X-Force Selector中文說明

X-Force 篩選者 是基於 Mark Minervini 概念設計的強勢標的篩選指標,旨在幫助交易者捕捉市場中的極端強勢標的。此指標運用多重篩選條件,使交易者能在價格達到特定關鍵位置時精準進場,專注於上漲動能強勁、突破阻力較小的標的。

指標篩選條件

100% 關鍵價位:當價格位於365根K棒的最低點的100%之上時,顯示該標的處於強勢區域,具備顯著的上漲動能。

25% 高點價位:同時,當價格位於365根K棒的高點以下25%之上時,代表該標的上方阻力較小,是一個潛在的突破信號。

滿足以上兩個條件的標的才會被視為進場機會,這符合 Minervini 所強調的「專注於強勢標的」的策略。Minervini 的概念強調當標的價格突破關鍵價位時,可能帶來更高的回報潛力,且風險相對較小。

加密貨幣與時間周期的應用

在加密貨幣交易中,1小時到4小時的小時間框架適合使用100%、66%、33%這些百分比範圍參數,以反映市場的高波動特性。對於更短周期,建議進一步縮小百分比,以提高指標對短期波動的敏感度,並增強篩選結果的準確性。

靈活的篩選與戰警風格

此指標的設計結合了 Minervini 的概念和戰警風格,旨在精準鎖定極具潛力的突破標的。X-Force 篩選者適合追隨趨勢的交易者,尤其是熱衷於 Mark Minervini 策略的投資者,使交易者能夠專注於市場中最具上漲動能的標的,實現更精確的進場決策。

English Description

X-Force Selector is a powerful trend-filtering indicator inspired by Mark Minervini’s trading concepts, designed to help traders capture assets with extreme strength in the market. By applying multiple filtering criteria, this indicator enables precise entry decisions when price reaches specific key levels, focusing on assets with strong upward momentum and minimal resistance.

Indicator Selection Criteria

100% Key Price Level: When the price is above 100% of the lowest low over the past 365 bars, it indicates the asset is in a strong zone with substantial upward momentum.

25% High Price Level: Additionally, when the price is within 25% below the 365-bar high, it signals reduced resistance above, indicating potential for a breakout.

Assets meeting both criteria are considered potential entry opportunities, aligning with Minervini's strategy of “focusing on strong assets.” Minervini’s concept emphasizes capturing high-potential assets as they break through critical levels, aiming for higher returns with relatively low risk.

Application to Cryptocurrency and Timeframes

In cryptocurrency trading, shorter timeframes such as 1H to 4H are well-suited for the 100%, 66%, and 33% thresholds, reflecting the high volatility of crypto markets. For even smaller timeframes, it is recommended to reduce these percentages to enhance the indicator’s sensitivity to short-term fluctuations, improving the accuracy of filtered results.

Flexible Filtering with a Battle-Ready Style

With a design inspired by Minervini's concepts and a battle-ready scanning approach, the X-Force Selector precisely locks onto high-potential breakout candidates. This indicator is ideal for trend-following traders, especially those applying Mark Minervini’s strategies, enabling them to concentrate on assets with the strongest upward momentum for precise entry decisions.

Z-VALUE

LV Stock QualityCritical financial and technical values are listed in the table.

PIOTROSKI_F_SCORE (expect. >5) -> The Piotroski score is a discrete score between zero and nine that reflects nine criteria used to determine the strength of a firm's financial position. The Piotroski score is used to determine the best value stocks, with nine being the best and zero being the worst. Having a score bigger than 5 is a good sign for the strength of a firm's financial position

ROE (expect. >11) --> Return on equity (ROE) is a measure of a company's financial performance. It is calculated by dividing net income by shareholders' equity. Because shareholders' equity is equal to a company’s assets minus its debt, ROE is a way of showing a company's return on net assets. A “good” ROE will depend on the company’s industry and competitors.

EPS_GROWTH (expect. >11) --> This indicator is calculated as the percentage change in Basic earnings per share for one year. This indicator reflects the growth rate of a company's basic profit per share outstanding for one year. It is calculated based using only common shares. An increase in EPS growth may signal that a company is becoming more profitable and efficient in its operations. A decline in EPS growth may signal that a company is spending more or losing business share. EPS growth should be viewed alongside other metrics like revenue and costs.

CURRENT_RATIO (expect. >1.25) --> The current ratio measures a company’s ability to pay current, or short-term, liabilities (debt and payables) with its current, or short-term, assets (cash, inventory, and receivables). Current ratios over 1.00 indicate that a company's current assets are greater than its current liabilities, meaning it could more easily pay of short-term debts.

OPERATING_MARGIN(expect. >11) --> The operating margin measures how much profit a company makes on a dollar of sales after paying for variable costs of production, such as wages and raw materials, but before paying interest or tax.

RETURN_CAPITAL (expect. >11) --> Return of capital (ROC) is a payment that an investor receives as a portion of their original investment and that is not considered income or capital gains from the investment.

ALTMAN_Z_SCORE (expect. >1.8) --> The Altman Z-score is the output of a credit-strength test that gauges a publicly traded manufacturing company's likelihood of bankruptcy. An Altman Z-score close to 0 suggests a company might be headed for bankruptcy, while a score closer to 3 suggests a company is in solid financial positioning.

REVENUE_GROWTH (expect. >11) --> Quarterly revenue growth is an increase in a company's sales in one quarter compared to sales of a different quarter. Comparing a company's financials from one period to another gives a clear picture of its revenue growth rate and can help investors identify the catalyst for such growth.

SUSTAINABLE_GROWTH (expect. >11) --> The sustainable growth rate (SGR) is the maximum rate of growth that a company or social enterprise can sustain without having to finance growth with additional equity or debt. In other words, it is the rate at which the company can grow while using its own internal revenue without borrowing from outside sources.

DEBT TO INCOME (expect. <0.4) --> A debt-to-income (DTI) ratio is a financial metric used by lenders to determine your borrowing risk. Your DTI ratio represents the total amount of debt you owe compared to the total amount of money you earn each month.

NORMALIZED ATR (expect. <8, W) --> The Normalized Average True Range (Normalized ATR) is an indicator used to measure market volatility by normalizing the average true range values. It does this by dividing the Average True Range (ATR) by the asset's closing price, converting it into a percentage. This normalization allows for the comparison of volatility levels across different securities or market conditions, regardless of the asset's price levels. The Normalized ATR helps traders to adjust their strategies based on relative volatility, rather than absolute price movements.

INDEX expect. EMA10>EMA20 --> it is expected to have EMA 10 > EMA 20 in weekly basis graph. It is known that having a strong trend in index will also increases chance of strong trend on stock levels. You need to select INDEX Market of stock via settings.

M. RELATIVE STRENGTH expect. MRS>1 --> Stan Weinstein uses the Mansfield RS indicator as another relative strength indicator. The indicator measures the variation in the 52-week ratio of stock and market.

VOLUME CHANGE (expect. >30) --> Having an increase on volume comparing to previous week can be a good sign if it occurs at the same time of breakout.

PRICE CHANGE (expect. >5 and <20) --> Having an increase on price comparing to previous week can be a good sign if it occurs at the same time of breakout.

It is better to look on weekly basis graphs.

CoffeeShopCrytpo Dynamic PPIIn the financial world, the Producer Price Index (PPI) is often used to measure how domestic products are performing over time, indicating the health of the market. Domestic products refer to goods and services that are produced within a specific country’s borders. However, in this indicator, we’ve taken that idea and applied it directly to financial assets, allowing traders to see how an asset is performing relative to its own base value over a given period of time.

Here, the asset’s base value is represented as 100%. When the asset performs above 100%, it's considered to be in a buyer's market—indicating strength and demand. Conversely, if the value dips below 100%, it's operating below its base value, signaling a potential seller's market.

Why This Matters:

This indicator not only converts an asset’s performance into a PPI-style calculation, but it also visualizes price movements as price candles. This dual perspective is crucial, because even if the asset’s performance is over 100%, the closing price might still fall below that threshold—adding nuance to your understanding of market conditions.

Key Features of the Indicator:

Bullish and Bearish Convergence Levels: These levels show whether the market leans bullish or bearish. If the Bullish Convergence level is higher than the Bearish one, the market is bullish, and vice versa. Importantly, these levels can signal shifts in market strength, regardless of where the PPI candles are positioned.

If Bullish Convergence is rising below Bearish, the bearish market is weakening and bullish pressure is growing. Conversely, if Bearish Convergence is falling above Bullish, the bearish side is losing ground.

Market Strength Visualizations:

Strong Bullish Market: Bullish Convergence is higher than Bearish, and it’s still rising.

Strong Bearish Market: Bearish Convergence is above Bullish, and it's climbing.

Weak Bullish Market: Bullish Convergence is above Bearish, but the PPI closes below Bullish Convergence.

Weak Bearish Market: Bearish Convergence is above Bullish, but the PPI closes above Bullish Convergence

Pullbacks:

Bullish Pullback: In a strong bullish market, the PPI shows lower closes below the Bullish Convergence.

Bearish Pullback: In a strong bearish market, the PPI shows higher closes above the Bullish Convergence.

Divergences:

Higher Price, Lower or Flat PPI: This indicates that while the asset’s price is rising, its underlying performance (relative to the PPI’s 100% base level) is not keeping up. Essentially, the asset is reaching new price highs, but its strength or "efficiency" of growth is weakening.

The PPI is designed to show the "return" of an asset's performance relative to its historical movement, so when it lags behind price, it suggests that the price rise may not be sustainable.

When you observe the first high of the PPI level above the bullish convergence level, followed by a second high of the PPI below the bullish convergence level in a bullish market, this creates a divergence.

Example of Divergence in image:

1. First High of PPI Above the Bullish Convergence Level:

This suggests strong bullish momentum. The asset’s performance, as measured by the PPI, is in line with or even outperforming price expectations, indicating the market is experiencing a robust bullish trend. The fact that the PPI level is above the bullish convergence line means that the asset is operating well above its base performance (above 100%) and bullish momentum is clearly dominant.

2. Second High of PPI Below the Bullish Convergence Level:

This marks a potential weakening of the bullish momentum. Although the market is still in a bullish state (since bullish convergence remains above bearish), the PPI failing to reach the bullish convergence level suggests that the asset’s performance is not keeping pace with price action or is underperforming relative to its earlier high.

The fact that this occurs while the market is still bullish (bullish convergence is greater than bearish) can signal a possible pullback or a temporary consolidation phase within the larger bullish trend.

What does a divergence mean:

Momentum Weakening: The second high of the PPI being below the bullish convergence line suggests that while prices may still be increasing, the strength behind the move is fading. The asset is not performing as strongly as it did during the first high, and the market’s confidence or momentum might be softening.

Potential Bullish Pullback: This could indicate that a pullback or correction within the larger bullish trend is underway. Traders might be taking profits, or buyers could be losing enthusiasm, causing the asset to stall temporarily. However, because the overall market remains bullish, this doesn’t necessarily mean a full reversal—just a cooling off period.

Caution in New Long Positions: If you see this divergence, it could be a sign to be more cautious about opening new long positions. It suggests that the asset may need to consolidate or correct before resuming its upward trend, and it’s worth waiting for confirmation of renewed momentum before jumping back in.

ATR Settings

Youll notice there are two ATR settings. One for short term and one for long term.

These values are based on your preferential strategy for what you consider to be long and short term.

The final ATR values are calculated against eachother and applied to the Volatility Label at the end of price.

This label shows you the current ATR as well as the previous candle ATR.

Why this is important:

If the short term ATR is greater than the long term ATR, then volatility is rising in the short term greater than the long term.

This gives your label a value greater than 1.0. This means the short term trend is about to move.

If the long term ATR is greater than the short term ATR, there is no volatility in the short term and only long term exists.

This gives you a value of less than 1.0. This means no volatility or ranging market in the short term.

ADA Stock-to-Flow Model (BSP)ADA Stock-to-Flow Model

This script implements a Stock-to-Flow (S2F) model for ADA (Cardano). The Stock-to-Flow ratio is a popular metric used to assess the scarcity of an asset by comparing its current supply (stock) to the rate at which it is being produced (flow). By visualizing the S2F ratio on ADA, this model helps traders and analysts evaluate potential long-term price trends based on supply scarcity.

Key features:

Calculates ADA's Stock-to-Flow ratio dynamically, adjusting for changes in circulating supply and emission rates.

Provides easy-to-read visualizations with adjustable timeframes, making it accessible for both novice and experienced traders.

The Stock-to-Flow model is widely used in analyzing assets like Bitcoin, and this adaptation for ADA gives unique insights into the relationship between its supply and market value. While the model offers a useful perspective on ADA’s potential trajectory, it should be used in conjunction with other tools for a comprehensive market analysis.

CAPE / Shiller PE RatioThe CAPE (Cyclically Adjusted Price-to-Earnings) or Shiller PE ratio is a popular valuation measure used by investors to assess whether a stock or index is over or undervalued relative to its historical earnings. Unlike the traditional P/E ratio, the CAPE ratio smooths earnings over ten years, adjusting for inflation and providing a more stable and long-term view of valuation.

This indicator lets you quickly calculate and visualize the CAPE ratio for any stock on TradingView, helping you make informed decisions about the sustainability of current price levels. With its clear presentation and intuitive setup, you can compare historical CAPE levels and identify potential opportunities for long-term investments or avoid overvalued markets.

Advantages of the CAPE Ratio:

Long-Term Focus : Smooth earnings over ten years, reducing the impact of short-term volatility.

Inflation-Adjusted : Provides a more precise, inflation-adjusted valuation measure over time.

Historical Comparison : Allows for benchmarking against long-term historical averages.

Market Sentiment Indicator : Can highlight overvalued or undervalued markets for long-term investors.

Reduces Noise : Filters out short-term earnings fluctuations, offering a more stable view.

Disadvantages of the CAPE Ratio:

Ignores Recent Earnings : Misses short-term earnings changes, which can affect current valuations.

Outdated Data : Relies on old earnings data that may not reflect recent company performance.

Less Effective for Growth Stocks : May undervalue high-growth stocks focused on future earnings.

Sector Limitations : Works best for broad markets, less so for fast-changing industries.

Debated Predictive Power : It’s unreliable for timing short-term market movements.

In short, the CAPE ratio is excellent for long-term valuation but has limitations for short-term or growth-focused investing.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Leonid's Bitcoin Sharpe RatioThe Sharpe ratio is an old formula used to value the risk-adjusted return of an asset. It was developed by Nobel Laureate William F. Sharpe. In this case, I have applied it to Bitcoin with an adjustable look-back date.

The Sharpe Ratio shows you the average return earned after subtracting out the risk-free rate per unit of volatility (I've defaulted this to 0.02 ).

Volatility is a measure of the price fluctuations of an asset or portfolio. Subtracting the risk-free rate from the mean return allows you to understand what the extra returns are for taking the risk.

If the indicator is flashing red, Bitcoin is temporarily overbought (expensive).

If the indicator is flashing green, Bitcoin is temporarily oversold (cheap).

The goal of this indicator is to signal out local tops & bottoms. It can be adjusted as far as the lookback time but I have found 25-26 days to be ideal.

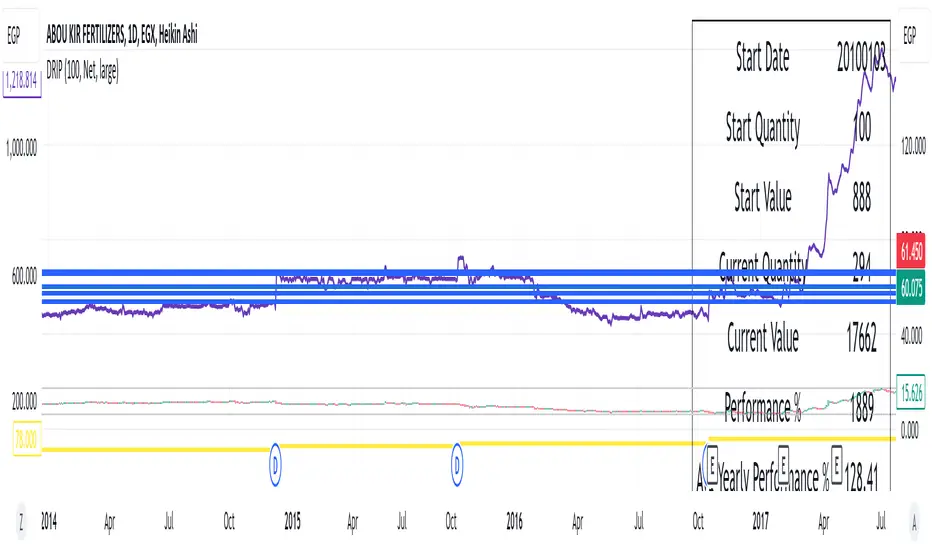

DRIP Yearly PerformanceOverview: The DRIP Yearly Performance indicator is designed for long-term investors using Dividend Reinvestment Plans (DRIP). This script calculates both the total and average yearly performance of an asset, factoring in the reinvestment of dividends over time. It provides key insights into portfolio growth by tracking the number of accumulated units from dividend reinvestment and how this impacts overall performance.

Key Features:

Dividend Reinvestment (DRIP) Calculation: Automatically adjusts the number of units held by reinvesting dividends, enhancing the calculation of total returns.

Custom Start Date: Choose a custom start date to begin tracking performance from a specific time period, allowing for more tailored performance analysis.

Performance Metrics: Displays key metrics such as the initial investment value, current value, total performance percentage, and the average yearly performance, all in an easy-to-read table format.

Visual Representation: Plots accumulated units and overall performance on the chart, with customizable colors for clarity.

Inputs Explained:

Start Quantity: Define the initial number of units (shares) held at the start of the investment.

Dividend Type: Choose between tracking Net or Gross dividends for reinvestment purposes. Net is always better unless you have a special case and you need to base your calculations on gross.

Start Date: Select a custom date to begin tracking performance. This allows users to focus on performance from any historical point.

Table Size: Customize the size of the text in the performance table to suit your visual preferences.

Performance Line Color: Choose the color of the performance plot line that tracks the value of your investment over time.

Accumulator Line Color: Customize the color of the line that tracks the accumulated units (shares) due to reinvested dividends.

Who Can Benefit: This indicator is ideal for long-term investors and dividend growth investors who want to measure their investment returns over time while factoring in the effects of dividend reinvestment.

Use Cases:

Tracking Dividend Impact: See how reinvesting dividends enhances your overall portfolio value.

Custom Performance Analysis: Set a custom start date to analyze performance from a specific point in time.

Visualizing Growth: Use the chart's plots to visually track your growing number of shares (units) and overall performance.

Universal Trend Following Valuation | viResearch Universal Trend Following Valuation | viResearch

Conceptual Foundation and Innovation

The "Universal Trend Following Valuation" script represents a comprehensive approach to trend-following systems. It combines multiple technical indicators and methods to assess market trends, integrating Sharpe, Sortino, and Omega ratios with various moving averages and Z-score calculations. By utilizing advanced statistical tools, the script provides traders with a well-rounded evaluation of trend strength, direction, and potential reversals. The inclusion of Z-scores and custom ratios allows for a more in-depth and accurate market analysis, making it a valuable tool for trend valuation.

Technical Composition and Calculation

This script is built on various performance metrics and trend-following methods. It features ratio calculations, such as Sharpe, Sortino, and Omega, which provide insight into the risk-adjusted performance of assets, helping traders gauge the strength of market trends. Weekly RSI values are smoothed using dema, ema, and median methods to offer a clearer view of trend momentum. Additionally, Z-scores are applied to these ratios and the weekly RSI, offering a standardized assessment of trend deviations from historical performance. A custom scoring system is used to generate a cumulative trend score, highlighting potential market reversals or confirmations.

Key Indicators and Features

The script uses weekly RSI and EMA/Dema smoothing to reduce market noise and produce clearer trend signals. The Sharpe, Sortino, and Omega ratio calculations help assess market performance and volatility, with Z-scores adding another analytical layer. Different moving averages (HMA, DEMA, SMMA) are incorporated to evaluate both short-term and long-term trends, making the script adaptable to various market conditions. Furthermore, the script provides trend confirmation through multiple layers by using indicators like the Supertrend and the Average True Range (ATR) factor to cross-check trends for increased reliability.

Practical Applications

This script is ideal for traders looking to systematically evaluate market trends and effectively position themselves. The combination of advanced statistical tools and customizable moving averages and ratios ensures that the script remains both flexible and powerful. It is particularly useful for confirming trends and highlighting potential reversals, giving traders a reliable signal for either trend continuation or reversals. The inclusion of Sharpe and Sortino ratios allows traders to focus on trends that offer a favorable risk-reward profile.

Advantages and Strategic Value

The "Universal Trend Following Valuation" script offers a detailed, multifaceted approach to trend analysis. Its use of advanced statistical tools provides a more precise evaluation of market trends, making it valuable for both novice and experienced traders. The script reduces noise while ensuring that the core trend signals remain accurate, helping traders make more informed decisions in volatile market conditions.

Summary and Usage Tips

Incorporating the "Universal Trend Following Valuation" into your trading system can significantly enhance your ability to follow and confirm trends. With its customizable parameters and alerts, this script offers a powerful and reliable tool for navigating market volatility and optimizing trade entries and exits. By combining trend-following signals with performance metrics, traders can refine their strategies with increased confidence.

Disclaimer: Backtests are based on past results and are not indicative of future performance.

Stef's Enterprise Value CalculatorI have learned the hard way why Enterprise Value is far more superior than Market Cap. That's why I made this indicator, but more importantly, why I added several features that other similar indicators just don't have. The key thing is to not just show you Enterprise Value of a company (it's true worth) but also the capability to see that line colored in a specific way, with key stats as a neat table, and the ability to chart the key facts that go into Enterprise Value, which are debt and cash.

I'll say it again: Market Cap is not nearly as good as Enterprise Value. Don't get tricked by what Market Cap does NOT show you and instead focus on Enterprise Value. I hope my indicator, and the features you see below, help investors and traders all over the world better understand this.

Here are the key features:

Enterprise Value Indicator Features:

1. Real-Time Enterprise Value (EV) Display: Track the EV of a company directly on your chart, providing a comprehensive measure of its true market value.

2. Custom Color Trends: Customize the color of your EV line based on specific trends you’re monitoring, allowing for personalized and insightful visual analysis.

3. Debt & Cash Visualization: Plot both debt and cash & equivalents on the same chart, offering a clear and concise view of a company’s financial health.

4. Key Metrics Table: View a table displaying essential metrics including:

- Average EV

- Highest EV

- Lowest EV

- MC-EV (Market Cap minus Enterprise Value)

MC-EV Charting: Easily chart MC-EV to understand how much debt a company has relative to its market cap, providing insight into financial leverage and growth potential.

Why MC-EV Matters: This metric is crucial for evaluating a company’s financial risk and operational efficiency, giving you an edge in making informed investment decisions.

Thanks for reading and I hope you find some value in this! More updates to come.

PE Ratio Intrinsic ValueThe "Median PE Ratio and Intrinsic Value" indicator is designed for traders and investors who wish to evaluate the intrinsic value of a stock based on a comparative analysis of Price-to-Earnings (PE) ratios across multiple stocks. This tool not only provides insights into whether a stock is undervalued or overvalued but also allows you to visualize the intrinsic value directly on the chart.

Comparison Across Multiple Stocks:

This indicator calculates the PE ratio for up to five different stocks, allowing you to compare the target stock's valuation against four other same sector companies. By default, the stocks included are Apple (AAPL), Google (GOOG), Microsoft (MSFT), and Amazon (AMZN), but you can customize these symbols to fit your analysis needs.

Dynamic PE Ratio Calculation:

The indicator calculates the PE ratio for each stock by dividing the current price by the earnings per share (EPS). The EPS data is retrieved based on the selected period, which can be one of the following:

FY (Fiscal Year)

FH (Fiscal Half-Year)

FQ (Fiscal Quarter)

TTM (Trailing Twelve Months)

You can easily switch between these periods using the provided input options, enabling a more customized analysis based on your preferred financial timeframe.

Once the PE ratios for the selected stocks are computed, the indicator calculates the average PE ratio. The average value is a robust measure that reduces the influence of outliers and provides a balanced view of market valuation.

The intrinsic value of the stock on the chart is calculated by multiplying its EPS by the median PE ratio of the selected stocks. This gives you an estimate of what the stock should be worth if it were to trade at a fair valuation relative to the chosen peers.

The intrinsic value is plotted directly on the price chart as a step line with breaks. This step line style is chosen to represent changes in intrinsic value clearly, with breaks indicating periods where the calculated value is not valid (e.g., negative intrinsic value). Only positive intrinsic values are displayed, helping you focus on meaningful data.

You can easily customize the stocks analyzed by entering the ticker symbols of your choice. Additionally, the indicator allows you to adjust the timeframe for EPS data, giving you flexibility depending on whether you are focused on long-term trends or shorter financial periods.

How to Use:

Compare the current stock price to the plotted intrinsic value. If the current price is below the intrinsic value, the stock may be undervalued. Conversely, if the price is above the intrinsic value, the stock might be overvalued. By comparing your stock against major market players, you can gauge whether it's trading at a premium or discount relative to other key companies in the sector. Use the period selection (FY, FQ, TTM) to adapt your analysis to different market conditions or earnings cycles, giving you more control over your valuation assessment.

Ideal For:

Long-term Investors looking to assess the intrinsic value of a stock based on comparative analysis.

Fundamental Analysts who want to combine multiple stocks' PE ratios to estimate a fair valuation.

Value Investors interested in finding undervalued opportunities by comparing the market price to intrinsic value.

Grayscale GSOL Solana Financials [NeoButane]This script shows Grayscale's GSOL financials based on the information from their website. Investors and traders like to use financials when making the decision to buy, sell, or hold.

►Usage

This script is specific to GSOL. Investors and traders use financials when making the decision to buy, sell, or hold. How one interprets financials is up to the individual. For example, investors who believe a Solana ETF is coming soon can view the "% Discount / Premium to NAV", which is currently over 600%, and decide not to buy because the premium would collapse if an ETF began trading.

►Configuration

Data select the data you'd like to display.

Show Highest label show the highest value of the entire data set.

Line Color an expression of self.

Extrapolate Data Using Average or Last Known Value Shows a line beyond the dataset, using the average of all past data or the last data point to predict newer data. % Discount / Premium to NAV, Share Premium, and SOL Per Share are supported.

→Data retrieved from Grayscale

AUM assets under management.

NAV net asset value.

Market Price market price of GSOL.

Shares Outstanding number of shares held in the open market.

→Data retrieved from Grayscale, modified by me

% Discount / Premium to NAV the % away NAV is from the market price of GSOL.

Formula: (GSOL - NAV) / NAV

Share Premium the actual $ premium of GSOL to its NAV.

Formula: GSOL - NAV

SOL Per Share the amount of SOL 1 share of GSOL can redeem. This is derived using Kraken's SOLUSD daily close prices.

Formula: Kraken's SOLUSD / NAV

SOL Price Using Market Price Premium the price of SOL if GSOL's market price was "correct" and the SOL Per Share ratio remained the same.

Formula: GSOL / SOL Per Share

►How this works

Grayscale has a spreadsheet of historical data available on their GSOL page. Since financials are not available for OTC:GSOL, I placed all the data into arrays to emulate a symbol's price (y) coordinates. UNIX time for each day, also in an array, is used as the time (x) coordinates. The UNIX arrays and data arrays are then looped to plot as lines, with data y2 being the next data point, making it appear as a continuous line.

Grayscale's GSOL was downloaded spreadsheet and opened in Excel. SOLUSD prices were exported using TradingView export function. The output of information was pasted into Pine Script. For matching up Kraken's SOLUSD prices to each Grayscale's data since GSOL does not trade daily, dates were converted to UNIX and matched with xlookup(). A library or seed will be used in the future for updating.

References

Data retrieved from Grayscale's website 2024/08/04.

www.grayscale.com

Quantity of Solana held by the trust can be seen in their filings. Ctrl + F "Quantity of

SOL "

www.grayscale.com

Q1 2024: www.grayscale.com

The high premium can partly be explained by private placement currently being closed. This means private sales can't dilute share value.

www.etf.com

Stef's Money Supply IndicatorI have been fascinated by the growth in the Money Supply. Well, I think we ALL have been fascinated by this and the corresponding inflation that followed. That's why I created my Money Supply Indicator because I always wanted to chart and analyze my symbols based on the Money Supply. This indicator gives you that capability in a way that no other indicator in this field currently offers. Let me explain:

How does the indicator work?

Chart any symbol, turn on this indicator, and instantly it will factor in the M2 money supply on the asset's underlying price. Essentially, you are seeing the price of the asset normalized for the corresponding rise in the money supply. In some ways, this is a rather unique inflation-adjusted view of a symbol's price.

More importantly, you can compare and contrast the symbol's price adjusted for the rise in the Money Supply vs. the symbol's price without that adjustment by indexing all lines to 100. This is essential for understanding if the asset is at all-time highs, lows, or possibly undervalued or overvalued based on the current money supply situation.

Why does this matter?

This tool provides a deeper understanding of how the overall money supply influences the value of assets over time. By adjusting asset prices for changes in the money supply, traders can see the true value of assets relative to the amount of money in circulation.

What features can you access with this indicator?

The ability to normalize all lines to a starting point of 100 allows traders to compare the performance of the Money Supply, the symbol price, and the symbol price adjusted for the money supply all on one readable chart. This feature is particularly useful for spotting divergences and understanding relative performance over time with a rising or falling Money Supply.

What else can you do?

This is just version 1, and so I'll be adding more features rather soon, but there are two other important features in the settings menu including the following:

• Get the capability to quickly spot the highest and lowest points on the Money Supply adjusted price of your asset.

• Get the capability to change the gradient colors of the line when going up or down.

• Turn on the Brrrrrrr printer text as a reminder of our Fed Overlord Jerome Powell... lol

• Drag this indicator onto your main chart to combine it with your candlesticks or other charting techniques.

Stef's Money Supply Indicator! I look forward to hearing your feedback.

Stock Value RainbowStock Valuation based on Book Value, Dividends, Cashflow, Earnings and Estimates and Money Multiplier

There are many ways to measure stock valuations: some methods are using book value, some are using dividends, some are using cashflow, some are using earnings and some using estimates data. Most of these valuation methods are based on multiplier effect which measure how many times the stock price could expand from their valuation base. This indicator attempts to unify all these measurements using just simple addition of all measurements such as: book value per share, dividend per share, cashflow per share, earning per share, and estimates of earning per share and then using multiplier effect to create beautiful rainbow to see how far the stock has growing up above or below their valuation base. The higher the stock price on rainbow spectrum means it is more expensive and the lower in the rainbow spectrum means it is cheaper. Here is the basic formula explanation:

SV = (BVPS + DPS + CFPS + EPS + EST) * MM

BVPS = Book Value Per Share (Asset - Liability)

DPS = Dividends Per Share

CFPS = Free Cash Flow Per Share

EPS = Earnings Per Share

EST = Estimates of EPS

MM = Money Multiplier (1x, 2x, ... ,10x)

- The gray line represents the stock value SV

- The rainbow above the gray line represents the multiplication factors from 1x, 2x, ..., 10x

- The rainbow below the gray line represents the division factors from 0.8x, 0.6x, ..., 0.2x

Check other script to value stock and index:

- Stock Value Rainbow: script to value stock based on book value, dividend, cash flow, earning and estimates.

- Index Value Rainbow: script to value index based on fed balance sheet and base money supply

- Gold Value Rainbow: script to value gold based on global money supply

- Stock Value US: script to check US stock value

- Stock Value EU: script to check EU stock value

- Stock Value JP: script to check JP stock value

- Stock Value CN: script to check CN stock value

Double FVG-BPR [QuantVue]The Double FVG BPR Indicator is a versatile tool that helps traders identify potential support and resistance levels through the concept of balanced price ranges.

A Balanced Price Range (BPR) is a zone on a price chart where the market has found equilibrium after a period of price imbalance.

It is identified by detecting a Fair Value Gap (FVG) in one direction, followed by an overlapping Fair Value Gap in the opposite direction.

Components of a Balanced Price Range

Fair Value Gap (FVG): A FVG occurs when there is a rapid price movement, creating a gap in the price chart where minimal trading occurs. This gap represents an imbalance between supply and demand.

Bullish FVG: A bullish FVG is identified when the low of a candle is higher than the high of a candle two periods ago, and the close of the previous candle is higher than the high of that same period.

Bearish FVG: A bearish FVG is identified when the high of a candle is lower than the low of a candle two periods ago, and the close of the previous candle is lower than the low of that same period.

Overlapping Fair Value Gap: For a BPR to be formed, an initial FVG must be followed by an overlapping FVG in the opposite direction. This creates a balanced zone where the price has moved up (or down) quickly and then moved down (or up) with similar intensity, suggesting a temporary equilibrium.

The area between the high and low points of these overlapping FVGs forms the BPR. This zone represents a temporary market equilibrium where supply and demand have balanced out after a period of significant price movement in both directions.

How to Use

Support and Resistance Levels: The upper and lower boundaries of the BPR act as dynamic support and resistance levels. Traders can use these levels to place buy and sell orders, anticipating that the price may find support or face resistance within these zones.

Trend Reversal and Continuation: The BPR can signal potential trend reversals or continuations.

If the price moves back into the BPR after a breakout, it may indicate a reversal. Conversely, if the price breaks out of the BPR with strong momentum, it may signal a trend continuation.

Sharpe RatioThe Sharpe Ratio Indicator is a widely-used tool designed to measure the risk-adjusted performance of an asset. The Sharpe Ratio helps investors understand how much excess return they are receiving for the extra volatility endured for holding a riskier asset. By comparing the return of an investment to the risk-free rate and accounting for the volatility of the investment's returns, the Sharpe Ratio provides a clear metric for evaluating the return on investment per unit of risk.

Features:

Calculation Period Input: Allows users to specify the period over which the Sharpe Ratio is calculated, making it flexible and adaptable to various trading strategies and time frames.

Risk-Free Rate Input: Users can set a specific risk-free rate, enabling a customized risk-return analysis based on prevailing market conditions or individual investment preferences.

Daily Returns Calculation: The indicator calculates daily returns, which are used to determine the mean return and standard deviation.

Sharpe Ratio Calculation: The indicator calculates the Sharpe Ratio by dividing the excess return (mean return minus risk-free rate) by the standard deviation of returns and annualizing the result (assuming 252 trading days in a year).

Visual Plot: The Sharpe Ratio is plotted on the chart, with a reference zero line to help users quickly assess whether the asset's returns are favorable relative to the risk-free rate.

How to Use:

Add the Indicator to Your Chart: Copy the script into the Pine Script editor on TradingView and add it to your chart.

Specify the Calculation Period: Adjust the Calculation Period input to match your desired time frame for the Sharpe Ratio calculation.

Set the Risk-Free Rate: Input the current risk-free rate (e.g., the yield on 10-year government bonds) to customize the risk-return analysis.

Interpret the Sharpe Ratio: A higher Sharpe Ratio indicates better risk-adjusted performance, while a ratio below zero suggests that the asset has underperformed relative to the risk-free rate.

Omega RatioThe Omega Ratio Indicator is a powerful tool designed to measure the risk-adjusted performance of an asset. Unlike traditional measures like the Sharpe or Sortino Ratios, the Omega Ratio considers both the frequency and magnitude of returns above and below a specified target return, providing a more comprehensive view of an asset's performance. This makes it an ideal choice for traders and investors seeking to evaluate the probability of achieving a desired return relative to the risk taken.

Features:

Calculation Period Input: Allows users to specify the period over which the Omega Ratio is calculated, making it flexible and adaptable to various trading strategies and time frames.

Target Return Input: Users can set a specific target return, enabling a customized risk-return analysis based on individual investment goals.

Daily Returns Calculation: The indicator calculates daily returns, which are used to determine the cumulative returns above and below the target return.

Omega Ratio Calculation: By dividing the cumulative returns above the target return by the cumulative returns below it, the indicator provides a clear measure of the likelihood of achieving the target return.

Visual Plot: The Omega Ratio is plotted on the chart, with a reference line at 1, helping users quickly assess whether the asset's returns are favorable relative to the target.

How to Use:

Add the Indicator to Your Chart: Copy the script into the Pine Script editor on TradingView and add it to your chart.

Specify the Calculation Period: Adjust the Calculation Period input to match your desired time frame for the Omega Ratio calculation.

Set the Target Return: Input your desired target return to customize the risk-return analysis.

Interpret the Omega Ratio: An Omega Ratio greater than 1 indicates that the asset's returns are more likely to exceed the target return than to fall short, whereas a ratio less than 1 suggests the opposite.

Sortino RatioThe Sortino Ratio Indicator is a custom script developed to measure the risk-adjusted performance of an asset. Unlike the Sharpe Ratio, which penalizes both upside and downside volatility equally, the Sortino Ratio specifically differentiates between harmful volatility (downside risk) and overall volatility. This makes it a preferred choice for traders and investors who are particularly concerned with downside risk.

Features:

Calculation Period Input: Users can specify the period over which the Sortino Ratio is calculated, making it adaptable to different time frames and trading strategies.

Daily Returns Calculation: The indicator calculates daily returns using logarithmic returns, which provides a more accurate reflection of percentage changes in price.

Mean Return and Downside Deviation: The script calculates the mean of daily returns and the downside deviation, focusing only on negative returns that fall below the mean.

Annualized Sortino Ratio: The Sortino Ratio is annualized assuming 252 trading days in a year, providing a standardized measure that can be easily compared across different assets and time periods.

Visual Plot: The indicator plots the Sortino Ratio on the chart, with a reference zero line to help users quickly assess the performance relative to the risk-free rate.

How to Use:

Add the Indicator to Your Chart: Copy the script into the Pine Script editor on TradingView and add it to your chart.

Specify the Calculation Period: Adjust the Calculation Period input to match your desired time frame for the Sortino Ratio calculation.

Interpret the Sortino Ratio: A higher Sortino Ratio indicates better risk-adjusted performance, while a ratio below zero suggests that the asset has underperformed relative to its downside risk.

Market Cap / Revenue RatioA variation of the P/S ratio, this script takes the future estimated revenue of the current stock versus it's Market Cap. It then compares the aforementioned Market Cap:Revenue ratio against a market bellwether's corresponding ratio (MSFT by default) to determine the following:

- Light green when the ratio is extremely low (Stock is very undervalued)

- Green when the ratio is low (Stock's multiple is lower by 20-50%)

- Blue when the ratio is close to the benchmark (Stock is fairly valued to benchmark multiple)

- Red when the ratio is high (Stock's mulitple is higher by 50% or more)

- Dark red when the ratio is extremely high (Stock is very overvalued)

CONFIGURABLE

- Full Table: Show the entire calculation table

- Minimalist: Go minimal and show only the ratio and color code

- Show Benchmark Multiple: Show the multiple ratio calculated between the current stock and the benchmark stock (MSFT by default)

NOTES

- When calculating the Market Cap, TradingView sometimes under-reports the number of shares and thus skews the Market Cap too low. This seems to happen for stocks with multiple share classes like GOOGL so be mindful that the data can be wrong for these kinds of stocks. You can check on this by going into the Indicator's Settings and select Show Full Table which will show the number of shares outstanding reported by TradingView.

- For certain stocks such as foreign ADRs, there won't be a future revenue estimate so the script will automatically use the Total Revenue for the most recent Quarter in these cases

Fair Value Calculator V 1.0Fair Value Calculator V 1.0

This indicator calculates the fair value of a stock based on the revenue growth rate and net profit margin of a company, providing a quick estimate of its intrinsic worth. The calculation takes into account:

Current Revenue: The company's current revenue

5-Year Growth Rate: Expected revenue annual growth rate (CAGR) over the next 5 years

Average PE Ratio: The average Price-to-Earnings ratio for the next 5 years

Average Profit Margin: The average profit margin for the next 5 years

Share Outstanding: The total number of shares outstanding

Yearly Share Buyback Rate: The percentage of shares bought back by the company each year

Discount Rate: The rate used to calculate the present value of the fair value

Using these inputs, the indicator estimates the fair value of the stock, providing a valuable tool for investors and traders to make informed decisions.

Note: all values can be adjusted by the user by entering the desired value and selecting the item in the setup menu.

How it works

The indicator calculates the future revenue based on the current revenue and the expected revenue annual growth rate (CAGR).

It then estimates the future earnings using the average profit margin.

The future price is calculated using the exit value of the PE ratio.

The present value of the fair value is calculated using the discount rate.

The indicator adjusts the fair value based on the yearly share buyback rate.

Benefits

Provides a quick but valuable estimate of a stock's fair value based on the revenue growth and the expected profit.

Helps investors and traders identify undervalued or overvalued stocks.

Allows users to adjust inputs to suit their own assumptions and scenarios.

Note

This indicator is for informational purposes only and should not be considered as investment advice. Always do your own research and consider multiple perspectives before making investment decisions.

True stock performance based on EY Bar divergenceI created this indicator to be used in conjunction with my other indicator "True stock performance based on Earnings Yield". I've detailed in that description how true performance is calculated. In short it measures how much EY is moving in relation to the stock price. The theory is that if stock price is moving heavily while EY isn't you have a sentiment driven trend and the stock isn't traded on fundamentals.

This indicators marks bars when stock performance divergences from true performance.

Green upward triangle = The true performance closes lower than previous while stock price is closing higher. This indicates a optimistic sentiment as stock price is pushed up even though price based on EY is moving down.

Red downward triangle = The true performance closes higher than previous while stock price closing lower. This indicates a negative sentiment as stock price is pushed down even though price based on EY is moving up.

How do I use it?

I use it to confirm when sentiment has taken taken over a stock. If you have a fair uptrend (when both stock performance and true performance are doing higher highs), optimistic divergencies are welcome. I've used NVIDIA from 2017 to 2019 to demonstrate.

But if true performance starts to make lower highs while stock performance keeps going up and you see optimistic divergencies, you can tell that the market is getting overoptimistic.

When the stock had crashed it eventually bottomed and started to make higher lows together with an uptrend of true performance, which I count as a fair uptrend. Regardless of that you start to see some negative divergencies indicating that people are scared that the stock will drop again and oversell. These opportunities can be good places to buy more.

But i don't care about earnings, I'm a technical trader. Do i have any use for it?

You possibly could, yes. If you want to follow the crowd, optimistic divergencies confirms that the market is still interested in the stock and may keep pushing the price up. But be careful. Negative divergencies almost never marks any tops, it often confirms downtrends and may indicate bottoms. Often the optimistic divergencies marks the top so don't buy more blindly using this indicator.

True stock performance based on Earnings YieldThe whole basis of the stock market is that you invest your money into a business that can use that money to increase it's earnings and pay you back for that investment with dividends and increased stock value. But because we are human the market often overbuy stocks that cant keep up their earnings with the current inflow of investments. We can also oversell a stock that is keeping up with earnings in regards to the stock price but we don't care because of the sentiment we have.

Earnings Yield is simply the percentage of Earnings Per Share in relation to the stock price. Alone, it's a great fundamental indicator to analyze a company. But I wanted to use it in another way and got tired of using the calculator all the time so that's why I made this indicator.

The goal is to see if the STOCK price is moving accordingly to the BUSINESS earnings. It works by calculating the difference of EY (TTM) previous close (1 bar) to the close thereafter. It then calculates the stock performance of the latest bar and divides that to get decimal form instead of percent. Then it divides the stock performance in decimal form with the difference of EY calculated before. The result shows how much the stock prices moves in relation to how much EY is moving. The theory is that if EY barely moves but the stock price moves heavily, you have a sentiment driven trend.

Example: Week 1 EY = 1.201. Week 2 EY = 1.105.

1.201 - 1.105 = 0.096

Week 2 performed a 11,2% increase in stock price. = 0.112 in decimal form.

0.112 / 0.096 = 1.67

1.67 is the multiple that plots this indicator.

Here is an good example of a stock that's currently in a highly sentiment driven trend, NVIDIA! (Posted 2024-03-30)

Here is an example of a Swedish stock that retail investors flocked to that have been blowned out completely.

When do I buy and sell?

This indicator is not meant to give exact entries or exits. The purpose is to scout the current and past sentiment, possible divergencies and see if a stock is over or under valued. I did add a 50 EMA to get some form of mean plotted. One could buy when true performance is low and sell when true performance drops below the 50 EMA. You could also just sell a part of your position and set a trailing exit with a ordinary 50 EMA or something like that. Often the sentiment will keep driving the price up. But if it last for 1 month or 1 year is impossible to tell.

Try it out and learn how it works and use it as you like. Cheers!

Statistics • Chi Square • P-value • SignificanceThe Statistics • Chi Square • P-value • Significance publication aims to provide a tool for combining different conditions and checking whether the outcome is significant using the Chi-Square Test and P-value.

🔶 USAGE

The basic principle is to compare two or more groups and check the results of a query test, such as asking men and women whether they want to see a romantic or non-romantic movie.

–––––––––––––––––––––––––––––––––––––––––––––

| | ROMANTIC | NON-ROMANTIC | ⬅︎ MOVIE |

–––––––––––––––––––––––––––––––––––––––––––––

| MEN | 2 | 8 | 10 |

–––––––––––––––––––––––––––––––––––––––––––––

| WOMEN | 7 | 3 | 10 |

–––––––––––––––––––––––––––––––––––––––––––––

|⬆︎ SEX | 10 | 10 | 20 |

–––––––––––––––––––––––––––––––––––––––––––––

We calculate the Chi-Square Formula, which is:

Χ² = Σ ( (Observed Value − Expected Value)² / Expected Value )

In this publication, this is:

chiSquare = 0.

for i = 0 to rows -1

for j = 0 to colums -1

observedValue = aBin.get(i).aFloat.get(j)

expectedValue = math.max(1e-12, aBin.get(i).aFloat.get(colums) * aBin.get(rows).aFloat.get(j) / sumT) //Division by 0 protection

chiSquare += math.pow(observedValue - expectedValue, 2) / expectedValue

Together with the 'Degree of Freedom', which is (rows − 1) × (columns − 1) , the P-value can be calculated.

In this case it is P-value: 0.02462

A P-value lower than 0.05 is considered to be significant. Statistically, women tend to choose a romantic movie more, while men prefer a non-romantic one.

Users have the option to choose a P-value, calculated from a standard table or through a math.ucla.edu - Javascript-based function (see references below).

Note that the population (10 men + 10 women = 20) is small, something to consider.

Either way, this principle is applied in the script, where conditions can be chosen like rsi, close, high, ...

🔹 CONDITION

Conditions are added to the left column ('CONDITION')

For example, previous rsi values (rsi ) between 0-100, divided in separate groups

🔹 CLOSE

Then, the movement of the last close is evaluated

UP when close is higher then previous close (close )

DOWN when close is lower then previous close

EQUAL when close is equal then previous close

It is also possible to use only 2 columns by adding EQUAL to UP or DOWN

UP

DOWN/EQUAL

or

UP/EQUAL

DOWN

In other words, when previous rsi value was between 80 and 90, this resulted in:

19 times a current close higher than previous close

14 times a current close lower than previous close

0 times a current close equal than previous close

However, the P-value tells us it is not statistical significant.

NOTE: Always keep in mind that past behaviour gives no certainty about future behaviour.

A vertical line is drawn at the beginning of the chosen population (max 4990)

Here, the results seem significant.

🔹 GROUPS

It is important to ensure that the groups are formed correctly. All possibilities should be present, and conditions should only be part of 1 group.

In the example above, the two top situations are acceptable; close against close can only be higher, lower or equal.

The two examples at the bottom, however, are very poorly constructed.

Several conditions can be placed in more than 1 group, and some conditions are not integrated into a group. Even if the results are significant, they are useless because of the group formation.

A population count is added as an aid to spot errors in group formation.

In this example, there is a discrepancy between the population and total count due to the absence of a condition.

The results when rsi was between 5-25 are not included, resulting in unreliable results.

🔹 PRACTICAL EXAMPLES

In this example, we have specific groups where the condition only applies to that group.

For example, the condition rsi > 55 and rsi <= 65 isn't true in another group.

Also, every possible rsi value (0 - 100) is present in 1 of the groups.

rsi > 15 and rsi <= 25 28 times UP, 19 times DOWN and 2 times EQUAL. P-value: 0.01171

When looking in detail and examining the area 15-25 RSI, we see this:

The population is now not representative (only checking for RSI between 15-25; all other RSI values are not included), so we can ignore the P-value in this case. It is merely to check in detail. In this case, the RSI values 23 and 24 seem promising.

NOTE: We should check what the close price did without any condition.

If, for example, the close price had risen 100 times out of 100, this would make things very relative.

In this case (at least two conditions need to be present), we set 1 condition at 'always true' and another at 'always false' so we'll get only the close values without any condition:

Changing the population or the conditions will change the P-value.

In the following example, the outcome is evaluated when:

close value from 1 bar back is higher than the close value from 2 bars back

close value from 1 bar back is lower/equal than the close value from 2 bars back

Or:

close value from 1 bar back is higher than the close value from 2 bars back

close value from 1 bar back is equal than the close value from 2 bars back

close value from 1 bar back is lower than the close value from 2 bars back

In both examples, all possibilities of close against close are included in the calculations. close can only by higher, equal or lower than close

Both examples have the results without a condition included (5 = 5 and 5 < 5) so one can compare the direction of current close.

🔶 NOTES

• Always keep in mind that:

Past behaviour gives no certainty about future behaviour.

Everything depends on time, cycles, events, fundamentals, technicals, ...

• This test only works for categorical data (data in categories), such as Gender {Men, Women} or color {Red, Yellow, Green, Blue} etc., but not numerical data such as height or weight. One might argue that such tests shouldn't use rsi, close, ... values.

• Consider what you're measuring

For example rsi of the current bar will always lead to a close higher than the previous close, since this is inherent to the rsi calculations.

• Be careful; often, there are na -values at the beginning of the series, which are not included in the calculations!

• Always keep in mind considering what the close price did without any condition

• The numbers must be large enough. Each entry must be five or more. In other words, it is vital to make the 'population' large enough.

• The code can be developed further, for example, by splitting UP, DOWN in close UP 1-2%, close UP 2-3%, close UP 3-4%, ...

• rsi can be supplemented with stochRSI, MFI, sma, ema, ...

🔶 SETTINGS

🔹 Population

• Choose the population size; in other words, how many bars you want to go back to. If fewer bars are available than set, this will be automatically adjusted.

🔹 Inputs

At least two conditions need to be chosen.

• Users can add up to 11 conditions, where each condition can contain two different conditions.

🔹 RSI

• Length

🔹 Levels

• Set the used levels as desired.

🔹 Levels

• P-value: P-value retrieved using a standard table method or a function.

• Used function, derived from Chi-Square Distribution Function; JavaScript

LogGamma(Z) =>

S = 1

+ 76.18009173 / Z

- 86.50532033 / (Z+1)

+ 24.01409822 / (Z+2)

- 1.231739516 / (Z+3)

+ 0.00120858003 / (Z+4)

- 0.00000536382 / (Z+5)

(Z-.5) * math.log(Z+4.5) - (Z+4.5) + math.log(S * 2.50662827465)

Gcf(float X, A) => // Good for X > A +1

A0=0., B0=1., A1=1., B1=X, AOLD=0., N=0

while (math.abs((A1-AOLD)/A1) > .00001)

AOLD := A1

N += 1

A0 := A1+(N-A)*A0

B0 := B1+(N-A)*B0

A1 := X*A0+N*A1

B1 := X*B0+N*B1

A0 := A0/B1

B0 := B0/B1

A1 := A1/B1

B1 := 1

Prob = math.exp(A * math.log(X) - X - LogGamma(A)) * A1

1 - Prob

Gser(X, A) => // Good for X < A +1

T9 = 1. / A

G = T9

I = 1

while (T9 > G* 0.00001)

T9 := T9 * X / (A + I)

G := G + T9

I += 1

G *= math.exp(A * math.log(X) - X - LogGamma(A))

Gammacdf(x, a) =>

GI = 0.

if (x<=0)

GI := 0

else if (x

Chisqcdf = Gammacdf(Z/2, DF/2)

Chisqcdf := math.round(Chisqcdf * 100000) / 100000

pValue = 1 - Chisqcdf

🔶 REFERENCES

mathsisfun.com, Chi-Square Test

Chi-Square Distribution Function

Bitcoin 5A Strategy@LilibtcIn our long-term strategy, we have deeply explored the key factors influencing the price of Bitcoin. By precisely calculating the correlation between these factors and the price of Bitcoin, we found that they are closely linked to the value of Bitcoin. To more effectively predict the fair price of Bitcoin, we have built a predictive model and adjusted our investment strategy accordingly based on this model. In practice, the prediction results of this model correspond quite high with actual values, fully demonstrating its reliability in predicting price fluctuations.

When the future is uncertain and the outlook is unclear, people often choose to hold back and avoid risks, or even abandon their original plans. However, the prediction of Bitcoin is full of challenges, but we have taken the first step in exploring.

Table of contents:

Usage Guide

Step 1: Identify the factors that have the greatest impact on Bitcoin price

Step 2: Build a Bitcoin price prediction model

Step 3: Find indicators for warning of bear market bottoms and bull market tops

Step 4: Predict Bitcoin Price in 2025

Step 5: Develop a Bitcoin 5A strategy

Step 6: Verify the performance of the Bitcoin 5A strategy

Usage Restrictions

🦮Usage Guide:

1. On the main interface, modify the code, find the BTCUSD trading pair, and select the BITSTAMP exchange for trading.

2. Set the time period to the daily chart.

3. Select a logarithmic chart in the chart type to better identify price trends.

4. In the strategy settings, adjust the options according to personal needs, including language, display indicators, display strategies, display performance, display optimizations, sell alerts, buy prompts, opening days, backtesting start year, backtesting start month, and backtesting start date.

🏃Step 1: Identify the factors that have the greatest impact on Bitcoin price

📖Correlation Coefficient: A mathematical concept for measuring influence

In order to predict the price trend of Bitcoin, we need to delve into the factors that have the greatest impact on its price. These factors or variables can be expressed in mathematical or statistical correlation coefficients. The correlation coefficient is an indicator of the degree of association between two variables, ranging from -1 to 1. A value of 1 indicates a perfect positive correlation, while a value of -1 indicates a perfect negative correlation.

For example, if the price of corn rises, the price of live pigs usually rises accordingly, because corn is the main feed source for pig breeding. In this case, the correlation coefficient between corn and live pig prices is approximately 0.3. This means that corn is a factor affecting the price of live pigs. On the other hand, if a shooter's performance improves while another shooter's performance deteriorates due to increased psychological pressure, we can say that the former is a factor affecting the latter's performance.

Therefore, in order to identify the factors that have the greatest impact on the price of Bitcoin, we need to find the factors with the highest correlation coefficients with the price of Bitcoin. If, through the analysis of the correlation between the price of Bitcoin and the data on the chain, we find that a certain data factor on the chain has the highest correlation coefficient with the price of Bitcoin, then this data factor on the chain can be identified as the factor that has the greatest impact on the price of Bitcoin. Through calculation, we found that the 🔵number of Bitcoin blocks is one of the factors that has the greatest impact on the price of Bitcoin. From historical data, it can be clearly seen that the growth rate of the 🔵number of Bitcoin blocks is basically consistent with the movement direction of the price of Bitcoin. By analyzing the past ten years of data, we obtained a daily correlation coefficient of 0.93 between the number of Bitcoin blocks and the price of Bitcoin.

🏃Step 2: Build a Bitcoin price prediction model

📖Predictive Model: What formula is used to predict the price of Bitcoin?

Among various prediction models, the linear function is the preferred model due to its high accuracy. Take the standard weight as an example, its linear function graph is a straight line, which is why we choose the linear function model. However, the growth rate of the price of Bitcoin and the number of blocks is extremely fast, which does not conform to the characteristics of the linear function. Therefore, in order to make them more in line with the characteristics of the linear function, we first take the logarithm of both. By observing the logarithmic graph of the price of Bitcoin and the number of blocks, we can find that after the logarithm transformation, the two are more in line with the characteristics of the linear function. Based on this feature, we choose the linear regression model to establish the prediction model.

From the graph below, we can see that the actual red and green K-line fluctuates around the predicted blue and 🟢green line. These predicted values are based on fundamental factors of Bitcoin, which support its value and reflect its reasonable value. This picture is consistent with the theory proposed by Marx in "Das Kapital" that "prices fluctuate around values."

The predicted logarithm of the market cap of Bitcoin is calculated through the model. The specific calculation formula of the Bitcoin price prediction value is as follows:

btc_predicted_marketcap = math.exp(btc_predicted_marketcap_log)

btc_predicted_price = btc_predicted_marketcap / btc_supply

🏃Step 3: Find indicators for early warning of bear market bottoms and bull market tops

📖Warning Indicator: How to Determine Whether the Bitcoin Price has Reached the Bear Market Bottom or the Bull Market Top?

By observing the Bitcoin price logarithmic prediction chart mentioned above, we notice that the actual price often falls below the predicted value at the bottom of a bear market; during the peak of a bull market, the actual price exceeds the predicted price. This pattern indicates that the deviation between the actual price and the predicted price can serve as an early warning signal. When the 🔴 Bitcoin price deviation is very low, as shown by the chart with 🟩green background, it usually means that we are at the bottom of the bear market; Conversely, when the 🔴 Bitcoin price deviation is very high, the chart with a 🟥red background indicates that we are at the peak of the bull market.

This pattern has been validated through six bull and bear markets, and the deviation value indeed serves as an early warning signal, which can be used as an important reference for us to judge market trends.

🏃Step 4:Predict Bitcoin Price in 2025

📖Price Upper Limit

According to the data calculated on February 25, 2024, the 🟠upper limit of the Bitcoin price is $194,287, which is the price ceiling of this bull market. The peak of the last bull market was on November 9, 2021, at $68,664. The bull-bear market cycle is 4 years, so the highest point of this bull market is expected in 2025. That is where you should sell the Bitcoin. and the upper limit of the Bitcoin price will exceed $190,000. The closing price of Bitcoin on February 25, 2024, was $51,729, with an expected increase of 2.7 times.

🏃Step 5: Bitcoin 5A Strategy Formulation

📖Strategy: When to buy or sell, and how many to choose?

We introduce the Bitcoin 5A strategy. This strategy requires us to generate trading signals based on the critical values of the warning indicators, simulate the trades, and collect performance data for evaluation. In the Bitcoin 5A strategy, there are three key parameters: buying warning indicator, batch trading days, and selling warning indicator. Batch trading days are set to ensure that we can make purchases in batches after the trading signal is sent, thus buying at a lower price, selling at a higher price, and reducing the trading impact cost.

In order to find the optimal warning indicator critical value and batch trading days, we need to adjust these parameters repeatedly and perform backtesting. Backtesting is a method established by observing historical data, which can help us better understand market trends and trading opportunities.

Specifically, we can find the key trading points by watching the Bitcoin price log and the Bitcoin price deviation chart. For example, on August 25, 2015, the 🔴 Bitcoin price deviation was at its lowest value of -1.11; on December 17, 2017, the 🔴 Bitcoin price deviation was at its highest value at the time, 1.69; on March 16, 2020, the 🔴 Bitcoin price deviation was at its lowest value at the time, -0.91; on March 13, 2021, the 🔴 Bitcoin price deviation was at its highest value at the time, 1.1; on December 31, 2022, the 🔴 Bitcoin price deviation was at its lowest value at the time, -1.

To ensure that all five key trading points generate trading signals, we set the warning indicator Bitcoin price deviation to the larger of the three lowest values, -0.9, and the smallest of the two highest values, 1. Then, we buy when the warning indicator Bitcoin price deviation is below -0.9, and sell when it is above 1.

In addition, we set the batch trading days as 25 days to implement a strategy that averages purchases and sales. Within these 25 days, we will invest all funds into the market evenly, buying once a day. At the same time, we also sell positions at the same pace, selling once a day.

📖Adjusting the threshold: a key step to optimizing trading strategy

Adjusting the threshold is an indispensable step for better performance. Here are some suggestions for adjusting the batch trading days and critical values of warning indicators:

• Batch trading days: Try different days like 25 to see how it affects overall performance.

• Buy and sell critical values for warning indicators: iteratively fine-tune the buy threshold value of -0.9 and the sell threshold value of 1 exhaustively to find the best combination of threshold values.

Through such careful adjustments, we may find an optimized approach with a lower maximum drawdown rate (e.g., 11%) and a higher cumulative return rate for closed trades (e.g., 474 times). The chart below is a backtest optimization chart for the Bitcoin 5A strategy, providing an intuitive display of strategy adjustments and optimizations.

In this way, we can better grasp market trends and trading opportunities, thereby achieving a more robust and efficient trading strategy.

🏃Step 6: Validating the performance of the Bitcoin 5A Strategy

📖Model interpretability validation: How to explain the Bitcoin price model?

The interpretability of the model is represented by the coefficient of determination R squared, which reflects the degree of match between the predicted value and the actual value. I divided all the historical data from August 18, 2015 into two groups, and used the data from August 18, 2011 to August 18, 2015 as training data to generate the model. The calculation result shows that the coefficient of determination R squared during the 2011-2015 training period is as high as 0.81, which shows that the interpretability of this model is quite high. From the Bitcoin price logarithmic prediction chart in the figure below, we can see that the deviation between the predicted value and the actual value is not far, which means that most of the predicted values can explain the actual value well.

The calculation formula for the coefficient of determination R squared is as follows:

residual = btc_close_log - btc_predicted_price_log

residual_square = residual * residual

train_residual_square_sum = math.sum(residual_square, train_days)

train_mse = train_residual_square_sum / train_days

train_r2 = 1 - train_mse / ta.variance(btc_close_log, train_days)

📖Model stability verification: How to affirm the stability of the Bitcoin price model when new data is available?

Model stability is achieved through model verification. I set the last day of the training period to February 2, 2024 as the "verification group" and used it as verification data to verify the stability of the model. This means that after generating the model if there is new data, I will use these new data together with the model for prediction, and then evaluate the interpretability of the model. If the coefficient of determination when using verification data is close to the previous training one and both remain at a high level, then we can consider this model as stability. The coefficient of determination calculated from the validation period data and model prediction results is as high as 0.83, which is close to the previous 0.81, further proving the stability of this model.

📖Performance evaluation: How to accurately evaluate historical backtesting results?

After detailed strategy testing, to ensure the accuracy and reliability of the results, we need to carry out a detailed performance evaluation on the backtest results. The key evaluation indices include:

• Net value curve: As shown in the rose line, it intuitively reflects the growth of the account net value. By observing the net value curve, we can understand the overall performance and profitability of the strategy.

The basic attributes of this strategy are as follows:

Trading range: 2015-8-19 to 2024-2-18, backtest range: 2011-8-18 to 2024-2-18

Initial capital: 1000USD, order size: 1 contract, pyramid: 50 orders, commission rate: 0.2%, slippage: 20 markers.

In the strategy tester overview chart, we also obtained the following key data:

• Net profit rate of closed trades: as high as 474 times, far exceeding the benchmark, as shown in the strategy tester performance summary chart, Bitcoin buys and holds 210 times.

• Number of closed trades and winning percentage: 100 trades were all profitable, showing the stability and reliability of the strategy.

• Drawdown rate & win-loose ratio: The maximum drawdown rate is only 11%, far lower than Bitcoin's 78%. Profit factor, or win-loose ratio, reached 500, further proving the advantage of the strategy.

Through these detailed evaluations, we can see clearly the excellent balance between risk and return of the Bitcoin 5A strategy.

⚠️Usage Restrictions: Strategy Application in Specific Situations

Please note that this strategy is designed specifically for Bitcoin and should not be applied to other assets or markets without authorization. In actual operations, we should make careful decisions according to our risk tolerance and investment goals.