BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

Volatility

Follow Line Strategy Version 2.5 (React HTF)Follow Line Strategy v2.5 (React HTF) - TradingView Script Usage

This strategy utilizes a "Follow Line" concept based on Bollinger Bands and ATR to identify potential trading opportunities. It includes advanced features like optional working hours filtering, higher timeframe (HTF) trend confirmation, and improved trend-following entry/exit logic. Version 2.5 introduces reactivity to HTF trend changes for more adaptive trading.

Key Features:

Follow Line: The core of the strategy. It dynamically adjusts based on price breakouts beyond Bollinger Bands, using either the low/high or ATR-adjusted levels.

Bollinger Bands: Uses a standard Bollinger Bands setup to identify overbought/oversold conditions.

ATR Filter: Optionally uses the Average True Range (ATR) to adjust the Follow Line offset, providing a more dynamic and volatility-adjusted entry point.

Optional Trading Session Filter: Allows you to restrict trading to specific hours of the day.

Higher Timeframe (HTF) Confirmation: A significant feature that allows you to confirm trade signals with the trend on a higher timeframe. This can help to filter out false signals and improve the overall win rate.

HTF Selection Method: Choose between Auto and Manual HTF selection:

Auto: The script automatically determines the appropriate HTF based on the current chart timeframe (e.g., 1min -> 15min, 5min -> 4h, 1h -> 1D, Daily -> Monthly).

Manual: Allows you to select a specific HTF using the Manual Higher Timeframe input.

Trend-Following Entries/Exits: The strategy aims to enter trades in the direction of the established trend, using the Follow Line to define the trend.

Reactive HTF Trend Changes: v2.5 exits positions not only based on the trade timeframe (TTF) trend changing, but also when the higher timeframe trend reverses against the position. This makes the strategy more responsive to larger market movements.

Alerts: Provides buy and sell alerts for convenient trading signal notifications.

Visualizations: Plots the Follow Line for both the trade timeframe and the higher timeframe (optional), making it easy to understand the strategy's logic.

How to Use:

Add to Chart: Add the "Follow Line Strategy Version 2.5 (React HTF)" script to your TradingView chart.

Configure Settings: Customize the strategy's settings to match your trading style and preferences. Here's a breakdown of the key settings:

Indicator Settings:

ATR Period: The period used to calculate the ATR. A smaller period is more sensitive to recent price changes.

Bollinger Bands Period: The period used for the Bollinger Bands calculation. A longer period results in smoother bands.

Bollinger Bands Deviation: The number of standard deviations from the moving average that the Bollinger Bands are plotted. Higher deviations create wider bands.

Use ATR for Follow Line Offset?: Enable to use ATR to calculate the Follow Line offset. Disable to use the simple high/low.

Show Trade Signals on Chart?: Enable to show BUY/SELL labels on the chart.

Time Filter:

Use Trading Session Filter?: Enable to restrict trading to specific hours of the day.

Trading Session: The trading session to use (e.g., 0930-1600 for regular US stock market hours). Use 0000-2400 for all hours.

Higher Timeframe Confirmation:

Enable HTF Confirmation?: Enable to use the HTF trend to filter trade signals. If enabled, only trades in the direction of the HTF trend will be taken.

HTF Selection Method: Choose between "Auto" and "Manual" HTF selection.

Manual Higher Timeframe: If "Manual" is selected, choose the specific HTF (e.g., 240 for 4 hours, D for daily).

Show HTF Follow Line?: Enable to plot the HTF Follow Line on the chart.

Understanding the Signals:

Buy Signal: The price breaks above the upper Bollinger Band, and the HTF (if enabled) confirms the uptrend.

Sell Signal: The price breaks below the lower Bollinger Band, and the HTF (if enabled) confirms the downtrend.

Exit Long: The trade timeframe trend changes to downtrend or the higher timeframe trend changes to downtrend.

Exit Short: The trade timeframe trend changes to uptrend or the higher timeframe trend changes to uptrend.

Alerts:

The script includes alert conditions for buy and sell signals. To set up alerts, click the "Alerts" button in TradingView and select the desired alert condition from the script. The alert message provides the ticker and interval.

Backtesting and Optimization:

Use TradingView's Strategy Tester to backtest the strategy on different assets and timeframes.

Experiment with different settings to optimize the strategy for your specific trading style and risk tolerance. Pay close attention to the ATR Period, Bollinger Bands settings, and the HTF confirmation options.

Tips and Considerations:

HTF Confirmation: The HTF confirmation can significantly improve the strategy's performance by filtering out false signals. However, it can also reduce the number of trades.

Risk Management: Always use proper risk management techniques, such as stop-loss orders and position sizing, when trading any strategy.

Market Conditions: The strategy may perform differently in different market conditions. It's important to backtest and optimize the strategy for the specific markets you are trading.

Customization: Feel free to modify the script to suit your specific needs. For example, you could add additional filters or entry/exit conditions.

Pyramiding: The pyramiding = 0 setting prevents multiple entries in the same direction, ensuring the strategy doesn't compound losses. You can adjust this value if you prefer to pyramid into winning positions, but be cautious.

Lookahead: The lookahead = barmerge.lookahead_off setting ensures that the HTF data is calculated based on the current bar's closed data, preventing potential future peeking bias.

Trend Determination: The logic for determining the HTF trend and reacting to changes is critical. Carefully review the f_calculateHTFData function and the conditions for exiting positions to ensure you understand how the strategy responds to different market scenarios.

Disclaimer:

This script is for informational and educational purposes only. It is not financial advice, and you should not trade based solely on the signals generated by this script. Always do your own research and consult with a qualified financial advisor before making any trading decisions. The author is not responsible for any losses incurred as a result of using this script.

Scalping 15min: EMA + MACD + RSI + ATR-based SL/TP📈 Strategy: 15-Minute Scalping — EMA + MACD + RSI + ATR-based SL/TP

This scalping strategy is designed for 15-minute charts and combines trend-following and momentum confirmation with dynamic stop loss and take profit levels based on volatility.

🔧 Indicators Used:

EMA 50 — identifies the main trend

MACD Histogram — confirms momentum direction

RSI (14) — filters overbought/oversold conditions

ATR (14) — dynamically sets SL and TP based on market volatility

📊 Entry Conditions:

Long Entry:

Price is above EMA 50

MACD histogram is positive

RSI is above 50 but below 70

Short Entry:

Price is below EMA 50

MACD histogram is negative

RSI is below 50 but above 30

🛑 Risk Management:

Stop Loss: 1×ATR (user-configurable)

Take Profit: 2×ATR (user-configurable)

These values can be adjusted in the script inputs depending on your risk/reward preference or market conditions.

⚠️ Notes:

Strategy is optimized for scalping fast-moving pairs (e.g. crypto, forex).

Works best in trending markets.

Use backtesting and forward testing before live trading.

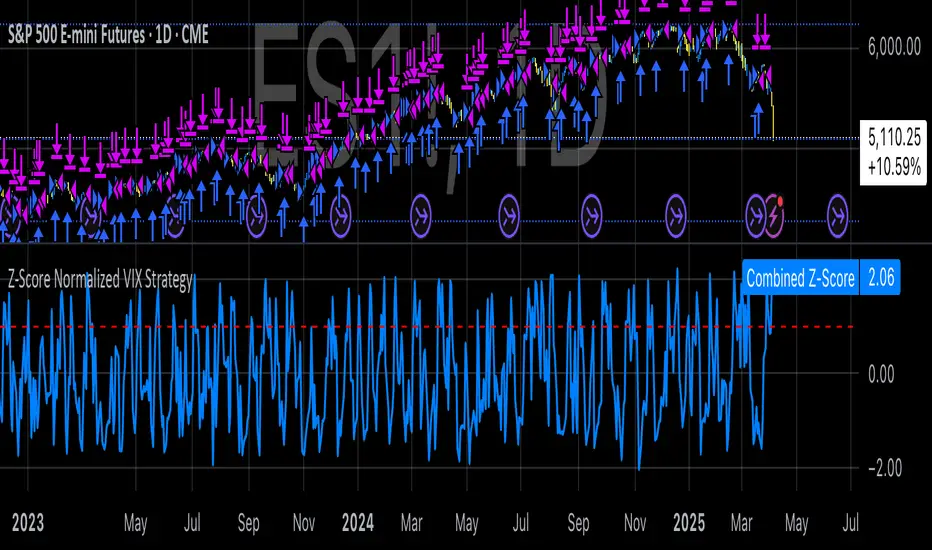

Z-Score Normalized VIX StrategyThis strategy leverages the concept of the Z-score applied to multiple VIX-based volatility indices, specifically designed to capture market reversals based on the normalization of volatility. The strategy takes advantage of VIX-related indicators to measure extreme levels of market fear or greed and adjusts its position accordingly.

1. Overview of the Z-Score Methodology

The Z-score is a statistical measure that describes the position of a value relative to the mean of a distribution in terms of standard deviations. In this strategy, the Z-score is calculated for various volatility indices to assess how far their values are from their historical averages, thus normalizing volatility levels. The Z-score is calculated as follows:

Z = \frac{X - \mu}{\sigma}

Where:

• X is the current value of the volatility index.

• \mu is the mean of the index over a specified period.

• \sigma is the standard deviation of the index over the same period.

This measure tells us how many standard deviations the current value of the index is away from its average, indicating whether the market is experiencing unusually high or low volatility (fear or calm).

2. VIX Indices Used in the Strategy

The strategy utilizes four commonly referenced volatility indices:

• VIX (CBOE Volatility Index): Measures the market’s expectations of 30-day volatility based on S&P 500 options.

• VIX3M (3-Month VIX): Reflects expectations of volatility over the next three months.

• VIX9D (9-Day VIX): Reflects shorter-term volatility expectations.

• VVIX (VIX of VIX): Measures the volatility of the VIX itself, indicating the level of uncertainty in the volatility index.

These indices provide a comprehensive view of the current volatility landscape across different time horizons.

3. Strategy Logic

The strategy follows a long entry condition and an exit condition based on the combined Z-score of the selected volatility indices:

• Long Entry Condition: The strategy enters a long position when the combined Z-score of the selected VIX indices falls below a user-defined threshold, indicating an abnormally low level of volatility (suggesting a potential market bottom and a bullish reversal). The threshold is set as a negative value (e.g., -1), where a more negative Z-score implies greater deviation below the mean.

• Exit Condition: The strategy exits the long position when the combined Z-score exceeds the threshold (i.e., when the market volatility increases above the threshold, indicating a shift in market sentiment and reduced likelihood of continued upward momentum).

4. User Inputs

• Z-Score Lookback Period: The user can adjust the lookback period for calculating the Z-score (e.g., 6 periods).

• Z-Score Threshold: A customizable threshold value to define when the market has reached an extreme volatility level, triggering entries and exits.

The strategy also allows users to select which VIX indices to use, with checkboxes to enable or disable each index in the calculation of the combined Z-score.

5. Trade Execution Parameters

• Initial Capital: The strategy assumes an initial capital of $20,000.

• Pyramiding: The strategy does not allow pyramiding (multiple positions in the same direction).

• Commission and Slippage: The commission is set at $0.05 per contract, and slippage is set at 1 tick.

6. Statistical Basis of the Z-Score Approach

The Z-score methodology is a standard technique in statistics and finance, commonly used in risk management and for identifying outliers or unusual events. According to Dumas, Fleming, and Whaley (1998), volatility indices like the VIX serve as a useful proxy for market sentiment, particularly during periods of high uncertainty. By calculating the Z-score, we normalize volatility and quantify the degree to which the current volatility deviates from historical norms, allowing for systematic entry and exit based on these deviations.

7. Implications of the Strategy

This strategy aims to exploit market conditions where volatility has deviated significantly from its historical mean. When the Z-score falls below the threshold, it suggests that the market has become excessively calm, potentially indicating an overreaction to past market events. Entering long positions under such conditions could capture market reversals as fear subsides and volatility normalizes. Conversely, when the Z-score rises above the threshold, it signals increased volatility, which could be indicative of a bearish shift in the market, prompting an exit from the position.

By applying this Z-score normalized approach, the strategy seeks to achieve more consistent entry and exit points by reducing reliance on subjective interpretation of market conditions.

8. Scientific Sources

• Dumas, B., Fleming, J., & Whaley, R. (1998). “Implied Volatility Functions: Empirical Tests”. The Journal of Finance, 53(6), 2059-2106. This paper discusses the use of volatility indices and their empirical behavior, providing context for volatility-based strategies.

• Black, F., & Scholes, M. (1973). “The Pricing of Options and Corporate Liabilities”. Journal of Political Economy, 81(3), 637-654. The original Black-Scholes model, which forms the basis for many volatility-related strategies.

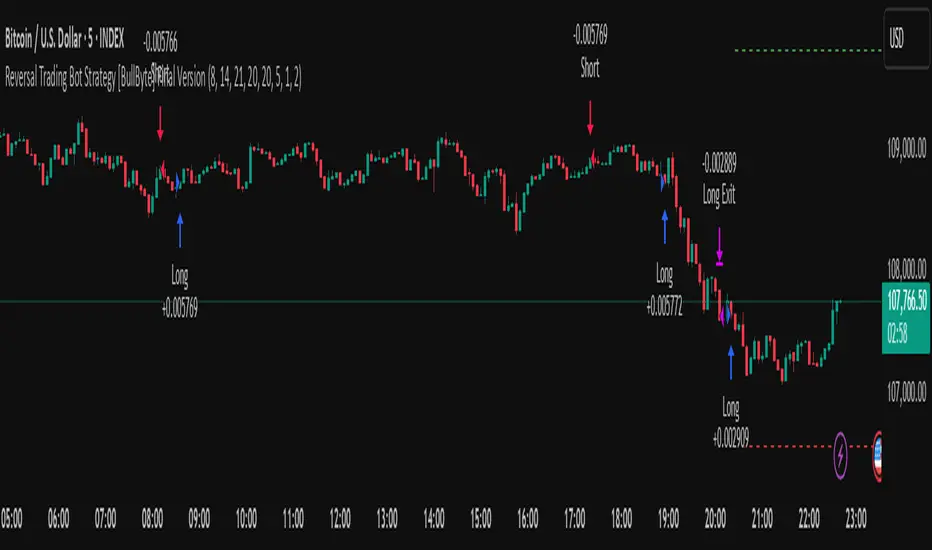

Reversal Trading Bot Strategy[BullByte]Overview :

The indicator Reversal Trading Bot Strategy is crafted to capture potential market reversal points by combining momentum, volatility, and trend alignment filters. It uses a blend of technical indicators to identify both bullish and bearish reversal setups, ensuring that multiple market conditions are met before entering a trade.

Core Components :

Technical Indicators Used :

RSI (Relative Strength Index) :

Purpose : Detects divergence conditions by comparing recent lows/highs in price with the RSI.

Parameter : Length of 8.

Bollinger Bands (BB) :

Purpose : Measures volatility and identifies price levels that are statistically extreme.

Parameter : Length of 20 and a 2-standard deviation multiplier.

ADX (Average Directional Index) & DMI (Directional Movement Index) :

Purpose : Quantifies the strength of the trend. The ADX threshold is set at 20, and additional filters check for the alignment of the directional indicators (DI+ and DI–).

ATR (Average True Range) :

Purpose : Provides a volatility measure used to set stop levels and determine risk through trailing stops.

Volume SMA (Simple Moving Average of Volume ):

Purpose : Helps confirm strength by comparing the current volume against a 20-period average, with an optional filter to ensure volume is at least twice the SMA.

User-Defined Toggle Filters :

Volume Filter : Confirms that the volume is above average (or twice the SMA) before taking trades.

ADX Trend Alignment Filter : Checks that the ADX’s directional indicators support the trade direction.

BB Close Confirmation : Optionally refines the entry by requiring price to be beyond the upper or lower Bollinger Band rather than just above or below.

RSI Divergence Exit : Allows the script to close positions if RSI divergence is detected.

BB Mean Reversion Exit : Closes positions if the price reverts to the Bollinger Bands’ middle line.

Risk/Reward Filter : Ensures that the potential reward is at least twice the risk by comparing the distance to the Bollinger Band with the ATR.

Candle Movement Filter : Optional filter to require a minimum percentage move in the candle to confirm momentum.

ADX Trend Exit : Closes positions if the ADX falls below the threshold and the directional indicators reverse.

Entry Conditions :

Bullish Entry :

RSI Divergence : Checks if the current close is lower than a previous low while the RSI is above the previous low, suggesting bullish divergence.

Bollinger Confirmation : Requires that the price is above the lower (or upper if confirmation is toggled) Bollinger Band.

Volume & Trend Filters : Combines volume condition, ADX strength, and an optional candle momentum condition.

Risk/Reward Check : Validates that the trade meets a favorable risk-to-reward ratio.

Bearish Entry :

Uses a mirror logic of the bullish entry by checking for bearish divergence, ensuring the price is below the appropriate Bollinger level, and confirming volume, trend strength, candle pattern, and risk/reward criteria.

Trade Execution and Exit Strateg y:

Trade Execution :

Upon meeting the entry conditions, the strategy initiates a long or short position.

Stop Loss & Trailing Stops :

A stop-loss is dynamically set using the ATR value, and trailing stops are implemented as a percentage of the close price.

Exit Conditions :

Additional exit filters can trigger early closures based on RSI divergence, mean reversion (via the middle Bollinger Band), or a weakening trend as signaled by ADX falling below its threshold.

This multi-layered exit strategy is designed to lock in gains or minimize losses if the market begins to reverse unexpectedly.

How the Strategy Works in Different Market Conditions :

Trending Markets :

The ADX filter ensures that trades are only taken when the trend is strong. When the market is trending, the directional movement indicators help confirm the momentum, making the reversal signal more reliable.

Ranging Markets :

In choppy markets, the Bollinger Bands expand and contract, while the RSI divergence can highlight potential turning points. The optional filters can be adjusted to avoid false signals in low-volume or low-volatility conditions.

Volatility Management :

With ATR-based stop-losses and a risk/reward filter, the strategy adapts to current market volatility, ensuring that risk is managed consistently.

Recommendation on using this Strategy with a Trading Bot :

This strategy is well-suited for high-frequency trading (HFT) due to its ability to quickly identify reversal setups and execute trades dynamically with automated stop-loss and trailing exits. By integrating this script with a TradingView webhook-based bot or an API-driven execution system, traders can automate trade entries and exits in real-time, reducing manual execution delays and capitalizing on fast market movements.

Disclaimer :

This script is provided for educational and informational purposes only. It is not intended as investment advice. Trading involves significant risk, and you should always conduct your own research and analysis before making any trading decisions. The author is not responsible for any losses incurred while using this script.

Smart Grid Scalping (Pullback) Strategy[BullByte]The Smart Grid Scalping (Pullback) Strategy is a high-frequency trading strategy designed for short-term traders who seek to capitalize on market pullbacks. This strategy utilizes a dynamic ATR-based grid system to define optimal entry points, ensuring precise trade execution. It integrates volatility filtering and an RSI-based confirmation mechanism to enhance signal accuracy and reduce false entries.

This strategy is specifically optimized for scalping by dynamically adjusting trade levels based on current market conditions. The grid-based system helps capture retracement opportunities while maintaining strict trade management through predefined profit targets and trailing stop-loss mechanisms.

Key Features :

1. ATR-Based Grid System :

- Uses a 10-period ATR to dynamically calculate grid levels for entry points.

- Prevents chasing trades by ensuring price has reached key levels before executing entries.

2. No Trade Zone Protection :

- Avoids low-volatility zones where price action is indecisive.

- Ensures only high-momentum trades are executed to improve success rate.

3. RSI-Based Entry Confirmation :

- Long trades are triggered when RSI is below 30 (oversold) and price is in the lower grid zone.

- Short trades are triggered when RSI is above 70 (overbought) and price is in the upper grid zone.

4. Automated Trade Execution :

- Long Entry: Triggered when price drops below the first grid level with sufficient volatility.

- Short Entry: Triggered when price exceeds the highest grid level with sufficient volatility.

5. Take Profit & Trailing Stop :

- Profit target set at a customizable percentage (default 0.2%).

- Adaptive trailing stop mechanism using ATR to lock in profits while minimizing premature exits.

6. Visual Trade Annotations :

- Clearly labeled "LONG" and "SHORT" markers appear at trade entries for better visualization.

- Grid levels are plotted dynamically to aid decision-making.

Strategy Logic :

- The script first calculates the ATR-based grid levels and ensures price action has sufficient volatility before allowing trades.

- An additional RSI filter is used to ensure trades are taken at ideal market conditions.

- Once a trade is executed, the script implements a trailing stop and predefined take profit to maximize gains while reducing risks.

---

Disclaimer :

Risk Warning :

This strategy is provided for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Users are advised to conduct their own due diligence and risk management before using this strategy in live trading.

The developer and publisher of this script are not responsible for any financial losses incurred by the use of this strategy. Market conditions, slippage, and execution quality can affect real-world trading outcomes.

Use this script at your own discretion and always trade responsibly.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

Litecoin Trailing-Stop StrategyAltcoins Trailing-Stop Strategy

This strategy is based on a momentum breakout approach using PKAMA (Powered Kaufman Adaptive Moving Average) as a trend filter, and a delayed trailing stop mechanism to manage risk effectively.

It has been designed and fine-tuned Altcoins, which historically shows consistent volatility patterns and clean trend structures, especially on intraday timeframes like 15m and 30m.

Strategy Logic:

Entry Conditions:

Long when PKAMA indicates an upward move

Short when PKAMA detects a downward trend

Minimum spacing of 30 bars between trades to avoid overtrading

Trailing Stop:

Activated only after a customizable delay (delayBars)

User can set trailing stop % and delay independently

Helps avoid premature exits due to short-term volatility

Customizable Parameters:

This strategy uses a custom implementation of PKAMA (Powered Kaufman Adaptive Moving Average), inspired by the work of alexgrover

PKAMA is a volatility-aware moving average that adjusts dynamically to market conditions, making it ideal for altcoins where trend strength and direction change frequently.

This script is for educational and experimental purposes only. It is not financial advice. Please test thoroughly before using it in live conditions, and always adapt parameters to your specific asset and time frame.

Feedback is welcome! Feel free to clone and adapt it for your own trading style.

02 SMC + BB Breakout (Improved)This strategy combines Smart Money Concepts (SMC) with Bollinger Band breakouts to identify potential trading opportunities. SMC focuses on identifying key price levels and market structure shifts, while Bollinger Bands help pinpoint overbought/oversold conditions and potential breakout points. The strategy also incorporates higher timeframe trend confirmation to filter out trades that go against the prevailing trend.

Key Components:

Bollinger Bands:

Calculated using a Simple Moving Average (SMA) of the closing price and a standard deviation multiplier.

The strategy uses the upper and lower bands to identify potential breakout points.

The SMA (basis) acts as a centerline and potential support/resistance level.

The fill between the upper and lower bands can be toggled by the user.

Higher Timeframe Trend Confirmation:

The strategy allows for optional confirmation of the current trend using a higher timeframe (e.g., daily).

It calculates the SMA of the higher timeframe's closing prices.

A bullish trend is confirmed if the higher timeframe's closing price is above its SMA.

This helps filter out trades that go against the prevailing long-term trend.

Smart Money Concepts (SMC):

Order Blocks:

Simplified as recent price clusters, identified by the highest high and lowest low over a specified lookback period.

These levels are considered potential areas of support or resistance.

Liquidity Zones (Swing Highs/Lows):

Identified by recent swing highs and lows, indicating areas where liquidity may be present.

The Swing highs and lows are calculated based on user defined lookback periods.

Market Structure Shift (MSS):

Identifies potential changes in market structure.

A bullish MSS occurs when the closing price breaks above a previous swing high.

A bearish MSS occurs when the closing price breaks below a previous swing low.

The swing high and low values used for the MSS are calculated based on the user defined swing length.

Entry Conditions:

Long Entry:

The closing price crosses above the upper Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bullish.

A bullish MSS must have occurred.

Short Entry:

The closing price crosses below the lower Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bearish.

A bearish MSS must have occurred.

Exit Conditions:

Long Exit:

The closing price crosses below the Bollinger Band basis.

Or the Closing price falls below 99% of the order block low.

Short Exit:

The closing price crosses above the Bollinger Band basis.

Or the closing price rises above 101% of the order block high.

Position Sizing:

The strategy calculates the position size based on a fixed percentage (5%) of the strategy's equity.

This helps manage risk by limiting the potential loss per trade.

Visualizations:

Bollinger Bands (upper, lower, and basis) are plotted on the chart.

SMC elements (order blocks, swing highs/lows) are plotted as lines, with user-adjustable visibility.

Entry and exit signals are plotted as shapes on the chart.

The Bollinger band fill opacity is adjustable by the user.

Trading Logic:

The strategy aims to capitalize on Bollinger Band breakouts that are confirmed by SMC signals and higher timeframe trend. It looks for breakouts that align with potential market structure shifts and key price levels (order blocks, swing highs/lows). The higher timeframe filter helps avoid trades that go against the overall trend.

In essence, the strategy attempts to identify high-probability breakout trades by combining momentum (Bollinger Bands) with structural analysis (SMC) and trend confirmation.

Key User-Adjustable Parameters:

Bollinger Bands Length

Standard Deviation Multiplier

Higher Timeframe

Higher Timeframe Confirmation (on/off)

SMC Elements Visibility (on/off)

Order block lookback length.

Swing lookback length.

Bollinger band fill opacity.

This detailed description should provide a comprehensive understanding of the strategy's logic and components.

***DISCLAIMER: This strategy is for educational purposes only. It is not financial advice. Past performance is not indicative of future results. Use at your own risk. Always perform thorough backtesting and forward testing before using any strategy in live trading.***

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

Arbitrage Spot-Futures Don++Strategy: Spot-Futures Arbitrage Don++

This strategy has been designed to detect and exploit arbitrage opportunities between the Spot and Futures markets of the same trading pair (e.g. BTC/USDT). The aim is to take advantage of price differences (spreads) between the two markets, while minimizing risk through dynamic position management.

[Operating principle

The strategy is based on calculating the spread between Spot and Futures prices. When this spread exceeds a certain threshold (positive or negative), reverse positions are opened simultaneously on both markets:

- i] Long Spot + Short Futures when the spread is positive.

- i] Short Spot + Long Futures when the spread is negative.

Positions are closed when the spread returns to a value close to zero or after a user-defined maximum duration.

[Strategy strengths

1. Adaptive thresholds :

- Entry/exit thresholds can be dynamic (based on moving averages and standard deviations) or fixed, offering greater flexibility to adapt to market conditions.

2. Robust data management :

- The script checks the validity of data before executing calculations, thus avoiding errors linked to missing or invalid data.

3. Risk limitation :

- A position size based on a percentage of available capital (default 10%) limits exposure.

- A time filter limits the maximum duration of positions to avoid losses due to persistent spreads.

4. Clear visualization :

- Charts include horizontal lines for entry/exit thresholds, as well as visual indicators for spread and Spot/Futures prices.

5. Alerts and logs :

- Alerts are triggered on entries and exits to inform the user in real time.

[Points for improvement or completion

Although this strategy is functional and robust, it still has a few limitations that could be addressed in future versions:

1. [Limited historical data :

- TradingView does not retrieve real-time data for multiple symbols simultaneously. This can limit the accuracy of calculations, especially under conditions of high volatility.

2. [Lack of liquidity management :

- The script does not take into account the volumes available on the order books. In conditions of low liquidity, it may be difficult to execute orders at the desired prices.

3. [Non-dynamic transaction costs :

- Transaction costs (exchange fees, slippage) are set manually. A dynamic integration of these costs via an external API would be more realistic.

4. User-dependency for symbols :

- Users must manually specify Spot and Futures symbols. Automatic symbol validation would be useful to avoid configuration errors.

5. Lack of advanced backtesting :

- Backtesting is based solely on historical data available on TradingView. An implementation with third-party data (via an API) would enable the strategy to be tested under more realistic conditions.

6. [Parameter optimization :

- Certain parameters (such as analysis period or spread thresholds) could be optimized for each specific trading pair.

[How can I contribute?

If you'd like to help improve this strategy, here are a few ideas:

1. Add additional filters:

- For example, a filter based on volume or volatility to avoid false signals.

2. Integrate dynamic costs:

- Use an external API to retrieve actual costs and adjust thresholds accordingly.

3. Improve position management:

- Implement hedging or scalping mechanisms to maximize profits.

4. Test on other pairs:

- Evaluate the strategy's performance on other assets (ETH, SOL, etc.) and adjust parameters accordingly.

5. Publish backtesting results :

- Share detailed analyses of the strategy's performance under different market conditions.

[Conclusion

This Spot-Futures arbitrage strategy is a powerful tool for exploiting price differentials between markets. Although it is already functional, it can still be improved to meet more complex trading scenarios. Feel free to test, modify and share your ideas to make this strategy even more effective!

[Thank you for contributing to this open-source community!

If you have any questions or suggestions, please feel free to comment or contact me directly.

Dual Keltner Channels Strategy [Eastgate3194]This strategy utilised 2 Keltner Channels to perform counter trade.

The strategy have 2 steps:

Long Position:

Step 1. Close price must cross under Outer Lower band of Keltner Channel.

Step 2. Close price cross over Inner Lower band of Keltner Channel.

Short Position:

Step 1. Close price must cross over Outer Upper band of Keltner Channel.

Step 2. Close price cross under Inner Upper band of Keltner Channel.

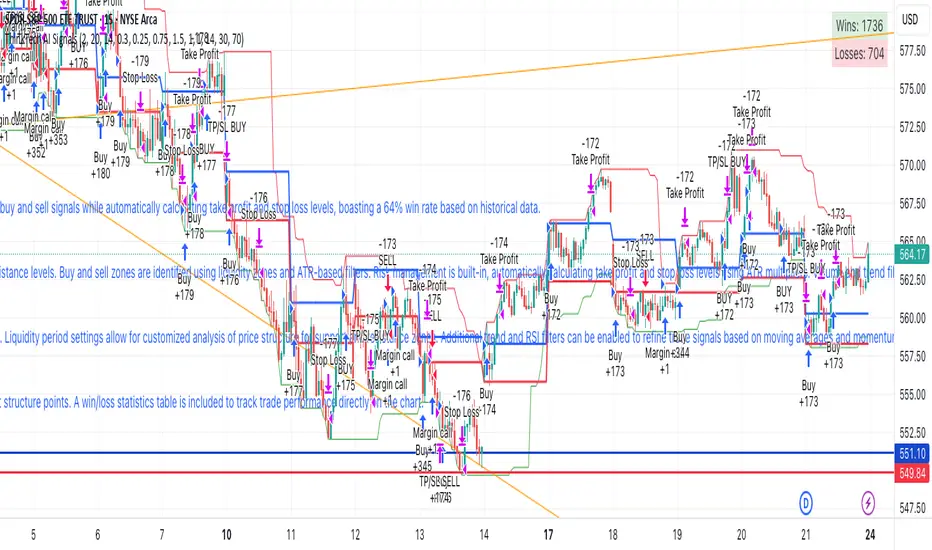

ThinkTech AI SignalsThink Tech AI Strategy

The Think Tech AI Strategy provides a structured approach to trading by integrating liquidity-based entries, ATR volatility thresholds, and dynamic risk management. This strategy generates buy and sell signals while automatically calculating take profit and stop loss levels, boasting a 64% win rate based on historical data.

Usage

The strategy can be used to identify key breakout and retest opportunities. Liquidity-based zones act as potential accumulation and distribution areas and may serve as future support or resistance levels. Buy and sell zones are identified using liquidity zones and ATR-based filters. Risk management is built-in, automatically calculating take profit and stop loss levels using ATR multipliers. Volume and trend filtering options help confirm directional bias using a 50 EMA and RSI filter. The strategy also allows for session-based trading, limiting trades to key market hours for higher probability setups.

Settings

The risk/reward ratio can be adjusted to define the desired stop loss and take profit calculations. The ATR length and threshold determine ATR-based breakout conditions for dynamic entries. Liquidity period settings allow for customized analysis of price structure for support and resistance zones. Additional trend and RSI filters can be enabled to refine trade signals based on moving averages and momentum conditions. A session filter is included to restrict trade signals to specific market hours.

Style

The strategy includes options to display liquidity lines, showing key support and resistance areas. The first 15-minute candle breakout zones can also be visualized to highlight critical market structure points. A win/loss statistics table is included to track trade performance directly on the chart.

This strategy is intended for descriptive analysis and should be used alongside other confluence factors. Optimize your trading process with Think Tech AI today!

FlexATRFlexATR: A Dynamic Multi-Timeframe Trading Strategy

Overview: FlexATR is a versatile trading strategy that dynamically adapts its key parameters based on the timeframe being used. It combines technical signals from exponential moving averages (EMAs) and the Relative Strength Index (RSI) with volatility-based risk management via the Average True Range (ATR). This approach helps filter out false signals while adjusting to varying market conditions — whether you’re trading on a daily chart, intraday charts (30m, 60m, or 5m), or even on higher timeframes like the 4-hour or weekly charts.

How It Works:

Multi-Timeframe Parameter Adaptation: FlexATR is designed to automatically adjust its indicator settings depending on the timeframe:

Daily and Weekly: On higher timeframes, the strategy uses longer periods for the fast and slow EMAs and standard periods for RSI and ATR to capture more meaningful trend confirmations while minimizing noise.

Intraday (e.g., 30m, 60m, 5m, 4h): The parameters are converted from “days” into the corresponding number of bars. For instance, on a 30-minute chart, a “day” might equal 48 bars. The preset values for a 30-minute chart have been slightly reduced (e.g., a fast EMA is set at 0.35 days instead of 0.4) to improve reactivity while maintaining robust filtering.

Signal Generation:

Entry Signals: The strategy enters long positions when the fast EMA crosses above the slow EMA and the RSI is above 50, and it enters short positions when the fast EMA crosses below the slow EMA with the RSI below 50. This dual confirmation helps ensure that signals are reliable.

Risk Management: The ATR is used to compute dynamic levels for stop loss and profit target:

Stop Loss: For a long position, the stop loss is placed at Price - (ATR × Stop Loss Multiplier). For a short position, it is at Price + (ATR × Stop Loss Multiplier).

Profit Target: The profit target is similarly set using the ATR multiplied by a designated profit multiplier.

Dynamic Trailing Stop: FlexATR further incorporates a dynamic trailing stop (if enabled) that adjusts according to the ATR. This trailing stop follows favorable price movements at a distance defined by a multiplier, locking in gains as the trend develops. The use of a trailing stop helps protect profits without requiring a fixed exit point.

Capital Allocation: Each trade is sized at 10% of the total equity. This percentage-based position sizing allows the strategy to scale with your account size. While the current setup assumes no leverage (a 1:1 exposure), the inherent design of the strategy means you can adjust the leverage externally if desired, with risk metrics scaling accordingly.

Visual Representation: For clarity and accessibility (especially for those with color vision deficiencies), FlexATR employs a color-blind friendly palette (the Okabe-Ito palette):

EMA Fast: Displayed in blue.

EMA Slow: Displayed in orange.

Stop Loss Levels: Rendered in vermilion.

Profit Target Levels: Shown in a distinct azzurro (light blue).

Benefits and Considerations:

Reliability: By requiring both EMA crossovers and an RSI confirmation, FlexATR filters out a significant amount of market noise, which reduces false signals at the expense of some delayed entries.

Adaptability: The automatic conversion of “day-based” parameters into bar counts for intraday charts means the strategy remains consistent across different timeframes.

Risk Management: Using the ATR for both fixed and trailing stops allows the strategy to adapt to changing market volatility, helping to protect your capital.

Flexibility: The strategy’s inputs are customizable via the input panel, allowing traders to fine-tune the parameters for different assets or market conditions.

Conclusion: FlexATR is designed as a balanced, adaptive strategy that emphasizes reliability and robust risk management across a variety of timeframes. While it may sometimes enter trades slightly later due to its filtering mechanism, its focus on confirming trends helps reduce the likelihood of false signals. This makes it particularly attractive for traders who prioritize a disciplined, multi-timeframe approach to capturing market trends.

ETH/USDT EMA Crossover Strategy - OptimizedStrategy Name: EMA Crossover Strategy for ETH/USDT

Description:

This trading strategy is designed for the ETH/USDT pair and is based on exponential moving average (EMA) crossovers combined with momentum and volatility indicators. The strategy uses multiple filters to identify high-probability signals in both bullish and bearish trends, making it suitable for traders looking to trade in trending markets.

Strategy Components

EMAs (Exponential Moving Averages):

EMA 200: Used to identify the primary trend. If the price is above the EMA 200, it is considered a bullish trend; if below, a bearish trend.

EMA 50: Acts as an additional filter to confirm the trend.

EMA 20 and EMA 50 Short: These short-term EMAs generate entry signals through crossovers. A bullish crossover (EMA 20 crosses above EMA 50 Short) is a buy signal, while a bearish crossover (EMA 20 crosses below EMA 50 Short) is a sell signal.

RSI (Relative Strength Index):

The RSI is used to avoid overbought or oversold conditions. Long trades are only taken when the RSI is above 30, and short trades when the RSI is below 70.

ATR (Average True Range):

The ATR is used as a volatility filter. Trades are only taken when there is sufficient volatility, helping to avoid false signals in quiet markets.

Volume:

A volume filter is used to confirm sufficient market participation in the price movement. Trades are only taken when volume is above average.

Strategy Logic

Long Trades:

The price must be above the EMA 200 (bullish trend).

The EMA 20 must cross above the EMA 50 Short.

The RSI must be above 30.

The ATR must indicate sufficient volatility.

Volume must be above average.

Short Trades:

The price must be below the EMA 200 (bearish trend).

The EMA 20 must cross below the EMA 50 Short.

The RSI must be below 70.

The ATR must indicate sufficient volatility.

Volume must be above average.

How to Use the Strategy

Setup:

Add the script to your ETH/USDT chart on TradingView.

Adjust the parameters according to your preferences (e.g., EMA periods, RSI, ATR, etc.).

Signals:

Buy and sell signals will be displayed directly on the chart.

Long trades are indicated with an upward arrow, and short trades with a downward arrow.

Risk Management:

Use stop-loss and take-profit orders in all trades.

Consider a risk-reward ratio of at least 1:2.

Backtesting:

Test the strategy on historical data to evaluate its performance before using it live.

Advantages of the Strategy

Trend-focused: The strategy is designed to trade in trending markets, increasing the probability of success.

Multiple filters: The use of RSI, ATR, and volume reduces false signals.

Adaptability: It can be adjusted for different timeframes, although it is recommended to test it on 5-minute and 15-minute charts for ETH/USDT.

Warnings

Sideways markets: The strategy may generate false signals in markets without a clear trend. It is recommended to avoid trading in such conditions.

Optimization: Make sure to optimize the parameters according to the market and timeframe you are using.

Risk management: Never trade without stop-loss and take-profit orders.

Author

Jose J. Sanchez Cuevas

Version

v1.0

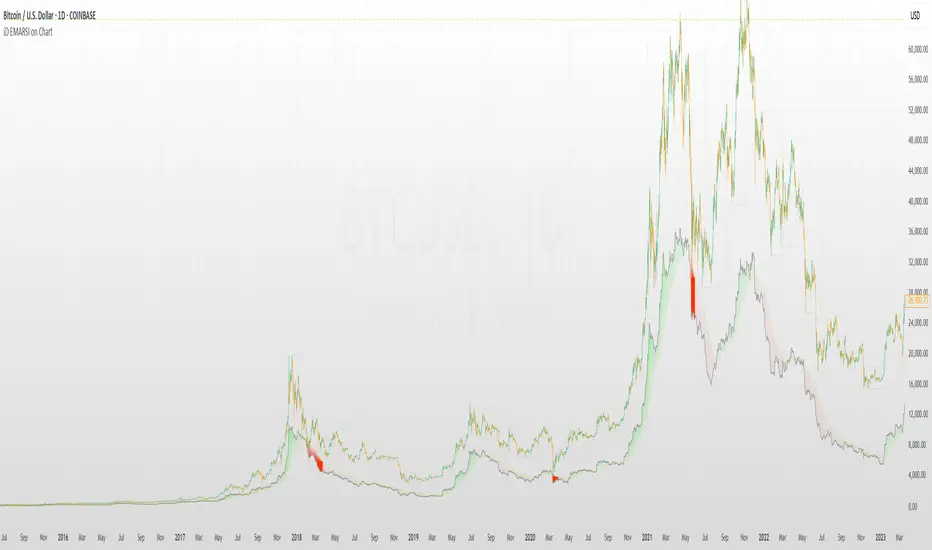

iD EMARSI on ChartSCRIPT OVERVIEW

The EMARSI indicator is an advanced technical analysis tool that maps RSI values directly onto price charts. With adaptive scaling capabilities, it provides a unique visualization of momentum that flows naturally with price action, making it particularly valuable for FOREX and low-priced securities trading.

KEY FEATURES

1 PRICE MAPPED RSI VISUALIZATION

Unlike traditional RSI that displays in a separate window, EMARSI plots the RSI directly on the price chart, creating a flowing line that identifies momentum shifts within the context of price action:

// Map RSI to price chart with better scaling

mappedRsi = useAdaptiveScaling ?

median + ((rsi - 50) / 50 * (pQH - pQL) / 2 * math.min(1.0, 1/scalingFactor)) :

down == pQL ? pQH : up == pQL ? pQL : median - (median / (1 + up / down))

2 ADAPTIVE SCALING SYSTEM

The script features an intelligent scaling system that automatically adjusts to different market conditions and price levels:

// Calculate adaptive scaling factor based on selected method

scalingFactor = if scalingMethod == "ATR-Based"

math.min(maxScalingFactor, math.max(1.0, minTickSize / (atrValue/avgPrice)))

else if scalingMethod == "Price-Based"

math.min(maxScalingFactor, math.max(1.0, math.sqrt(100 / math.max(avgPrice, 0.01))))

else // Volume-Based

math.min(maxScalingFactor, math.max(1.0, math.sqrt(1000000 / math.max(volume, 100))))

3 MODIFIED RSI CALCULATION

EMARSI uses a specially formulated RSI calculation that works with an adaptive base value to maintain consistency across different price ranges:

// Adaptive RSI Base based on price levels to improve flow

adaptiveRsiBase = useAdaptiveScaling ? rsiBase * scalingFactor : rsiBase

// Calculate RSI components with adaptivity

up = ta.rma(math.max(ta.change(rsiSourceInput), adaptiveRsiBase), emaSlowLength)

down = ta.rma(-math.min(ta.change(rsiSourceInput), adaptiveRsiBase), rsiLengthInput)

// Improved RSI calculation with value constraint

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

4 MOVING AVERAGE CROSSOVER SYSTEM

The indicator creates a smooth moving average of the RSI line, enabling a crossover system that generates trading signals:

// Calculate MA of mapped RSI

rsiMA = ma(mappedRsi, emaSlowLength, maTypeInput)

// Strategy entries

if ta.crossover(mappedRsi, rsiMA)

strategy.entry("RSI Long", strategy.long)

if ta.crossunder(mappedRsi, rsiMA)

strategy.entry("RSI Short", strategy.short)

5 VISUAL REFERENCE FRAMEWORK

The script includes visual guides that help interpret the RSI movement within the context of recent price action:

// Calculate pivot high and low

pQH = ta.highest(high, hlLen)

pQL = ta.lowest(low, hlLen)

median = (pQH + pQL) / 2

// Plotting

plot(pQH, "Pivot High", color=color.rgb(82, 228, 102, 90))

plot(pQL, "Pivot Low", color=color.rgb(231, 65, 65, 90))

med = plot(median, style=plot.style_steplinebr, linewidth=1, color=color.rgb(238, 101, 59, 90))

6 DYNAMIC COLOR SYSTEM

The indicator uses color fills to clearly visualize the relationship between the RSI and its moving average:

// Color fills based on RSI vs MA

colUp = mappedRsi > rsiMA ? input.color(color.rgb(128, 255, 0), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(240, 9, 9, 95), '', group= 'RSI < EMA', inline= 'dn')

colDn = mappedRsi > rsiMA ? input.color(color.rgb(0, 230, 35, 95), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(255, 47, 0), '', group= 'RSI < EMA', inline= 'dn')

fill(rsiPlot, emarsi, mappedRsi > rsiMA ? pQH : rsiMA, mappedRsi > rsiMA ? rsiMA : pQL, colUp, colDn)

7 REAL TIME PARAMETER MONITORING

A transparent information panel provides real-time feedback on the adaptive parameters being applied:

// Information display

var table infoPanel = table.new(position.top_right, 2, 3, bgcolor=color.rgb(0, 0, 0, 80))

if barstate.islast

table.cell(infoPanel, 0, 0, "Current Scaling Factor", text_color=color.white)

table.cell(infoPanel, 1, 0, str.tostring(scalingFactor, "#.###"), text_color=color.white)

table.cell(infoPanel, 0, 1, "Adaptive RSI Base", text_color=color.white)

table.cell(infoPanel, 1, 1, str.tostring(adaptiveRsiBase, "#.####"), text_color=color.white)

BENEFITS FOR TRADERS

INTUITIVE MOMENTUM VISUALIZATION

By mapping RSI directly onto the price chart, traders can immediately see the relationship between momentum and price without switching between different indicator windows.

ADAPTIVE TO ANY MARKET CONDITION

The three scaling methods (ATR-Based, Price-Based, and Volume-Based) ensure the indicator performs consistently across different market conditions, volatility regimes, and price levels.

PREVENTS EXTREME VALUES

The adaptive scaling system prevents the RSI from generating extreme values that exceed chart boundaries when trading low-priced securities or during high volatility periods.

CLEAR TRADING SIGNALS

The RSI and moving average crossover system provides clear entry signals that are visually reinforced through color changes, making it easy to identify potential trading opportunities.

SUITABLE FOR MULTIPLE TIMEFRAMES

The indicator works effectively across multiple timeframes, from intraday to daily charts, making it versatile for different trading styles and strategies.

TRANSPARENT PARAMETER ADJUSTMENT

The information panel provides real-time feedback on how the adaptive system is adjusting to current market conditions, helping traders understand why the indicator is behaving as it is.

CUSTOMIZABLE VISUALIZATION

Multiple visualization options including Bollinger Bands, different moving average types, and customizable colors allow traders to adapt the indicator to their personal preferences.

CONCLUSION

The EMARSI indicator represents a significant advancement in RSI visualization by directly mapping momentum onto price charts with adaptive scaling. This approach makes momentum shifts more intuitive to identify and helps prevent the scaling issues that commonly affect RSI-based indicators when applied to low-priced securities or volatile markets.

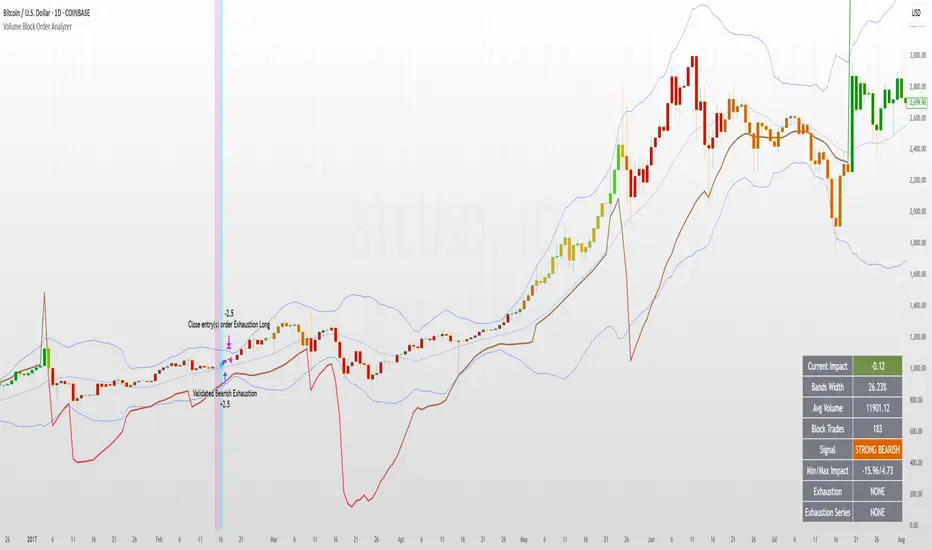

Volume Block Order AnalyzerCore Concept

The Volume Block Order Analyzer is a sophisticated Pine Script strategy designed to detect and analyze institutional money flow through large block trades. It identifies unusually high volume candles and evaluates their directional bias to provide clear visual signals of potential market movements.

How It Works: The Mathematical Model

1. Volume Anomaly Detection

The strategy first identifies "block trades" using a statistical approach:

```

avgVolume = ta.sma(volume, lookbackPeriod)

isHighVolume = volume > avgVolume * volumeThreshold

```

This means a candle must have volume exceeding the recent average by a user-defined multiplier (default 2.0x) to be considered a significant block trade.

2. Directional Impact Calculation

For each block trade identified, its price action determines direction:

- Bullish candle (close > open): Positive impact

- Bearish candle (close < open): Negative impact

The magnitude of impact is proportional to the volume size:

```

volumeWeight = volume / avgVolume // How many times larger than average

blockImpact = (isBullish ? 1.0 : -1.0) * (volumeWeight / 10)

```

This creates a normalized impact score typically ranging from -1.0 to 1.0, scaled by dividing by 10 to prevent excessive values.

3. Cumulative Impact with Time Decay

The key innovation is the cumulative impact calculation with decay:

```

cumulativeImpact := cumulativeImpact * impactDecay + blockImpact

```

This mathematical model has important properties:

- Recent block trades have stronger influence than older ones

- Impact gradually "fades" at rate determined by decay factor (default 0.95)

- Sustained directional pressure accumulates over time

- Opposing pressure gradually counteracts previous momentum

Trading Logic

Signal Generation

The strategy generates trading signals based on momentum shifts in institutional order flow:

1. Long Entry Signal: When cumulative impact crosses from negative to positive

```

if ta.crossover(cumulativeImpact, 0)

strategy.entry("Long", strategy.long)

```

*Logic: Institutional buying pressure has overcome selling pressure, indicating potential upward movement*

2. Short Entry Signal: When cumulative impact crosses from positive to negative

```

if ta.crossunder(cumulativeImpact, 0)

strategy.entry("Short", strategy.short)

```

*Logic: Institutional selling pressure has overcome buying pressure, indicating potential downward movement*

3. Exit Logic: Positions are closed when the cumulative impact moves against the position

```

if cumulativeImpact < 0

strategy.close("Long")

```

*Logic: The original signal is no longer valid as institutional flow has reversed*

Visual Interpretation System

The strategy employs multiple visualization techniques:

1. Color Gradient Bar System:

- Deep green: Strong buying pressure (impact > 0.5)

- Light green: Moderate buying pressure (0.1 < impact ≤ 0.5)

- Yellow-green: Mild buying pressure (0 < impact ≤ 0.1)

- Yellow: Neutral (impact = 0)

- Yellow-orange: Mild selling pressure (-0.1 < impact ≤ 0)

- Orange: Moderate selling pressure (-0.5 < impact ≤ -0.1)

- Red: Strong selling pressure (impact ≤ -0.5)

2. Dynamic Impact Line:

- Plots the cumulative impact as a line

- Line color shifts with impact value

- Line movement shows momentum and trend strength

3. Block Trade Labels:

- Marks significant block trades directly on the chart

- Shows direction and volume amount

- Helps identify key moments of institutional activity

4. Information Dashboard:

- Current impact value and signal direction

- Average volume benchmark

- Count of significant block trades

- Min/Max impact range

Benefits and Use Cases

This strategy provides several advantages:

1. Institutional Flow Detection: Identifies where large players are positioning themselves

2. Early Trend Identification: Often detects institutional accumulation/distribution before major price movements

3. Market Context Enhancement: Provides deeper insight than simple price action alone

4. Objective Decision Framework: Quantifies what might otherwise be subjective observations

5. Adaptive to Market Conditions: Works across different timeframes and instruments by using relative volume rather than absolute thresholds

Customization Options

The strategy allows users to fine-tune its behavior:

- Volume Threshold: How unusual a volume spike must be to qualify

- Lookback Period: How far back to measure average volume

- Impact Decay Factor: How quickly older trades lose influence

- Visual Settings: Labels and line width customization

This sophisticated yet intuitive strategy provides traders with a window into institutional activity, helping identify potential trend changes before they become obvious in price action alone.

Advanced Adaptive Grid Trading StrategyThis strategy employs an advanced grid trading approach that dynamically adapts to market conditions, including trend, volatility, and risk management considerations. The strategy aims to capitalize on price fluctuations in both rising (long) and falling (short) markets, as well as during sideways movements. It combines multiple indicators to determine the trend and automatically adjusts grid parameters for more efficient trading.

How it Works:

Trend Analysis:

Short, long, and super long Moving Averages (MA) to determine the trend direction.

RSI (Relative Strength Index) to identify overbought and oversold levels, and to confirm the trend.

MACD (Moving Average Convergence Divergence) to confirm momentum and trend direction.

Momentum indicator.

The strategy uses a weighted scoring system to assess trend strength (strong bullish, moderate bullish, strong bearish, moderate bearish, sideways).

Grid System:

The grid size (the distance between buy and sell levels) changes dynamically based on market volatility, using the ATR (Average True Range) indicator.

Grid density also adapts to the trend: in a strong trend, the grid is denser in the direction of the trend.

Grid levels are shifted depending on the trend direction (upwards in a bear market, downwards in a bull market).

Trading Logic:

The strategy opens long positions if the trend is bullish and the price reaches one of the lower grid levels.

It opens short positions if the trend is bearish and the price reaches one of the upper grid levels.

In a sideways market, it can open positions in both directions.

Risk Management:

Stop Loss for every position.

Take Profit for every position.

Trailing Stop Loss to protect profits.

Maximum daily loss limit.

Maximum number of positions limit.

Time-based exit (if the position is open for too long).

Risk-based position sizing (optional).

Input Options:

The strategy offers numerous settings that allow users to customize its operation:

Timeframe: The chart's timeframe (e.g., 1 minute, 5 minutes, 1 hour, 4 hours, 1 day, 1 week).

Base Grid Size (%): The base size of the grid, expressed as a percentage.

Max Positions: The maximum number of open positions allowed.

Use Volatility Grid: If enabled, the grid size changes dynamically based on the ATR indicator.

ATR Length: The period of the ATR indicator.

ATR Multiplier: The multiplier for the ATR to fine-tune the grid size.

RSI Length: The period of the RSI indicator.

RSI Overbought: The overbought level for the RSI.

RSI Oversold: The oversold level for the RSI.

Short MA Length: The period of the short moving average.

Long MA Length: The period of the long moving average.

Super Long MA Length: The period of the super long moving average.

MACD Fast Length: The fast period of the MACD.

MACD Slow Length: The slow period of the MACD.

MACD Signal Length: The period of the MACD signal line.

Stop Loss (%): The stop loss level, expressed as a percentage.

Take Profit (%): The take profit level, expressed as a percentage.

Use Trailing Stop: If enabled, the strategy uses a trailing stop loss.

Trailing Stop (%): The trailing stop loss level, expressed as a percentage.

Max Loss Per Day (%): The maximum daily loss, expressed as a percentage.

Time Based Exit: If enabled, the strategy exits the position after a certain amount of time.

Max Holding Period (hours): The maximum holding time in hours.

Use Risk Based Position: If enabled, the strategy calculates position size based on risk.

Risk Per Trade (%): The risk per trade, expressed as a percentage.

Max Leverage: The maximum leverage.

Important Notes:

This strategy does not guarantee profits. Cryptocurrency markets are volatile, and trading involves risk.

The strategy's effectiveness depends on market conditions and settings.

It is recommended to thoroughly backtest the strategy under various market conditions before using it live.

Past performance is not indicative of future results.

IU BBB(Big Body Bar) StrategyDESCRIPTION

The IU BBB (Big Body Bar) Strategy is a price action-based trading strategy that identifies high-momentum candles with significantly larger body sizes compared to the average. It enters trades when a strong bullish or bearish move occurs and manages risk using an ATR-based trailing stop-loss system.

USER INPUTS:

- Big Body Threshold – Defines how many times larger the candle body should be compared to the average body ( default is 4 ).

- ATR Length – The period for the Average True Range (ATR) used in the trailing stop-loss calculation ( default is 14 ).

- ATR Factor – Multiplier for ATR to determine the trailing stop distance ( default is 2 ).

LONG CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is higher than the opening price (bullish candle).

SHORT CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is lower than the opening price (bearish candle).

LONG EXIT:

- ATR-based trailing stop-loss dynamically adjusts, locking in profits as the price moves higher.

SHORT EXIT:

- ATR-based trailing stop-loss dynamically adjusts, securing profits as the price moves lower.

WHY IT IS UNIQUE:

- Unlike traditional momentum strategies, this system adapts to volatility by filtering trades based on relative candle size.

- It incorporates an ATR-based trailing stop-loss, ensuring risk management and profit protection.

- The strategy avoids choppy market conditions by only trading when significant momentum is present.

HOW USERS CAN BENEFIT FROM IT:

- Catch Strong Price Moves – The strategy helps traders enter trades when the market shows decisive momentum.

- Effective Risk Management – The ATR-based trailing stop ensures that winning trades remain profitable.

- Works Across Markets – Can be applied to stocks, forex, crypto, and indices with proper optimization.

- Fully Customizable – Users can adjust sensitivity settings to match their trading style and time frame.

IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different

The Dual SuperTrend with VIX Filter Strategy combines traditional trend following with market volatility analysis. Unlike conventional SuperTrend strategies that focus solely on price action, this experimental system incorporates VIX (Volatility Index) as an adaptive filter to create a more context-aware trading approach. By analyzing where current volatility stands relative to historical norms, the strategy adjusts to different market environments rather than applying uniform logic across all conditions.

BTCUSD 6hr Long Short Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Dual SuperTrend Core

The strategy uses two SuperTrend indicators with different sensitivity settings:

- SuperTrend 1: Length = 13, Multiplier = 3.5

- SuperTrend 2: Length = 8, Multiplier = 5.0

The SuperTrend calculation follows this process:

1. ATR = Average of max(High-Low, |High-PreviousClose|, |Low-PreviousClose|) over 'length' periods

2. UpperBand = (High+Low)/2 - (Multiplier * ATR)

3. LowerBand = (High+Low)/2 + (Multiplier * ATR)

Trend direction is determined by:

- If Close > previous LowerBand, Trend = Bullish (1)

- If Close < previous UpperBand, Trend = Bearish (-1)

- Otherwise, Trend = previous Trend

🔶 VIX Analysis Framework

The core innovation lies in the VIX analysis system:

1. Statistical Analysis:

- VIX Mean = SMA(VIX, 252)

- VIX Standard Deviation = StdDev(VIX, 252)

- VIX Z-Score = (Current VIX - VIX Mean) / VIX StdDev

2. **Volatility Bands:

- Upper Band 1 = VIX Mean + (2 * VIX StdDev)

- Upper Band 2 = VIX Mean + (3 * VIX StdDev)

- Lower Band 1 = VIX Mean - (2 * VIX StdDev)

- Lower Band 2 = VIX Mean - (3 * VIX StdDev)

3. Volatility Regimes:

- "Very Low Volatility": VIX < Lower Band 1

- "Low Volatility": Lower Band 1 ≤ VIX < Mean

- "Normal Volatility": Mean ≤ VIX < Upper Band 1

- "High Volatility": Upper Band 1 ≤ VIX < Upper Band 2

- "Extreme Volatility": VIX ≥ Upper Band 2

4. VIX Trend Detection:

- VIX EMA = EMA(VIX, 10)

- VIX Rising = VIX > VIX EMA

- VIX Falling = VIX < VIX EMA

Local performance:

🔶 Entry Logic Integration

The strategy combines trend signals with volatility filtering:

Long Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bullish (trend = 1)

- AND selected VIX filter condition must be satisfied

Short Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bearish (trend = -1)

- AND selected VIX filter condition must be satisfied

Available VIX filter rules include:

- "Below Mean + SD": VIX < Lower Band 1

- "Below Mean": VIX < VIX Mean

- "Above Mean": VIX > VIX Mean

- "Above Mean + SD": VIX > Upper Band 1

- "Falling VIX": VIX < VIX EMA

- "Rising VIX": VIX > VIX EMA

- "Any": No VIX filtering

█ Trade Direction

The strategy allows testing in three modes:

1. **Long Only:** Test volatility effects on uptrends only

2. **Short Only:** Examine volatility's impact on downtrends only

3. **Both (Default):** Compare how volatility affects both trend directions

This enables comparative analysis of how volatility regimes impact bullish versus bearish markets differently.

█ Usage

Use this strategy as an experimental framework:

1. Form a hypothesis about how volatility affects trend reliability

2. Configure VIX filters to test your specific hypothesis

3. Analyze performance across different volatility regimes

4. Compare results between uptrends and downtrends

5. Refine your volatility filtering approach based on results

6. Share your findings with the trading community

This framework allows you to investigate questions like:

- Are uptrends more reliable during rising or falling volatility?

- Do downtrends perform better when volatility is above or below its historical average?

- Should different volatility filters be applied to long vs. short positions?

█ Default Settings

The default settings serve as a starting point for exploration:

SuperTrend Parameters:

- SuperTrend 1 (Length=13, Multiplier=3.5): More responsive to trend changes

- SuperTrend 2 (Length=8, Multiplier=5.0): More selective filter requiring stronger trends

VIX Analysis Settings:

- Lookback Period = 252: Establishes a full market cycle for volatility context

- Standard Deviation Bands = 2 and 3 SD: Creates statistically significant regime boundaries

- VIX Trend Period = 10: Balances responsiveness with noise reduction

Default VIX Filter Selection:

- Long Entry: "Above Mean" - Tests if uptrends perform better during above-average volatility

- Short Entry: "Rising VIX" - Tests if downtrends accelerate when volatility is increasing

Feel Free to share your insight below!!!

[3Commas] Turtle StrategyTurtle Strategy

🔷 What it does: This indicator implements a modernized version of the Turtle Trading Strategy, designed for trend-following and automated trading with webhook integration. It identifies breakout opportunities using Donchian channels, providing entry and exit signals.

Channel 1: Detects short-term breakouts using the highest highs and lowest lows over a set period (default 20).

Channel 2: Acts as a confirmation filter by applying an offset to the same period, reducing false signals.

Exit Channel: Functions as a dynamic stop-loss (wait for candle close), adjusting based on market structure (default 10 periods).

Additionally, traders can enable a fixed Take Profit level, ensuring a systematic approach to profit-taking.

🔷 Who is it for:

Trend Traders: Those looking to capture long-term market moves.