S/R and Reversal BarsToday I'm proposing an idea to form S/R with a slightly different basic idea. This is a combination of CCI and candlestick study, and we will use this to mark possible reversal candles and possible S/R lines.

This is nothing complicated, I've used a basic CCI indicator with certain rules/system to mark S/R levels on the chart. (Have loaded traditional CCI indicator on bottom for comparison)

S/R levels are market as followed

Cross -

Lime = Support

Red = Resistance

Zero/Balance line - Yellow circles

The idea is to use this indicator to trade sideways market more successfully, in trending market this can be futile if you are not waiting for the break-out or breakdowns with confirmation.

Since this is based on CCI, it will give static result only when bar is closed, till then it will be susceptible for repaint. This is inherited nature from CCI readings on current bar. I could change this to only making reading on closed bar (historical bar), but that takes away from the uniqueness of this indicator in giving early indications.

This is a great tool for intraday scalping, but it does work on all timeframes, it's not bound by granularity.

This is for education purpose only.

Past success or seemingly positive results on published posts are not indication of future success.

Centered Oscillators

TASC 2023.11 VAcc█ OVERVIEW

The November 2023 edition of TASC's Traders' Tips features an article titled "VAcc: A Momentum Indicator Based On Velocity And Acceleration" by Scott Cong. This script implements the author's momentum indicator based on simple physics concepts.

█ CONCEPTS

The indicator is named VAcc as it is derived from the average velocity (V) and acceleration (Acc) over a specified lookback period. Consequently, its readings reflect two valuable characteristics of price data: rate (indicating the speed at which the price is moving) and rate of change (indicating whether the price is speeding up or slowing down).

In the article, the author reports that for longer periods, VAcc behaves similarly to the MACD , albeit with a more responsive nature. For shorter periods, VAcc exhibits characteristics reminiscent of the stochastic oscillator , but it trends more prominently and is less prone to overbought/oversold saturation.

To incorporate VAcc into trading strategies, the author suggests considering the following two permutations for the velocity and acceleration data series:

Strong upward condition: Velocity is rising, and acceleration is rising above zero.

Strong downward condition: Velocity is falling, and acceleration is falling.

In the current implementation, the chart displays the average velocity as a line, while the average acceleration is presented as a histogram.

█ CALCULATIONS

The calculation of VAcc involves the following steps:

For the current closing price, C , and for each bar C (i) within a specified lookback period from the current bar, the script calculates velocities, V (i) = ( C - C (i))/i. These velocities are then subjected to an exponential moving average to obtain the smoothed average velocity.

Similarly, for each bar within the lookback period, accelerations are calculated as Acc (i) = ( V - V (i))/i and then averaged without smoothing.

VAcc (Velocity & Acceleration)VAcc (Velocity & Acceleration) is a momentum indicator published by Scott Cong in Stocks & Commodities V. 41:09 (8–15). It applies concepts from physics, namely velocity and acceleration, to financial markets. VAcc functions similarly to the popular MACD (Moving Average Convergence Divergence) indicator when using a longer lookback period, but produces more responsive results. With shorter periods, VAcc exhibits characteristics reminiscent of the stochastic oscillator.

🟠 Algorithm

The average velocity over the past n periods is defined as

((C - C_n) / n + (C - C_{n-1}) / (n - 1) + … + (C - C_i) / i + (C - C_1) / 1) / n

At its core, the velocity is a weighted average of the rate of change over the past n periods.

The calculation of the acceleration follows a similar process, where it’s defined as

((V - V_n) / n + (V - V_{n - 1}) / (n - 1) + … + (V - V_i) / i + (V - V_1) / 1) / n

🟠 Comparison with MACD

A comparison of VAcc and MACD on the daily Nasdaq 100 (NDX) chart from August 2022 helps demonstrate VAcc's improved sensitivity. Both indicators utilized a lookback period of 26 days and smoothing of 9 periods.

The VAcc histogram clearly shows a divergence forming, with momentum weakening as prices reached new highs. In contrast, the corresponding MACD histogram significantly lagged in confirming the divergence, highlighting VAcc's ability to identify subtle shifts in trend momentum more immediately than the traditional MACD.

Ichimoku Oscillator With Divergences [ChartPrime]The Ichimoku Oscillator is a trading indicator designed to streamline the interpretation of Ichimoku clouds. It aims to refine and condense the complexities of the Chikou (the lag line), presenting its implications in real-time through an oscillator format, beneficial for those familiar with Ichimoku components but to have a new interpretation of their indicators.

The basics of an Ichimoku:

Conversion Line (Tenkan-Sen): It represents a midpoint of the highest and lowest prices over a specific period, usually 9 periods, reflecting short-term price movements.

Base Line (Kijun-Sen): It acts similarly to the Conversion Line but over a longer period, typically 26 periods, representing medium-term price movements.

Leading Span A & B (Kumo): Span A is the average of the Conversion Line and Base Line, and Span B is the midpoint of the highest and lowest prices over a usually longer period, typically 52 periods. Their interaction denotes trend direction, and the cloud color changes depending on whether Span A is above or below Span B, indicating bullish or bearish market conditions, respectively.

Lagging Span (Chikou Span): It is the current closing price plotted 26 periods behind, assisting in confirming the trend direction and potential momentum.

Advantage of an Oscillator:

Utilizing the oscillator format allows traders to interpret market dynamics more efficiently by visualizing the momentum and trend strength in a bounded range, enabling quick assessments of overbought or oversold conditions. Creating this oscillator provides multiple advantageous; particularly in sideway markets, helping to identify potential reversal points and offering insights on market entries and exits. When building this oscillator we've put a focus on unique interpretations such as overbought and sold areas and divergences; otherwise not found in traditional Ichimoku techniques. It is important to note these divergences are naturally not 100% real time.

When the oscillator turns green; the market is in an uptrend, red for downtrend and yellow for a transitioning market. The center line and the inner most cloud represent a balanced market state.

Key Features & Input Parameters:

Signal Source: Allows the selection of the price data source for signal generation, such as closing prices, and it’s the foundational parameter upon which the oscillator functions.

Normalization Settings: Users can select the normalization mode (“All”, “Window”, or “Disabled”), influencing how the oscillator scales its values. When enabled, it will scale from 100 to -100, allowing the user to understand better the relative positioning of price data.

Smoothing: This indicator offers advanced smoothing features, with options for additional smoothing, allowing traders to adjust the signal's sensitivity to price movements.

Kumo & Chikou Visibility: Traders can customize the visibility settings of Kumo and Chikou, tailoring the display of each component to their preference, enabling a cleaner and more intuitive view of market conditions.

Color Coding: Each component and condition, like bullish or bearish states, can be color-coded, providing visual cues to enhance the interpretability of market trends and states.

Color on Conversion: The oscillator provides an option to color the signal based on the crossover of the conversion and base lines.

Divergence: The oscillator can detect and highlight regular and hidden bullish and bearish divergences between the signal and price, aiding traders in identifying potential trend reversals or continuations.

Alerts:

The list of inbuilt alerts are provided below:

Inside Cloud: The signal line is inside the cloud.

Up Out of Cloud: The signal line crossed above the cloud.

Down Out of Cloud: The signal line crossed below the cloud.

Future Kumo Cross Bullish: The future Kumo lines have crossed in a bullish manner.

Future Kumo Cross Bearish: The future Kumo lines have crossed in a bearish manner.

Current Kumo Cross Bullish: The current Kumo lines have crossed in a bullish manner.

Current Kumo Cross Bearish: The current Kumo lines have crossed in a bearish manner.

Conversion Base Bullish: The conversion line crossed above the base line.

Conversion Base Bearish: The conversion line crossed below the base line.

Signal Bullish on Conversion Base: The signal line crossed above the maximum of conversion and base lines.

Signal Bearish on Conversion Base: The signal line crossed below the minimum of conversion and base lines.

Chikou Bullish: The Chikou line crossed above zero.

Chikou Bearish: The Chikou line crossed below zero.

Signal Over Max: The signal line crossed above the max level.

Signal Over High: The signal line crossed above the high level.

Signal Under Min: The signal line crossed below the min level.

Signal Under Low: The signal line crossed below the low level.

Chikou Over Max: The Chikou line crossed above the max level.

Chikou Over High: The Chikou line crossed above the high level.

Chikou Under Min: The Chikou line crossed below the min level.

Chikou Under Low: The Chikou line crossed below the low level.

Signal Crossover MA: The signal line crossed over the moving average.

Signal Crossunder MA: The signal line crossed under the moving average.

Regular Bullish Divergence: Regular bullish divergence detected.

Hidden Bullish Divergence: Hidden bullish divergence detected.

Regular Bearish Divergence: Regular bearish divergence detected.

Hidden Bearish Divergence: Hidden bearish divergence detected.

Bounce off of Kumo Up: Bullish Bounce off of Kumo.

Bounce off of Kumo Down: Bearish Bounce off of Kumo.

By providing a cohesive visualization of the Ichimoku elements and market momentum within a bounded range, this oscillator is a unique tool and insight into markets.

RVI_HTFThe "RVI_HTF" indicator is a tool designed to assist traders in analyzing market trends using the Relative Vigor Index (RVI) across different timeframes. It enables users to customize various aspects of the indicator's appearance and behavior. By monitoring the RVI on different timeframes, tracking its relationship with the moving average, and paying attention to extreme arrows above the 80 or below the 20 line, traders can anticipate potential reversals, trends, or changes in market momentum.

Above 80 Line: When the RVI moves above the 80 line, it suggests that the market may be overbought. Extreme upward arrows (indicating potential sell signals) can be a sign that a bullish trend might be reaching an exhaustion point. Traders may anticipate a possible trend reversal or pullback.

Below 20 Line: When the RVI dips below the 20 line, it implies that the market might be oversold. Extreme downward arrows (indicating potential buy signals) can be an early signal of a potential bullish reversal. Traders may anticipate an upcoming uptrend or bounce.

Crossing Above Moving Average: When the RVI crosses above its moving average on the selected timeframe, it can serve as an early indication of potential bullish strength in the market. This suggests that buying pressure may be increasing.

Crossing Below Moving Average: Conversely, when the RVI crosses below its moving average, it can signal potential bearish momentum. This indicates that selling pressure may be gaining strength.

Variables:

Timeframe (TF) Selection:

The indicator allows you to select the timeframe for the RVI calculation. You can choose from various options such as 1 minute (1), 5 minutes (5), 15 minutes (15), 30 minutes (30), 60 minutes (60), 240 minutes (240), Daily (D), Weekly (W), Monthly (M), or use "Auto" to automatically select a higher timeframe based on your current chart's timeframe.

Moving Average Type (MA_Type):

Function: Allows users to select the type of moving average used in RVI calculations.

Options: You can select from various moving average types, including:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

SMMA (Smoothed Moving Average, also known as RMA)

WMA (Weighted Moving Average)

VWMA (Volume Weighted Moving Average)

DEMA (Double Exponential Moving Average)

Moving Average Length (MA_Length):

Function: Permits users to set the number of periods for the selected moving average type.

Purpose: Controls the sensitivity of the RVI indicator. Longer lengths provide smoother results, while shorter lengths react more quickly to price changes.

Up Arrow Color (upArrowColor):

Function: Enables users to customize the color of arrows that indicate potential Overbought areas. (Only shown when the TF is same as or lower than the chart TF)

Down Arrow Color (downArrowColor):

Function: Allows users to specify the color of downward-pointing arrows signaling potential Oversold areas. (Only shown when the TF is same as or lower than the chart TF)

RVI Up Color (firstColor):

Function: Defines the color of the RVI line when it indicates a bullish condition on the higher timeframe.

RVI Down Color (secondColor):

Function: Specifies the color of the RVI line when it suggests a bearish condition on the higher timeframe.

RVI-Based Moving Average Up Color (firstColorMA):

Function: Customizes the color of the RVI-based moving average line when it indicates a bullish condition.

RVI-Based Moving Average Down Color (secondColorMA):

Function: Defines the color of the RVI-based moving average line when it suggests a bearish condition.

GKD-C Correlation Trend [Loxx]The Giga Kaleidoscope GKD-C Correlation Trend is a confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ GKD-C Correlation Trend

The Correlation Trend Indicator (CTI) by John Ehlers is predicated on comparing the price curve of a security to an ideal trend line, which is conceptualized as a straight line with an upward trajectory. The CTI quantifies this relationship through the Spearman correlation, calculating how closely the price curve aligns with this ideal trend line over a specified period.

Ehlers envisions this indicator as a mean reverting trend identification oscillator, which can oscillate between values of +1.0 and -1.0, irrespective of the asset or time frame being analyzed. The underlying principle is to decipher how well the price history of a security corresponds to a presumed ideal trend, which is represented by a straight upward line. This indicator thus serves to help traders understand the trend dynamics of the market they are operating in.

In practical terms, the CTI could be utilized by traders to gauge the strength and direction of prevailing market trends, aiding in the decision-making process for entering or exiting trades.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

What is an Metamorphosis indicator?

The concept of a metamorphosis indicator involves the integration of two or more GKD indicators to generate a compound signal. This is achieved by evaluating the accuracy of each indicator and selecting the signal from the indicator with the highest accuracy. As an illustration, let's consider a scenario where we calculate the accuracy of 10 indicators and choose the signal from the indicator that demonstrates the highest accuracy.

The resulting output from the metamorphosis indicator can then be utilized in a GKD-BT backtest by occupying a slot that aligns with the purpose of the metamorphosis indicator. The slot can be a GKD-B, GKD-C, or GKD-E slot, depending on the specific requirements and objectives of the indicator. This allows for seamless integration and utilization of the compound signal within the GKD-BT framework.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

6. GKD-M - Metamorphosis module (Metamorphosis, Number 8 in the NNFX algorithm, but not part of the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Multi-Ticker CC Backtest

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: Advance Trend Pressure as shown on the chart above

Confirmation 2: uf2018

Continuation: Coppock Curve

Exit: Rex Oscillator

Metamorphosis: Baseline Optimizer

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, GKD-M, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

? Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

[blackcat] L3 CCI-RSI ComboCCI-RSI Combo indicator is a combination indicator that includes CCI and RSI. It uses some parameters to calculate the values of CCI and RSI, and generates corresponding charts based on these values. On the chart, when CCI exceeds 100 or falls below -100, yellow or magenta filling areas are displayed. Additionally, gradient colors are used on the RSI chart to represent different value ranges. Based on the values of CCI and RSI, buying or selling signals can be identified and "B" or "S" labels are displayed at the corresponding positions. It utilizes some technical indicators and logic to generate buying and selling signals, and displays the corresponding labels on the chart.

Here are the main parts of the code:

1. Definition of some variables:

- `N`, `M`, `N1`: Parameters used to calculate CCI and RSI.

- `xcn(cond, len)` and `xex(cond, len)`: Two functions used to calculate the number of times a condition is met.

2. Calculation of CCI (Commodity Channel Index):

- Calculate the CCI value based on the formula `(TYP - ta.sma(TYP, M)) / (0.015 * ta.stdev(TYP, M))`.

- Use the `plot()` function to plot CCI on the chart and set the color based on its value.

3. Calculation of RSI (Relative Strength Index):

- First calculate RSI1 by taking the average of positive differences between closing prices and the average of all absolute differences, and then multiplying by 100.

- Then use the ALMA function to transform RSI1 into a smoother curve.

- Use the `plot()` function to plot RSI on the chart and select gradient colors for shading based on its value.

4. Setting up the gradient color array:

- Create a color array using `array.new_color()` and add a series of color values to it.

5. Generating buying and selling signals based on conditions:

- Use logical operators and technical indicator functions to determine the conditions for buying and selling.

- Use the `label.new()` function to draw the corresponding labels on the chart to represent buying or selling signals.

MADALGO`s Enhanced OBV DivergencesDescription:

MADALGO's Enhanced OBV Divergences indicator is a unique tool designed for traders to visualize the divergences between price action and On Balance Volume (OBV), a fundamental aspect often indicative of underlying strength or weakness in the market. By keenly identifying these divergences, traders are better positioned to anticipate potential trend reversals or trend continuations, making this script an invaluable addition to their technical analysis toolkit.

This script meticulously scans for both regular and hidden bullish/bearish divergences, providing a comprehensive view of market sentiment. The core of this indicator is built around the OBV, which cumulatively adds or subtracts volume based on the price movement per period, thus providing a running total of volume and portraying the force behind the price movements.

The regular divergences are classic indicators of a potential reversal in the current trend, while hidden divergences are often indicative of trend continuation. These divergences are pinpointed based on the relative positions of the OBV and price highs/lows, over customizable lookback periods and within specified lookback ranges.

Features:

Regular and Hidden Divergences: Clearly marked bullish and bearish divergences provide insights into potential market turning points.

On Balance Volume (OBV) Line: Visualize the continuous flow of buying and selling pressure, enabling the identification of accumulation or distribution phases essential for understanding the market's strength or weakness.

Moving Average of OBV: An optional feature to smooth the OBV line, aiding in the identification of the overarching trend.

Dynamic Statistics Label: A floating label provides real-time updates on essential statistics like the Rate of Percentage Change (RPC) of OBV, the last divergences, and bars since the last divergences.

Inputs:

Pivot Lookback Right and Pivot Lookback Left: Define the lookback periods for identifying pivot points in the OBV line.

Max of Lookback Range and Min of Lookback Range: Define the range for considering divergences.

RPC Period: Defines the period for calculating the Rate of Percentage Change of the OBV.

MA Period: Defines the period for the optional moving average of the OBV.

Plot Bullish, Plot Hidden Bullish, Plot Bearish, Plot Hidden Bearish: Toggle visibility of respective divergences.

Plot Moving Average: Toggle visibility of the OBV moving average.

Usage:

Add the script to your TradingView chart.

Tailor the input parameters in the settings panel to align with your analysis requirements.

The divergences, OBV line, and optional moving average will be plotted on your chart, with a dynamic label displaying real-time statistics.

Set up alerts to be notified of identified divergences, enabling timely decision-making.

Alerts:

Regular bullish/bearish divergence in OBV found: Triggered when a regular bullish or bearish divergence is identified.

Hidden bullish/bearish divergence in OBV found: Triggered when a hidden bullish or bearish divergence is identified.

Underlying Concepts:

The OBV Divergences indicator is rooted in the principle that volume precedes price movement. When prices are rising with increased volume, it suggests that buying pressure is prevailing and may lead to continued upward momentum. Conversely, rising prices with decreasing volume might indicate a lack of buying conviction and could signal a potential price reversal. The identification of divergences between price and OBV can therefore serve as a powerful signal for traders. These examples can be seen below in the image

The Moving Average of the OBV further aids in understanding the prevailing trend by smoothing out the OBV line, providing a clearer picture of the market's longer-term momentum. The Rate of Percentage Change (RPC) provides insight into the momentum of volume, offering an additional layer of analysis. Together, these additional features enhance the core OBV analysis, enabling a more nuanced understanding of volume dynamics fundamental for making more informed trading decisions.

License:

This Source Code Form is subject to the terms of the Mozilla Public License, v. 2.0. If a copy of the MPL was not distributed with this file, you can obtain one at Mozilla Public License 2.0.

PCA-Risk IndicatorOBJECTIVE:

The objective of this indicator is to synthesize, via PCA (Principal Component Analysis), several of the most used indicators with in order to simplify the reading of any asset on any timeframe.

It is based on my Bitcoin Risk Long Term indicator, and is the evolution of another indicator that I have not published 'Average Risk Indicator'.

The idea of this indicator is to use statistics, in this case the PCA, to reduce the number of dimensions (indicator) to aggregate them in some synthetic indicators (PCX)

I invite you to dig deeper into the PCA, but that is to try to keep as much information as possible from the raw data. The signal minus the noise.

I realized this indicator a year ago, but I publish it now because I do not see the interest to keep it private.

USAGE:

Unlike the Bitcoin Risk Long Term indicator, it does not make sense to change or disable the input indicators unless you use the 'Average Indicator' function. Because each input is weighted to generate the outputs, the PCX.

I extracted several courses (Bitcoin, Gold, S&P, CAC40) on several timeframes (W, D, 4h, 1h) of Trading view and use the Excel generated for the data on which I played the PCA analysis.

The results:

explained_variance_ratio: 0.55540809 / 0.13021972 / 0.07303142 / 0.03760925

explained_variance: 11.6639671 / 2.73470717 / 1.53371209 / 0.7898212

Interpretation:

Simply put, 55% of the information contained in each indicator can be represented with PC1, +13% with PC2, +7% with PC3, +3% with PC4.

What is important to understand is that PC1, which serves as a thermometer in a way, gives a simple indication of over-buying or over-selling area better than any other indicator.

PC2, difficult to interpret, is more reactive because precedes PC1, but can give false signals.

PC3 and PC4 do not seem relevant to me.

The way I use it is to take PC1 for Risk indicator, and display PC2 with 'Area'. When PC2 turns around and PC1 arrives on extremes, it can be good points to act.

NOTES :

- It is surprising that a simple average of all the indicators gives a fairly relevant result

- With Average indicator as Risk indicator, you can combine the indicators of your choice and see the predictive power with the staining of bars.

- You can add alerts on the levels of your choice on the Risk Indicator

- If you have any idea of adding an indicator, modification, criticism, bug found: share them, it’s appreciated!

---- FR ----

OBJECTIF :

L'objectif de cet indicateur est de synthétiser, via l'ACP (Analyse en Composantes Principales), plusieurs indicateurs parmi les plus utilisés avec afin de simplifier la lecture de n'importe quel actif sur n'importe quel timeframe.

Il est inspiré de mon indicateur 'Bitcoin Risk Long Term indicator', et est l'évolution d'un autre indicateur que je n'ai pas publié 'Average Risk Indicator'.

L'idée de cet indicateur est d'utiliser les statistiques, en l'occurence l'ACP, pour réduire le nombre de dimensions (indicateur) pour les agréger dans quelques indicateurs synthétiques (PCX)

Je vous invite à creuser l'ACP, mais c'est chercher à conserver un maximum d'informations à partir de la donnée brute. Le signal moins le bruit.

J'ai réalisé cet indicateur il y a un an, mais je le publie maintenant car je ne vois pas l'intérêt de le garder privé.

UTILISATION :

Contrairement à 'Bitcoin Risk Long Term indicator', il ne fait pas sens de modifier ou désactiver les indicateurs inputs, sauf si vous utiliser la fonction 'Average Indicator'. Car chaque input est pondéré pour générer les outputs, les PCX.

J'ai extrait plusieurs cours (Bitcoin, Gold, S&P, CAC40) sur plusieurs timeframes (W, D, 4h, 1h) de Trading view et utiliser les Excel généré pour la data sur laquelle j'ai joué l'analyse ACP.

Les résultats :

explained_variance_ratio : 0.55540809 / 0.13021972 / 0.07303142 / 0.03760925

explained_variance : 11.6639671 / 2.73470717 / 1.53371209 / 0.7898212

Interprétation :

Pour faire simple, 55% de l'information contenu dans chaque indicateur peut être représenté avec PC1, +13% avec PC2, +7% avec PC3, +3% avec PC4.

Ce qui faut y comprendre c'est que le PC1, qui sert de thermomètre en quelque sorte, donne une indication simple de zone de sur-achat ou sur-vente mieux que n'importe quel autre indicateur.

PC2, difficile à interpréter, est plus réactif car précède PC1, mais peut donner des faux signaux.

PC3 et PC4 ne me semble pas pertinent.

La manière dont je m'en sert c'est de prendre PC1 pour Risk indicator, et d'afficher PC2 avec 'Region'. Lorsque PC2 se retourne et que PC1 arrive sur des extrêmes, cela peut être des bons points pour agir.

NOTES :

- Il est étonnant de constater qu'une simple moyenne de tous les indicateurs donne un résultat assez pertinent

- Avec Average indicator comme Risk indicator, vous pouvez combiner les indicateurs de vos choix et voir la force prédictive avec la coloration des bars.

- Vous pouvez ajouter des alertes sur les niveaux de votre choix sur le Risk Indicator

- Si vous avez la moindre idée d'ajout d'indicateur, modification, critique, bug trouvé : partagez-les, c'est apprécié !

Heatmap MACD StrategyHello traders

A customer gave me the idea indirectly after I made an update to that script:

Supertrend MTF Heatmap

Important Notes

The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

I wanted to showcase that any Heatmap script can be converted into a strategy.

The strategy default settings are:

Initial Capital: 100000 USD

Position Size: 1 contract

Commission Percent: 0.075%

Slippage: 1 tick

No margin/leverage used

For example, those are realistic settings for trading CFD indices with low timeframes, but not the best possible settings for all assets/timeframes.

Concept

The Heatmap MACD Strategy allows selecting one MACD in five different timeframes.

You'll get an exit signal whenever one of the 5 MACDs changes direction.

Then, the strategy re-enters whenever all the MACDs are in the same direction again.

It takes:

long trades when all the 5 MACD histograms are bullish

short trades when all the 5 MACD histograms are bearish

You can select the same timeframe multiple times if you don't need five timeframes.

For example, if you only need the 30min, the 1H, and 2H, you can set your timeframes as follow:

30m

30m

30m

1H

2H

Risk Management Features

Nothing too fancy

All the features below are pips-based

Stop-Loss

Trailing Stop-Loss

Stop-Loss to Breakeven after a certain amount of pips has been reached

Take Profit 1st level and closing X% of the trade

Take Profit 2nd level and close the remaining of the trade

What's next?

I'll publish this script's open-source Pineconnector, ProfitView, and AutoView versions for educational purposes.

Thank you

Dave

Triple Ehlers Market StateClear trend identification is an important aspect of finding the right side to trade, another is getting the best buying/selling price on a pullback, retracement or reversal. Triple Ehlers Market State can do both.

Three is always better

Ehlers’ original formulation produces bullish, bearish and trendless signals. The indicator presented here gate stages three correlation cycles of adjustable lengths and degree thresholds, displaying a more refined view of bullish, bearish and trendless markets, in a compact and novel way.

Stick with the default settings, or experiment with the cycle period and threshold angle of each cycle, then choose whether ‘Recent trend weighting’ is included in candle colouring.

John Ehlers is a highly respected trading maths head who may need no introduction here. His idea for Market State was published in TASC June 2020 Traders Tips. The awesome interpretation of Ehlers’ work on which Triple Ehlers Market State’s correlation cycle calculations are based can be found at:

DISCLAIMER: None of this is financial advice.

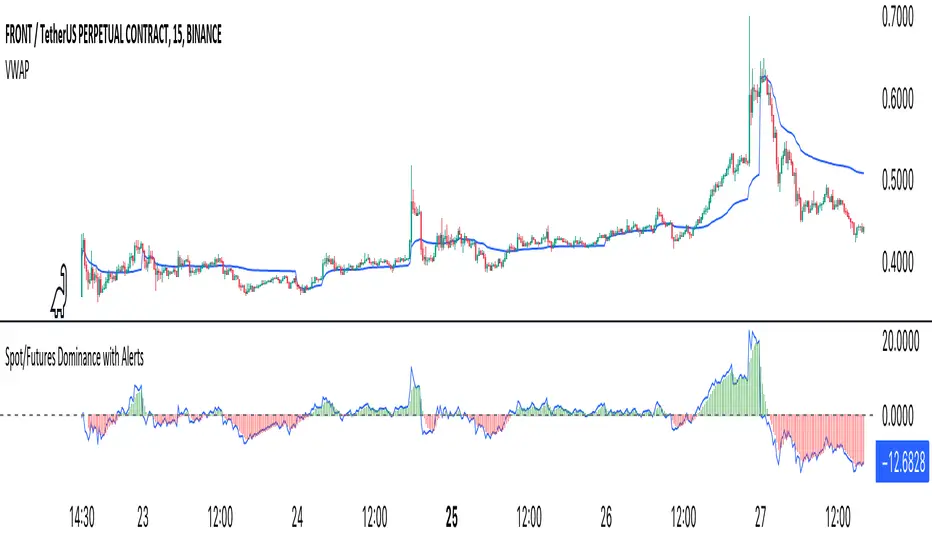

Crypto Spot/Futures Dominance Indicator with AlertsFutures/Spot Dominance Indicator:

Overview:

The futures/spot dominance indicator is a versatile tool used by traders and analysts to assess the relative strength or dominance of the futures market in relation to the spot (or cash) market for a specific asset. It offers insights into market sentiment, potential arbitrage opportunities, and risk management while incorporating the VWAP indicator for added context.

How It Works:

This indicator automatically detects and adapts to the futures symbol applied to the chart, simplifying the setup for traders. However, it still necessitates manual input of the corresponding spot pair to ensure accuracy.

Automatic Futures Symbol Detection: The indicator starts by automatically detecting the futures symbol on the trading chart, eliminating the need for manual configuration. This ensures that the indicator is applied to the correct futures contract.

Manual Spot Pair Entry: To provide a reliable reference point for the comparison, traders must manually input the corresponding spot symbol via the indicator's inputs. For instance, if the indicator detects the BTCUSDT.P futures symbol, traders would manually enter the BTCUSDT spot symbol.

Gathering Data: The indicator collects historical price data for both the detected futures contract and the manually specified spot symbol. This data includes open, high, low, and close prices, as well as trading volume.

VWAP Calculation: To gain a deeper understanding of price trends and market dynamics, the indicator calculates the VWAP (Volume Weighted Average Price) for both the futures and spot markets. The VWAP places more weight on prices with higher trading volume, offering a weighted average that reflects market consensus.

Premium/Discount Calculation: By subtracting the VWAP of the spot market from the VWAP of the futures market, the indicator quantifies the premium or discount of the futures price concerning the spot price. A positive value indicates a premium, while a negative value suggests a discount.

Plotting: The premium/discount value is displayed as a line on the chart, often alongside moving averages or other smoothing techniques for improved trend analysis.

Alerts: In addition to its analysis capabilities, this indicator now includes alerts to enhance your trading experience. It alerts you in the following scenarios:

Premium Above Average: Notifies you when the premium crosses above the average line.

Premium Below Average: Alerts you when the premium crosses below the average line.

Premium Above Zero: Provides an alert when the premium crosses above the zero line.

Premium Below Zero: Generates an alert when the premium crosses below the zero line.

Benefits of the Futures/Spot Dominance Indicator:

Sentiment Analysis: Traders use the indicator to assess market sentiment. A futures premium might signify bullish sentiment, while a discount could indicate bearish sentiment.

Arbitrage Opportunities: Identifying price discrepancies between futures and spot markets can help traders spot arbitrage opportunities, where they can profit from price differentials.

Risk Management: The indicator assists in evaluating risks associated with futures positions, helping traders manage their exposure effectively.

Trend Confirmation: When used in conjunction with other technical indicators, futures/spot dominance, along with VWAP, can provide additional confirmation of price trends.

Hedging: Investors and corporations use this tool to gauge the effectiveness of hedging strategies based on futures contracts.

Speculative Trading: Traders and investors use the indicator to inform speculative positions, aligning their trades with perceived market strength or weakness.

Insightful Analysis: Futures/spot dominance analysis, enriched by VWAP data, offers insights into market behavior during specific events or changes in economic conditions.

In summary, the futures/spot dominance indicator, with its integration of VWAP and automatic futures symbol detection, provides traders and investors with a comprehensive tool to assess market dynamics. It aids in sentiment analysis, risk management, and trend confirmation while offering potential arbitrage opportunities. The newly added alerts enhance the indicator's functionality, providing timely notifications of key market events. However, it relies on manual input of the corresponding spot pair to ensure precise comparisons between futures and spot markets. It should be used alongside other analysis techniques for a well-rounded view of the market.

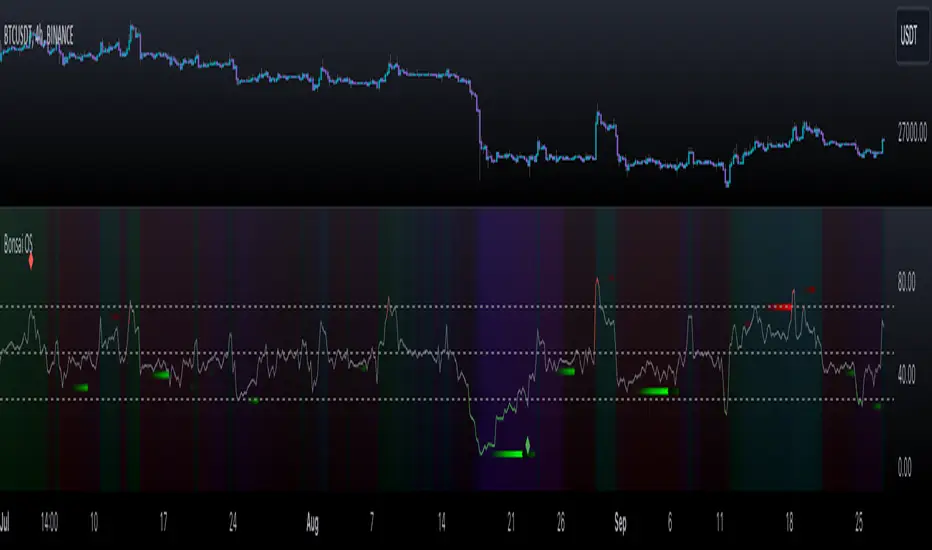

Bonsai OS (Oscillators)Bonsai OS combines four oscillators (RSI, CCI, Stochastic, MACD) in one interface. Features divergence detection, color-intensity, and insights into divergences. Assists traders in spotting potential pivot points.

═════════════════════════════════════════════════════════════════════════

🌳 Bonsai OS 🌳 Advanced Oscillator Suite

📘 Overview

Bonsai OS is a tool tailored for traders focusing on reversal strategies and those keen on identifying market divergences. Combining multiple oscillators into one unified interface, it aids traders in pinpointing potential pivot reversal points.

📌 Algorithm Logic

• Multi-Oscillator Integration: Bonsai OS calculates and integrates the values from four standard oscillators: RSI, CCI, Stochastic, and MACD. Each oscillator's value is derived from its respective mathematical formula, analyzing historical data points.

• Divergence Detection: The tool runs a series of comparisons between price action and oscillator values. When discrepancies (divergences) are observed, they are highlighted, suggesting potential market reversals.

• Price Strength Visualization: A gradient background that is determined by an average of the oscillator values in relation to their historical norms, thereby providing a visual cue about the current price strength, whether it is strong or weak.

• Alerts: Users can set up notifications based on specific divergence insights. Once set criteria are met, alerts are triggered.

🎯 Purpose

• For Professionals: Bonsai OS offers integrated oscillator readings, allowing a more in-depth market analysis.

• For Beginners: Simplified readings and visual cues make it easier for newcomers to understand oscillator indicators and market conditions.

🛠 Distinctive Elements

• Oscillator Fusion: Bonsai OS goes beyond just grouping oscillators. It looks for matching divergences across them, aiming to find stronger signals for market reversals.

• Divergence Indicators: Bonsai OS identifies divergence patterns between price trends and oscillator readings, highlighting their intensity with color variations.

• Insight into Failed Divergences: Recognizing not all divergences lead to reversals, Bonsai OS provides markers for potential false signals, helping traders exercise caution and fine-tune their strategies.

Getting Bullish/Bearish and Divergences

📊 Features

• Data Source Customization: Users have the flexibility to choose between default data inputs or adjust to their preferred price points (like High & Low).

• Combined Divergence Signals: Beyond individual oscillator divergences, Bonsai OS identifies instances when several oscillators indicate divergence at the same time.

• Adaptable Outputs: Outputs like 'Bullish Divergence ▲', 'Getting Bullish ▲', 'Getting Bearish ▼' and 'Bearish Divergence ▼' are plotted as non-displayable 1 or 0 for seamless integration into other custom indicators, ensuring a harmonious integration.

Here's an example of a custom indicator that can be used for inputting data from external sources:

//@version=5

indicator("My Script Template", overlay = true)

group_name = "External Source"

external = input.source(title = "Source", defval = close, inline = "external", group = group_name)

val = input.int(title = ">", defval = 0, inline = "external", group = group_name)

// Your logic follows here...

Bonsai OS as External Source

🎛 How To Use Bonsai OS

1. Select the desired oscillator.

2. Monitor the color changes for market condition insights.

3. Look out for divergence markers to anticipate potential market shifts.

4. If required, set up alerts for real-time updates.

Indicator Settings Menu

📜 Feedback & Continual Development

We welcome your feedback. It's essential for the continuous improvement of Bonsai OS and to better serve the TradingView community.

❗️ Disclaimer

Trading involves risks. Bonsai OS aims to provide an analytical tool to support traders, but it's essential to complement its insights with other research. Always seek advice from financial professionals and trade responsibly.

Weighted Bulls-Bears Variety Smoothed [Loxx]Weighted Bulls-Bears Variety Smoothed highlights potential buy and sell moments in the market. Users can customize the data source and select their preferred type of moving average for calculations. The resulting visualization is a column-style plot that changes color based on bullish or bearish market conditions. Additionally, the script can color chart bars and provide visual markers to indicate buying ("Long") or selling ("Short") opportunities. Alerts can also be set for these trading signals.

█ Inputs:

Users can choose the source for calculations (e.g., closing price).

They can set periods for calculations and smoothing.

They can select the type of moving average they prefer for smoothing: EMA, FEMA, LWMA, SMA, or SMMA.

█ Weighted Bulls-Bears Calculation:

It determines the highest and lowest prices over a user-defined period.

Then, it calculates the 'bull' and 'bear' values based on these highest and lowest prices. These values are weighted based on their distance from the current price.

█ Extras

Alerts

Signals

GKD-C Chaos Visual Averages [Loxx]The Giga Kaleidoscope GKD-C Chaos Visual Averages is a confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

? GKD-C Chaos Visual Averages

One of the most common errors made by inexperienced traders is attempting to extract excessive information from a single chart by employing numerous unnecessary indicators. The outcome often entails a cluttered chart filled with lines, erratic patterns, and an assortment of distracting elements, all of which weave a conflicting narrative for the trader.

This on-screen "clutter" can bewilder new traders, compelling them to open or maintain unprofitable positions until the dreaded Margin Call looms.

The advice is clear: Keep it simple. But how can one achieve this simplicity?

Enter the Chaos Visual Averages indicator

This indicator not only generates the most precise reversal signals available but also equips traders to seamlessly align with prevailing trends and engage in counter-trend trading to realign with the overall market direction.

For traders opting to employ Chaos, a clean and uncluttered chart is recommended, eschewing the use of additional oscillators, as all the necessary components are already integrated into Visual Chaos.

Tip: Crafting a straightforward and profitable trading system with Chaos involves marking Weekly and Daily Support and Resistance lines and executing counter-trend trades as price approaches these key levels, utilizing the Overbought Extreme and Oversold Extreme signals from the 15-minute Chaos.

Pros:

Remarkable precision in identifying market reversals.

Visually appealing and easily interpretable market conditions.

Suitable for both trend-following and counter-trend trading.

Robust back-testing results (nearly 95% accuracy on "Extreme" signals).

An all-encompassing indicator capable of supporting a livelihood through trading.

Cons:

In rare instances, even with Overbought "Extreme" and Oversold "Extreme" conditions, the indicator may lead to trading against a robust trend, resulting in significant drawdowns before eventual price reversal.

Overbought "Extreme" and Oversold "Extreme" signals can be infrequent when trading on the 15-minute timeframe and above. To mitigate this, it is advisable to trade at least 8 major currency pairs to receive "Extreme" signals with greater frequency."

? Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

What is an Metamorphosis indicator?

The concept of a metamorphosis indicator involves the integration of two or more GKD indicators to generate a compound signal. This is achieved by evaluating the accuracy of each indicator and selecting the signal from the indicator with the highest accuracy. As an illustration, let's consider a scenario where we calculate the accuracy of 10 indicators and choose the signal from the indicator that demonstrates the highest accuracy.

The resulting output from the metamorphosis indicator can then be utilized in a GKD-BT backtest by occupying a slot that aligns with the purpose of the metamorphosis indicator. The slot can be a GKD-B, GKD-C, or GKD-E slot, depending on the specific requirements and objectives of the indicator. This allows for seamless integration and utilization of the compound signal within the GKD-BT framework.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

6. GKD-M - Metamorphosis module (Metamorphosis, Number 8 in the NNFX algorithm, but not part of the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Multi-Ticker CC Backtest

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: Advance Trend Pressure as shown on the chart above

Confirmation 2: uf2018

Continuation: Coppock Curve

Exit: Rex Oscillator

Metamorphosis: Baseline Optimizer

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, GKD-M, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

? Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

Auto Fibo on IndicatorsThis drawing tool aims to draw auto Fibonacci Retracement Levels on desired indicators.

Users can define the target indicator to draw Auto Fibo Lines, from the "settings tab":

There are six commonly used indicators below the charts that can be selected to draw Fibonacci Retracement lines on:

RSI : Relative Strength Index

CCI : Commodity Channel Index

MFI : Money Flow Index

STOCHASTIC : Stochastic Oscillator

CMF : Chaikin Money Flow

CMO : Chande Momentum Oscillator

Fibonacci Retracement Levels will appear automatically after applying the indicator.

The "Auto Fibo on Indicators" tool looks back. It checks the indicator levels for a desired number of bars and then draws the Fibonacci Levels automatically in the right way, considering the final movements of the indicator.

There are five commonly used Fibonacci Levels added between the Highest and Lowest values such as:

%23.6

%38.2

%50 (Not precisely a Fibonacci Level, indeed)

%61.8 (Golden Ratio)

%78.6

Four extra levels can be added from the settings tab by checking their boxes:

%127.2 (adjustable level)

%161.8

%261.8

%361.8

Default lookback bars of Auto Fibo Levels: 144 (which is also a Fibonacci number)

Default Indicator: RSI

Default Indicator length: 14

Default data source: CLOSE

Users can also define and show overbought and oversold levels by unchecking the "Do not Show Indicator Overbought / Oversold Levels?" button from the settings menu.

In technical analysis, Fibonacci Levels on price can guide valuable trading signals for investors.

Levels can be significant support and resistance levels for breakouts and turning points.

This drawing tool aims to follow those necessary levels on indicators to observe critical levels and breakouts.

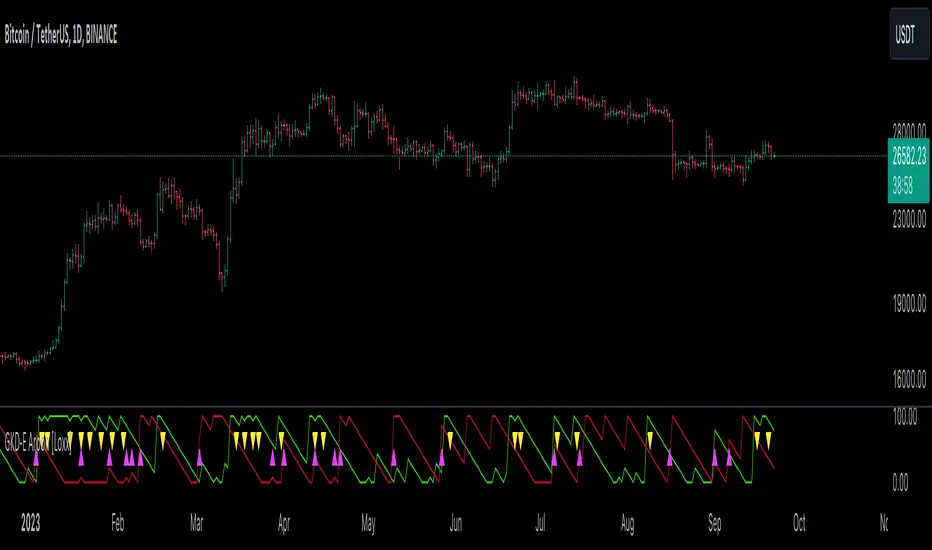

GKD-E Aroon [Loxx]The Giga Kaleidoscope GKD-E Aroon is an exit module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ GKD-E Aroon

The Aroon Indicator is a technical analysis tool used to assess the strength and direction of a trend in a financial market, such as stocks, forex, or commodities. It consists of two lines: the Aroon Up and the Aroon Down. These lines measure the time it takes for an asset's price to reach its highest and lowest points within a specific period, usually 25 periods.

The Aroon Up line quantifies how many periods it has been since the highest price point occurred, while the Aroon Down line measures the number of periods since the lowest price point. The values range from 0 to 100, with higher values indicating a stronger trend. When the Aroon Up is above the Aroon Down, it suggests a bullish trend, and when the Aroon Down is above the Aroon Up, it indicates a bearish trend. Traders use these signals to make informed decisions about buying or selling assets and to identify potential trend changes. The Aroon Indicator can be a valuable tool in a trader's technical analysis toolkit.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).