Alpha Trend Strength Pro🔥 What You’ll See on the Chart

✅ A floating label appears near the most recent candle.

✅ Label shows:

🔥 Trend direction: Uptrend / Downtrend / Neutral / Near VWAP

💪 Trend strength: Strong / Moderate / Weak / Range

📈 EMA alignment

🎯 RSI momentum state

💥 MACD crossover

📊 Volatility condition (Expanding / Contracting)

🔵 VWAP proximity if enabled

✅ The chart background turns:

Green for Uptrend

Red for Downtrend

Neutral/Gray if in range (no background color)

⚙️ Customize Settings

Click the gear icon ⚙️ next to the script’s name on your chart.

Change things like:

Show/hide background color

Toggle VWAP-based filtering

Adjust RSI, MACD, Bollinger parameters

Statistics

Hidden Markov ModelDescription

This model uses a Hidden Markov Model to detect potential tops and bottoms. It is designed to probabilistically identify market regime changes and predict potential reversal point using a forward algorithm to calculate the probability of a state.

State 0: (Normal Trading): Market continuation patterns, balanced buying/selling

State 1: (Top Formation): Exhaustion patterns at price highs

State 2: (Bottom Formation): Capitulation patterns at price lows

Background: The HMM assumes that market behavior follows hidden states that aren't directly observable, but can be inferred from observable market data (emissions). The model uses a (somewhat simplified) Bayesian inference to estimate these probabilities.

How to use

1) Identify the trend (you can also use it counter-trend)

2) For longing, look for a green arrow. The probability values should be red. For shorting, look for a red arrow. The probability values should be green

3) For added confluence, look for high probability values

xetra//@version=5

indicator("First Candle Range", overlay=true)

// Налаштування сесії

session = input.session("0930-1030", title="Сесія")

// Визначити, чи поточна свічка — перша у сесії

is_new_session = ta.change(time(session))

// Змінні для збереження значень першої свічки

var float first_high = na

var float first_low = na

var int first_index = na

// Коли настає нова сесія — зберігаємо high та low першої свічки

if is_new_session

first_high := high

first_low := low

first_index := bar_index

// Побудова ліній

if not na(first_index)

line.new(first_index, first_high, bar_index, first_high, color=color.green, width=1, extend=extend.right)

line.new(first_index, first_low, bar_index, first_low, color=color.red, width=1, extend=extend.right)

// (Опційно) Заливка області між high та low

bgcolor(time(session) and bar_index == first_index ? color.new(color.orange, 85) : na)

Session SizeAnalyze previous Sessions Size (Asia, London, New York) and give back the average range size in points.

Great tool if you want to take seriously the time and price

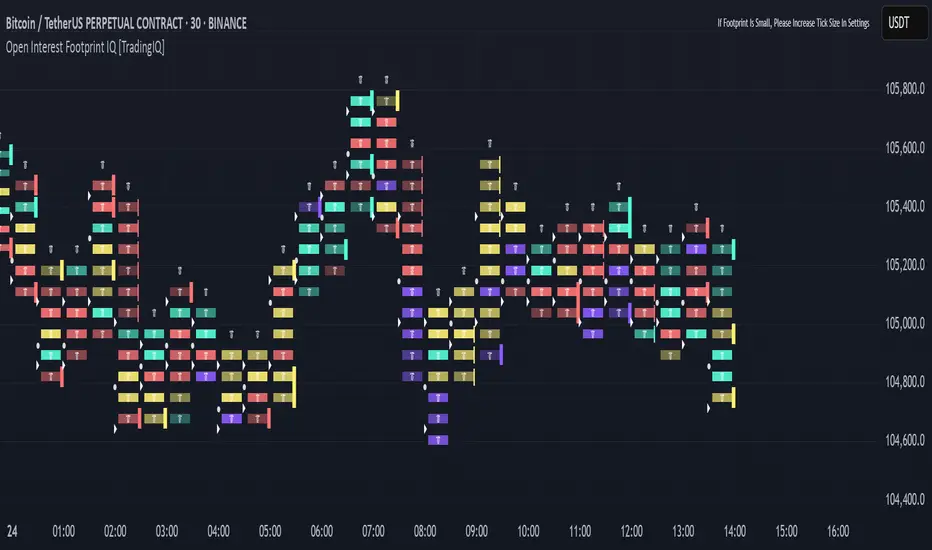

Open Interest Footprint IQ [TradingIQ]Hello Traders!

Th e Open Interest Footprint IQ indicator is an advanced visualization tool designed for cryptocurrency markets. It provides a granular, real-time breakdown of open interest changes across different price levels, allowing traders to see how aggressive market participation is distributed within each bar.

Unlike standard footprint charts that rely solely on volume, this indicator offers unique insights by focusing on the interaction between price action and changes in open interest (OI) — a leading metric often used to infer trader intent and positioning.

How it works

The Open Interest Footprint IQ processes lower timeframe price and open interest data to build a footprint-style chart that shows how traders are positioning themselves within each candle.

Here’s a breakdown of the process:

1. Granular OI & Price Sampling

The script retrieves lower-timeframe data (1-minute, 1-second, or 1-tick, based on your setting).

For each candle, it captures:

High and low prices

Price change direction

Change in open interest (OI)

2. Classifying Trader Behavior

For each lower-timeframe segment, the indicator determines the type of positioning occurring based on price movement and OI change:

If price is moving up and open interest is increasing, it suggests that long positions are being opened. This is considered a "Longs Opening" event, labeled as UU (Up/Up).

If price is moving up but open interest is decreasing, it indicates that short positions are being closed. This is referred to as UD (Up/Down), or "Shorts Closing."

If price is moving down and open interest is increasing, it signals that short positions are being opened. This is known as DU (Down/Up), or "Shorts Opening."

If price is moving down while open interest is also decreasing, it means that long positions are being closed. This is labeled as DD (Down/Down), or "Longs Closing."

These are stored in separate arrays and displayed at specific price levels.

It is particularly useful for identifying:

Where longs or shorts are opening/closing positions

Stacked imbalances (indicative of potential absorption or exhaustion)

Value area zones and POC (Point of Control) based on OI, not volume

This footprint runs on your choice of sub-bar granularity and is ideal for high-frequency trading, scalping, and entries based on order flow dynamics.

Key Features

Footprint Visualization

At each price level within a candle:

Long/short opening and closing behavior is broken down.

Delta (net open interest change) is displayed both numerically and color-coded.

Optional gradient coloring shows intensity and type of flow (longs/shorts opened/closed).

Cumulative or per-bar reset modes allow you to track OI evolution over time.

The image above explains the information that each Footprint box shows across a candlestick!

Each footprint box shows:

OI Delta

OI Delta %

Longs Opened (LO)

Longs Closed (LC)

Shorts Opened (SO)

Shorts Closed (SC)

The image above explains the color-coding feature of the indicator.

Boxes are color coded to show which position action

dominated at the price area.

For this example:

Green boxes = Long positions being opened dominated

Purple boxes = Long positions being closed dominated

Red boxes = Short positions being opened dominated

Yellow boxes = Short positions being closed dominated

All colors are customizable.

Additionally, for traders who are only interested in whether OI increased/decreased, a "two-color" option is available in the settings.

For the two-color option, footprint boxes can be one of two colors. Showing whether OI increased or decreased at the level.

Cumulative Levels

Open Interest Footprint IQ contains a "Cumulative Levels" feature that tracks/stores open interest change at tick levels over time, rather than resetting per bar.

With the "Cumulative Levels" feature enabled, traders can see open interest changes persist across all candlesticks. This feature is useful for determining whether longs opening, longs closing, shorts opening, or shorts closing are dominating at particular price areas over time rather than on a single bar.

A useful feature to see if shorts/longs are favoring certain price throughout the day, week, month, etc.

Input Settings Explained

Granularity (Dropdown: Granularity)

Options: 1-Minute, 1-Second, 1-Tick

Determines how finely the script samples the lower timeframe data to construct the footprint.

For precision:

1-Tick = Highest accuracy, but more resource-intensive.

1-Second/1-Minute = Suitable for broader or more zoomed-out analysis.

Tick Level Distance (Tick Level Distance (0 = Auto))

Defines the vertical spacing between levels in the footprint chart.

If 0, the script uses an automatic calculation based on ATR to adapt to volatility.

Set a manual value (e.g., 5) to control the height granularity of each level in ticks.

Cumulative Levels (Toggle)

If enabled, the footprint builds cumulatively over time, rather than resetting per candle.

Use case: Visualize ongoing buildup of OI activity across a session or day.

Cumulative Levels Reset TF (Timeframe)

Sets the reset interval for the cumulative view (e.g., reset daily, hourly, etc.)

Works only when Cumulative Levels is enabled.

Delta Box Display Settings

Show Delta Percentage

Toggles the display of the percentage change in OI across the footprint level.

Helpful to gauge how aggressive positioning is relative to total OI at that level.

Show Longs/Shorts (Opened/Closed)

Show Longs Opened: Displays OI increase in up candles (price ↑, OI ↑).

Show Longs Closed: Displays OI decrease in down candles (price ↓, OI ↓).

Show Shorts Opened: OI increase in down candles (price ↓, OI ↑).

Show Shorts Closed: OI decrease in up candles (price ↑, OI ↓).

These behaviors are color-coded to give traders instant context:

Blue-green for longs opening.

Purple for longs closing.

Red for shorts opening.

Yellow for shorts closing.

Value Area & POC

Value Area % (Value Area %)

Controls how much cumulative open interest is used to define the value area.

Example: 70% means the smallest range of prices that contains 70% of total OI in that bar will be marked.

Helps identify zones of interest, support/resistance, and institutional levels.

The image above explains how to identify the VAH/VAL/POC shown by Open Interest Footprint IQ.

VAH = Upper 🞂

POC = ●

VAL = Lower 🞂

Imbalances

Imbalance Percentage

Defines the minimum delta % required at a level to be marked as an imbalance.

If the net open interest change at a level exceeds this threshold, a visual marker appears.

Stacked Imbalance Count

If the number of consecutive imbalance levels meets this count, a “Stacked Imbalance” alert will trigger.

This can signal aggressive buying or selling pressure, potential breakout zones, or institutional absorption.

Color Settings

Longs Opened / Closed, Shorts Opened / Closed

Customize the color palette for each order flow behavior.

These colors appear in the background gradient of the footprint boxes.

Up/Down Only Mode

Toggle to override all behavior-based colors with a single Up Color and Down Color.

Useful if you prefer a simple bull/bear view.

Up Color / Down Color

If "Up/Down Only" is enabled, these two colors are used to represent all net positive or negative deltas.

Special Notes

Crypto only: This script works only with crypto tickers on TradingView.

For other assets (stocks, futures), a warning message will appear instead.

OI data must be available from the exchange (many perpetual pairs support this).

If the footprint is too small or invisible, increase your tick level spacing in the settings.

Alerts

When a stacked imbalance is detected, an alert is fired ("Stacked Imbalance").

This feature is useful for automated systems, bots, or simply staying informed of potential trade setups.

And that's all for now!

If you have any questions or features you'd like to see feel free to share them in the comments below!

Thank you traders!

Auto LevelsAutomatically paints open, high, low, and close levels from previous periods.

RTH data only in traditional cash markets.

Previous periods included are:

- Day

- Week

- Month

- Quarter

- Year.

Customization options allow for:

- Enabling/disabling of each type of level for each period

- Text size and colors of labels

- Colors and styles of lines

- Line extension length

*Also, there is a close-price ray included. Can be disabled.

Creates new levels once they generate, and removes old and outdated levels.

The idea is to be transparent about the relevancy of levels and portray them as they generate in time. Full 2-way-ray horizontal lines can appear to give false-reaction data in historical bars from before the level was generated. This can give traders a false sense of importance to a level.

Works on any ticker/symbol.

Known bugs:

** Open levels distort based on open/closed status in traditional markets. Fix pending.

** Different candle types (Heikin Ashi) distort all open/close level data. Fix pending.

** Line extension doesn't work in closed markets. Fix pending.

Message me on twitter for other bug reports.

Z Score Overlay [BigBeluga]🔵 OVERVIEW

A clean and effective Z-score overlay that visually tracks how far price deviates from its moving average. By standardizing price movements, this tool helps traders understand when price is statistically extended or compressed—up to ±4 standard deviations. The built-in scale and real-time bin markers offer immediate context on where price stands in relation to its recent mean.

🔵 CONCEPTS

Z Score Calculation:

Z = (Close − SMA) ÷ Standard Deviation

This formula shows how many standard deviations the current price is from its mean.

Statistical Extremes:

• Z > +2 or Z < −2 suggests statistically significant deviation.

• Z near 0 implies price is close to its average.

Standardization of Price Behavior: Makes it easier to compare volatility and overextension across timeframes and assets.

🔵 FEATURES

Colored Z Line: Gradient coloring based on how far price deviates—

• Red = oversold (−4),

• Green = overbought (+4),

• Yellow = neutral (~0).

Deviation Scale Bar: A vertical scale from −4 to +4 standard deviations plotted to the right of price.

Active Z Score Bin: Highlights the current Z-score bin with a “◀” arrow

Context Labels: Clear numeric labels for each Z-level from −4 to +4 along the side.

Live Value Display: Shows exact Z-score on the active level.

Non-intrusive Overlay: Can be applied directly to price chart without changing scaling behavior.

🔵 HOW TO USE

Identify overbought/oversold areas based on +2 / −2 thresholds.

Spot potential mean reversion trades when Z returns from extreme levels.

Confirm strong trends when price remains consistently outside ±2.

Use in multi-timeframe setups to compare strength across contexts.

🔵 CONCLUSION

Z Score Overlay transforms raw price action into a normalized statistical view, allowing traders to easily assess deviation strength and mean-reversion potential. The intuitive scale and color-coded display make it ideal for traders seeking objective, volatility-aware entries and exits.

Daily Trading Barometer (DTB) with DJIA OverlayThe "Daily Trading Barometer (DTB) with DJIA Overlay" is a custom technical indicator designed to identify intermediate-term overbought and oversold conditions in the stock market, inspired by Edson Gould's original DTB methodology. This indicator combines three key components:

A 7-day advance-decline oscillator, a 20-day volume oscillator, and a 28-day DJIA price ratio, normalized into a composite index scaled around 110–135. Values below 110 signal potential oversold conditions, while values above 135 indicate overbought territory, aiding in timing market reversals.

The overlay of a normalized DJIA plot allows for visual correlation with the broader market trend. Use this tool to anticipate turning points in oscillating markets, though it’s best combined with other indicators for confirmation. Ideal for traders seeking probabilistic insights into bear or bull market transitions.

How to use -

If the DTB line (blue) and normalized DJIA (orange) are under the green dashed line, high probability for a long and reversal.

Use with the symbol SPX/QQQ

Dow Jones Industrial Average - DJIA

Gap % Distribution Table (2% Bins)Description

This indicator displays a Gap % Distribution Table categorized in 2% bins ranging from `< -20%` to `> +20%`. It calculates the gap between today’s open and the previous day’s close, and groups occurrences into defined bins. The table includes:

Gap range, count, and percentage for each bin

A total row summarizing all entries

Customizable appearance including:

Font color, cell background fill (with transparency), and table border color

Column headers and full outer border

Date filtering using selectable start and end dates

Position control for placing the table on the chart area

Ideal for analyzing the historical behavior of opening gaps for any instrument.

SIP Evaluator and Screener [Trendoscope®]The SIP Evaluator and Screener is a Pine Script indicator designed for TradingView to calculate and visualize Systematic Investment Plan (SIP) returns across multiple investment instruments. It is tailored for use in TradingView's screener, enabling users to evaluate SIP performance for various assets efficiently.

🎲 How SIP Works

A Systematic Investment Plan (SIP) is an investment strategy where a fixed amount is invested at regular intervals (e.g., monthly or weekly) into a financial instrument, such as stocks, mutual funds, or ETFs. The goal is to build wealth over time by leveraging the power of compounding and mitigating the impact of market volatility through disciplined, consistent investing. Here’s a breakdown of how SIPs function:

Regular Investments : In an SIP, an investor commits to investing a fixed sum at predefined intervals, regardless of market conditions. This consistency helps inculcate a habit of saving and investing.

Cost Averaging : By investing a fixed amount regularly, investors purchase more units when prices are low and fewer units when prices are high. This approach, known as dollar-cost averaging, reduces the average cost per unit over time and mitigates the risk of investing a large amount at a peak price.

Compounding Benefits : Returns generated from the invested amount (e.g., capital gains or dividends) are reinvested, leading to exponential growth over the long term. The longer the investment horizon, the greater the potential for compounding to amplify returns.

Dividend Reinvestment : In some SIPs, dividends received from the underlying asset can be reinvested to purchase additional units, further enhancing returns. Taxes on dividends, if applicable, may reduce the reinvested amount.

Flexibility and Accessibility : SIPs allow investors to start with small amounts, making them accessible to a wide range of individuals. They also offer flexibility in terms of investment frequency and the ability to adjust or pause contributions.

In the context of the SIP Evaluator and Screener , the script simulates an SIP by calculating the number of units purchased with each fixed investment, factoring in commissions, dividends, taxes and the chosen price reference (e.g., open, close, or average prices). It tracks the cumulative investment, equity value, and dividends over time, providing a clear picture of how an SIP would perform for a given instrument. This helps users understand the impact of regular investing and make informed decisions when comparing different assets in TradingView’s screener. It offers insights into key metrics such as total invested amount, dividends received, equity value, and the number of installments, making it a valuable resource for investors and traders interested in understanding long-term investment outcomes.

🎲 Key Features

Customizable Investment Parameters: Users can define the recurring investment amount, price reference (e.g., open, close, HL2, HLC3, OHLC4), and whether fractional quantities are allowed.

Commission Handling: Supports both fixed and percentage-based commission types, adjusting calculations accordingly.

Dividend Reinvestment: Optionally reinvests dividends after a user-specified period, with the ability to apply tax on dividends.

Time-Bound Analysis: Allows users to set a start year for the analysis, enabling historical performance evaluation.

Flexible Dividend Periods: Dividends can be evaluated based on bars, days, weeks, or months.

Visual Outputs: Plots key metrics like total invested amount, dividends, equity value, and remainder, with customizable display options for clarity in the data window and chart.

🎲 Using the script as an indicator on Tradingview Supercharts

In order to use the indicator on charts, do the following.

Load the instrument of your choice - Preferably a stable stocks, ETFs.

Chose monthly timeframe as lower timeframes are insignificant in this type of investment strategy

Load the indicator SIP Evaluator and Screener and set the input parameters as per your preference.

Indicator plots, investment value, dividends and equity on the chart.

🎲 Visualizations

Installments : Displays the number of SIP installments (gray line, visible in the data window).

Invested Amount : Shows the cumulative amount invested, excluding reinvested dividends (blue area plot).

Dividends : Tracks total dividends received (green area plot).

Equity : Represents the current market value of the investment based on the closing price (purple area plot).

Remainder : Indicates any uninvested cash after each installment (gray line, visible in the data window).

🎲 Deep dive into the settings

The SIP Evaluator and Screener offers a range of customizable settings to tailor the Systematic Investment Plan (SIP) simulation to your preferences. Below is an explanation of each setting, its purpose, and how it impacts the analysis:

🎯 Duration

Start Year (Default: 2020) : Specifies the year from which the SIP calculations begin. When Start Year is enabled via the timebound option, the script only considers data from the specified year onward. This is useful for analyzing historical SIP performance over a defined period. If disabled, the script uses all available data.

Timebound (Default: False) : A toggle to enable or disable the Start Year restriction. When set to False, the SIP calculation starts from the earliest available data for the instrument.

🎯 Investment

Recurring Investment (Default: 1000.0) : The fixed amount invested in each SIP installment (e.g., $1000 per period). This represents the regular contribution to the SIP and directly influences the total invested amount and quantity purchased.

Allow Fractional Qty (Default: True) : When enabled, the script allows the purchase of fractional units (e.g., 2.35 shares). If disabled, only whole units are purchased (e.g., 2 shares), with any remaining funds carried forward as Remainder. This setting impacts the precision of investment allocation.

Price Reference (Default: OPEN): Determines the price used for purchasing units in each SIP installment. Options include:

OPEN : Uses the opening price of the bar.

CLOSE : Uses the closing price of the bar.

HL2 : Uses the average of the high and low prices.

HLC3 : Uses the average of the high, low, and close prices.

OHLC4 : Uses the average of the open, high, low, and close prices. This setting affects the cost basis of each purchase and, consequently, the total quantity and equity value.

🎯 Commission

Commission (Default: 3) : The commission charged per SIP installment, expressed as either a fixed amount (e.g., $3) or a percentage (e.g., 3% of the investment). This reduces the amount available for purchasing units.

Commission Type (Default: Fixed) : Specifies how the commission is calculated:

Fixed ($) : A flat fee is deducted per installment (e.g., $3).

Percentage (%) : A percentage of the investment amount is deducted as commission (e.g., 3% of $1000 = $30). This setting affects the net amount invested and the overall cost of the SIP.

🎯 Dividends

Apply Tax On Dividends (Default: False) : When enabled, a tax is applied to dividends before they are reinvested or recorded. The tax rate is set via the Dividend Tax setting.

Dividend Tax (Default: 47) : The percentage of tax deducted from dividends if Apply Tax On Dividends is enabled (e.g., 47% tax reduces a $100 dividend to $53). This reduces the amount available for reinvestment or accumulation.

Reinvest Dividends After (Default: True, 2) : When enabled, dividends received are reinvested to purchase additional units after a specified period (e.g., 2 units of time, defined by Dividends Availability). If disabled, dividends are tracked but not reinvested. Reinvestment increases the total quantity and equity over time.

Dividends Availability (Default: Bars) : Defines the time unit for evaluating when dividends are available for reinvestment. Options include:

Bars : Based on the number of chart bars.

Weeks : Based on weeks.

Months : Based on months (approximated as 30.5 days). This setting determines the timing of dividend reinvestment relative to the Reinvest Dividends After period.

🎯 How Settings Interact

These settings work together to simulate a realistic SIP. For example, a $1000 recurring investment with a 3% commission and fractional quantities enabled will calculate the number of units purchased at the chosen price reference after deducting the commission. If dividends are reinvested after 2 months with a 47% tax, the script fetches dividend data, applies the tax, and adds the net dividend to the investment amount for that period. The Start Year and Timebound settings ensure the analysis aligns with the desired timeframe, while the Dividends Availability setting fine-tunes dividend reinvestment timing.

By adjusting these settings, users can model different SIP scenarios, compare performance across instruments in TradingView’s screener, and gain insights into how commissions, dividends, and price references impact long-term returns.

🎲 Using the script with Pine Screener

The main purpose of developing this script is to use it with Tradingview Pine Screener so that multiple ETFs/Funds can be compared.

In order to use this as a screener, the following things needs to be done.

Add SIP Evaluator and Screener to your favourites (Required for it to be added in pine screener)

Create a watch list containing required instruments to compare

Open pine screener from Tradingview main menu Products -> Screeners -> Pine or simply load the URL - www.tradingview.com

Select the watchlist created from Watchlist dropdown.

Chose the SIP Evaluator and Screener from the "Choose Indicator" dropdown

Set timeframe to 1 month and update settings as required.

Press scan to display collected data on the screener.

🎲 Use Case

This indicator is ideal for educational purposes, allowing users to experiment with SIP strategies across different instruments. It can be applied in TradingView’s screener to compare SIP performance for stocks, ETFs, or other assets, helping users understand how factors like commissions, dividends, and price references impact returns over time.

QQQ NQ NDX SPY SPX ES Price Convert Overlay

_____________________________________________________________________

QQQ NQ NDX SPY SPX ES Price Convert Overlay Indicator

____________________

This 'Prices Overlay' indicator is a minimalist tool for traders who want to track and compare Nasdaq and S&P 500 instruments quickly and clearly, boosting efficiency and decision-making with minimal distraction.

How to Use It

____________________

Add the indicator onto your TradingView chart.

Adjust your Right Margin in TradingView Settings > Canvas to show as much or as little of the line as you want, based on the "Price Buffer" indicator setting.

Select which instruments to overlay (e.g., QQQ, SPX).

Adjust levels, buffer, font, transparency, and update interval.

Features and Functions

____________________

1. Automatic Ticker Detection:

The indicator identifies the ticker of your current chart (e.g., NQ, ES, SPY).

It then shows price levels for related instruments, eg:

On an NQ or MNQ chart, it can display QQQ or NDX levels.

On an ES or MES chart, it can display SPY or SPX levels.

...and vice versa

2. Adjustable Number of Levels

You can choose how many price levels to show, from 10 to 100.

This lets you decide how much detail you want based on your trading needs.

3. Visual Customization

Price Buffer: Move the lines and labels horizontally closer/further price action.

Font Size: Pick from "Tiny," "Small," or "Normal" for label text size.

Line Transparency: Adjust the opacity of the lines (0% = solid, 100% = invisible) to blend them with your chart.

4. Support for Micro Futures

Works with both regular futures (NQ, ES) and micro futures (MNQ, MES), perfect for traders using smaller contract sizes.

5. Update Frequency

Set how often the price levels refresh, from every 5 seconds to every 60 seconds.

This keeps the data current without slowing down your chart.

6. Accurate Price Conversion

Uses specific multipliers for each instrument (e.g., 100.0 for NDX and SPX, 1.0 for QQQ and SPY) to calculate and display price levels correctly.

Fetches real-time prices and converts them to match your chart’s scale.

Price conversions courtesy of PtGambler.

Benefits

____________________

Easier Analysis: See how prices from different instruments line up on one chart—no need for multiple screens or math.

Customizable: Turn on/off instruments and tweak visuals to fit your trading style.

Time-Saving: Automates price conversions, letting you focus on trading decisions.

Thanks!

____________________

Thank you for your interest in my work. This is something I use every day for my trading and wanted to share it with the public. If you have any comments, bugs, or suggestions, please leave them here, or you can find me on Twitter or Discord.

@ ContrarianIRL

Open-source developer for over 25 years

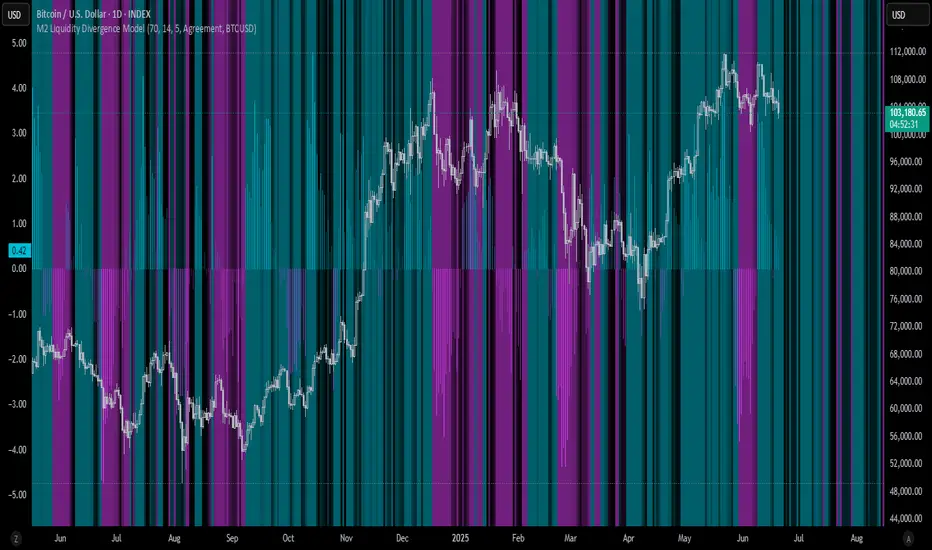

M2 Liquidity Divergence ModelM2 Liquidity Divergence Model

The M2 Liquidity Divergence Model is a macro-aware visualization tool designed to compare shifts in global liquidity (M2) against the performance of a benchmark asset (default: Bitcoin). This script captures liquidity flows across major global economies and highlights whether price action is aligned ("Agreement") or diverging ("Divergence") from macro trends.

🔍 Core Features

M2 Global Liquidity Index (GLI):

Aggregates M2 money supply from major global economies, FX-adjusted, including extended contributors like India, Brazil, and South Africa. The slope of this composite is used to infer macro liquidity trends.

Lag Offset Control:

Allows the M2 signal to lead benchmark asset price by a configurable number of days (Lag Offset), useful for modeling the forward-looking nature of macro flows.

Gradient Macro Context (Background):

Displays a color-gradient background—aqua for expansionary liquidity, fuchsia for contraction—based on the slope and volatility of M2. This contextual backdrop helps users visually anchor price action within macro shifts.

Divergence Histogram (Optional):

Plots a histogram showing dynamic correlation or divergence between the liquidity index and the selected benchmark.

Agreement Mode: M2 and asset are moving together.

Divergence Mode: Highlights break in expected macro-asset alignment.

Adaptive Transparency Scaling:

Histogram and background gradients scale their visual intensity based on statistical deviation to emphasize stronger signals.

Toggle Options:

Show/hide the M2 Liquidity Index line.

Show/hide divergence histogram.

Enable/disable visual offset of M2 to benchmark.

🧠 Suggested Usage

Macro Positioning: Use the background context to align directional trades with macro liquidity flows.

Disagreement as Signal: Use divergence plots to identify when price moves against macro expectations—potential reversal or exhaustion zones.

Time-Based Alignment: Adjust Lag Offset to synchronize M2 signals with asset price behavior across different market conditions.

⚠️ Disclaimer

This indicator is designed for educational and analytical purposes only. It does not constitute financial advice or an investment recommendation. Always conduct your own research and consult a licensed financial advisor before making trading decisions.

Intraweek Highs & Lows🔎 Track and analyze intraweek price extremes with full flexibility.

The indicator detects weekly highs or lows for any selected weekday and monitors when other days break those levels.

⚙️ Inputs

Select day

Pick which weekday’s extreme you want to monitor.

Find Low/High

Select whether you want to track Lows or Highs.

Use candle Wick/Body

Choose if extremes are calculated by full wick or candle body.

Cutoff date

Toggle the date-based filter and choose the starting date for event display.

MC Geopolitical Tension Events📌 Script Title: Geopolitical Tension Events

📖 Description:

This script highlights key geopolitical and military tension events from 1914 to 2024 that have historically impacted global markets.

It automatically plots vertical dashed lines and labels on the chart at the time of each major event. This allows traders and analysts to visually assess how markets have responded to global crises, wars, and significant political instability over time.

🧠 Use Cases:

Historical backtesting: Understand how market responded to past geopolitical shocks.

Contextual analysis: Add macro context to technical setups.

🗓️ List of Geopolitical Tension Events in the Script

Date Event Title Description

1914-07-28 WWI Begins Outbreak of World War I following the assassination of Archduke Franz Ferdinand.

1929-10-24 Wall Street Crash Black Thursday, the start of the 1929 stock market crash.

1939-09-01 WWII Begins Germany invades Poland, starting World War II.

1941-12-07 Pearl Harbor Japanese attack on Pearl Harbor; U.S. enters WWII.

1945-08-06 Hiroshima Bombing First atomic bomb dropped on Hiroshima by the U.S.

1950-06-25 Korean War Begins North Korea invades South Korea.

1962-10-16 Cuban Missile Crisis 13-day standoff between the U.S. and USSR over missiles in Cuba.

1973-10-06 Yom Kippur War Egypt and Syria launch surprise attack on Israel.

1979-11-04 Iran Hostage Crisis U.S. Embassy in Tehran seized; 52 hostages taken.

1990-08-02 Gulf War Begins Iraq invades Kuwait, triggering U.S. intervention.

2001-09-11 9/11 Attacks Coordinated terrorist attacks on the U.S.

2003-03-20 Iraq War Begins U.S.-led invasion of Iraq to remove Saddam Hussein.

2008-09-15 Lehman Collapse Bankruptcy of Lehman Brothers; peak of global financial crisis.

2014-03-01 Crimea Crisis Russia annexes Crimea from Ukraine.

2020-01-03 Soleimani Strike U.S. drone strike kills Iranian General Qasem Soleimani.

2022-02-24 Ukraine Invasion Russia launches full-scale invasion of Ukraine.

2023-10-07 Hamas-Israel War Hamas launches attack on Israel, sparking war in Gaza.

2024-01-12 Red Sea Crisis Houthis attack ships in Red Sea, prompting Western naval response.

Deviation Trend Profile [BigBeluga]🔵 OVERVIEW

A statistical trend analysis tool that combines moving average dynamics with standard deviation zones and trend-specific price distribution.

This is an experimental indicator designed for educational and learning purposes only.

🔵 CONCEPTS

Trend Detection via SMA Slope: Detects trend shifts when the slope of the SMA exceeds a ±0.1 threshold.

Standard Deviation Zones: Calculates ±1, ±2, and ±3 levels from the SMA using ATR, forming dynamic envelopes around the mean.

Trend Distribution Profile: Builds a histogram that shows how often price closed within each deviation zone during the active trend phase.

🔵 FEATURES

Trend Signals: Immediate shift markers using colored circles at trend reversals.

SMA Gradient Coloring: The SMA line dynamically changes color based on its directional slope.

Trend Duration Label: A label above the histogram shows how many bars the current trend has lasted.

Trend Distribution Histogram: Visual bin-based profile showing frequency of price closes within deviation bands during trend lookback period.

Adjustable Bin Count: Set the granularity of the distribution using the “Bins Amount” input.

Deviation Labels and Zones: Clearly marked ±1, ±2, ±3 lines with consistent color scheme.

Trend Strength Insight:

• Wide profile skewed to ±2/3 = strong directional trend.

• Profile clustered near SMA = potential trend exhaustion or range.

🔵 HOW TO USE

Use trend shift dots as entry signals:

• 🔵 = Bullish start

• 🔴 = Bearish start

Trade with the trend when price clusters in outer zones (±2 or ±3).

Be cautious or fade the trend when price distribution contracts toward the SMA.

View across multiple timeframes for trend confluence or divergence.

🔵 CONCLUSION

Deviation Trend Profile visualizes how price distributes during trends relative to statistical deviation zones.

It’s a powerful confluence tool for identifying strength, exhaustion, and the rhythm of price behavior—ideal for swing traders and volatility analysts alike.

Luma DCA Simulator (BTC only)Luma DCA Simulator – Guide

What is the Luma DCA Simulator?

The Luma DCA Tracker shows how regular Bitcoin investments (Dollar Cost Averaging) would have developed over a freely selectable period – directly in the chart, transparent and easy to follow.

Settings Overview

1. Investment amount per interval

Specifies how much capital is invested at each purchase (e.g. 100).

2. Start date

Defines the point in time from which the simulation begins – e.g. 01.01.2020.

3. Investment interval

Determines how frequently investments are made:

– Daily

– Weekly

– Every 14 days

– Monthly

4. Language

Switches the info box display between English and German.

5. Show investment data (optional)

If activated, the chart will display additional values such as total invested capital, BTC amount, current value, and profit/loss.

What the Chart Displays

Entry points: Each DCA purchase is marked as a point in the price chart.

Average entry price: An orange line visualizes the evolving DCA average.

Info box (bottom left) with a live summary of:

– Total invested capital

– Total BTC acquired

– Average entry price

– Current portfolio value

– Profit/loss in absolute terms and percentage

Note on Accuracy

This simulation is for illustrative purposes only.

Spreads, slippage, fees, and tax effects are not included.

Actual results may vary.

Technical Note

For daily or weekly intervals, the chart timeframe should be set to 1 day or lower to ensure all purchases are accurately included.

Larger timeframes (e.g. weekly or monthly charts) may result in missed investments.

Currency Handling

All calculations are based on the selected chart symbol (e.g. BTCUSD, BTCEUR, BTCUSDT).

The displayed currency is automatically determined by the chart used.

Adaptive Multi-MA OptimizerAdaptive Multi-MA Optimizer

This indicator provides a powerful, customizable solution for traders seeking dynamically optimized moving averages with precision and control. It integrates multiple custom-built moving average types, applies real-time volatility-based optimization, and includes an optional composite smoothing engine.

🧠 Key Features

Dynamic Optimization:

Automatically selects the optimal lookback length based on market volatility stability using a custom standard deviation differential model.

Multiple Custom MA Types:

Includes fully custom implementations of:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

VWMA (Volume Weighted MA)

DEMA (Double EMA)

TEMA (Triple EMA)

Hull MA

ALMA (Arnaud Legoux MA)

Composite MA Option:

A unique "Composite" mode blends all supported MAs into a single average, then applies optional smoothing for enhanced signal clarity.

Dynamic Smoothing:

The composite mode supports volatility-adjusted smoothing (based on optimized lookback), making it adaptable to different market regimes.

Fully Custom Logic:

No built-in MA functions are used — every moving average is hand-coded for transparency and educational value.

⚙️ How It Works

Optimization:

The script evaluates a range of lengths (minLen to maxLen) using the standard deviation of price returns. It selects the length with the most stable recent volatility profile.

Calculation:

The selected MA type is calculated using that optimized length. If "Composite" is chosen, all MA types are averaged and smoothed dynamically.

Visualization:

The adaptive MA is plotted on the chart, changing color based on its position relative to price.

📌 Use Cases

Trend-following strategies that adapt to different market conditions.

Traders wanting a high-fidelity composite of multiple MAs.

Analysts interested in visualizing market smoothness without lag-heavy signals.

Coders looking to learn how to build custom indicators from scratch.

🧪 Inputs

MA Type: Choose from 8 MA types or a blended Composite.

Lookback Range: Control min/max and step size for optimization.

Source: Choose any price series (e.g., close, hl2).

⚠️ Disclaimer

This indicator is for educational and informational purposes only and does not constitute financial advice, trading advice, or investment recommendations. Use of this script is at your own risk. Past performance does not guarantee future results. Always perform your own analysis and consult with a qualified financial advisor before making trading decisions.

Adaptive Normalized Global Liquidity OscillatorAdaptive Normalized Global Liquidity Oscillator

A dynamic, non-repainting oscillator built on real central bank balance sheet data. This tool visualizes global liquidity shifts by aggregating monetary asset flows from the world’s most influential central banks.

🔍 What This Script Does:

Aggregates Global Liquidity:

Includes Federal Reserve (FED) assets and subtracts liabilities like the Treasury General Account (TGA) and Reverse Repo Facility (RRP), combined with asset positions from the ECB, BOJ, PBC, BOE, and over 10 other central banks. All data is normalized into USD using FX rates.

Adaptive Normalization:

Optimizes the lookback period dynamically based on rate-of-change stability—no fixed lengths, enabling adaptation across macro conditions.

Self-Optimizing Weighting:

Applies inverse standard deviation to balance raw liquidity, smoothed momentum (HMA), and standardized deviation from the mean.

Percentile-Ranked Highlights:

Liquidity readings are ranked relative to history—extremes are visually emphasized using gradient color and adaptive transparency.

Non-Repainting Design:

Data is anchored with bar index awareness and offset techniques, ensuring no forward-looking bias. What you see is what was known at that time.

⚠️ Important Interpretation Note:

This is not a zero-centered oscillator like RSI or MACD. The signal line does not represent neutrality at zero.

Instead, a dynamic baseline is calculated using a rolling mean of scaled liquidity.

0 is irrelevant on its own—true directional signals come from crosses above or below this adaptive baseline.

Even negative values may signal strength if they are rising above the moving average of past liquidity conditions.

✅ What to Watch For:

Crossover Above Dynamic Baseline:

Indicates liquidity is expanding relative to recent conditions—supports a risk-on interpretation.

Crossover Below Dynamic Baseline:

Suggests deteriorating liquidity conditions—may align with risk-off shifts.

Percentile Extremes:

Readings near the top or bottom historical percentiles can act as contrarian or confirmation signals, depending on momentum.

⚙️ How It Works:

Bounded Normalization:

The final oscillator is passed through a tanh function, keeping values within and reducing distortion.

Adaptive Transparency:

The strength of deviations dynamically adjusts plot intensity—visually highlighting stronger liquidity shifts.

Fully Customizable:

Toggle which banks are included, adjust dynamic optimization ranges, and control visual display options for plot and background layers.

🧠 How to Use:

Trend Confirmation:

Sustained rises in the oscillator above baseline suggest underlying monetary support for asset prices.

Macro Turning Points:

Reversals or divergences, especially near OB/OS zones, can foreshadow broader risk regime changes.

Visual Context:

Use the dynamic baseline to see if liquidity is supportive or suppressive relative to its own adaptive history.

📌 Disclaimer:

This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making trading or investment decisions.

Luma DCA Tracker (BTC)Luma DCA Tracker (BTC) – User Guide

Function

This indicator simulates a regular Bitcoin investment strategy (Dollar Cost Averaging). It calculates and visualizes:

Accumulated BTC amount

Average entry price

Total amount invested

Current portfolio value

Profit/loss in absolute and percentage terms

Settings

Investment per interval

Fixed amount to be invested at each interval (e.g., 100 USD)

Start date

The date when DCA simulation begins

Investment interval

Choose between:

daily, weekly, every 14 days, or monthly

Show investment data

Displays additional chart lines (total invested, value, profit, etc.)

Chart Elements

Orange line: Average DCA entry price

Grey dots: Entry points based on selected interval

Info box (bottom left): Live summary of all key values

Notes

Purchases are simulated at the closing price of each interval

No fees, slippage, or taxes are included

The indicator is a simulation only and not linked to an actual portfolio

GCM Price Based ColorIndicator Name:

GCM Price Based Color Indicator

Detailed Description:

The GCM Price Based Color Indicator is a unique tool designed to help traders spot potential "pump" events in the market. Unlike traditional Volume Rate of Change (VROC) indicators, this script is conditional: it calculates a VROC value only when both the average volume and the price are increasing. This focus helps filter out volume surges that don't accompany immediate price appreciation, highlighting more relevant "pump" signals.

Key Features & Calculation Logic:

Conditional Volume Rate of Change (VROC):

It first calculates a Simple Moving Average (SMA) of the volume over a user-defined length (lookback period).

It then checks two conditions:

Is the current SMA volume greater than the previous bar's SMA volume (i.e., volumeIncreasing)?

Is the current close price greater than the previous bar's close price (i.e., valueIncreasing)?

Only if both volume Increasing AND value Increasing are true, a VROC value is calculated as (current _ MA _ volume - previous _ MA _ volume) * (100 / previous _ MA _ volume). Otherwise, the VROC for that bar is 0.

Historical Normalization:

The raw VROC value is then normalized against its own historical maximum value observed since the indicator was applied. This scaling brings all VROC values into a common 0-100 range.

Why is this important? Normalization makes the indicator's readings comparable across different assets (e.g., high-volume vs. low-volume stocks/cryptos) and different timeframes, making it easier to interpret the strength of a "pump" relative to its own past.

Dynamic Plot Color (Price-Based):

The plot line's color itself provides an immediate visual cue about the current bar's price action:

Green: close is greater than close (price is up for the current bar).

Red: close is less than close (price is down for the current bar).

Grey: close is equal to close (price is flat for the current bar).

Important Note: The plot color reflects the price movement of the current bar, not the magnitude of the VROC Normalized value itself. This means you can have a high vrocNormalized value (indicating a strong conditional volume surge) but a red plot color if the very next bar's price closes lower, providing a multi-faceted view.

Thresholds & Alerts:

Two horizontal lines (small Pump Threshold and big Pump Threshold) are plotted to visually mark significant levels of normalized pump strength.

Customizable alerts can be set up to notify you when VROC Normalized reaches or exceeds these thresholds, helping you catch potential pump events in real-time.

How to Use It:

Identify Potential Pumps: Look for upward spikes in the VROC Normalized line. Higher spikes indicate stronger pump signals (i.e., a larger increase in average volume coinciding with an increasing price).

Monitor Thresholds: Pay attention when the VROC Normalized line crosses above your small Pump Threshold or big Pump Threshold. These are configurable levels to suit different assets and trading styles.

Observe Plot Color: The line color provides crucial context. A high VROC Normalized (strong pump signal) with a green line indicates current price momentum is still positive. If VROC Normalized is high but the line turns red, it might suggest the initial pump is losing steam or experiencing a pullback.

Combine with Other Tools: This indicator is best used in conjunction with other technical analysis tools (e.g., support/resistance, trend lines, other momentum indicators) for confirmation and a more holistic trading strategy.

Indicator Inputs:

Lookback period (1 - 4999) (default: 420): This length determines the period for the Simple Moving Average (SMA) of volume. A higher value will smooth the volume average more, reacting slower, while a lower value will make it more reactive. Adjust based on the timeframe and asset volatility.

Big Pump Threshold (0.01 - 99.99) (default: 10.0): The normalized VROC Normalized level that signifies a "Big Pump." When VROC Normalized reaches or exceeds this level, an alert can be triggered.

Small Pump Threshold (0.01 - 99.99) (default: 0.5): The normalized VROC Normalized level that signifies a "Small Pump." This is a lower threshold for earlier or less significant pump activity.

Alerts:

Small Pump: Triggers when VROC Normalized crosses above or equals the small Pump Threshold.

Big Pump: Triggers when VROC Normalized crosses above or equals the big Pump Threshold.

Best Practices & Considerations:

Timeframes: The indicator can be used on various timeframes, but its effectiveness may vary. Experiment to find what works best for your chosen asset and trading style.

Volatility: Highly volatile assets might require different threshold settings compared to less volatile ones.

Lag: Due to the use of a Simple Moving Average (SMA) for volume, there will be some inherent lag in the calculation.

Normalization Start: The historic Max for normalization starts with a default value of 10.0. For the very first bars, or if there hasn't been a significant VROC yet, the VROC Normalized might behave differently until a true historical maximum VROC establishes itself.

Not Financial Advice: This indicator is a tool for analysis and does not constitute financial advice. Always perform your own research and manage your risk.

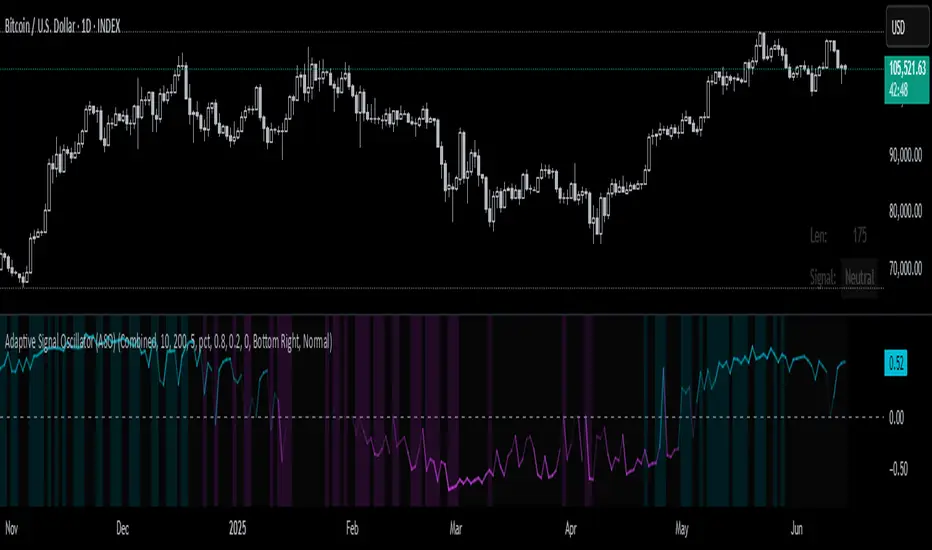

Adaptive Signal Oscillator (ASO)📘 Adaptive Signal Oscillator (ASO)

A fully dynamic, self-calibrating oscillator that adapts to any asset or timeframe by optimizing for real-time signal stability and volatility structure — without relying on static parameters or hardcoded thresholds.

🔍 Overview

The Adaptive Signal Oscillator (ASO) is a next-generation technical analysis tool designed to provide context-aware long/short signals across crypto, equities, or forex markets. Unlike traditional oscillators (RSI, Stochastics, MACD), ASO requires no manual tuning of lookback periods or overbought/oversold zones — it self-optimizes based on current market behavior.

🧠 How It Works

✅ 1. Dynamic Lookback Optimization

ASO evaluates a range of lookback lengths between user-defined minLen and maxLen. For each length, it calculates the standard deviation of returns and finds the one with the least volatility change (i.e., the most stable structure). This length is dynamically assigned as bestLen, recalculated on every bar.

✅ 2. Multi-Layer Signal Composition

Four independent signal layers are computed using bestLen:

RSI Layer: Measures relative price strength via a custom dynamic RSI.

Z-Score Layer: Standardized deviation of price from its mean.

Volatility Layer: Standard deviation of log or percent returns.

Price Position Layer: Current price percentile within the lookback window.

Each of these layers is transformed into a percentile score scaled to the range .

✅ 3. Volatility-Based Weighting

The standard deviation (volatility) of each signal layer is computed. Less volatile layers are weighted more heavily, ensuring the final composite signal prioritizes stable, consistent inputs.

Weights are normalized and combined to form a composite score, representing a dynamically blended, noise-weighted signal across the four layers.

✅ 4. Optional Adaptive Smoothing

A boolean toggle lets users apply smoothing to the final score. The smoothing window scales proportionally to bestLen, preserving adaptiveness even during trend transitions.

✅ 5. Percentile-Based Thresholding

Rather than using arbitrary fixed thresholds, ASO converts the composite score into a ranked percentile. Long/short signals are then generated based on user-defined percentile bands, adapting naturally to each asset’s behavior.

📈 Interpreting ASO

Score > Threshold → Strong long signal (highlighted in aqua).

Score < Threshold → Strong short signal (highlighted in fuchsia).

Crossing h_thresh (e.g., 0) → Neutral-to-bias change; useful for early trend cues.

The background and label update in real time to reflect the current regime and bestLen.

⚙️ Inputs

minLen, maxLen, step: Define the search range for optimal lookback length.

retMethod: Choose between log or percent return calculations.

threshHigh, threshLow: Define signal zones using percentiles.

smooth: Enable dynamic score smoothing.

h_thresh: Midline crossover zone for directional context.

⚠️ Disclaimer

This tool is designed for exploratory and educational purposes only. It does not offer financial advice or trading recommendations. Past performance is not indicative of future results.

Always consult a licensed financial advisor before making investment decisions.

Flux Capacitor (FC)# Flux Capacitor

**A volume-weighted, outlier-resistant momentum oscillator designed to expose hidden directional pressure from institutional participants.**

---

### Why "Flux Capacitor"?

The name pays homage to the fictional energy core in *Back to the Future* — an invisible engine that powers movement. Similarly, this indicator detects whether price movement is being powered by real market participation (volume) or if it's coasting without conviction.

---

### Methodology

The Flux Capacitor fuses three statistical layers:

- **Normalized Momentum**: `(Close – Open) / ATR`

Controls for raw price size and volatility.

- **Volume Scaling**:

Amplifies the effect of price moves that occur with elevated volume.

- **Robust Normalization**:

- *Winsorization* caps outlier spikes.

- *MAD-Z scoring* normalizes the signal across assets (crypto, futures, stocks).

- This produces consistent scaling across timeframes and symbols.

The result is a smooth oscillator that reliably indicates **liquidity-backed momentum** — not just price movement.

---

### Signal Events

- **Divergence (D)**: Price makes higher highs or lower lows, but Flux does not.

- **Absorption (A)**: Candle shows high volume and small body, while Flux opposes the candle direction — indicates smart money stepping in.

- **Compression (◆)**: High volume with low momentum — potential breakout zone.

- **Zero-Cross**: Indicates directional regime flip.

- **Flux Acceleration**: Histogram shows pressure rate of change.

- **Regime Background**: Color fades with weakening trend conviction.

All signals are color-coded and visually compact for easy pattern recognition.

---

### Interpreting Divergence & Absorption Correctly

Signal strength improves significantly when it appears **in the correct zone**:

#### Divergence:

| Signal | Zone | Meaning | Strength |

|--------|------------|------------------------------------------|--------------|

| Green D | Below 0 | Bullish reversal forming in weakness | **Strong** |

| Green D | Above 0 | Bullish, but less convincing | Moderate |

| Red D | Above 0 | Bearish reversal forming in strength | **Strong** |

| Red D | Below 0 | Bearish continuation — low warning value | Weak |

#### Absorption:

| Signal | Zone | Meaning | Strength |

|--------|------------|-----------------------------------------|--------------|

| Green A | Below 0 | Buyers absorbing panic-selling | **Strong** |

| Green A | Above 0 | Support continuation | Moderate |

| Red A | Above 0 | Sellers absorbing FOMO buying | **Strong** |

| Red A | Below 0 | Trend continuation — not actionable | Weak |

Look for **absorption or divergence signals in “enemy territory”** for the most actionable entries.

---

### Reducing Visual Footprint

If your chart shows a long line of numbers across the top of the Flux Capacitor pane (e.g. "FC 14 20 9 ... Bottom Right"), it’s due to TradingView’s *status line input display*.

**To fix this**:

Right-click the indicator pane → **Settings** → **Status Line** tab → uncheck “Show Indicator Arguments”.

This frees up vertical space so top-edge signals (like red `D` or yellow `◆`) remain visible and unobstructed.

---

### Features

- Original MAD-Z based momentum design

- True volume-based divergence and absorption logic

- Built-in alerts for all signal types

- Works across timeframes (1-min to weekly)

- Minimalist, responsive layout

- 25+ customizable parameters

- No future leaks, no repainting

---

### Usage Scenarios

- **Trend confirmation**: Flux > 0 confirms bullish trend strength

- **Reversal detection**: Divergence or absorption in opposite territory = high-probability reversal

- **Breakout anticipation**: Compression signal inside range often precedes directional move

- **Momentum shifts**: Watch for zero-crosses + flux acceleration spikes

---

### ⚠ Visual Note for BTC, ETH, Crude Oil & Futures

These high-priced or rapidly accelerating instruments can visually compress any linear oscillator. You may notice the Flux Capacitor’s line appears "flat" or muted on these assets — especially over long lookbacks.

> **This does not affect signal validity.** Divergence, absorption, and compression triggers still fire based on underlying logic — only the line’s amplitude appears reduced due to scaling constraints.

---

### Disclaimer

This indicator is for educational purposes only. It is not trading advice. Past results do not guarantee future performance. Use in combination with your own risk management and analysis.