Fibonacci ATR Fusion - Strategy [presentTrading]Open-script again! This time is also an ATR-related strategy. Enjoy! :)

If you have any questions, let me know, and I'll help make this as effective as possible.

█ Introduction and How It Is Different

The Fibonacci ATR Fusion Strategy is an advanced trading approach that uniquely integrates Fibonacci-based weighted averages with the Average True Range (ATR) to identify and capitalize on significant market trends.

Unlike traditional strategies that rely on single indicators or static parameters, this method combines multiple timeframes and dynamic volatility measurements to enhance precision and adaptability. Additionally, it features a 4-step Take Profit (TP) mechanism, allowing for systematic profit-taking at various levels, which optimizes both risk management and return potential in long and short market positions.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The Fibonacci ATR Fusion Strategy utilizes a combination of technical indicators and weighted averages to determine optimal entry and exit points. Below is a breakdown of its key components and operational logic.

🔶 1. Enhanced True Range Calculation

The strategy begins by calculating the True Range (TR) to measure market volatility accurately.

TR = max(High - Low, abs(High - Previous Close), abs(Low - Previous Close))

High and Low: Highest and lowest prices of the current trading period.

Previous Close: Closing price of the preceding trading period.

max: Selects the largest value among the three calculations to account for gaps and limit movements.

🔶 2. Buying Pressure (BP) Calculation

Buying Pressure (BP) quantifies the extent to which buyers are driving the price upwards within a period.

BP = Close - True Low

Close: Current period's closing price.

True Low: The lower boundary determined in the True Range calculation.

🔶 3. Ratio Calculation for Different Periods

To assess the strength of buying pressure relative to volatility, the strategy calculates a ratio over various Fibonacci-based timeframes.

Ratio = 100 * (Sum of BP over n periods) / (Sum of TR over n periods)

n: Length of the period (e.g., 8, 13, 21, 34, 55).

Sum of BP: Cumulative Buying Pressure over n periods.

Sum of TR: Cumulative True Range over n periods.

This ratio normalizes buying pressure, making it comparable across different timeframes.

🔶 4. Weighted Average Calculation

The strategy employs a weighted average of ratios from multiple Fibonacci-based periods to smooth out signals and enhance trend detection.

Weighted Avg = (w1 * Ratio_p1 + w2 * Ratio_p2 + w3 * Ratio_p3 + w4 * Ratio_p4 + Ratio_p5) / (w1 + w2 + w3 + w4 + 1)

w1, w2, w3, w4: Weights assigned to each ratio period.

Ratio_p1 to Ratio_p5: Ratios calculated for periods p1 to p5 (e.g., 8, 13, 21, 34, 55).

This weighted approach emphasizes shorter periods more heavily, capturing recent market dynamics while still considering longer-term trends.

🔶 5. Simple Moving Average (SMA) of Weighted Average

To further smooth the weighted average and reduce noise, a Simple Moving Average (SMA) is applied.

Weighted Avg SMA = SMA(Weighted Avg, m)

- m: SMA period (e.g., 3).

This smoothed line serves as the primary signal generator for trade entries and exits.

🔶 6. Trading Condition Thresholds

The strategy defines specific threshold values to determine optimal entry and exit points based on crossovers and crossunders of the SMA.

Long Condition = Crossover(Weighted Avg SMA, Long Entry Threshold)

Short Condition = Crossunder(Weighted Avg SMA, Short Entry Threshold)

Long Exit = Crossunder(Weighted Avg SMA, Long Exit Threshold)

Short Exit = Crossover(Weighted Avg SMA, Short Exit Threshold)

Long Entry Threshold (T_LE): Level at which a long position is triggered.

Short Entry Threshold (T_SE): Level at which a short position is triggered.

Long Exit Threshold (T_LX): Level at which a long position is exited.

Short Exit Threshold (T_SX): Level at which a short position is exited.

These conditions ensure that trades are only executed when clear trends are identified, enhancing the strategy's reliability.

Previous local performance

🔶 7. ATR-Based Take Profit Mechanism

When enabled, the strategy employs a 4-step Take Profit system to systematically secure profits as the trade moves in the desired direction.

TP Price_1 Long = Entry Price + (TP1ATR * ATR Value)

TP Price_2 Long = Entry Price + (TP2ATR * ATR Value)

TP Price_3 Long = Entry Price + (TP3ATR * ATR Value)

TP Price_1 Short = Entry Price - (TP1ATR * ATR Value)

TP Price_2 Short = Entry Price - (TP2ATR * ATR Value)

TP Price_3 Short = Entry Price - (TP3ATR * ATR Value)

- ATR Value: Calculated using ATR over a specified period (e.g., 14).

- TPxATR: User-defined multipliers for each take profit level.

- TPx_percent: Percentage of the position to exit at each TP level.

This multi-tiered exit strategy allows for partial position closures, optimizing profit capture while maintaining exposure to potential further gains.

█ Trade Direction

The Fibonacci ATR Fusion Strategy is designed to operate in both long and short market conditions, providing flexibility to traders in varying market environments.

Long Trades: Initiated when the SMA of the weighted average crosses above the Long Entry Threshold (T_LE), indicating strong upward momentum.

Short Trades: Initiated when the SMA of the weighted average crosses below the Short Entry Threshold (T_SE), signaling robust downward momentum.

Additionally, the strategy can be configured to trade exclusively in one direction—Long, Short, or Both—based on the trader’s preference and market analysis.

█ Usage

Implementing the Fibonacci ATR Fusion Strategy involves several steps to ensure it aligns with your trading objectives and market conditions.

1. Configure Strategy Parameters:

- Trading Direction: Choose between Long, Short, or Both based on your market outlook.

- Trading Condition Thresholds: Set the Long Entry, Short Entry, Long Exit, and Short Exit thresholds to define when to enter and exit trades.

2. Set Take Profit Levels (if enabled):

- ATR Multipliers: Define how many ATRs away from the entry price each take profit level is set.

- Take Profit Percentages: Allocate what percentage of the position to close at each TP level.

3. Apply to Desired Chart:

- Add the strategy to the chart of the asset you wish to trade.

- Observe the plotted Fibonacci ATR and SMA Fibonacci ATR indicators for visual confirmation.

4. Monitor and Adjust:

- Regularly review the strategy’s performance through backtesting.

- Adjust the input parameters based on historical performance and changing market dynamics.

5. Risk Management:

- Ensure that the sum of take profit percentages does not exceed 100% to avoid over-closing positions.

- Utilize the ATR-based TP levels to adapt to varying market volatilities, maintaining a balanced risk-reward ratio.

█ Default Settings

Understanding the default settings is crucial for optimizing the Fibonacci ATR Fusion Strategy's performance. Here's a precise and simple overview of the key parameters and their effects:

🔶 Key Parameters and Their Effects

1. Trading Direction (`tradingDirection`)

- Default: Both

- Effect: Determines whether the strategy takes both long and short positions or restricts to one direction. Selecting Both allows maximum flexibility, while Long or Short can be used for directional bias.

2. Trading Condition Thresholds

Long Entry (long_entry_threshold = 58.0): Higher values reduce false positives but may miss trades.

Short Entry (short_entry_threshold = 42.0): Lower values capture early short trends but may increase false signals.

Long Exit (long_exit_threshold = 42.0): Exits long positions early, securing profits but potentially cutting trends short.

Short Exit (short_exit_threshold = 58.0): Delays short exits to capture favorable movements, avoiding premature exits.

3. Take Profit Configuration (`useTakeProfit` = false)

- Effect: When enabled, the strategy employs a 4-step TP mechanism to secure profits at multiple levels. By default, it is disabled to allow users to opt-in based on their trading style.

4. ATR-Based Take Profit Multipliers

TP1 (tp1ATR = 3.0): Sets the first TP at 3 ATRs for initial profit capture.

TP2 (tp2ATR = 8.0): Targets larger trends, though less likely to be reached.

TP3 (tp3ATR = 14.0): Optimizes for extreme price moves, seldom triggered.

5. Take Profit Percentages

TP Level 1 (tp1_percent = 12%): Secures 12% at the first TP.

TP Level 2 (tp2_percent = 12%): Exits another 12% at the second TP.

TP Level 3 (tp3_percent = 12%): Closes an additional 12% at the third TP.

6. Weighted Average Parameters

Ratio Periods: Fibonacci-based intervals (8, 13, 21, 34, 55) balance responsiveness.

Weights: Emphasizes recent data for timely responses to market trends.

SMA Period (weighted_avg_sma_period = 3): Smoothens data with minimal lag, balancing noise reduction and responsiveness.

7. ATR Period (`atrPeriod` = 14)

Effect: Sets the ATR calculation length, impacting TP sensitivity to volatility.

🔶 Impact on Performance

- Sensitivity and Responsiveness:

- Shorter Ratio Periods and Higher Weights: Make the weighted average more responsive to recent price changes, allowing quicker trade entries and exits but increasing the likelihood of false signals.

- Longer Ratio Periods and Lower Weights: Provide smoother signals with fewer false positives but may delay trade entries, potentially missing out on significant price moves.

- Profit Taking:

- ATR Multipliers: Higher multipliers set take profit levels further away, targeting larger price movements but reducing the probability of reaching these levels.

- Fixed Percentages: Allocating equal percentages at each TP level ensures consistent profit realization and risk management, preventing overexposure.

- Trade Direction Control:

- Selecting Specific Directions: Restricting trades to Long or Short can align the strategy with market trends or personal biases, potentially enhancing performance in trending markets.

- Risk Management:

- Take Profit Percentages: Dividing the position into smaller percentages at multiple TP levels helps lock in profits progressively, reducing risk and allowing the remaining position to ride further trends.

- Market Adaptability:

- Weighted Averages and ATR: By combining multiple timeframes and adjusting to volatility, the strategy adapts to different market conditions, maintaining effectiveness across various asset classes and timeframes.

---

If you want to know more about ATR, can also check "SuperATR 7-Step Profit".

Enjoy trading.

Strategy

Stoch RSI and RSI Buy/Sell Signals with MACD Trend FilterDescription of the Indicator

This Pine Script is designed to provide traders with buy and sell signals based on the combination of Stochastic RSI, RSI, and MACD indicators, enhanced by the confirmation of candle colors. The primary goal is to facilitate informed trading decisions in various market conditions by utilizing different indicators and their interactions. The script allows customization of various parameters, providing flexibility for traders to adapt it to their specific trading styles.

Usefulness

This indicator is not just a mashup of existing indicators; it integrates the functionality of multiple momentum and trend-detection methods into a cohesive trading tool. The combination of Stochastic RSI, RSI, and MACD offers a well-rounded approach to analyzing market conditions, allowing traders to identify entry and exit points effectively. The inclusion of color-coded signals (strong vs. weak) further enhances its utility by providing visual cues about the strength of the signals.

How to Use This Indicator

Input Settings: Adjust the parameters for the Stochastic RSI, RSI, and MACD to fit your trading style. Set the overbought/oversold levels according to your risk tolerance.

Signal Colors:

Strong Buy Signal: Indicated by a green label and confirmed by a green candle (close > open).

Weak Buy Signal: Indicated by a blue label and confirmed by a green candle (close > open).

Strong Sell Signal: Indicated by a red label and confirmed by a red candle (close < open).

Weak Sell Signal: Indicated by an orange label and confirmed by a red candle (close < open).

Example Trading Strategy Using This Indicator

To effectively use this indicator as part of your trading strategy, follow these detailed steps:

Setup:

Timeframe : Select a timeframe that aligns with your trading style (e.g., 15-minute for intraday, 1-hour for swing trading, or daily for longer-term positions).

Indicator Settings : Customize the Stochastic RSI, RSI, and MACD parameters to suit your trading approach. Adjust overbought/oversold levels to match your risk tolerance.

Strategy:

1. Strong Buy Entry Criteria :

Wait for a strong buy signal (green label) when the RSI is at or below the oversold level (e.g., ≤ 35), indicating a deeply oversold market. Confirm that the MACD shows a decreasing trend (bearish momentum weakening) to validate a potential reversal. Ensure the current candle is green (close > open) if candle color confirmation is enabled.

Example Use : On a 1-hour chart, if the RSI drops below 35, MACD shows three consecutive bars of decreasing negative momentum, and a green candle forms, enter a buy position. This setup signals a robust entry with strong momentum backing it.

2. Weak Buy Entry Criteria :

Monitor for weak buy signals (blue label) when RSI is above the oversold level but still below the neutral (e.g., between 36 and 50). This indicates a market recovering from an oversold state but not fully reversing yet. These signals can be used for early entries with additional confirmations, such as support levels or higher timeframe trends.

Example Use : On the same 1-hour chart, if RSI is at 45, the MACD shows momentum stabilizing (not necessarily negative), and a green candle appears, consider a partial or cautious entry. Use this as an early warning for a potential bullish move, especially when higher timeframe indicators align.

3. Strong Sell Entry Criteria :

Look for a strong sell signal (red label) when RSI is at or above the overbought level (e.g., ≥ 65), signaling a strong overbought condition. The MACD should show three consecutive bars of increasing positive momentum to indicate that the bullish trend is weakening. Ensure the current candle is red (close < open) if candle color confirmation is enabled.

Example Use : If RSI reaches 70, MACD shows increasing momentum that starts to level off, and a red candle forms on a 1-hour chart, initiate a short position with a stop loss set above recent resistance. This is a high-confidence signal for potential price reversal or pullback.

4. Weak Sell Entry Criteria :

Use weak sell signals (orange label) when RSI is between the neutral and overbought levels (e.g., between 50 and 64). These can indicate potential short opportunities that might not yet be fully mature but are worth monitoring. Look for other confirmations like resistance levels or trendline touches to strengthen the signal.

Example Use : If RSI reads 60 on a 1-hour chart, and the MACD shows slight positive momentum with signs of slowing down, place a cautious sell position or scale out of existing long positions. This setup allows you to prepare for a possible downtrend.

Trade Management:

Stop Loss : For buy trades, place stop losses below recent swing lows. For sell trades, set stops above recent swing highs to manage risk effectively.

Take Profit : Target nearby resistance or support levels, apply risk-to-reward ratios (e.g., 1:2), or use trailing stops to lock in profits as price moves in your favor.

Confirmation : Align these signals with broader trends on higher timeframes. For example, if you receive a weak buy signal on a 15-minute chart, check the 1-hour or daily chart to ensure the overall trend is not bearish.

Real-World Example: Imagine trading on a 15-minute chart :

For a buy:

A strong buy signal (green) appears when the RSI dips to 32, MACD shows declining bearish momentum, and a green candle forms. Enter a buy position with a stop loss below the most recent support level.

Alternatively, a weak buy signal (blue) appears when RSI is at 47. Use this as a signal to start monitoring the market closely or enter a smaller position if other indicators (like support and volume analysis) align.

For a sell:

A strong sell signal (red) with RSI at 72 and a red candle signals to short with conviction. Place your stop loss just above the last peak.

A weak sell signal (orange) with RSI at 62 might prompt caution but can still be acted on if confirmed by declining volume or touching a resistance level.

These strategies show how to blend both strong and weak signals into your trading for more nuanced decision-making.

Technical Analysis of the Code

1. Stochastic RSI Calculation:

The script calculates the Stochastic RSI (stochRsiK) using the RSI as input and smooths it with a moving average (stochRsiD).

Code Explanation : ta.stoch(rsi, rsi, rsi, stochLength) computes the Stochastic RSI, and ta.sma(stochRsiK, stochSmoothing) applies smoothing.

2. RSI Calculation :

The RSI is computed over a user-defined period and checks for overbought or oversold conditions.

Code Explanation : rsi = ta.rsi(close, rsiLength) calculates RSI values.

3. MACD Trend Filter :

MACD is calculated with fast, slow, and signal lengths, identifying trends via three consecutive bars moving in the same direction.

Code Explanation : = ta.macd(close, macdLengthFast, macdLengthSlow, macdSignalLength) sets MACD values. Conditions like macdLine < macdLine confirm trends.

4. Buy and Sell Conditions :

The script checks Stochastic RSI, RSI, and MACD values to set buy/sell flags. Candle color filters further confirm valid entries.

Code Explanation : buyConditionMet and sellConditionMet logically check all conditions and toggles (enableStochCondition, enableRSICondition, etc.).

5. Signal Flags and Confirmation :

Flags track when conditions are met and ensure signals only appear on appropriate candle colors.

Code Explanation : Conditional blocks (if statements) update buyFlag and sellFlag.

6. Labels and Alerts :

The indicator plots "BUY" or "SELL" labels with the RSI value when signals trigger and sets alerts through alertcondition().

Code Explanation : label.new() displays the signal, color-coded for strength based on RSI.

NOTE : All strategies can be enabled or disabled in the settings, allowing traders to customize the indicator to their preferences and trading styles.

MMRI Chart (Primary)The **Mannarino Market Risk Indicator (MMRI)** is a financial risk measurement tool created by financial strategist Gregory Mannarino. It’s designed to assess the risk level in the stock market and economy based on current bond market conditions and the strength of the U.S. dollar. The MMRI considers factors like the U.S. 10-Year Treasury Yield and the Dollar Index (DXY), which indicate investor confidence in government debt and the dollar's purchasing power, respectively.

The formula for MMRI uses the 10-Year Treasury Yield multiplied by the Dollar Index, divided by a constant (1.61) to normalize the risk measure. A higher MMRI score suggests increased market risk, while a lower score indicates more stability. Mannarino has set certain thresholds to interpret the MMRI score:

- **Below 100**: Low risk.

- **100–200**: Moderate risk.

- **200–300**: High risk.

- **Above 300**: Extreme risk, indicating market instability and potential downturns.

This tool aims to provide insight into economic conditions that may affect asset classes like stocks, bonds, and precious metals. Mannarino often updates MMRI scores and risk analyses in his public market updates.

Z-Score RSI StrategyOverview

The Z-Score RSI Indicator is an experimental take on momentum analysis. By applying the Relative Strength Index (RSI) to a Z-score of price data, it measures how far prices deviate from their mean, scaled by standard deviation. This isn’t your traditional use of RSI, which is typically based on price data alone. Nevertheless, this unconventional approach can yield unique insights into market trends and potential reversals.

Theory and Interpretation

The RSI calculates the balance between average gains and losses over a set period, outputting values from 0 to 100. Typically, people look at the overbought or oversold levels to identify momentum extremes that might be likely to lead to a reversal. However, I’ve often found that RSI can be effective for trend-following when observing the crossover of its moving average with the midline or the crossover of the RSI with its own moving average. These crossovers can provide useful trend signals in various market conditions.

By combining RSI with a Z-score of price, this indicator estimates the relative strength of the price’s distance from its mean. Positive Z-score trends may signal a potential for higher-than-average prices in the near future (scaled by the standard deviation), while negative trends suggest the opposite. Essentially, when the Z-Score RSI indicates a trend, it reflects that the Z-score (the distance between the average and current price) is likely to continue moving in the trend’s direction. Generally, this signals a potential price movement, though it’s important to note that this could also occur if there’s a shift in the mean or standard deviation, rather than a meaningful change in price itself.

While the Z-Score RSI could be an insightful addition to a comprehensive trading system, it should be interpreted carefully. Mean shifts may validate the indicator’s predictions without necessarily indicating any notable price change, meaning it’s best used in tandem with other indicators or strategies.

Recommendations

Before putting this indicator to use, conduct thorough backtesting and avoid overfitting. The added parameters allow fine-tuning to fit various assets, but be careful not to optimize purely for the highest historical returns. Doing so may create an overly tailored strategy that performs well in backtests but fails in live markets. Keep it balanced and look for robust performance across multiple scenarios, as overfitting is likely to lead to disappointing real-world results.

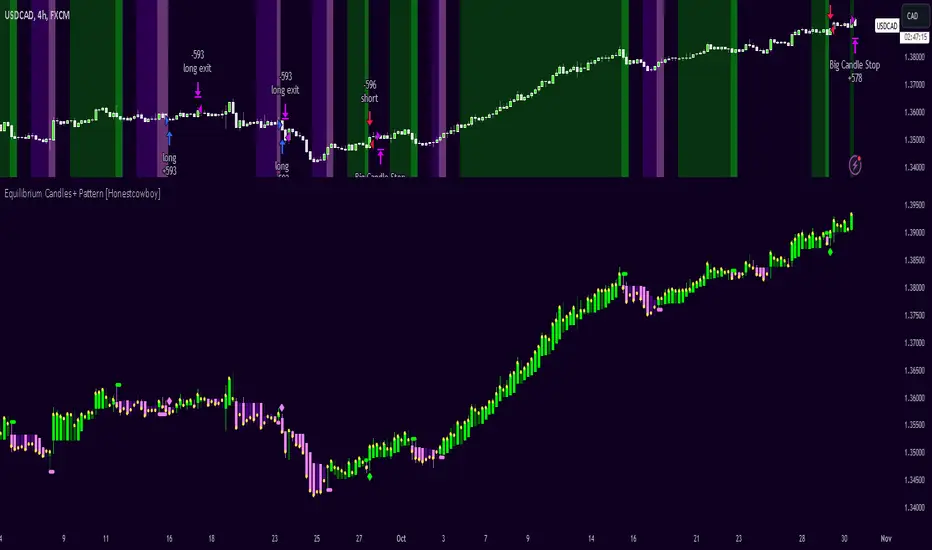

Equilibrium Candles + Pattern [Honestcowboy]The Equilibrium Candles is a very simple trend continuation or reversal strategy depending on your settings.

How an Equilibrium Candle is created:

We calculate the equilibrium by measuring the mid point between highest and lowest point over X amount of bars back.

This now is the opening price for each bar and will be considered a green bar if price closes above equilibrium.

Bars get shaded by checking if regular candle close is higher than open etc. So you still see what the normal candles are doing.

Why are they useful?

The equilibrium is calculated the same as Baseline in Ichimoku Cloud. Which provides a point where price is very likely to retrace to. This script visualises the distance between close and equilibrium using candles. To provide a clear visual of how price relates to this equilibrium point.

This also makes it more straightforward to develop strategies based on this simple concept and makes the trader purely focus on this relationship and not think of any Ichimoku Cloud theories.

Script uses a very simple pattern to enter trades:

It will count how many candles have been one directional (above or below equilibrium)

Based on user input after X candles (7 by default) script shows we are in a trend (bg colors)

On the first pullback (candle closes on other side of equilibrium) it will look to enter a trade.

Places a stop order at the high of the candle if bullish trend or reverse if bearish trend.

If based on user input after X opposite candles (2 by default) order is not filled will cancel it and look for a new trend.

Use Reverse Logic:

There is a use reverse logic in the settings which on default is turned on. It will turn long orders into short orders making the stop orders become limit orders. It will use the normal long SL as target for the short. And TP as stop for the short. This to provide a means to reverse equity curve in case your pair is mean reverting by nature instead of trending.

ATR Calculation:

Averaged ATR, which is using ta.percentile_nearest_rank of 60% of a normal ATR (14 period) over the last 200 bars. This in simple words finds a value slightly above the mean ATR value over that period.

Big Candle Exit Logic:

Using Averaged ATR the script will check if a candle closes X times that ATR from the equilibrium point. This is then considered an overextension and all trades are closed.

This is also based on user input.

Simple trade management logic:

Checks if the user has selected to use TP and SL, or/and big candle exit.

Places a TP and SL based on averaged ATR at a multiplier based on user Input.

Closes trade if there is a Big Candle Exit or an opposite direction signal from indicator.

Script can be fully automated to MT5

There are risk settings in % and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

There is also a simple buy and sell alert feature if you don't want to fully automate but still get alerts. These are available in the dropdown when creating an alert.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

The backtest uses a 4% exposure per trade and a 10 point slippage. I did not include a commission cause I'm not personaly aware what the commissions are on most forex brokers. I'm only aware of minimal slippage to use in a backtest. Trading conditions vary per broker you use so always pay close attention to trading costs on your own broker. Use a full automation at your own risk and discretion and do proper backtesting.

SuperATR 7-Step Profit - Strategy [presentTrading] Long time no see!

█ Introduction and How It Is Different

The SuperATR 7-Step Profit Strategy is a multi-layered trading approach that integrates adaptive Average True Range (ATR) calculations with momentum-based trend detection. What sets this strategy apart is its sophisticated 7-step take-profit mechanism, which combines four ATR-based exit levels and three fixed percentage levels. This hybrid approach allows traders to dynamically adjust to market volatility while systematically capturing profits in both long and short market positions.

Traditional trading strategies often rely on static indicators or single-layered exit strategies, which may not adapt well to changing market conditions. The SuperATR 7-Step Profit Strategy addresses this limitation by:

- Using Adaptive ATR: Enhances the standard ATR by making it responsive to current market momentum.

- Incorporating Momentum-Based Trend Detection: Identifies stronger trends with higher probability of continuation.

- Employing a Multi-Step Take-Profit System: Allows for gradual profit-taking at predetermined levels, optimizing returns while minimizing risk.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy revolves around detecting strong market trends and capitalizing on them using an adaptive ATR and momentum indicators. Below is a detailed breakdown of each component of the strategy.

🔶 1. True Range Calculation with Enhanced Volatility Detection

The True Range (TR) measures market volatility by considering the most significant price movements. The enhanced TR is calculated as:

TR = Max

Where:

High and Low are the current bar's high and low prices.

Previous Close is the closing price of the previous bar.

Abs denotes the absolute value.

Max selects the maximum value among the three calculations.

🔶 2. Momentum Factor Calculation

To make the ATR adaptive, the strategy incorporates a Momentum Factor (MF), which adjusts the ATR based on recent price movements.

Momentum = Close - Close

Stdev_Close = Standard Deviation of Close over n periods

Normalized_Momentum = Momentum / Stdev_Close (if Stdev_Close ≠ 0)

Momentum_Factor = Abs(Normalized_Momentum)

Where:

Close is the current closing price.

n is the momentum_period, a user-defined input (default is 7).

Standard Deviation measures the dispersion of closing prices over n periods.

Abs ensures the momentum factor is always positive.

🔶 3. Adaptive ATR Calculation

The Adaptive ATR (AATR) adjusts the traditional ATR based on the Momentum Factor, making it more responsive during volatile periods and smoother during consolidation.

Short_ATR = SMA(True Range, short_period)

Long_ATR = SMA(True Range, long_period)

Adaptive_ATR = /

Where:

SMA is the Simple Moving Average.

short_period and long_period are user-defined inputs (defaults are 3 and 7, respectively).

🔶 4. Trend Strength Calculation

The strategy quantifies the strength of the trend to filter out weak signals.

Price_Change = Close - Close

ATR_Multiple = Price_Change / Adaptive_ATR (if Adaptive_ATR ≠ 0)

Trend_Strength = SMA(ATR_Multiple, n)

🔶 5. Trend Signal Determination

If (Short_MA > Long_MA) AND (Trend_Strength > Trend_Strength_Threshold):

Trend_Signal = 1 (Strong Uptrend)

Elif (Short_MA < Long_MA) AND (Trend_Strength < -Trend_Strength_Threshold):

Trend_Signal = -1 (Strong Downtrend)

Else:

Trend_Signal = 0 (No Clear Trend)

🔶 6. Trend Confirmation with Price Action

Adaptive_ATR_SMA = SMA(Adaptive_ATR, atr_sma_period)

If (Trend_Signal == 1) AND (Close > Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Elif (Trend_Signal == -1) AND (Close < Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Else:

Trend_Confirmed = False

Local Performance

🔶 7. Multi-Step Take-Profit Mechanism

The strategy employs a 7-step take-profit system

█ Trade Direction

The SuperATR 7-Step Profit Strategy is designed to work in both long and short market conditions. By identifying strong uptrends and downtrends, it allows traders to capitalize on price movements in either direction.

Long Trades: Initiated when the market shows strong upward momentum and the trend is confirmed.

Short Trades: Initiated when the market exhibits strong downward momentum and the trend is confirmed.

█ Usage

To implement the SuperATR 7-Step Profit Strategy:

1. Configure the Strategy Parameters:

- Adjust the short_period, long_period, and momentum_period to match the desired sensitivity.

- Set the trend_strength_threshold to control how strong a trend must be before acting.

2. Set Up the Multi-Step Take-Profit Levels:

- Define ATR multipliers and fixed percentage levels according to risk tolerance and profit goals.

- Specify the percentage of the position to close at each level.

3. Apply the Strategy to a Chart:

- Use the strategy on instruments and timeframes where it has been tested and optimized.

- Monitor the positions and adjust parameters as needed based on performance.

4. Backtest and Optimize:

- Utilize TradingView's backtesting features to evaluate historical performance.

- Adjust the default settings to optimize for different market conditions.

█ Default Settings

Understanding default settings is crucial for optimal performance.

Short Period (3): Affects the responsiveness of the short-term MA.

Effect: Lower values increase sensitivity but may produce more false signals.

Long Period (7): Determines the trend baseline.

Effect: Higher values reduce noise but may delay signals.

Momentum Period (7): Influences adaptive ATR and trend strength.

Effect: Shorter periods react quicker to price changes.

Trend Strength Threshold (0.5): Filters out weaker trends.

Effect: Higher thresholds yield fewer but stronger signals.

ATR Multipliers: Set distances for ATR-based exits.

Effect: Larger multipliers aim for bigger moves but may reduce hit rate.

Fixed TP Levels (%): Control profit-taking on smaller moves.

Effect: Adjusting these levels affects how quickly profits are realized.

Exit Percentages: Determine how much of the position is closed at each TP level.

Effect: Higher percentages reduce exposure faster, affecting risk and reward.

Adjusting these variables allows you to tailor the strategy to different market conditions and personal risk preferences.

By integrating adaptive indicators and a multi-tiered exit strategy, the SuperATR 7-Step Profit Strategy offers a versatile tool for traders seeking to navigate varying market conditions effectively. Understanding and adjusting the key parameters enables traders to harness the full potential of this strategy.

Oscillator Price Divergence & Trend Strategy (DPS) // AlgoFyreThe Oscillator Price Divergence & Trend Strategy (DPS) strategy combines price divergence and trend indicators for trend trading. It uses divergence conditions to identify entry points and a trend source for directional bias. The strategy incorporates risk management through dynamic position sizing based on a fixed risk amount. It allows for both long and short positions with customizable stop-loss and take-profit levels. The script includes visualization options for entry, stop-loss, and take-profit levels, enhancing trade analysis.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Divergence-Trend Combination

🔸Dynamic Position Sizing

🔸Customizable Risk Management

🔶 FUNCTIONALITY

🔸Indicators

🞘 Trend Indicator

🞘 Oscillator Source

🔸Conditions

🞘 Long Entry

🞘 Short Entry

🞘 Take Profit

🞘 Stop Loss

🔶 INSTRUCTIONS

🔸Adding the Strategy to the Chart

🔸Configuring the Strategy

🔸Backtesting and Practice

🔸Market Awareness

🔸Visual Customization

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Divergence Trend Trading with Dynamic Position Sizing strategy uniquely combines price divergence indicators with trend analysis to optimize entry and exit points. Unlike static trading strategies, it employs dynamic position sizing based on a fixed risk amount, ensuring consistent risk management. This approach allows traders to adapt to varying market conditions by adjusting position sizes according to predefined risk parameters, enhancing both flexibility and control in trading decisions. The strategy's integration of customizable stop-loss and take-profit levels further refines its risk management capabilities, making it a robust tool for both trending and volatile markets.

🔸Divergence-Trend Combination By combining trend direction with divergence conditions, the strategy enhances the accuracy of entry signals, aligning trades with prevailing market trends.

🔸Dynamic Position Sizing This strategy calculates position sizes dynamically, based on a fixed risk amount, allowing traders to maintain consistent risk exposure across trades.

🔸Customizable Risk Management Traders can set flexible risk-reward ratios and adjust stop-loss and take-profit levels, tailoring the strategy to their risk tolerance and market conditions.

🔶 FUNCTIONALITY The Divergence Trend Trading with Dynamic Position Sizing strategy leverages a combination of trend indicators and price and oscillator divergences to identify optimal trading opportunities. This strategy is designed to capitalize on medium to long-term price movements and works best on h1, h4 or D1 timeframes. It allows traders to manage risk effectively while taking advantage of both long and short positions.

🔸Indicators 🞘 Trend Indicator: A long trend is used to determine market direction, ensuring trades align with prevailing trends.

Recommendation: We recommend using the Adaptive MAs (Hurst, CVaR, Fractal) // AlgoFyre indicator with the following settings for trend detection. However, you can use any trend indicator that suits your trading style, e.g. an EMA 200.

🞘 Oscillator Source: The oscillator source is used for momentum price divergence identification. Any momentum oscillator can be used, e.g. RSI, Stochastic etc. A good oscillator is the Stochastic with the following settings:

🔸Conditions 🞘 Long Entry: A long entry condition is met if price closes above the trend AND selected divergence conditions are met, e.g. regular bullish divergence with a 10 bar lookback period with the divergence being below the 50 point mean. If the info table shows all 3 columns in the same color, the entry conditions are met and a position is opened.

🞘 Short Entry: A short entry condition is met if price closes below the trend AND selected divergence conditions are met, e.g. regular bearish divergence with a 10 bar lookback period with the divergence being above the 50 point mean.

🞘 Take Profit: Take Profit is determined by the Risk to Reward Ratio settings depending on the price distance between the entry price and the stop loss price, e.g. if stop loss is 1% away from entry and Risk Reward Ratio is 3:1 then Take Profit will be set at 3% from entry.

🞘 Stop Loss: Stop loss is a fixed level away from the trend source. For long positions, stop loss is set below the trend, and for short positions, above the trend.

🔶 INSTRUCTIONS The Divergence Trend Trading with Dynamic Position Sizing strategy can be set up by adding it to your TradingView chart and configuring parameters such as the oscillator source, trend source, and risk management settings. This strategy is designed to capitalize on short-term price movements by dynamically adjusting position sizes based on predefined risk parameters. Enhance the accuracy of signals by combining this strategy with additional indicators like trend-following or momentum-based tools. Adjust settings to better manage risk and optimize entry and exit points.

🔸Adding the Strategy to the Chart:

Go to your TradingView chart.

Click on the "Indicators" button at the top.

Search for "Divergence Trend Trading with Dynamic Position Sizing // AlgoFyre" in the indicators list.

Click on the strategy to add it to your chart.

🔸Configuring the Strategy:

Open the strategy settings by clicking on the gear icon next to its name on the chart.

Oscillator Source: Select the source for the oscillator. An oscillator like Stochastic needs to be attached to the chart already in order to be used as an oscillator source to be selectable.

Trend Source: Choose the trend source to determine market direction. A trend indicator like Adaptive MAs (Hurst, CVaR, Fractal) // AlgoFyre needs to be attached to the chart already in order to be used as a trend source to be selectable.

Stop Loss Percentage: Set the stop loss distance from the trend source as a percentage.

Risk/Reward Ratio: Define the desired risk/reward ratio for trades.

🔸Backtesting and Practice:

Backtest the strategy on historical data to understand how it performs in various market environments.

Practice using the strategy on a demo account before implementing it in live trading.

🔸Market Awareness:

Keep an eye on market news and events that might cause extreme price movements. The strategy reacts to price data and might not account for news-driven events that can cause large deviations.

🔸Visual Customization Visualization Settings: Customize the display of entry price, take profit, and stop loss levels.

Color Settings: Switch to the AlgoFyre theme or set custom colors for bullish, bearish, and neutral states.

Table Settings: Enable or disable the information table and adjust its position.

🔶 CONCLUSION

The Divergence Trend Trading with Dynamic Position Sizing strategy provides a robust framework for capitalizing on short-term market trends by combining price divergence with dynamic position sizing. This strategy leverages divergence conditions to identify entry points and utilizes a trend source for directional bias, ensuring trades align with prevailing market conditions. By incorporating dynamic position sizing based on a fixed risk amount, traders can effectively manage risk and adapt to varying market conditions. The strategy's customizable stop-loss and take-profit levels further enhance its risk management capabilities, making it a versatile tool for both trending and volatile markets. With its strategic blend of technical indicators and risk management, the Divergence Trend Trading strategy offers traders a comprehensive approach to optimizing trade execution and maximizing potential returns.

NNFX RSI EMA FVMA MACD ALGOThis Pine Script introduces a cutting-edge trading strategy that seamlessly integrates multiple technical indicators—namely, the Flexible Variable Moving Average ( FVMA ), Relative Strength Index ( RSI ), Moving Average Convergence Divergence ( MACD ), and Exponential Moving Average ( EMA )—to deliver a sophisticated trading experience. This script stands out due to its comprehensive approach, robust risk management, and the inclusion of crucial data tables for various timeframes, making it an invaluable tool for traders seeking to enhance their market performance.

Originality of the Strategy:

The originality of this script lies in its unique combination of multiple powerful indicators, enabling traders to benefit from diverse perspectives on market dynamics. This mashup enhances decision-making processes, providing multiple layers of confirmation for trade entries and exits. The strategy is designed to offer an innovative solution for traders looking to improve their performance through well-defined rules and a solid framework.

Flexible Variable Moving Average (FVMA):

The FVMA adapts dynamically to market conditions, offering a more responsive trend line than traditional moving averages. This flexibility allows for quick identification of trends and reversals, crucial for fast-paced trading environments.

Exponential Moving Average (EMA):

By giving greater weight to recent price data, the EMA enhances sensitivity to price changes, allowing for more accurate entries and exits when used alongside the FVMA. This combination maximizes the effectiveness of the strategy in identifying optimal trading opportunities.

Relative Strength Index (RSI):

The RSI helps identify overbought or oversold conditions, integrating seamlessly with other indicators to enhance the strategy's ability to pinpoint potential reversal points. This aspect of the strategy ensures that traders can make informed decisions based on market momentum.

Moving Average Convergence Divergence (MACD):

The MACD serves as an essential confirmation tool, providing insights into trend strength and momentum. This enhances the accuracy of entry and exit signals, allowing traders to make more informed decisions based on robust technical analysis.

Multi-Take Profit (TP) and Stop Loss (SL) Levels:

The strategy supports multiple TPs, allowing traders to lock in profits at various levels while effectively managing risk through a robust SL system. This flexibility caters to diverse trading styles and risk profiles, ensuring that the strategy can adapt to individual trader needs.

Default Properties:

Take Profit Levels: TP1 is set to 2.0, and TP2 is set to 2.9, which is designed to enhance profit potential while maintaining a solid risk-reward ratio.

Stop Loss: A SL is set at 2% of the 5% account balance, which helps to preserve capital and manage risk effectively, adhering to the guideline of not risking more than 5-10% of the account balance per trade.

Labeling System for Exits: Automatic labeling of TP and SL exits on the chart provides clear visualization of trading outcomes. This feature supports informed decision-making and performance tracking, aligning with the guideline of providing transparent results.

Custom Alerts System:

The inclusion of customizable alerts for trade entries, exits, and SL/TP hits keeps traders informed in real-time, enabling prompt actions without constant market monitoring. This is crucial for effective trade management and helps traders respond quickly to market changes.

API Boxes for Automated Trading:

The strategy features API boxes, allowing traders to set up automated trading based on indicator signals. This functionality enables seamless integration with trading platforms, enhancing efficiency and streamlining the trading process, which is particularly valuable for traders looking to optimize their execution.

Data Tables for Enhanced Analysis:

The script includes data tables displaying critical insights across various timeframes: 2-hour, daily, weekly, and monthly. These tables provide a comprehensive overview of market conditions, allowing traders to analyze trends and make informed decisions based on a broad spectrum of data. By leveraging this information, traders can identify high-probability setups and align their strategies with prevailing market trends, significantly increasing their chances of success.

Default Properties:

Initial Capital: £1,000, ensuring a realistic starting point for traders.

Risk per Trade: 5% of the account balance, promoting sustainable trading practices.

Commission: 0.1%, reflecting realistic transaction costs that traders may encounter.

Slippage: 1%, accounting for potential market volatility during trade execution.

Take Profit Levels:

TP1: 2.0

TP2: 2.9

Stop Loss (SL): 2% of the 5% account balance, which is well within acceptable risk parameters.

Compliance with TradingView Guidelines:

This script fully complies with TradingView's guidelines, specifically:

Strategy Results:

The strategy is designed to publish backtesting results that do not mislead traders. The realistic parameters outlined in the default properties ensure that traders have a clear understanding of potential outcomes.

The dataset used for backtesting has sufficient trades to produce a reliable sample size, aligning with the guideline of ideally having more than 100 trades.

Any deviations from recommended practices are justified in the script description, ensuring transparency and adherence to best practices.

The script explains the default properties in detail, providing a thorough understanding of how these settings influence performance.

Why This Script is Worth Paying For:

This Pine Script offers an unparalleled trading experience through its unique combination of technical indicators, comprehensive trade management features, and detailed data tables for multiple timeframes. Here are compelling reasons to invest in this strategy:

Holistic Approach: The integration of multiple indicators ensures a well-rounded perspective on market conditions, increasing the likelihood of successful trades.

Advanced Risk Management: The flexibility of multiple TPs and SLs empowers traders to tailor their risk profiles according to individual strategies, enhancing overall profitability.

Automated Trading Capability: The inclusion of API boxes for automated trading streamlines execution, allowing traders to capitalize on opportunities without the need for manual intervention.

Comprehensive Data Analysis: The detailed data tables provide invaluable insights across different timeframes, enabling traders to make informed decisions based on robust market analysis.

In summary, this innovative Pine Script represents a powerful tool designed to empower traders at all levels. Its originality, synergistic functionality, and comprehensive features create a dynamic and effective trading environment, justifying its value and positioning it as a must-have for anyone serious about achieving consistent trading success.

Support Resistance Pivot EMA Scalp Strategy [Mauserrifle]A strategy that creates signals based on: pivots, EMA 9+20, RSI, ATR, VWAP, wicks and volume.

The strategy is developed as a helper for quick long option scalping. This strategy is primarily designed for intraday trading on the 2m SPY chart with extended hours. However, users can adapt it for use on different symbols and timeframes. These signals are meant as a helper rather than fully automated trading bots.

One of the key elements is its pivot-based calculation, driven by my integrated indicator "Support and Resistance Pivot Points/Lines ". It enables multi-timeframe pivot calculations which are used to generate the signals and offers customizability, allowing you to define rounding methods and cooldown periods to refine pivot levels. The pivots, in combination with EMA crossovers, VWAP trend, and additional filters (RSI, ATR, VWAP, wicks and volume), create an entry and exit strategy for scalping opportunities that is useful for 0/1 DTE options with an average trade time of six minutes with the default setup for SPY. Option trading should be done outside TradingView. At this moment of release there is no option trading support.

All parameters used in the strategy are tweaked based on deep backtests results and real-time behavior. Be mindful that past performance does not guarantee future results.

The strategy is designed for intermediate and advanced users who are familiar intraday option scalping techniques.

How It Works

The strategy identifies entries based on multiple conditions, including: recently above pivot, recent EMA crossovers, RSI range, candle patterns, and VWAP uptrend. It avoids trades below the VWAP lower band due to poor backtesting results in those conditions. It creates a great number of signals when it detects an uptrend, which entails: VWAP and its lower/upper band slopes are going up, and the number of next high pivot points is greater than the number of lower pivot points. This indicates that we hope it will keep going up. In historical testing, this showed favorable results. This uptrend criteria runs on 15m charts max (where up to the VWAP effectiveness is the greatest).

The strategy also checks for candle and volume patterns, identified in backtesting to improve entry levels on historic data. Which include:

A red candle after multiple green ones, hoping to jump on a trend during a small pullback

Zero lower wick

Percentage and volume is up after lower volume candles

Percentage is up and the first and second EMA slopes are going up

Percentage is up, the first EMA is higher than the second, the price low is below the second EMA and price close above it

The VWAP uptrend overrules the candle and volume conditions (thus lots of signals during those moments).

The above is the base for many signals. There is a strict mode that adds extra checks such as:

not trading when there is no next low or high pivot

requiring a VWAP uptrend only

minimum candle percentages

This mode is for analyzing history and seeing performance during these conditions. It is worth it to create a separate alert for strict mode so you are aware of these conditions during trading.

When no stop has been defined, exits will always happen on pivot crossunder confirmations. If a stop is defined (default config), the strategy exits a position when:

the position is negative or no trail has been set

at least 1 bar has past

OR no stop has been defined (overrules previous)

trail has not been activated

The second exit condition happens when the close is below first EMA(9 by default) and when:

the position has been above first EMA

the gap between close and last pivot isn't small

the position is negative or no trail has been set

OR no stop has been defined (overrules above)

trail has not been activated

There are some more variations on this but the above are the most common. These exit conditions are a safety net because the strategy heavily relies on and favors stops. The settings allow changing stops, profit takers and trails. You can configure it to always sell without the conditions above.

The script will paint the pivot lines, trailing activation/stops, EMAs and entry/exits; with extra information in the data panel. For a complete view add VWAP and RSI to your chart, which are available from TradingView official indicator library. The strategy will not rely on those added indicators since VWAP and RSI are programmed in. You can add them to track the behavior of the signals based on these filters you have configured and have a complete view trading this strategy.

As mentioned earlier, the default settings are built for SPY 2m charts, with extended hours and real-time data. Open the strategy on this chart to study how all input parameters are used. If you don't have real-time data you need to adjust the minimum volume settings (set it to 0 at first).

The backtest

The default backtest configuration is set up to simulate SPY option trading.

Start capital is set to 10,000 and we risk around 5% of that per trade (1 contract)

Commission is set to 0.005%. The reason: at the time of this publication the SPY index price is approximately $580. Two ITM 0/1 DTE options contracts, each priced around $280, which is approximately $560. The typical commission for such a trade is around $3. To simulate this commission in the backtest on the SPY index itself, a commission of 0.005% per trade has been applied, approximating the options trading costs.

Slippage of 3 is set reflecting liquid SPY

The bar magnifier feature is turned on to have more realistic fills

Trading

In backtesting, setting commission and slippage to 0 on the SPY 2m chart shows many trades result around breaking even. Personally, I view them as an opportunity and safety net to help manage emotional decisions for exits. The signals are designed for short option scalps, allowing traders to take small profits and potentially re-enter during the strategy’s position window. It's advisable to take small potential profits, such as 4%, whenever the opportunity arises and consider re-entering if the setup still looks favorable, for example price still above ema9. Exiting a long position below ema9 is a common strategy for 2m scalping.

The average trade duration is approximately 6 minutes (3 bars). The choice between ITM (in-the-money), ATM (at-the-money), or OTM (out-of-the-money) options will depend on your trading style. Personally, I’ve seen better results with ITM options because they tend to move more in sync with the underlying index, thanks to their higher delta.

It’s important to note that the signals are designed to be a helper for manual trading rather than to automate a bot. Users are encouraged to take small profits and re-enter positions if favorable conditions persist. Be mindful that past performance does not guarantee future results.

For the default SPY setup the losses will mostly be 4-10% for ITM options. Be mindful of extreme volatile conditions where losses may reach 30% quickly, especially when trading ATM/OTM options.

The following settings can be changed:

8 pivot timeframes with left/right bars and days rendered

Here you can configure the timeframes for the pivots, which are crucial. The strategy wants that a crossover has happened recently (so it might enter after a crossunder if the crossover was recent) or the price is still above the crossed pivot.

When you decide to use a pivot timeframe higher than your chart, make sure it aligns the same starting point as the chart timeframe. As stated in the 43000478429 docs, there is a dependency between the resolution and the alignment of a starting point:

1–14 minutes — aligns to the beginning of a week

15–29 minutes — aligns to the beginning of a month

from 30 minutes and higher — aligns to the beginning of a year

This alignment also affects the setting of rendered days. I recommend a max value of 5 days for 1-14 minutes timeframes.

Also make sure a higher pivot timeframe can be divided by the lower. For instance I had repaint issues using 3m pivots on a 2m chart. But 4m pivots work fine.

Please look up docs 43000478429 to make sure this information is still up to date.

Pivot rounding

The pivot rounding option is used to add pivots based on a rounded price and limit the number of pivots. While this feature is disabled by default it can be useful with tweaking strategy variations, because many orders are placed at rounded levels and tend to act as strong price barriers.

There are multiple rounding methods: round, ceil/floor, roundn (decimal) and rounding to the minimal tick.

The next feature is a powerful extension called "Cooldown rounding":

Pivot cooldown rounding

This rounds new pivot levels for a cooldown period to keep the previous pivot line instead of adding a new line when they match the rounded value within the cooldown period. The existing line will be extended. This feature is useful because it makes sure the initial line is added to the exact high/low pivot level but any future lines within the rounding will just extend the existing line. This limits the number of pivots while still having precise levels (which normal rounding lacks) and allows more precise pivot trading.

This feature also helps ensure that the number of rendered lines will not exceed 500 too much, which is the render limit on TradingView.

You can set a maximum minutes for the cooldown. The default is 3 years which will enable the cooldown rounding permanently on the intraday (due to the max bar limit).

Pivot always added when new higher/lower pivot

When using cooldown rounding, one may find it useful to override this behavior when a new lower or higher pivot level has been reached. When enabled the new level will be added despite the fact that they may be rounded the same in the cooldown check. This is a good balance between limiting pivots but also allowing preciser trading.

VWAP bands multiplier

This is used to tweak the inner VWAP working for the upper and lower band. The default VWAP multiplier (0.9) is set based on backtesting since it performed better on historic data (the strategy does not trade below the lowerband). When you add the VWAP indicator from the TradingView library to the chart, make sure it uses the same multiplier setting as within this strategy so you have a correct view of the conditions the strategy acts on.

ATR EMA smoothing length

Used to tweak the ATR EMA smoothing. By default it is set up to 4 based on deep backtesting historic data.

EMA lengths

Changing the EMA length allows you to fine tune the EMA crossing behavior. By default the strategy is set up to EMA 9 and 20 which are considered commonly used values on the 2-minute chart.

Trading intraday time restrictions

For intraday charts you can configure when the strategy starts trading after market open and when it stops, including a hard sell. This makes sure there are no open positions left for the day during backtesting and can also aid in your trading style. For example some scalpers will not trade in the first two hours. Having no signals during this time can be beneficial. It is possible to configure these settings based on the number of bars or minutes.

Not trading on days the market closes earlier

By default the strategy does not trade on days the market closes earlier in the US. This makes sure there are no open positions left open during backtesting. Make sure to change it when using it on such a day. The days are: day before independence day, day after thanksgiving, Christmas eve and new years eve.

Not trading below VWAP lowerband

Backtesting has shown poor performance when trading below the VWAP lowerband but you are free to allow it to trade in such conditions. Past performance does not guarantee future results.

Minimum volume

A minimum volume can be set up. The current value is based on better deep backtest results for SPY using real-time data (48000). When you do not have a data plan for SPY, please set it to 0 and tweak based on backtests.

Minimum ATRP

The strategy has shown during my trading that it is sensitive to higher ATRP values and more volatile market conditions. There is more chance the index moves and we can profit from this during option scalping (if it moves in your favor). The default is based on SPY backtesting (0.04%), as a balance to have a lot of trades but also capture minimal movement.

RSI range

A RSI range can be set using a minimum and maximum value so we can limit trading during overbought/oversold conditions. Backtesting for SPY has shown the strategy performs better on historic data within a tighter range, so a default range has been set to 40-65.

Allow orders on every tick (no effect on stop/profit/trail)

This setting is used to allow orders on every tick. The strategy has been developed without trading on every tick but you can change this, for example when you have configured a setup different than the default configuration that you know works well with this. The default setup will not work well with it due to too many constant signals.

Stop percentage + ATRP threshold

One of the most important settings for managing the risk. I recommend setting a stop percentage first and later the ATRP threshold where the stop is calculated based on the current ATRP value. The calculated value will only be in effect when it is greater than the normal stop--the normal stop acts as baseline. The default stop is low (0.03). With a default ATRP threshold stop of 1.12, the calculated value overrules the normal stop when the value is greater. 0.03 acts as a minimum value but in reality the stop will most likely be higher on average for SPY with the default ATRP threshold.

For the default SPY setup the losses will be around 4-10% for ITM options. Be mindful of extreme volatile conditions where losses may reach 30% quickly, especially when trading ATM/OTM options.

Profit taker percentage + ATRP threshold

Same principles as the stop percentage above, but for profit taking. There is a very high ATRP threshold of 4 set by default. Backtests showed that trailing stops perform better on historic data.

Trailing stop

Used to set up a trailing stop. A useful feature to secure profit after a run-up, or get out with a small loss after initial activation. It is important to not use too tight values because they will give unrealistic backtest results and trigger too fast in real-time. Both the trail activation level and trail stop itself can be configured with a percentage value and ATRP value. I recommend setting up the ATRP last. By default the values are 0.05 for activation and 0.03 for the stop based on SPY real-time behavior.

Always sell on pivot crossunder confirmation

The strategy includes pivot crossunder confirmations as sell condition. By default it will not sell on every crossunder confirmation but checks for different conditions (explained in detail earlier in this description). You can change this behavior.

Always sell below first EMA when position has been above

The strategy sells below the first EMA when the position has been above it. By default it will not always sell but checks for different conditions (mentioned earlier in this description). You can change this behavior.

Buy modes pivot

By default the strategy buys between pivots as long as there has been a pivot crossover and EMAs crossover recently or price is still above it. You can change the behavior so it only buys on pivot crossovers or pivot crossover confirmations. Backtesting on the default setup shows decreased performance but for other strategy variations and pivot setups this feature can be useful since many scalpers do not buy between pivots.

Strict mode

There is a strict mode that adds extra checks such as not trading when there is no next low or high pivot, requiring a VWAP uptrend only and minimum candle percentages. This mode is for analyzing history and seeing performance during these conditions. It is worth it to create a separate alert for strict mode so you are aware of these conditions during trading. The deep backtests improved with these setting but past performance does not guarantee future results.

In the strict mode section you can override the stop, minimum ATRP, set up a minimum percentage, only trade VWAP uptrends and to not trade candles without a wick.

A summary and some extra detail

At the time of release only long trades are supported

The strategy is meant for quick scalping but one might find other uses for it

Enable extended hours on intraday charts so it captures more pivots

It does not trade extended hours (pre and post market) since options do not trade during those times

real-time data is recommended and required if a symbol has delayed data by default

You can configure that it trades minutes after market open and hard sells minutes after market open

The entries have a specific label text, example: "833 LE1 / 569.71 / P:569.8". This means: / / . The condition number is only for development/debug purposes for me when you have an issue.

The strategy cannot be tweaked to work on multiple symbols and timeframes with a single config. So you will have to make a config for every timeframe and symbol. I recommend using the Indicator Templates feature of TradingView. This way you can save the settings per timeframe and symbol

The strategy is per default config very dependent on (trailing) stops because it trades between pivots too. It wants that a pivot and EMA crossover has happened more recently than a crossunder. But you can change this behavior to always force crossover buys and crossunder sells.

It’s recommended to set up alerts to notify you of entry and exit signals. Watching the chart alone might cause you to miss trades, especially in fast-moving markets.

Only a max of 500 lines can be rendered on the chart, but the strategy will function with more under the hood. When you exceed 500 you will notice the beginning of the chart has no pivots, but beneath everything functions for backtesting.

Changing settings

Changing the settings for a different symbol and/or timeframe can be a challenging task. Here's a how-to you could use the first time to help you get going:

Set commission and slippage to 0. I prefer to do this so it is more clear whether you are balancing on break-even trades

Enable the pivot timeframe equal or above your chart timeframe. Avoid repainting as discussed earlier by choosing timeframes that align with the same timeframe

Set all volume, ATR, stop, profit takers and trail values to 0

Make sure strict mode is disabled at the bottom of the settings

You now have a clean state and you should see the backtest results purely based on pivot and EMA conditions

Tweak the stop and profit taker, beginning with the simple values and then ATRP threshold

At the last moment tweak the trailing stops. Tight trailing stops create an unrealistic backtest so you will need to tweak them based on real-time behavior of the symbol you're using which you will have to monitor during signals while the market is open. The default values are low (2m intraday SPY). Only with the bar magnifier feature it is somewhat possible to tweak realistic with history data. The tighter they are, the more unrealistic your backtest results. As a starting point, set the trailing stop low and find the highest activation level that doesn't change the results drastically, then increase the stop to the value you think reflects real-time behavior.

Keep refining by testing it during real-time behavior. Does it exit too early according to your own judgment? You need to increase the stop and maybe the activation level.

I hope you will find this useful!

DISCLAIMER

Trading is risky & most day traders lose money. This indicator is purely for informational & educational purposes only. Past performance does not guarantee future results.

Central Pivot Point Cross & Retrace Strategy // AlgoFyreThe Central Pivot Point Cross & Retrace Strategy uses pivot points for trend identification and trade entry. It combines accumulation/distribution indicators with pivot point levels to generate signals. The strategy incorporates dynamic position sizing based on a fixed risk amount and allows for both long and short positions with customizable stop-loss levels.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Pivot Point-Based Trading

🔸Accumulation/Distribution

🔸Dynamic Position Sizing

🔸Customizable Risk Management

🔶 FUNCTIONALITY

🔸Indicators

🞘 Pivot Points

🞘 Accumulation/Distribution

🔸Conditions

🞘 Long Entry

🞘 Short Entry

🞘 Take Profit

🞘 Stop Loss

🔶 INSTRUCTIONS

🔸Adding the Strategy to the Chart

🔸Configuring the Strategy

🔸Backtesting and Practice

🔸Market Awareness

🔸Visual Customization

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Central Pivot Point Cross & Retrace Strategy uniquely combines pivot point analysis with accumulation/distribution indicators to identify optimal entry and exit points. It employs dynamic position sizing based on a fixed risk amount, ensuring consistent risk management across trades. This approach allows traders to adapt to varying market conditions by adjusting position sizes according to predefined risk parameters, enhancing both flexibility and control in trading decisions. The strategy's integration of customizable stop-loss levels further refines its risk management capabilities.

🔸Pivot Point-Based Trading This strategy utilizes daily pivot points to identify key support and resistance levels, providing a framework for trend identification and trade entry. The central pivot point serves as the intraday point of balance between buyers and sellers, with the largest amount of trading volume assumed to take place in this area.

🔸Accumulation/Distribution The strategy incorporates the Accumulation/Distribution (A/D) line, an underrated volume-based indicator, to establish the main trend. The A/D line is used in conjunction with a trend based indicator like the 200-period Exponential Moving Average (EMA) to confirm trend direction and strength.

🔸Dynamic Position Sizing Position sizes are calculated dynamically based on a fixed risk amount, allowing traders to maintain consistent risk exposure across trades.

🔸Customizable Risk Management Traders can set flexible risk-reward ratios and adjust stop-loss and take-profit levels, tailoring the strategy to their risk tolerance and market conditions. The strategy recommends taking partial profits at S1 or R1 levels and moving the stop-loss to break-even for remaining positions.

🔶 FUNCTIONALITY The Central Pivot Point Cross & Retrace Strategy leverages pivot points and accumulation/distribution indicators to identify optimal trading opportunities. This strategy is designed to capitalize on price movements around key pivot levels by dynamically adjusting position sizes based on predefined risk parameters. It allows traders to manage risk effectively while taking advantage of both long and short positions.

🔸Indicators 🞘 Pivot Points: Calculates daily pivot points (PP, R1, R2, S1, S2) to identify key support and resistance levels. The central pivot point is crucial for determining market bias and entry points.

🞘 Accumulation/Distribution: Uses the A/D line and with a trend based indicator like the 200 EMA to determine market direction and trend strength. This combination helps eliminate noise and provides more reliable trend signals. We recommend using the Adaptive MAs (Hurst, CVaR, Fractal) // AlgoFyre , but any moving average could be used.

🔸Conditions 🞘 Long Entry: Initiates a long position when the price crosses above the central pivot point (PP), retraces back to it and the A/D line is above its 200 EMA, indicating an uptrend. A limit entry order is set at the PP for entering the long trade.

🞘 Short Entry: Initiates a short position when the price crosses below the central pivot point (PP), retraces back to it and the A/D line is below its 200 EMA, indicating a downtrend. A limit entry order is set at the PP for entering the short trade.

🞘 Take Profit: 50% of the position is closed as profit when R1 for Longs and S1 for Shorts is reached. The position is fully closed when R2 for Longs and S2 for Shorts is reached.

🞘 Stop Loss: Stop loss is set via strategy settings. When the first 50% take profit for both long and shorts is taken, stop loss for both will be moved to break-even/entry.

🔶 INSTRUCTIONS

The Central Pivot Point Cross & Retrace Strategy can be set up by adding it to your TradingView chart and configuring parameters such as the accumulation/distribution source, stop-loss percentage, and risk management settings. This strategy is designed to capitalize on price movements around key pivot levels by dynamically adjusting position sizes based on predefined risk parameters. Enhance the accuracy of signals by combining this strategy with additional indicators like trend-following or momentum-based tools. Adjust settings to better manage risk and optimize entry and exit points.

🔸Adding the Strategy to the Chart Go to your TradingView chart.

Click on the "Pine Editor" button at the bottom of the chart.

Copy and paste the strategy code into the Pine Editor.

Click "Add to Chart" to apply the strategy.

Add the technical indicator "Accumulation/Distribution" to the chart.

Add the trend indicator " Adaptive MAs (Hurst, CVaR, Fractal) // AlgoFyre " or any other MA to the chart and move it to the "Accumulation/Distribution" pane.

Set the source of your trend indicator to "Accumulation/Distribution".

🔸Configuring the Strategy Open the strategy settings by clicking on the gear icon next to its name on the chart.

Accumulation/Distribution Source: Select the source for the accumulation/distribution indicator.

Accumulation/Distribution EMA Source: Select the source for the trend indicator.

Stop Loss Percentage: Set the stop loss distance from the pivot point as a percentage.

Risk Amount: Define the fixed risk amount for position sizing.

Base Order Size: Set the base order size for position calculations.

Number of Positions: Specify the maximum number of positions allowed.

Time Frame: Adjust the time frame based on the currency pair or asset being traded (e.g., 15-minute for EUR/USD, 30-minute for GBP/USD).

🔸Backtesting and Practice Backtest the strategy on historical data to understand how it performs in various market environments.

Practice using the strategy on a demo account before implementing it in live trading.

Test different time frames and asset pairs to find the most suitable combinations.

🔸Market Awareness Keep an eye on market news and events that might cause extreme price movements. The strategy reacts to price data and might not account for news-driven events that can cause large deviations.

Remember that this strategy is not recommended for stocks due to the A/D line's inability to account for gaps in its calculation.

🔸Visual Customization Visualization Settings: Customize the display of entry price, take profit, and stop loss levels.

Color Settings: Switch to the AlgoFyre theme or set custom colors for bullish, bearish, and neutral states.

Table Settings: Enable or disable the information table and adjust its position.

🔶 CONCLUSION

The Central Pivot Point Cross & Retrace Strategy provides a robust framework for capitalizing on price movements around key pivot levels by combining pivot point analysis with accumulation/distribution indicators. This strategy leverages pivot point crossovers to identify entry points and utilizes the A/D line crossover with its 200 EMA for trend confirmation, ensuring trades align with prevailing market conditions. By incorporating dynamic position sizing based on a fixed risk amount, traders can effectively manage risk and adapt to varying market conditions. The strategy's focus on trading around the central pivot point and its customizable stop-loss and take-profit levels further enhance its risk management capabilities, making it a versatile tool for both trending and ranging markets. With its strategic blend of technical indicators and risk management, the Central Pivot Point Cross & Retrace Strategy offers traders a comprehensive approach to optimizing trade execution and maximizing potential returns across various currency pairs and commodities.

VIDYA ProTrend Multi-Tier ProfitHello! This time is about a trend-following system.

VIDYA is quite an interesting indicator that adjusts dynamically to market volatility, making it more responsive to price changes compared to traditional moving averages. Balancing adaptability and precision, especially with the more aggressive short trade settings, challenged me to fine-tune the strategy for a variety of market conditions.

█ Introduction and How it is Different

The "VIDYA ProTrend Multi-Tier Profit" strategy is a trend-following system that combines the VIDYA (Variable Index Dynamic Average) indicator with Bollinger Bands and a multi-step take-profit mechanism.