Combo Backtest 123 Reversal & D_DSP (Detrended Synthetic Price) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Detrended Synthetic Price is a function that is in phase with the

dominant cycle of real price data. This DSP is computed by subtracting

a half-cycle exponential moving average (EMA) from the quarter cycle

exponential moving average.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

Oscillators

TradingView Alerts to MT4 MT5 + dynamic variables NON-REPAINTINGAccidentally, I’m sharing open-source profitable Forex strategy. Accidentally, because this was aimed to be purely educational material. A few days ago TradingView released a very powerful feature of dynamic values from PineScript now being allowed to be passed in Alerts. And thanks to TradingConnector, they could be instantly executed in MT4 or MT5 platform of any broker in the world. So yeah - TradingConnector works with indices and commodities, too.

The logic of this EURUSD 6h strategy is very simple - it is based on Stochastic crossovers with stop-loss set under most recent pivot point. Setting stop-loss with surgical precision is possible exactly thanks to allowance of dynamic values in alerts. TradingConnector has been also upgraded to take advantage of these dynamic values and it now enables executing trades with pre-calculated stop-loss, take-profit, as well as stop and limit orders.

Another fresh feature of TradingConnector, is closing positions only partly - provided that the broker allows it, of course. A position needs to have trade_id specified at entry, referred to in further alerts with partial closing. Detailed spec of alerts syntax and functionalities can be found at TradingConnector website. How to include dynamic variables in alert messages can be seen at the very end of the script in alertcondition() calls.

The strategy also takes commission into consideration.

Slippage is intentionally left at 0. Due to shorter than 1 second delivery time of TradingConnector, slippage is practically non-existing. This can be achieved especially if you’re using VPS server, hosted in the same datacenter as your brokers’ servers. I am using such setup, it is doable. Small slippage and spread is already included in commission value.

This strategy is NON-REPAINTING and uses NO TRAILING-STOP or any other feature known to be faulty in TradingView backtester. Does it make this strategy bulletproof and 100% success-guaranteed? Hell no! Remember the no.1 rule of backtesting - no matter how profitable and good looking a script is, it only tells about the past. There is zero guarantee the same strategy will get similar results in the future.

To turn this script into study so that alerts can be produced, do 2 things:

1. comment “strategy” line at the beginning and uncomment “study” line

2. comment lines 54-59 and uncomment lines 62-65.

Then add script to the chart and configure alerts.

This script was build for educational purposes only.

Certainly this is not financial advice. Anybody using this script or any of its parts in any way, must be aware of high risks connected with trading.

Thanks @LucF and @a.tesla2018 for helping me with code fixes :)

On Balance Volume Oscillator Strategy [QuantNomad]Looking for the way to use OBV Oscillator in a strategy.

Here is my first try. I just enter to position of a cross of 2 emas based on OBV.

Here is my original oscillator indicator:

Combo Backtest 123 Reversal & Cueing Off Sup/Res Levels This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Cueing Off Support And Resistance Levels, by Thom Hartle

modified by HPotter for trade signals.

The related article is copyrighted material from Stocks & Commodities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Confluence This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is modified version of Dale Legan's "Confluence" indicator written by Gary Fritz.

================================================================

Here is Gary`s commentary:

Since the Confluence indicator returned several "states" (bull, bear, grey, and zero),

he modified the return value a bit:

-9 to -1 = Bearish

-0.9 to 0.9 = "grey" (and zero)

1 to 9 = Bullish

The "grey" range corresponds to the "grey" values plotted by Dale's indicator, but

they're divided by 10.

WARNING:

- For purpose educate only

- This script to change bars colors.

VRSI-MARSI StrategyI wanted to create an indicator which resembles price movement, aside to volume movement.

The "yellow-blue" line is the MA(5) of the RSI (9) of closing price.

The "orange" line is the MA(5) of the RSI (9) of Volume .

(Default plot of RSI and VRSI is not visible but can be made visible ("Settings" > "Style" > set "Opacity" of "RSI & VRSI"))

The Long (Buy) condition is triggered when the MA(5) of the RSI (9, close) goes up.

The Short (Sell) condition is triggered when the MA(5) of the RSI (9, close) goes down.

Comparing the price movement with the "orange" Volume line helps to spot a possible trend change,

for example when price goes up and an ascending Volume line starts to flatten or starts descending,

this could be a sign that the Bullish trend is weakening, predicting a possible trend change.

Or, when for example a downwards price movement is accompanied with a rising Volume line, this can be a sign of large Bearish power.

Because it still is a RSI indicator, the midline (50), and Oversold/Overbought area's (20-30 & 70-80) are important to watch, especially the MARSI!

A second strategy is made (VRSI-MARSI Strategy 2) where the Long/Short condition is triggered when "MA RSI (close) - MA RSI ( Volume )" crosses.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------

The Long & Short entries, as well as the Entry Close are visible 1 bar after the trigger.

When the blue line changes in a yellow line (and vice versa) it will show a candle earlier (see yellow dashed lines = (1)).

Also, the condition is fulfilled when the candle closes (2), but the order doesn't take place in the same bar, but the next (3).

Because this is a strategy the "actual Order" will not take place at the "Close" of the candle (2), but at the "Open" at the NEXT candle (3).

I also have this strategy as a study (A+B), where the "Buy" & "Sell" shows a candle earlier.

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------

The entries are default 5% of equity, without pyramiding, which already gives large profits.

A large part of the profit is because of the Entry Close of the Long & Short entries.

You can easily turn these off (Settings > Inputs) to see what profit the strategy gives without Entry Close.

Here they are disabled:

-------------------------------------------------------------------------------------------------------------------------------------------------------------------------

More information available in the script ;-)

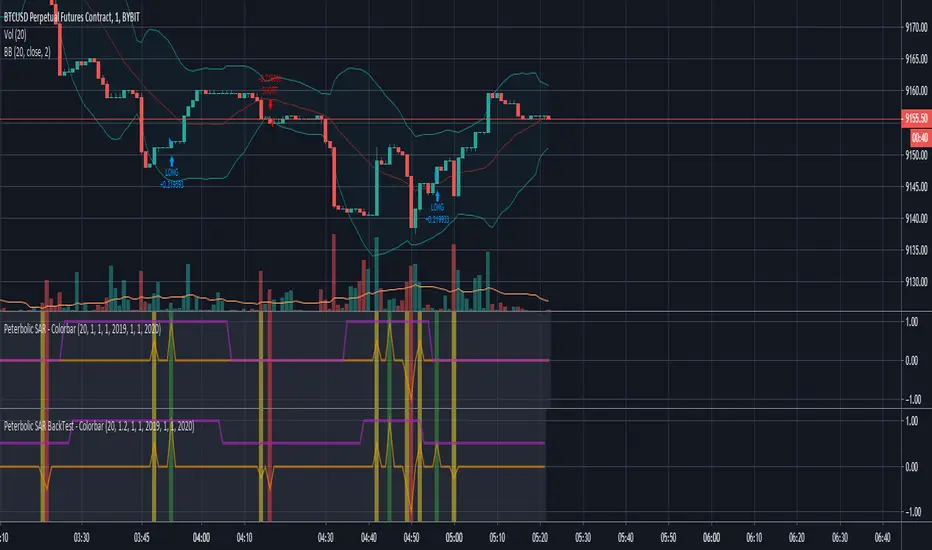

PB SAR BackTest - ColorbarIndicator with buy/sell alerts for setup/trigger conditions

Built upon Peterbolic SAR current version as of publishing

SuperTrend BacktesterThis is a backtesting script for the famous Super Trend.

Features

- Custom Date Range

- Custom Targets and Risks

Requested by Dlatrella

Combo Backtest 123 Reversal & Comparative Relative Strength This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Comparative Relative Strength Strategy for ES

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Commodity Selection Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Commodity Selection Index ("CSI") is a momentum indicator. It was

developed by Welles Wilder and is presented in his book New Concepts in

Technical Trading Systems. The name of the index reflects its primary purpose.

That is, to help select commodities suitable for short-term trading.

A high CSI rating indicates that the commodity has strong trending and volatility

characteristics. The trending characteristics are brought out by the Directional

Movement factor in the calculation--the volatility characteristic by the Average

True Range factor.

Wilder's approach is to trade commodities with high CSI values (relative to other

commodities). Because these commodities are highly volatile, they have the potential

to make the "most money in the shortest period of time." High CSI values imply

trending characteristics which make it easier to trade the security.

The Commodity Selection Index is designed for short-term traders who can handle

the risks associated with highly volatile markets.

WARNING:

- For purpose educate only

- This script to change bars colors.

Stochastic CCI BF 🚀Simply a Stochastic RSI and CCI mix with a Rate of Change filter to stay out of choppy sideways markets.

SIGNALS

For a long signal we need both the CCI above 0 and the stochastic line to be higher than the last candle.

For a short signal we need both the CCI below 0 and the stochastic line to be lower than the last candle.

INSTRUCTIONS

Pay attention to the background color.

Green = go long

Red = go short

White = no trade

RISK

We use a simple 3% stop loss.

If we get stopped out, we wait for the next signal before re-entering.

Tested on XBTUSD BitMex Daily chart.

BandPass EOS - 1hThis is a strategy i made for EOS

Opens a long position if the PB line (the red line in the oscillator) crossover the low of the band, the zero line or the top of the band.

If the PB line makes a crossunder in the top of the band, the zero line or the bottom of the band it closes the long position and immediately opens a short position.

Also, the PB value must be higher than 5 candles before if it is a long position and PB must be lower than 5 candles before to open a short position

I got the BandPass Script from www.tradingview.com and made some changes in the configs to adapt the strategy.

If someone has any doubt i can answer below

Pivot Point Reversal + RSI StrategyThis strategy joins the Pivot Reversal strategy with the RSI indicator.

We check RSI level at the pivot point level and only if RSI condition is satisfied we update levels for stop orders.

The strategy works pretty good for crypto, 30m, 1h, 2h timeframes.

Easy to Use Stochastic + RSI StrategyA simple strategy that yields some great results.

CODE VARIABLES

LINE 2 - Here you can change your currency and amount you want to invest on each entry.

LINE 10/11/12 - Here we establish what date we want to start backtesting from. Simply change the defval on each line to change the date (In the code below we start on Jan 1st, 2014).

LINES 19 through 27 - Here we set our Stochastic and RSI sensitivity (Currently %K = 14, %D = 3, RSI = 14). Change these to your preference.

LINE 39/41 - Here we execute our orders (Currently set when %K crosses %D under the 20 value and RSI is less than 50 to BUY, %K crosses %D above the 80 value and RSI is greater than 60 to SELL). Change these to your preference.

NOTE: As a beginner you may not want to short stock, therefore LINE 6 was added to only allow long positions.

I didn't overlay the RSI value over the Stochastics because it was too cluttered. Just add the RSI indictor seperately to your layout.

As always, couple this with trend following and exit/entry rules to make the profitability even higher!

Cheers!

Combo Backtest 123 Reversal & EMA & Volume WeightingThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from Stocks & Commodities 2009 Oct

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & DMI & Moving Average This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from Stocks & Commodities Aug 2009

WARNING:

- For purpose educate only

- This script to change bars colors.

Easy to Use 50/100/200 Day Moving Average StrategyWhenever you see someone publish a chart or idea, what's the one thing you almost always see? Moving Averages!

Many investors focus on these indictors solely as entry and exit points, so here's an easy to manipulate strategy to backtest and see if this is feasible on your security.

CODE VARIABLES

LINE 2 - Here you can change your currency and amount you want to invest on each entry.

LINE 8/9/10 - Here we establish the 50 (Fast), 100 (Medium) and 200 (Slow) day variables. These can be adjusted to your choosing.

LINE 13/14/15 - Here we establish what date we want to start backtesting from. Simple change the defval on each line to change the date (In the code below we start on Jan 1st, 2010).

LINE 20/23 - Here, within the crossover and crossunder functions, we set which MA's must cross to enter and exit a trade. Below we have the 50 day moving above and under the 200 day. Simple change the variables to FastMA, MediumMA and SlowMA to your choosing.

NOTE: As a beginner you may not want to short stock, therefore LINE 5 was added to only allow long positions.

Hope this helps, from one beginner to another.

Cheers!

[BACKTEST]Traders Dynamic Index Indicator Alert by JustUncleLBy request, this script is a "strategy" version of my "Traders Dynamic Index Indicator Alert" script, made available for backtesting to help find optimal trade settings for a particular asset.

Easy to Use MACD+RSI Strategy

BEGINNERS REJOICE!

Easy to use strategy test using MACD with RSI as a confirming indicator. The code is structured to make it easy to manipulate the variables to your choosing.

EASY TO CHANGE CODE VARIABLES

LINE 2 = Change the amount you invest every trade and the currency

LINE 8/9/10 = Change the defval of each of these lines to backtest from a certain date

LINE 16/17/18 = Change the MACD sensitivity by changing the defval on each line

LINE 21 = Change the value after close toadjust the sensitivity of the RSI

LINE 37/39 = Change/remove the < and > variables for macdLine and rsivalue after the crossover/crossunder to adjust your buying point further.

As a beginner you may not feel comfortable with shorting stocks, therefore LINE 5 was added to only allows long positions.

Funny how a simple indicator can return such a high profitability. Couple this with some trend/exit strategies and you'll have something really special!

REAL STRATEGY : Dow_Factor_MFI/RSI_DVOG_StrategyI'm actually one of those who think it's more important to extract clues from indicators than strategy, but I wanted to test the data about the probability and dow factor I've shared for a long time.

Usually, Bitcoin is used as an eye stain for strategy success, since the graph has increased significantly from the beginning.

To prevent this, I used a commission and in the last lines of document I shared Bitmex's Bitcoin and Ethereum 1W test results.

I don't think there's a factor to repaint. ( Warn me if u see or observe )

I considered Bitcoin because I found working with liquid parities much more realistic.

Ethereum and Bitmex have been featured as a spot and may soon find a place at the CME , so I've evaluated the Ethereum .

But since the Ethereum Bitmex was also spot new, I deleted results that were less than 10 closed trades.

Since the Dow Theory also looks at the harmony in the indices, just try it in the Cryptocurrency market.

Use as indicator in other markets. Support with channels, trend lines with big periods and other supportive indicators.

And my personal suggestion : Use this script and indicator TF : 4H and above.

Specifications :

Commission. ( % 0.125 )

Switchable Methods ( Relative Strength Index / Money Flow Index )

Alarms. (Buy / Sell )

Position closure when horizontal market rates weighs.

Progressive gradual buy/sell alarms.

Clean code layout that will not cause repaint. (Caution : source = close )

Switchable barcolor option (I / 0 )

*****Test results :*****

drive.google.com

Summary:

It was a realistic test.

It has achieved great success in some markets, but as I mentioned earlier, use it only to gain insight into the price movements of cryptos.

Use as indicator in other markets.

This code is open source under the MIT license. If you have any improvements or corrections to suggest, please send me a pull request via the github repository : github.com

Stay tuned ! Noldo.

Strategy based on the principles of Price ActionIt is considered the percentage of candles with low and high closure for a certain period. Then, a moving average is built from these values. When the moving average of the ratio of tall candles to low candles is greater than the ratio of low candles to high, then long (that is, when the green line crosses the red). And vice versa - a condition for short. It also works on crypto with other settings. Idea for improvement: you can make partial exit by taking, at certain profit levels, the chart will be more stable. Result with a commission of 0.004% You can create an optimizer, and use this strategy on any liquid asset. (Sorry for google translator)