TASC 2025.04 The Ultimate Oscillator█ OVERVIEW

This script implements an alternative, refined version of the Ultimate Oscillator (UO) designed to reduce lag and enhance responsiveness in momentum indicators, as introduced by John F. Ehlers in his article "Less Lag In Momentum Indicators, The Ultimate Oscillator" from the April 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers states that indicators are essentially filters that remove unwanted noise (i.e., unnecessary information) from market data. Simply put, they process a series of data to place focus on specific information, providing a different perspective on price dynamics. Various filter types attenuate different periodic signals within the data. For instance, a lowpass filter allows only low-frequency signals, a highpass filter allows only high-frequency signals, and a bandpass filter allows signals within a specific frequency range .

Ehlers explains that the key to removing indicator lag is to combine filters of different types in such a way that the result preserves necessary, useful signals while minimizing delay (lag). His proposed UltimateOscillator aims to maintain responsiveness to a specific frequency range by measuring the difference between two highpass filters' outputs. The oscillator uses the following formula:

UO = (HP1 - HP2) / RMS

Where:

HP1 is the first highpass filter.

HP2 is another highpass filter that allows only shorter wavelengths than the critical period of HP1.

RMS is the root mean square of the highpass filter difference, used as a scaling factor to standardize the output.

The resulting oscillator is similar to a bandpass filter , because it emphasizes wavelengths between the critical periods of the two highpass filters. Ehlers' UO responds quickly to value changes in a series, providing a responsive view of momentum with little to no lag.

█ USAGE

Ehlers' UltimateOscillator sets the critical periods of its highpass filters using two parameters: BandEdge and Bandwidth :

The BandEdge sets the critical period of the second highpass filter, which determines the shortest wavelengths in the response.

The Bandwidth is a multiple of the BandEdge used for the critical period of the first highpass filter, which determines the longest wavelengths in the response. Ehlers suggests that a Bandwidth value of 2 works well for most applications. However, traders can use any value above or equal to 1.4.

Users can customize these parameters with the "Bandwidth" and "BandEdge" inputs in the "Settings/Inputs" tab.

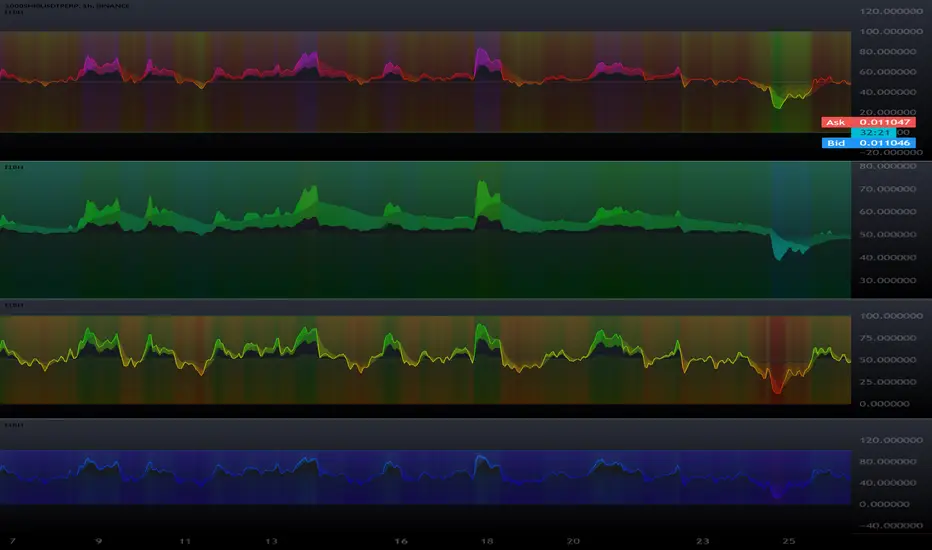

The script plots the UO calculated for the specified "Source" series in a separate pane, with a color based on the chart's foreground color. Positive UO values indicate upward momentum or trends, and negative UO values indicate the opposite.

Additionally, this indicator provides the option to display a "cloud" from 10 additional UO series with different settings for an aggregate view of momentum. The "Cloud" input offers four display choices: "Bandwidth", "BandEdge", "Bandwidth + BandEdge", or "None".

The "Bandwidth" option calculates oscillators with different Bandwidth values based on the main oscillator's setting. Likewise, the "BandEdge" option calculates oscillators with varying BandEdge values. The "Bandwidth + BandEdge" option calculates the extra oscillators with different values for both parameters.

When a user selects any of these options, the script plots the maximum and minimum oscillator values and fills their space with a color gradient. The fill color corresponds to the net sum of each UO's sign , indicating whether most of the UOs reflect positive or negative momentum. Green hues mean most oscillators are above zero, signifying stronger upward momentum. Red hues mean most are below zero, indicating stronger downward momentum.

Tasc

TASC 2025.03 A New Solution, Removing Moving Average Lag█ OVERVIEW

This script implements a novel technique for removing lag from a moving average, as introduced by John Ehlers in the "A New Solution, Removing Moving Average Lag" article featured in the March 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers explains that the average price in a time series represents a statistical estimate for a block of price values, where the estimate is positioned at the block's center on the time axis. In the case of a simple moving average (SMA), the calculation moves the analyzed block along the time axis and computes an average after each new sample. Because the average's position is at the center of each block, the SMA inherently lags behind price changes by half the data length.

As a solution to removing moving average lag, Ehlers proposes a new projected moving average (PMA) . The PMA smooths price data while maintaining responsiveness by calculating a projection of the average using the data's linear regression slope.

The slope of linear regression on a block of financial time series data can be expressed as the covariance between prices and sample points divided by the variance of the sample points. Ehlers derives the PMA by adding this slope across half the data length to the SMA, creating a first-order prediction that substantially reduces lag:

PMA = SMA + Slope * Length / 2

In addition, the article includes methods for calculating predictions of the PMA and the slope based on second-order and fourth-order differences. The formulas for these predictions are as follows:

PredictPMA = PMA + 0.5 * (Slope - Slope ) * Length

PredictSlope = 1.5 * Slope - 0.5 * Slope

Ehlers suggests that crossings between the predictions and the original values can help traders identify timely buy and sell signals.

█ USAGE

This indicator displays the SMA, PMA, and PMA prediction for a specified series in the main chart pane, and it shows the linear regression slope and prediction in a separate pane. Analyzing the difference between the PMA and SMA can help to identify trends. The differences between PMA or slope and its corresponding prediction can indicate turning points and potential trade opportunities.

The SMA plot uses the chart's foreground color, and the PMA and slope plots are blue by default. The plots of the predictions have a green or red hue to signify direction. Additionally, the indicator fills the space between the SMA and PMA with a green or red color gradient based on their differences:

Users can customize the source series, data length, and plot colors via the inputs in the "Settings/Inputs" tab.

█ NOTES FOR Pine Script® CODERS

The article's code implementation uses a loop to calculate all necessary sums for the slope and SMA calculations. Ported into Pine, the implementation is as follows:

pma(float src, int length) =>

float PMA = 0., float SMA = 0., float Slope = 0.

float Sx = 0.0 , float Sy = 0.0

float Sxx = 0.0 , float Syy = 0.0 , float Sxy = 0.0

for count = 1 to length

float src1 = src

Sx += count

Sy += src

Sxx += count * count

Syy += src1 * src1

Sxy += count * src1

Slope := -(length * Sxy - Sx * Sy) / (length * Sxx - Sx * Sx)

SMA := Sy / length

PMA := SMA + Slope * length / 2

However, loops in Pine can be computationally expensive, and the above loop's runtime scales directly with the specified length. Fortunately, Pine's built-in functions often eliminate the need for loops. This indicator implements the following function, which simplifies the process by using the ta.linreg() and ta.sma() functions to calculate equivalent slope and SMA values efficiently:

pma(float src, int length) =>

float Slope = ta.linreg(src, length, 0) - ta.linreg(src, length, 1)

float SMA = ta.sma(src, length)

float PMA = SMA + Slope * length * 0.5

To learn more about loop elimination in Pine, refer to this section of the User Manual's Profiling and optimization page.

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

TASC 2025.01 Linear Predictive Filters█ OVERVIEW

This script implements a suite of tools for identifying and utilizing dominant cycles in time series data, as introduced by John Ehlers in the "Linear Predictive Filters And Instantaneous Frequency" article featured in the January 2025 edition of TASC's Traders' Tips . Dominant cycle information can help traders adapt their indicators and strategies to changing market conditions.

█ CONCEPTS

Conventional technical indicators and strategies often rely on static, unchanging parameters, which may fail to account for the dynamic nature of market data. In his article, John Ehlers applies digital signal processing principles to address this issue, introducing linear predictive filters to identify cyclic information for adapting indicators and strategies to evolving market conditions.

This approach treats market data as a complex series in the time domain. Analyzing the series in the frequency domain reveals information about its cyclic components. To reduce the impact of frequencies outside a range of interest and focus on a specific range of cycles, Ehlers applies second-order highpass and lowpass filters to the price data, which attenuate or remove wavelengths outside the desired range. This band-limited analysis isolates specific parts of the frequency spectrum for various trading styles, e.g., longer wavelengths for position trading or shorter wavelengths for swing trading.

After filtering the series to produce band-limited data, Ehlers applies a linear predictive filter to predict future values a few bars ahead. The filter, calculated based on the techniques proposed by Lloyd Griffiths, adaptively minimizes the error between the latest data point and prediction, successively adjusting its coefficients to align with the band-limited series. The filter's coefficients can then be applied to generate an adaptive estimate of the band-limited data's structure in the frequency domain and identify the dominant cycle.

█ USAGE

This script implements the following tools presented in the article:

Griffiths Predictor

This tool calculates a linear predictive filter to forecast future data points in band-limited price data. The crosses between the prediction and signal lines can provide potential trade signals.

Griffiths Spectrum

This tool calculates a partial frequency spectrum of the band-limited price data derived from the linear predictive filter's coefficients, displaying a color-coded representation of the frequency information in the pane. This mode's display represents the data as a periodogram . The bottom of each plotted bar corresponds to a specific analyzed period (inverse of frequency), and the bar's color represents the presence of that periodic cycle in the time series relative to the one with the highest presence (i.e., the dominant cycle). Warmer, brighter colors indicate a higher presence of the cycle in the series, whereas darker colors indicate a lower presence.

Griffiths Dominant Cycle

This tool compares the cyclic components within the partial spectrum and identifies the frequency with the highest power, i.e., the dominant cycle . Traders can use this dominant cycle information to tune other indicators and strategies, which may help promote better alignment with dynamic market conditions.

Notes on parameters

Bandpass boundaries:

In the article, Ehlers recommends an upper bound of 125 bars or higher to capture longer-term cycles for position trading. He recommends an upper bound of 40 bars and a lower bound of 18 bars for swing trading. If traders use smaller lower bounds, Ehlers advises a minimum of eight bars to minimize the potential effects of aliasing.

Data length:

The Griffiths predictor can use a relatively small data length, as autocorrelation diminishes rapidly with lag. However, for optimal spectrum and dominant cycle calculations, the length must match or exceed the upper bound of the bandpass filter. Ehlers recommends avoiding excessively long lengths to maintain responsiveness to shorter-term cycles.

TASC 2024.12 Dynamic ADX Histogram█ OVERVIEW

This script introduces a new version of the ADX oscillator, designed by Neil Jon Harrington and featured in the "Revisualizing The ADX Oscillator" article from the December 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

The directional movement index (DMI+ and DMI−) and average directional index (ADX) indicators have long been popular with technical analysts. Developed by J. Welles Wilder in the 1970s, these indicators provide information about the direction and strength of price movements across bars. The DMI+ measures positive price movement, the DMI- measures negative price movement, and the ADX gauges the average strength of price trends. Although these indicators can provide helpful insights into price action and momentum, Neil Jon Harrington argues they are often misunderstood or misapplied.

Harrington's indicator, the Dynamic ADX Histogram (DADX), applies directional information to the ADX based on DMI+ and DMI- values to create a single oscillator centered around 0. The indicator displays the oscillator as a histogram with dynamic colors based on ADX movements and user-defined strength thresholds. The author believes this modification of the ADX and DMI data offers a more intuitive visualization of the information provided by Wilder's calculations.

An additional feature of the DADX is the option to use average (smooth) DMI+ and DMI- values in the oscillator's calculation, which reduces noise and choppiness at the cost of added lag.

█ USAGE

The "ADX Length" input determines the number of bars in the DMI and ADX calculation. The "DMI Smoothing Length" input controls the number of bars in the DMI smoothing calculation. Use a value of 1 for non-smoothed DMI data.

The sign of the DADX indicates the direction of price movements based on the difference between the smoothed DMI+ and DMI- values. The absolute value of the oscillator corresponds to the ADX, representing the trend strength.

The "Low Threshold" and "High Threshold" inputs define the ADX thresholds for categorizing trending, non-trending, and exhaustion states. The low threshold specifies the minimum absolute oscillator value required to indicate a trend, and the high threshold marks the absolute value where trend strength is excessive, possibly suggesting an upcoming consolidation or reversal. The indicator colors the histogram based on these thresholds and changes in the ADX, with brighter colors denoting a strengthening trend and darker colors signaling a weakening trend.

TASC 2024.11 Ultimate Strength Index█ OVERVIEW

This script implements the Ultimate Strength Index (USI) indicator, introduced by John Ehlers in his article titled "Ultimate Strength Index (USI)" from the November 2024 edition of TASC's Traders' Tips . The USI is a modified version of Wilder's original Relative Strength Index (RSI) that incorporates Ehlers' UltimateSmoother lowpass filter to produce an output with significantly reduced lag.

█ CONCEPTS

Many technical indicators, including the RSI, lag due to their heavy reliance on historical data. John Ehlers reformulated the RSI to substantially reduce lag by applying his UltimateSmoother filter to upward movements ( strength up - SU ) and downward movements ( strength down - SD ) in the time series, replacing the standard process of smoothing changes with rolling moving averages (RMAs). Ehlers' recent works, covered in our recent script publications, have shown that the UltimateSmoother is an effective alternative to other classic averages, offering notably less lag in its response.

Ehlers also modified the RSI formula to produce an index that ranges from -1 to +1 instead of 0 to 100. As a result, the USI indicates bullish conditions when its value moves above 0 and bearish conditions when it falls below 0.

The USI retains many of the strengths of the traditional RSI while offering the advantage of reduced lag. It generally uses a larger lookback window than the conventional RSI to achieve similar behavior, making it suitable for trend trading with longer data lengths. When applied with shorter lengths, the USI's peaks and valleys tend to align closely with significant turning points in the time series, making it a potentially helpful tool for timing swing trades.

█ CALCULATIONS

The first step in the USI's calculation is determining each bar's strength up (SU) and strength down (SD) values. If the current bar's close exceeds the previous bar's, the calculation assigns the difference to SU. Otherwise, SU is zero. Likewise, if the current bar's close is below the previous bar's, it assigns the difference to SD. Otherwise, SD is zero.

Next, instead of the RSI's typical smoothing process, the USI's calculation applies the UltimateSmoother to the short-term average SU and SD values, reducing high-frequency chop in the series with low lag.

Finally, this formula determines the USI value:

USI = ( Ult (SU) − Ult (SD)) / ( Ult (SU) + Ult (SD)),

where Ult (SU) and Ult (SD) are the smoothed average strength up and strength down values.

TASC 2024.07 Gaps and Extreme Closes█ OVERVIEW

This script, inspired by Perry Kaufman's article "Trading Opening Gaps and Extreme Closes in Stocks" from the TASC's July 2024 edition of Traders' Tips , provides analytical insights into stock price behaviors following significant price moves. The information about the frequency, pullbacks, and closing patterns of these extreme price movements can aid in developing more effective trading strategies by understanding what to expect during volatile market conditions.

█ CONCEPTS

Perry Kaufman's article investigates the behavior of stock prices following substantial opening gaps and extreme closing moves to identify patterns and expectations that traders can utilize to make informed decisions. The motivation behind the article is to offer traders a more scientific approach to understanding price movements during volatile market conditions, particularly during earnings season or significant economic events. Kaufman's analysis reveals that stock prices have a history of exhibiting certain behaviors after substantial price gaps and extreme closes. This script follows Perry Kaufman's study and helps provide insight into how prices often behave after significant price changes. This analysis can help traders establish price movement expectations and potential strategies for trading such occurrences.

█ CALCULATIONS

Input Parameters:

This script offers users the choice to analyze "Opening Gaps" or "Extreme Closes" for price movements of different predefined magnitudes in a specified direction ("Upward" or "Downward").

Outputs:

Based on the specified inputs, the script performs the following calculations for the active ticker displayed on the chart:

Frequency of Extreme Price Movements : Quantifies the occurrences of directional price movements within predefined percentage ranges.

Average Pullbacks : Computes the average retracement (pullback) from analyzed price movements within each percentage range.

Average Closes : Analyzes the typical closing behavior relative to the directional price movements within each range.

The script organizes the results from these calculations within the table on a separate chart pane, providing users with helpful insights into how a stock historically behaved following significant price movements.

TASC 2024.04 The Ultimate Smoother█ OVERVIEW

This script presents an implementation of the digital smoothing filter introduced by John Ehlers in his article "The Ultimate Smoother" from the April 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

The UltimateSmoother preserves low-frequency swings in the input time series while attenuating high-frequency variations and noise. The defining input parameter of the UltimateSmoother is the critical period , which represents the minimum wavelength (highest frequency) in the filter's pass band. In other words, the filter attenuates or removes the amplitudes of oscillations at shorter periods than the critical period.

According to Ehlers, one primary advantage of the UltimateSmoother is that it maintains zero lag in its pass band and minimal lag in its transition band, distinguishing it from other conventional digital filters (e.g., moving averages ). One can apply this smoother to various input data series, including other indicators.

█ CALCULATIONS

Ehlers derived the UltimateSmoother using inspiration from the design principles he learned from his experience with analog filters , as described in the original publication. On a technical level, the UltimateSmoother's unique response involves subtracting a high-pass response from an all-pass response . At very low frequencies (lengthy periods), where the high-pass filter response has virtually no amplitude, the subtraction yields a frequency and phase response practically equivalent to the input data. At other frequencies, the subtraction achieves filtration through cancellation due to the close similarities in response between the high-pass filter and the input data.

TASC 2024.03 Rate of Directional Change█ OVERVIEW

This script implements the Rate of Directional Change (RODC) indicator introduced by Richard Poster in the "Taming The Effects Of Whipsaw" article featured in the March 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Richard Poster discusses an approach to potentially reduce false trend-following strategy entry signals due to whipsaws in forex data. The RODC indicator is central to this approach. The idea behind RODC is that one can characterize market whipsaw as alternating up and down ZigZag segments. By counting the number of up and down segments within a lookback window, the RODC indicator aims to identify if the window contains a significant whipsaw pattern:

RODC = 100 * Segments / Window Size (bars)

Larger RODC values suggest elevated whipsaw in the calculation window, while smaller values signify trending price activity.

█ CALCULATIONS

• For each price bar, the script iterates through the lookback window to identify up and down segments.

• If the price change between subsequent bars within the window is in the direction opposite to the current segment and exceeds the specified threshold , the calculation interprets the condition as a reversal point and the start of a new segment.

• The script uses the number of segments within the window to calculate RODC according to the above formula.

• Finally, the script applies a simple moving average to smoothen the RODC data.

Users can change the length of the lookback window , the threshold value, and the smoothing length in the "Inputs" tab of the script's settings.

TASC 2024.02 Price-Time Filtering█ OVERVIEW

This script implements a price-time trend filter proposed by Alfred François Tagher in the “Trend Identification By Price And Time Filtering” article from the February 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Alfred François Tagher proposed a rule set designed to minimize the impact of stochastic price movements, facilitating the identification of larger-scale trends. The rules are:

• If the most recent week's close exceeds the previous week's high, the trend is up.

• If the most recent week's close is below the previous week's low, the trend is down.

• The trend remains unchanged until one of the above conditions occurs.

Similar rules can also apply to monthly bars.

The author argues that this approach integrates characteristics of conventional price action and time dynamics filters, so he refers to it as price-time filtering .

█ CALCULATIONS

This script applies the above price-time filtering rules and offers multiple ways to view the results on a chart:

• In the "Oscillator" view mode, the script counts and displays the number of bars in the uptrend and downtrend.

• In the "Linebreak" view mode, the trend filter is presented in a format resembling a point-and-figure (P&F) chart , with the length of each bar corresponding to the high-low range of the respective trend.

• In both view modes, the script offers bar coloring of the main chart based on the identified trend.

TASC 2023.12 Growth and Value Switching System█ OVERVIEW

This script implements a rotation system for trading value and growth ETFs, as developed by Markos Katsanos and detailed in the article titled 'Growth Or Value?' in TASC's December 2023 edition of Traders' Tips . The purpose of this script is to demonstrate how short-term momentum can be employed to track market trends and provide clarity on when to switch between value and growth.

█ CONCEPTS

The central concept of the presented rotation strategy is based on the observation that the stock market undergoes cycles favoring either growth or value stocks. Consequently, the script introduces a momentum trading system that is designed to switch between value and growth equities based on prevailing market conditions. Specifically tailored for long-term index investors, the system focuses on trading Vanguard's value and growth ETFs ( VTV and VUG ) on a weekly timeframe.

To identify the ETF likely to outperform, the script uses a custom relative strength indicator applied to both VTV and VUG in comparison with an index ( SPY ). To minimize risk and drawdowns during bear markets, when both value and growth experience downtrends, the script employs the author's custom volume flow indicator (VFI) and blocks trades when its reading indicates money outflow . Positions are closed if the relative strength of the current open trade ETF falls below that of the other ETF for two consecutive weeks and is also below its moving average. Additionally, the script implements a stop-loss when the ETF is trading below its 40-week moving average, but only during bear markets.

The script plots the relative strengths of the value and growth equities along with the signals triggered by the aforementioned rules. Information about the current readings of the relative strength and volume flow indicators, along with the current open position, is displayed in a table.

█ CALCULATIONS

The script uses the request.security() function to gather price data for both equities and the reference index. Custom relative strength and volume flow indicators are calculated based on the formulas presented in the original article. By default, the script employs the same parameters for these indicators as proposed in the original article for VTV and VUG on a weekly timeframe.

TASC 2023.11 VAcc█ OVERVIEW

The November 2023 edition of TASC's Traders' Tips features an article titled "VAcc: A Momentum Indicator Based On Velocity And Acceleration" by Scott Cong. This script implements the author's momentum indicator based on simple physics concepts.

█ CONCEPTS

The indicator is named VAcc as it is derived from the average velocity (V) and acceleration (Acc) over a specified lookback period. Consequently, its readings reflect two valuable characteristics of price data: rate (indicating the speed at which the price is moving) and rate of change (indicating whether the price is speeding up or slowing down).

In the article, the author reports that for longer periods, VAcc behaves similarly to the MACD , albeit with a more responsive nature. For shorter periods, VAcc exhibits characteristics reminiscent of the stochastic oscillator , but it trends more prominently and is less prone to overbought/oversold saturation.

To incorporate VAcc into trading strategies, the author suggests considering the following two permutations for the velocity and acceleration data series:

Strong upward condition: Velocity is rising, and acceleration is rising above zero.

Strong downward condition: Velocity is falling, and acceleration is falling.

In the current implementation, the chart displays the average velocity as a line, while the average acceleration is presented as a histogram.

█ CALCULATIONS

The calculation of VAcc involves the following steps:

For the current closing price, C , and for each bar C (i) within a specified lookback period from the current bar, the script calculates velocities, V (i) = ( C - C (i))/i. These velocities are then subjected to an exponential moving average to obtain the smoothed average velocity.

Similarly, for each bar within the lookback period, accelerations are calculated as Acc (i) = ( V - V (i))/i and then averaged without smoothing.

TASC 2023.10 COT Commercials Indicator█ OVERVIEW

This script implements the COT Commercials Indicator introduced by Alfred François Tagher in an article featured in TASC's October 2023 edition of Traders' Tips . The indicator is designed for use in futures markets and represents a fast stochastic (%K) calculated based on the commercial open interest values of an asset derived from the weekly Commitments Of Traders (COT) report .

█ CONCEPTS

The COT report, issued by the Commodity Futures Trading Commission (CFTC) , presents a breakdown of reportable open interest positions held by various trader groups—commercial, noncommercial, and nonreportable (small traders). Open interest reflects the total number of derivative contracts entered by market participants but not yet settled. Consequently, it can serve as a measure of market activity and liquidity.

The indicator showcased here aims to analyze changes in the reported net values of open interest for commercial traders/hedgers (often referred to as 'smart money', as they deal directly in underlying commodities). The net values are positive when the commercial traders have more long positions than short ones and negative when they hold more short positions than long ones. Positive net values indicate that commercial traders hold more long positions than short ones, while negative values indicate the opposite. Thus, overbought and oversold conditions of the COT Commercials Indicator potentially suggest collective bullish and bearish sentiments, respectively.

█ CALCULATIONS

The calculations involve these steps:

1. Net open interest values are extracted from COT data using the LibraryCOT library provided by TradingView.

2. A fast stochastic indicator (%K) is then applied to normalize these net values.

The script also provides an option of calculating and plotting the indicator curve for noncommercial (speculators) open interest.

TASC 2023.08 Channeling Your Inner Chartist█ OVERVIEW

TASC's August 2023 edition of Traders' Tips features an article written by Stella Osoba titled “Using Price Channels.” The article offers a basic look at using price channels, with a primary focus on Donchian channels . Following the article, the script provides an example of how to calculate and utilize the Donchian channel to gain insights into the price behavior and potential trend movements.

█ CONCEPTS

The use of price channels is a long-standing and fundamental charting technique commonly associated with trend-following trading strategies. Price channels help identify the trend on the chart and facilitate trading in its direction. The Donchian channel, in particular, consists of three lines. The upper line is conventionally calculated as the highest high over a specified lookback period, while the lower line is defined as the lowest low over the same period. The central line represents the midpoint between the upper and lower lines.

The Donchian channel provides a simple and intuitive visual representation of price behavior. Breaking through the lower line, for instance, can indicate weakness and selling pressure, while breaking through the upper line can signal buying pressure. By observing these breakout points, one can gain insight into potential beginnings or endings of long-term trends. However, it is important to note that breakouts often lead to price reversals, so they should be carefully evaluated

█ CALCULATIONS

To illustrate a simple Donchian trading system, this script calculates and plots the channel lines, as well as potential entry points for long positions (green triangles) and short positions (red triangles).

TASC 2023.07 Keeping With The Larger Trend█ OVERVIEW

TASC's July 2023 edition of Traders' Tips features an article by Barbara Star titled "Stay On Track With The Supertrend Indicator". The article explores how the supertrend indicator , whether used as a standalone tool or in conjunction with other indicators, can assist traders in aligning with the larger trend. Drawing inspiration from the article, this script enhances the supertrend indicator with additional visual and analytical features, making it easier to analyze the readings and make informed trading decisions.

█ CONCEPTS

Over the past few years, the supertrend indicator has gained significant popularity among traders. Unlike moving averages, it incorporates both price and volatility information, enabling traders to navigate upward or downward trends despite occasional price disruptions.

When using the supertrend indicator, a trader may consider entering a long position when the price surpasses the supertrend line or retraces to it after the initial crossover. Similarly, for short positions, a trader could enter when the price drops below the supertrend line or retests it. Exiting these positions can be triggered by the opposite scenario, such as a price drop below the supertrend line for long positions or a price rise above the supertrend line for short positions. To assist in monitoring the distance between the price and the indicator line, this script introduces the following display features:

Breach levels, representing fractions of the most recent maximum distance.

On-chart signals indicating crossings of the highest and lowest breach levels.

An infobox displaying the average value of the maximum distance.

█ CALCULATIONS

For calculating the supertrend line, this script uses the built-in function ta.supertrend() . Additionally, the script showcases the use of state-of-the-art PineScript® functionality, including methods and tables .

TASC 2023.06 Stochastic Distance Oscillator█ OVERVIEW

This script implements the stochastic distance oscillator (SDO) , a momentum indicator introduced by Vitali Apirine in an article featured in TASC's June 2023 edition of Traders' Tips . The SDO is a variation of the classic stochastic oscillator and is designed to identify overbought and oversold levels, as well as detect bull and bear trend changes.

█ CONCEPTS

Unlike the classic stochastic oscillator, which compares an asset's price to its past price range, the SDO measures the size of the current distance relative to the maximum-minimum distance range over a set number of periods. The current distance is defined as the distance between the current price and the price n periods ago.

The readings of the SDO can be used to identify the following states of the asset price:

Uptrend state: the oscillator crosses over 50 from a non-uptrend state.

Downtrend state: the oscillator crosses under -50 from a non-downtrend state.

Overbought state: the oscillator is in an uptrend and crosses -50 for the first time.

Oversold state: the oscillator is in a downtrend and crosses 50 for the first time.

Trend continuity: the oscillator crosses 0 in the direction of the current trend.

The script indicates these five conditions using on-chart signals and background coloring.

█ CALCULATIONS

The SDO is calculated as follows:

1. Calculate the distance between the current price and the price n periods ago, as well as the maximum and minimum distances for the selected lookback period. The author recommends using one of two values of n , 14 or 40 bars.

2. Calculate the time series % D that represents the relation between the asset's current distance and its distance range over a loockback period:

% D = (Abs(current distance) − Abs(minimum distance)) / (Abs(maximum distance) − Abs(minimum distance)) * 100

3. Use the calculated % D to obtain the SDO:

If the closing price is above the close n periods ago, SDO = % D

If the closing price is below the close n periods ago, SDO = −% D

If the closing price equals the close n periods ago or the current distance equals the minimum distance, SDO = 0

4. Smooth the SDO using an exponential moving average (EMA). The author recommends using an EMA in the range from 3 to 6 .

Adjustable input parameters include the number of periods n , the lookback period for calculating % D , the smoothing EMA length, and the overbought/oversold threshold level.

TASC 2023.05 Cong Adaptive Moving Average█ OVERVIEW

TASC's May 2023 edition of Traders' Tips features an article titled "An Adaptive Moving Average For Swing Trading" by Scott Cong. The article presents a new adaptive moving average (AMA) that adjusts its parameters automatically based on market volatility. The AMA tracks price closely during trending movements and remains flat during congestion areas.

█ CONCEPTS

Conventional moving averages (MAs) use a fixed lookback period, which may lead to limited performance in constantly changing market conditions. Perry Kaufman's adaptive moving average , first described in his 1995 book Smarter Trading, is a great example of how an AMA can self-adjust to adapt to changing environments. Scott Cong draws inspiration from Kaufman's approach and proposes a new way to calculate the AMA smoothing factor.

█ CALCULATIONS

Following Perry Kaufman's approach, Scott Cong's AMA is calculated progressively as:

AMA = α * Close + (1 − α) * AMA(1),

where:

Close = Close of the current bar

AMA(1) = AMA value of the previous bar

α = Smoothing factor between 0 and 1, defined by the lookback period

The smoothing factor determines the performance of AMA. In Cong's approach, it is calculated as:

α = Result / Effort,

where:

Result = Highest price of the n period − Lowest price of the n period

Effort = Sum(TR, n ), where TR stands for Wilder’s true range values of individual bars of the n period

n = Lookback period

As the price range is always no greater than the total journey, α is ensured to be between 0 and 1.

TASC 2023.04 Undersampled Double MA█ OVERVIEW

TASC's April 2023 edition of Traders' Tips features an article entitled "Just Ignore Them: Undersampling The Data As A Smoothing Technique" by John Ehlers, which explores a method for reducing noise through data sampling. This script implements the article's proposed Undersampled Double MA indicator.

█ CONCEPTS

The conventional approach to reducing the impact of noise in the market data on trading rules is to use smoothing filters like moving averages. However, John Ehlers suggests that changing the sample rate of the datastream is a simple and effective way to smooth the data and reduce noise. Specifically, he argues that undersampling the data removes high-frequency components contributing to noisiness. Notably, the elimination of these components produces less lag than that of conventional smoothing filters.

The Undersampled Double MA indicator implemented in this script represents a practical application of smoothing with undersampling. It samples the data at a given rate (for instance, once every five bars, as suggested by Ehlers), then processes the resulting data using a Hann window filter with two different periods, producing two smooth data streams that traders can use in the same way as the combination of two conventional moving averages of different lengths (i.e., fast and slow MAs).

█ CALCULATIONS

The script samples data once every N th bar (by default, N = 5) and smooths the undersampled data with 6-period and 12-period Hann filters, which it plots on the main chart. Users can adjust the sampling period and the periods of each Hann filter to their liking from the inputs in the script settings.

TASC 2023.03 Every Little Bit Helps - Special EditionMy first Published contribution.

Gracious thank you to all Pine Coders,

this has subtle features that have multiple shifts based on inputs.

with some experimentation, one might try pushing other sources

at the hue dials and see more dynamic indication.

for John Ehlers article

TASC Magazine This Month.

- Special Edition.

TASC 2023.03 Every Little Bit Helps█ OVERVIEW

TASC's February 2023 edition of Traders' Tips includes an article titled "Every Little Bit Helps: Averaging The Open And Close To Reduce Noise" by John Ehlers. This code implements the numerical example from this article.

█ CONCEPTS

Using theories from digital signal processing as a starting point, John Ehlers argues that using the average of the open and close as the source time series of an indicator instead of using only the closing price can often lead to noise reduction in the output. This effect especially applies when there is no gap between the current bar's opening and the previous bar's closing prices. This trick can reduce noise in many common indicators such as the RSI, MACD, and Stochastic.

█ CALCULATIONS

Following the example presented in the original publication, this script illustrates the proposed strategy using the Relative Strength Index (RSI) as a test indicator. It plots two series:

RSI calculated using only closing prices as its source.

RSI of the same length as the first, but calculated using the average of open and close prices as its source, i.e. (open+close)/2 .

This script demonstrates that using the average of open and close as the calculation source results in a smoother indicator. To visually emphasize the advantage of this proposed trick, the script's color scheme is sensitive to both the RSI value and the difference between the two RSI data streams.

TASC 2023.01 TRAdj EMA█ OVERVIEW

TASC's January 2023 edition of Traders' Tips includes an article titled "True Range Adjusted Exponential Moving Average (TRadj EMA)" by Vitali Apirine. This code implements the indicator presented in that publication.

█ CONCEPTS

The True Range Adjusted Exponential Moving Average (TRAdj EMA) is a trend-following indicator that considers volatility for a quicker response to price changes. It is an EMA that modulates its weighting factor based on the true range (TR) of the asset.

In a trading strategy, traders can use a TRAdj EMA in tandem with an EMA of the same length to identify an asset's trend, or they can use it alongside another TRAdj EMA of a different length to identify turning points and filter price movements.

█ CALCULATIONS

The following steps are performed to calculate the indicator:

• Calculate the asset's TR according to the standard definition proposed by J. Welles Wilder, Jr.

• Define the true range adjustment factor as:

TRAdj =( Current TR − Minimum TR) ⁄ ( Maximum TR − Minimum TR ),

where Maximum TR and Minimum TR are the maximum and minimum TR values over the specified lookback period .

• Calculate the TRAdj EMA in the same manner as a traditional EMA, but with a weighting factor defined as:

2*(1 + TRAdj * Multiplier ) ⁄ ( EMA length + 1),

where Multiplier is an input parameter that ranges from 5 to 10. For comparison, a traditional EMA uses a weighting factor of 2 ⁄ ( EMA length + 1).

TASC 2022.12 Short-Term Continuation And Reversal Signals█ OVERVIEW

TASC's December 2022 edition Traders' Tips includes an article by Barbara Star titled "Short-Term Continuation And Reversal Signals". This is the code that implements the concepts presented in this publication.

█ CONCEPTS

The article takes two classic indicators, the Commodity Channel Index (CCI) and the Directional Movement Indicator (DMI), makes changes to the traditional ways of visualizing their readings, and uses them together to generate potential signals. The author first discusses the benefits of converting the DMI indicator to an oscillator format by subtracting the −DI from the +DI, which is then displayed as a histogram. Next, the author shows how the use of an on-chart visual framework (i.e., choosing the line style and color, coloring price bars, etc.) can help traders interpret the signals produced the considered pair of indicators.

█ CALCULATIONS

The article offers the following signals based on the readings of the DMI and CCI pair, suitable for several types of trades:

• Short-term trend change signals:

A DMI oscillator above zero indicates that prices are in an uptrend. A DMI oscillator below the zero line and falling means that selling pressure is dominating and price is trending down. The sign of the DMI oscillator is indicated by the color of the price bars (which correlates with the color of the DMI histogram). Namely, green, red and grey price bars correspond to the DMI oscillator above, below and equal to zero . Colored price bars and the DMI oscillator make it easy for trend traders to recognize changes in short-term trends.

• Trend continuation signals:

Blue circles appear near the bottom of the oscillator chart border when the DMI is above the zero line and the price is above its simple moving average in an uptrend . Dark red circles appear near the top of the chart in a downtrend when the DMI oscillator is below its zero line and below the 18-period moving average. Trend continuation signals are useful for those looking to add to existing positions, as well as for traders waiting for a pullback after a trend has started.

• Reversal signals:

The CCI signals a reversal to the downside when it breaks out of its +100 and then returns at some point, crossing below the +100 level. This is indicated by a magenta-colored diamond shape near the top the chart. The CCI signals a reversal to the upside when it moves below its −100 level and then at some point comes back to cross above the −100 level. This is indicated by a yellow diamond near the bottom of the chart. Reversal signals offer short-term rallies for countertrend traders as well as for swing traders looking for longer-term moves using the interplay between continuation and reversal signals.

TASC 2022.11 Phasor Analysis█ OVERVIEW

TASC's November 2022 edition Traders' Tips includes an article by John Ehlers titled "Recurring Phase Of Cycle Analysis". This is the code that implements the phasor analysis indicator presented in this publication.

█ CONCEPTS

The article explores the use of phasor analysis to identify market trends.

An ordinary rotating phasor diagram is a two-dimensional vector, anchored to the origin, whose rotation rate corresponds to the cycle period in the price data stream. Similarly, Ehlers' phasor is a representation of angular phase rotation along the course of time. Its angle reflects the current phase of the cycle. Angles -180, -90, +90 and +180 degrees correspond to the beginning, valley, peak and end of the cycle, respectively.

If the observed cycle is very long, the market can be considered trending . In his article, John Ehlers defined trending behavior to occur when the derived instantaneous cycle period value is greater that 60 bars. The author also introduced guidelines for long and short entries in a trending state. Depending on the tuning of the indicator period input, a long entry position may occur when the phasor angle is around the approximate vicinity of −90 degrees, while a short entry position may occur when the phasor angle will be around the approximate vicinity of +90 degrees. Applying these definitive guidelines, the author proposed a state variable that is indicated by +1 for a trending long position, 0 for cycling, and −1 for a trending short position (or out).

The phasor angle, the cycle period, and the state variable are made available with three selectable display modes provided for this TradingView indicator.

█ CALCULATIONS

The calculations are carried out as follows.

First, the price data stream is correlated with cosine and sine of a fixed cycle period. This produces two new data streams that correspond to the projections of the frequency domain phasor diagram to the horizontal (so-called real ) and vertical (so-called imaginary ) axis respectively. The wavelength of the cycle period input should be set for the midrange vicinities of the phasor to coincide with the peaks and valleys of the charted price data.

Secondly, the phase angle of the phasor is easily computed as the arctangent of the ratio of the imaginary component to the real component. The difference between the current phasor values and its last is then employed to calculate a derived instantaneous period and market state. This computation is then repeated successively for each individual bar over the entire duration of the data set.