Uptrick: Logarithmic Crypto Bands

Description :

Introduction

The `Uptrick: Logarithmic Crypto Bands` indicator introduces an innovative approach to technical analysis tailored specifically for the cryptocurrency markets. By leveraging logarithmic transformations combined with dynamic exponential bands, this indicator offers a sophisticated method for identifying critical support and resistance levels, assessing market trends, and evaluating volatility. Its unique approach stands out from traditional indicators by addressing the specific challenges of high volatility and erratic price movements inherent in cryptocurrency trading.

Originality and Usefulness

** 1. Unique Logarithmic Transformation: **

- Innovation : Unlike traditional indicators that often use raw price data, the Uptrick: Logarithmic Crypto Bands applies a logarithmic transformation to the closing prices: logPrice = math.log(close). This approach is original because it reduces the impact of extreme price fluctuations, providing a smoother and more stable price series. This transformation addresses a common issue in cryptocurrency markets where large price swings can obscure true market trends.

- Advantage : The logarithmic transformation compresses the price range, which allows traders to better identify long-term trends and reduce the noise caused by outlier price movements. This results in a more reliable basis for analysis and enhances the ability to detect meaningful market patterns.

**2. Dynamic Exponential Bands :**

- Innovation : The indicator employs exponential calculations to derive dynamic support and resistance levels based on a central base line : baseLine * math.pow(multiplier, n). Unlike static bands that remain fixed regardless of market conditions, these bands adjust dynamically according to market volatility.

- Advantage : The dynamic nature of the bands provides a more responsive and adaptive tool for traders. As market volatility changes, the bands widen or narrow accordingly, offering a more accurate reflection of potential support and resistance levels. This adaptability improves the tool's effectiveness in varying market conditions compared to static or traditional bands.

Detailed Description and Substantiation

**1. Logarithmic Price Calculation :**

- Code : ` logPrice = math.log(close)

- Description : This calculation converts the closing price into its logarithmic value. By compressing the price range, it minimizes the distortion caused by extreme price movements, which can be particularly pronounced in the volatile cryptocurrency markets.

- Purpose : To provide a stabilized price series that facilitates more accurate trend analysis and reduces the influence of erratic price fluctuations.

**2. Moving Averages of Logarithmic Prices :**

- ** Long-Term Moving Average :**

- Code : maLongLogPrice = ta.sma(logPrice, longLength)

longLength = 2000

- ** Description : A simple moving average of the logarithmic price over a long period. This average helps filter out short-term noise and provides insight into the long-term market trend.

- Purpose : To offer a perspective on the overall market direction, making it easier to identify enduring trends and distinguish them from short-term price movements.

- Short-Term Moving Average :

- Code : maShortLogPrice = ta.sma(logPrice, shortLength) shortLength = 900

- Description : A simple moving average of the logarithmic price over a shorter period. This component captures more immediate price trends and potential reversal points.

- Purpose : To detect short-term trends and changes in market direction, allowing traders to make timely trading decisions based on recent price action.

**3. Base Line Calculation :**

- Code : baseLine = math.exp(maShortLogPrice)

- Description : Converts the short-term moving average of the logarithmic price back to the original price scale. This base line serves as the central reference point for calculating the surrounding bands.

- Purpose : To establish a benchmark level from which the exponential bands are calculated, providing a central reference for assessing potential support and resistance levels.

**4. Band Calculation and Plotting :**

- ** Code :**

- Band 1: plot(baseLine * math.pow(multiplier, 1), color=color.new(color.yellow, 20), linewidth=1, title="Band 1")

- Band 2: plot(baseLine * math.pow(multiplier, 2), color=color.new(color.yellow, 20), linewidth=1, title="Band 2")

- Band 3: plot(baseLine * math.pow(multiplier, 3), color=color.new(color.yellow, 20), linewidth=1, title="Band 3")

- Band 4: plot(baseLine * math.pow(multiplier, 4), color=color.new(color.yellow, 20), linewidth=1, title="Band 4")

- Band 5: plot(baseLine * math.pow(multiplier, 5), color=color.new(color.yellow, 10), linewidth=1, title="Band 5")

- Band 6: plot(baseLine * math.pow(multiplier, 6), color=color.new(color.yellow, 0), linewidth=1, title="Band 6")

- * Multiplier : Set at 1.3, adjusts the spacing between bands to accommodate varying levels of market volatility.

- Description : Bands are plotted at exponential intervals from the base line. Each band represents a potential support or resistance level, with the spacing between them increasing exponentially. The color opacity of each band indicates its level of significance, with closer bands being more relevant for immediate trading decisions.

** How to Use the Indicator :**

**1. Identifying Support and Resistance Levels :**

- Support Levels : The lower bands, closer to the base line, can act as potential support levels. When the price approaches these bands from above, they may indicate areas where the price could stabilize or reverse direction.

- Resistance Levels : The upper bands, further from the base line, serve as resistance levels. When the price nears these bands from below, they can act as barriers to price movement, potentially leading to reversals or stalls.

**2. Confirming Trends :**

- Uptrend Confirmation : When the price consistently remains above the base line and moves towards higher bands, it signals a strong bullish trend. This confirmation helps traders capitalize on upward price movements.

- Downtrend Confirmation : When the price stays below the base line and approaches lower bands, it indicates a bearish trend. This confirmation assists traders in acting on downward price movements.

3. Analyzing Volatility :

- Wide Bands : Wider spacing between bands reflects higher market volatility. This indicates a more turbulent trading environment, where price movements are less predictable. Traders may need to adjust their strategies to handle increased volatility.

- Narrow Bands : Narrower bands suggest lower volatility and a more stable market environment. This can result in more predictable price movements and clearer trading signals.

**4. Entry and Exit Points :**

- Entry Points : Consider buying when the price bounces off the base line or a band, which could signal support in an uptrend.

- Exit Points : Evaluate selling or taking profits when the price nears upper bands or shows signs of reversal at these levels. This approach helps in locking in gains or minimizing losses during a downtrend.

**Chart Example:**

Here you can see how the price reacted getting closer to this level. All green circles show a bounce-off. So just from looking at the chart we can see a potential bounce again pretty soon.

** Disclosure :**

- ** Performance Claims :** The `Uptrick: Logarithmic Crypto Bands` indicator is designed to assist traders in analyzing price levels and trends. It is important to understand that this tool provides historical data analysis and does not guarantee future performance. The features and benefits described are based on historical market behavior and should not be seen as a prediction of future results. Traders should use this indicator as part of a broader trading strategy and consider other factors before making trading decisions.

Bands and Channels

Volatility with Power VariationVolatility Analysis using Power Variation

The "Volatility with Power Variation" indicator is designed to measure market volatility. It focuses on providing traders with a clear understanding of how much the market is moving and how this movement changes over time.. This indicator helps in identifying potential periods of market expansion or contraction, based on volatility.

What the indicator does:

This indicator analyzes volatility which refers to the degree of variation in the returns of a financial instrument over time. It's an important measure to understand how much the price and returns of a asset fluctuates. High volatility means large price swings, meanwhile low volatility indicates smaller and consolidating movements. Realized (Historical) Volatility refers to volatility based on past price data.

Power Variation

Power Variation is an extension of the traditional methods used to calculate realized volatility. Instead of simply summing up squared returns (as done in calculating variance), Power Variation raises the magnitude of returns to a power p . This allows the indicator to capture different types of market behavior depending on the chosen value of p .

When P = 2, the Power variation behaves like a traditional variance measure. Lower values of p (e.g., p=1) make the indicator more sensitive to smaller price changes, meanwhile higher values make it more responsive to large jumps, but smaller price moves wont affect the measure that much or won't most likely.

Bipower Variation

Bipower variation is another method used to analyze the changes in price. It specifically isolates the continuous part of price movements from the jumps, which can help by understanding whether volatility is coming from regular market activity or from sharp, sudden moves.

How to Use the Indicator.

Understand Realized and Historical Volatility. Volatility after periods of low volatility you can eventually expect a expansion or an increase in volatility. Conversely, after periods of high volatility, the market often contracts and volatility decreases. If the variation plot is really low and you start seeing it increasing, shown by the standard deviation channels and moving average and you see it trending and increasing then that means you can expect for volatility to increase which means more price moves and expansions. Also if the scaling seems messed up, then use the logarithmic chart scale.

Uptrick: Price Exaggerator

## Uptrick: Price Exaggerator

** Purpose and Overview **:

The "Uptrick: Price Exaggerator" is an innovative Pine Script™ indicator that provides traders with a unique way to visualize potential price extremes. Unlike traditional indicators that focus on historical price data or statistical patterns, this script applies dynamic multipliers to the asset’s closing price to project exaggerated price levels. This approach offers fresh insights into potential market extremes and can be particularly useful for identifying possible overbought or oversold conditions.

** Functionality **:

- ** Dynamic Price Exaggeration **: This script applies a range of multipliers to the closing price to generate several projected price levels. These levels are plotted as lines on the chart, helping traders visualize potential future price extremes beyond typical market ranges.

- ** Highly Customizable **: Users can adjust multipliers, select different source prices (like open, high, low), and choose colors to match their trading strategies and preferences.

- ** Real-Time Updates **: The plotted levels update in real-time, reflecting the latest market conditions and providing an ongoing perspective on potential price extremes.

** Detailed Inputs and Configuration **:

1. ** Multiplier Settings **:

- ** Purpose **: Adjusts the degree of price exaggeration to visualize potential extreme price levels.

- ** Inputs **:

- **Multiplier 1**: Default 0.9 (90% of the source price)

- **Multiplier 2**: Default 0.8 (80% of the source price)

- **Multiplier 3**: Default 1.1 (110% of the source price)

- **Multiplier 4**: Default 1.2 (120% of the source price)

- **Multiplier 5**: Default 1.5 (150% of the source price)

- ** Impact **: Higher multipliers show more distant potential levels, indicating possible resistance or support at extreme levels. Lower multipliers highlight nearer levels, suggesting smaller potential movements.

2. ** Source Price Selection **:

- ** Purpose **: Determines the base data for calculating exaggerated price levels.

- **Inputs**:

- **Source 1**: Default is closing price (can be customized)

- **Source 2**: Default is closing price

- **Source 3**: Default is closing price

- **Source 4**: Default is closing price

- **Source 5**: Default is closing price

- ** Customization **: Users can select various sources (e.g., open, high, low) for each multiplier, tailoring the tool to their analytical needs.

3. ** Color Customization **:

- ** Purpose **: Enhances visual clarity by distinguishing between different exaggerated levels.

- **Inputs**:

- **Color 1**: Default red

- **Color 2**: Default blue

- **Color 3**: Default green

- **Color 4**: Default orange

- **Color 5**: Default purple

- ** Customization **: Colors can be adjusted to fit user preferences and chart color schemes.

4. ** Plotting the Lines **:

- ** Purpose **: Provides a visual representation of potential future price extremes on the chart.

- ** Implementation **: Lines are plotted based on the selected multipliers and source prices, offering a clear view of potential price scenarios.

** Using the Script for Market Analysis **:

1. ** Identifying Overbought Conditions **:

- ** Method **: Observe exaggerated price levels above the current market price. Approaching or exceeding higher multiplier levels may indicate overbought conditions.

- ** Analysis **: These levels can act as potential resistance zones where price reversals or consolidations might occur.

2. ** Spotting Oversold Conditions **:

- ** Method **: Observe exaggerated price levels below the current market price. If the price approaches or falls below lower multiplier levels, it may suggest oversold conditions.

- ** Analysis **: These levels might serve as support zones where price bounces or stabilization could happen.

3. ** Detecting Smaller Movements **:

- **Detailed Examination**: Lower multiplier levels can highlight minor support and resistance levels, useful for traders focusing on smaller price fluctuations.

- ** Fine-Tuning **: Adjust multipliers to zoom in on specific price ranges and better detect small market movements.

** How to Use the Script **:

1. ** Add the Script to Your Chart **:

- Scroll to the bottom of this description and right where there is the source code, click ' Add to Favourites ' - Now you can go to a chart, go to your ' favorites ', and you will find it there.

2. ** Configure Inputs **:

- Click the gear icon next to the script in the indicators panel to open settings.

- Adjust multipliers, source prices, and colors according to your analysis needs.

3. ** Interpret the Levels **:

- Analyze the plotted levels to assess potential overbought or oversold conditions and identify possible price extremes.

- Combine insights with other indicators and patterns for more informed trading decisions.

** Conceptual Framework **:

The "Uptrick: Price Exaggerator" offers a novel approach to market analysis by exaggerating price levels through dynamic multipliers. This unique method extends beyond conventional indicators, providing traders with a different perspective on potential price movements and market extremes. By customizing inputs and visualizing potential price scenarios, this script enhances market analysis and supports diverse trading strategies.

** Originality and Uniqueness **:

This script stands out by applying dynamic multipliers to the source price, offering a fresh way to anticipate potential market extremes. Unlike standard indicators, which often rely on historical data or statistical methods, the "Uptrick: Price Exaggerator" provides a distinctive view of future price levels. Its customizable features and real-time updates offer traders a flexible tool that can adapt to various market conditions and personal trading styles.

Harmonic Moving Average Confluence with Cross SignalsHarmonic Moving Average Confluence with Cross Signals

Overview:

The "Harmonic Moving Average Confluence with Cross Signals" is a custom indicator designed to analyze harmonic moving averages and identify confluence zones on a chart. It provides insights into potential trading opportunities through cross signals and confluence detection.

Features:

Harmonic Moving Averages (HMAs):

38.2% HMA

50% HMA

61.8% HMA

These HMAs are calculated based on a base period and plotted on the chart to identify key support and resistance levels.

Cross Detection:

Buy Signal: Triggered when the 38.2% HMA crosses above the 50% HMA.

Sell Signal: Triggered when the 38.2% HMA crosses below the 50% HMA.

Buy signals are marked with green triangles below the candles.

Sell signals are marked with red triangles above the candles.

Confluence Detection:

Confluence zones are identified where two or more HMAs are within a specified percentage difference from each other.

Confluence Strength: Default minimum strength is set to 3.

Threshold Percentage: Default is set to 0.0002%.

Confluence zones are marked with blue circles on the chart, with 80% opacity.

Default Settings:

Base Period: 50

Minimum Confluence Strength: 3

Confluence Threshold: 0.0002%

Confluence Circles Opacity: 80%

How to Use It:

Setup:

Add the indicator to your trading chart.

The indicator will automatically calculate and plot the harmonic moving averages and detect cross signals and confluence zones based on the default settings.

Interpreting Signals:

Buy Signal: Look for green triangles below the candles indicating a potential buying opportunity when the 38.2% HMA crosses above the 50% HMA.

Sell Signal: Look for red triangles above the candles indicating a potential selling opportunity when the 38.2% HMA crosses below the 50% HMA.

Confluence Zones: Blue circles represent areas where two or more HMAs are within the specified threshold percentage, indicating potential trading zones.

Adjusting Parameters:

Base Period: Adjust to change the period of the moving averages if needed.

Minimum Confluence Strength: Set to control how many confluence zones need to be present to display a circle.

Threshold Percentage: Set to adjust the sensitivity of confluence detection.

Usage Tips:

Use the signals in conjunction with other technical analysis tools to enhance your trading strategy.

Monitor confluence zones for possible high-interest trading opportunities.

I hope this version aligns better with your needs. If there's anything specific you'd like to adjust or add, just let me know!

TrendFusion [CrypTolqa]This code colors the SMA line red when the RSI is below 50 and the CCI is below 0, and green when the RSI is above 50 and the CCI is above 0. For cases that do not meet the specified details, the line is displayed in gray.

Helacator Ai ThetaHelacator Ai Theta is a state-of-the-art advanced script. It helps the trader find the possibility of a trend reversal in the market. By finding that point at which the three black crows pattern combines with the three white soldiers pattern, it is the most cherished pattern in technical analysis for its signal of strong bullish or bearish momentum. Therefore, it is a very strong predictive tool in the ability of shifting markets.

Key Highlights: Three White Soldiers and Three Black Crows Patterns

The script identifies these candlestick formations that consist of three consecutive candles, either bullish (Three White Soldiers) or bearish (Three Black Crows). These patterns help the trader identify possible trend reversal points as they provide an early signal of a change in the market direction. It is with great care that the script is written to evaluate the position and relationship between the candlesticks for maintaining the accuracy of pattern recognition. Moving Averages for Trend Filtering:

Two important ones used are moving averages for filtering any signals not in accordance with the general trend. The length of these MAs is variable, allowing the traders to be in a position to adapt the script for use under different market conditions. The moving averages ensure that signals are only taken in the direction that supports the general market flow, so it leads to more reliability within the signals. The MAs are not plotted on the chart for the sake of clarity, but they still perform a crucial function in signal filtering and can be displayed optionally for a more detailed investigation. Cooldown filter to reduce over-trading

This is part of what is implemented in the script to prevent generation of consecutive signals too quickly. All this helps to reduce market noise and not overtrade—only when market conditions are at their best. The cooldown period can be set to be adjusted according to the trader's preference, making the script more versatile in its use. Practical Considerations: Educational Purpose: This script is for educational purposes only and should be part of a comprehensive trading approach. Proper risk management techniques should be observed while at the same time taking into consideration prevailing market conditions before making any trading decision.

No Guaranteed Results: The script is aimed at bringing signal accuracy into improvement to align with the broader market trend and reducing noise, but past performance cannot guarantee future success. Traders should use this script within their broad trading approach. Clean and Simple Chart Display: The primary goal of this script is to have a clear and simple display on the chart. The signals are prominently marked with "BUY" and "SELL," and the color of the bars has changed according to the last signal, thus traders can easily read the output. Community and Open Source Open Source Contribution: This script is open for contribution by the TradingView community. Any suggestions regarding improvements are highly welcomed. Candlestick patterns, moving averages, and the combination of the cooldown filter are presented in such a way as to give traders something special, and any modifications or extra touch by the community is appreciated. Attribution and Transparency: The script is based on standard technical analysis principles and for all parts inspired by or derivated from other available open-source scripts, credit is given where it is due. In this way, transparency ensures that the script adheres to TradingView's standards and promotes a collaborative community environment.

D-Shape Breakout Signals [LuxAlgo]The D-Shape Breakout Signals indicator uses a unique and novel technique to provide support/resistance curves, a trailing stop loss line, and visual breakout signals from semi-circular shapes.

🔶 USAGE

D-shape is a new concept where the distance between two Swing points is used to create a semi-circle/arc, where the width is expressed as a user-defined percentage of the radius. The resulting arc can be used as a potential support/resistance as well as a source of breakouts.

Users can adjust this percentage (width of the D-shape) in the settings ( "D-Width" ), which will influence breakouts and the Stop-Loss line.

🔹 Breakouts of D-Shape

The arc of this D-shape is used for detecting breakout signals between the price and the curve. Only one breakout per D-shape can occur.

A breakout is highlighted with a colored dot, signifying its location, with a green dot being used when the top part of the arc is exceeded, and red when the bottom part of the arc is surpassed.

When the price reaches the right side of the arc without breaking the arc top/bottom, a blue-colored dot is highlighted, signaling a "Neutral Breakout".

🔹 Trailing Stop-Loss Line

The script includes a Trailing Stop-Loss line (TSL), which is only updated when a breakout of the D-Shape occurs. The TSL will return the midline of the D-Shape subject to a breakout.

The TSL can be used as a stop-loss or entry-level but can also act as a potential support/resistance level or trend visualization.

🔶 DETAILS

A D-shape will initially be colored green when a Swing Low is followed by a Swing High, and red when a Swing Low is followed by a Swing High.

A breakout of the upper side of the D-shape will always update the color to green or to red when the breakout occurs in the lower part. A Neutral Breakout will result in a blue-colored D-shape. The transparency is lowered in the event of a breakout.

In the event of a D-shape breakout, the shape will be removed when the total number of visible D-Shapes exceeds the user set "Minimum Patterns" setting. Any D-shape whose boundaries have not been exceeded (and therefore still active) will remain visible.

🔹 Trailing Stop-Loss Line

Only when a breakout occurs will the midline of the D-shape closest to the closing price potentially become the new Trailing Stop value.

The script will only consider middle lines below the closing price on an upward breakout or middle lines above the closing price when it concerns a downward breakout.

In an uptrend, with an already available green TSL, the potential new Stop-Loss value must be higher than the previous TSL value; while in a downtrend, the new TSL value must be lower.

The Stop-Loss line won't be updated when a "Neutral Breakout" occurs.

🔶 SETTINGS

Swing Length: Period used for the swing detection, with higher values returning longer-term Swing Levels.

🔹 D-Patterns

Minimum Patterns: Minimum amount of visible D-Shape patterns.

D-Width: Width of the D-Shape as a percentage of the distance between both Swing Points.

Included Swings: Include "Swing High" (followed by a Swing Low), "Swing Low" (followed by a Swing High), or "Both"

Style Historical Patterns: Show the "Arc", "Midline" or "Both" of historical patterns.

🔹 Style

Label Size/Colors

Connecting Swing Level: Shows a line connecting the first Swing Point.

Color Fill: colorfill of Trailing Stop-Loss

Curved Price Channels (Zeiierman)█ Overview

The Curved Price Channels (Zeiierman) is designed to plot dynamic channels around price movements, much like the traditional Donchian Channels, but with a key difference: the channels are curved instead of straight. This curvature allows the channels to adapt more fluidly to price action, providing a smoother representation of the highest high and lowest low levels.

Just like Donchian Channels, the Curved Price Channels help identify potential breakout points and areas of trend reversal. However, the curvature offers a more refined approach to visualizing price boundaries, making it potentially more effective in capturing price trends and reversals in markets that exhibit significant volatility or price swings.

The included trend strength calculation further enhances the indicator by offering insight into the strength of the current trend.

█ How It Works

The Curved Price Channels are calculated based on the asset's average true range (ATR), scaled by the chosen length and multiplier settings. This adaptive size allows the channels to expand and contract based on recent market volatility. The central trendline is calculated as the average of the upper and lower curved bands, providing a smoothed representation of the overall price trend.

Key Calculations:

Adaptive Size: The ATR is used to dynamically adjust the width of the channels, making them responsive to changes in market volatility.

Upper and Lower Bands: The upper band is calculated by taking the maximum close value and adjusting it downward by a factor proportional to the ATR and the multiplier. Similarly, the lower band is calculated by adjusting the minimum close value upward.

Trendline: The trendline is the average of the upper and lower bands, representing the central tendency of the price action.

Trend Strength

The Trend Strength feature in the Curved Price Channels is a powerful feature designed to help traders gauge the strength of the current trend. It calculates the strength of a trend by analyzing the relationship between the price's position within the curved channels and the overall range of the channels themselves.

Range Calculation:

The indicator first determines the distance between the upper and lower curved channels, known as the range. This range represents the overall volatility of the price within the given period.

Range = Upper Band - Lower Band

Relative Position:

The next step involves calculating the relative position of the closing price within this range. This value indicates where the current price sits in relation to the overall range.

RelativePosition = (Close - Trendline) / Range

Normalization:

To assess the trend strength over time, the current range is normalized against the maximum and minimum ranges observed over a specified look-back period.

NormalizedRange = (Range - Min Range) / (Max Range - Min Range)

Trend Strength Calculation:

The final Trend Strength is calculated by multiplying the relative position by the normalized range and then scaling it to a percentage.

TrendStrength = Relative Position * Normalized Range * 100

This approach ensures that the Trend Strength not only reflects the direction of the trend but also its intensity, providing a more comprehensive view of market conditions.

█ Comparison with Donchian Channels

Curved Price Channels offer several advantages over Donchian Channels, particularly in their ability to adapt to changing market conditions.

⚪ Adaptability vs. Fixed Structure

Donchian Channels: Use a fixed period to plot straight lines based on the highest high and lowest low. This can be limiting because the channels do not adjust to volatility; they remain the same width regardless of how much or how little the price is moving.

Curved Price Channels: Adapt dynamically to market conditions using the Average True Range (ATR) as a measure of volatility. The channels expand and contract based on recent price movements, providing a more accurate reflection of the market's current state. This adaptability allows traders to capture both large trends and smaller fluctuations more effectively.

⚪ Sensitivity to Market Movements

Donchian Channels: Are less sensitive to recent price action because they rely on a fixed look-back period. This can result in late signals during fast-moving markets, as the channels may not adjust quickly enough to capture new trends.

Curved Price Channels: Respond more quickly to changes in market volatility, making them more sensitive to recent price action. The multiplier setting further allows traders to adjust the channel's sensitivity, making it possible to capture smaller price movements during periods of low volatility or filter out noise during high volatility.

⚪ Enhanced Trend Strength Analysis

Donchian Channels: Do not provide direct insight into the strength of a trend. Traders must rely on additional indicators or their judgment to gauge whether a trend is strong or weak.

Curved Price Channels: Includes a built-in trend strength calculation that takes into account the distance between the upper and lower channels relative to the trendline. A broader range between the channels typically indicates a stronger trend, while a narrower range suggests a weaker trend. This feature helps traders not only identify the direction of the trend but also assess its potential longevity and strength.

⚪ Dynamic Support and Resistance

Donchian Channels: Offer static support and resistance levels that may not accurately reflect changing market dynamics. These levels can quickly become outdated in volatile markets.

Curved Price Channels: Offer dynamic support and resistance levels that adjust in real-time, providing more relevant and actionable trading signals. As the channels curve to reflect price movements, they can help identify areas where the price is likely to encounter support or resistance, making them more useful in volatile or trending markets.

█ How to Use

Traders can use the Curved Price Channels in similar ways to Donchian Channels but with the added benefits of the adaptive, curved structure:

Breakout Identification:

Just like Donchian Channels, when the price breaks above the upper curved band, it may signal the start of a bullish trend, while a break below the lower curved band could indicate a bearish trend. The curved nature of the channels helps in capturing these breakouts more precisely by adjusting to recent volatility.

Volatility:

The width of the price channels in the Curved Price Channels indicator serves as a clear indicator of current market volatility. A wider channel indicates that the market is experiencing higher volatility, as prices are fluctuating more dramatically within the period. Conversely, a narrower channel suggests that the market is in a lower volatility state, with price movements being more subdued.

Typically, higher volatility is observed during negative trends, where market uncertainty or fear drives larger price swings. In contrast, lower volatility is often associated with positive trends, where prices tend to move more steadily and predictably. The adaptive nature of the Curved Price Channels reflects these volatility conditions in real time, allowing traders to assess the market environment quickly and adjust their strategies accordingly.

Support and Resistance:

The trend line act as dynamic support and resistance levels. Due to it's adaptive nature, this level is more reflective of the current market environment than the fixed level of Donchian Channels.

Trend Direction and Strength:

The trend direction and strength are highlighted by the trendline and the directional candle within the Curved Price Channels indicator. If the price is above the trendline, it indicates a positive trend, while a price below the trendline signals a negative trend. This directional bias is visually represented by the color of the directional candle, making it easy for traders to quickly identify the current market trend.

In addition to the trendline, the indicator also displays Max and Min values. These represent the highest and lowest trend strength values within the lookback period, providing a reference point for understanding the current trend strength relative to historical levels.

Max Value: Indicates the highest recorded trend strength during the lookback period. If the Max value is greater than the Min value, it suggests that the market has generally experienced more positive (bullish) conditions during this time frame.

Min Value: Represents the lowest recorded trend strength within the same period. If the Min value is greater than the Max value, it indicates that the market has been predominantly negative (bearish) over the lookback period.

By assessing these Max and Min values, traders gain an immediate understanding of the underlying trend. If the current trend strength is close to the Max value, it indicates a strong bullish trend. Conversely, if the trend strength is near the Min value, it suggests a strong bearish trend.

█ Settings

Trend Length: Defines the number of bars used to calculate the core trendline and adaptive size. A length of 200 will create a smooth, long-term trendline that reacts slowly to price changes, while a length of 20 will create a more responsive trendline that tracks short-term movements.

Multiplier: Adjusts the width of the curved price channels. A higher value tightens the channels, making them more sensitive to price movements, while a lower value widens the channels. A multiplier of 10 will create tighter channels that are more sensitive to minor price fluctuations, which is useful in low-volatility markets. A multiplier of 2 will create wider channels that capture larger trends and are better suited for high-volatility markets.

Trend Strength Length: Defines the period over which the maximum and minimum ranges are calculated to normalize the trend strength. A length of 200 will smooth out the trend strength readings, providing a stable indication of trend health, whereas a length of 50 will make the readings more reactive to recent price changes.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Magic Linear Regression Channel [MW]Introduction

The Magic Linear Regression Channel indicator provides users with a way to quickly include a linear regression channel ANYWHERE on their chart, in order to find channel breakouts and bounces within any time period. It uses a novel method that allows users to adjust the start and end period of the regression channel in order to quickly make adjustments faster, with fewer steps, and with more precision than with any other linear regression channel tool. It includes Fibonacci bands AND a horizontal mode in order for users to quickly define significant price levels based on the high, low, open, and close prices defined by the start period.

Settings

Start Time: This is initially MANUALLY SELECTED ON THE CHART when the indicator is first loaded.

End time: This is also initially MANUALLY SELECTED ON THE CHART when the indicator is first loaded.

Horizontal Line: This forces the baseline to be horizontal. The band distance is defined by the maximum price distance from the band.

Horizontal Line Type: This snaps the horizontal line to the close, high, low, or open price. Or, it can also use a regression calculation for the selected time period to define the y-position of the line.

Extend Line N Bars: How many bars to the left in which to extend the baseline and bands.

Show Baseline ONLY!!: Removes all lines except the baseline and it’s extension.

Add Half Band: Includes a band that is half the distance between the baseline and the top and bottom bands

Add Outer Fibonacci Band: Includes a band that is 1.618 (phi) times the default band distance

Add Inner Fibonacci Band - Upper: Includes a band that is 0.618 (1/phi) times the default band distance

Add Inner Fibonacci Band - Lower: Includes a band that is 0.382 (1 - 1/phi) times the default band distance

Calculations

This indicator uses the least squares approach for generating a straight regression line, which can be reviewed at Wikipedia’s “Simple Linear Regression” page. It sums all of the x-values, and y-values, as well as the sum of the product of corresponding x and y values, and the sum of the squares of the x-values. These values are used to calculate the slope and intercept using the following equations:

slope = (n * sum_xy - sum_x * sum_y) / (n * sum_xx - sum_x * sum_x)

And

intercept = (sum_y - slope * sum_x) / n

The slope and intercept are then used to generate the baseline and the corresponding bands using the user-selected offsets.

How to Use

When the Magic Linear Regression Channel indicator is first added to the chart, there will be a blue prompt behind the “Indicators, Metrics & Strategies” window. Close the window, then select a START POINT by clicking at a desired location on the chart. Next, you will be prompted to select an END POINT. The end point MUST be placed after the START POINT. At this time a channel will be generated. Once you’ve selected the START POINT and END POINT, you can adjust them by dragging them anywhere on the chart. Each adjustment will generate a new channel making it easier for you to quickly visualize and recognize any channel exits and bounces.

The Magic Linear Regression Channel indicator works great at identifying wave patterns. Place the start line at a top or bottom pivot point. Place the end line at the next respective top or bottom pivot. This will give you a complete wave form to work with. When price reaches a band and rejects, it can be a strong indication that price may move back to one of the bands in the channel. If price exits the channel with volume that supports the exit, it may be an indication of a breakout.

You can also use the horizontal mode to identify key levels, then add Fibonacci bands based on regression calculations for the given time period to provide more meaningful areas of support and resistance.

Other Usage Notes and Limitations

Occasionally, off-by-1 errors appear which makes the extended lines protrude at a slightly incorrect angle. This is a known bug and will be addressed in the next release.

It's important for traders to be aware of the limitations of any indicator and to use them as part of a broader, well-rounded trading strategy that includes risk management, fundamental analysis, and other tools that can help with reducing false signals, determining trend direction, and providing additional confirmation for a trade decision. Diversifying strategies and not relying solely on one type of indicator or analysis can help mitigate some of these risks.

Double Donchian Channels [CrossTrade]Dual Channel System

The indicator incorporates two Donchian Channels - the Inner Channel and the Outer Channel. These channels are adjustable, allowing users to define their lengths according to their trading strategy.

Inner Channel: With a default length of 100 periods, the Inner Channel provides a closer view of market trends and potential support and resistance areas. It includes an upper, lower, and middle line (average of the upper and lower), offering detailed insights into shorter-term price movements.

Outer Channel: Set with a default length of 300 periods, the Outer Channel offers a broader perspective, ideal for identifying long-term trends and stronger levels of support and resistance.

Dynamic Color Coding: The middle lines of both channels change color based on the relationship between the previous close and the channel's basis. This feature provides an immediate visual cue regarding market sentiment.

Touching Bars Highlighting: The indicator highlights bars that touch the upper or lower bands of either channel. This is particularly useful for identifying potential reversals or continuation patterns.

Pullback Identification: By differentiating between bars that touch the Inner Channel only and those that touch the Outer Channel, the indicator helps in identifying pullbacks within a broader trend.

Customizable Alert System: Users can set up alerts for specific conditions - a bar touching the bottom band of the Inner Channel (green), the bottom band of the Outer Channel (blue), the upper band of the Inner Channel (red), and the upper band of the Outer Channel (orange). These alerts assist in timely decision-making and can be tailored to individual trading styles.

The indicator is a versatile tool designed to adapt to various trading styles and timeframes. Its features make it suitable for trend analysis, identifying potential reversal points, and understanding market volatility.

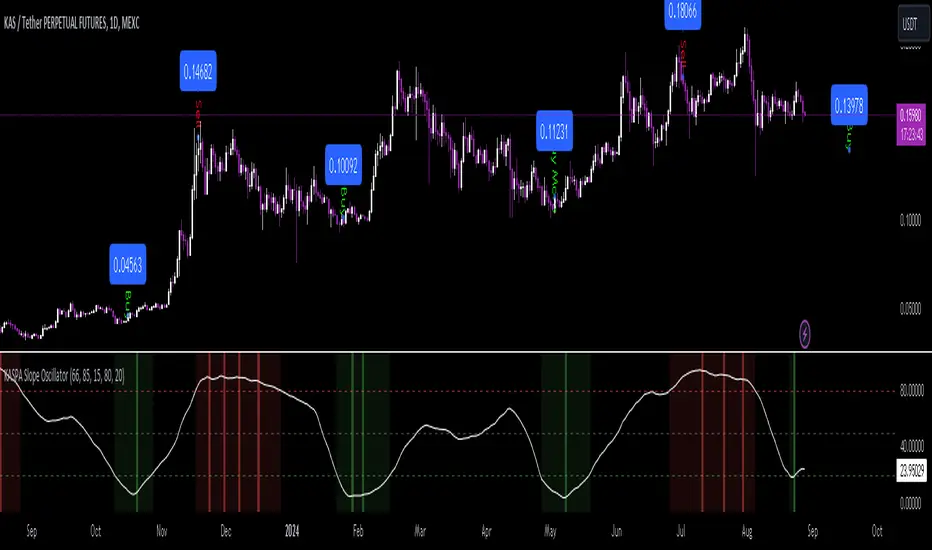

KASPA Slope OscillatorKASPA Slope Oscillator for analyzing KASPA on the 1D (daily) chart.

The indicator is plotted in a separate pane below the price chart and uses a mathematical approach to calculate and visualize the momentum or "slope" of KASPA's price movements.

Input Parameters:

Slope Window (days):

Defines the period (66 days by default) over which the slope is calculated.

Normalization Window (days):

The window size (85 days) for normalizing the slope values between 0 and 100.

Smoothing Period:

The number of days (15 days) over which the slope values are smoothed to reduce noise.

Overbought and Oversold Levels:

Threshold levels set at 80 (overbought) and 20 (oversold), respectively.

Calculation of the Slope:

Logarithmic Price Calculation:

Converts the close price of KASPA into a logarithmic scale to account for exponential growth or decay.

Rolling Slope:

Computes the rate of change in logarithmic prices over the defined slope window.

Normalization:

The slope is normalized between 0 and 100, allowing easier identification of extreme values.

Smoothing and Visualization:

Smoothing the Slope:

A Simple Moving Average (SMA) is applied to the normalized slope for the specified smoothing period.

Plotting the Oscillator:

The smoothed slope is plotted on the oscillator chart. Horizontal lines indicate overbought (80), oversold (20), and the mid-level (50).

Background Color Indications:

Background colors (red or green) indicate when the slope crosses above the overbought or below the oversold levels, respectively, signaling potential buy or sell conditions.

Detection of Local Maxima and Minima:

The code identifies local peaks (maxima) above the overbought level and troughs (minima) below the oversold level.

Vertical background lines are highlighted in red or green at these points, signaling potential reversals.

Short Summary:

The oscillator line fluctuates between 0 and 100, representing the normalized momentum of the price.

Red background areas indicate periods when the oscillator is above the overbought level (80), suggesting a potential overbought condition or a sell signal.

Green background areas indicate periods when the oscillator is below the oversold level (20), suggesting a potential oversold condition or a buy signal.

The vertical lines on the background mark local maxima and minima where price reversals may occur.

(I also want to thank @ForgoWork for optimizing visuality and cleaning up the source code)

Cash Cycle BandCash cycle band shows the number of days and the profit margin compared to the previous period (it does not indicate how profitable the company is, but how well it is managed).

Cash cycle band consists of 6 sections:

1. DPO is the days payables outstanding in the "red" followed by O/D which is overdraft or short-term debt (if any) .

2. DIO is the days inventory outstanding in the "green" followed by classified inventory (if any) consists of finished goods. work in process and raw materials.

3. DSO is days sales outstanding in "blue".

4. DWC is days converting working capital to revenue in "orange".

5. CCC is days converting inventory and resources to cash flow in "yellow".

6. GPM is gross profit margin and OPM is operating profit margin.

The "😱" emoji indicates a value if it increases by more than or decreases by less than 20%, e.g.

- DPO, finished goods, work in process, raw materials, GPM, OPM is decreasing.

- O/D, DIO, DSO, DWC, CCC is increasing.

The "🔥" emoji indicates a value if it increases by more than or decreases, e.g.

- DPO, finished goods, work in process, raw materials, GPM, OPM is increasing.

- O/D, DIO, DSO, DWC, CCC is decreasing.

The order of the list depends on the day of each item, the more days more high.

Ranges and Breakouts [AlgoAlpha]💥 Ranges and Breakouts by AlgoAlpha is a dynamic indicator designed for traders seeking to identify market ranges and capitalize on breakout opportunities. This tool automatically detects ranges based on price action over a specified period, visualizing these ranges with shaded boxes and midlines, making it easy to spot potential breakout scenarios. The indicator includes advanced features such as customizable pivot detection, internal range allowance, and automatic trend color changes for quick market analysis.

Key Features

💹 Dynamic Range Detection : Automatically identifies market ranges using customizable look-back and confirmation periods.

🎯 Breakout Alerts : Get alerted to bullish and bearish breakouts for potential trading opportunities.

📊 Visual Aids : Displays pivot highs/lows within ranges and plots midlines with adjustable styles for easier market trend interpretation.

🔔 Alerts : Signals potential take-profit points based on volatility and moving average crossovers.

🎨 Customizable Appearance : Choose between solid, dashed, or dotted lines for midlines and adjust the colors for bullish and bearish zones.

How to Use

⭐ Add the Indicator : Add the indicator to favorites by pressing the star icon. Adjust the settings like the look-back period, confirmation length, and pivot detection to match your trading strategy.

👀 Monitor the Chart : Watch for new ranges to form, highlighted by shaded boxes on the chart. Midlines and range bounds will appear to help you gauge potential breakout points.

⚡ React to Breakouts : Pay attention to color changes and alert signals for bullish or bearish breakouts. Use these signals to enter or exit trades.

🔔 Set Alerts : Customize alert conditions for new range formations, breakout signals, and take-profit levels to stay on top of market movements without constant monitoring.

How It Works

The indicator detects price ranges by analyzing the highest and lowest prices over a specified period. It confirms a range if these levels remain unchanged for a set number of bars, at which point it visually marks the range with shaded boxes. Pivots are identified within these ranges, and a midline is plotted to help interpret potential breakouts. When price breaks out of these defined ranges, the indicator changes the chart's background color to signal a bullish or bearish trend. Alerts can be set for range formation, breakouts, and take-profit opportunities, helping traders stay proactive in volatile markets.

Abnormal value check1. indicator settings

BB Length: Sets the period used for the Bollinger Band calculation. The default is 20 periods.

BB Multiplier: Sets the multiplier to be used in the Bollinger Band calculation. The default is 2.5 multiplier.

Equilibrium volume reset: Selects whether or not the volume should be reset if it is out of equilibrium. The default setting is reset. 2.

2. bollinger band calculation

This indicator calculates Bollinger Bands (upper and lower bands and a reference line) from price and volume data.

Bollinger Bands are indicators used to measure price and volume volatility and are identified as anomalies when prices break through the bands.

3. display of abnormal prices

Abnormal Buying Price (ABP): The background color changes when the price significantly exceeds the upper limit of the Bollinger Band. The color is green.

Abnormal Selling Price (ASP): The background color changes when the price is significantly below the lower limit of the Bollinger Band. The color is red.

Abnormal High Volume (AHV): The background color changes when the volume is significantly above the upper Bollinger Band. The color is white.

Abnormal Low Volume (ALV): The background color changes when the volume is significantly below the lower limit of the Bollinger Band. The color is yellow. 4.

4. display of signals

Abnormal Price Signal: A triangle signal is displayed when the price rises or falls compared to the previous data. The color is orange for an increase and purple for a decrease.

Volume Abnormal Signal: A triangle signal is displayed when volume is up or down compared to the previous data. Rises are colored orange and falls are colored purple. 5.

5. price and volume history display

RSAB_P: Displays price anomaly history. Rising prices are displayed in green, and falling prices in red.

RSAB_V: Displays the volume anomaly history. Green indicates an increase and red indicates a decrease. 6.

6. display of equilibrium

PPE: Displays a line indicating the state of volume balance. A positive volume balance is displayed in orange, and a negative volume balance is displayed in purple.

Summary of usage

Add indicator to chart: Add this Pine Script™ code as an indicator in TradingView.

Set parameters: Based on the settings above, adjust the values to suit your trading strategy and analysis.

See signals and color changes on the chart: Visually identify price and volume anomalies to help you make trading decisions.

This indicator uses Bollinger Bands to identify abnormal price and volume movements to help you improve your trading timing and strategies.

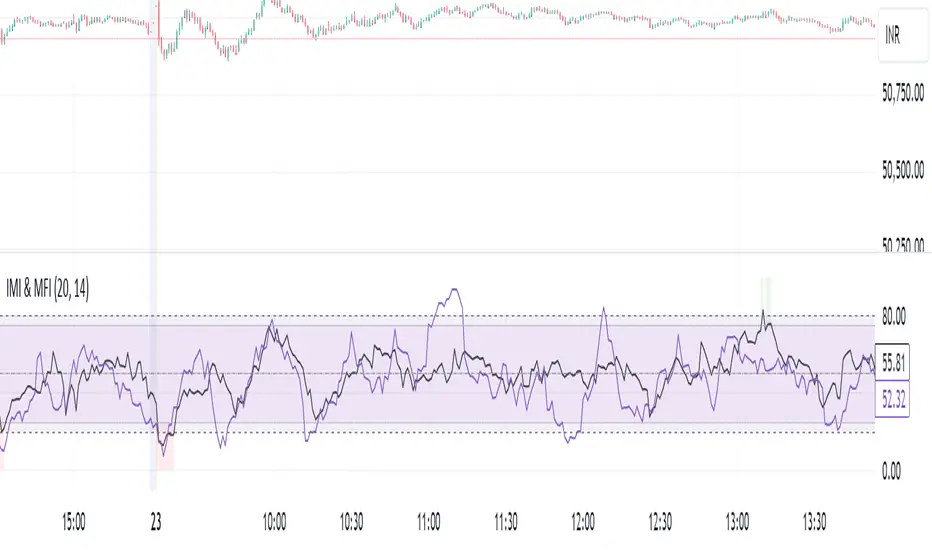

IMI and MFI CombinedFor a strategy using the combined IMI (Intraday Momentum Index), MFI (Money Flow Index), and Bollinger Bands on a 1-minute chart of Bank NIFTY (Bank Nifty Index), here's how you can interpret the indicators and define a sell signal strategy:

Strategy Explanation:

IMI (Intraday Momentum Index):

IMI measures the ratio of upward price changes to downward price changes over a specified period, indicating momentum.

In the script, IMI is plotted with a range from 0 to 100. Levels above 75 are considered overbought, and levels below 25 are oversold.

Strategy Condition: A sell signal can be considered when IMI is above 75, indicating a potentially overbought market condition.

MFI (Money Flow Index):

MFI measures the strength of money flowing in and out of a security, using price and volume.

In the script, MFI is plotted with levels at 80 (overbought) and 20 (oversold).

Strategy Condition: A sell signal can be considered when MFI is above 80, suggesting an overbought condition in the market.

Bollinger Bands:

Bollinger Bands consist of a middle band (SMA) and upper/lower bands representing volatility levels around the price.

In the script, Bollinger Bands are plotted with a length of 20 and a standard deviation multiplier of 2.

Strategy Condition: While not explicitly used for generating sell signals in this script, Bollinger Bands can help confirm price volatility and potential reversals when combined with other indicators.

Sell Signal Criteria:

IMI Sell Signal: Look for instances where IMI rises above 75. This indicates that the recent upward price momentum may be reaching an unsustainable level, potentially signaling a reversal or a pullback in prices.

MFI Sell Signal: Look for MFI rising above 80. This suggests that the market has experienced strong buying pressure, possibly leading to an overbought condition where a price correction or reversal might occur.

Implementation Considerations:

Confirmation: Consider waiting for both IMI and MFI to confirm the overbought condition simultaneously before entering a sell trade. This can increase the reliability of the signal.

Risk Management: Use stop-loss orders to manage risk in case the market moves against the anticipated direction after the sell signal is triggered.

Timeframe: This strategy is tailored for a 1-minute chart, meaning signals should be interpreted and acted upon quickly due to the rapid nature of price movements in intraday trading.

By combining these indicators and interpreting their signals, you can develop a systematic approach to identifying potential sell opportunities in the Bank NIFTY index on a 1-minute timeframe. Adjustments to indicator parameters and additional technical analysis may further refine the strategy based on your trading preferences and risk tolerance.

Inside Candle - Multi TimeframesIndicator looks for inside candle on 3 timeframes. Chart's default timeframe and 2 higher timeframes to spot Inside candle on any of these timeframes.

Main purpose was to look at multiple inside candle at multiple timeframes to identify consolidation within consolidation and implement intraday, hence for 15min chart timeframe.

However, code works for all timeframes from 5 min to quarterly and higher timeframes will be picked automatically.

Reference and credits

This indicator is inspired by and uses code from:

- Author Name - // © Fab_Coin_

-

Advanced Keltner Channel/Oscillator [MyTradingCoder]This indicator combines a traditional Keltner Channel overlay with an oscillator, providing a comprehensive view of price action, trend, and momentum. The core of this indicator is its advanced ATR calculation, which uses statistical methods to provide a more robust measure of volatility.

Starting with the overlay component, the center line is created using a biquad low-pass filter applied to the chosen price source. This provides a smoother representation of price than a simple moving average. The upper and lower channel lines are then calculated using the statistically derived ATR, with an additional set of mid-lines between the center and outer lines. This creates a more nuanced view of price action within the channel.

The color coding of the center line provides an immediate visual cue of the current price momentum. As the price moves up relative to the ATR, the line shifts towards the bullish color, and vice versa for downward moves. This color gradient allows for quick assessment of the current market sentiment.

The oscillator component transforms the channel into a different perspective. It takes the price's position within the channel and maps it to either a normalized -100 to +100 scale or displays it in price units, depending on your settings. This oscillator essentially shows where the current price is in relation to the channel boundaries.

The oscillator includes two key lines: the main oscillator line and a signal line. The main line represents the current position within the channel, smoothed by an exponential moving average (EMA). The signal line is a further smoothed version of the oscillator line. The interaction between these two lines can provide trading signals, similar to how MACD is often used.

When the oscillator line crosses above the signal line, it might indicate bullish momentum, especially if this occurs in the lower half of the oscillator range. Conversely, the oscillator line crossing below the signal line could signal bearish momentum, particularly if it happens in the upper half of the range.

The oscillator's position relative to its own range is also informative. Values near the top of the range (close to 100 if normalized) suggest that price is near the upper Keltner Channel band, indicating potential overbought conditions. Values near the bottom of the range (close to -100 if normalized) suggest proximity to the lower band, potentially indicating oversold conditions.

One of the strengths of this indicator is how the overlay and oscillator work together. For example, if the price is touching the upper band on the overlay, you'd see the oscillator at or near its maximum value. This confluence of signals can provide stronger evidence of overbought conditions. Similarly, the oscillator hitting extremes can draw your attention to price action at the channel boundaries on the overlay.

The mid-lines on both the overlay and oscillator provide additional nuance. On the overlay, price action between the mid-line and outer line might suggest strong but not extreme momentum. On the oscillator, this would correspond to readings in the outer quartiles of the range.

The customizable visual settings allow you to adjust the indicator to your preferences. The glow effects and color coding can make it easier to quickly interpret the current market conditions at a glance.

Overlay Component:

The overlay displays Keltner Channel bands dynamically adapting to market conditions, providing clear visual cues for potential trend reversals, breakouts, and overbought/oversold zones.

The center line is a biquad low-pass filter applied to the chosen price source.

Upper and lower channel lines are calculated using a statistically derived ATR.

Includes mid-lines between the center and outer channel lines.

Color-coded based on price movement relative to the ATR.

Oscillator Component:

The oscillator component complements the overlay, highlighting momentum and potential turning points.

Normalized values make it easy to compare across different assets and timeframes.

Signal line crossovers generate potential buy/sell signals.

Advanced ATR Calculation:

Uses a unique method to compute ATR, incorporating concepts like root mean square (RMS) and z-score clamping.

Provides both an average and mode-based ATR value.

Customizable Visual Settings:

Adjustable colors for bullish and bearish moves, oscillator lines, and channel components.

Options for line width, transparency, and glow effects.

Ability to display overlay, oscillator, or both simultaneously.

Flexible Parameters:

Customizable inputs for channel width multiplier, ATR period, smoothing factors, and oscillator settings.

Adjustable Q factor for the biquad filter.

Key Advantages:

Advanced ATR Calculation: Utilizes a statistical method to generate ATR, ensuring greater responsiveness and accuracy in volatile markets.

Overlay and Oscillator: Provides a comprehensive view of price action, combining trend and momentum analysis.

Customizable: Adjust settings to fine-tune the indicator to your specific needs and trading style.

Visually Appealing: Clear and concise design for easy interpretation.

The ATR (Average True Range) in this indicator is derived using a sophisticated statistical method that differs from the traditional ATR calculation. It begins by calculating the True Range (TR) as the difference between the high and low of each bar. Instead of a simple moving average, it computes the Root Mean Square (RMS) of the TR over the specified period, giving more weight to larger price movements. The indicator then calculates a Z-score by dividing the TR by the RMS, which standardizes the TR relative to recent volatility. This Z-score is clamped to a maximum value (10 in this case) to prevent extreme outliers from skewing the results, and then rounded to a specified number of decimal places (2 in this script).

These rounded Z-scores are collected in an array, keeping track of how many times each value occurs. From this array, two key values are derived: the mode, which is the most frequently occurring Z-score, and the average, which is the weighted average of all Z-scores. These values are then scaled back to price units by multiplying by the RMS.

Now, let's examine how these values are used in the indicator. For the Keltner Channel lines, the mid lines (top and bottom) use the mode of the ATR, representing the most common volatility state. The max lines (top and bottom) use the average of the ATR, incorporating all volatility states, including less common but larger moves. By using the mode for the mid lines and the average for the max lines, the indicator provides a nuanced view of volatility. The mid lines represent the "typical" market state, while the max lines account for less frequent but significant price movements.

For the color coding of the center line, the mode of the ATR is used to normalize the price movement. The script calculates the difference between the current price and the price 'degree' bars ago (default is 2), and then divides this difference by the mode of the ATR. The resulting value is passed through an arctangent function and scaled to a 0-1 range. This scaled value is used to create a color gradient between the bearish and bullish colors.

Using the mode of the ATR for this color coding ensures that the color changes are based on the most typical volatility state of the market. This means that the color will change more quickly in low volatility environments and more slowly in high volatility environments, providing a consistent visual representation of price momentum relative to current market conditions.

Using a good IIR (Infinite Impulse Response) low-pass filter, such as the biquad filter implemented in this indicator, offers significant advantages over simpler moving averages like the EMA (Exponential Moving Average) or other basic moving averages.

At its core, an EMA is indeed a simple, single-pole IIR filter, but it has limitations in terms of its frequency response and phase delay characteristics. The biquad filter, on the other hand, is a two-pole, two-zero filter that provides superior control over the frequency response curve. This allows for a much sharper cutoff between the passband and stopband, meaning it can more effectively separate the signal (in this case, the underlying price trend) from the noise (short-term price fluctuations).

The improved frequency response of a well-designed biquad filter means it can achieve a better balance between smoothness and responsiveness. While an EMA might need a longer period to sufficiently smooth out price noise, potentially leading to more lag, a biquad filter can achieve similar or better smoothing with less lag. This is crucial in financial markets where timely information is vital for making trading decisions.

Moreover, the biquad filter allows for independent control of the cutoff frequency and the Q factor. The Q factor, in particular, is a powerful parameter that affects the filter's resonance at the cutoff frequency. By adjusting the Q factor, users can fine-tune the filter's behavior to suit different market conditions or trading styles. This level of control is simply not available with basic moving averages.

Another advantage of the biquad filter is its superior phase response. In the context of financial data, this translates to more consistent lag across different frequency components of the price action. This can lead to more reliable signals, especially when it comes to identifying trend changes or price reversals.

The computational efficiency of biquad filters is also worth noting. Despite their more complex mathematical foundation, biquad filters can be implemented very efficiently, often requiring only a few operations per sample. This makes them suitable for real-time applications and high-frequency trading scenarios.

Furthermore, the use of a more sophisticated filter like the biquad can help in reducing false signals. The improved noise rejection capabilities mean that minor price fluctuations are less likely to cause unnecessary crossovers or indicator movements, potentially leading to fewer false breakouts or reversal signals.

In the specific context of a Keltner Channel, using a biquad filter for the center line can provide a more stable and reliable basis for the entire indicator. It can help in better defining the overall trend, which is crucial since the Keltner Channel is often used for trend-following strategies. The smoother, yet more responsive center line can lead to more accurate channel boundaries, potentially improving the reliability of overbought/oversold signals and breakout indications.

In conclusion, this advanced Keltner Channel indicator represents a significant evolution in technical analysis tools, combining the power of traditional Keltner Channels with modern statistical methods and signal processing techniques. By integrating a sophisticated ATR calculation, a biquad low-pass filter, and a complementary oscillator component, this indicator offers traders a comprehensive and nuanced view of market dynamics.

The indicator's strength lies in its ability to adapt to varying market conditions, providing clear visual cues for trend identification, momentum assessment, and potential reversal points. The use of statistically derived ATR values for channel construction and the implementation of a biquad filter for the center line result in a more responsive and accurate representation of price action compared to traditional methods.

Furthermore, the dual nature of this indicator – functioning as both an overlay and an oscillator – allows traders to simultaneously analyze price trends and momentum from different perspectives. This multifaceted approach can lead to more informed decision-making and potentially more reliable trading signals.

The high degree of customization available in the indicator's settings enables traders to fine-tune its performance to suit their specific trading styles and market preferences. From adjustable visual elements to flexible parameter inputs, users can optimize the indicator for various trading scenarios and time frames.

Ultimately, while no indicator can predict market movements with certainty, this advanced Keltner Channel provides traders with a powerful tool for market analysis. By offering a more sophisticated approach to measuring volatility, trend, and momentum, it equips traders with valuable insights to navigate the complex world of financial markets. As with any trading tool, it should be used in conjunction with other forms of analysis and within a well-defined risk management framework to maximize its potential benefits.

Future SD ProjectionFuture Standard Deviation Projector

This innovative indicator projects price volatility into the future, helping traders anticipate potential price ranges and breakouts. It calculates standard deviation bands based on recent price action and extends them forward, providing a unique perspective on future price movement possibilities.

Key Features:

- Projects standard deviation bands into the future

- Customizable lookback period for volatility calculation

- Adjustable future projection timeframe

- Flexible standard deviation multiplier

- Clear visual signals for band breaches

How it works:

1. Calculates standard deviation from recent closing prices

2. Projects upper and lower bands into the future

3. Plots these bands on the chart

4. Signals with arrows when closing price crosses projected bands

Use this indicator to:

- Gauge potential future price ranges

- Identify possible breakout levels

- Assess market volatility expectations

- Enhance your trading strategy with forward-looking volatility projections

Customize the settings to align with your trading timeframe and risk tolerance. Remember, while this tool offers valuable insights, it should be used in conjunction with other analysis methods for comprehensive trading decisions.

Note: Past performance and projections do not guarantee future results. Always manage your risk appropriately.

RSI with Bollinger Bands Scalp Startegy (1min)

------------------------------------------------------------------------------

The "RSI with Bollinger Bands Scalp Strategy (1min)" is a highly effective tool designed for traders who engage in short-term scalping on the 1-minute chart. This indicator combines the strengths of the RSI (Relative Strength Index) and Bollinger Bands to generate precise buy signals, helping traders make quick and informed decisions in fast-moving markets.

How It Works:

RSI (Relative Strength Index):

The RSI is a widely-used momentum oscillator that measures the speed and change of price movements. It operates on a scale of 0 to 100 and helps identify overbought and oversold conditions in the market.

This strategy allows customization of the RSI's lower and upper bands (default settings: 30 for the lower band and 70 for the upper band) and the RSI length (default: 14).

Bollinger Bands:

Bollinger Bands consist of a central moving average (the basis) and two bands that represent standard deviations above and below the basis. These bands expand and contract based on market volatility.

In this strategy, the Bollinger Bands are used to identify potential buy and sell signals based on the price's relationship to the upper and lower bands.

Signal Generation:

Buy Signal: A buy signal is triggered when two conditions are met:

The RSI value falls below the specified lower band, indicating an oversold condition.

The price crosses below the lower Bollinger Band.

The buy signal is then issued on the first positive candle (where the closing price is greater than or equal to the opening price) after these conditions are met.

Sell Signal: In this version of the strategy, the sell signal is currently disabled to focus solely on generating and optimizing the buy signals for scalping.

Strategy Highlights:

This indicator is particularly effective for traders who focus on 1-minute charts and want to capitalize on rapid price movements.

The combination of RSI and Bollinger Bands ensures that buy signals are only generated during significant oversold conditions, helping to filter out false signals.

Customization:

Users can adjust the RSI length, Bollinger Bands length, and the standard deviation multiplier to better fit their specific trading style and the asset they are trading.

The moving average type for Bollinger Bands can be selected from various options, including SMA, EMA, SMMA, WMA, and VWMA, allowing further customization based on individual preferences.

Usage:

Use this indicator on a 1-minute chart to identify potential buy opportunities during short-term price dips.

Since the sell signals are disabled, this strategy is best used in conjunction with other indicators or strategies to manage exit points effectively.

This "RSI with Bollinger Bands Scalp Strategy (1min)" indicator is a valuable tool for traders looking to enhance their short-term trading performance by focusing on high-probability entry points in volatile market conditions.

ka66: Bar Range BandsThis tool takes a bar's range, and reflects it above the high and below the low of that bar, drawing upper and lower bands around the bar. Repeated for each bar. There's an option to then multiply that range by some multiple. Use a value greater than 1 to get wider bands, and less than one to get narrower bands.

This tool stems out of my frustration from the use of dynamic bands (like Keltner Channels, or Bollinger Bands), in particular for estimating take profit points.

Dynamic bands work great for entries and stop loss, but their dynamism is less useful for a future event like taking profit, in my experience. We can use a smaller multiple, but then we can often lose out on a bigger chunk of gains unnecessarily.

The inspiration for this came from a friend explaining an ICT/SMC concept around estimating the magnitude of a trend, by calculating the Asian Session Range, and reflecting it above or below on to the New York and London sessions. He described this as standard deviation of the Asian Range, where the range can thus be multiplied by some multiple for a wider or narrower deviation.

This, in turn, also reminded me of the Measured Move concept in Technical Analysis. We then consider that the market is fractal in nature, and this is why patterns persist in most timeframes. Traders exist across the spectrum of timeframes. Thus, a single bar on a timeframe, is made up of multiple bars on a lower timeframe . In other words, when we reflect a bar's range above or below itself, in the event that in a lower timeframe, that bar fit a pattern whose take profit target could be estimated via a Measured Move , then the band's value becomes a more valid estimate of a take profit point .

Yet another way to think about it, by way of the fractal nature above, is that it is essentially a simplified dynamic support and resistance mechanism , even simpler than say the various Pivot calculations (e.g. Classical, Camarilla, etc.).

This tool in general, can also be used by those who manually backtest setups (and certainly can be used in an automated setting too!). It is a research tool in that regard, applicable to various setups.

One of the pitfalls of manual backtesting is that it requires more discipline to really determine an exit point, because it's easy to say "oh, I'll know more or less where to exit when I go live, I just want to see that the entry tends to work". From experience, this is a bad idea, because our mind subconsciously knows that we haven't got a trained reflex on where to exit. The setup may be decent, but without an exit point, we will never have truly embraced and internalised trading it. Again, I speak from experience!

Thus, to use this to research take profit/exit points:

Have a setup in mind, with all the entry rules.

Plot your setup's indicators, mark your signals.

Use this indicator to get an idea of where to exit after taking an entry based on your signal.

Credits:

@ICT_ID for providing the idea of using ranges to estimate how far a trend move might go, in particular he used the Asian Range projected on to the London and New York market sessions.

All the technicians who came up with the idea of the Measured Move.

Tether Ratio ChannelTether Ratio Channel is an on-chain metric that tracks the ebb & flow of the ratio of BTC market cap / stablecoin market cap.

This ratio is relevant to traders, as it tends to lead total crypto market cap's short to medium term trend, and has for many years.

The ratio's most straightforwards visualization may be Stablecoin Supply Oscillator , a legacy on-chain metric that captures the ratio but isn't useful on its own as a trading tool.

Tether Ratio Channel builds on top of Stablecoin Supply Oscillator, to create a new metric that's:

Signal-generating , with clear entry & exit signals

Unambiguous , so use is mechanical

Optimized , with the intent to generate signals as close as possible to BTC local tops & bottoms

Normalized across its history , so each signal has a rich uniform history & context

METRIC CONSTRUCTION