M.Right_Top & Bottom Finder 1.0Thank you @Lazybear for the calculations for squeeze and BB, and all of the other great pine-coders who inspired me to create my own indicator to share!

This is the result of hours of work learning to code pine and tweaking until everything fits exactly what I was looking for.

After using it for a while and seeing the benefits personally, I figured now might be a good time to share with everyone while we are in such great market volatility, maybe I can save you some losses.

Basically, my indicator is meant to use volatility and standard deviations to show you the top and bottom of trends.

It does indeed work on lower timeframes, I typically use it on 5m, 30m, 4hr, and 1d.

What to look for:

When it detects the trend bottoming it will send a green histogram bar down, I also created a different shade green for even more likely bottoms.

When it detects the top of the trend it will send a red bar up, I have a brighter red for more certain tops.

The length of the histogram bar is also an indication as well. Sometimes there will be a reversal while still just showing the gray bar.

I just added alerts, so hopefully those work. If not, I will update.

Let me know if you have any questions, and enjoy.

Cheers!

Deviation

Standard deviation of the exponential moving average

This indicator emphasizes price movements when it moves away from or closer to the chosen moving average, within the envelope of its standard deviation. It serves as a complement to other indicators or can be used within a strategy by itself.

Bias(Deviation Rate)Deviation rate (BIAS), by calculating the distance between the closing price and a moving average to reflect the reversal created by the degree of deviation between the price and the moving average during a certain period of time.

Above the zero axis is called positive deviation and belongs to the bullish zone, while below the zero axis is called negative deviation and belongs to the bearish zone.

Regardless of whether it is a positive deviation or a negative deviation, whenever the gap between the stock price and the moving average becomes larger, it means that the stock price has an overbought/oversold condition, and a high probability will result in a reversal.

Tradingview ToolkitA new trader's biggest barrier to entry is lack of understanding where they are in terms of time and price and with tradingview free they are often limited to just 1 or 2 extra indicators as many new traders slap on RSI and MACD as 2/3 free ones. While these indicators are fine for trend analysis, its important to know where the price is in relation to time. Thus, this all-in-one script is meant to have a lot of customizable utility to save on indicator spots and act as a hotspot for many common needs.

-2 Sets of VWAP line w/ standard deviation bands with customizable timeframes.

-1 more customizable timeframe VWAP line (no std dev bands) to use as a long time frame reference

-Ability to plot previous VWAP close prices over current timeframe on all VWAP lines w/ basic color changing if price closes above/below

-2 Sets of Bollinger Bands with customizable source length and MA type

-3 customizable moving averages with custom timeframe/resolutions

-Inside candle barcolor repainter to easily notice if a candle was inside the range of the previous candle (price contraction)

Not meant to have everything on at once, but simply a place to enable and disable different things and save spots for more important things

HuD DE | TEHuD DE | TE Expert is a combination of two indicators.

1. DE or Deviation Expert

DE is based on ema5 and ema20. This MA algorithm is to filter signals such as trend and convergence/divergence. It is represented by HA Candles.

There are 4 signals to assist traders in making decisions

i. Golden Cross = possible entry point ( Green Triangle )

ii. Death Cross = possible exit point ( Red Triangle )

iii. Cross Up Level 0 = look for Buy opportunity ( Green Diamond )

iv. Cross Down Level 0 = look for Sell opportunity ( Red Diamond )

There are also ema lines to monitor the movement of current candle movement.

2. TE or Trend Expert

TE is based on ema5 movement to assist traders to see the overall trend of chart movement.

The movement is represented by HA Candles.

There are 4 ema's lines to monitor HA Candles movements.

This lines act as support / resistance which can assist traders to see the current trend of the chart.

For example, if line is green ( Uptend) and the next candle drop below the first green ema lines, next line (ema10) acts as support.

If next candle breaks ema10, we can consider making an exit plan. Or for swing traders, they can consider waiting until candle drop below ema50 ( purple line ) before deciding to exit.

Note: This indicator setting only suitable for Bursa Malaysia market.

SKYNET buy/sell 2.0The SKYNET buy/sell 2.0 indicator generates buy and sell signals based on the following conditions:

**Anchor line : This anchor line is calculated based on certain parameters.

The anchor line is calculated in such a way that the stock/instrument moves around this anchor line.

The calculation of the anchor line uses a look back period which is set to 9 by default. The user can go to the indicator settings and change it to suit their trading style.

Note:

1) As the look back period increases, the number of signals generated on the chart decreases.

2) This indicator will only work on charts/stocks/instruments which are actually traded in the market i.e actual contracts of the stock/instrument is traded in the market. Hence, it will not work on indexes.

BUY signal: When the stock/instrument deviates to the upside of the anchor line by a specific margin, the Buy signal is generated.

SELL signal: When the stock/instrument deviates to the downside of the anchor line by a specific margin, the Sell signal is generated.

Disclaimer: This indicator is not 100% accurate and false signals are generated from time to time. Trading in the markets involves huge risks and one should always do his/her own research before making any trading decisions. This indicator is only designed to help you make a trading decision.

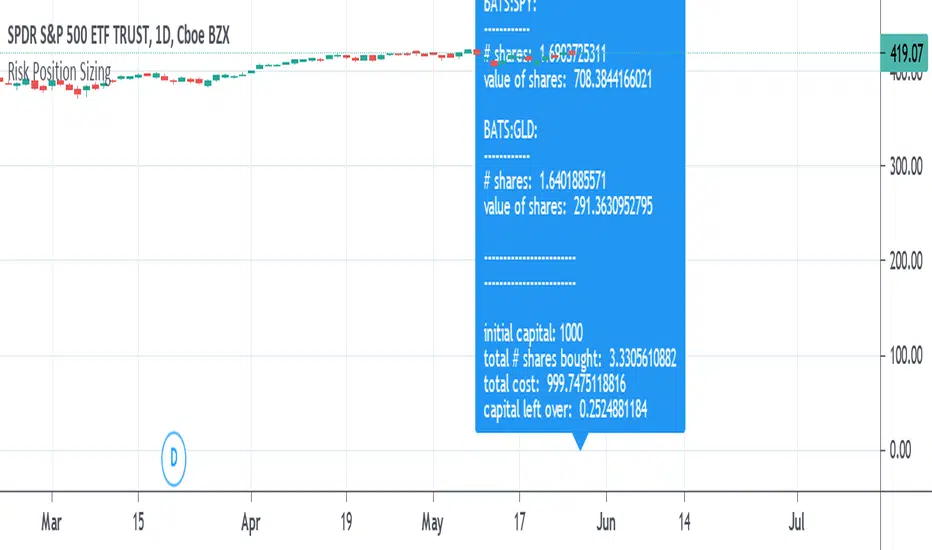

Risk Position Sizing tool using Coefficient of VariationA way to manage portfolio risk using relative standard deviation, also known as coefficient of variation. This tool tells you how much of each stock in shares and in value to buy adjusted for their volatility risk for a given starting account capital. A problem many people have is how to diversify an account and adjusting it for the risk involved in each equity. Many would put in an equal amount of capital value into each share but is it really equal if some equities have more risk than others? A solution is to adjust the portfolio by giving less weight to those that are more volatile or risky. It's done by using a starting percent of the account, preferably a small percent of it, and buying up shares with that same amount for each equity. Each equity will also be divided by the COV to risk adjust the portfolio by giving less weight to the more volatile stocks. This is done until as much of the initial capital in the account as possible is spent.

COV is how far away the price is from the mean or average. The further the price is from the mean the more risk or volatility there is. It uses standard deviation in its calculation. The problem with SD and ATR is that they are not relative to the past or to other equities to compare to. An application where COV can be used is risk portfolio management formulas. This does not take into account correlation or other equation parts in some portfolio management formulas but only the risk or volatility, the default volatility length is mostly arbitrary, and the lower risk stocks may end up being the slowest in performance.

The text label will show how many shares will be bought and how much value each equity will have. At the end it will show the initial capital that was started off with, the total shares bought, the total value of all the shares, and the amount of capital left over. If the sources are not blank then they will be used, to blank them you will need to reset the settings to default otherwise they might still be read. If you want to add more than the given 10 equity spaces to the portfolio then you will need to add in the code manually and add it to the chart. The denominator is perhaps the important part in these types of risk position sizing tools, you can change to other things such as risk-reward ratio instead of volatility or change the volatility type, etc.

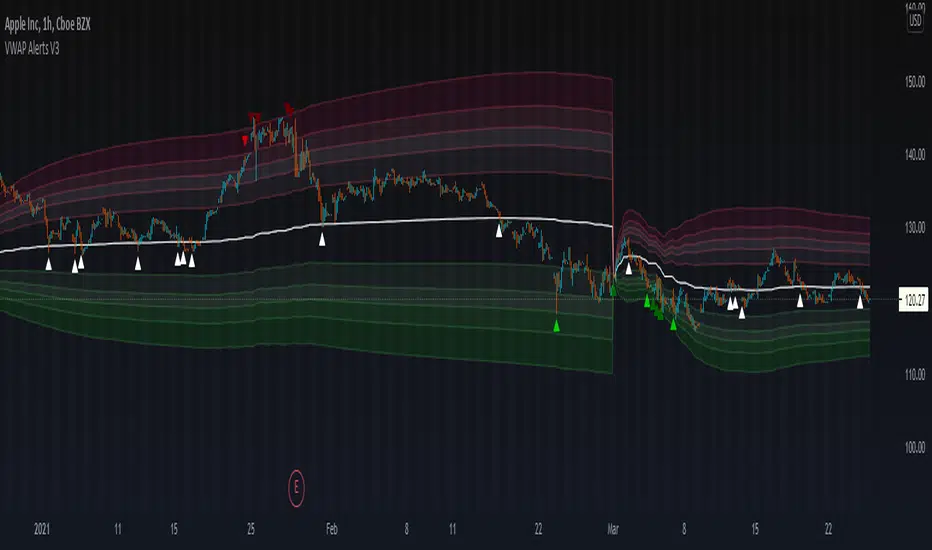

VWAP Alerts V3VWAP Alerts signal over bought/over sold conditions, relative to volume weighted average price, while deviation bands plot an extremely accurate point of mean reversion.

VWAP Alerts V3 includes multiple timeframe selection, along with multiplier input for deviation band setting

Alerts can be set for each individual band, for extreme oversold/overbought conditions, use "Vwap Low Deviation 4" and "Vwap High Deviation 4".

Alerts can also be set for VWAP bounces, by simply setting "VWAP Alert"

VWAP Oscillator CandlesThe VWAP oscillator plots VWAP as the zero line with price, relative to VWAP. This can be use the same way you would traditionally use VWAP, with a much clearer picture of deviation from VWAP. Also, after creating the script, I noticed divergence was extremely noticeable here!

Enhanced Sigma by Cryptorhythms [CR]Enhanced Sigma by Cryptorhythms

Sigma is basically the deviation of returns compared to past returns. The higher / lower the value, shows you how deviated from the average this current bars returns are.

While perhaps not usable as a complete strategy for entering and exiting, its still quite useful and informative. It can give interesting signals as to potential turning points in price action. This behavior extends to all timeframes both long term and short term.

There are 2 overbought and oversold zones here inthe indicator. One is adaptive and will change to suit the shorter term giving your extra potential signals. The fixed line shows a general level for highly deviated values.

Expect a number of further totally unique and exclusive sigma based indicators from CR in the near future. We are nowhere near done extracting the alpha from this concept!

How to get access

This indicator is available for standalone purchase or as part of our subscription options. Please see my signature or profile for more information or contact me directly.

B3 HL2MA Painter ~ Extremely Smooth Average & Bar PaintMy HL2MA is a 'proprietary' formula based on the idea that I never again want to see a jagged average line. I released a version of this a long time ago, but I wanted to update it to how I have it on my charts in other platforms. Here are some notes about this moving average script:

The default input value is 5, and I suggest the range of use 4-6 with the rare occasion of using 3 or 7.

For me 5 is what I use UNLESS I AM IN A TRADE, then I might switch to 4 if I have some profits to lock, or 6 if I want to stay in for a lengthier trade.

This average when kept within the above parameters is the smoothest MA in my arsenal, HL2 refers to the middle of the candles which further de-noises the line.

The colors are green/red for good movement with the confirmed trend.

The colors are gray for movement against the current trend (signaling a possible mean reversion)

The colors blue & yellow appear when signaling possible chop or trend exhaustion.

Carried forward from the last time I posted this, the bias for longs and shorts is depicted as the color of the average line green or maroon, and ALERTS are based on that overall bias created the line by itself.

Also carried from the last post, the green and maroon clouds depict the price deviance from the line; when the cloud stretches wide it may be time to take profits and enter back in closer to the line.

Thanks again for liking and following!!!!

This share is in response to my 10,000th like on TradingView!

Favorite this one, and enjoy :-)

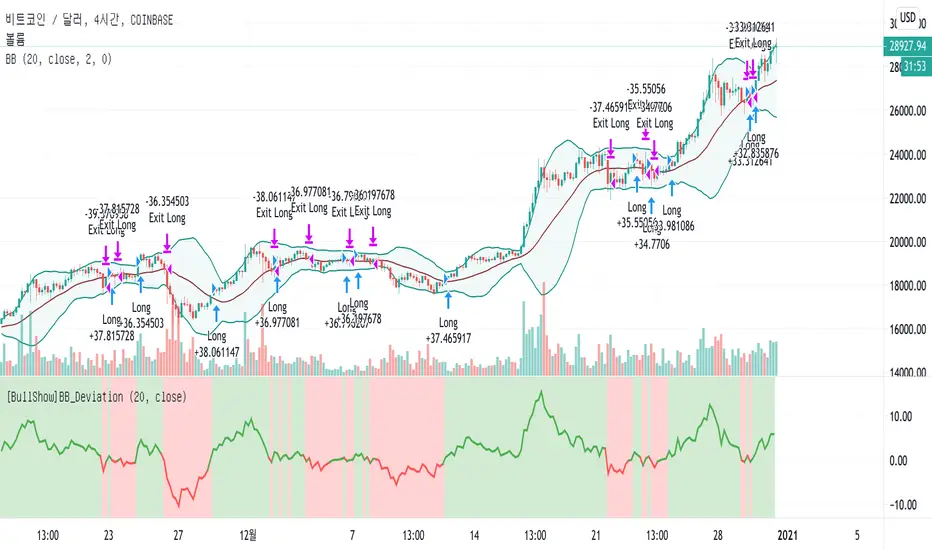

[BullShow]BollingerBands_Deviation StrategyHello Everyone.

Are you enjoying this crazy bull market?

I want to Introduce very classic and simple but powerful strategy.

My strategy is using Bollinger Bands. Yes! It's the indicator that everyone knows and uses.

First of all, let's look at how Wikipedia defines the Bollinger Bands.

Bollinger Bands - Wikipedia

------------

Introduce

Bollinger Bands (/ˈbɒlɪnjdʒər bændz/) are a type of statistical chart characterizing the prices and volatility over time of a financial instrument or commodity, using a formulaic method propounded by John Bollinger in the 1980s.

Purpose

The purpose of Bollinger Bands is to provide a relative definition of high and low prices of a market. By definition, prices are high at the upper band and low at the lower band. This definition can aid in rigorous pattern recognition and is useful in comparing price action to the action of indicators to arrive at systematic trading decisions.

Interpretation

The use of Bollinger Bands varies widely among traders. Some traders buy when price touches the lower Bollinger Band and exit when price touches the moving average in the center of the bands. Other traders buy when price breaks above the upper Bollinger Band or sell when price falls below the lower Bollinger Band. Moreover, the use of Bollinger Bands is not confined to stock traders; options traders, most notably implied volatility traders, often sell options when Bollinger Bands are historically far apart or buy options when the Bollinger Bands are historically close together, in both instances, expecting volatility to revert towards the average historical volatility level for the stock.

------------

However, the use of the Bollinger Bands described on the website is only very abstract without precise guidelines.

So, by calculating the deviation of the 20-days moving average line, the center line of the Bollinger Bands, I chose a strategy to buy when the deviation starts to widen and sell when the separation starts to narrow again.

As a result, I found a strategy that would give you a decent return.

Due to the nature of the strategy, trades in the box zone are frequent, so the win rate is small, but when the price trend is confirmed, you can get a big profit.

Therefore, you can expect good returns from pair with a clear trend rather than pair that trade frequently in the box zone.

If you are interested in my strategy, Use the link below to obtain access to this indicator or PM me to obtain access

Thank you for your supporting.

안녕하세요 여러분.

이 미친 강세장을 즐기고 있습니까?

매우 고전적이고 단순하지만 강력한 전략을 소개하고 싶습니다.

제 전략은 볼린저 밴드를 사용하는 것입니다. 예! 모두가 알고 사용하는 그 지표입니다.

그러나 웹에서 설명하는 사용 방법은 정확한 지침없이 매우 추상적 일 뿐입니다.

따라서 저는 볼린저 밴드의 중심선 인 20 일 이동 평균선의 편차를 계산하여 편차가 확대되기 시작하면 매수하고 편차가 다시 좁아지기 시작하면 매도하는 전략을 선택했습니다.

결과적으로, 나는 당신에게 적절한 수익을 줄 전략을 찾았습니다.

전략의 특성상 박스 존에서의 거래가 빈번해 승률은 적지 만 가격 추세가 확인되면 큰 수익을 얻을 수 있습니다.

따라서 박스 존에서 자주 거래되는 패어보다는 명확한 추세의 패어에서 좋은 수익을 기대할 수 있습니다.

전략에 관심이 있으시거나 사용을 원하신다면 아래를 참고 해 주시거나 PM을 보내주세요.

감사합니다.

Back Testing

*initial_capital: $10000

*default_qty_value: 100%

*commission_value: 0.1%

*Period: 2017.01.01~

Profit

BTCUSD: 3109%

ETHUSD: 11160%

YFIUSDT: 823.88%

ZILUSDT: 570.84%

BNBUSDT: 937.18%

LINKUSDT: 471.41%

*Due to the nature of the strategy, a pair with a strong trend yields better results.

*전략 특성상 추세가 강한 패어에서 더 좋은 결과를 도출합니다.

*Optimized for a 4 hour time frame and a 12 hour time frame.

*4 시간 시간 프레임과 12 시간 시간 프레임에 최적화되었습니다.

Exponential Deviation Bands Width [ChuckBanger]This indicator is a compliment to Exponential Deviation Bands . It is the difference between the upper and the lower bands divided by the middle band. It is an easy way to visualize consolidation before price movements or periods of higher volatility.

How it works

During a period of high volatility, the distance between the two bands will widen and Exponential Deviation Bands width will increase. And the opposite occurs during a period of low volatility, the distance between the two bands will contract and Exponential Deviation Bands width will decrease. Meaning there is a tendency for bands to alternate between expansion and contraction.

When the bands are relatively far apart, that is often is a sign that the current trend is ending. When the distance between the two bands is relatively narrow that often is a sign that the market is about to initiate a bigger move in either direction.

VWAP + Fibo Dev Extensions StrategyBased on my VWAP + Fibo deviations indicator, I tested some strategies to see if the indicator can be profitable; and I got it !

This strategy uses:

H1 timeframe

Weekly VWAP

+1.618 / +2.618 / -1.618 / -2.618 Deviations Extensions to create 2 bands

The value of the deviation

First, the 2 bands are plotted : +1.618/+2.618 painted in red and -1.618/-2.618 painted in lime.

Then, we wait for the deviation value to reach at least 150 (see thumbnail) to avoid littles moves when the gaps between bands are too short.

Entry long position :

first candle must crossunder the -1.618 level and low have to stay over the -2.618

low of the second one must stay in the lime band

enter the third one if the deviation value is over limit (150)

Exit long position :

TP : when a high crossover VWAP

SL : when a low crossunder -2.618

Entry short position :

first candle must crossover the +1.618 level and high have to stay under the +2.618

high of the second one must stay in the red band

enter the third one if the deviation value is over limit (150)

Exit short position :

TP : when a low crossunder VWAP

SL : when a high crossover +2.618

Notes :

this strategy uses pyramiding (5), be careful and calculate your risk management

the comission value is set to 0.08% to include slippages when entering a trade because of market orders

This strategy is not an advice to invest, make your own decisions.

MAD v1 [Intromoto]Hey traders,

This script shows a plotshape on candles, respective of deviation % from the chosen moving average. The further price is from the MA, theoretically, the faster and more reliably price should return to that moving average or close to it.

Users have the following inputs:

- Type of MA to measure the deviations from, i.e EMA, SMA, WMA, VWMA.

- Accompanying moving averages for reference. Fast, med, slowest

- Offset

- AVP resolution

- AVP length

- Use without AVP or other filter

- Use with AVP filter

- Hide/Show High Deviations

- Hide/Show Medium-High Deviations

- Hide/how Smallest High Deviations

- Hide/Show Smallest Low Deviations

- Hide/Show Medium-Low Deviations

- Hide/Show Low Deviations

- Optional size adjustment for low % deviations, used for lower time frames

There are individual plotshapes from deviation percentages in brackets between percentages in both directions of the moving average. i.e 1%-2%, 2%-3%, etc, up to 20% whereby there is a plotshape for all deviations about 20% above the MA and one plotshape for all deviations below -20% below the MA

The plotshapes are color coded from pink and blue . The style menu is setup to show the deviations as they would appear at their respective height above or below the MA. The current filter is a calculation of the average difference between all bars over the length input.

Depending on what time frame you trade within, it may be suggested that these signals are more likely to assist with long exits than short entries, but I have used it for both successfully under certain time frames. Checking off the "Trading Below 3m" box changes the size of the smaller deviations from auto to tiny, which are more visible.

I'll be adding and testing different filters applied to reduce deviation signals that are heavily against the trend or discounting larger time frame momentum. This script, especially the filters I have and will continue to add are experimental. Please use at your own risk.

Thanks for your time!

Please PM me for access.

SSHSH_DevVolatility is a market pulse, like breathing. And it's deviations is being considered as a signal attenuation.

When You want to know how far is the current price of it's mean value, You can use this indicator to determine 3-sigma rule.

The mean line (like moving average) shows if the market is in it's UpTrend state or the DownTrend state.

When it hits it's upper level - so we can say that the Uptrend has ended. The vice versa for the DownTrend.

Use it with the faster tuning when You trade the higher timeframes, and with the slower tuning on a lower timeframes.

{PM me in TradingView to arrange subscription access}

Linear Regression Band BasicLinear Regression Band implements a BB like structure but with the middle line using solely a linear regression as input. In addition unlike bollinger bands , the market price never wicks out of the linear regression band. This is because it gives the absolute possible range taken from the middle line.

Volume Weighted DeviationsVolume !weighted!

deviations.

Important: I don't really know how people generally compute deviations from VWAP/VWMA, but smth tells me generally it's just a Av Dev/St Dev based on mean, not on appropriate basis, like volume weighted mean in our case. This version is mathematically correct, it first calculates weighted mean, than utilizes this weighted in mean in AvDev & StDef functions modified to take into account weights.

Spread by//Every spread & central tendency measure in 1 script with comfortable visualization, including scrips's status line.

Spread measures:

- Standard deviation (for most cases);

- Average deviation (if there are extreme values);

- GstDev - Geometric Standard Deviation (exclusively for Geometric Mean);

- HstDev - Harmonic Deviation (exclusively for Harmonic Mean).

These modified functions will calculate everything right, they will take source, length, AND basis of your choice, unlike the ones from TW.

Central tendency measures:

- Mean (if everything's cool & equal);

- Median (values clustering towards low/high part of the rolling window);

- Trimean (3/more distinguishable clusters of data);

- Midhinhe (2 distinguishable clusters of data);

- Geometric Mean ( |low.. ... ... .. .... ... . . . . . . . . . . . .high| this kinda data); <- Exp law

- Harmonic Mean { |low. . . . . . . . . . . . . . .. . . .high| kinda data). <- Reciprocal law

Listen:

1) Don't hesitate using Standard Deviation with non-mean, like "Midhinge Standard Devition", despite what ol' stats gurus gonna say, it works when it's appropriate;

2) Don't check log space while using Geometric Mean & Geometric Standard Deviation, these 2 implement log stuff by design, I mean unless u wanna make it double xd

3) You can use this script, modify it how you want, ask me questions whatever, just make money using it;

4) Use Midrange & Midpoints in tandem when data follows ~addition law (like this . . . . . . . . . . . . . . . . . . . . .). <- just addition law

Look at the data, choose spread measure first, then choose central tendency measure, not vice versa.

!!!

Ain't gonna place ® sign on standard deviations like one B guy did in 1980s lmao, but if your wanna use Harmonic Deviations in science/write about/cite it/whatever, pls give me a lil credit at least, I've never seen it anywhere and unfortunately had to develop it by myself. it's useful when your data develops by reciprocals law (opposite to exponential).

Peace TW

VAMA Volume Adjusted Moving Average BandsThis indicator is standard deviation bands using a live analysis adaptation of Richard Arms' Volume Adjusted Moving Average as their basis. VAMA utilizes a period length that is based on volume increments rather than time.

• SampleN - N volume bars used as sample to calculate average volume , 0 equals all bars.

• VAMA Source - Price used for volume weighted calculations.

• VAMA Length - Specified number of volume ratio buckets to be reached.

• VAMA VI Fct - Size of volume ratio buckets.

• VAMA Strict - Must meet desired volume requirements, even if number of bars has to exceed VAMA Length to do it.

• STDV Factor - Standard Deviation multiplier.

• STDV Length - Standard Deviation period.

• Brightness - Color opaqueness for the band fills.

Please see previous published example here for more details on VAMA's usage and inability to redraw the past on time based charts.

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

BTCUSDT Volume Weighted Average Price & KairiThis indicator calculates VWAP (Volume Weighted Average Price) for major crypto exchanges with BTCUSDT pairs and shows what percentage each exchange deviates from VWAP.

I made a "BTCUSD" version of this in the past, but many people also want to see “BTCUSDT”, so I made this indicator.

When the parameter "Display" is "Basis", this deviation is expressed in%. Therefore, VWAP is always drawn as "0.00%".

VWAP is calculated using the BTCUSDT prices and volumes of the following exchanges.

These exchanges are the ones Binance refers to when indexing.

- Bitfinex

- Binance

- Huobi

- OKEx

- Bittrex

- HitBTC

VWAP of this indicator calculates the volume for each candlestick , so it will be closer to the actual value.

When there is a big movement in the short term, it is easy to be swayed.

If you set the parameter "Display" to "Basis_SMA", it will calculate the simple moving average of the deviation rate, so it will be hard to be swayed.

Set the desired "Length".

If you want to know the actual value of VWAP , set the parameter "Display" to "Price" and the actual BTCUSDT prices will be displayed.

Warning: This indicator also shows BTCUSDTPERP, but these pairs are not included in the VWAP calculation. be careful.

Harmonic MADsNo, it's not a new saturation plugin for your fruity loops.

...

These are Mean Average Deviations calculated from Harmonic Mean.

...

In my previous research I tried to develop "Harmonic Average Deviations", since applying stdevs on Harmonic Mean calculated from reciprocals ain't make sense. Din't work out, prolly cuz by definition stdevs doesn't like negatives. So in the end I ended up using Mean Average Deviations, and turned out it works great. Generally market data doesn't distribute normally, so t's a great tool, now weird kurtosis won't be a problem.