Volume

Dillon's Double VWAP StrategyThis is based on Dillon's double VWAP strategy.

I enters when the ADX is low (aka not a trending market) and it's not close to the VWAP reset. Check it out.

Big Snapper Alerts R3.0 + Chaiking Volatility condition + TP RSI//@version=5

//

// Bannos

// #NotTradingAdvice #DYOR

// Disclaimer.

// I AM NOT A FINANCIAL ADVISOR.

// THESE IDEAS ARE NOT ADVICE AND ARE FOR EDUCATION PURPOSES ONLY.

// ALWAYS DO YOUR OWN RESEARCH

//

// Author: Adaptation from JustUncleL Big Snapper by Bannos

// Date: May-2022

// Version: R1.0

//Description of this addon - Script using several new conditions to give Long/short and SL levels which was not proposed in the Big Snapper strategy "Big Snapper Alerts R3.0"

//"

//This strategy is based on the use of the Big Snapper outputs from the JustUncleL script and the addition of several conditions to define filtered conditions selecting signal synchrones with a trend and a rise of the volatility.

//Also the strategy proposes to define proportional stop losses and dynamic Take profit using an RSI strategy.

// After delivering the temporary ong/short signal and ploting a green or purple signal, several conditions are defined to consider a Signal is Long or short.

//Let s take the long signal as example(this is the same process with the opposite values for a short).

//step 1 - Long Definition:

// Snapper long signal stored in the buffer variable Longbuffer to say that in a close future, we could have all conditions for a long

// Now we need some conditions to combine with it:

//the second one is to be over the Ma_medium(55)

//and because this is not selective enough, the third one is a Volatility indicator "Chaikin Volatility" indicator giving an indication about the volatility of the price compared to the 10 last values

// -> Using the volatility indicator gives the possibility to increase the potential rise if the volatility is higher compared to the last periods.

//With these 3 signals, we get a robust indication about a potential long signal which is then stored in the variable "Longe"

//Now we have a long signal and can give a long signal with its Stop Loss

// The Long Signal is automatically given as the 3 conditions above are satisfied.

// The Stop loss is a function of the last Candle sizes giving a stop below the 70% of the overall candle which can be assimilated to a Fibonacci level. Below this level it makes sense to stop the trade as the chance to recover the complete Candle is more than 60%

//Now we are in an open Long and can use all the mentioned Stop loss condition but still need a Take Profit condition

//The take profit condition is based on a RSI strategy consisting in taking profit as soon as the RSI come back from the overbought area (which is here defined as a rsi over 70) and reaching the 63.5 level to trigger the Take Profit

//This TP condition is only active when Long is active and when an entry value as been defined.

//Entry and SL level appreas as soon as a Long or short arrow signal does appears. The Take profit will be conidtioned to the RSI.

//The final step in the cycle is a reinitialization of all the values giving the possibility to detect and treat any long new signal coming from the Big Snapper signal.

Ranged Volume DCA Strategy - R3c0nTraderUpdate: Republishing this as Public Open-Source script.

Credits:

Thank you "EvoCrypto" for granting me permission to use "Ranged Volume" to create this strategy.

Thank you "junyou0424" for granting me permission to use "DCA Bot with SuperTrend Emulator" which I used for adding bot inputs, calculations, and strategy

What does this do?

This script is mainly used for backtesting a Ranged Volume strategy to see how a 3Commas bot would perform.

I created this script out of necessity and I wanted a way to test a 3Commas DCA bot with a strategy based on “Volume.”

I came across "EvoCrypto’s" "Ranged Volume" study and strategy in TradingView and I liked it. I wanted to configure it so it can be used for DCA bot backtesting. I used parts from "junyou0424’s" "DCA Bot with SuperTrend Emulator" to add the following:

1. The Start Time and End Time

2. Price deviation to open safety orders (%)

3. Target Take Profit (%)

4. Trailing deviation

5. Base Order and Safety Order

6. Safety order volume scale

7. Safety order step scale

8. Max safety orders

In addition to the above, I also added chart indicators for "Take Profit" as well as "Safety Order"

Pre-requisites:

You can use this script without a 3Commas account and see how 3Commas DCA Bot and Ranged Volume strategy would perform vs. a non-DCA strategy. However, I highly recommend signing up for their free account and going through their training. This would give you a base understanding on the settings you will see in this strategy and why you will need to know them.

That said these are the pre-requisites I suggest you have:

1. Base Knowledge of 3Commas DCA bots

2. Base knowledge of settings such as “Max safety trades count”, “safety order volume scale” and “safety order step scale”. If these are alien to you, I suggest you read up on these.

3. Knowledge of setting up a Single-pair 3Commas bot for receiving custom TradingView signal.

4. A paper-bot to test your ideas. (Do not use a real money bot until you have tested it sufficiently with a paper-bot. You alone are responsible for your results!)

5. Add the study I created called "R3c0nTrader’s Ranged Volume Study” which adds a separate chart in its own pane showing the volume spikes. It will also generate the “buy” signals for your bot. NOTE: The study also has the same color scheme as this strategy and having the colors in both the strategy and the study will make things easier to see. If you use EvoCrypto’s Ranged Volume Study instead, just keep in mind that the colors won’t match, and you will have to manually match them.

6. Make your buy signals from your strategy are the same as in your study! To do this, use the same “Volume Range Length” you entered in the STRATEGY and enter that value for the “Volume Range Length” in the STUDY. Also ensure you have the same settings for “Heikin Ashi” (On or Off).

Comparisons of Ranged Volume Strategy vs Ranged Volume DCA Strategy

BTCUSD

Beware of Strategies that claim super high profits. This can easily be done by lowering the initial capital to something unrealistic. If I did that with this strategy and set the initial capital $100 and base order size to $100, I get a net profit of 2,864% which is not realistic.

How to Use

1. On the “Inputs” tab:

a. Set your Start and End Time to backtest against.

b. Set your “Volume Range Length” (number of bars to look back)

c. “Heikin Ashi Colors” – Usually I leave this enabled

d. “Show Bar Colors” – Leave enabled

e. “Show Break-Out” – Leave enabled

f. “Show Range” – Leave enabled

g. Set your other inputs which are those settings you would find in your 3Commas bot that you want to test (e.g., Price deviation to open safety orders, Target Take Profit, Base order, Safety order, etc.).

h. Quick Example for BTCUSD on 2hr chart:

i. Price deviation to open safety orders (%) = 6

ii. Target Take Profit (%) = 14

iii. Trailing deviation = 0

iv. Base order = 100

v. Safety order = 200

vi. Safety order volume scale = 2

vii. Safety order step scale = 1.4

viii. Max safety order = 5

2. On the “Properties” tab, set your initial capital, base currency, etc.

a. Initial capital – Default is 10,000 (Please use realistic values here. The amount here should be able to cover ALL your safety orders if they were triggered. Ideally, you should have funds left over and not use all trade capital.)

b. Base currency – Select your currency

c. Order Size - Not used. Use the “Inputs” tab to change your base order size.

d. Leave “Pyramiding” set to 999. This acts as a ceiling to the “Max safety orders” on the “Inputs” tab. It must always be higher than your “Max safety orders.” For example, if you set your “Max safety orders” to “4” and “Pyramiding” to “4” then it effectively means you have “3” “Max safety orders” and not “4” because it is counting each successive entry including the initial order.

e. “Commission” - Optional

f. “Verify price for limit orders” – Leave at zero. This does not change anything that I can tell.

g. Optional - Enter a value for “Commission”

h. Slippage – Optional. Slippage does not occur in backtesting but does occur in real trading but it can be simulated. Example use case for tracking performance of a real money bot: You enter the start date and time of your bot’s trade into this strategy and you notice some values are a little off due to slippage (average price, take profit, safety orders are not lining up) then you would go back here and increase the slippage until those lines up close enough with your actuals.

i. Margin for long positions – I don’t use this honestly.

j. Margin for short positions – I don’t use this honestly.

k. Recalculate “After order is filled” and “On every tick” – I don’t use this honestly.

3. “Style” tab

a. Ranged Volume Bar Coloring - You must disable bar coloring in any studies you added or this may not work properly

i. Color 0 – Default Yellow; appears when a volume breakout occurs

ii. Color 1 – Default Red; appears when a volume breakdown occurs

iii. Color 2 – Light Blue; appears when Close is higher than the Open

iv. Color 3 – Dark Blue; appears when the Close is lower than the Open

b. Take profit – Default Green; take profit line

c. Safety order – Default Light Blue; safety order line

d. No Safety Orders left – Default Red; when a trade runs out of safety orders, the line turns red and there is no safety orders left underneath to catch any further falling price movements.

e. Avg Position Price – Default Orange; your average position price for any given trade.

f. Take Profit Plot Area – Default Green; creates a highlighted area for your take profit

g. SO Plot Area – Default Light Blue; creates a highlighted area for your safety orders

h. Trades on chart – Show or hide your trades on the chart

i. Signal labels – Show or hide the trade signal labels on the chart

j. Quantity – Show or hide the trade quantity on the chart

Explanation of Chart lines and colors on chart

Buy/Sell StratThis strategy will produce a buy or sell signal when the following criteria are met:

9 EMA crosses 21 EMA

Recently closed candlestick has 15% higher average volume than previous 5 candles

A candlestick reversal pattern

Price crosses 9 EMA

Feel free to use and modify as you see fit. Happy trading!

TASC 2022.04 S&P500 Hybrid Seasonal System█ OVERVIEW

TASC's April 2022 edition of Traders' Tips includes the "Sell In May? Stock Market Seasonality" article authored by Markos Katsanos. This is the code implementing the "Hybrid Seasonal System" from the article.

█ CONCEPTS

In his article, Markos Katsanos takes an updated look at the "Sell in May" adage by reviewing recent historical data for seasonal equity market tendencies. The author explores the development of a trading strategy (a set of buy and sell rules) based on this research.

He starts from the enhanced buy & hold system featured in his July 2021 TASC article, and adds additional technical conditions. These include volatility conditions ( VIX and ATR ) plus the "Volume Flow Indicator" (VFI), which is a custom money flow indicator that Katsanos introduced in his June 2004 TASC article. He provides an example of a trading system that others can test for themselves and modify as they see fit. The author notes that the system could likely be improved further by adding money management conditions (such as a stop-loss), or by adding more technical conditions not considered in the scope of this article.

█ CALCULATIONS

The entry and exit rules that constitute the trading system are defined below. The critical values of VIX, ATR and VFI (specified below) used in the calculations were determined by optimization for a daily chart of the SPY ETF . By default, the strategy only allows long entries. However, the script offers the possibility to initiate short entries upon exiting long trades through the "Long Only" toggle in the script's inputs.

Long Entry Rules

• Seasonal: The seasonal trade is initiated on the first business day October at the open.

• Volatility: In case of high volatility, that is if the VIX is above 60% or the 15-day ATR was above 90% over the past 25 days, the seasonal trade is deferred until later in the month or year, when the volatility subsides.

Exit/Short Entry Rules

• Seasonal: The exit/short signal is triggered on the first business day of August at the open.

• Volatility: The exit/short signal is triggered if VIX is above 120 % (i.e. 2 times the corresponding threshold parameter).

• Money flow (VFI): The exit/short signal is triggered if the VFI crosses under a critical value (-20) while its 10-day moving average is pointing down.

Join TradingView!

Volume fight strategyThe Volume fight strategy looks for the predominance of bullish or bearish trading volume on the chart by dividing the trading volume in the bar into 2 parts - "bullish volume" and "bearish volume", and comparing the weighted average values by volume with each other at a given distance.

This strategy is suitable for any instrument (cryptocurrency, Forex, stocks) and is able to work on any TF.

The Volume fight strategy should be used as an auxiliary indicator that tells you who is currently prevailing in the market - " bulls "or"bears".

To configure the strategy , it is necessary to set the range of evaluation of the predominance of bullish or bearish volume (the number of bars, by default-24 bars for TF=1H). The smaller the TF, the higher the range value should be used to filter out false signals.

When there is a predominance of "bulls" on the chart, a green triangle appears (relevant at the close of the bar) and the histogram is highlighted in green, when "bears" appear on the chart, a red triangle appears (relevant at the close of the bar) and the histogram is highlighted in red.

In the strategy settings, there is smoothing to reduce false signals and highlight the flat zone by specifying a percentage, at least which should be the difference between the forces of the "bullish" and "bearish" volume . If the difference between the volume forces is less than the specified one (by default-15%), the zone is considered flat and is displayed in gray on the histogram.

If you set the percentage to zero, the flat zones will not be highlighted, but there will be much more false signals, since the strategy becomes very sensitive when the smoothing percentage decreases.

There is a function-to show the color background of the current trading zone. For" bullish "- green, for" bearish " - red.

In the settings, you can enable the display and use of each signal in the trading zone, not only the initial one, but also each after the flat zone. By default, only the signal of the beginning of the ascending/descending zone is used.

The strategy has alerts for "bullish" and "bearish" movements.

👉Use alerts - "alert() function calls only"

If you have any questions, you can write to me in private messages or by using the contacts in my signature.

----------------------------------------------------

Стратегия Volume fight ищет на графике преобладание бычьего или медвежьего объёма торгов путём разделения торгового объёма в баре на 2 части - "бычий объём" и "медвежий объём", и сравнения средне-взвешенных значений по объёму между собой на заданной дистанции.

Данная стратегия подходит для любого инструмента (криптовалюта, Forex, акции) и способен работать на любом ТФ.

Стратегию Volume fight следует использовать как вспомогательный индикатор, который подсказывает Вам кто сейчас преобладает на рынке - "быки" или "медведи".

Для настройки стратегии необходимо выставить диапазон оценки преобладания бычьего или медвежьего объема (количество баров, по умолчанию - 24 бара для ТФ=1Ч). Чем меньше ТФ, тем выше следует использовать значение диапазона, чтобы отфильтровать ложные сигналы.

При возникновении преобладания на графике "быков" появляется зелёный треугольник (актуален по закрытию бара) и гистограмма подсвечивается зелёным цветом, при возникновении на графике "медведей" появляется красный треугольник (актуален по закрытию бара) и гистограмма подсвечивается красным цветом.

В настройках стратегии есть сглаживание для уменьшения ложных сигналов и выделения зоны флета с помощью указания процента, не менее которого, должна быть разница между силами "бычьего" и "медвежьего" объёма. Если разница между силами объёмов меньше заданного (по умолчанию - 15%), то зона считается флетовой и отображается на гистограмме серым цветом.

Если выставить процент равным нулю, то зоны флета выделяться не будут, но будет гораздо больше ложных сигналов, так как стратегия становится очень чувствительной при снижении процента сглаживания.

Есть функция - показывать цветовой фон текущей торговой зоны. Для "бычьего" - зелёный, для "медвежьего" - красный.

В настройках можно включить отображение и использование каждого сигнал в торговой зоне, не только начального, но и каждого после зоны флета. По умолчанию - только сигнал начала восходящей/нисходящей зоны.

Стратегия имеет оповещения для "бычьего" и "медвежьего" движения.

👉 Используйте оповещения - "Только при вызове функции alert()".

По любым вопросам Вы можете написать мне в личные сообщения или по контактам в моей подписи.

Logistic strategyThis strategy is loosely based on the logistic function. This function is often used to model population growth. I used it here to model price change using the z-score of net volume as the parameter to the exponential function.

3 Indicator Strategy (StochRSI, MFI & EMA) With Safety OrdersThis strategy uses Stochastic RSI, Money Flow Index and EMA with settings for lower time-frames.

It also features safety orders based on 3 different take profit and stop loss methods.

Recommended Indicator Settings for lower time-frames;

Stoch RSI: 1,1,100,100

MFI: 30

EMA: 100

Take Profit/Stop Loss Settings:

There are 3 TP/SL types available;

- Pips -> based on minticks

- Base Value -> manually entering a value for the actual profit/loss.

- Opposite Signal -> e.g. if the current open order is long, strategy waits for the next short signal.

Super Breakout day trading This is an intraday indicator which uses Bollinger band and volume flow and MA to alert buy and sell signal.

A user can use this indicator to help make entry and exits. This indicator wont show entry and exist of larger time frames like Day week month.

This indicator uses Bollinger bands but try to minimize it shortcoming where it will buy and keep holding and eventually sell at a loss.

By adding addition parameters around volume it check if the price has reached its peak

Dollar cost averaging This is a testing startergy based on dollar cost averaging and sell on high points.

Swing VWAP Crypto and Stocks StrategyThis is a strategy designed for swing trading on markets such as crypto and stocks.

Its components are:

VWAP

Time Management

Risk management

Rules for entry:

We entry only on Monday, if our close of the candle crossed above VWAP

Rules for exit

We exit always on Sunday or if we either hit the TP/SL levels.

If you have any questions let me know

LPB MicroCycles StrategyWhat it is:

We use the Hodrick-Prescott filter applied to the closing price, and then take the outputted trendline and apply a custom vwap, the time frame of which is based on user input, not the default 1 day vwap . Then we go long if the value 2 bars ago is greater then one bar ago. We sell and color the bars and lines when the if the value of 2 bars ago is less than one bar ago.

Also included:

GUI for backtesting

ATR Based Stop Loss

How to use:

Go long when the indicators suggest it, and use the stop losses to reduce risk.

Best if paired with a volatility measurement (inside candles, average true range , bollingerband%B)

Volume Difference Delta Cycle OscillatorVolume Difference Delta Cycle Oscillator indicator:

Using the power of my Volume Difference Indicator and standard deviations based on Bollinger Bands and more, we present this wonderful indicator with the following features:

Price Action Histogram: This is the bread and butter of this graph, if the PAH is above 0, this is considered a BULL cycle, and if below 0, this is considered a BEAR cycle. The histogram will move up and down based on the Histagram settings you set in the properties field. Be careful, we advise using default settings.

Custom Overbought & Oversold Lines:mean

These lines can be used to identify when to buy and sell the security, and help you make sense of the action of the histogram. Change the color, size, and linewidth!

These lines are what are used to perform the trades with the strategy as well, so if you change them, they will make an impact on the strategy itself.

EzSpot Background:

Do you want to turn your brain off and just trade when you you're inside an Overbought or Oversold line? Awesome! Turn on EzSpot backgrounds, and when it's green, go long, when it's red go short! Simple as that!

How it works:

By taking the Delta of the Volume Difference Indicator we're able to find the rate of change of the amount of change of volume, allowing us to see changes in volume before price changes. To add onto these, we supercharge it by taking the output of this line as the input source of bollinger bands which we use to output the %B of the Delta of the Volume Difference Indicator.

Separately, we calculate the %B of the current close to use later.

The final step is taking the second %B (which is an indication of where price lies on the curve of historical price data), and from it subtract the first %B, which allows us to visualize the standard deviation of the closing price, minus the standard deviation of Delta of the Volume Difference , which in essence allows us to see when volume changes but price does not and vice versa.

This final output is then plotted along with an over bought and over sold line, which we use to perform our trades on.

Simplified: This indicator shows the cycles of price action - volume based on the rate of the rate of volume changes based on price and the closing price.

Super Simple: Notice when volume increases but price hasn't, and vice versa with this indicator.

BBPBΔ(OBV-PVT)BB - Time Series Decomposition & Volume WeightedThis is an indicator that shows 5 different points of information:

#1 The Trendline is uses a time-series decomposition to remove noise and seasonality data to provide a trendline without using moving averages. This is then further processed by a custom VWAP block that weights it based on the time frame you're currently using.

#2 BB%B - This is the blue histogram that's partially transparent. This is used to find when a security is overbought or oversold.

#3 BB%B of the Δ(OBV-PVT). This is the green histogram. We took the OBV and subtracted the PVT from it, then we found the delta of that compared to the previous candle. This output a line, which we wrapped in bollinger bands to find the BB%B of this line. This line is represented as a histogram, for visual clarity.

#4 Long and Short Indicators: Long is represented by a green dot, and short is represented by a red dot.

#5 Zones - there are multiple zones, which are used to identify overbought and oversold zones.

How to use the indicator:

Simple way: Long on green dot, Short on red dot. Use stop losses and take profits.

Slightly More Complex: Same as above, but also close out longs, when the green histogram drops but the blue does not. As this means price action hasn't caught up with volume. Use stop losses and take profits.

Full Usage: Long only when both the green, blue and yellow lines are below 0, and sell when the blue or green histogram rises above 1. Perform the opposite for the shorting. Ignore the dots if you use this method, they are for simple reference points til you get used to this indicator. Use stop losses and take profits.

Supertrend + Stoch Strategy Multi-pair Signal AlarmBITSTAMP:BTCUSD

An entry alarm on Supertrend Stoch Strategy . It can monitor 10 trading pairs in one alarm.

Use this script on any trading pair and deploy the alarm. The alert comment shows the pair name, direction, entry point, sl/tp, and percentage of your position you should cost.

I currently use it as a signal for my grid trading.

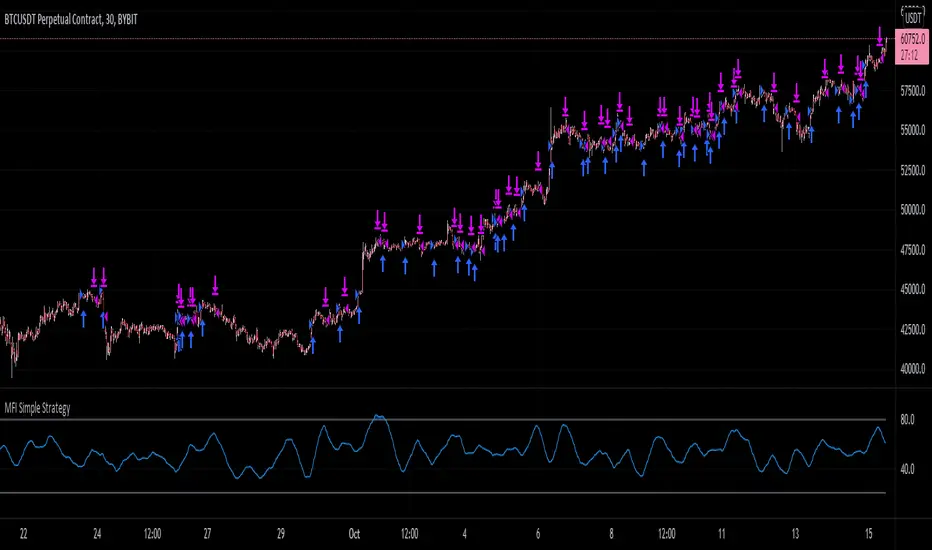

MFI Simple StrategyHere I've made a simple strategy based off a simple moving average of an MFI length.

Back tested on a BYBIT:BTCUSDT 30m chart.

Conditions:

---When the price is above the golden SMA of 200 bars---

- Buy: when MFI is moving up

- Sell: when MFI is moving down

- Stop: golden SMA of 200 bars

If you would like alerts:

1.) Add the strategy to your chart,

2.) Go to "Create Alert",

3.) Select "MFI Simple Strategy" in your alert creator,

4.) Select whatever notifications settings or message settings,

5.) Finally, click "Create" and you're good to go.

Disclaimer: Please do your own research before making any decisions financially. Past results do not guarantee future results.

Bollinger band & Volume based strategy V2this script is upgraded version of previous one the major change is deleted script which find a highest price after entry the last of strategy is same.

If current volume is above daily average volume, and three bollinger band`s Standard Deviation, 1 and 1.5 and 2 if the current lowest price is bigger then 1 stdev and current closed is bigger then 1.5 stdev and the last,highest price is above 2.0 stdev, it defined current market is bullish and had momentum.

and the Short will entered when ma60 and ma120 is undercrossed it work as prevent current price is way lower then entry price.

**this script is working in 15min Only in BTC market or USDT**

** basic equity setting is 500$, set your own**

**if you will use this in real-trade,plz comment the result to me**

Ps: i wanna know why my script is only working well in 15 min tick, anyone who has similar phenomenon or if you had a answer about it, please comment me.

Vol ST VMThis script works with super trend and volume. Based on super trend and MA signal we can go for buy/sell.

Use min 1Hr time frame.

We can use this mostly for 24Hr markets.

Volume and Moving average,will this model working in real-trade?i`ve recently made this script through few month,understand me if there are some incorrect grammar or something.

basically this script is based on moving average strategy and the bollinger bands

if the buy volume is bigger than sell volume,also buy volume is bigger then daily average volume than it`s defined current market is bullish and entered(of course there is some other conditions)

the exit condition is find the highest price after entered,keep refresh the highest price through time and then,if the current price is ?%lower then highest price,it will closed the position.

my question is this : 1 this model will working in real-trade?

2 why the winning rate is 100%?

- i`ve coded if the position margin over -10%,close the position this code isn`t work? or the other profit line is prevent that happened?

Daily HIGH/LOW strategyThis is a DAILY High/LOW strategy combined with a moving average and volume for more accuracy.

The rules are simple :

For long if we had a cross of the high with the previous high and close of the candle is above moving average and chaikin money flow volume is positive we have a long entry.

We exit when we cross down the moving average with the close of the candle.

For short if we had a crossdown of the low with the previous low and close of the candle is below moving average and chaikin money flow volume is negative we have a short entry.

We exit when we cross above the moving average with the close of the candle.

This strategy has no risk management inside so use it with caution.

If you have any questions, let me know

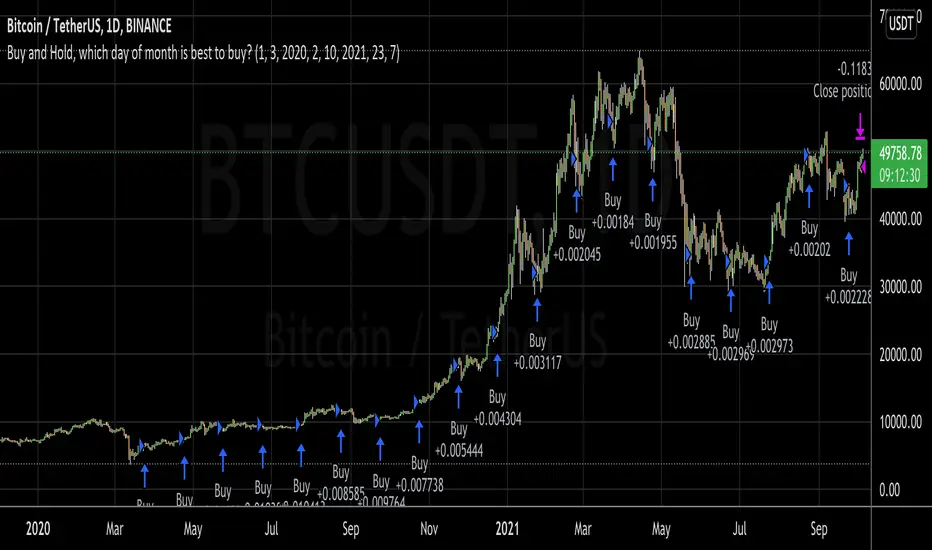

Buy and Hold, which day of month is best to buy?I wanted to invest a certain fiat amount each month and was wondering which day would be best to do this.

So, with this script, you can set your entry day. On the last day of the date range, it will close all positions. You can then see what amount of the asset you have accumulated to date. If you try all the days of the month and see when you can sell the most amount of the asset, you've found the best buy date of the month for that asset.

A second option is to set an exit day. This is good for a strategy where you would go long (buy) on the entry date and short (sell) on the exit day.

This was inspired by people running out of money by the end of the month and selling their asset, which could make the price fall. Then when they receive the wages by the 5th or so, they would rebuy, causing the price to go up.

TemaVWAPRSI StrategyExchange: Kraken

Timeframe: 5m

Pair: ETH/USD

If you use this for any other exchange or pair, you'll have to tweak the settings, most importantly are the trailing stop ticks. This strategy is currently in what I would call beta mode. It uses the volume weighted average price indicator, rate of change, two triple exponential moving averages and the relative strength index to find buy and sell signals.