Gap Trend Lines by @eyemaginativeSummary:

The "Gap Trend Lines" script is designed to identify and visualize gaps between the close of one candle and the opening of the next on a TradingView chart. It draws extended trend lines to visually connect these gaps, helping traders to identify significant price movements between consecutive candles.

Functionality:

Indicator Setup:

The script is set as an overlay indicator on the main chart.

It includes settings for maximum line and label counts, ensuring efficient performance.

Parameter Customization:

Gap Threshold: Defines the minimum gap size considered significant.

Line Colors: Allows customization of colors for small and large gaps.

Line Thickness and Style: Provides options to adjust the thickness and style (solid, dotted, dashed) of the trend lines.

Drawing Extended Trend Lines:

For each bar (candlestick) on the chart, the script checks if there is a gap between the previous candle's close and the current candle's open.

If a gap is detected (i.e., close != open), it determines the size of the gap.

Depending on the size relative to the defined threshold, it selects the appropriate color (small or large gap).

It then draws an extended trend line that starts from the close of the previous candle (bar_index , close ) and extends to the open of the current candle (bar_index, open).

The trend line is drawn with the specified thickness, color, and style.

Dynamic Line Attribute Changes:

The script includes a function (changeLineAttributes()) that periodically changes the color and style of the trend lines.

By default, it changes the color every 4 hours (adjustable), alternating between green and the original color.

Enhanced Functionality:

Handles both small and large gaps with different visual cues (colors).

Supports extended trend lines that span both past and future directions (extend=extend.both), ensuring visibility across the entire chart.

Usage:

Traders can use the "Gap Trend Lines" script to:

Identify and analyze gaps between candlesticks.

Visualize significant price movements or breaks in continuity.

Customize the appearance of trend lines for better clarity and analysis.

By utilizing this script, traders can gain insights into price gap dynamics directly on TradingView charts, aiding in decision-making and strategy development.

Forecasting

Exponential Grid [Phi, Pi, Euler]If you disagree with one of the EMH principles that price is too random, then by definition you must agree that historic price has deterministic function to a scenario ahead.

I personally believe that constants like phi, pi and e can mimic exponential growth of the price.

In this script, first grid is based on the Lowest price multiplied with self fraction of the constant.

For example:

If you are familiar with fib ratio 1.272, then you must know that it is 1.618 to the power of 0.5.

With default settings of exponent step 0.25

First grid = Lowest price x phi^0.25

Second grid = Lowest price x phi^0.25x2

Third grid = Lowest price x phi^0.25x3 and so on

The script will automatically find the lowest price and update the grid values.

Or you can set up your custom Lowest price manually if you feel like the All Time Low level loses its relevance value after long period.

There are 64 grids including Lowest price level. And it wasn't by a chance. Pine Script has a limitation of max 64 plots. Number of grids shown in the chart depends on the highest price. Once price breaks above ATH a couple of next grids will be plotted automatically. In most cases if everything is plotted, the chart appears squeezed and you'll need to zoom in to see it. Therefore, I adjusted it relatively to the scale of the chart for the comfort.

In some cases 64 plots aren't enough to cover the whole chart. For example, let's take a look at NVIDIA chart:

Since the price has started with 0.0333, it is way too small to cover all with default settings.

We are left with 2 choices:

Either Enable "Round"

OR increase Exponent Step (from 0.25 to 0.5 in the particular example below)

If you set constant to pi or e which is a bigger number than phi, expect the gaps to be bigger. To reduce it to a more gradual way of expansion you can decrease Exponent Step.

Earnings Beat IndicatorThis indicator seeks to predict whether a stock will beat or miss earnings by forecasting revenues, and subsequently net income, using linear regression. The y-values of this regression are revenues and the x-axis is an economic series of your choosing. Double-click the status line (the words "US" and "GDP") to change economic datasets. The full list of economic datasets available in TradingView is in the Help Center.

Instructions:

1. Double-click on the status line (the fields "US" and "GDP"). The inputs tab will pop up.

2. Type in the country and data codes for the economic datasets you believe have the highest correlation with revenues and net margins respectively.

3. Check the correlation coefficient between financial data and economic data by interpreting the white and gray numbers on the status line - white for the correlation coefficient between revenues and your chosen economic dataset, and gray for the correlation coefficient between net margins and your chosen economic dataset. These numbers should be as close to +1 or -1 as possible.

4. Interpret the results - the blue number indicates whether revenues will beat estimates and the green number indicates whether earnings will beat estimates. A 1 for both outputs indicates a double beat, a 1 and a 0 indicates a revenue beat but not an earnings beat, a 0 and a 1 indicates an earnings beat but not a revenue beat, and a 0 and a 0 indicates a double miss.

- DickZhones

COT-NocTradingIndicator Description:

Commitments of Traders (COT) Data Indicator

The Commitments of Traders (COT) Data Indicator on TradingView provides insights into market sentiment based on the weekly CFTC (Commodity Futures Trading Commission) reports. It plots three key lines derived from this data, offering valuable information for traders seeking to understand positioning trends among large speculators, commercial hedgers, and small traders.

Lines Plotted:

Commercials: Reflects positions held by commercial entities engaged in the production or sale of the underlying commodity. Their positions often act as a hedge against physical market exposure.

Non Commercials: Represents positions held by large speculators, typically hedge funds and large financial institutions, who often take more significant positions based on their market outlook.

Retail Traders: Shows positions held by small traders, including individual retail traders and smaller institutional players, providing insights into the broader retail sentiment.

Labeling:

Each line is accompanied by a label to clearly identify its corresponding group, enhancing clarity and ease of interpretation for traders analyzing the indicator.

Usage:

Trend Confirmation: Monitor the positioning of commercial and non commercial relative to retail traders to confirm trends and potential reversals.

Sentiment Analysis: Assess shifts in market sentiment based on changes in positioning across different trader categories.

Trading Signals: Use crossovers, divergences, and extreme positioning relative to historical data to generate potential trading signals.

This indicator is valuable for traders looking to incorporate institutional positioning data into their trading strategies, offering a deeper understanding of market dynamics beyond price action alone.

ADX and SADX, SDIThe indicator aims to analyze and visualize the Average Directional Index (ADX) and its smoothed versions, along with directional indicators (DI) to help traders identify trend strength and potential buy/sell signals.

Indicator Settings:

The indicator is named "ADX and SADX, SDI" and is set to display prices with a precision of 2 decimal places.

Users can customize the ADX smoothing length, DI length, ADX smoothing period, and DI smoothing period through input variables.

Directional Movement (DM) Calculation:

The function dirmov calculates the positive and negative directional movements (DM) and the smoothed values of the positive directional index (DI+) and negative directional index (DI-).

This is done using the average true range (ATR) to normalize the DM values.

Average Directional Index (ADX) Calculation:

The function adx calculates the ADX, which measures the strength of a trend.

It uses the DI+ and DI- values to compute the ADX value.

Smoothed ADX and DI Calculation:

The ADX values are further smoothed using a simple moving average (SMA).

The DI difference is also smoothed and used to determine the trend direction.

Buy and Sell Signals:

A buy signal is generated when the DI+ crosses above DI- and the smoothed DI difference is increasing.

A sell signal is generated when the DI- crosses above DI+ and the smoothed DI difference is decreasing.

Plotting:

The ADX, smoothed ADX, smoothed DI difference (SPM), DI+, and DI- values are plotted on the chart.

Horizontal lines are drawn to indicate threshold levels (e.g., level 22).

Background and bar colors change based on buy (lime) and sell (maroon) signals to visually indicate these conditions.

Purpose of the Code:

This Pine Script code is used to create a custom indicator on TradingView that helps traders identify the strength and direction of a trend. The Average Directional Index (ADX) is used to measure trend strength, while the Directional Indicators (DI+ and DI-) are used to determine the direction of the trend. The smoothed versions of these indicators (SADX and SDI) provide additional confirmation and smoothing to reduce noise and false signals. Traders can use the buy and sell signals generated by this indicator to make informed trading decisions based on the trend strength and direction.

Important Note:

This script is provided for educational purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Median Analyst ConsensusThe Median Analyst Consensus Indicator provides an unbiased, easy-to-interpret view of market sentiment by leveraging TradingView's comprehensive financial data library. This tool displays the median 12-month price target and the percentage difference from the current price directly on your charts.

Key Features

1. Accurate Market Sentiment: By consolidating analyst ratings and price targets from multiple reputable sources like Bloomberg, Refinitiv (formerly Thomson Reuters), S&P Capital IQ, and Morningstar, this indicator displays the median analyst consensus. Using the median ensures outlier ratings don't skew the overall sentiment, providing a more robust representation.

2. Simplicity at a Glance: View the median 12-month price target and percentage difference from the current price directly on your chart. No need to juggle multiple reports - key insights are surfaced within your normal trading workflow.

3. Data-Driven Transparency: If no analyst data is available for a particular asset, the indicator will not display, ensuring you only see reliable information. The number of contributing analysts is also shown for context.

Why the Median?

The median is favored over the mean to minimize the impact of outlier ratings that could distort the consensus view. By taking the middle value across all analyst projections, the median provides a more stable, outlier-resistant measure of market sentiment.

Powered by TradingView Data

This indicator taps into TradingView's financial data library, which aggregates analyst ratings, estimates, and recommendations from leading institutional data providers. TradingView sources this data from firms like FactSet, Bloomberg, Refinitiv, S&P Capital IQ, and Morningstar, ensuring a comprehensive and trusted view of analyst sentiment.

The library provides variables like:

syminfo.recommendations_buy

syminfo.recommendations_sell

syminfo.target_price_median

syminfo.recommendations_buy_strong

syminfo.recommendations_sell_strong

The indicator calculates and displays the median of these analyst inputs.

Usage

The indicator displays:

The median 12-month price target across analysts

The percentage difference between the price target and current price

The number of contributing analyst estimates

If no analyst data is available, the indicator does not display, ensuring full transparency.

The Median Analyst Consensus Indicator provides an unbiased, easy-to-interpret view of market sentiment by leveraging TradingView's comprehensive financial data library. This tool offers a new perspective on potential trade opportunities directly on your charts.

Disclaimer

While the data is sourced from reputable providers, analyst forecasts should not be construed as investment recommendations. This indicator aims to synthesize market opinions, but investment decisions are solely your responsibility. As with any analytical tool, you should conduct your own research and risk assessments before executing any trades.

ΔYoY(Economics)Year over year indicator which will benchmark the most recent data vs 1 year lookback; Will automate the lookback for quarterly and monthly data based on timeframe selected (3M for quarterly, 1M for monthly). Tradingview will aggregate weekly data into a monthly data point. SMA applied to get the average over some x period.

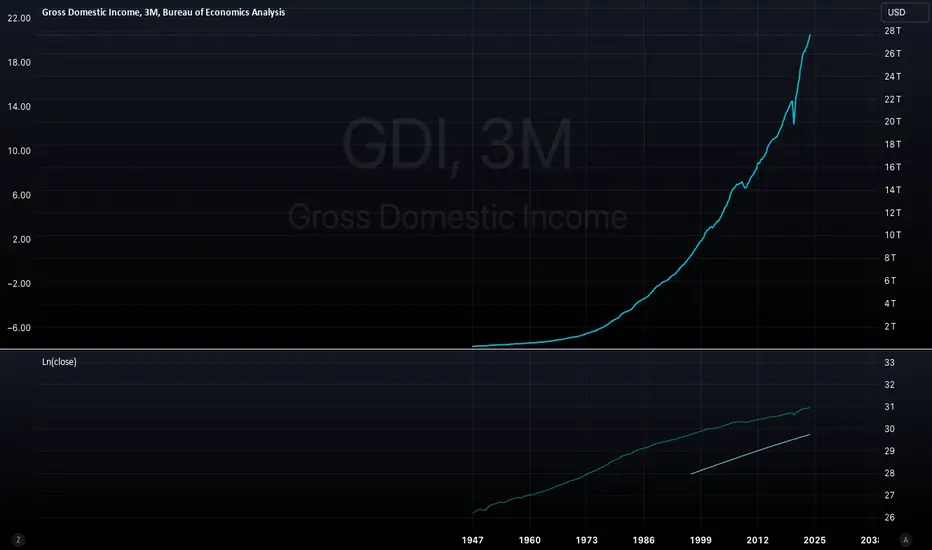

Ln(close)Natural log indicator for normalizing data. SMA applied so you can take the average of that normalization factor. Personally use it for US economic data where the value is very large (GDI, Fed Balance Sheet, USM2 etc.) and the year over year delta is not pertinent (USM2) or not available (GDI.. although I did make an indicator to get YoY :D). Any additional ideas leave a comment and I'll take a look.

Nasan Moving Average with ForecastThe "Nasan Moving Average with Forecast" indicator is a technical analysis forecasting tool that combines the principles of historical data analysis and random walk theory. It calculates a customized moving average (Nasan Moving Average) by integrating price data and statistical measures and projects future price points by generating forecast values within calculated volatility bounds, creating a dynamic and insightful visualization of potential market movements. This indicator to blend past market behavior with probabilistic future trends to enhance forecasting.

Input Parameters:

len: Differencing length (default 21, Use a minimum of 5 and for lower time frames less than 15 min use values between 300 -3000)

len1: Correction Factor Length 1 (default 21, this determines the length of the MA you want , eg. 10 MA, 50 MA, 100 MA, )

len2: Correction Factor Length 2 (default 9, this works best if it is ~ </=1/2 of len1 )

len3: Smoothing Length (default 5, I would not change this and only use if I want to introduce lag where you want to use it for cross over strategies).

forecast_points: Number of points to forecast (default 30).

m: Multiplier for standard deviation (default 2.5).

bl: Block length for calculating max/min values (default 100).

use_calculated_max_min: Boolean to decide whether to use calculated max/min values.

Nasan Moving Average Calculation:

Calculates the simple moving average (mean) and standard deviation (sd) of the typical price (hlc3).

Computes intermediate variables (a, b, c, etc.) based on log transformation and cumulative sum.

Applies weighted moving averages (wma) to these intermediate variables to smooth them and derive the final value c6.

Plots c6 as the Nasan Moving Average if the bar is confirmed. To learn more see Nasan Moving Average.

Forecast Points Calculation:

Calculates maximum (max_val) and minimum (min_val) values for the forecast, either using a fixed value or based on standard deviation and a multiplier.

Initializes an array to store forecast values and creates polyline objects for plotting.

If the current bar is one of the last three bars and confirmed:

Clears and reinitializes the polyline.

Initializes the first forecast value from the cumulative sum c.

Generates subsequent forecast values using a random value within the range .

Updates the forecast array and plots the forecast points as an orange curved polyline.

Plotting Max/Min Values:

Plots max_val and min_val as green and red lines, respectively, to indicate the bounds of the forecast range.

Components of the Forecasting Model

Historical Dependence:

Nasan Moving Average Calculation: The script calculates a custom moving average (c6) that incorporates historical price data (hlc3), standard deviations (sd), and weighted moving averages (wma). This part of the code processes historical data to create a smoothed representation of the price trend.

Max/Min Value Calculation: The maximum (max_val) and minimum (min_val) values for the forecast can be calculated based on the historical standard deviation of a transformed variable b over a block length (bl). This introduces historical volatility into the bounds for the forecast.

Random Walk Model:

Random Value Generation: Within the forecast points calculation, a random value (random_val) is generated for each forecast point within the range . This random value introduces stochasticity into the model, characteristic of a random walk process.

Cumulative Sum for Forecasting: The script uses a cumulative sum (prev_f + random_val) to generate the next forecast point (next_f). This is a typical approach in random walk models where each new point is based on the previous point plus some random noise.

Explanation of the Forecast Model

Random Walk Characteristics: Each new forecast point is generated by adding a random value to the previous point, making the model a random walk with drift, where the drift is influenced by historical correction factors (c1, c4).

Historical and Statistical Dependence: The bounds of the random values and the initial conditions are derived from historical data, ensuring that the forecast respects historical volatility and trends.

The forecasting model in the script is a hybrid approach: It uses a random walk to generate future points, characterized by adding random values to the previous forecasted value.

The historical and statistical dependence is incorporated through initial conditions, scaling factors, and bounds derived from historical price data and its statistical properties.

This combination ensures that the forecasts are not purely stochastic but are grounded in historical price behavior, making the model more robust and potentially more accurate in reflecting market conditions.

ALT Trend DetectionALT Trend Detection Indicator

Overview:

The "ALT Trend Detection" indicator is designed to help traders analyze the relationship between Bitcoin's dominance, Bitcoin's price, and the potential impact on altcoin prices. This indicator uses various time frames and average true range (ATR) calculations to detect trends and provide insights into the altcoin market conditions based on Bitcoin's movements.

How It Works:

BTC Dominance and Price Data:

The indicator fetches Bitcoin dominance data (percentage of the total cryptocurrency market cap that Bitcoin represents) and Bitcoin price data using the selected time frame.

It calculates whether Bitcoin dominance and price are trending up, down, or remaining stable based on ATR calculations.

Altcoin Trend Detection:

The indicator then evaluates different scenarios based on the combination of Bitcoin dominance and price movements. These scenarios help predict the potential impact on altcoin prices.

For instance, if Bitcoin dominance is up and Bitcoin price is up, it might indicate a bearish trend for altcoins. Conversely, if Bitcoin dominance is down and Bitcoin price is up, it might indicate a bullish trend for altcoins (altseason).

Table Display:

The indicator displays a table on the chart that summarizes the current conditions for Bitcoin dominance, Bitcoin price, and the expected impact on altcoins. Each cell in the table is color-coded to provide a quick visual representation of the trends.

Usage:

Add the indicator to your TradingView chart.

Customize the time frame, ATR multiplier, table position, table size, and background color as per your preference.

Observe the table displayed on the chart. It shows the current state of Bitcoin dominance, Bitcoin price, and the potential trend for altcoin prices based on predefined scenarios.

Use this information to make informed trading decisions about altcoins. For example, if the table shows "ALT SEASON" in green, it might be a good time to consider investing in altcoins.

By analyzing the interaction between Bitcoin dominance and price, this indicator helps traders identify potential opportunities and risks in the altcoin market.

Anchored Monte Carlo Shuffled Projection [LuxAlgo]The Anchored Monte Carlo Shuffled Projection tool randomly simulates future price points based on historical bar movements made before a user-anchored point in time.

By anchoring our data and projections to a single point in time, users can better understand and reflect on how the price played out while taking into consideration our random simulations.

🔶 USAGE

After selecting the indicator to apply to the chart, you will be prompted to "Set the Anchor Point". Do so by clicking on the desired location on your chart, only time is used as the anchor point.

Note: To select a new anchor point when applied to the chart, click on the 'More' dropdown next to the indicator status bar (○○○), then select "Reset points...".

Alternate Method: You are also able to click and drag the vertical line that displays on the anchor point bar when the indicator is highlighted.

By randomly simulating bar movements, a range is developed of potential price action which could be utilized to locate future price development as well as potential support/resistance levels.

Performing numerous simulations and taking the average at each step will converge toward the result highlighted by the "Average Line", and can point out where the price might develop, assuming the trend and amount of volatility persist.

Current closing price + Sum of changes in the calculation window

This constraint will cause the simulations always to display an endpoint consistent with the current lookback's slope.

While this may be helpful to some traders, this indicator includes an option to produce a less biased range, as seen below:

🔶 DETAILS

The Anchored Monte Carlo Shuffled Projection tool creates simulations based on prices within a user-set lookback window originating at the specified anchor point. Simulations are done as follows:

Collect each bar's price changes in the user-set window.

Randomize the order of each change in the window.

Project the cumulative sum of the shuffled changes from the current closing price.

Collect data on each point along the way.

This is the process for the Default calculation; for the 'Randomize Direction' calculation, when added onto the front for every other change, the value is inverted, creating the randomized endpoints for each simulation.

The script contains each simulation's data for that bar, with a maximum of 1000 simulations.

To get a glimpse behind the scenes, each simulation (up to 99) can be viewed using the 'Visualize Simulations' Options, as seen below.

Because the script holds the full simulation data, the script can also calculate this data, such as standard deviations.

In this script the Standard deviation lines are the average of all standard deviations across the vertical data groups, this provides a singular value that can be displayed a distance away from the simulation center line.

🔶 SETTINGS

Lookback: Sets the number of Bars to include in calculations.

Simulation Count: Sets the number of randomized simulations to calculate. (Max 1000)

Randomize Direction: See Details Above. Creates a more 'Normalized' Distribution

Visualize Simulations: See Details Above. Turns on Visualizations, and colors are randomly generated. Visualized max does not cap the calculated max. If 1000 simulations are used, the data will be from 1000 simulations, however, only the last 99 simulations will be visualized.

🔹 Standard Deviations

Standard Deviation Multiplier: Sets the multiplier to use for the Standard Deviation distance away from the center line.

🔹 Style

Extend Lines: Extends the Simulated Value Lines into the future for further reference and analysis.

Velocity And Acceleration with Strategy: Traders Magazine◙ OVERVIEW

Hi, Ivestors and Traders... This Indicator, the focus is Scott Cong's article in the Stocks & Commodities September issue, “VAcc: A Momentum Indicator Based On Velocity And Acceleration”. I have also added a trading strategy for you to benefit from this indicator. First of all, let's look at what the indicator offers us and what its logic is. First, let's focus on the logic of the strategy.

◙ CONCEPTS

Here is a new indicator based on some simple physics concepts that is easy to use, responsive and precise. Learn how to calculate and use it.

The field of physics gives us some important principles that are highly applicable to analyzing the markets. In this indicator, I will present a momentum indicator. Scott Cong developed based on the concepts of velocity and acceleration this indicator. Of the many characteristics of price that traders and analysts often study, rate and rate of change are useful ones. In other words, it’s helpful to know: How fast is price moving, and is it speeding up or slowing down? How is price changing from one period to the next? The indicator I’m introducing here is calculated using the current bar (C) and every bar of a lookback period from the current bar. He named the indicator the VAcc since it’s based on the average of velocity line (av) and acceleration line (Acc) over the lookback period. For longer periods, the VAcc behaves the same way as the MACD, only it’s simpler, more responsive, and more precise. Interestingly, for shorter periods, VAcc exhibits characteristics of an oscillator, such as the stochastics oscillator.

◙ CALCULATION

The calculation of VAcc involves the following steps:

1. Relatively weighted average where the nearer price has the largest influence.

weighted_avg (float src, int length) =>

float sum = 0.0

for _i = 1 to length

float diff = (src - src ) / _i

sum += diff

sum /= length

2. The Velocity Average is smoothed with an exponential moving average. Now it get:

VAcc (float src, int period, int smoothing) =>

float vel = ta.ema(weighted_avg(src, period), smoothing)

float acc = weighted_avg(vel, period)

3. Similarly, accelerations for each bar within the lookback period and scale factor are calculated as:

= VAcc(src, length1, length2)

av /= (length1 * scale_factor)

◙ STRATEGY

In fact, Scott probably preferred to use it in periods 9 and 26 because it was similar to Macd and used the ratio of 0.5. However, I preferred to use the 8 and 21 periods to provide signals closer to the stochastic oscillator in the short term and used the 0.382 ratio. The logic of the strategy is this

Long Strategy → acc(Acceleration Line) > 0.1 and av(Velocity Average Line) > 0.1(Long Factor)

Short strategy → acc(Acceleration Line) < -0.1 and av(Velocity Average Line) < -0.1(Long Factor)

Here, you can change the Short Factor and Long Factor as you wish and produce more meaningful results that are closer to your own strategy.

I hope you benefits...

◙ GENEL BAKIŞ

Merhaba Yatırımcılar ve Yatırımcılar... Bu Gösterge, Scott Cong'un Stocks & Emtia Eylül sayısındaki “VAcc: Hız ve İvmeye Dayalı Bir Momentum Göstergesi” başlıklı makalesine odaklanmaktadır. Bu göstergeden faydalanabilmeniz için bir ticaret stratejisi de ekledim. Öncelikle göstergenin bize neler sunduğuna ve mantığının ne olduğuna bakalım. Öncelikle stratejinin mantığına odaklanalım.

◙ KAVRAMLAR

İşte kullanımı kolay, duyarlı ve kesin bazı basit fizik kavramlarına dayanan yeni bir gösterge. Nasıl hesaplanacağını ve kullanılacağını öğrenin.

Fizik alanı bize piyasaları analiz etmede son derece uygulanabilir bazı önemli ilkeler verir. Bu göstergede bir momentum göstergesi sunacağım. Scott Cong bu göstergeyi hız ve ivme kavramlarına dayanarak geliştirdi. Yatırımcıların ve analistlerin sıklıkla incelediği fiyatın pek çok özelliği arasında değişim oranı ve oranı yararlı olanlardır. Başka bir deyişle şunu bilmek faydalı olacaktır: Fiyat ne kadar hızlı hareket ediyor ve hızlanıyor mu, yavaşlıyor mu? Fiyatlar bir dönemden diğerine nasıl değişiyor? Burada tanıtacağım gösterge, mevcut çubuk (C) ve mevcut çubuktan bir yeniden inceleme döneminin her çubuğu kullanılarak hesaplanır. Göstergeye, yeniden inceleme dönemi boyunca hız çizgisinin (av) ve ivme çizgisinin (Acc) ortalamasına dayandığı için VAcc adını verdi. Daha uzun süreler boyunca VACc, MACD ile aynı şekilde davranır, yalnızca daha basit, daha duyarlı ve daha hassastır. İlginç bir şekilde, daha kısa süreler için VAcc, stokastik osilatör gibi bir osilatörün özelliklerini sergiliyor.

◙ HESAPLAMA

VAcc'nin hesaplanması aşağıdaki adımları içerir:

1. Yakın zamandaki fiyatın en büyük etkiye sahip olduğu göreceli ağırlıklı ortalamayı hesaplatıyoruz.

weighted_avg (float src, int length) =>

float sum = 0.0

for _i = 1 to length

float diff = (src - src ) / _i

sum += diff

sum /= length

2. Hız Ortalamasına üstel hareketli ortalamayla düzleştirme uygulanır. Şimdi bu şekilde aşağıdaki kod ile bunu şöyle elde ediyoruz:

VAcc (float src, int period, int smoothing) =>

float vel = ta.ema(weighted_avg(src, period), smoothing)

float acc = weighted_avg(vel, period)

3. Benzer şekilde, yeniden inceleme süresi ve ölçek faktörü içindeki her bir çubuk için fiyattaki ivmelenler yada momentum şu şekilde hesaplanır:

= VAcc(src, length1, length2)

av /= (length1 * scale_factor)

◙ STRATEJİ

Aslında Scott muhtemelen Macd'e benzediği ve 0,5 oranını kullandığı için 9. ve 26. periyotlarda kullanmayı tercih etmişti. Ancak kısa vadede stokastik osilatöre daha yakın sinyaller sağlamak için 8 ve 21 periyotlarını kullanmayı tercih ettim ve 0,382 oranını kullandım. Stratejinin mantığı şu

Uzun Strateji → acc(İvme Çizgisi) > 0,1 ve av(Hız Ortalama Çizgisi) > 0,1(Uzun Faktör)

Kısa strateji → acc(İvme Çizgisi) < -0,1 ve av(Hız Ortalama Çizgisi) < -0,1(Uzun Faktör)

Burada Kısa Faktör ve Uzun Faktör' ü dilediğiniz gibi değiştirip, kendi stratejinize daha yakın, daha anlamlı sonuçlar üretebilirsiniz.

umarım faydasını görürsün...

Leading MACDThe Moving Average Convergence Divergence (MACD) indicator is one of the most popular and versatile tools used by traders to identify potential buy and sell signals. It helps traders determine the strength and direction of a trend by comparing different moving averages of a security's price. The traditional MACD uses two exponential moving averages (EMAs), a fast EMA (typically 12 periods) and a slow EMA (typically 26 periods), along with a signal line (typically a 9-period EMA of the MACD line) to generate trading signals.

Our "Custom MACD with Leading Length" script for TradingView enhances the traditional MACD by introducing an additional smoothing factor called the "leading length." This customization aims to reduce noise and provide a potentially earlier indication of trend changes, making it a valuable tool for traders seeking to optimize their trading strategies.

- **Purpose:** This additional smoothing factor is designed to reduce noise and provide a potentially leading signal, enhancing the accuracy of trend identification.

## How It Works

1. **Calculate the MACD Line:**

The MACD line is calculated by subtracting the slow EMA from the fast EMA. This difference represents the convergence or divergence between the two EMAs.

2. **Calculate the Signal Line:**

The signal line is an EMA of the MACD line. This additional smoothing helps to generate clearer buy and sell signals based on crossovers with the MACD line.

3. **Calculate the Histogram:**

The histogram represents the difference between the MACD line and the signal line. It visually indicates the strength and direction of the trend. A positive histogram suggests a bullish trend, while a negative histogram indicates a bearish trend.

4. **Apply Leading Length Smoothing:**

To incorporate the leading length, the script applies a simple moving average (SMA) to both the MACD and signal lines using the leading length parameter. This additional smoothing helps to further reduce noise and potentially provides earlier signals of trend changes.

## Benefits of the Leading MACD

### Reduced Noise

The leading length parameter adds an extra layer of smoothing to the MACD and signal lines, helping to filter out market noise. This can be particularly beneficial in volatile markets, where frequent price fluctuations can generate false signals.

### Potential Early Signals

By smoothing the MACD and signal lines, the leading length can help to provide earlier indications of trend changes. This can give traders a potential edge in entering or exiting trades before the broader market reacts.

### Enhanced Trend Identification

The combination of the traditional MACD with the leading length smoothing can enhance the accuracy of trend identification. Traders can use this tool to confirm the strength and direction of trends, making it easier to make informed trading decisions.

### Versatility

The Custom MACD with Leading Length can be applied to various timeframes and asset classes, including stocks, forex, commodities, and cryptocurrencies. Its adaptability makes it a valuable tool for traders with different strategies and preferences.

## Practical Applications

### Buy Signal

A typical buy signal occurs when the MACD line crosses above the signal line. With the additional smoothing provided by the leading length, traders might receive this signal slightly earlier, allowing them to enter a long position sooner. This can be particularly advantageous in capturing the beginning of a bullish trend.

### Sell Signal

Conversely, a sell signal is generated when the MACD line crosses below the signal line. The leading length smoothing can help to provide this signal earlier, enabling traders to exit a long position or enter a short position before the trend reversal is fully recognized by the market.

### Divergence Analysis

Traders can also use the Custom MACD with Leading Length for divergence analysis. Bullish divergence occurs when the price makes a new low, but the MACD line forms a higher low. This suggests that the downward momentum is weakening, potentially leading to a bullish reversal. Bearish divergence is the opposite, where the price makes a new high, but the MACD line forms a lower high, indicating a potential bearish reversal.

### Confirmation Tool

The Custom MACD with Leading Length can be used in conjunction with other technical indicators to confirm trading signals. For example, traders might use it alongside support and resistance levels, trendlines, or other momentum indicators to validate their trade entries and exits.

## Conclusion

The Custom MACD with Leading Length is a powerful enhancement of the traditional MACD indicator. By introducing an additional smoothing factor, it aims to reduce noise and provide earlier signals of trend changes. This makes it a valuable tool for traders seeking to improve their market analysis and trading strategies.

Whether you are a day trader, swing trader, or long-term investor, the Custom MACD with Leading Length can help you make more informed decisions by offering clearer insights into market trends. Its adaptability to different timeframes and asset classes further enhances its utility, making it a versatile addition to any trader's toolkit.

Experiment with the parameters to find the optimal settings that suit your trading style and preferences. Use the Custom MACD with Leading Length to gain a deeper understanding of market dynamics and enhance your trading performance.

VolCorrBeta [NariCapitalTrading]Indicator Overview: VolCorrBeta

The VolCorrBeta indicator is designed to analyze and interpret intermarket relationships. This indicator combines volatility, correlation, and beta calculations to provide a comprehensive view of how certain assets (BTC, DXY, CL) influence the ES futures contract (I tailored this indicator to the ES contract, but it will work for any symbol).

Functionality

Input Symbols

BTCUSD : Bitcoin to USD

DXY : US Dollar Index

CL1! : Crude Oil Futures

ES1! : S&P 500 Futures

These symbols can be customized according to user preferences. The main focus of the indicator is to analyze how the price movements of these assets correlate with and lead the price movements of the ES futures contract.

Parameters for Calculation

Correlation Length : Number of periods for calculating the correlation.

Standard Deviation Length : Number of periods for calculating the standard deviation.

Lookback Period for Beta : Number of periods for calculating beta.

Volatility Filter Length : Length of the volatility filter.

Volatility Threshold : Threshold for adjusting the lookback period based on volatility.

Key Calculations

Returns Calculation : Computes the daily returns for each input symbol.

Correlation Calculation : Computes the correlation between each input symbol's returns and the ES futures contract returns over the specified correlation length.

Standard Deviation Calculation : Computes the standard deviation for each input symbol's returns and the ES futures contract returns.

Beta Calculation : Computes the beta for each input symbol relative to the ES futures contract.

Weighted Returns Calculation : Computes the weighted returns based on the calculated betas.

Lead-Lag Indicator : Calculates a lead-lag indicator by averaging the weighted returns.

Volatility Filter : Smooths the lead-lag indicator using a simple moving average.

Price Target Estimation : Estimates the ES price target based on the lead-lag indicator (the yellow line on the chart).

Dynamic Stop Loss (SL) and Take Profit (TP) Levels : Calculates dynamic SL and TP levels using volatility bands.

Signal Generation

The indicator generates buy and sell signals based on the filtered lead-lag indicator and confirms them using higher timeframe analysis. Signals are debounced to reduce frequency, ensuring that only significant signals are considered.

Visualization

Background Coloring : The background color changes based on the buy and sell signals for easy visualization (user can toggle this on/off).

Signal Labels : Labels with arrows are plotted on the chart, showing the signal type (buy/sell), the entry price, TP, and SL levels.

Estimated ES Price Target : The estimated price target for ES futures is plotted on the chart.

Correlation and Beta Dashboard : A table displayed in the top right corner shows the current correlation and beta values for relative to the ES futures contract.

Customization

Traders can customize the following parameters to tailor the indicator to their specific needs:

Input Symbols : Change the symbols for BTC, DXY, CL, and ES.

Correlation Length : Adjust the number of periods used for calculating correlation.

Standard Deviation Length : Adjust the number of periods used for calculating standard deviation.

Lookback Period for Beta : Change the lookback period for calculating beta.

Volatility Filter Length : Modify the length of the volatility filter.

Volatility Threshold : Set a threshold for adjusting the lookback period based on volatility.

Plotting Options : Customize the colors and line widths of the plotted elements.

Funding Rate [CryptoSea]The Funding Rate Indicator by is a comprehensive tool designed to analyze funding rates across multiple cryptocurrency exchanges. This indicator is essential for traders who want to monitor funding rates and their impact on market trends.

Key Features

Exchange Coverage: Includes data from major exchanges such as Binance, Bitmex, Bybit, HTX, Kraken, OKX, Bitstamp, and Coinbase.

Perpetual Futures and Spot Markets: Fetches and analyzes pricing data from both perpetual futures and spot markets to provide a holistic view.

Smoothing and Customization: Allows users to smooth funding rates using a moving average, with customizable MA lengths for tailored analysis.

Dynamic Candle Coloring: Option to color candles based on trading conditions, enhancing visual analysis.

In the example below, the indicator shows how the funding rate shifts with market conditions, providing clear visual cues for bullish and bearish trends.

How it Works

Data Integration: Uses a secure security fetching function to retrieve pricing data while preventing look-ahead bias, ensuring accurate and reliable information.

TWAP Calculation: Computes Time-Weighted Average Prices (TWAP) for both perpetual futures and spot prices, forming the basis for funding rate calculations.

Funding Rate Calculation: Determines the raw funding rate by comparing TWAPs of perpetual futures and spot prices, then applies smoothing to highlight significant trends.

Color Coding: Highlights the funding rate with distinct colors (bullish and bearish), making it easier to interpret market conditions at a glance.

In the example below, the indicator effectively differentiates between bullish and bearish funding rates, aiding traders in making informed decisions based on current market dynamics.

Application

Market Analysis: Enables traders to analyze the impact of funding rates on market trends, facilitating more strategic decision-making.

Trend Identification: Assists in identifying potential market reversals by monitoring shifts in funding rates.

Customizable Settings: Provides extensive input settings for exchange selection, MA length, and candle coloring, allowing for personalized analysis.

The Funding Rate Indicator by is a powerful addition to any trader's toolkit, offering detailed insights into funding rates across multiple exchanges to navigate the cryptocurrency market effectively.

Total Cross CalculatorThe Indicator calculates the total number of the death and golden crosses in the total chart which can help the moving average user to compare the number of signals generated by the moving average pair in the given timeframe.

If Indicator is not plotting anything then right click on the indicator's scale and click on "Auto(data fits the screen)" option.

Please visit it's previous version if you want to use the indicator on the moving averages created by yourself. Link is here

CPR by MTThe CPR indicator, or Central Pivot Range indicator, is a technical analysis tool used in trading to identify potential support and resistance levels based on the price action of a security. Developed by pivot point theory, it is particularly popular among day traders and swing traders. The CPR indicator consists of three lines:

1. **Pivot Point (PP):** This is the central line and is calculated as the average of the high, low, and closing prices from the previous trading period.

\

2. **Top Central Pivot (TC):** This is calculated by subtracting the low from the PP and then adding the result to the PP.

\

3. **Bottom Central Pivot (BC):** This is calculated by subtracting the high from the PP and then adding the result to the PP.

\

### How to Use the CPR Indicator

- **Trend Identification:** A wide CPR range indicates low volatility and a potential sideways or consolidation phase. A narrow CPR range indicates high volatility and a potential strong trending move.

- **Support and Resistance:** The top and bottom central pivots act as immediate resistance and support levels. If the price is above the TC, it indicates a bullish sentiment, while if it is below the BC, it indicates a bearish sentiment.

- **Entry and Exit Points:** Traders use the CPR lines to determine optimal entry and exit points. For example, if the price breaks above the TC and sustains, it may signal a buy opportunity, whereas a drop below the BC may signal a sell opportunity.

### Practical Example

Suppose a stock had a high of $105, a low of $95, and a closing price of $100 on the previous day. The CPR levels for the next day would be calculated as follows:

1. **Pivot Point (PP):**

\

2. **Top Central Pivot (TC):**

\

3. **Bottom Central Pivot (BC):**

\

The levels for the next day would be PP = $100, TC = $110, and BC = $90. Traders would then use these levels to assess potential trading strategies based on where the price moves relative to these levels.

### Conclusion

The CPR indicator is a useful tool for traders looking to understand market conditions and make informed decisions about entry and exit points. Its effectiveness comes from its ability to highlight key price levels derived from historical price data, helping traders predict potential market movements.

Johnny's Trend Lines, Supports and ResistancesInspired and based on ismailcarlik's Trend Lines, Supports and Resistances.

Additions include an overall upgrade to Pinescript v5, changes in the way resistance and support levels are calculated, improved visual queues, and additional customization options.

This indicator is meticulously crafted to provide traders with visual tools for identifying trend lines, support, and resistance levels, enhancing the decision-making process in trading activities.

Features and Functionality

Trend Lines: The indicator allows users to enable or disable trend lines, adjust the number of points to check for establishing a trend, and set parameters for trend validation, including the maximum violation and exceptions for the last bars.

Support and Resistance: It offers tools to identify and visualize key support and resistance levels based on recent pivot points. This includes adjustable parameters for the maximum violations allowed and the exclusion of recent bars from the analysis.

Pivot Points: Users can define the pivot length for calculating highs and lows, which helps in marking significant pivot points that are instrumental in trend analysis.

Alerts and Notifications: The indicator is equipped with customizable alerts for trend line breaches and pivot point formations, which can be set to trigger at different frequencies based on user preference.

How It Works

Input Flexibility: Users can adjust various settings like the length of trend lines and pivot points, enabling or disabling specific features like marking pivots, and managing alert settings directly from the indicator’s input panel.

Dynamic Analysis: By analyzing the price action relative to the calculated trend lines and pivot points, the indicator dynamically identifies potential trend reversals, continuations, and significant price levels.

Visualization: It plots trend lines and marks support and resistance levels directly on the chart, with options to extend these lines and add labels for better clarity. Violated trend lines can be visually differentiated by changing their style and width.

Practical Application

Trend Line Strategy: Traders can use the trend lines to determine the strength of the current market trend and to spot potential reversal points.

Support and Resistance Strategy: By marking where the price has historically faced resistance or found support, traders can plan entry and exit points, set stop-loss orders, or identify breakout opportunities.

Pivot Points Strategy: Pivot points serve as vital indicators for intraday trading or long-term trend analysis, providing insights into potential support and resistance levels.

Customization and Alerts

Custom Alerts: Traders can set alerts for when the price crosses trend lines or when new support or resistance levels are formed, helping them stay informed of critical market movements without having to continuously monitor the charts.

Visual Customization: Users can personalize the appearance of trend lines and labels, choosing from a variety of colors and styles to match their chart setup or preferences.

"Johnny's Trend Lines, Supports and Resistances" is an essential tool for traders who rely on technical analysis, offering detailed insights and real-time updates on market conditions, trend strength, and potential price barriers.

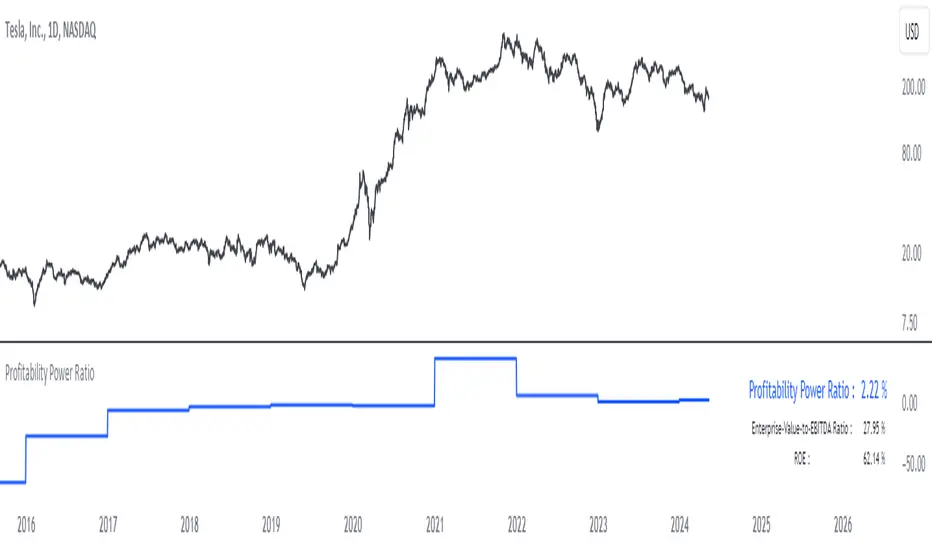

Profitability Power RatioProfitability Power Ratio

The Profitability Power Ratio is a financial metric designed to assess the efficiency of a company's operations by evaluating the relationship between its Enterprise Value (EV) and Return on Equity (ROE). This ratio provides insights into how effectively a company generates profits relative to its equity and overall valuation.

Qualities and Interpretations:

1. Efficiency Benchmark: The Profitability Power Ratio serves as a benchmark for evaluating how efficiently a company utilizes its equity capital to generate profits. A higher ratio indicates that the company is generating significant profits relative to its valuation, reflecting efficient use of invested capital.

2. Financial Health Indicator: This ratio can be used as an indicator of financial health. A consistently high or improving ratio over time suggests strong operational efficiency and sustainable profitability.

3. Investment Considerations: Investors can use this ratio to assess the attractiveness of an investment opportunity. A high ratio may signal potential for good returns, but it's important to consider the underlying reasons for the ratio's level to avoid misinterpretation.

4. Risk Evaluation: An excessively high Profitability Power Ratio could also signal elevated risk. It may indicate aggressive financial leveraging or unsustainable growth expectations, which could pose risks during economic downturns or market fluctuations.

Interpreting the Ratio:

1. Higher Ratio: A higher Profitability Power Ratio typically signifies efficient capital utilization and strong profitability relative to the company's valuation.

2. Lower Ratio: A lower ratio may suggest inefficiencies in capital allocation or lower profitability relative to enterprise value.

3. Benchmarking: Compare the company's ratio with industry peers and historical performance to gain deeper insights into its financial standing and operational efficiency.

Using the Indicator:

The Profitability Power Ratio is plotted on a chart to visualize trends and fluctuations over time. Users can customize the color of the plot to emphasize this metric and integrate it into their financial analysis toolkit for comprehensive decision-making.

Disclaimer: The Profitability Power Ratio is a financial metric designed for informational purposes only and should not be considered as financial or investment advice. Users should conduct thorough research and analysis before making any investment decisions based on this indicator. Past performance is not indicative of future results. All investments involve risks, and users are encouraged to consult with a qualified financial advisor or professional before making investment decisions.

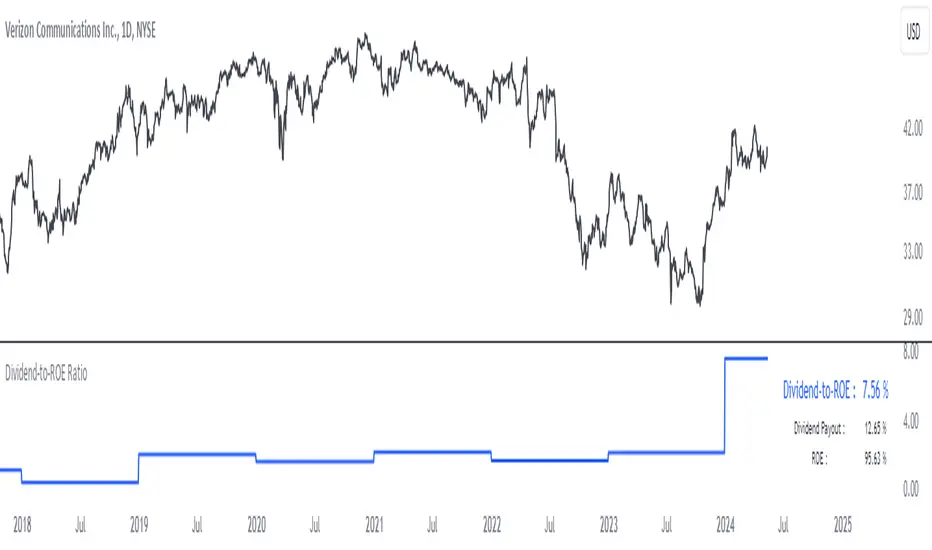

Dividend-to-ROE RatioDividend-to-ROE Ratio Indicator

The Dividend-to-ROE Ratio indicator offers valuable insights into a company's dividend distribution relative to its profitability, specifically comparing the Dividend Payout Ratio (proportion of earnings as dividends) to the Return on Equity (ROE), a measure of profitability from shareholder equity.

Interpretation:

1. Higher Ratio: A higher Dividend-to-ROE Ratio suggests a stable dividend policy, where a significant portion of earnings is returned to shareholders. This can indicate consistent dividend payments, often appealing to income-seeking investors.

2. Lower Ratio: Conversely, a lower ratio implies that the company retains more earnings for growth, potentially signaling a focus on reinvestment for future expansion rather than immediate dividend payouts.

3. Excessively High Ratio: An exceptionally high ratio may raise concerns. While it could reflect a generous dividend policy, excessively high ratios might indicate that a company is distributing more earnings than it can sustainably afford. This could potentially hinder the company's ability to reinvest in its operations, research, or navigate economic downturns effectively.

Utility and Applications:

The Dividend-to-ROE Ratio can be particularly useful in the following scenarios:

1. Income-Oriented Investors: For investors seeking consistent dividend income, a higher ratio signifies a company's commitment to distributing profits to shareholders, potentially aligning with income-oriented investment strategies.

2. Financial Health Assessment: Analysts and stakeholders can use this ratio to gauge a company's financial health and dividend sustainability. It provides insights into management's capital allocation decisions and strategic focus.

3. Comparative Analysis: When comparing companies within the same industry, this ratio helps in benchmarking dividend policies and identifying outliers with unusually high or low ratios.

Considerations:

1. Contextual Analysis: Interpretation should be contextualized within industry standards and the company's financial history. Comparing the ratio with peers in the same sector can provide meaningful insights.

2. Financial Health: It's crucial to evaluate this indicator alongside other financial metrics (like cash flow, debt levels, and profit margins) to grasp the company's overall financial health and sustainability of its dividend policy.

Disclaimer: This indicator is for informational purposes only and does not constitute financial advice. Investors should conduct thorough research and consult with financial professionals before making investment decisions based on this ratio.

CAPEX RatioUnderstanding the CAPEX Ratio: An Essential Financial Metric

Introduction

In the world of finance, understanding how companies allocate their resources and reinvest their earnings is crucial for investors and analysts. One fundamental metric used to assess a company's investment behavior is the CAPEX Ratio. This article delves into what the CAPEX Ratio signifies, its advantages, and how to interpret its implications.

What is the CAPEX Ratio?

The CAPEX Ratio, short for Capital Expenditure Ratio, is a financial indicator that measures the proportion of a company's capital expenditures (CAPEX) relative to various financial metrics such as revenue, free cash flow, net income, or total assets. CAPEX represents investments made by a company to acquire or maintain its physical assets.

Interpreting the Results

Each variant of the CAPEX Ratio provides unique insights into a company's financial strategy:

• CAPEX to Revenue Ratio: This ratio shows what portion of a company's revenue is being reinvested into capital investments. A higher ratio might indicate aggressive expansion plans or a need for infrastructure upgrades.

• CAPEX to Free Cash Flow Ratio: By comparing CAPEX with free cash flow, this ratio reveals how much of a company's available cash is dedicated to capital investments. It helps assess financial health and sustainability.

• CAPEX to Net Income Ratio: This ratio measures how much of a company's net income is being channeled back into capital expenditures. A high ratio relative to net income could signal a company's commitment to growth and development.

• CAPEX to Total Assets Ratio: This metric assesses the proportion of total assets being allocated towards capital expenditures. It provides a perspective on the company's investment intensity relative to its overall asset base.

Advantages of Using CAPEX Ratios

• Insight into Investment Strategy: Helps investors understand where a company is directing its resources.

• Evaluation of Financial Health: Indicates how efficiently a company is reinvesting profits or available cash.

• Comparative Analysis: Enables comparisons across companies or industries to gauge investment priorities.

How to Use the CAPEX Ratio

• Comparative Analysis: Compare the CAPEX Ratios over time or against industry peers to spot trends or outliers.

• Investment Decision-Making: Consider CAPEX Ratios alongside other financial metrics when making investment decisions.

Conclusion

In conclusion, the CAPEX Ratio is a valuable financial metric that offers deep insights into a company's investment behavior and financial health. By analyzing different variants of this ratio, investors and analysts can make informed decisions about a company's growth prospects and financial stability.

Correlated Movement Indicator V2Hello!

This script was briefly known as as Bing Chilling. I converted this to Pine Script V5 to ensure compliance with publishing requirements.

This script tracks RSI and inserts an indicator when correlated movement is detected. Proximity of current tick to indicator origin tick determines freshness of the indicator.

DO NOT sit on the indicator for a long time. This is not a magic solution. It is very accurate but, not always precise. Ensure that you use other factors to determine the relevance of the indicator on current tick. This script can technically be used on any security/commodity/currency. Your Mileage May Vary! Proceed with caution as always.

General Workflow:

Look at proximity to where the flag is placed, general volatility, and other indicators and you can potentially determine the direction/strength. Not always the duration. The indicator could be for 30s, 1hr, 1 day, or whatever the market feels like. It depends on precision/quantity of pricing data. ex. 30min tick rate pricing vs. 1 day tick rate pricing will change the scope.

So if the time scope shows all sell from 1 week -> 3 months except for a couple recent buy indicators on the day, then it may be a bad call long term but, might be good for a short term play. Very volatile. Careful.

If it was all green with long term indicators such as 1 month -> 1 year, then it looks more like a buy and forget type strategy.

If it's all green with a recent red then you can try and figure out what the relative the bottom is so you can buy for long term at a slightly more favorable price.

Flip all that for shorting. I highly recommend AGAINST shorting since the stakes are very different and usually involves taking out what is essentially a loan to bet against the market.

This script pairs nicely with the top pick indicator when you search "Heiken Ashi". I use that to determine peaks and pits to better guess a good time to open a position.

This should be used alongside other indicators. Good for short term day trading and long term hold and forget. (Don't actually forget. Set some alerts periodically.)

Please use caution. Please do not take what I've said here as fact and diamond pepe hands bet all on green to the moon. This, like all the other strategies and indicators on this site, are used as tools to inform you about potential and to categorize/depict data in a more human recognizable way. If you have access to a paper account try there first.

Happy trading!

- Zetsu

Engulfing CandlesThis script serves as the "Engulfing Candles" indicator in TradingView. Here's what it does:

- It identifies bullish candlestick patterns where the current candle's high is lower than the previous candle's high, the current candle's low is higher than the previous candle's low, the current candle's close is higher than the previous candle's close, and the current candle's open is higher than the previous candle's open. It also identifies bearish candlestick patterns where the conditions are reversed.

- The indicator colors bullish candles in a specific color (Yellow Green) to visually highlight the bullish pattern, and colors bearish candles in another color (Purple pink) to visually highlight the bearish pattern.

- Additionally, it triggers an alert when either the bullish or bearish triangle shape appears, notifying traders with the message "A Southern Star Shadows pattern has appeared!"