Supertrend LSMA long StrategyThis is a long strategy which combines Super trend indicator with LSMA moving average.

In general it tends to works better with long trending markets such as stocks and cryptos using a big timeframe.

The rules are simple

Long entry:

Supertrend is telling us to go long and close of a candle is above moving average

Long exit:

Supertrend is telling us to go short

IF you have any questions, let me know !

Trend

Pivot Reversal strategy long onlyPivot Point Reversal Strategy

Pivot point reversal strategy is based on the first support level’s price action during the bullish trend and the first resistance level during the bearish trend . Traders follow the main trend and enter into the trade after reversal analyzing pivot point levels.

This version is an upgraded version, combining the initial pivot point reversal strategy together with one of the most accuracy moving average in my opinion for day trade, the Least square moving average.

At the same time I applied an option to backtest using a date range and a leverage calculator.

The default options are optimized for BTC /USDT 2H charts, using 0.1% comission fee.

If you have any questions, let me know

Vwap mtf Swing Stock StrategyThis is a trending strategy designed for stock market, especially long trending assets such as TSLA, NIO, AMAZON and so on.

Its made of volatility bands and weekly VWAP, in this case daily and weekly.

This strategy has been adapted to go long only.

Rules for entry

For long , we want to enter close of a candle is above vwap weekly, and at the same time the close of a candle cross-under the lower volatility band.

For exit , we want to enter close of a candle is below vwap weekly, and at the same time the close of a candle cross-over the upper volatility band.

This strategy does not have a risk management inside, so use it with caution.

If you have any questions, let me know !

Ichimoku + RSI Crypto trending strategyThis is a crypto trending strategy designed for big timeframes such as 3-4h+.

Its components are:

RSI

ICHIMOKU full pack

Heikin Ashi candles for logic calculation inside

Rules for entry.

For long : we have a long cross condition on ichimoku and price is above the ichimoku lines, and at the same time RSI value is > 50.

For long : we have a short cross condition on ichimoku and price is below the ichimoku lines, and at the same time RSI value is < 50.

Rules for exit

We exit whenever we receive an opposite signal of the initial entry.

SInce this strategy is using no risk management inside, I recommend to be careful with it .

If you have any questions, let me know !

3 RSI 6sma/ema ribbon crypto strategyThis is a very efficient swing trading strategy designed for crypto long timeframes like 2h+.

Initially we have 3 RSI .

AFter that we use them as source for 6 SMA/EMA for each RSI, 5, 30, 50, 70, 90, 100. With those we create a ribbon that we are going to use in order to check the direction of the trend.

Rules for entry:

For long : if either all the SMA/EMA's from the 2nd RSI are telling us to go long, or all the all SMA/EMA's from the 3rd rsi are telling us to go long F

For short : if either all the SMA/EMA's from the 2nd RSI are telling us to go short, or all the all SMA/EMA's from the 3rd rsi are telling us to go short

We exit when we get an opposite condition than the entry one.

Caution: this strategy has no risk management inside, so use it with caution. If you have any questions , let me know !

Momentum Trading By Mahfuz AzimA following indicator is Momentum Trading that uses fast QQE crosses with Moving Averages

Use for trend direction filtering. QQE or Qualitative Quantitative Estimation is based

Relative strength index (RSI), but uses a smoothing technique as an additional transformation. Three crosses can be selected (all selected by default)

Stochastic Optimized Trend Tracker *Strategy*Stochastic OTT is Anıl Özekşi's latest derived version of Optimized Trend Tracker on Stochastic Oscillator.

He tried to solve the fake signals of Stochastic Oscillator by adopting OTT on the indicator.

He advised users to set the stochastic smoothing parameters to 500 and 200 on his latest video about SOTT.

He personally uses 1 min charts on stock market so the parameters of the indicator might have to be optimized for other time frames nad markets.

He exaggerated the Stochastic to 1000's to have better signals of percent values of OTT .

Also hes used VIDYA in both calculations of OTT and Stochastic smoothing.

Said, Kıvanç Özbilgiç.

I just made a Strategy version of the script so that we lads can backtest it. The codes for that are yet again from Kıvanç Özbilgiç :) I just copy-pasted a few and did some adjustments. Hope you enjoy!

#betonyetmez

TEMA Cross +HTF BacktestThis is a follow up to a previous script release called " TEMA Cross Backtest ".

This new strategy uses two TEMA crosses, one for trend direction, one for entry and exit. The entry and exit parameters are the same as the previous script. The trend direction is based on a user configurable higher timeframe TEMA cross which determines when to take longs or shorts. When the indicator is purple, it is looking for shorts, and when it is yellow, it is looking for longs. The background of the chart is colored accordingly to see the trend direction at a glance.

The default settings are the ones I have found produce the highest backtest results. The backtest is set by default to use a $500 account, and use $500 for every entry and exit, no matter the direction or overall profit/loss.

Parts of script borrowed from other public scripts.

RSI Trend CryptoDear community,

Today I want to present you one of my favorite and simple trading bots: The RSI Trend.

This bot is based on the RSI, which normally is used as a trend reversal indicator. However, here it’s used as a trend finding indicator, often with great success. This bot making long-only trades, which is quite successful in bull-markets like the one we’re currently in.

In case you want to use an emergency exit for your trade, toggle the Emergency Exit parameter. During bull-markets it’s better in the long term to keep this option off.

Currently the bot only makes one trade at a time (pyramiding = 1), for higher risk and higher rewards you can increase this parameter. More than 5 is not advised.

I’ve optimized this bot on 15min time frame. It has some decent results for most cryptos on this TF, feel free to test this out.

In case you want to hook this bot up to your exchange, feel free to edit the ALERT messages in the code.

Default Trading Rules:

Long: RSI crosses over 35

Close Long: RSI crosses under 75

Emergency Exit: RSI crosses under 10

ELIA MULTI INDICATORS STRATEGYExperimental multi indicators strategy, to catch right entry and avoid noise.

Each indicator included in the strategy, assume a value based on its status and because is a trend-follow strategy, some indicator value are higher then the other

Backtested on ETHUSDTPERP

BINANCE:ETHUSDTPERP

Combo Backtest 123 Reversal & Modified Price-Volume Trend This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from

Stocks & Commodities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Bollinger Band with Fib Golden Ratio (0.618)This startegy uses Fib level (0.618) of Bollinger Band for long entry. I find this is the only strategy which gives similar results on the different time frames. I have tested QQQ for 1H, 2H , 3H and 4H charts , all showed over 70% winning rate.

BB settings 50 , mult 1.5 (or you can use 2.5 or 3 )

Note: for the basis I have used VWMA instead of SMA .

BUY

=========

ema 50 is above ema 200

when the price close or low touches BB50(Fib0.615) lower band

Exit

=========

when the price crossover BB50(Fib0.615) upper band

Stop Loss

=========

Stop oss set to 5% , configurable

Strategy works similar to mean reversion style. When it touches the lower bans (which 0.615 level of the BB50) , it bounces from there.

Warning

=========

This strategy is for educational purposes only. Please do your own reserach for trading decissions.

Donchian Channels Strategy by KrisWatersDoncian Channels is a trend tracking indicator developed by Richard Doncian. The upper line of the channel is determined by the highest value seen by the price in the defined period, the lower line of the channel is determined by the lowest value seen by the price in the defined period. The middle line takes the average value of the lower and upper channels.

Strategy Settings:

- Can apply only LONG positions.

- Can apply only SHORT positions.

- Use LONG/SHORT both.

- You can use ATR as a second exit condition. If ATR stop disabled, Donchian upper or lower channel value is use for the exit rule to long and short positions.

Strategy can be able to optimize by changing channel lengths and timeframe.

Twin Optimized Trend Tracker Strategy TOTTAnıl Özekşi's new strategy which is a combination of 2 Optimized Trend Tracker lines which are vertical displaced from original version with a COEFFICIENT to cope with sideways' false signals which he explained in "Toy Borsacı İçin OTT Kullanım Kılavuzu 2"

original version of OTT:

OTT Strategy and Screener:

You can find a detailed explanation with subtitles from the developer of OTT Anıl Özekşi himself as: "Toy Borsacı İçin OTT Kullanım Kılavuzu 2"

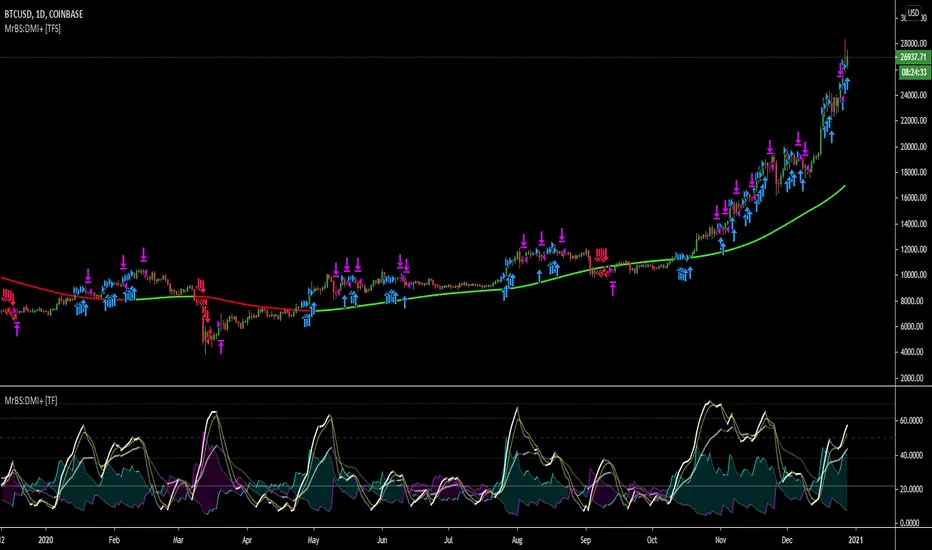

MrBS:Directional Movement Index [Trend Friend Strategy]This goes with my MrBS:DMI+ indicator. I originally combined them into one, but then you cannot set alerts based on what the ADX and DMI is doing, only strategy alerts, so separate ones have more flexibility and uses.

Indicator Version is found under "MrBS:Directional Movement Index " ()

//// THE IDEA

The majority of profits made in the market come from trending markets. Of course there are strategies that would say otherwise but for the majority of people, THE TREND IS YOUR FRIEND (until the end). The idea is to follow the trend, entering once it has established its self and exiting positions when the trend weakens. This strategy gives a rough idea of the returns produced from following purely the ADX signals. At first Heikin Ashi values were used for the calculation but the results show it's not that effective. The functionality to switch between calculation types has been left in, so we can uses HA candle data to generate signals from while looking at an OHLC chart, if we want to experiment. Due to the way strategies work, we are unable to get reliable results when running the strategy on the HA chart even if we are calculating the signals from the real OHLC values. It is best to always run strategies on standard charts.

When using this strategy, I look for confirmation of the signal based on stochastic (14:3:6) direction, reversal level of stochastic, and divergance, to add confidence and adjust position size accordingly. I am going to try and code some version of that in future updates, if anyone can help or has suggestions please drop me a message.

//// INDICATOR DETAILS

- The default settings are for optimized Daily charts, for 4 hour I would suggest a smoothing of 2.

- The default values used for calculation are the Real OHLC, we can change this to Heikin Ashi in the menu.

- The strategy enters a position when ADX crosses the threshold level, and closes the position when ADX starts to fall.

- There is a signal filter in the form of a 377 period Hull Moving Average, which the price must be above or bellow for long and short positions respectively.

- The strategy closes the position when a cross-under of the ADX and its 4 period EMA. This is an attempt to stay into positions longer as sometimes the ADX will fall for 1 bar and then keep rising, while the overall trend is strong. The downside to this is that we exit trades later and this affects our max drawdown.

Pyramiding Entries On Early Trends (by Coinrule)Pyramiding the entries in a trading strategy may be risky but at the same time very profitable with a proper risk management approach. This strategy seeks to spot early signs of uptrends and increase the position's size while the right conditions persist.

Each trade comes with its stop-loss and take-profit to enforce a proportional risk/reward profile.

The strategy uses a mix of Moving Average based setups to define the buy-signal.

The Moving Average (200) is above the Moving Average (100), which prevents from buying when the uptrend is already in its late stages

The Moving Average (9) is above the Moving Average (100), indicating that the coin is not in a downtrend.

The price crossing above the Moving Average (9) confirms the potential upside used to fire the buy order.

Each entry comes with a stop-loss and a take-profit in a ratio of 1-to-1. After over 400 backtests, we opted for a 3% TP and 3% SL, which provides the best results.

The strategy is optimized on a 1-hour time frame.

The Advantages of this strategy are:

It offers the possibility of adjusting the size of the position proportionally to the confidence in the possibilities that an uptrend will eventually form.

Low drawdowns. On average, the percentage of trades in profit is above 60%, and the stop-loss equal to the take-profit reduces the overall risk.

This strategy returned good returns both with trading pairs with Fiat/stable coins and with BTC. Considering the mixed trends that cryptocurrencies experienced during 2020 vs BTC, this strengthens the strategy's reliability.

The strategy assumes each order to trade 20% of the available capital and pyramids the entries up to 7 times.

A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

OCC Trend Combo 1 day BTC MoonflagRuns on BTC 1 DAY (NOTE USE THIS NOT THE PREVIOUS VERSION - DEFAULTS TUNED TO 1 day BTC HERE)

USE DEFAULT SETTINGS

The strategy is to maximise the profit for OCC longs (ALMA algo)

Longs start when the price action settles around the ALMA OCC, then typically breaks up

Then follow the trend indcator (blue/orange)

Shorts normally happen when the price action crosses below the ALMA OCC, although these initiate faster than the 1 day time setting - so watchout for shorts - are harder to predict than longs

So this catches most of the big move longs at their initiation

trend Screener List1This is type of custom screener I searched and made to screen bulk stocks any one can modify it, other may get help out of it.

in my code i have made defined

1. uptrend= ema(close,55)> ema(close,144) and ema(close,144)> ema(close,388) and ema(close,388)> ema(close,576) and close>ema(close,388)

2. downtrend = ema(close,55)< ema(close,144) and ema(close,144)< ema(close,388) and ema(close,388)<ema(close,576) and close<ema(close,388)

if the indicator is printing DOWNTREND=TRUE or UPTREND=TRUE then the corresponding stock is in currently in that trend out of the stocks listed in the code

in one code only 40 (max) stocks can be called.

to add more stocks I copied same code and changed the stocks in the code, now you can screen 80 stocks at a time.

This code runs on each bar and checks if the stocks is in uptrend or down trend.

you can customize this screener according to your requirement.

//thanks @QuantNomad from where i solved my problem of screening my top stock for custom trend screener

//idea and motivation taken from

after adding another code you can screen 80 stocks at a time and so on , below following link is how it will look like

Catch the Big FishVolume based script to catch a big move. Works best on 5 min timeframe.

The default sma duration for volume is set to 150 = number of candles in 5 mins timeframe for 2 days.

Heavy volume is defined as = more than 9 times of sma.

Both parameters are configurable.

Trading strategy: Long buy at high / Short sell at low of the candle where the script gives the signal.

Important note regarding SL - for Long / Short positions respectively, the SL should be placed at low / high of previous candle, and NOT of the same candle.

SuperTREX strategyThis is the strategy of Super Trex that i put as open source before

i just add option for non security MTF and take profit steps as i shown before

for different coins or assets you need to set different parameters

Wilder's Volatility Trailing Stop Strategy with various MA'sFor Educational Purposes. Results can differ on different markets and can fail at any time. Profit is not guaranteed.

This only works in a few markets and in certain situations. Changing the settings can give better or worse results for other markets. This strategy is based on Wilder's Volatility System. It is an ATR trailing stop that is used for long term trends. This strategy focuses on the trailing stop alone and goes long and short only when it goes above or below the trailing line. It is similar to Donchian channels except it does not include the certain period channel breakout, only the trailing signal. This is only the trailing stop and an attempt to show how well it works standalone as Wilder described.

In his book, Wilder recommends a multiplier of 2.8-3.1 and an ATR lookback of 7 periods along with a running moving average or otherwise known as Wilder's moving average. The calculation and programming part for the trailing stop varies everywhere. I opted to keep it as simple and accurate as I could think of and interpret from the book. The variations to these types of indicators are numerous unfortunately, but Wilder seems to be the original author of ATR and this ATR-based trailing stop. In his book he says to use the significant closing price or highest/lowest closing price for the calculation part but I also included the option of choosing the highest high and lowest low, and the option to choose various moving averages in case anyone wants to experiment.

Comparing this and Donchian channels, it seems that a 2.5 multiplier is somewhat similar to the middle band of DCs and a 3.0 multiplier is somewhat similar to a double length middle band of DCs. It's hard to say which is the better trailing stop for a long term strategy. It's hard to beat the simplicity of DCs but maybe some might find a need for more inputs in a trailing stop or maybe an ATR based one like Wilder's can work better depending on what setting or strategy it's used in.

The Lazy Trader - Index (ETF) Trend Following Robot50/150 moving average, index (ETF) trend following robot. Coded for people who cannot psychologically handle dollar-cost-averaging through bear markets and extreme drawdowns (although DCA can produce better results eventually), this robot helps you to avoid bear markets. Be a fair-weathered friend of Mr Market, and only take up his offer when the sun is shining! Designed for the lazy trader who really doesn't care...

Recommended Chart Settings:

Asset Class: ETF

Time Frame: Daily

Necessary ETF Macro Conditions:

a) Country must have healthy demographics, good ratio of young > old

b) Country population must be increasing

c) Country must be experiencing price-inflation

Default Robot Settings:

Slow Moving Average: 50 (integer) //adjust to suit your underlying index

Fast Moving Average: 150 (integer) //adjust to suit your underlying index

Bullish Slope Angle: 5 (degrees) //up angle of moving averages

Bearish Slope Angle: -5 (degrees) //down angle of moving averages

Average True Range: 14 (integer) //input for slope-angle formula

Risk: 100 (%) //100% risk means using all equity per trade

ETF Test Results (Default Settings):

SPY (1993 to 2020, 27 years), 332% profit, 20 trades, 6.4 profit factor, 7% drawdown

EWG (1996 to 2020, 24 years), 310% profit, 18 trades, 3.7 profit factor, 10% drawdown

EWH (1996 to 2020, 24 years), 4% loss, 26 trades, 0.9 profit factor, 36% drawdown

QQQ (1999 to 2020, 21 years), 232% profit, 17 trades, 3.6 profit factor, 2% drawdown

EEM (2003 to 2020, 17 years), 73% profit, 17 trades, 1.1 profit factor, 3% drawdown

GXC (2007 to 2020, 13 years), 18% profit, 14 trades, 1.3 profit factor, 26% drawdown

BKF (2009 to 2020, 11 years), 11% profit, 13 trades, 1.2 profit factor, 33% drawdown

A longer time in the markets is better, with the exception of EWH. 6 out of 7 tested ETFs were profitable, feel free to test on your favourite ETF (default settings) and comment below.

Risk Warning:

Not tested on commodities nor other financial products like currencies (code will not work), feel free to leave comments below.

Moving Average Slope Angle Formula:

Reproduced and modified from source:

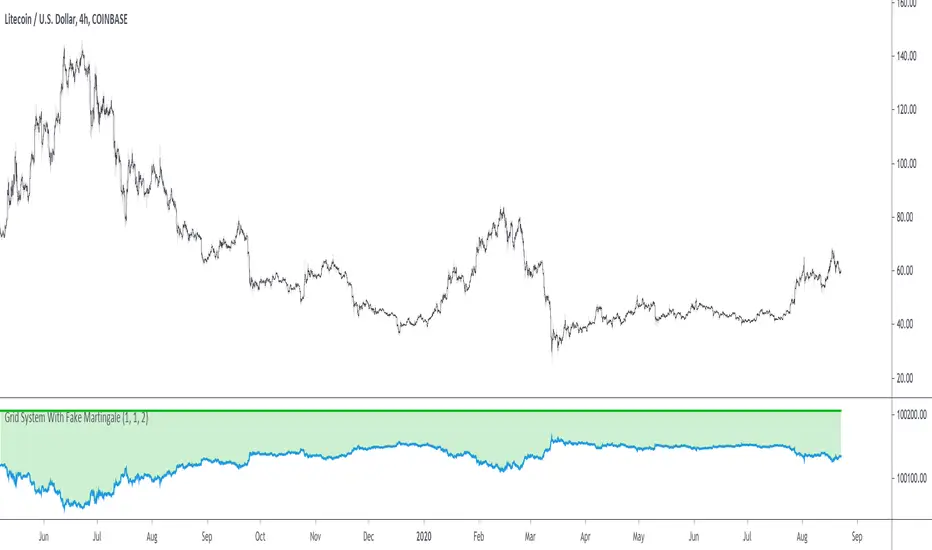

Grid System With Fake MartingaleThe proposed strategy is based on a grid system with a money management that tries to replicate the effect of a martingale without having to double your position size after each loss, hence the name "fake martingale". Note that a balance using this strategy is still subject to exponential decay, the risk is not minimized, as such, it would be dangerous to use this strategy.

For more information on the martingale and grid systems see:

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the security you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, generating fewer trades as a result.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after each win.

How It Works

Let's illustrate how we replicate a martingale without doubling our exposure with a simple casino example. Imagine you are playing roulette, and that you are betting on colors (black/red), your payout is 1 to 1, in the case you win, you will have your initial stake back plus a profit equal to your initial stake.

If your strategy is to recover any previous losses, you can double your stake each time you lose, once you win you will get back the previous losses plus a profit equal to your original stake, this is the martingale system. So how can we win back previous losses without having to double our stake? We could do that by doubling the payout ratio after a loss, so after a loss, we must use a payout ratio of 2:1, if we lose once again we must use a payout of 4:1...etc, our payout ratio would be subject to exponential growth instead of our stake.

Of course, the payout ratio is fixed with casino games, but in trading, we can manipulate the position of our take profit in order to replicate such effect, this is what this strategy is doing. So after a loss, we place our take profit such that a win recover our losses back plus generate a profit.

Advantages

The advantage of this approach is that unlike the martingale we don't double our position size, which instead can remain constant, this is a huge advantage as a martingale will require a significant capital in order to tank a series of losses.

Disadvantages

The main disadvantage of this method is that the price might never reach our take profit after a long losing streak, our balance would remain in the red and we couldn't do anything about it except reset the strategy.

Frictional costs are still a disadvantage, as such, we would need to place our take profits in order to account for them, while this is still better than purchasing additional shares, it minimizes the chances of the price reaching the take profit.

Conclusions

An alternative money management system replicating the effect of a martingale as been presented, we can see that such a system is far from being perfect, and it would be foolish to use it, however, it stills offer a convenient alternative to less aggressive progressive position sizing systems.

I have been receiving some messages from users criticizing me for exposing the martingale money management system, and I understand why but I can't agree, talking about it allow me to warn users against it, the grid-martingale methodology is will create more harm than anything else, the reward is only one side of the story and should always be compared against the risk, so always take a look at all the statics in a backtest.

Thanks for reading!

Shout-Out

This post was made possible thanks to my patrons:

@Happymono, @AmariMars, @kkhaial, @Nugehe, @LucF, @Nosmok, @iflostio, @DankBeans, @ecletv, @Neverstorm, @alex.crown.jr, @uk503, @xkingshotss, @vsov, @jbelka, @yatrader2, @hughza, @ganh