(2) Two AlertsCurrent Trading View free plan allows only ONE active alert.

This simple indicator Allows to trigger this ONE and ONLY alert when price reaches Higher, or Lower price level.

You can set levels and turn alerts for them on/off in settings, or by just drag-n-dropping Horizontal lines on the chart.

To set the only alert you need to create new alert, and change it's following parameters :

condition : 2alerts

Any alert function() call

Feel free to modify it on your needs.

Options

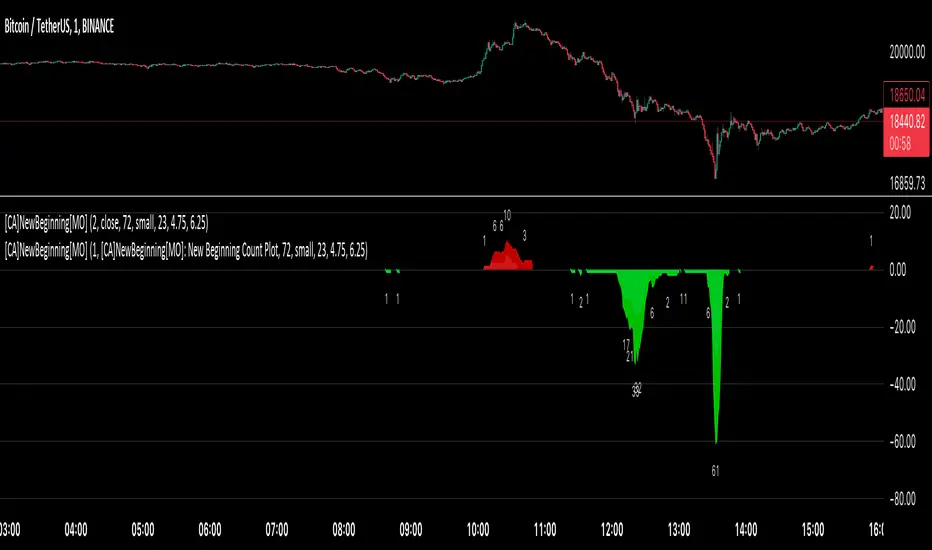

[ChasinAlts] A New Beginning[MO]Hello Tradeurs, firstly let me say this… Please do not think that this dump is over (so I want to gift you one of the best gifts I CAN gift you at the PERFECT TIME...which is now) but I believe it to be the final one before a New Beginning is upon us. I hope that anybody that sees this within the next day or so listens to me when I tell you this… Follow the instructions below, IF ANYTHING, just to set the alert to be notify you so you can see why I’m about to tell you everything that I’m about to tell you. That being that this indicator is pure magic…..BUT you must stay in your lane when using it (ie. ultimately, understand its use case) and most importantly, how many people you expose it to. The good thing about it is it produces very few alerts. In fact, it was built SOLELY to find the very tips of MAJOR dumps/pumps (with its current default settings). I honestly cannot remember where I acquired the code so if anyone recognizes it please direct me to the source so I can give a shoutout. In the past it has been so astonishingly accurate that I didn’t want to publish it but I've just been...in the mood I suppose recently.

Now…it is SPECIFICALLY meant for the 1min TF. I’ll say it again… It is meant for ONE MINUTE CHARTS…it was built for 1min charts, it will only work as well as I’m describing to you on the…you guessed it…ONE MINUTE CHART (again, with the default settings how they are, that is). If any of you use it for this present dump (November 8, 2022) and want to thank me for it or speak very highly about it or give it a bunch of likes… DO NOT!!! I will reword this so you fully comprehend my urgency on this matter. I do not want this indicator getting out for every Joe Schmoe (or stupid YouTuber) to use and spread because the manipulators will see to it that it will no longer work. Things that will happen that will cause it to gain the popularity that I do not want it to have are the following:

1) You "like" the indicator in TradingView to show appreciation/that your using it so that it will show up in your indicators list (to get past this you need to select all of the text of the script on the indicator's page and copy and paste it into the “Pine Editor”. Then select "save" and name it as you wish. Now, it is in your indicator list under the name that you saved it as.

2) You *favorite* the indicator in TradingView

3) You leave comments in the comments section on the indicators page in TradingView (I really do love hearing comments about anything regarding my indicators(positive or negative..though I haven't gotten any negative yet SO BRING IT ON), even though I don’t get too many of them, so if you are grateful (or hateful) PLEASE message me privately (and really I truly truly do appreciate getting comments/messages so if it has benefited you make sure to message me as I might have more for those that do express their gratitude) and tell me anything that you want to tell me or ask me anything that you wanna ask me there).

One major thing that will help to suppress its popularity will be that if anybody goes back on historical charts to see its accuracy they most likely will not be able to go far back enough on the 1min TF to be able to Witness its efficacy so I'm banking on that helping to keep a lid on things.

The settings used (as well as the TF used) really should not be changed if using it for its intended purpose. On little dumps that last for a few hours os so will produce points somewhere in the 40 to 60 range at the dumps/pumps peak. Each coin is worth one point and there are 40 coins per set and 2 sets (that you will have to link together) and when the under the hood indicator is triggered for that coin it will add a point to the score. With the settings how they are and on the 1min TF(if I hadn't mentioned it yet. lol) a good point alert threshold to use to catch the apex of heavy pumps/dumps would be between 70 to 80 points(80 is max). Ultimately is the users choice to input the alert threshold of points in the indicators settings(default is 72). If you’re trying to nail the very bottom of a hard pump/dump, DO NOT fall for times where it peaks at 50 to 60. You’re looking for 70 or above.

*** This is the most important thing to do as you will not receive an alert if you do not do this correctly. You have to add the indicator two times to the chart. One of the indicators needs to be under “Coin Set 1“ and the other under “Coin Set 2“. Now, in “Set 1“ you need to go to the setting entitled “Select New Beginning Count Plot from drop-down“ and you need to open the drop-down and select the plot entitled “A New Beginning Count Plot”. This will link both the indicators and since there are 40 coins per iteration of the script, when you link them it could give you a max of 80 points total at the very peak of a very strong dump...which will obviously be rare. You CAN use only one copy of the script (but need to change the alert setting to a MAX of 40) but in my experience it's best to use both of them and to link them. It gives you a more well-rounded outcome. Good luck my people and always remember...Much love...Much Love. May the force be with your trades. -ChasinAlts out.

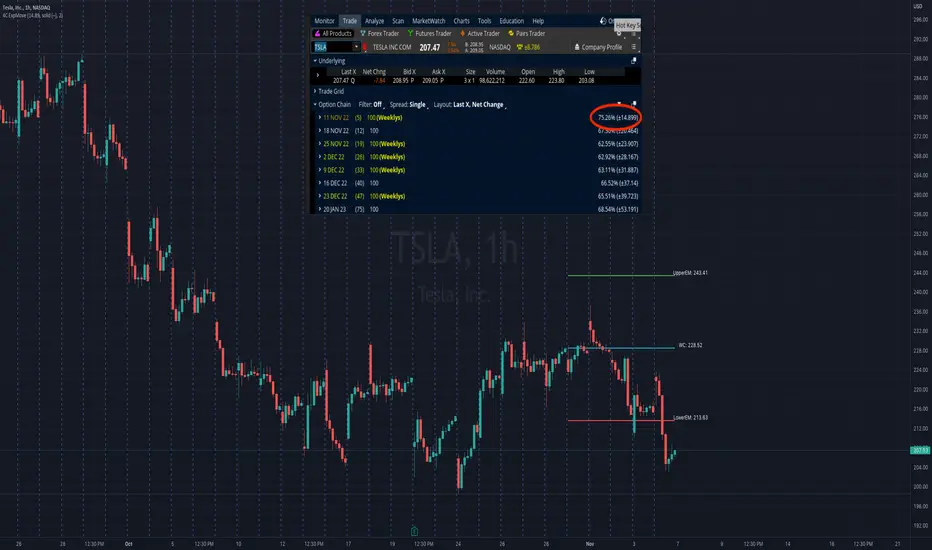

4C Expected Move (Weekly Options)This indicator plots the Expected Move (EM) calculated from weekly options pricing, for a quick visual reference.

The EM is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of implied volatility.

This range can be viewed as support and resistance, or once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

The EM range is based on the Weekly close of the prior week.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Look at the stock's option chain and find the weekly expected move. You will have to do your own research to find where this information is displayed depending on your broker.

See screenshot example on the chart. This is the Thinkorswim platform's option chain, and the Implied Volatility % and the calculated EM is circled in red. Use the +- number in parentheses, NOT the % value.

Input that number into the indicator on a weekly basis, ideally on the weekend sometime after the cash market close on Friday, and before the Market open at the beginning of the trading week.

The indicator must be manually updated each week.

It will automatically start over at the beginning of the week.

RedK Magic Ribbon JeetendraGaurCross Over Strategy

Moving average Cross Over Strategy

Please use in 1 minute Expiry

Moving Averages SelectionHello everyone, I present my first script. In it I collect a group of fully configurable moving averages, both in color, value and selection of the ones we want to observe.

The moving averages I collect are 3 of each of the following types:

EMA: An exponential moving average ( EMA ) is a type of moving average (MA) that places a greater weight and significance on the most recent data points.

SMA: It is simply the average price over the specified period. The average is called "moving" because it is plotted on the chart bar by bar, forming a line that moves along the chart as the average value changes.

HMA: The Hull Moving Average ( HMA ) attempts to minimize the lag of a traditional moving average while retaining the smoothness of the moving average line. Developed by Alan Hull in 2005, this indicator makes use of weighted moving averages to prioritize more recent values and greatly reduce lag.

RMA: The Rolling Moving Average, sometimes referred to as "Smoothed Moving Average", gives the recent prices most weighting, though the historic prices are also weighted, each given less weighting further back in time.

WMA: The weighted moving average ( WMA ) is a technical indicator that traders use to generate trade direction and make a buy or sell decision. It assigns greater weighting to recent data points and less weighting on past data points.

I am open to any opinion and advice for improvement, greetings, I hope you find it useful :)

LazyScalp BoardThis indicator allows you to quickly view all important parameters in the table.

The table consists of a daily volume indicator, an average volume for a certain period, a volatility indicator (normalized ATR) and a correlation coefficient.

All parameters can be flexibly customized. You can also customize the table display, styles, and more.

This indicator is primarily useful for intraday traders and scalpers to quickly select an instrument to trade.

Higher Time Frame Average True RangesPurpose: This script will help an options trader asses risk and determine good entry and exit strategies

Background Information: The true range is the greatest of: current high minus the current low; the absolute value of the current high minus the previous close; and the absolute value of the current low minus the previous close. The Average True Range (ATR) is a 14-day moving average of the true range. Traders use the ATR indicator to assess volatility in stocks and decide when to enter and exit trades. It is important to note the limitations of using True Range and ATR: These indications cannot tell you the direction of your options trade (call vs. put) and they cannot tell you whether a particular trend is about to reverse. However, it can be used to assess if volatility has peaked for a particular direction and time period.

How this script works: This indicator calculates true range for the daily (DTR), weekly (WTR), and monthly (MTR) time frames and compares it to the Average True Range (ATR) for each of those time frames (DATR, WATR, and MATR). The comparison is displayed into a colored table in the upper right-hand corner of the screen. When a daily, weekly, or monthly true range reaches 80% of its respective ATR, the row for that time frame will turn Orange indicating medium risk for staying in the trade. If the true range goes above 100% of the respective ATR, then the row will turn Red indicating high risk for staying in the trade. When the row for a time period turns red, volatility for the time period has likely peaked and traders should heavily consider taking profits. It is important to note these calculations start at different times for each time frame: Daily (Today’s Open), Weekly (Monday’s Open), Monthly (First of the Month’s Open). This means if it’s the 15th of the month then the Monthly True Range is being calculated for the trading days in the first half of the month (approximately 10 trade days).

The script also plots three sets of horizontal dotted lines to visually represent the ATR for each time period. Each set is generated by adding and subtracting the daily, weekly, and monthly ATRs from that time periods open price. For example, the weekly ATR is added and subtracted from Mondays open price to visually represent the true range for that week. The DATR is represented by red lines, the WATR is represented by the green lines, and the MATR is represented by the blue lines. These plots could also be used to assess risk as well.

How to use this script: Use the table to assess risk and determine potential exit strategies (Green=Low Risk, Orange=Medium Risk, Red=High Risk. Use the dotted lines to speculate what a stock’s price could be in a given time period (Daily=Red, Weekly=Green, and Monthly=Blue). And don’t forget the true range’s calculation and plots starts at the beginning of each time period!

Reset Strike Options-Type 2 (Gray Whaley) [Loxx]For a reset option type 2, the strike is reset in a similar way as a reset option 1. That is, the strike is reset to the asset price at a predetermined future time, if the asset price is below (above) the initial strike price for a call (put). The payoff for such a reset call is max(S - X, 0), and max(X - S, 0) for a put, where X is equal to the original strike X if not reset, and equal to the reset strike if reset. Gray and Whaley (1999) have derived a closed-form solution for the price of European reset strike options. The price of the call option is then given by (via "The Complete Guide to Option Pricing Formulas")

c = Se^(b-r)T2 * M(a1, y1; p) - Xe^(-rT2) * M(a2, y2; p) - Se^(b-r)T1 * N(-a1) * N(z2) * e^-r(T2-T1) + Se^(b-r)T2 * N(-a1) * N(z1)

p = Se^(b-r)T1 * N(a1) * N(-z2) * e^-r(T2-T1) + Se^(b-r)T2 * N(a1) * N(-z1) + Xe^(-rT2) * M(-a2, -y2; p) - Se^(b-r)T2 * M(-a1, -y1; p)

where b is the cost-of-carry of the underlying asset, a is the volatility of the relative price changes in the asset, and r is the risk-free interest rate. K is the strike price of the option, T1 the time to reset (in years), and T2 is its time to expiration. N(x) and M(a,b; p) are, respectively, the univariate and bivariate cumulative normal distribution functions. Further

a1 = (log(S/X) + (b+v^2/2)T1) / v*T1^0.5 ... a2 = a1 - v*T1^0.5

z1 = ((b+v^2/2)(T2-T1)) / v*(T2-T1)^0.5 ... z2 = z1 - v*(T2-T1)^0.5

y1 = (log(S/X) + (b+v^2/2)T1) / v*T1^0.5 ... y2 = a1 - v*T1^0.5

and p = (T1/T2)^0.5. For reset options with multiple reset rights, see Dai, Kwok, and Wu (2003) and Liao and Wang (2003).

Inputs

Asset price ( S )

Strike price ( K )

Reset time ( T1 )

Time to maturity ( T2 )

Risk-free rate ( r )

Cost of carry ( b )

Volatility ( s )

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Numerical Greeks Outputs

Delta D

Elasticity L

Gamma G

DGammaDvol

GammaP G

Vega

DvegaDvol

VegaP

Theta Q (1 day)

Rho r

Rho futures option r

Phi/Rho2

Carry

DDeltaDvol

Speed

Strike Delta

Strike gamma

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Writer Extendible Option [Loxx]These options can be exercised at their initial maturity date /I but are extended to T2 if the option is out-of-the-money at ti. The payoff from a writer-extendible call option at time T1 (T1 < T2) is (via "The Complete Guide to Option Pricing Formulas")

c(S, X1, X2, t1, T2) = (S - X1) if S>= X1 else cBSM(S, X2, T2-T1)

and for a writer-extendible put is

c(S, X1, X2, T1, T2) = (X1 - S) if S< X1 else pBSM(S, X2, T2-T1)

Writer-Extendible Call

c = cBSM(S, X1, T1) + Se^(b-r)T2 * M(Z1, -Z2; -p) - X2e^-rT2 * M(Z1 - vT^0.5, -Z2 + vT^0.5; -p)

Writer-Extendible Put

p = cBSM(S, X1, T1) + X2e^-rT2 * M(-Z1 + vT^0.5, Z2 - vT^0.5; -p) - Se^(b-r)T2 * M(-Z1, Z2; -p)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

Asset price ( S )

Initial strike price ( X1 )

Extended strike price ( X2 )

Initial time to maturity ( t1 )

Extended time to maturity ( T2 )

Risk-free rate ( r )

Cost of carry ( b )

Volatility ( s )

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Numerical Greeks Output

Delta

Elasticity

Gamma

DGammaDvol

GammaP

Vega

DvegaDvol

VegaP

Theta (1 day)

Rho

Rho futures option

Phi/Rho2

Carry

DDeltaDvol

Speed

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Reset Strike Options-Type 1 [Loxx]In a reset call (put) option, the strike is reset to the asset price at a predetermined future time, if the asset price is below (above) the initial strike price. This makes the strike path-dependent. The payoff for a call at maturity is equal to max((S-X)/X, 0) where is equal to the original strike X if not reset, and equal to the reset strike if reset. Similarly, for a put, the payoff is max((X-S)/X, 0) Gray and Whaley (1997) x have derived a closed-form solution for such an option. For a call, we have

c = e^(b-r)(T2-T1) * N(-a2) * N(z1) * e^(-rt1) - e^(-rT2) * N(-a2)*N(z2) - e^(-rT2) * M(a2, y2; p) + (S/X) * e^(b-r)T2 * M(a1, y1; p)

and for a put,

p = e^(-rT2) * N(a2) * N(-z2) - e^(b-r)(T2-T1) * N(a2) * N(-z1) * e^(-rT1) + e^(-rT2) * M(-a2, -y2; p) - (S/X) * e^(b-r)T2 * M(-a1, -y1; p)

where b is the cost-of-carry of the underlying asset, a is the volatil- ity of the relative price changes in the asset, and r is the risk-free interest rate. X is the strike price of the option, r the time to reset (in years), and T is its time to expiration. N(x) and M(a, b; p) are, respec- tively, the univariate and bivariate cumulative normal distribution functions. The remaining parameters are p = (T1/T2)^0.5 and

a1 = (log(S/X) + (b+v^2/2)T1) / vT1^0.5 ... a2 = a1 - vT1^0.5

z1 = (b+v^2/2)(T2-T1)/v(T2-T1)^0.5 ... z2 = z1 - v(T2-T1)^0.5

y1 = log(S/X) + (b+v^2)T2 / vT2^0.5 ... y2 = y1 - vT2^0.5

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

Asset price ( S )

Initial strike price ( X1 )

Extended strike price ( X2 )

Initial time to maturity ( t1 )

Extended time to maturity ( T2 )

Risk-free rate ( r )

Cost of carry ( b )

Volatility ( s )

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Numerical Greeks Ouput

Delta

Elasticity

Gamma

DGammaDvol

GammaP

Vega

DvegaDvol

VegaP

Theta (1 day)

Rho

Rho futures option

Phi/Rho2

Carry

DDeltaDvol

Speed

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Fade-in Options [Loxx]A fade-in call has the same payoff as a standard call except the size of the payoff is weighted by how many fixings the asset price were inside a predefined range (L, U). If the asset price is inside the range for every fixing, the payoff will be identical to a plain vanilla option. More precisely, for a call option, the payoff will be max(S(T) - X, 0) X 1/n Sum(n(i)), where n is the total number of fixings and n(i) = 1 if at fixing i the asset price is inside the range, and n(i) = 0 otherwise. Similarly, for a put, the payoff is max(X - S(T), 0) X 1/n Sum(n(i)).

Brockhaus, Ferraris, Gallus, Long, Martin, and Overhaus (1999) describe a closed-form formula for fade-in options. For a call the value is given by

max(X - S(T), 0) X 1/n Sum(n(i))

describe a closed-form formula for fade-in options. For a call the value is given by

c = 1/n * Sum(S^((b-r)*T) * (M(-d5, d1; -p) - M(-d3, d1; -p)) - Xe^(-rT) * (M(-d6, d2; -p) - M(-d4, d2; -p))

where n is the number of fixings, p = (t1^0.5/T^0.5), t1 = iT/n

d1 = (log(S/X) + (b + v^2/2)*T) / (v * T^0.5) ... d2 = d1 - v*T^0.5

d3 = (log(S/L) + (b + v^2/2)*t1) / (v * t1^0.5) ... d4 = d3 - v*t1^0.5

d5 = (log(S/U) + (b + v^2/2)*t1) / (v * t1^0.5) ... d6 = d5 - v*t1^0.5

The value of a put is similarly

p = 1/n * Sum(Xe^(-rT) * (M(-d6, -d2; -p) - M(-d4, -d2; -p))) - S^((b-r)*T) * (M(-d5, -d1; -p) - M(-d3, -d1; -p)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

Asset price ( S )

Strike price ( K )

Lower barrier ( L )

Upper barrier ( U )

Time to maturity ( T )

Risk-free rate ( r )

Cost of carry ( b )

Volatility ( s )

Fixings ( n )

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

cbnd3() = Cumulative Bivariate Distribution

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Log Contract Ln(S/X) [Loxx]A log contract, first introduced by Neuberger (1994) and Neuberger (1996), is not strictly an option. It is, however, an important building block in volatility derivatives (see Chapter 6 as well as Demeterfi, Derman, Kamal, and Zou, 1999). The payoff from a log contract at maturity T is simply the natural logarithm of the underlying asset divided by the strike price, ln(S/ X). The payoff is thus nonlinear and has many similarities with options. The value of this contract is (via "The Complete Guide to Option Pricing Formulas")

L = e^(-r * T) * (log(S/X) + (b-v^2/2)*T)

The delta of a log contract is

delta = (e^(-r*T) / S)

and the gamma is

gamma = (e^(-r*T) / S^2)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Log Option [Loxx]A log option introduced by Wilmott (2000) has a payoff at maturity equal to max(log(S/X), 0), which is basically an option on the rate of return on the underlying asset with strike log(X). The value of a log option is given by: (via "The Complete Guide to Option Pricing Formulas")

e^−rT * n(d2)σ√(T − t) + e^−rT*(log(S/K) + (b −σ^2/2)T) * N(d2)

where N(*) is the cumulative normal distribution function, n(*) is the normal density function, and

d = ((log(S/X) + (b - v^2/2)*T) / (v*T^0.5)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Log Contract Ln(S) [Loxx]A log contract, first introduced by Neuberger (1994) and Neuberger (1996), is not strictly an option. It is, however, an important building block in volatility derivatives (see Chapter 6 as well as Demeterfi, Derman, Kamal, and Zou, 1999). The payoff from a log contract at maturity T is simply the natural logarithm of the underlying asset divided by the strike price, ln(S/ X). The payoff is thus nonlinear and has many similarities with options. The value of this contract is (via "The Complete Guide to Option Pricing Formulas")

L = e^(-r * T) * (log(S/X) + (b-v^2/2)*T)

The delta of a log contract is

delta = (e^(-r*T) / S)

and the gamma is

gamma = (e^(-r*T) / S^2)

An even simpler version of the log contract is when the payoff simply is ln(S). The payoff is clearly still nonlinear in the underlying asset. It follows that the value of this contract is:

L = e^(-r * T) * (log(S) + (b-v^2/2)*T)

The theta/time decay of a log contract is

theta = - 1/T * v^2

and its exposure to the stock price, delta, is

delta = - 2/T * 1/S

This basically tells you that you need to be long stocks to be delta- neutral at any time. Moreover, the gamma is

gamma = 2 / (T * S^2)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = volatility of the underlying asset price

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Powered Option [Loxx]At maturity, a powered call option pays off max(S - X, 0)^i and a put pays off max(X - S, 0)^i . Esser (2003 describes how to value these options (see also Jarrow and Turnbull, 1996, Brockhaus, Ferraris, Gallus, Long, Martin, and Overhaus, 1999). (via "The Complete Guide to Option Pricing Formulas")

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = volatility of the underlying asset price

i = power

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

combin(x) = Combination function, calculates the number of possible combinations for two given numbers

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Capped Standard Power Option [Loxx]Power options can lead to very high leverage and thus entail potentially very large losses for short positions in these options. It is therefore common to cap the payoff. The maximum payoff is set to some predefined level C. The payoff at maturity for a capped power call is min . Esser (2003) gives the closed-form solution: (via "The Complete Guide to Option Pricing Formulas")

c = S^i * (e^((i - 1) * (r + i*v^2 / 2) - i * (r - b))*T) * (N(e1) - N(e3)) - e^(-r*T) * (X*N(e2) - (C + X) * N(e4))

while the value of a put is

e1 = (log(S/X^(1/i)) + (b + (i - 1/2)*v^2)*T) / v*T^0.5

e3 = (log(S/(C + X)^(1/i)) + (b + (i - 1/2)*v^2)*T) / v*T^0.5

e4 = e3 - i * v * T^0.5

In the case of a capped power put, we have

p = e^(-r*T) * (X*N(-e2) - (C + X) * N(-e4)) - S^i * (e^((i - 1) * (r + i*v^2 / 2) - i * (r - b))*T) * (N(-e1) - N(-e3))

where e1 and e2 is as before. e3 and e4 has to be changed to

e3 = (log(S/(X - C)^(1/i)) + (b + (i - 1/2)*v^2)*T) / v*T^0.5

e4 = e3 - i * v * T^0.5

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

i = power

c = Capped on pay off

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Standard Power Option [Loxx]Standard power options (aka asymmetric power options) have nonlinear payoff at maturity. For a call, the payoff is max(S^i - X, 0), and for a put, it is max(X - S^i , 0), where i is some power (i > 0). The value of this power call is given by (see Heynen and Kat, 1996c; Zhang, 1998; and Esser, 2003). (via "The Complete Guide to Option Pricing Formulas")

c = S^i * (e^((i - 1) * (r + i*v^2 / 2) - i * (r - b))*T) * N(d1) - X*e^(-r*T) * N(d2)

while the value of a put is

p = X*e^(-r*T) * N(-d2) - S^i * (e^((i - 1) * (r + i*v^2 / 2) - i * (r - b))*T) * N(-d1)

where

d1 = (log(S/X^(1/i)) + (b + (i - 1/2)*v^2)*T) / v*T^0.5

d2 = d1 - i * v * T^0.5

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

pwr = power

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Power Contract [Loxx]There are two main categories of power options. Standard power options' payoff depends on the price of the underlying asset raised to some power. For powered options, the "standard" payoff (stock price in excess of the exercise price) is raised to some power.

A power contract is a simple derivative instrument paying (S/ X)^i at maturity, where i is some fixed power. The value of such a power contract is given by Shaw (1998) as: (via "The Complete Guide to Option Pricing Formulas")

VPower = (S/X)^i * e^((b-v^2)/2)*i - r + i^2 * v^2/2)*T

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

lambda = Jump rate per year

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Moneyness Options [Loxx]A moneyness option is basically a plain vanilla option where the strike is set to a percentage of the future/forward price. For example, a 120% moneyness call would have a strike equal to 120% of the forward price. A 120% moneyness put would have a spot equal to 120% of the strike. The value of this option is given in percent of the forward. The value of a moneyness call or put is thus given by: (via "The Complete Guide to Option Pricing Formulas")

c = p = c^-rT * (N(d1) - LN(d2))

where L = X/F for a call and L = F/X for a put, and

d1 = (-log(L) + v^2*T/2) / (v*T^0.5)

d2 = d1 - (v*T^0.5)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

lambda = Jump rate per year

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Forward Start Options [Loxx]A forward start option with time to maturity T starts at-the-money or proportionally in- or out-of-the-money after a known elapsed time t in the future. The strike is set equal to a positive constant a times the asset price S after the known time t. If a is less than unity, the call (put) will start 1 - a percent in-the-money (out-of-the- money); if a is unity, the option will start at-the-money; and if a is larger than unity, the call (put) will start a - 1 percentage out-of-the- money (in-the-money).A forward start option can be priced using the Rubinstein (1990) formula: (via "The Complete Guide to Option Pricing Formulas")

c = S*e^(b-r)t * (e^(b-r)(T-t) * N(d1)) - alpha * e^-r(T-t) * N(d2))

p = S*e^(b-r)t * (alpha*e^r(T-t) * N(-d2)) - e^-(b-r)(T-t) * N(-d1))

where

d1 = (log(1/alpha) + (b + v^2/2)(T-1))/v*(T-t)^0.5

d2 = d1 - v*(T-t)^0.5

Application

Employee options are often of the forward starting type. Ratchet options (aka cliquet options) consist of a series of forward starting options.

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

a = Alpha

T1 = Time to forward start

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

v = volatility of the underlying asset price

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Executive Stock Options [Loxx]The Jennergren and Naslund (1993) formula takes into account that an employee or executive often loses her options if she has to leave the company before the option's expiration: (via "The Complete Guide to Option Pricing Formulas")

c = e^(-lambda*T) * (Se^((b-r)T) * N(d1) - Xe^-rT * N(d2))

p = e^(-lambda*T) * (Xe^(-rT) * N(-d2) - Se^(b-r)T * N(-d1))

where

d1 = (log(S/X) + (b + v^2/2)T) / vT^0.5

d2 = d1 - vT^0.5

lambda is the jump rate per year. The value of the executive option equals the ordinary Black-Scholes option price multiplied by the probability e —AT that the executive will stay with the firm until the option expires.

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

lambda = Jump rate per year

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Variable Purchase Options [Loxx]Handley (2001) describes how to value variable purchase options (VPO). A VPO is basically a call option, but where the number of underlying shares is stochastic rather than fixed, or more precisely, a deterministic function of the asset price. The strike price of a VPO is typically a fixed discount to the underlying share price at maturity. The payoff at maturity is equal to max , where N is the number of shares. VPOs may be an interesting tool for firms that need to raise capital relatively far into the future at a given time. The number of underlying shares N is decided on at maturity and is equal to

N = X / St(1 -D)

where X is the strike price, ST is the asset price at maturity, and D is the fixed discount expressed as a proportion 0 > D < 1. The number of shares is in this way a deterministic function of the asset price. Further, the number of shares is often subjected to a minimum and maximum. In this case, we will limit the minimum number of shares to Nmin = X / U(1 -D) if, the asset price at maturity is above a predefined level U at maturity. Similarly, we will reach the maximum number of shares A T = x if the stock price at maturity is equal Nmax = X / L(1 -D) or lower than a predefined level L. Based on Handley (2001), we get the following closed-form solution: (via "The Complete Guide to Option Pricing Formulas")

c = XD / 1-D e^-rT + Nmin(Se^(b-r)T * N(d1) - Ue^-rT * N(d2))

- Nmax(Le^-rT * N(-d4) - Se^(b-r)T * N(-d3))

+ Nmax(L(1-D)e^-rT * N(-d6) - Se^(b-r)T * N(-d5))

where

d1 = (log(S/U) + (b+v^2/2)T) / vT^0.5 ... d2 = d1 - vT^0.5

d3 = (log(S/L) + (b+v^2/2)T) / vT^0.5 ... d4 = d3 - vT^0.5

d5 = (log(S/L(1-D)) + (b+v^2/2)T) / vT^0.5 ... d6 = d5 - vT^0.5

Inputs

Asset price (S)

Strike price (K)

Discount %

Lower bound

Upper bound

Time to maturity

Risk-free rate (r) %

Cost of carry (b) %

Volatility (v) %

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen