engaged in QE4 in response to the economic impact of the COVID-19 pandemic, purchasing Treasuries and MBS in an effort to provide liquidity.

Quantitative Tightening (QT) Periods:

QT1:

Start: October 1, 2017

End: August 1, 2019

Description: The Federal Reserve began shrinking its balance sheet in 2017, gradually reducing its holdings of U.S. Treasuries and mortgage-backed securities. This period ended in August 2019 when the Fed decided to stop reducing its balance sheet.

QT2:

Start: June 1, 2022

End: Ongoing (as of March 2025)

Description: The Federal Reserve started QT again in June 2022, reducing its holdings of U.S. Treasuries and MBS in response to rising inflation. The Fed has continued this tightening cycle.

These periods are key moments in U.S. monetary policy, where the Fed either injected liquidity into the economy (QE) or reduced its balance sheet by not reinvesting maturing securities (QT). The exact dates and nature of these policies may vary based on interpretation and adjustments to the Fed's actions during those times.

M2 Global Liquidity Index - 10 Week Lead

M2 Global Liquidity Index - Forward Projection (10 Weeks)

This indicator provides a 10-week forward projection of the M2 Global Liquidity Index, offering traders insight into potential future market conditions based on global money supply trends.

What This Indicator Shows

The M2 Global Liquidity Index aggregates M2 money stock data from five major economies:

- China (CNY)

- United States (USD)

- European Union (EUR)

- Japan (JPY)

- Great Britain (GBP)

All values are converted to USD and presented as a unified global liquidity metric, providing a comprehensive view of worldwide monetary conditions.

Forward Projection Feature

This adaptation displays the indicator 10 weeks ahead of the current price, allowing you to visualize potential future liquidity conditions that might influence market behavior. The projection maintains data integrity while providing an advanced view of the liquidity landscape.

Trading Applications

- Anticipate potential market reactions to changing global liquidity conditions

- Identify divergences between projected liquidity and current price action

- Develop longer-term strategic positions based on forward liquidity projections

- Enhance your macro-economic analysis toolkit

Credit

This indicator is an adaptation of the original "M2 Global Liquidity Index" created by Mik3Christ3ns3n. Full credit for the original concept and implementation goes to the original author. This version simply adds a 10-week forward projection to the existing calculations.

Disclaimer

This indicator is for informational purposes only and should be used as one of many tools in your analysis. Past performance and projections are not guarantees of future results.

FinFluential Global M2 Money Supply // Days Offset =The "Global M2 Money Supply" indicator calculates and visualizes the combined M2 money supply from multiple countries and regions worldwide, expressed in trillions of USD.

M2 is a measure of the money supply that includes cash, checking deposits, and easily convertible near-money assets. This indicator aggregates daily M2 data from various economies, converts them into a common USD base using forex exchange rates, and plots the total as a single line on the chart.

It is designed as an overlay indicator aligned to the right scale, making it ideal for comparing global money supply trends with price action or other market data.

Key Features

Customizable Time Offset: Users can adjust the number of days to shift the M2 data forward or backward (from -1000 to +1000 days) via the indicator settings. This allows for alignment with historical events or forward-looking analysis.

Global Coverage Includes:

Eurozone: Eurozone M2 (converted via EUR/USD)

North America: United States, Canada

Non-EU Europe: Switzerland, United Kingdom, Finland, Russia

Pacific: New Zealand

Asia: China, Taiwan, Hong Kong, India, Japan, Philippines, Singapore

Latin America: Brazil, Colombia, Mexico

Middle East: United Arab Emirates, Turkey

Africa: South Africa

Cash Flow YieldsCash Flow Yields Indicator

This indicator offers a straightforward way to visualize a company’s cash flow metrics—Free Cash Flow (FCF), Operating Cash Flow (OCF), and Capital Expenditures (CapEx)—as yields relative to its market capitalization. With the flexibility to switch between Trailing Twelve Months (TTM) and Quarterly data, it’s perfect for spotting financial efficiency trends at a glance. Values are plotted as dynamic lines with smart color coding and labeled for clarity.

Features:

TTM & Quarterly Data: Toggle between financial periods to suit your analysis.

Color-Coded Lines: Green for positive OCF, teal for positive FCF, and blue for CapEx. Red and maroon kick in when values turn negative.

Yield Perspective: See FCF, OCF, and CapEx as percentages of market cap, making it easy to compare cash flow strength across companies.

Clear Labels: The latest values pop up on the chart, positioned to the right of the last bar.

Simple & Intuitive: No clutter - just clean lines and numbers to help you focus on what matters.

To use it, add it to your chart and toggle between TTM or Quarterly to see trends. FCF should roughly equal OCF minus CapEx. Adjust your view to focus on companies with strong FCF yields for potential opportunities.

This indicator is freely available and open-source on TradingView for everyone to use. Enjoy!

EMA Ribbon with 100 MA BY TIJUThe EMA Ribbon with 100 MA is a powerful and visually intuitive indicator designed to help traders identify trends, momentum, and potential support/resistance levels using multiple Exponential Moving Averages (EMAs). By plotting a series of EMAs with varying periods, the script creates a "ribbon" effect on the chart, making it easier to spot trend direction and strength at a glance.

Key Features:

Multiple EMAs for Trend Analysis:

The script plots 8 EMAs with periods ranging from 20 to 55, creating a gradient ribbon effect.

The 100-period EMA is added as a thick blue line, acting as a key level for long-term trend analysis.

Customizable Periods:

Each EMA period is fully customizable, allowing traders to tailor the indicator to their preferred trading style and timeframe.

Visual Clarity:

The EMAs are color-coded, making it easy to distinguish between different periods and identify the overall trend direction.

Dynamic Support/Resistance:

The EMAs act as dynamic support and resistance levels, helping traders identify potential entry and exit points.

Drop Candles Feature:

The script includes an option to drop the first N candles, ensuring cleaner calculations and avoiding false signals during the initial periods.

How to Use:

Trend Identification:

Uptrend: When the shorter-period EMAs are stacked above the longer-period EMAs, it indicates a strong uptrend.

Downtrend: When the longer-period EMAs are stacked above the shorter-period EMAs, it indicates a strong downtrend.

Consolidation: When the EMAs are intertwined, it suggests a sideways or weak trend.

Support/Resistance Levels:

Use the EMAs as dynamic support/resistance levels. For example, in an uptrend, the price may bounce off the lower EMAs.

100-Period EMA:

The 100-period EMA (thick blue line) acts as a key level for long-term trend analysis. A price above this line suggests a bullish bias, while a price below suggests a bearish bias.

Customization:

Adjust the EMA periods and colors to suit your trading strategy.

Use the Drop first N candles option to avoid false signals during the initial periods.

Example Use Cases:

Trend Following:

Enter long positions when the price is above the EMA ribbon and the EMAs are stacked in an uptrend.

Enter short positions when the price is below the EMA ribbon and the EMAs are stacked in a downtrend.

Dynamic Support/Resistance:

Use the EMAs as dynamic support/resistance levels for setting stop-loss or take-profit targets.

Confirmation Tool:

Combine the EMA Ribbon with other indicators (e.g., RSI, MACD) to confirm trade signals.

Settings:

MA-1 to MA-8 Periods: Adjust the periods for the 8 EMAs (default: 20, 25, 30, 35, 40, 45, 50, 55).

MA-100 Period: Adjust the period for the 100 EMA (default: 100).

Source: Choose the price source for the EMAs (default: Close).

Drop First N Candles: Drop the first N candles to avoid false signals (default: 1).

Why Use EMA Ribbon ?

Versatility: Suitable for all trading styles (scalping, day trading, swing trading) and timeframes.

Visual Appeal: The color-coded ribbon makes it easy to interpret the trend at a glance.

Customizable: Tailor the indicator to your specific trading strategy.

Dynamic Levels: Use the EMAs as dynamic support/resistance levels for better risk management.

Stock Earnings Viewer for Pine ScreenerThe script, titled "Stock Earnings Viewer with Surprise", fetches actual and estimated earnings, calculates absolute and percent surprise values, and presents them for analysis. It is intended to use in Pine Screener, as on chart it is redundant.

How to Apply to Pine Screener

Favorite this script

Open pine screener www.tradingview.com

Select "Stock Earnings Viewer with Surprise" in "Choose indicator"

Click "Scan"

Data

Actual Earnings: The reported earnings per share (EPS) for the stock, sourced via request.earnings().

Estimated Earnings: Analyst-predicted EPS, accessed with field=earnings.estimate.

Absolute Surprise: The difference between actual and estimated earnings (e.g., actual 1.2 - estimated 1.0 = 0.2).

Percent Surprise (%): The absolute surprise as a percentage of estimated earnings (e.g., (0.2 / 1.0) * 100 = 20%). Note: This may return NaN or infinity if estimated earnings are zero, due to division by zero.

Practical Use

This screener script allows users to filter stocks based on earnings metrics. For example, you could screen for stocks where Percent Surprise > 15 to find companies exceeding analyst expectations significantly, or use Absolute Surprise < -0.5 to identify underperformers.

EPS Line Indicator - cristianhkrOverview

The EPS Line Indicator displays the Earnings Per Share (EPS) of a publicly traded company directly on a TradingView chart. It provides a historical trend of EPS over time, allowing investors to track a company's profitability per share.

Key Features

📊 Plots actual EPS data for the selected stock.

📅 Updates quarterly as new EPS reports are released.

🔄 Smooths missing values by holding the last reported EPS.

🔍 Helps track long-term profitability trends.

How It Works

The script retrieves quarterly EPS using request.financial(syminfo.tickerid, "EARNINGS_PER_SHARE", "Q", barmerge.gaps_off).

If EPS data is missing for a given period, the last available EPS value is retained to maintain continuity.

The EPS values are plotted as a continuous green line on the chart.

A baseline at EPS = 0 is included to easily identify profitable vs. loss-making periods.

How to Use This Indicator

If the EPS line is trending upwards 📈 → The company is growing earnings per share, a strong sign of profitability.

If the EPS line is declining 📉 → The company’s EPS is shrinking, which may indicate financial weakness.

If EPS is negative (below zero) ❌ → The company is reporting losses per share, which can be a warning sign.

Limitations

Only works with stocks that report EPS data (not applicable to cryptocurrencies or commodities).

Does not adjust for stock splits or other corporate actions.

Best used on daily, weekly, or monthly charts for clear earnings trends.

Conclusion

This indicator is a powerful tool for investors who want to visualize earnings per share trends directly on a price chart. By showing how EPS evolves over time, it helps assess a company's profitability trajectory, making it useful for both fundamental analysis and long-term investing.

🚀 Use this indicator to track EPS growth and make smarter investment decisions!

CAPE / Shiller PE Ratio - cristianhkrThe Cyclically Adjusted Price-to-Earnings Ratio (CAPE Ratio), also known as the Shiller P/E Ratio, is a long-term valuation measure for stocks. It was developed by Robert Shiller and smooths out earnings fluctuations by using an inflation-adjusted average of the last 10 years of earnings.

This TradingView Pine Script indicator calculates the CAPE Ratio for a specific stock by:

Fetching historical Earnings Per Share (EPS) data using request.earnings().

Adjusting the EPS for inflation by dividing it by the Consumer Price Index (CPI).

Computing the 10-year (40-quarter) moving average of the inflation-adjusted EPS.

Calculating the CAPE Ratio as (Stock Price) / (10-year Average EPS adjusted for inflation).

Plotting the CAPE Ratio on the chart with a reference line at CAPE = 20, a historically significant threshold.

Revenue & Net IncomeRevenue & Net Income Indicator

This indicator provides a clear visual representation of a company's revenue and net income, with the flexibility to switch between Trailing Twelve Months (TTM) and Quarterly data. Values are automatically converted into billions and displayed in both an area chart and a dynamic table.

Features:

TTM & Quarterly Data: Easily toggle between financial periods.

Intuitive Visuals: Semi-transparent area charts make trends easy to spot.

Smart Number Formatting: Revenue below 1B is shown with two decimals (e.g., "0.85B"), while larger values use one decimal (e.g., "1.2B").

Customizable Table: Displays the most recent revenue and net income figures, with adjustable position and text size.

Light Mode: Switch table text to black with a white header for better readability on light backgrounds.

This indicator is freely available and open-source on TradingView for all. It is designed to help traders enhance their market analysis and strategic decision-making.

Trading Sessions Background ColorTrading Sessions Background Color

This indicator provides a visual representation of the major trading sessions — Asia, London, and USA — by applying distinct background colors to the chart. It allows traders to easily identify active market hours and session overlaps.

Features:

Customizable Sessions: Users can modify time ranges, and colors according to their preferences.

Predefined Major Trading Sessions: The indicator includes Asia, London, and USA sessions by default.

Time Zone Adjustment: A configurable UTC offset ensures accurate session display.

Clear Visual Differentiation: Background colors indicate when each session is active.

Usage Instructions:

Apply the indicator to a TradingView chart.

Adjust session settings and time zone offset as needed.

The chart background will update dynamically to reflect the active trading session.

Monthly Buy IndicatorIt shows us the the total balance when buying monthly, ploting the total invested amount and total current balance along the time.

Opening the Data Window, it displays the profit (%) and the number of trades.

The "Allow Fractional Purchase" flag can be used to check the the performance of the ticker, disregarding how much the monthly amount is set vs the price of the ticker.

The trades are considering buying the available amount on the 1st candle of each month, at the Open price. The "Total Balance" considers the close price of each candle.

RV- Intrinsic Value AnalyzerWhy These Metrics Matter in IVA Pro (Intrinsic Value Analyzer)?

The IVA Pro consolidates key valuation, profitability, and efficiency metrics into a single, easy-to-read table. These indicators provide a comprehensive view of a company’s financial health, helping traders and investors make informed decisions based on growth potential, profitability, and valuation. The color-coded signals (green for strong, orange for moderate, and red for weak values) simplify fundamental analysis and enable quick comparisons across different stocks.

Key Fundamental Parameters in IVA Pro

Market Capitalization (Market Cap): Measures a company's total market value, helping assess size, stability, and growth potential.

Earnings Yield (TTM): Indicates how much profit a company generates relative to its stock price—useful for comparing against bonds and other assets.

Return on Capital Employed (ROCE): Shows how efficiently a company generates profits using its capital—a key profitability metric.

Return on Equity (ROE): Evaluates how well a company uses shareholder funds to generate earnings.

Price-to-Earnings Ratio (PE): Helps determine whether a stock is overvalued or undervalued based on earnings.

Price-to-Book Ratio (PB): Assesses if a stock is trading above or below its net asset value—useful for asset-heavy industries.

Price-to-Sales Ratio (PS): Helps evaluate revenue potential, particularly for growth-stage companies.

PEG Ratio: Enhances PE ratio by factoring in earnings growth—ideal for identifying undervalued growth stocks.

Forward PE Ratio: Provides a future-looking valuation based on projected earnings.

Forward PS Ratio: Helps evaluate future revenue potential and overall stock valuation.

TradFi Fundamentals: Enhanced Macroeconomic Momentum Trading Introduction

The "Enhanced Momentum with Advanced Normalization and Smoothing" indicator is a tool that combines traditional price momentum with a broad range of macroeconomic factors. I introduced the basic version from a research paper in my last script. This one leverages not only the price action of a security but also incorporates key economic data—such as GDP, inflation, unemployment, interest rates, consumer confidence, industrial production, and market volatility (VIX)—to create a comprehensive, normalized momentum score.

Previous indicator

Explanation

In plain terms, the indicator calculates a raw momentum value based on the change in price over a defined lookback period. It then normalizes this momentum, along with several economic indicators, using a method chosen by the user (options include simple, exponential, or weighted moving averages, as well as a median absolute deviation (MAD) approach). Each normalized component is assigned a weight reflecting its relative importance, and these weighted values are summed to produce an overall momentum score.

To reduce noise, the combined momentum score can be further smoothed using a user-selected method.

Signals

For generating trade signals, the indicator offers two modes:

Zero Cross Mode: Signals occur when the smoothed momentum line crosses the zero threshold.

Zone Mode: Overbought and oversold boundaries (which are user defined) provide signals when the momentum line crosses these preset limits.

Definition of the Settings

Price Momentum Settings:

Price Momentum Lookback: The number of days used to compute the percentage change in price (default 50 days).

Normalization Period (Price Momentum): The period over which the price momentum is normalized (default 200 days).

Economic Data Settings:

Normalization Period (Economic Data): The period used to normalize all economic indicators (default 200 days).

Normalization Method: Choose among SMA, EMA, WMA, or MAD to standardize both price and economic data. If MAD is chosen, a multiplier factor is applied (default is 1.4826).

Smoothing Options:

Apply Smoothing: A toggle to enable further smoothing of the combined momentum score.

Smoothing Period & Method: Define the period and type (SMA, EMA, or WMA) used to smooth the final momentum score.

Signal Generation Settings:

Signal Mode: Select whether signals are based on a zero-line crossover or by crossing user-defined overbought/oversold (OB/OS) zones.

OB/OS Zones: Define the upper and lower boundaries (default upper zones at 1.0 and 2.0, lower zones at -1.0 and -2.0) for zone-based signals.

Weights:

Each component (price momentum, GDP, inflation, unemployment, interest rates, consumer confidence, industrial production, and VIX) has an associated weight that determines its contribution to the overall score. These can be adjusted to reflect different market views or risk preferences.

Visual Aspects

The indicator plots the smoothed combined momentum score as a continuous blue line against a dotted zero-line reference. If the Zone signal mode is selected, the indicator also displays the upper and lower OB/OS boundaries as horizontal lines (red for overbought and green for oversold). Buy and sell signals are marked by small labels ("B" for buy and "S" for sell) that appear at the bottom or top of the chart when the score crosses the defined thresholds, allowing traders to quickly identify potential entry or exit points.

Conclusion

This enhanced indicator provides traders with a robust approach to momentum trading by integrating traditional price-based signals with a suite of macroeconomic indicators. Its normalization and smoothing techniques help reduce noise and mitigate the effects of outliers, while the flexible signal generation modes offer multiple ways to interpret market conditions. Overall, this tool is designed to deliver a more nuanced perspective on market momentum.

Cryptolabs Global Liquidity Cycle Momentum IndicatorCryptolabs Global Liquidity Cycle Momentum Indicator (LMI-BTC)

This open-source indicator combines global central bank liquidity data with Bitcoin price movements to identify medium- to long-term market cycles and momentum phases. It is designed for traders who want to incorporate macroeconomic factors into their Bitcoin analysis.

How It Works

The script calculates a Liquidity Index using balance sheet data from four central banks (USA: ECONOMICS:USCBBS, Japan: FRED:JPNASSETS, China: ECONOMICS:CNCBBS, EU: FRED:ECBASSETSW), augmented by the Dollar Index (TVC:DXY) and Chinese 10-year bond yields (TVC:CN10Y). This index is:

- Logarithmically scaled (math.log) to better represent large values like central bank balances and Bitcoin prices.

- Normalized over a 50-period range to balance fluctuations between minimum and maximum values.

- Compared to prior-year values, with the number of bars dynamically adjusted based on the timeframe (e.g., 252 for 1D, 52 for 1W), to compute percentage changes.

The liquidity change is analyzed using a Chande Momentum Oscillator (CMO) (period: 24) to measure momentum trends. A Weighted Moving Average (WMA) (period: 10) acts as a signal line. The Bitcoin price is also plotted logarithmically to highlight parallels with liquidity cycles.

Usage

Traders can use the indicator to:

- Identify global liquidity cycles influencing Bitcoin price trends, such as expansive or restrictive monetary policies.

- Detect momentum phases: Values above 50 suggest overbought conditions, below -50 indicate oversold conditions.

- Anticipate trend reversals by observing CMO crossovers with the signal line.

It performs best on higher timeframes like daily (1D) or weekly (1W) charts. The visualization includes:

- CMO line (green > 50, red < -50, blue neutral), signal line (white), Bitcoin price (gray).

- Horizontal lines at 50, 0, and -50 for improved readability.

Originality

This indicator stands out from other momentum tools like RSI or basic price analysis due to:

- Unique Data Integration: Combines four central bank datasets, DXY, and CN10Y as macroeconomic proxies for Bitcoin.

- Dynamic Prior-Year Analysis: Calculates liquidity changes relative to historical values, adjustable by timeframe.

- Logarithmic Normalization: Enhances visibility of extreme values, critical for cryptocurrencies and macro data.

This combination offers a rare perspective on the interplay between global liquidity and Bitcoin, unavailable in other open-source scripts.

Settings

- CMO Period: Default 24, adjustable for faster/slower signals.

- Signal WMA: Default 10, for smoothing the CMO line.

- Normalization Window: Default 50 periods, customizable.

Users can modify these parameters in the Pine Editor to tailor the indicator to their strategy.

Note

This script is designed for medium- to long-term analysis, not scalping. For optimal results, combine it with additional analyses (e.g., on-chain data, support/resistance levels). It does not guarantee profits but supports informed decisions based on macroeconomic trends.

Data Sources

- Bitcoin: INDEX:BTCUSD

- Liquidity: ECONOMICS:USCBBS, FRED:JPNASSETS, ECONOMICS:CNCBBS, FRED:ECBASSETSW

- Additional: TVC:DXY, TVC:CN10Y

Higher Time Frame Fair Value Gap [ZeroHeroTrading]A fair value gap (FVG) highlights an imbalance area between market participants, and has become popular for technical analysis among price action traders.

A bullish (respectively bearish) fair value gap appears in a triple-candle pattern when there is a large candle whose previous candle’s high (respectively low) and subsequent candle’s low (respectively high) do not fully overlap the large candle. The space between these wicks is known as the fair value gap.

The following script aims at identifying higher timeframe FVG's within a lower timeframe chart. As such, it offers a unique perspective on the formation of FVG's by combining the multiple timeframe data points in the same context.

You can change the indicator settings as you see fit to achieve the best results for your use case.

Features

It draws higher timeframe bullish and bearish FVG's on the chart.

For bullish (respectively bearish) higher timeframe FVG's, it adds the buying (respectively selling) pressure as a percentage ratio of the up (respectively down) volume of the second higher timeframe bar out of the total up (respectively down) volume of the first two higher timeframe bars.

It adds a right extended trendline from the most recent lowest low (respectively highest high) to the top (respectively bottom) of the higher timeframe bullish (respectively bearish) FVG.

It detects and displays higher timeframe FVG's as early as one starts forming.

It detects and displays lower timeframe (i.e. chart's timeframe) FVG's upon confirmation.

It allows for skipping inside first bars when evaluating FVG's.

It allows for dismissing higher timeframe FVG's if there is no update for any period of the chart's timeframe. For instance, this can occur at lower timeframes during low trading activity periods such as extended hours.

Settings

Higher Time Frame FVG dropdown: Selects the higher timeframe to run the FVG detection on. Default is 15 minutes. It must be higher than, and a multiple of, the chart's timeframe.

Higher Time Frame FVG color select: Selects the color of the text to display for higher timeframe FVG's. Default is black.

Show Trend Line checkbox: Turns on/off trendline display. Default is on.

Show Lower Time Frame FVG checkbox: Turns on/off lower timeframe (i.e. chart's timeframe) FVG detection. Default is on.

Show Lower Time Frame FVG color select: Selects the color of the border for lower timeframe (i.e. chart's timeframe) FVG's. Default is white.

Include Inside Bars checkbox: Turns on/off the inclusion of inside first bars when evaluating FVG's. Default is on.

With Consistent Updates checkbox: Turns on/off consistent updates requirement. Default is on.

Enhanced Interval Candle with Breakout Detection and Detailed InThis indicator visualizes the last candle of a user-defined time interval (e.g., 1 hour, 4 hours, 1 day) on the current chart, providing enhanced details and breakout detection. It fetches the open, high, low, and close prices of the interval candle and draws a stylized representation of it, offset to the right of the current bar. The candle body and wicks are colored according to whether the interval candle closed bullishly (green) or bearishly (red). In addition to the candle itself, the indicator displays horizontal dotted lines representing the high, low, and midpoint of the interval candle, along with labels showing their exact values. These labels are dynamically updated as the interval candle changes. Furthermore, the script detects and visualizes breakouts of the interval candle's high or low. When the current price closes above the interval high, a green dashed line and a "Bullish Breakout" label are displayed. Conversely, when the current price closes below the interval low, a red dashed line and a "Bearish Breakout" label are shown. The breakout lines and labels are also dynamically updated. This indicator helps traders easily track the price action of a higher timeframe candle and spot potential breakouts based on that candle's range. The user can configure the time interval to suit their trading needs.

TradFi Fundamentals: Momentum Trading with Macroeconomic DataIntroduction

This indicator combines traditional price momentum with key macroeconomic data. By retrieving GDP, inflation, unemployment, and interest rates using security calls, the script automatically adapts to the latest economic data. The goal is to blend technical analysis with fundamental insights to generate a more robust momentum signal.

Original Research Paper by Mohit Apte, B. Tech Scholar, Department of Computer Science and Engineering, COEP Technological University, Pune, India

Link to paper

Explanation

Price Momentum Calculation:

The indicator computes price momentum as the percentage change in price over a configurable lookback period (default is 50 days). This raw momentum is then normalized using a rolling simple moving average and standard deviation over a defined period (default 200 days) to ensure comparability with the economic indicators.

Fetching and Normalizing Economic Data:

Instead of manually inputting economic values, the script uses TradingView’s security function to retrieve:

GDP from ticker "GDP"

Inflation (CPI) from ticker "USCCPI"

Unemployment rate from ticker "UNRATE"

Interest rates from ticker "USINTR"

Each series is normalized over a configurable normalization period (default 200 days) by subtracting its moving average and dividing by its standard deviation. This standardization converts each economic indicator into a z-score for direct integration into the momentum score.

Combined Momentum Score:

The normalized price momentum and economic indicators are each multiplied by user-defined weights (default: 50% price momentum, 20% GDP, and 10% each for inflation, unemployment, and interest rates). The weighted components are then summed to form a comprehensive momentum score. A horizontal zero line is plotted for reference.

Trading Signals:

Buy signals are generated when the combined momentum score crosses above zero, and sell signals occur when it crosses below zero. Visual markers are added to the chart to assist with trade timing, and alert conditions are provided for automated notifications.

Settings

Price Momentum Lookback: Defines the period (in days) used to compute the raw price momentum.

Normalization Period for Price Momentum: Sets the window over which the price momentum is normalized.

Normalization Period for Economic Data: Sets the window over which each macroeconomic series is normalized.

Weights: Adjust the influence of each component (price momentum, GDP, inflation, unemployment, and interest rate) on the overall momentum score.

Conclusion

This implementation leverages TradingView’s economic data feeds to integrate real-time macroeconomic data into a momentum trading strategy. By normalizing and weighting both technical and economic inputs, the indicator offers traders a more holistic view of market conditions. The enhanced momentum signal provides additional context to traditional momentum analysis, potentially leading to more informed trading decisions and improved risk management.

The next script I release will be an improved version of this that I have added my own flavor to, improving the signals.

Blockchain Fundamentals: Liquidity Cycle MomentumLiquidity Cycle Momentum Indicator

Overview:

This indicator analyzes global liquidity trends by calculating a unique Liquidity Index and measuring its year-over-year (YoY) percentage change. It then applies a momentum oscillator to the YoY change, providing insights into the cyclical momentum of liquidity. The indicator incorporates a limited historical data workaround to ensure accurate calculations even when the chart’s history is short.

Features Breakdown:

1. Limited Historical Data Workaround

Function: The limit(length) function adjusts the lookback period when there isn’t enough historical data (i.e., near the beginning of the chart), ensuring that calculations do not break due to insufficient data.

2. Global Liquidity Calculation

Data Sources:

TVC:CN10Y (10-year yield from China)

TVC:DXY (US Dollar Index)

ECONOMICS:USCBBS (US Central Bank Balance Sheet)

FRED:JPNASSETS (Japanese assets)

ECONOMICS:CNCBBS (Chinese Central Bank Balance Sheet)

FRED:ECBASSETSW (ECB assets)

Calculation Methodology:

A ratio is computed (cn10y / dxy) to adjust for currency influences.

The Liquidity Index is then derived by multiplying this ratio with the sum of the other liquidity components.

3. Year-over-Year (YoY) Percent Change

Computation:

The indicator determines the number of bars that approximately represent one year.

It then compares the current Liquidity Index to its value one year ago, calculating the YoY percentage change.

4. Momentum Oscillator on YoY Change

Oscillator Components:

1. Calculated using the Chande Momentum Oscillator (CMO) applied to the YoY percent change with a user-defined momentum length.

2. A weighted moving average (WMA) that smooths the momentum signal.

3. Overbought and Oversold zones

Signal Generation:

Buy Signal: Triggered when the momentum crosses upward from an oversold condition, suggesting a potential upward shift in liquidity momentum.

Sell Signal: Triggered when crosses below an overbought condition, indicating potential downward momentum.

State Management:

The indicator maintains a state variable to avoid repeated signals, ensuring that a new buy or sell signal is only generated when there’s a clear change in momentum.

5. Visual Presentation and Alerts

Plots:

The oscillator value and signalline are plotted for visual analysis.

Overbought and oversold levels are marked with dashed horizontal lines.

Signal Markers:

Buy and sell signals are marked with green and maroon circles, respectively.

Background Coloration:

Optionally, the chart’s background bars are colored (yellow for buy signals and fuchsia for sell signals) to enhance visual cues when signals are triggered.

Conclusion

In summary, the Liquidity Cycle Momentum Indicator provides a robust framework to analyze liquidity trends by combining global liquidity data, YoY changes, and momentum oscillation. This makes it an effective tool for traders and analysts looking to identify cyclical shifts in liquidity conditions and potential turning points in the market.