Price based concepts / quantifytools- Overview

Price based concepts incorporates a collection of multiple price action based concepts. Main component of the script is market structure, on top of which liquidity sweeps and deviations are built on, leaving imbalances the only standalone concept included. Each concept can be enabled/disabled separately for creating a selection of indications that one deems relevant for their purposes. Price based concepts are quantified using metrics that measure their expected behavior, such as historical likelihood of supportive price action for given market structure state and volume traded at liquidity sweeps. The concepts principally work on any chart, whether that is equities, currencies, cryptocurrencies or commodities, charts with volume data or no volume data. Essentially any asset that can be considered an ordinary speculative asset. The concepts also work on any timeframe, from second charts to monthly charts. None of the indications are repainted.

Market structure

Market structure is an analysis of support/resistance levels (pivots) and their position relative to each other. Market structure is considered to be bullish on a series of higher highs/higher lows and bearish on a series of lower highs/lower lows. Market structure shifts from bullish to bearish and vice versa on a break of the most recent pivot high/low, indicating weak ability to defend a key level from the dominating side. Supportive market structure typically provides lengthier and sustained trending environment, making it an ideal point of confluence for establishing directional bias for trades.

Liquidity sweeps

Liquidity sweeps are formed when price exceeds a pivot level that served as a provable level of demand once and is expected to display demand again when revisited. A simple way to look at liquidity sweeps is re-tests of untapped support/resistance levels.

Deviations

Deviations are formed when price exceeds a reference level (market structure shift level/liquidity sweep level) and shortly closes back in, leaving participating breakout traders in an awkward position. On further adverse movement, stuck breakout traders are forced to cover their underwater positions, creating ideal conditions for a lengthier reversal.

Imbalances

Imbalances, also known as fair value gaps or single prints, depict areas of inefficient and one sided transacting. Given inclination for markets to trade efficiently, price is naturally attracted to areas that lack proper participation, making imbalances ideal targets for entries or exits.

Key takeaways

- Price based concepts consists of market structure, liquidity sweeps, deviations and imbalances.

- Market structure shifts from bullish to bearish and vice versa on a break of the most recent pivot high/low, indicating weak ability to defend a key level from the dominating side.

- Supportive market structure tends to provide lengthier and sustained movement for the dominating side, making it an ideal foundation for establishing directional bias for trades.

- Liquidity sweeps are formed when price exceeds an untapped support/resistance level that served as a provable level of demand in the past, likely to show demand again when revisited.

- Deviations are formed when price exceeds a key level and shortly closes back in, leaving breakout traders in an awkward position. Further adverse movement compels trapped participants to cover their positions, creating ideal conditions for a reversal.

- Imbalances depict areas of inefficient and one sided transacting where price is naturally attracted to, making them ideal targets for entries or exits.

- Price based concepts are quantified using metrics that measure expected behavior, such as historical likelihood of supportive structure and volume traded at liquidity sweeps.

- For practical guide with practical examples, see last section.

Accessing script 🔑

See "Author's instructions" section, found at bottom of the script page.

Disclaimer

Price based concepts are not buy/sell signals, a standalone trading strategy or financial advice. They also do not substitute knowing how to trade. Example charts and ideas shown for use cases are textbook examples under ideal conditions, not guaranteed to repeat as they are presented. Price based concepts notify when a set of conditions are in place from a purely technical standpoint. Price based concepts should be viewed as one tool providing one kind of evidence, to be used in conjunction with other means of analysis.

Price based concepts are backtested using metrics that reasonably depict their expected behaviour, such as historical likelihood of supportive price movement on each market structure state. The metrics are not intended to be elaborate and perfect, but to serve as a general barometer for feedback created by the indications. Backtesting is done first and foremost to exclude scenarios where the concepts clearly don't work or work suboptimally, in which case they can't be considered as valid evidence. Even when the metrics indicate historical reactions of good quality, price impact can and inevitably does deviate from the expected. Past results do not guarantee future performance.

- Example charts

Chart #1 : BTCUSDT

Chart #2 : EURUSD

Chart #3 : ES futures

Chart #4 : NG futures

Chart #5 : Custom timeframes

- Concepts

Market structure

Knowing when price has truly pivoted is much harder than it might seem at first. In this script, pivots are determined using a custom formula based on volatility adjusted average price, a fundamentally different approach to the widely used highest/lowest price within X amount of bars. The script calculates average price within set period and adjusts it to volatility. Using this formula, the script determines when price has turned significantly enough and aggressively enough to constitute a relevant pivot, resulting in high accuracy while ruling out subjective decision making completely. Users can adjust length of market structure basis and sensitivity of volatility adjustment to achieve desired magnitude of pivots, reflected on the average swing metrics. Note that structure pivots are backpainted. Typical confirmation time for a pivot is within 2-3 bars after peak in price.

Market structure shifts

Generally speaking, traders consider market structure to have shifted when most recent structure high/low gets taken out, flipping underlying bias from one side over to the other (e.g. from bullish structure favoring upside to bearish structure favoring downside). However, there are many ways to approach the concept and the most popular method might not always be the best one. Users can determine their own market structure shift rules by choosing source (close, high, low, ohlc4 etc.) for determining structure shift. Users can also choose additional rules for structure shift, such as two consecutive closes above/below pivot to qualify as a valid shift.

Liquidity sweeps

Users can set maximum amount of bars liquidity levels are considered relevant from the moment of confirmed pivot. By default liquidity levels are monitored for 250 bars and then discarded. Level of tolerance can be set to anything between 100 and 1000 bars. For each liquidity sweep, relative volume (volume relative to volume moving average) is stored and added to average calculations for keeping track of typical depth of liquidity found at sweeps.

Deviations

Users can set a maximum amount of bars price has to spend above/below reference level to consider a deviation to be in place. By default set to 6 bars.

Imbalances

Users can set a desired fill point for imbalances using the following options: 100%, 75%, 50%, 25%. Users can also opt for excluding insignificant imbalances to attain better relevance in indications.

- Backtesting

Built-in backtesting is based on metrics that are considered to reasonably quantify expected behaviour of the main concept, market structure. Structure feedback is monitored using two metrics, supportive structure and structure period gain. Rest of the metrics provided are informational in nature, such as average swing and average relative volume traded at liquidity sweeps. Main purpose of the metrics is to form a general barometer for monitoring whether or not the concepts can be viewed as valid evidence. When the concepts are clearly not working optimally, one should adjust expectations accordingly or take action to improve performance. To make any valid conclusions of performance, sample size should also be significant enough to eliminate randomness effectively. If sample size on any individual chart is insufficient, one should view feedback scores on multiple correlating and comparable charts to make up for the loss.

For more elaborate backtesting, price based concepts can be used in any other script that has a source input, including fully mechanic strategies utilizing Tradingview's native backtester. Each concept and their indications (e.g. higher low on a bearish structure, lower high on a bullish structure, market structure shift up, imbalance filled etc.) can be utilized separately and used as a component in a backtesting script of your choice.

Structure feedback

Structure feedback is monitored using two metrics, likelihood of supportive price movement following a market structure shift and average structure period gain. If either of the two employed tests indicate failed reactions beyond a tolerable level, one should take action to improve feedback by adjusting the settings. If feedback metrics after adjusting the settings are still insufficient, the concepts are working suboptimally for the given chart and cannot be regarded as valid technical evidence as they are.

Metric #1 : Supportive structure

Each structure pivot is benchmarked against its respective structure shift level. Feedback is considered successful if structure pivot takes place above market structure shift level (in the case of bullish structure) or below market structure shift level (in the case of bearish structure). Structure feedback constitutes as one test indicating how often a market structure state results in price movement that can be considered supportive.

Metric #2 : Structure period gain

Each structure period is expected to present favorable appreciation, measured from one market structure shift level to another. E.g. bullish structure period gain is measured from market structure shift up level to market structure shift down level that ends the bullish structure period. Bearish structure is measured in a vice versa manner, from market structure shift down level to market structure shift up level that ends the bearish structure period. Feedback is considered successful if average structure period gain is supportive for a given structure (positive for bullish structure, negative for bearish structure).

Additional metrics

On top of structure feedback metrics, percentage gain for each swing (distance between a pivot to previous pivot) is recorded and stored to average calculations. Average swing calculations shed light on typical pivot magnitude for better understanding changes made in market structure settings. Average relative volume traded at liquidity sweep on the other hand gives a clue of depth of liquidity typically found on a sweeps.

Feedback scores

When market structure (basis for most concepts) is working optimally, quality threshold for both feedback metrics are met. By default, threshold for supportive structure is set to 66%, indicating valid feedback on 2/3 of backtesting periods on average. On top, average structure period gain needs to be positive (for bullish structures) and negative (for bearish structure) to qualify as valid feedback. When both tests are passed, a tick indicating valid feedback will appear next to feedback scores, otherwise an exclamation mark indicating suboptimal performance on either or both. If both or either test fail, market structure parameters need to be optimized for better performance or one needs to adjust expectations accordingly.

Verifying backtest calculations

Backtest metrics can be toggled on via input menu, separately for bullish and bearish structure. When toggled on, both cumulative and average counters used in backtesting will appear on "Data Window" tab. Calculation states are shown at a point in time where cursor is hovered. E.g. when hovering cursor on 4th of January 2021, backtest calculations as they were during this date will be shown.

- Alerts

Available alerts are the following.

- HH/HL/LH/LL/EQL/EQH on a bullish/bearish structure

- Bullish/bearish market structure shift

- Bullish/bearish imbalance created

- Bullish/bearish imbalance filled

- Bullish/bearish liquidity sweep

- Bullish/bearish deviation

- Visuals

Each concept can be enabled/disabled separately for creating a selection indications that one deems relevant for their purposes. On top, each concept has a stealth visual option for more discreet visuals.

Unfilled imbalances and untapped liquidity levels can be extended forward to better gauge key areas of interest.

Liquidity sweeps have an intensity option, using color and width to visualize volume traded at sweep.

Market structure states and market structure shifts can be visualized as chart color.

Metric table can be offsetted horizontally or vertically from any four corners of the chart, allowing space for tables from other scripts.

Table sizes, label sizes and colors are fully customizable via input menu.

- Practical guide

The basic idea behind market structure is that a side (bulls or bears) have shown significant weakness on a failed attempt to defend a key level (most recent pivot high/low). In the same way, a side has shown significant strength on a successful attempt to break through a key level. This successful break through a key level often leads to sustained lengthier movement for the side that provably has the upper hand, making it an ideal tool for establishing directional bias.

Multi-timeframe view of market structure provides crucial guidance for analyzing market structure states on any individual timeframe. If higher timeframe market structure is bullish, it doesn't make sense to expect contradicting lower timeframe market structure to provide significant adverse movement, but rather a normal correction within a long term trend. In the same way, if lower timeframe market structure is in agreement with higher timeframe market structure, one can expect a reliable trending environment to ensue as multiple points of confluence are in place.

Bullish structure can be considered constructive on a series of higher highs and higher lows, indicating strong interest from bulls to sustain an uptrend. Vice versa is true for bearish structure, a series of lower highs and lower lows can be considered constructive. When structure does not indicate strong interest to maintain a supportive trend (lower highs on bullish structure, higher lows on bearish structure), a structure shift and a turn in trend might be nearing.

Market structure shifts are of great interest for breakout traders who position for continuation. Structure shifts can indeed be fertile ground for executing a breakout trade, but breakouts can easily turn into fakeouts that leave participants in an awkward position. When price moves further away from the underwater participants, potential for snowball effect of covering positions and driving price further away is elevated.

Liquidity sweeps as a concept is based on the premise that pivoting price is evidence of meaningful depth of liquidity found at/around pivot. If liquidity existed at a pivot once, it is likely to exist there in the future as well. When price grinds against liquidity, it is on a path of resistance rather than path of least resistance. Pivots are also attractive placements for traders to set stop-losses, which act as fuel for price to move to the opposite direction when swept and triggered.

Behind tightly formed pivots are potentially many stop-loss orders lulled in the comfort of having many layers of levels protecting their position. Compression that leaves such clusters of unswept liquidity rarely goes unvisited.

As markets strive for efficient and proper transacting most of the time, imbalances serve as points in price where price is naturally attracted to. However, imbalances too are contextual and sometimes one sided trading is rewarded with follow through, rather than with a fill. Identifying market regimes give further clue into what to expect from imbalances. In a ranging environment, one can expect imbalances to fill relatively quick, making them ideal targets for entries and exits.

On a strongly trending environment on the other hand imbalances tend to stick for a much longer time. In such environments continuation can be expected with no fills or only partial fills. Signs of demand preventing fill attempts serve as additional clues for imminent continuation.

Deviation

Monday_Weekly_Range/ErkOzi/Deviation Level/V1"Hello, first of all, I believe that the most important levels to look at are the weekly Fibonacci levels. I have planned an indicator that automatically calculates this. It models a range based on the weekly opening, high, and low prices, which is well-detailed and clear in my scans. I hope it will be beneficial for everyone.

***The logic of the Monday_Weekly_Range indicator is to analyze the weekly price movement based on the trading range formed on Mondays. Here are the detailed logic, calculation, strategy, and components of the indicator:

***Calculation of Monday Range:

The indicator calculates the highest (mondayHigh) and lowest (mondayLow) price levels formed on Mondays.

If the current bar corresponds to Monday, the values of the Monday range are updated. Otherwise, the values are assigned as "na" (undefined).

***Calculation of Monday Range Midpoint:

The midpoint of the Monday range (mondayMidRange) is calculated using the highest and lowest price levels of the Monday range.

***Fibonacci Levels:

// Calculate Fibonacci levels

fib272 = nextMondayHigh + 0.272 * (nextMondayHigh - nextMondayLow)

fib414 = nextMondayHigh + 0.414 * (nextMondayHigh - nextMondayLow)

fib500 = nextMondayHigh + 0.5 * (nextMondayHigh - nextMondayLow)

fib618 = nextMondayHigh + 0.618 * (nextMondayHigh - nextMondayLow)

fibNegative272 = nextMondayLow - 0.272 * (nextMondayHigh - nextMondayLow)

fibNegative414 = nextMondayLow - 0.414 * (nextMondayHigh - nextMondayLow)

fibNegative500 = nextMondayLow - 0.5 * (nextMondayHigh - nextMondayLow)

fibNegative618 = nextMondayLow - 0.618 * (nextMondayHigh - nextMondayLow)

fibNegative1 = nextMondayLow - 1 * (nextMondayHigh - nextMondayLow)

fib2 = nextMondayHigh + 1 * (nextMondayHigh - nextMondayLow)

***Fibonacci levels are calculated using the highest and lowest price levels of the Monday range.

Common Fibonacci ratios such as 0.272, 0.414, 0.50, and 0.618 represent deviation levels of the Monday range.

Additionally, the levels are completed with -1 and +1 to determine at which level the price is within the weekly swing.

***Visualization on the Chart:

The Monday range, midpoint, Fibonacci levels, and other components are displayed on the chart using appropriate shapes and colors.

The indicator provides a visual representation of the Monday range and Fibonacci levels using lines, circles, and other graphical elements.

***Strategy and Usage:

The Monday range represents the starting point of the weekly price movement. This range plays an important role in determining weekly support and resistance levels.

Fibonacci levels are used to identify potential reaction zones and trend reversals. These levels indicate where the price may encounter support or resistance.

You can use the indicator in conjunction with other technical analysis tools and indicators to conduct a more comprehensive analysis. For example, combining it with trendlines, moving averages, or oscillators can enhance the accuracy.

When making investment decisions, it is important to combine the information provided by the indicator with other analysis methods and use risk management strategies.

Thank you in advance for your likes, follows, and comments. If you have any questions, feel free to ask."

Anchored Three Sigma RangeThis indicator serves to display the standard deviation model based on open price from the selected anchored timeframe. Per statistics the price may stay within the three sigma range most of the time, most significantly within first sigma range 68% of the time.

If price breaks the statistical probabilities and out of the three sigma range entirely it could be considered anomalous and perhaps useful for trade planning, use the fib extensions in various ways to have dynamic profit targets, support or resistance.

How is this different

This indicator differs from others in that I've not really seen any others generating solely horizontal levels, anchored from open price and including fib extensions.

How to use

To use this indicator add to the chart, select anchor timeframe, fib display mode and adjust style to liking. Depending on trade plans use the range breaks, consolidations or fib extensions as required.

One could utilize range consolidation for advanced options neutral trades, range breaks for scalping directionally or high fib extensions for rejection based trades. Based on timeframe anchorage there could be some really amazing combinations for any style of trading, comment any unique findings!

What markets

This indicator can be used on anything that has a price :D

Conditions

Any condition is applicable.

Average Variation Bands OscillatorSimilar to how a donchian% of channel helps to visualize trend and volatility, this tool helps identify those same characteristics, if the oscillator is generally above the 50 mark, it is considered to be trending upwards, and the reverse if it is generally bellow 50.

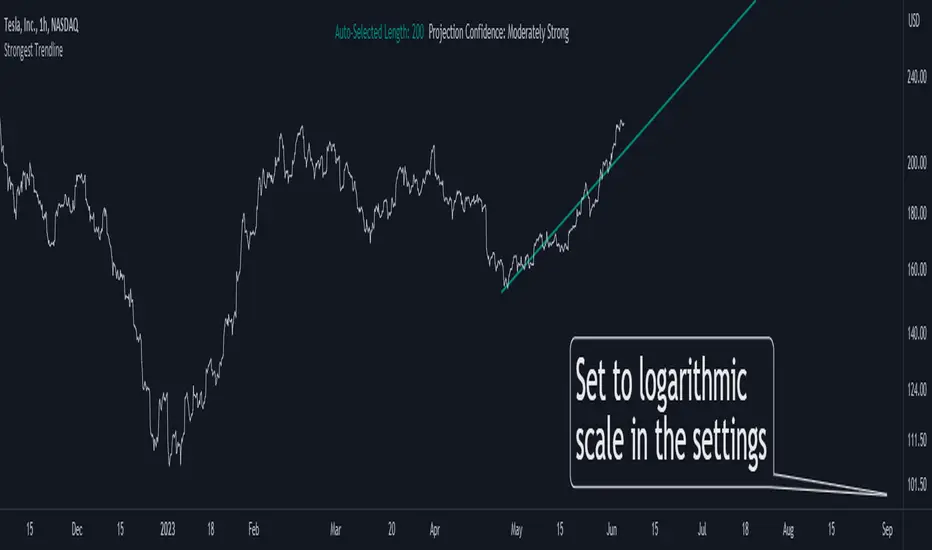

Strongest TrendlineUnleashing the Power of Trendlines with the "Strongest Trendline" Indicator.

Trendlines are an invaluable tool in technical analysis, providing traders with insights into price movements and market trends. The "Strongest Trendline" indicator offers a powerful approach to identifying robust trendlines based on various parameters and technical analysis metrics.

When using the "Strongest Trendline" indicator, it is recommended to utilize a logarithmic scale . This scale accurately represents percentage changes in price, allowing for a more comprehensive visualization of trends. Logarithmic scales highlight the proportional relationship between prices, ensuring that both large and small price movements are given due consideration.

One of the notable advantages of logarithmic scales is their ability to balance price movements on a chart. This prevents larger price changes from dominating the visual representation, providing a more balanced perspective on the overall trend. Logarithmic scales are particularly useful when analyzing assets with significant price fluctuations.

In some cases, traders may need to scroll back on the chart to view the trendlines generated by the "Strongest Trendline" indicator. By scrolling back, traders ensure they have a sufficient historical context to accurately assess the strength and reliability of the trendline. This comprehensive analysis allows for the identification of trendline patterns and correlations between historical price movements and current market conditions.

The "Strongest Trendline" indicator calculates trendlines based on historical data, requiring an adequate number of data points to identify the strongest trend. By scrolling back and considering historical patterns, traders can make more informed trading decisions and identify potential entry or exit points.

When using the "Strongest Trendline" indicator, a higher Pearson's R value signifies a stronger trendline. The closer the Pearson's R value is to 1, the more reliable and robust the trendline is considered to be.

In conclusion, the "Strongest Trendline" indicator offers traders a robust method for identifying trendlines with significant predictive power. By utilizing a logarithmic scale and considering historical data, traders can unleash the full potential of this indicator and gain valuable insights into price trends. Trendlines, when used in conjunction with other technical analysis tools, can help traders make more informed decisions in the dynamic world of financial markets.

Volume+This volume indicator uses a long WMA to establish an average volume and calculates the standard deviation based on that average. Each deviation level from 1 to 3 is also plotted with the bar color gradually increasing in intensity when more than one standard deviation is exceeded.

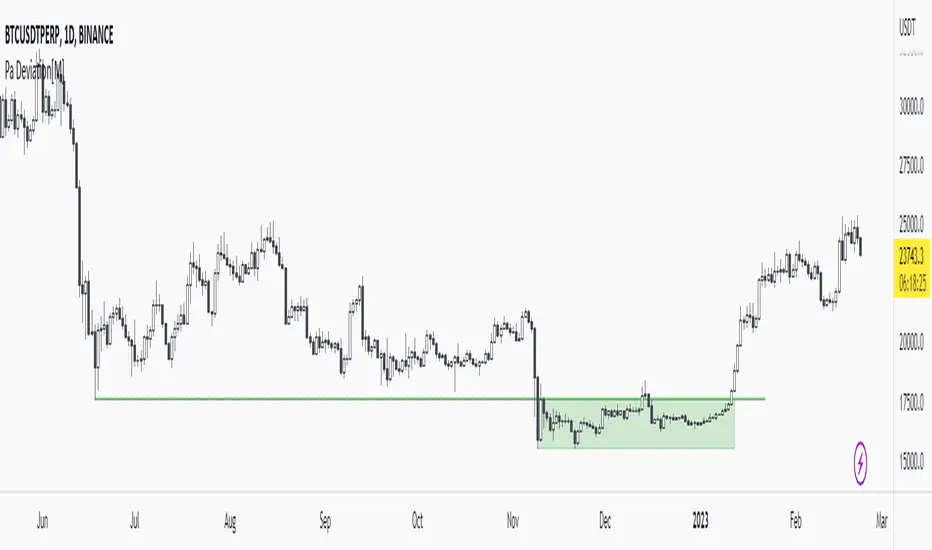

Pa Deviation[M]Hello everyone,

First of all, what is deviation?

It can be said that the price goes down (or goes out) under the past pivot zone and enters the range again after lingering for a while. (I think so)

I think there is a sign of trend reversal as it hunts the stops below (or above) the pivot zone as well. (RektProof also has a strategy for this.)

In this indicator, I determined the deviation limits with the atr of the pivot regions. For example, the deviation area (pivot zone - atr) must be greater than. It should also make a grand entrance into the range.

Let me tell you a little about the settings:

Pivot Length: It is the value entered for determining the pivot regions. For example, if the pivot length is 5, the low must be less than the past 5 lows and the next 5 lows.

Minimum Bar: The value that determines the minimum bar of the deviation area. For example, if the minimum bar is 4, the indicator will show deviation areas consisting of minimum 4 bars.

Example Deviation:

1.Pivots and Pivot Lines

As you can see in the image, there are many pivot points. Let's take the lowest pivot point and draw an imaginary line. This is our pivot line

2.Deviation

As you can see, an accumulation has occurred under our pivot line. If the price goes above our pivot line again, it will be a deviation.

3.Return to Range

Voila! Price accumulated below the pivot line and splendidly rose above the pivot line. This is the deviation area for us now.

Other Examples:

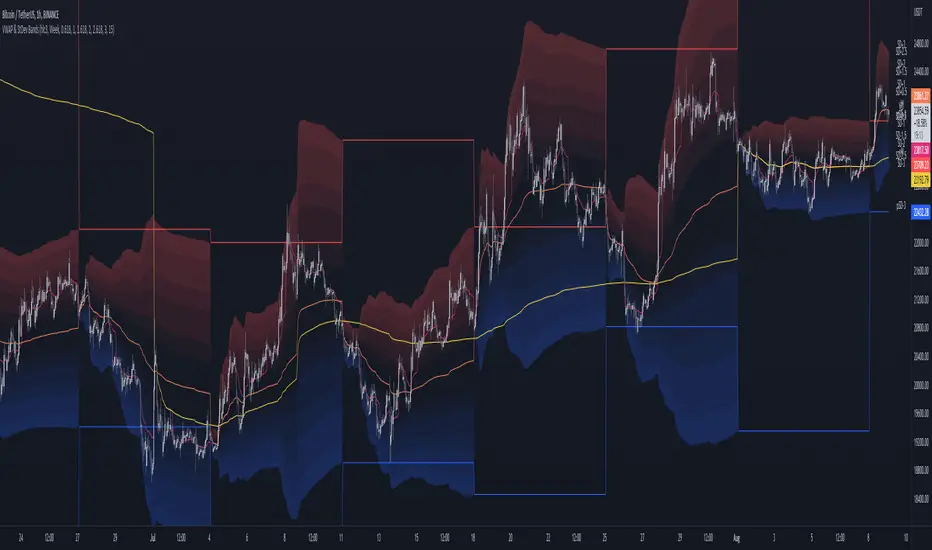

MTF VWAP & StDev BandsMulti Timeframe Volume Weighted Average Price with Standard Deviation Bands

I used the script "Koalafied VWAP D/W/M/Q/Y" by Koalafied_3 and made some changes, such as adding more standard deviation bands.

The script can display the daily, weekly, monthly, quarterly and yearly VWAP.

Standard deviation bands values can be changed (default values are 0.618, 1, 1.618, 2, 2.618, 3).

Also the previous standard deviation bands can be displayed.

[Sidders]Std. Deviation from Mean/MA (Z-score)This indicator visualizes in a straight forward way the distance price is away from the mean in absolute standard deviations (Z-score) over a certain lookback period (can be configured). Additionally I've included a moving average of the distance, the MA type can be configured in the settings.

Personally using this indicator for some of my algo mean reversion strategies. Price reaching the extreme treshold (can be configured in settings, standard is 3) could be seen as a point where price will revert to the mean.

I've included alerts for when price crosses into extreme areas, as well as alerts for when crosses back into 'normal' territory again. Both are also plotted on the indicator through background coloring/shapes.

Since I've learned so much from other developers I've decided to open source the code. Let me know if you have any ideas on how to improve, I'll see if I can implement them.

Enjoy!

Sequence Distribution Reporta basic tool to retrieve statistics of the distribution of price range sequences.

DMT TEMPELTON PECK STRATEGYIntroduction Templeton Peck Strategy Version .

Bring your A-game to the market in A-Team style with DMT Templeton Peck – you’ll love it when this plan comes together!

Using customized standard deviations between historic price action ranges and volume metrics, DMT Templeton Peck enables traders to never miss a change in trend.

In its default state, the DMT Templeton Peck Strategy displays key information, such as:

• Small trend line

• Large trend line

• Position entry prices

• Take profit levels

• Stop levels

• Buy and sell trend signals

In addition to providing core functionality for the indicator’s strategy signals, traders can use this data to enter or exit trades.

When price crosses both trend lines and consolidates there is a high probability that price will continue to move in the same direction. The most profitable results are achieved when trading in the direction of the current large time frame trend.

When small and large trend lines cross a trading signal is generated which can be used to automate trades. Please see the ‘TradingView Alerts’ section of this document for further details.

The Small & Large trend line’s display can be toggled, and their colors modified in the indicator’s style options as shown below.

Basic Strategy

In its simplest form, the strategy is to buy when the price crosses and consolidates above both trend lines and sell when the price crosses and consolidates below both trend lines.

Set amount of first entry to the inputs data.

You can add a commission fee.

Adjust initial capital for your needs.

How to Trade

Confident traders may choose to enter a long position at the point

#1 when the price passes above both trend lines and begins to consolidate.

However, the safer trade is to wait for the trend lines to cross at a point

#2 and then look for an entry in the direction of the local trend.

One price action begins to reverse to the downside the strategy reverses. Confident traders may choose to enter point

#3 when the price passes both trend lines and begins to consolidate once again under the previous price action structure that is now acting as resistance.

A sell signal is generated at the point

#4 which produced a small profit; however, a new short position could have been opened when the price retraced to resistance at a point

#5 and experienced a repeated number of strong rejections.

Do not worry if you miss a trade as there is often more than a single opportunity to enter – like at position #5 when price action retests the previous local price structure as resistance.

The indicator can be used on smaller time frames to scalp or find an entry after a larger time frame has signaled, however smaller time frames will also be “choppy” and should only be traded with a paper-tested strategy.

Traders should take profit on positions at resistance & support levels and look to have fully exited the trade by the time the price crosses back over both trend lines and/or loses a previously established price level.

Indicator Tuning

In its default state, the indicator is tuned for swing trades using 30 minute & 1 hour time frames, however, you are encouraged to experiment with the indicator options.

The input also allows you to set separately longs and shorts for a better view of the trend and to avoid hunts.

Large & Small Length options define how many historic candles are used for the calculation of the relevant trend line.

As a rule of thumb, larger time frames would use smaller values and smaller time frames would use larger values, ie. On a daily chart, a large and small length could be defined as 400 and 100 respectively.

Please be aware that there are limits to the amount of historical data for any intraday level based on your TradingView subscription level:

• Basic – 5000 bars/candles

• Pro & Pro+ - 10000 bars/candles

• Premium – 20000 bars/cables

TradingView Backtest

By utilizing TradingView backtest you can set a specific date for your analysis.

TrendTracers Bitcoin Stock to Flow ModelFor the best results, make sure to view this indicator on a bitcoin chart with a very long history (e.g. BNC:BLX)!

This model treats Bitcoin as being comparable to commodities such as gold, silver or platinum. These are known as ‘store of value’ commodities because they retain value over long time frames due to their relative scarcity. It is difficult to significantly increase their supply i.e. the process of searching for gold and then mining it is expensive and takes time. Bitcoin is similar because it is also scarce. In fact, it is the first-ever scarce digital object to exist. There are a limited number of coins in existence and it will take a lot of electricity and computing effort to mine the remaining coins still to be mined, therefore the supply rate is consistently low.

The stock-to-flow model predicts value changes in a straightforward manner. It compares an asset’s current stock to the rate of new production, or how much is produced in a year.

Calculation:

Take bitcoin production in a period, divide it by that period and then multiply by 365 to get the estimated yearly production and then calculate the stock to flow.

yearlyFlow = ((stockChange) / period ) * 365

stockToFlow = (stock - missingBitcoins) / yearlyFlow

Model Value = -1.84ᵉ * stockToFlow³.³⁶ (mathematical model to calculate the model price)

For more information about the calculations followed: stats.buybitcoinworldwide.com

Features:

Works on the Daily, Weekly and Monthly Timeframe.

Allows you to adjust between a 10-day period and a 463-day period.

Has the option to account for missing bitcoins, lets you adjust the amount of missing bitcoins.

The ability to toggle a standard deviation of the Model Value with a multiplier of 1, 2 or 3

Displays a Stock to Flow Deviation Ratio: If the Deviation Ratio is close to 0 it means the price of Bitcoin is close to the Model Value Line(or Stock to Flow Ratio). If the Deviation Ratio is close to 1 or -1, it means the price of bitcoin is near the selected deviation levels.

You can toggle between the Overlay version and the Oscillator version, default is on Oscillator version. If you want to switch: Untick Oscillator mode in the indicator settings, click on the three dots and select "move to existing pane above". Then click on the three dots again and select Pin to scale A. Done!

As a bonus: Now you can toggle a "1-year Realized Price" graph, while it's not officially part of the Stock to Flow Model it does share similar technicals about supply and scarcity. The 1-year Realized Price is the realized market cap divided by total amount of generated coins.

I just noticed that, while the color gradient function is pretty cool, it does not allow for end users to customize their colors after applying this indicator to their chart. Sorry!

Loft Strategy V4This strategy is an advanced version of the Loft Strategy V1, I shared earlier. (Loft Strategy V1 consists of a kalman filter (by alexgrover ) and a "stop and reverse" line which is following and the kalman filter. If the price goes in the same direction as the position side, the "stop and reverse" line approaches the kalman filter as set on the "Approach Decrease Step" parameter.)

In addition to the previous version, it includes a martingale like deviation and multiple take-profit.

Here it is some parameters definitions of the strategy:

Kalman Filter: The higher this parameter, the faster and more aggressive the filter. Otherwise the filter goes very smoothly

Beginning Approach: First approximation as a percentage of stop-n-reverse line

Final Approach: Minimum approximation of stop-n-reverse line

Approach Decrease Step: If the price moves in the same direction as the strategy, the approach percentage is reduced by this parameter. Otherwise nothing do

Base Order Quantity: Initial capital of position

Max Safe Order Attempt: This parameter determines the maximum number of times the strategy will raise the bet after losing in a row.

Safe Order Deviation: if the last trade is loss, multiply the bet by this parameter (aka. martingale factor)

Profit Deviation: if last trade in loss, multiply the take-profit points

Max Order Quantity: Maximum capital allowed for a position

TP1, TP2, TP3 : Take profit spots in percentage

QT1, QT2, QT3: Amount of take-profit spots

Stop Loss: Maximum stop loss allowed for a trade

Long Entry, Short Entry: Only long side, only short side or both side

Safe Stop After TP2: If the price reaches the TP2 point, move the stop-loss point to the entry price.

Safe Stop After TP1: If the price reaches TP1, move the stop-loss point to the stop-n-reverse line.

Weighted Standard Deviation BandsLinearly weighted standard deviations over linearly weighted mean.

The rationale of the study can be deduced from my latest publications where I go deeper into explaining the benefits of linear weighting, but in short, I can remind that by using linear weighting we are able to increase the information gain by communicating the sequential nature of time series to the calculations via linear weighting.

Note, that multiplier parameters can take both negative and positive values resulting in ability to have, for example, 1st and 6th weighted standard deviations higher than the weighted mean.

Despite the modification of the classic standard deviation formula, I assume that mathematical qualities of standard deviation will hold due to the fact we can alternately weight the window itself, and then apply the classic standard deviation over the weighted window. In both cases, the results will be the same.

Aight that was too formal, but your short strangles should be happy

Here is it, for you

Anchored TWAP with StDev Bands [MrShadow]TWAP with:

- Anchoring: Custom, Day, Week, Month, Quarter, Year (custom anchoring can be selected by dragging a vertical line through the chart)

- Standard Devation Bands

- Auto-coloring depending on the trend

Ergodic Mean Deviation Indicator [CC]The Ergodic Mean Deviation Indicator was created by William Blau and this is a hidden gem that takes the difference between the current price and it's exponential moving average and then double smooths the result to create this indicator. This double smoothing of course creates a lag that allows it to give off a sustained buy signal during a bullish trend and vice versa. This is a very fun indicator to experiment with and surprised that no one on here gives William Blau much attention so I will go ahead and publish the rest of his scripts eventually. I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

[UPRIGHT Trading] Top & Bottom Finder [Premium]Hello Traders,

Today I'm releasing an updated version of my previous Top & Bottom Finder (M.Right_Top & Bottom Finder 1.0).

The timing of this release couldn't be more perfect with everyone trying to 'find the bottom'. And the increased volatility that we've been seeing as of late.

Essentially, my indicator uses volatility and standard deviations among other things to assist you in finding the top or bottom of trends. You may also notice that it uses a lot of different strength indicators to provide an additional layer of complexity and confirmation.

Not just an RSI, but an RSI ema, smoothed OBV RSI's, and other volume RSI's. This is a truly unique and powerful tool for any Trader - whether you've just started or you've been trading for 20 years, I'm confident you will find value in the UPRIGHT Trading Top & Bottom Finder.

How to use it:

When it detects the trend Bottoming or Topping the histogram will change color. Bottom - Green/blue, Top - Red, (different shades of colors for different types of detection).

I've spent several hours tweaking the calculations and filters to enhance the accuracy, so this will be a noticeable upgrade from my original Top & Bottom Finder.

The length of the histogram bar can be an indication in itself, especially when it lines up close to one of the plotted lines and has noticeable direction change following this.

I've added a lot of text and pictures to help display it's capabilities, features, and customizability.

As always, it's fully customizable with alerts. Can toggle any thing on or off, and change the colors to suit your style.

3 Unique RSI's, different colors on the histogram will show different levels of detection. Some are more accurate in some timeframes than others. Bright Green and Bright Red are the most different from the rest.

I've jam-packed this indicator with Buy/Sell and Confirmation Signals and even background highlights (with colors that can mesh together). Feel free to find what works best for you.

RSI color indications and background highlights aid in confirmation. Also, as mentioned previously, sometimes a gray bar will land on a Fib and it will be a bottom signal.

The above chart should look like this

Good luck Traders,

Cheers,

Mike

(UPRIGHT Trading)

Time-of-Day DeviationCreates a 'Time-of-Day' Deviation cone starting from the first bar of the session based upon data from previous days.

DailyDeviationLibrary "DailyDeviation"

Helps in determining the relative deviation from the open of the day compared to the high or low values.

hlcDeltaArrays(daysPrior, maxDeviation, spec, res) Retuns a set of arrays representing the daily deviation of price for a given number of days.

Parameters:

daysPrior : Number of days back to get the close from.

maxDeviation : Maximum deviation before a value is considered an outlier. A value of 0 will not filter results.

spec : session.regular (default), session.extended or other time spec.

res : The resolution (default = '1440').

Returns: Where OH = Open vs High, OL = Open vs Low, and OC = Open vs Close

fromOpen(daysPrior, maxDeviation, comparison, spec, res) Retuns a value representing the deviation from the open (to the high or low) of the current day given number of days to measure from.

Parameters:

daysPrior : Number of days back to get the close from.

maxDeviation : Maximum deviation before a value is considered an outlier. A value of 0 will not filter results.

comparison : The value use in comparison to the current open for the day.

spec : session.regular (default), session.extended or other time spec.

res : The resolution (default = '1440').

[cache_that_pass] 1m 15m Function - Weighted Standard DeviationTradingview Community,

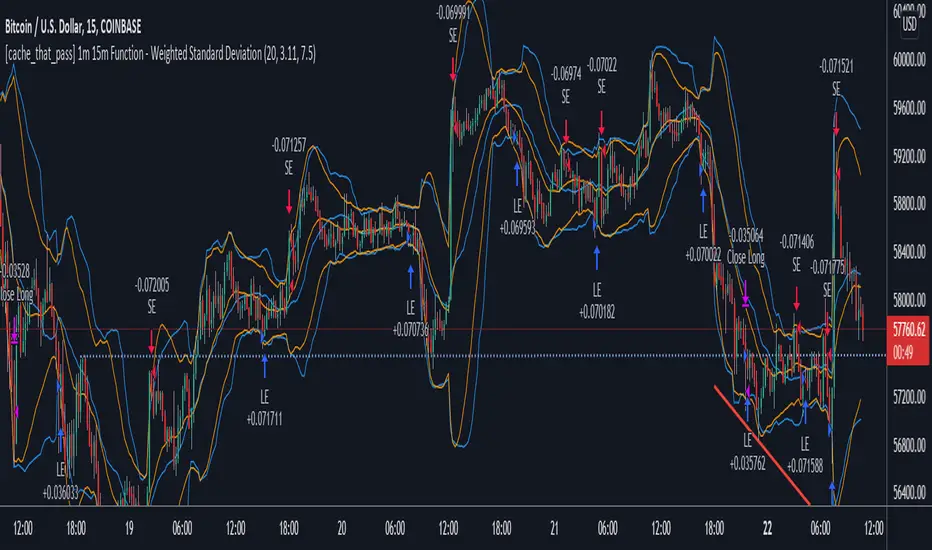

As I progress through my journey, I have come to the realization that it is time to give back. This script isn't a life changer, but it has the building blocks for a motivated individual to optimize the parameters and have a production script ready to go.

Credit for the indicator is due to @rumpypumpydumpy

I adapted this indicator to a strategy for crypto markets. 15 minute time frame has worked best for me.

It is a standard deviation script that has 3 important user configured parameters. These 3 things are what the end user should tweak for optimum returns. They are....

1) Lookback Length - I have had luck with it set to 20, but any value from 1-1000 it will accept.

2) stopPer - Stop Loss percentage of each trade

3) takePer - Take Profit percentage of each trade

2 and 3 above are where you will see significant changes in returns by altering them and trying different percentages. An experienced pinescript programmer can take this and build on it even more. If you do, I ask that you please share the script with the community in an open-source fashion.

It also already accounts for the commission percentage of 0.075% that Binance.US uses for people who pay fees with BNB.

How it works...

It calculates a weighted standard deviation of the price for the lookback period set (so 20 candles is default). It recalculates each time a new candle is printed. It trades when price lows crossunder the bottom of that deviation channel, and sells when price highs crossover the top of that deviation channel. It works best in mid to long term sideways channels / Wyckoff accumulation periods.

Ehlers Deviation Scaled Super Smoother [CC]The Deviation Scaled Super Smoother was created by John Ehlers and this is an excellent moving average that changes direction very quickly and can keep up with the current underlying trend. This indicator works by applying a Hann Windowed Moving Average to the stock's momentum and scaling that by the Root Mean Square and then using that value in the input for a Super Smoother . I have included strong buy and sell signals in addition to normal ones so lighter colors are normal signals and darker colors are strong ones. Buy when the line turns green and sell when it turns red.

Let me know if there are any other scripts you would like to see me publish!

WhaleCrew Crypto ArbitrageVisualizes the price difference (deviation) off BTC/ETH across multiple exchanges (Spot and/or Perpetuals)

Spot prices are represented by circles, while perpetual prices are shown as crosses.

Spot:

Binance

FTX

Bitfinex

Coinbase

Perpetuals:

Binance

FTX

Bybit

BitMEX

Volume TrendsThis script provides clear volume trends on any time frame. You set a long term volume trend moving average (ex 100 periods). A shorter term MA of your choice (10 in this example) will oscillate above and below based on the standard deviations of its current value relative to the long term #.

Similarly, large volume bars are plotted in terms of st dev above the long term MA.

Very useful in spotting capitulation bottoms and/or blow-off tops.