[GTH decimals heatmap] (wide screen advised)Preface

I share my personal general view on indicators below; skip ahead to the Description below if you are not interested.

It is my personal conviction that most - if not all - indicators rely mainly on trader's belief that they work, and in a feedback system like free markets they might become a self-fulfilling prophecy as a result, if (!) a big part of the traders believes in it, because some famous trader releases an indicator, or such person's public statement goes viral.

One of those voodoo indicators is the famous "follow-through day". There is zero statistical evidence for its validity, beyond the validity of a statement like "If it's bright at day it's usually the sun shining". The uselessness was proven exactly on its inventor's YT channel, Investors Business Daily. According to the examiner, its inventor William J. O'Neil himself could not explain the values used for this indicator. It might have been an incidental observation at some point without general validity. A.k.a "curve fitting". Still, it's being used by many today.

Another one of those indicators is the three points reversal on the S&P 500 Volatility Index (VIX) which allegedly might potentially maybe indicate a possible shift in trend. Both indicators share an immediately problematic feature: They use absolute values. Nothing is ever absolute in a highly subjective and emotionally driven game like the markets where a lot of money can be made and lost.

Most indicators can not produce additional information since they can only re-pack price/volume action. Many times an interpretion of the distance between price and a moving average and/or the slope of a moving average deliver very similar - if not better - results than MACD, RSI etc., especially with standard settings, the origin of which are usually unknown (always a warning sign). Very few indicators can deliver information which is otherwise hard to quantify, e. g. market noise (Kaufman's Efficiency Ratio or Price Density) or volatility, standard deviation etc.

It is common knowledge that trading the markets is a game of probability. No indicator works all the time (or at all, see above). In order to make decisions based on any indicator, the probability for its validity and the conditions under which validity seemed to have occurred, must be known. Otherwise it is just coffee grounds reading under the illusion of adding to the edge, when in fact it is only adding to the trees, making it even harder to see the forest.

Description

A common belief is that whole or half-dollar prices tend to be attraction points in price action, so a number of traders include those into decision making. But are they really...?

Spoiler Alert:

Generally, it is safe to say that for the big majority of stocks there is very thin evidence for it. It depends vastly on the asset, the timeframe used and the market period (pre/post/main trading times). If at all, there seems to be an above random but still thin evidence for whole prices being significant attraction points. Interesting/surprising patterns are visible on many stocks/timeframes/session periods, though.

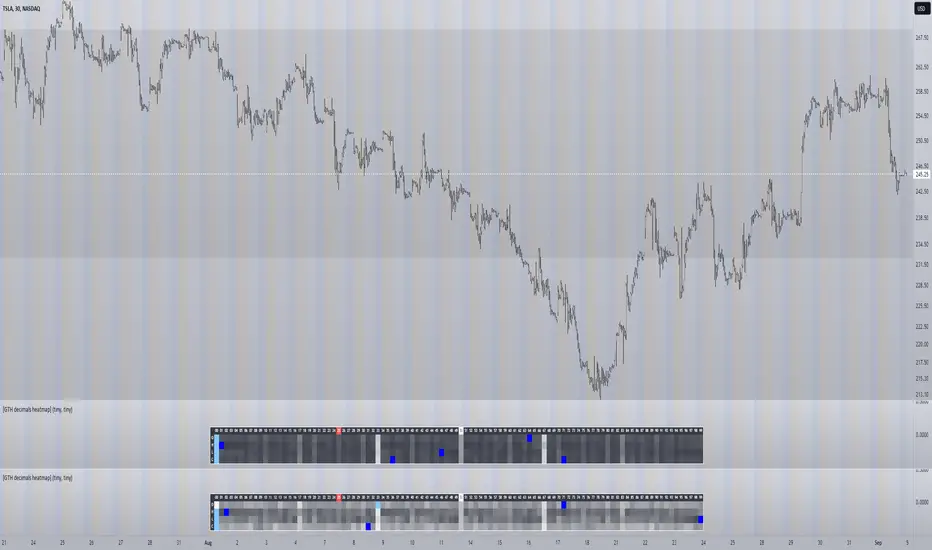

The screenshot shows TSLA, 30m timeframe, two heatmaps added. The top one shows pre/post-market data only, the bottom one main market data only. The cyan fields indicate the strongest occurrence, the dark blue fields indicate the weakest occurrence of open/high/low/close prices at the respective decimal. The red field indicates the current/last price decimal.

Clearly, TSLA displays a strong pre-market attraction for .00, followed by .33 and .67 and .50. This pattern of thirds seems to be a unique feature of TSLA. In the main trading session it is being diluted by a more random distribution.

Other interesting equities to examine:

SPY: No significant pattern on any timeframe!

META: Generally weak patterns on all timeframes, but interestingly on the 1D there is evidence for less randomness on O and H, more on L and most on C.

AAPL: 1D, foggy attraction areas around .35 and .12. Whole price is no attraction area at all! Very weak attraction around .73.

AMD: Strong pattern on D, W, M, attraction areas around 1/16th intervals. No patterns on lower timeframes.

AMZN: Significant differences between pre/post and main session. Strong 1/16th pattern below D in pre/post.

TAOP: Strong 1/5th pattern on all timeframes.

Read the tool tips and go explore!

Statistics

Candle Tick SizeHello everyone!

I dont think it exists, I couldnt find it any way I searched, maybe it is part of a bigger indicator. This is a really basic code, all it does, it shows the tick/pip size of the candles forming. You can adjust on how many candles should it show. Also because the code counts the point size of the candles from high to low, you can adjust that how many ticks are in one point, like for ES and NQ 4 ticks to a point, which is the basic setting. It helps me with entrys when I calculate the contract size so my risk/reward stays pretty much the same depending on the candle size for my entrys.

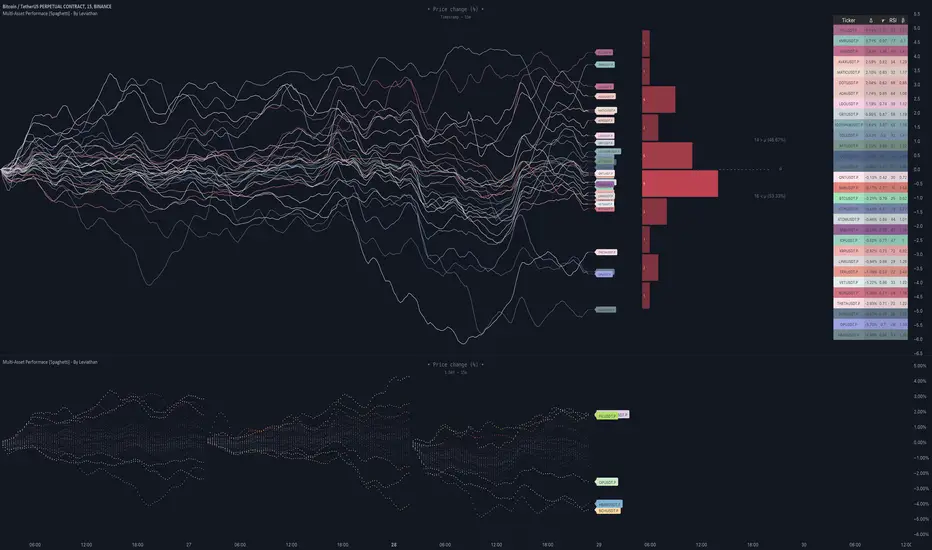

Multi-Asset Performance [Spaghetti] - By LeviathanThis indicator visualizes the cumulative percentage changes or returns of 30 symbols over a given period and offers a unique set of tools and data analytics for deeper insight into the performance of different assets.

Multi Asset Performance indicator (also called “Spaghetti”) makes it easy to monitor the changes in Price, Open Interest, and On Balance Volume across multiple assets simultaneously, distinguish assets that are overperforming or underperforming, observe the relative strength of different assets or currencies, use it as a tool for identifying mean reversion opportunities and even for constructing pairs trading strategies, detect "risk-on" or "risk-off" periods, evaluate statistical relationships between assets through metrics like correlation and beta, construct hedging strategies, trade rotations and much more.

Start by selecting a time period (e.g., 1 DAY) to set the interval for when data is reset. This will provide insight into how price, open interest, and on-balance volume change over your chosen period. In the settings, asset selection is fully customizable, allowing you to create three groups of up to 30 tickers each. These tickers can be displayed in a variety of styles and colors. Additional script settings offer a range of options, including smoothing values with a Simple Moving Average (SMA), highlighting the top or bottom performers, plotting the group mean, applying heatmap/gradient coloring, generating a table with calculations like beta, correlation, and RSI, creating a profile to show asset distribution around the mean, and much more.

One of the most important script tools is the screener table, which can display:

🔸 Percentage Change (Represents the return or the percentage increase or decrease in Price/OI/OBV over the current selected period)

🔸 Beta (Represents the sensitivity or responsiveness of asset's returns to the returns of a benchmark/mean. A beta of 1 means the asset moves in tandem with the market. A beta greater than 1 indicates the asset is more volatile than the market, while a beta less than 1 indicates the asset is less volatile. For example, a beta of 1.5 means the asset typically moves 150% as much as the benchmark. If the benchmark goes up 1%, the asset is expected to go up 1.5%, and vice versa.)

🔸 Correlation (Describes the strength and direction of a linear relationship between the asset and the mean. Correlation coefficients range from -1 to +1. A correlation of +1 means that two variables are perfectly positively correlated; as one goes up, the other will go up in exact proportion. A correlation of -1 means they are perfectly negatively correlated; as one goes up, the other will go down in exact proportion. A correlation of 0 means that there is no linear relationship between the variables. For example, a correlation of 0.5 between Asset A and Asset B would suggest that when Asset A moves, Asset B tends to move in the same direction, but not perfectly in tandem.)

🔸 RSI (Measures the speed and change of price movements and is used to identify overbought or oversold conditions of each asset. The RSI ranges from 0 to 100 and is typically used with a time period of 14. Generally, an RSI above 70 indicates that an asset may be overbought, while RSI below 30 signals that an asset may be oversold.)

⚙️ Settings Overview:

◽️ Period

Periodic inputs (e.g. daily, monthly, etc.) determine when the values are reset to zero and begin accumulating again until the period is over. This visualizes the net change in the data over each period. The input "Visible Range" is auto-adjustable as it starts the accumulation at the leftmost bar on your chart, displaying the net change in your chart's visible range. There's also the "Timestamp" option, which allows you to select a specific point in time from where the values are accumulated. The timestamp anchor can be dragged to a desired bar via Tradingview's interactive option. Timestamp is particularly useful when looking for outperformers/underperformers after a market-wide move. The input positioned next to the period selection determines the timeframe on which the data is based. It's best to leave it at default (Chart Timeframe) unless you want to check the higher timeframe structure of the data.

◽️ Data

The first input in this section determines the data that will be displayed. You can choose between Price, OI, and OBV. The second input lets you select which one out of the three asset groups should be displayed. The symbols in the asset group can be modified in the bottom section of the indicator settings.

◽️ Appearance

You can choose to plot the data in the form of lines, circles, areas, and columns. The colors can be selected by choosing one of the six pre-prepared color palettes.

◽️ Labeling

This input allows you to show/hide the labels and select their appearance and size. You can choose between Label (colored pointed label), Label and Line (colored pointed label with a line that connects it to the plot), or Text Label (colored text).

◽️ Smoothing

If selected, this option will smooth the values using a Simple Moving Average (SMA) with a custom length. This is used to reduce noise and improve the visibility of plotted data.

◽️ Highlight

If selected, this option will highlight the top and bottom N (custom number) plots, while shading the others. This makes the symbols with extreme values stand out from the rest.

◽️ Group Mean

This input allows you to select the data that will be considered as the group mean. You can choose between Group Average (the average value of all assets in the group) or First Ticker (the value of the ticker that is positioned first on the group's list). The mean is then used in calculations such as correlation (as the second variable) and beta (as a benchmark). You can also choose to plot the mean by clicking on the checkbox.

◽️ Profile

If selected, the script will generate a vertical volume profile-like display with 10 zones/nodes, visualizing the distribution of assets below and above the mean. This makes it easy to see how many or what percentage of assets are outperforming or underperforming the mean.

◽️ Gradient

If selected, this option will color the plots with a gradient based on the proximity of the value to the upper extreme, zero, and lower extreme.

◽️ Table

This section includes several settings for the table's appearance and the data displayed in it. The "Reference Length" input determines the number of bars back that are used for calculating correlation and beta, while "RSI Length" determines the length used for calculating the Relative Strength Index. You can choose the data that should be displayed in the table by using the checkboxes.

◽️ Asset Groups

This section allows you to modify the symbols that have been selected to be a part of the 3 asset groups. If you want to change a symbol, you can simply click on the field and type the ticker of another one. You can also show/hide a specific asset by using the checkbox next to the field.

Pro Bollinger Bands CalculatorThe "Pro Bollinger Bands Calculator" indicator joins our suite of custom trading tools, which includes the "Pro Supertrend Calculator", the "Pro RSI Calculator" and the "Pro Momentum Calculator."

Expanding on this series, the "Pro Bollinger Bands Calculator" is tailored to offer traders deeper insights into market dynamics by harnessing the power of the Bollinger Bands indicator.

Its core mission remains unchanged: to scrutinize historical price data and provide informed predictions about future price movements, with a specific focus on detecting potential bullish (green) or bearish (red) candlestick patterns.

1. Bollinger Bands Calculation:

The indicator kicks off by computing the Bollinger Bands, a well-known volatility indicator. It calculates two pivotal Bollinger Bands parameters:

- Bollinger Bands Length: This parameter sets the lookback period for Bollinger Bands calculations.

- Bollinger Bands Deviation: It determines the deviation multiplier for the upper and lower bands, typically set at 2.0.

2. Visualizing Bollinger Bands:

The Bollinger Bands derived from the calculations are skillfully plotted on the price chart:

- Red Line: Represents the upper Bollinger Band during bearish trends, suggesting potential price declines.

- Teal Line: Represents the lower Bollinger Band in bullish market conditions, signaling the possibility of price increases.

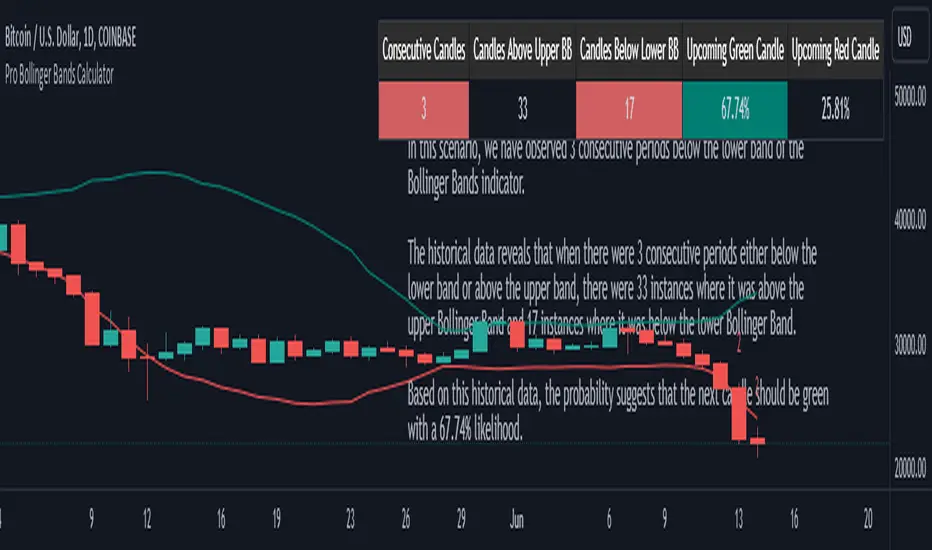

3.Analyzing Consecutive Candlesticks:

The indicator's core functionality revolves around tracking consecutive candlestick patterns based on their relationship with the Bollinger Bands lines. To be considered for analysis, a candlestick must consistently close either above (green candles) or below (red candles) the Bollinger Bands lines for multiple consecutive periods.

4. Labeling and Enumeration:

To convey the count of consecutive candles displaying consistent trend behavior, the indicator meticulously assigns labels to the price chart. The position of these labels varies depending on the direction of the trend, appearing either below (for bullish patterns) or above (for bearish patterns) the candlesticks. The label colors match the candle colors: green labels for bullish candles and red labels for bearish ones.

5. Tabular Data Presentation:

The indicator complements its graphical analysis with a customizable table that prominently displays comprehensive statistical insights. Key data points within the table encompass:

- Consecutive Candles: The count of consecutive candles displaying consistent trend characteristics.

- Candles Above Upper BB: The number of candles closing above the upper Bollinger Band during the consecutive period.

- Candles Below Lower BB: The number of candles closing below the lower Bollinger Band during the consecutive period.

- Upcoming Green Candle: An estimated probability of the next candlestick being bullish, derived from historical data.

- Upcoming Red Candle: An estimated probability of the next candlestick being bearish, also based on historical data.

6. Custom Configuration:

To cater to diverse trading strategies and preferences, the indicator offers extensive customization options. Traders can fine-tune parameters such as Bollinger Bands length, upper and lower band deviations, label and table placement, and table size to align with their unique trading approaches.

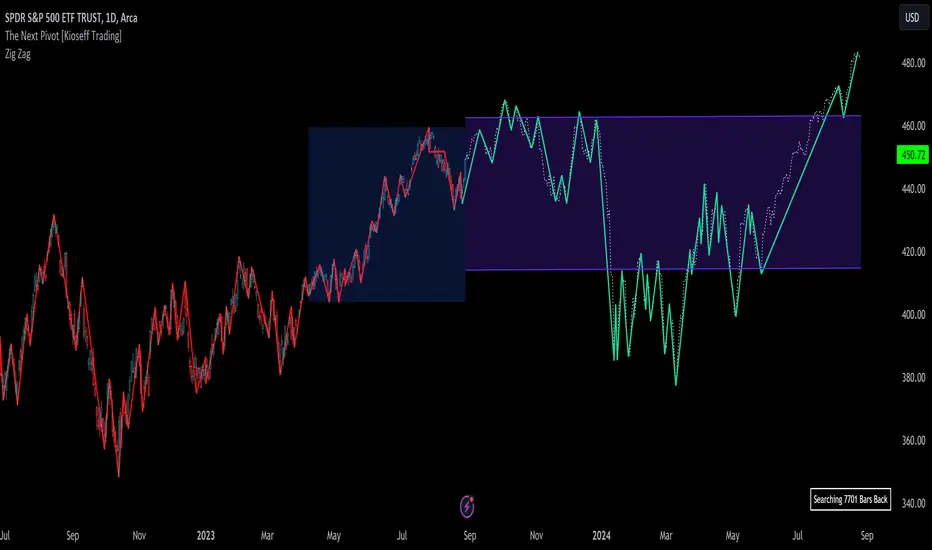

The Next Pivot [Kioseff Trading]Hello!

This script "The Next Pivot" uses various similarity measures to compare historical price sequences to the current price sequence!

Features

Find the most similar price sequence up to 100 bars from the current bar

Forecast price path up to 250 bars

Forecast ZigZag up to 250 bars

Spearmen

Pearson

Absolute Difference

Cosine Similarity

Mean Squared Error

Kendall

Forecasted linear regression channel

The image above shows/explains some of the indicator's capabilities!

The image above highlights the projected zig zag (pivots) pattern!

Colors are customizable (:

Additionally, you can plot a forecasted LinReg channel.

Should load times permit it, the script can search all bar history for a correlating sequence. This won't always be possible, contingent on the forecast length, correlation length, and the number of bars on the chart.

Reasonable Assessment

The script uses various similarity measures to find the "most similar" price sequence to what's currently happening. Once found, the subsequent price move (to the most similar sequence) is recorded and projected forward.

So,

1: Script finds most similar price sequence

2: Script takes what happened after and projects forward

While this may be useful, the projection is simply the reaction to a possible one-off "similarity" to what's currently happening. Random fluctuations are likely and, if occurring, similarities between the current price sequence and the "most similar" sequence are plausibly coincidental.

That said, if you have any ideas on cool features to add please let me know!

Thank you (:

Position and Risk Calculator (for Indices) [dR-Algo]Position and Risk Calculator : Your Ultimate Risk Management Tool for Indices

The difference between a novice and a seasoned trader often comes down to one essential element: risk management. While trading indices, the challenges are even more intense due to market volatility and leverage. The Position and Risk Calculator steps in here to bridge the gap, providing you with an efficient tool designed exclusively for indices trading.

Key Features:

User-Friendly Interface: Designed to integrate effortlessly with your TradingView chart, this tool's interface is intuitive and clutter-free.

Dynamic Price Level Adjustment: Move your Entry, Stop Loss, and Take Profit levels directly on the chart for an interactive experience.

Account Balance Input: Customize the tool to understand your unique financial situation by inputting your current account balance.

Trade Risk Customization: Define how much you're willing to risk per trade, and the tool will do the rest.

Automated Calculations: The indicator calculates the maximum monetary risk and translates it into the maximum lot size you can afford. It delivers a full-integer lot size to make your trading decisions easier.

Comprehensive Risk Evaluation: Beyond lot sizes, it provides you with the Cost-to-Reward Ratio (CRV) of your trade, the actual monetary risk according to the calculated lot size, and the potential profit.

How To Use:

Once you add the Position and Risk Calculator to your TradingView chart, a new interactive panel appears. Here’s how it works:

Set Price Levels: Using draggable lines on the chart, set your Entry Price, Stop Loss, and Take Profit levels.

Account Details: Go to settings and enter your Account Balance and your desired risk percentage per trade.

Automatic Calculations: As soon as the above details are set, the indicator goes to work. It first calculates your maximum risk in monetary terms and then translates that into the maximum lot size you can take for the trade.

Review and Trade: The indicator shows you all the vital statistics - CRV of the trade, the money at risk according to the calculated lot size, and the possible profit.

Why Choose This Tool?

Informed Decisions: Your trading decisions will be based on concrete numbers, removing guesswork.

Time-saving: No need for manual calculations or using separate tools; everything is in one place.

Focus on Trading: By automating the risk management aspect, this tool allows you to focus more on your trading strategy and market analysis.

Tailor-Made for Indices: Unlike many other tools that try to serve all markets, the Position and Risk Calculator is designed specifically for indices trading.

Remember, effective risk management is what separates successful traders from those who burn out. The Position and Risk Calculator not only helps you define your risk but also helps you understand it, empowering you to trade with confidence.

So why not give yourself the best chance of success? Add the Position and Risk Calculator to your TradingView setup and experience the difference it can make.

Ticker Correlation Matrix Table and Heatmap [SS]Hello everyone,

I am in the process of releasing some of my own utility indicators/things I use to reference and perform analyses.

I do a lot of quantitative/math based analyses, including correlation assessments that I traditionally would need to export data from Tradingview and perform in SPSS, Excel or R. I have been slowly building a repertoire of Excel/R functionality right on pinescript so I do not need to constantly export data and can perform the assessments right on Tradingview.

This is an example of such an indicator.

About the Indicator:

It is a correlation table/matrix indicator. It will allow up to 10 ticker inputs, which can be stocks, economic data, anything available on Tradingview, and it will perform a correlation assessment in a matrix / heatmap style.

The indicator will show the various correlations among all of the selected ticker inputs and will colour them based on correlation strength and type.

Strong negative correlations will appear bright red.

Strong positive correlations will appear bright green.

Complete absence of correlation (i.e. 0) will show bright orange.

The rest will show a darker shade to indicate less strength/correlation.

Calculation Functions

In addition to outputting a correlation matrix, the indicator is also able to express the relationship between tickers in a linear expression using the y = mx + b formula.

If we look at table, we can see that MSFT and AAPL have a significantly strong correlation of 0.82.

If we wanted to express this relationship mathmatically, we can ask the indicator to represent the linear relationship in our y = mx + b format. We simply toggle to our menu and select the Convert From MSFT (Ticker 2) and convert to APPL (Ticker 3):

When we select this, a new table will populate below and give you the expression as well as the amount of error associated with it:

In this case, we can see that the equation is y = 0.553x + 0.626 with a range of around 10 points in either direction.

This means that, to convert MSFT to AAPL, we would multiply the MSFT price by 0.553 and then add 0.626. So if we try it, MSFT closed at 328.41. So we substitute:

AAPL price = 0.553(328.41) + 0.626

AAPL price = 181.61 + 0.626

AAPL Price = 182.24 +/- 10

AAPL actually closed at 184.12. So pretty good. If we try another, let's do SPY to XLF:

So we substitute, SPY closed at 449.16.

XLF Price = 449.16(0.077) + 0.084

XLF price = 34.59 + 0.084

XLF price = 34.67

XLF actually closed at 34.49.

This is handy if you want to see how one stock price may affect another. If you are long on one stock and short on another, you can use this to determine what the likely outcome may be for the alternative stock. However, I recommend only performing this on tickers that have a relationship of 0.7 or higher, or a relationship of -0.7 or lower.

I always had to use SPSS to do this, so being able to do this right in Pinescript for me is a huge convenience!

Some other uses:

As I tend to post educational stuff on Tradingview and I frequently use correlation matrices, I have formatted the indicator to be more aesthetically pleasing for these purposes. Thus, you can unselect extra ticker slots that you do not need. IF I only need to display 3 tickers, I can unselect tickers 4 - 10. The end result is a cleaner table:

Essential Functions:

The assessment length is defaulted to 75 candles on the daily timeframe. Be sure to have the daily timeframe opened when you are viewing the indicator.

You can increase or decrease the assessment length as you desire.

You can also specify the source. The source is defaulted to close, but if you want to see the direct correlation of ticker's highs and/or lows, you can modify the source input in the settings menu to look at this.

Just remember to have the chart opened to whatever timeframe you are looking at.

And that's the indicator! Hopefully you find it helpful. Its more of an academic indicator, but it is performing a function that I personally use frequently in analyses, so I hope you may also benefit from it as well!

Thanks for checking it out! Safe trades everyone!

Bollinger Bands Heatmap (BBH)The Bollinger Bands Heatmap (BBH) Indicator provides a unique visualization of Bollinger Bands by displaying the full distribution of prices as a heatmap overlaying your price chart. Unlike traditional Bollinger Bands, which plot the mean and standard deviation as lines, BBH illustrates the entire statistical distribution of prices based on a normal distribution model.

This heatmap indicator offers traders a visually appealing way to understand the probabilities associated with different price levels. The lower the weight of a certain level, the more transparent it appears on the heatmap, making it easier to identify key areas of interest at a glance.

Key Features

Dynamic Heatmap: Changes in real-time as new price data comes in.

Fully Customizable: Adjust the scale, offset, alpha, and other parameters to suit your trading style.

Visually Engaging: Uses gradients of colors to distinguish between high and low probabilities.

Settings

Scale

Tooltip: Scale the size of the heatmap.

Purpose: The 'Scale' setting allows you to adjust the dimensions of each heatmap box. A higher value will result in larger boxes and a more generalized view, while a lower value will make the boxes smaller, offering a more detailed look at price distributions.

Values: You can set this from a minimum of 0.125, stepping up by increments of 0.125.

Scale ATR Length

Tooltip: The ATR used to scale the heatmap boxes.

Purpose: This setting is designed to adapt the heatmap to the instrument's volatility. It determines the length of the Average True Range (ATR) used to size the heatmap boxes.

Values: Minimum allowable value is 5. You can increase this to capture more bars in the ATR calculation for greater smoothing.

Offset

Tooltip: Offset mean by ATR.

Purpose: The 'Offset' setting allows you to shift the mean value by a specified ATR. This could be useful for strategies that aim to capitalize on extreme price movements.

Values: The value can be any floating-point number. Positive values shift the mean upward, while negative values shift it downward.

Multiplier

Tooltip: Bollinger Bands Multiplier.

Purpose: The 'Multiplier' setting determines how wide the Bollinger Bands are around the mean. A higher value will result in a wider heatmap, capturing more extreme price movements. A lower value will tighten the heatmap around the mean price.

Values: The minimum is 0, and you can increase this in steps of 0.2.

Length

Tooltip: Length of Simple Moving Average (SMA).

Purpose: This setting specifies the period for the Simple Moving Average that serves as the basis for the Bollinger Bands. A higher value will produce a smoother average, while a lower value will make it more responsive to price changes.

Values: Can be set to any integer value.

Heat Map Alpha

Tooltip: Opacity level of the heatmap.

Purpose: This controls the transparency of the heatmap. A lower value will make the heatmap more transparent, allowing you to see the price action more clearly. A higher value will make the heatmap more opaque, emphasizing the bands.

Values: Ranges from 0 (completely transparent) to 100 (completely opaque).

Color Settings

High Color & Low Color: These settings allow you to customize the gradient colors of the heatmap.

Purpose: Use contrasting colors for better visibility or colors that you prefer. The 'High Color' is used for areas with high density (high probability), while the 'Low Color' is for low-density areas (low probability).

Usage Scenarios for Settings

For Volatile Markets: Increase 'Scale ATR Length' for better smoothing and set a higher 'Multiplier' to capture wider price movements.

For Trend Following: You might want to set a larger 'Length' for the SMA and adjust 'Scale' and 'Offset' to focus on more probable price zones.

These are just recommendations; feel free to experiment with these settings to suit your specific trading requirements.

How To Interpret

The heatmap gives a visual representation of the range within which prices are likely to move. Areas with high density (brighter color) indicate a higher probability of the price being in that range, whereas areas with low density (more transparent) indicate a lower probability.

Bright Areas: Considered high-probability zones where the price is more likely to be.

Transparent Areas: Considered low-probability zones where the price is less likely to be.

Tips For Use

Trend Confirmation: Use the heatmap along with other trend indicators to confirm the strength and direction of a trend.

Volatility: Use the density and spread of the heatmap as an indication of market volatility.

Entry and Exit: High-density areas could be potential support and resistance levels, aiding in entry and exit decisions.

Caution

The Bollinger Bands Heatmap assumes a normal distribution of prices. While this is a standard assumption in statistics, it is crucial to understand that real-world price movements may not always adhere to a normal distribution.

Conclusion

The Bollinger Bands Heatmap Indicator offers traders a fresh perspective on Bollinger Bands by transforming them into a visual, real-time heatmap. With its customizable settings and visually engaging display, BBH can be a useful tool for traders looking to understand price probabilities in a dynamic way.

Feel free to explore its features and adjust the settings to suit your trading strategy. Happy trading!

Pairs Trade DataThis indicator is helpful when doing pairs trade as when a pair is charted in the style of StockA/StockB, it will display a table with data on the two stocks, mainly the price, and the individual tickers with exchanges.

JK - Q SuiteThis indicator is primarily for identifying pauses in Stage 2 uptrends, modelled on Qullamaggie's style of trading, but fits well with many traders including William O' Neil. or Mark Minervini.

I built this for my own purposes, and have gradually added range of tools into a single suite. My goal has also to be as clean as possible, while providing clear, actionable information.

This suite includes all of the following:

Moving averages (10, 20, 50, 200)

Coloured bars showing tightening price (blue under 75% of ADR, orange under 50% of ADR)

A 'markets' dashboard (top-right), showing the major indexes. Red if 10<20MA, or price <20MA

A 'sectors' dashboard (top-right, below markets). Red if 5<10MA, or price <10MA - see note below

Strength / Weakness information - two cells at the top, bottom-right. See below

Stock information - glanceable stock info as quick filters. The thresholds for ADR, Average volume, and Dollar Volume can be customised.

NOTE - if the 'tightening coloured candles' are not showing, the indicator needs to be at the top of the stack. Click the triple squares at the very bottom-right of the TradingView interface, and drag the indicator to the top, should work then!

=============

Sectors

These are based on the 11 official Sectors, tracked using index funds (XLY, XLK etc). HOWEVER, TradingView does NOT use the official 11 sectors - therefore I've done my best to match TradingViews ones to the official ones, but doesn't always work... e.g. 'Electronic Technology' is typically semiconductors, which are classes as 'Industrials', but Apple is the same sector in TV, but classed as 'Technology' using the official 11 Sectors.

If TradingView move to use the official 11 I'll update this, but for now it's a best guess and will sometimes be wrong, sorry!

Strength / Weakness information

This was an experiment in trying not to give too much back to the market! Typically the strategy would be to sell if price closes below 10MA (Weakness), however there may be large pops that can be advantageous to sell into.

The 'Strength' information (top cell, bottom-right), checks how far the price is extended above 10MA - this is customisable as a multiple of ADR. You may find that in weak markets (like now), it can be best to take profits quickly - in good markets, you could increase this as stocks make bigger or more sustained moves.

=============

While I'm not the best coder - and I've hacked and tried and changed different things - this has been a labour of love and essential for me.

If you have any suggestions, while I may or may not be able to implement them, I'm certainly open to ideas!

Crypto/DXY ScoringHi!

This indicator "Crypto/DXY Scoring", a multi-purpose script, consists of various comparison statistics (including an alternative RS/RSMOM model) to show the strength of a currency against the DXY.

Features

"Contrived" RS/RSMOM alternative model

Compare the strength of the crypto currency on your chart to any asset (DXY default)

Glass's ∆

Z-comparison

Hedges' g

Cliff's Delta

Z-score for log returns

RRG graph (with adjusted dimensions) Traditional RRG graph coming soon (:

Let's go over some simplified interpretations of what's shown on the chart!

The image above provides generalized interpretations for the three of the data series plotted by the indicator.

The image above further explains the other plots for the indicator!

The image above shows the final result!

Underlying Theory

"When the dollar is strong as indicated by the DXY, it usually means that investors are seeking safety in traditional assets. Bitcoin (crypto) is often considered a "risk-on" asset, meaning investors might sell BTC in favor of holding dollars, thus driving BTC prices down."

Given the complexities associated with this relationship, including its contentious implications and a variable correlation between crypto and the DXY, this theory is one within a plethora.

That said, regardless of accuracy, this indicator adheres to the theory outlined above (:

The image above shows the purpose of the red/lime columns and the corresponding red/green lines.

Should the crypto on your chart and the DXY (or comparison symbol) exhibit negative correlation, and should the performance of DXY (or comparison symbol) hold any predictive utility for the subsequent performance of the crypto on your chart, the red columns violating the red line might indicate an upcoming "dump" for the crypto on your chart.

Lime green columns violating the green line may indicator an inverse response.

Alternative Relative Rotation Graph

In its current state, the alternated dimensions for the Relative Rotation Graph cause it to function more as a "Relative Performance Graph".

Fear not; a traditional RRG graph is coming soon!

The image above shows our alternative RRG!

Interpretation

With this model, you can quickly/intuitively assess the relative performance of the display cryptos against an index of their performance.

The image above shows generalized interpretations of the model!

That's it for this indicator! Thank you for checking it out; more to come (:

CE - 42MACRO Fixed Income and Macro This is Part 2 of 2 from the 42MACRO Recreation Series

However, there will be a bonus Indicator coming soon!

The CE - 42MACRO Fixed Income and Macro Table is a next level Macroeconomic and market analysis indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro regimes,

track a multiplex of important Assets, Indices, Bonds and ETF's to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction.

For traders and especially investors, the unique functionalities will be of high value.

Quick guide on how to use it:

docs.google.com

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form an advanced,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 1nd part "CE - 42MACRO Equity Factor"

for a more wholistic approach and higher accuracy.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets:

Convertibles ( AMEX:CWB )

Leveraged Loans ( AMEX:BKLN )

High Yield Credit ( AMEX:HYG )

Preferreds ( NASDAQ:PFF )

Emerging Market US$ Bonds ( NASDAQ:EMB )

Long Bond ( NASDAQ:TLT )

5-10yr Treasurys ( NASDAQ:IEF )

5-10yr TIPS ( AMEX:TIP )

0-5yr TIPS ( AMEX:STIP )

EM Local Currency Bonds ( AMEX:EMLC )

BDCs ( AMEX:BIZD )

Barclays Agg ( AMEX:AGG )

Investment Grade Credit ( AMEX:LQD )

MBS ( NASDAQ:MBB )

1-3yr Treasurys ( NASDAQ:SHY )

Bitcoin ( AMEX:BITO )

Industrial Metals ( AMEX:DBB )

Commodities ( AMEX:DBC )

Gold ( AMEX:GLD )

Equity Volatility ( AMEX:VIXM )

Interest Rate Volatility ( AMEX:PFIX )

Energy ( AMEX:USO )

Precious Metals ( AMEX:DBP )

Agriculture ( AMEX:DBA )

US Dollar ( AMEX:UUP )

Inverse US Dollar ( AMEX:UDN )

Functionalities:

Fixed Income and Macro Table

Shows relative market Asset performance

Comes with different Calculation options like RoC,

Sharpe ratio, Sortino ratio, Omega ratio and Normalization

Allows for advanced market (health) performance

Provides the calculated, realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Visuals - for your best experience only use one (+ BarColoring) at a time:

You can visualize all important metrics:

- GRID regimes of the currently chosen calculation type

- Risk On/Risk Off with background colouring and additional +1/-1 values

- a smoother GRID model

- a smoother Risk On/ Risk Off metric

- Barcoloring for enabled metric of the above

If you have more suggestions, please write me

Fixed Income and Macro:

The visualisation of the relative performance of the different assets provides valuable information about the current market environment and the actual market performance.

It furthermore makes it possible to obtain a deeper understanding of how the interconnected market works and makes it simple to identify the actual market direction,

thus also providing all the information to derive overall market health, market strength or weakness.

Utility:

The Fixed Income and Macro Table is divided in 4 Columns which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Fixed Income/ Macro Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Fixed Income/ Macro Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

******

This Indicator again is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.

If you have questions or need a more in-depth guide DM me.

GM

Multiple Percentile Ranks (up to 5 sources at a time)This indicator is a visual percentile rank indicator that can display 1 to 5 sources at one time.

The options:

“Sources”

Choose the number of sources you would like to display. The minimum is 1, the maximum is 5.

“Label percent position”

The label for the current percentage of where the source candle ranks.

“Label position”

This displays the source/s you’ve selected, and the chosen bottom rank % and top rank %.

“Label text size”

Displays the text size of all labels.

“Display current % labels”

Switches the labels on/off only for the current percentage rank of each source.

Source options:

ATR: Average True Range

CCI: Commodity Channel Index

COG: Centre of Gravity

Close: closing price

Close Percent: close percentage from previous close

Dollar Value: volume * (high * low * close / 3)

EOM: Ease of Movement: how much volume it takes to move the price in a certain direction

OBV: On-Balance Volume

RANGE: percentage range of the close price

RSI: Relative Strength Index

RVI: Relative Vigor Index

Time Close: if you select the 1 second timeframe it will provide the gap of time between each 1 second close

Volume: each bar’s volume

Volume (MA): volume moving average

Source # where # is the number of the source. Selects the source you’d like.

Ma Length is the number of previous candles to consider when calculating the moving average of the source. Note, the “MA Length” only applies to sources that have the “(MA)” at the end of their name.

Bottom % is the bottom percentage rank of the source you’ve selected. This is a filter to display the candle line graph in red once the percentage rank is equal to the percentage you’ve chosen or below.

Top % is the top percentage rank of the source you’ve selected. This is a filter to display the candle line graph in green once the percentage rank is equal to the percentage you’ve chosen or higher.

A simple example of how to use the indicator:

Select the dropdown menu for source 1 and select volume.

As the candles populate, it will look at previous candles and assign a percentage rank of where the candles are in relation to previous candles.

*Note, the way Tradingview works is it will populate the first candle the chart was active, and continue on. So, let’s say the 3rd candle was the highest volume day. This candle will show up as 100%. If the next day, the 4th candle has an even higher volume, it will show up as 100% also, the previous candles won’t “repaint” to other values and are instead set based on when they were confirmed. So, this indicator works best when there are a lot of previous candles to compare itself to.

To use the bottom % rank filter enter a percentage such as 5%. As it comes across a candle that is 5% or less compared to previous volume candles, then the line graph will shade in red.

The same can be said for the top % rank. So, if you want to see the line graph change to green when it comes across the top 99th percentile rank of volume bars, then set the top % rank to 1% and it will give you extremely high-volume bars in green instead of blue.

COT TFF Data (S&P_500_CONSOLIDATED)Commitment of Traders - Traders in Financial Futures (Futures and Options)

Custom python script is used to create the Pinescript strings from a spreadsheet containing the dates + net positions. Data is then input manually in Pinescript (can only fit 4-5 years of data).

This data set is from the: S&P_500_CONSOLIDATED

Source: cftc.gov

COT TFF Data (VIX_FUTURES)Commitment of Traders - Traders in Financial Futures (Futures and Options)

Custom python script is used to create the Pinescript strings from a spreadsheet containing the dates + net positions. Data is then input manually in Pinescript (can only fit 4-5 years of data).

This data set is from the: VIX_FUTURES

Source: cftc.gov

dharmatech : Standard Deviation ChannelDESCRIPTION

Based on version by leojez.

Adds a 3rd standard deviation level.

Twice as fast as original version.

Refactored and simplified source code.

HOW TO USE

Load your chart

Adjust the timeframe and zoom of the chart so that the trend you're interested in is in view.

Add the indicator

Use the measuring tool to measure the number of bars from the start of the trend to the latest candle.

Open settings for the indicator.

Set the length value to the number of bars that you noted.

All Candlestick Patterns on Backtest [By MUQWISHI]▋ INTRODUCTION :

The “All Candlestick Patterns on Backtest” indicator generates a table that offers a clear visualization of the historical return percentages for each candlestick pattern strategy over a specified time period. This table serves as an organized resource, serving as a launching point for in-depth research into candle formations. It may help to rectify any misconceptions surrounding candlestick patterns, refine trading approaches, and it could be foundation to make informed decisions in trading journey.

_______________________

▋ OVERVIEW:

_______________________

▋ CREDIT:

Credit to public technical “*All Candlestick Patterns*” indicator.

_______________________

▋ TABLE:

_______________________

▋ CHART:

_______________________

▋ INDICATOR SETTINGS:

#Section One: Table Setting

#Section Two: Backtest Setting

(1) Backtest Starting Period.

Note: If the datetime of the first candle on the chart is after the entreated datetime, the calculation will start from the first candle on the chart.

(2) Initial Equity ($).

(3) Leverage: Current Equity x Leverage Value.

(4) Entry Mode:

- “At Close”: Execute entry order as soon as the candle confirmed.

- “Breakout High (Low for Short)”: Stop limit buy order, entry order will be executed as soon as the next candle breakout the high of last pattern’s candle (low for short)

(5) Cancel Entry Within Bars: This option is applicable with {Entry Mode = Breakout High (Low for Short)}, to cancel the Entry Order if it's not executed within certain selected number of bars.

(6) Stoploss Range: the range refers to high of pattern - low of pattern.

(7) Risk:Reward: the calculation of risk:reward range start from entry price level. For example: A pattern triggered with range 10 points, and entry price is 100.

- For 1:1~risk:reward would the stoploss at 90 and takeprofit at 110.

- For 1:3~risk:reward would the stoploss at 90 and takeprofit at 130.

#Section Three: Technical & Candle Patterns

_______________________

▋ Comments:

This table was developed for research and educational purposes.

Candlestick patterns are almost similar as seen in “*All Candlestick Patterns*” indicator.

The table results should not be taken as a major concept to build a trading decision.

Personally, I see candlestick patterns as a means to comprehend the psychology of the market, and help to follow the price action.

Please let me know if you have any questions.

Thank you.

CE - 42MACRO Equity Factor Table This is Part 1 of 2 from the 42MACRO Recreation Series

The CE - 42MACRO Equity Factor Table is a whole toolbox packaged in a single indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro Regime, use a multiplex of important Assets and Indices to form a high probability Implied Correlation expectation and allows to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction, as well as the underlying asset.

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form a proper,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 2nd part "CE - 42MACRO Yield and Macro"

for a more wholistic approach and higher accuracy.

Due to coding limitations they can not be merged into one Indicator.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets, with more to come:

Dividend Compounders ( AMEX:SPHD )

Mid Caps ( AMEX:VO )

Emerging Markets ( AMEX:EEM )

Small Caps ( AMEX:IWM )

Mega Cap Growth ( NASDAQ:QQQ )

Brazil ( AMEX:EWZ )

United Kingdom ( AMEX:EWU )

Growth ( AMEX:IWF )

United States ( AMEX:SPY )

Japan ( AMEX:DXJ )

Momentum ( AMEX:MTUM )

China ( AMEX:FXI )

Low Beta ( AMEX:SPLV )

International ex-US ( NASDAQ:ACWX )

India ( AMEX:INDA )

Eurozone ( AMEX:EZU )

Quality ( AMEX:QUAL )

Size ( AMEX:OEF )

Functionalities:

1. Correlations

Takes a measure of Cross Market Correlations

2. Implied Trend

Calculates the trend for each Asset and uses the Correlation to obtain the Implied Trend for the underlying Asset

There are multiple functionalities to enhance Signal Speed and precision...

Reading a signal only over a certain threshold, otherwise being colored in gray to signal noise or unclear market behavior

Normalization of Signal

Double Normalization of Signal for more Speed... ideal for the Crypto Market

Using an additional Hull Moving Average to enhance Signal Speed

Additional simple Background coloring to get a Signal from the HMA

Barcoloring based on the Implied Correlation

3. Equity Factor Table

Shows market realized Asset performance

Provides the approximate realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Now into the juicy stuff...

Visuals:

There is a variety of options to change visual settings of what is plotted and where

+ additional considerations.

Everything that is relevant in the underlying logic which can improve comprehension can be visualized with these options.

More to come

Market Correlation:

The Market Correlation Table takes the Correlation of all the Assets to the Asset on the Chart,

it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single Asset.

(To enhance the Signal you can apply the mentioned Indicator on the relevant Assets to find your target Asset movements that you intend to capture...

and then change the length of the Indicator in here)

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement.

This is strengthened by taking the average of all Implied Trends.

Thus the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset over the defined time duration,

providing alpha for Traders and Investors alike.

Equity Factors:

The table provides valuable information about the current market environment (whether it's risk on or risk off),

the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction,

makes it possible to derive overall market Health and shows market strength or weakness.

Utility:

The Equity Factor Table is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

This whole Indicator, as well as the second part, is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.

If you have questions or need a more in-depth guide DM me.

Will make a guide to all functionalities if necessity becomes apparent.

GM

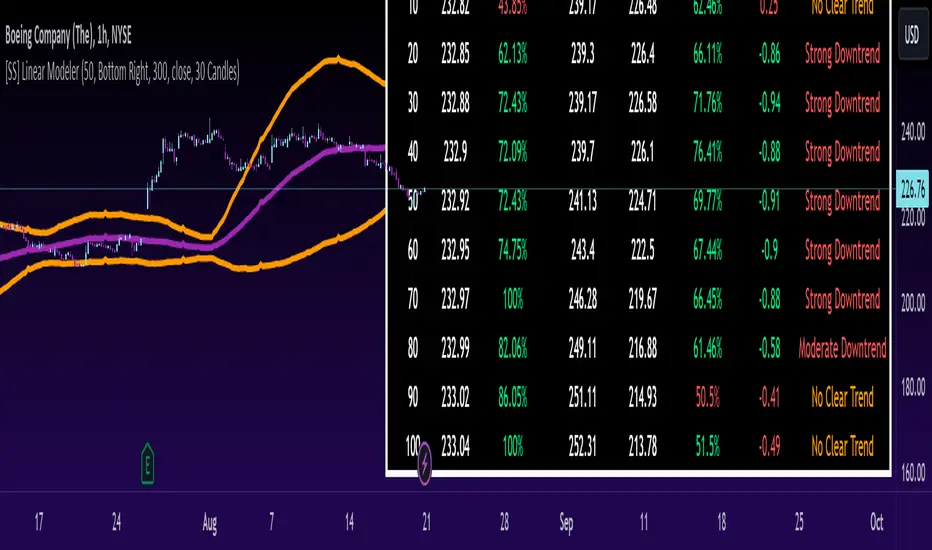

[SS] Linear ModelerHello everyone,

This is the linear modeler indicator.

It is a statistical based indicator that provides a likely price target and range based on a linear regression time series analysis.

To represent it visually, all the indicator does is it represents a linear regression channel and actually plots out the range at various points based on the current trend (see the chart below):

The indicator will perform the same assessment, but give you a working range and timeline for targets.

As well, the indicator will back-test the range and variables to see how it is performing and how reliable the results are likely to be.

General Functions:

In the chart above you can see all the various parameters and functions.

The indicator will display the most likely target (MLT) to be expected within the next pre-determined timeframe (by candles).

So for the first target, the indicator is saying within the next 10 candles, BA's MLT is 221.46 and based on BT results the reliability of this assessment is around 46%.

The indicator will also display the anticipated range at each designated timeframe.

In the chart above, we can see that at 20 candles, the likely range that BA should be trading in is 204 and 238 with a reliability of around 62% based on previous performance.

Plot Functions:

As this is performing a linear time series projection, you can have the indicator plot the projected ranges. Simply go to the settings menu and select the desired forecast length:

This will plot out the desired range and result over the specified time period. Here is an example of BA plotted over the next 50 candles on the hourly:

You can technically use this as an SMA/EMA type indicator, just keep in mind it may be a bit slower than a traditional EMA and SMA indicator, as it is processing a lot of data and plotting out forecasted data as opposed to an SMA or EMA.

If you wish to use it as an EMA or SMA, you can unselect the "Display Chart" Function to hide the table, and you can also select the "Plot Label" function. This will display the current projection analytics directly on your plotted line so you don't need to reference the table at all:

Tips on use:

I use this on the larger and smaller timeframes. On all timeframes, I will look to targets that display 90% to 100% in the BT results.

Bear in mind, this does not mean that we will 100% of the time hit this target, these targets can fail, it just means that there is a higher confidence of hitting this target than other, less reliable targets.

I will plot these targets out if they fall within the implied range of the timeframe I am looking at and will act on them according to the price action.

This is a great indicator to use in combination with other range based indicators. If you use the implied range from options to help guide your trading, you can see which targets are likely to be hit based on the current trend that fall within that implied range.

You can also assess the strength of the trends at various points in time and have an actionable range with a reliability reading at various points in time.

That is pretty much the bulk of the indicator.

Hopefully you find it helpful and useful.

As always, leave your questions and suggestions below.

Thanks for reading and checking it out!

Guassian Distribution Forecast [prediction intervals]The Indicator

The Indicator combines volatility and frequency distributions to forecast an area of possible price expansion with an approximate confidence interval / level and level of significance (significance level).

The Script Formula

Additional comments

To alter the models forecasting precision to reflect a given confidence interval, e.g the 90% confidence level (C.L.), use the 1.64 multiplier (toggle value in "Standard normal distribution sd" setting), to use a specific C.L., e.g. the 85th percentile either search for this on google, or calculate it yourself using a Standard Normal Distribution Probability table. Additionaly volatility may be changed by toggling the lookback period setting, this can be thought of as widening the distribution tails.

The look forward parameter is currently fixed at 20, this is because it does not currently work correctly with higher integers, I will try resolve this problem and any other bugs as soon as possible

External Indicator Analysis Overlay | Buy/Sell | HTF Heikin-AshiThis chart overlay offers multiple candlestick display options. The Regular (Japanese) and the Heikin-Ashi candles are well known. The Mari-Ashi (or Renko) option is something special as it should be timeframe independent, so that sideways action should be represented in one candle. That is difficult to realize as an overlay on the normal candlestick structure, but perhaps the chosen implementation is useful nonetheless. The Velocity option is experimental and is designed to show if the price has accelerated too much in a trend direction. In this case, the highs and lows do not reflect the actual highs and lows, but indicate the overshooting velocity. The opening of the candle also depends on the inherent velocity, but the close of the candle is always the actual close. Anyway, it doesn't look very useful, but the option is there.

All options can be applied to higher timeframes. A usable setting is obtained by disabling only the body of the TradingView candles in regular mode and enabling this overlay.

A large part of this overlay consists of buy/sell indication settings. For activation it is necessary to select an external source. For example the “Relative Bi-Directional Volatility Range”, specifically the Trend Shift Signal (TSS). This signal switches from 0 to 1, if the trend becomes bullish or from 0 to -1, if the trend becomes bearish. It will be automatically detected without specifying the Indication Type. Alternatively, the Volatility Moving Average (VMA) would meet the requirements for the Indication Type “Buy = positive | Sell = negative”. The Moving Average Convergence Divergence (MACD) also fulfills these conditions. Another example is to use any Moving Average with the Indication Type “Buy = rising | Sell = falling”. In the chart above the Hull Moving Average (HMA) is used. In addition, it is possible to reverse the signal, so that positive signals become negative and vice versa. The signals will be labeled as Buy or Sell on the chart.

The user can analyze whether the provided signals are good or bad indications for going long or short or simply for rebalancing a portfolio. Therefore, it is possible to set a starting point for the analysis and choose a weighting for the investments from 0% to 100% of the portfolio. To avoid sleepless nights, a very reliable (and conservative) setting seems to be Rebalancing with 50% (very similar to the well-known 60/40 portfolio). The calculation results are shown in a table.

As a small addition there is the possibility to label the peaks by setting the distance between the highs/lows. This will make the quality of the buy and sell signals even more clear.

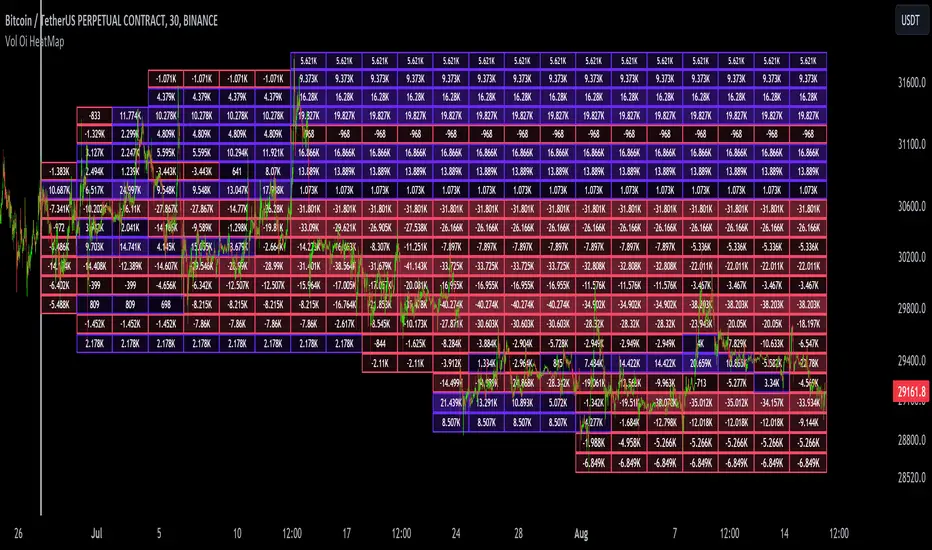

Dynamic Liquidity Map [Kioseff Trading]Hello!

Just a quick/fun project here: "Dynamic Heatmap".

This script draws a volume delta or open interest delta heatmap for the asset on your chart.

The adjective "Dynamic" is used for two reasons (:

1: Self-Adjusting Lower Timeframe Data

The script requests ~10 lower timeframe volume and open interest data sets.

When using the fixed range feature the script will, beginning at the start time, check the ~10 requested lower timeframes to see which of the lower timeframes has available data.

The script will always use the lowest timeframe available during the calculation period. As time continues, the script will continue to check if new lower timeframe data (lower than the currently used lowest timeframe) is available. This process repeats until bar time is close enough to the current time that 1-minute data can be retrieved.

The image above exemplifies the process.

Incrementally lower timeframe data will be used as it becomes available.

1: Fixed range capabilities

The script features a "fixed range" tool, where you can manually set a start time (or drag & drop a bar on the chart) to determine the interval the heatmap covers.

From the start date, the script will calculate the calculate the sub-intervals necessary to draw a rows x columns heatmap. Consequently, setting the start time further back will draw a heat map with larger rows x columns, whereas, a start time closer to the current bar time will draw a more "precise" heatmap with smaller rows x columns.

Additionally, the heatmap can be calculated using open interest data.

The image above shows the heatmap displaying open interest delta.

The image above shows alternative settings for the heatmap.

Delta values have been hidden alongside grid border colors. These settings can be replicated to achieve a more "traditional" feel for the heatmap.

Thanks for checking this out!

Volume SuperTrend AI (Expo)█ Overview

The Volume SuperTrend AI is an advanced technical indicator used to predict trends in price movements by utilizing a combination of traditional SuperTrend calculation and AI techniques, particularly the k-nearest neighbors (KNN) algorithm.

The Volume SuperTrend AI is designed to provide traders with insights into potential market trends, using both volume-weighted moving averages (VWMA) and the k-nearest neighbors (KNN) algorithm. By combining these approaches, the indicator aims to offer more precise predictions of price trends, offering bullish and bearish signals.

█ How It Works

Volume Analysis: By utilizing volume-weighted moving averages (VWMA), the Volume SuperTrend AI emphasizes the importance of trading volume in the trend direction, allowing it to respond more accurately to market dynamics.

Artificial Intelligence Integration - k-Nearest Neighbors (k-NN) Algorithm: The k-NN algorithm is employed to intelligently examine historical data points, measuring distances between current parameters and previous data. The nearest neighbors are utilized to create predictive modeling, thus adapting to intricate market patterns.

█ How to use

Trend Identification

The Volume SuperTrend AI indicator considers not only price movement but also trading volume, introducing an extra dimension to trend analysis. By integrating volume data, the indicator offers a more nuanced and robust understanding of market trends. When trends are supported by high trading volumes, they tend to be more stable and reliable. In practice, a green line displayed beneath the price typically suggests an upward trend, reflecting a bullish market sentiment. Conversely, a red line positioned above the price signals a downward trend, indicative of bearish conditions.

Trend Continuation signals

The AI algorithm is the fundamental component in the coloring of the Volume SuperTrend. This integration serves as a means of predicting the trend while preserving the inherent characteristics of the SuperTrend. By maintaining these essential features, the AI-enhanced Volume SuperTrend allows traders to more accurately identify and capitalize on trend continuation signals.

TrailingStop

The Volume SuperTrend AI indicator serves as a dynamic trailing stop loss, adjusting with both price movement and trading volume. This approach protects profits while allowing the trade room to grow, taking into account volume for a more nuanced response to market changes.

█ Settings

AI Settings:

Neighbors (k):

This setting controls the number of nearest neighbors to consider in the k-Nearest Neighbors (k-NN) algorithm. By adjusting this parameter, you can directly influence the sensitivity of the model to local fluctuations in the data. A lower value of k may lead to predictions that closely follow short-term trends but may be prone to noise. A higher value of k can provide more stable predictions, considering the broader context of market trends, but might lag in responsiveness.

Data (n):

This setting refers to the number of data points to consider in the model. It allows the user to define the size of the dataset that will be analyzed. A larger value of n may provide more comprehensive insights by considering a wider historical context but can increase computational complexity. A smaller value of n focuses on more recent data, possibly providing quicker insights but might overlook longer-term trends.

AI Trend Settings:

Price Trend & Prediction Trend:

These settings allow you to adjust the lengths of the weighted moving averages that are used to calculate both the price trend and the prediction trend. Shorter lengths make the trends more responsive to recent price changes, capturing quick market movements. Longer lengths smooth out the trends, filtering out noise, and highlighting more persistent market directions.

AI Trend Signals:

This toggle option enables or disables the trend signals generated by the AI. Activating this function may assist traders in identifying key trend shifts and opportunities for entry or exit. Disabling it may be preferred when focusing on other aspects of the analysis.

Super Trend Settings:

Length:

This setting determines the length of the SuperTrend, affecting how it reacts to price changes. A shorter length will produce a more sensitive SuperTrend, reacting quickly to price fluctuations. A longer length will create a smoother SuperTrend, reducing false alarms but potentially lagging behind real market changes.

Factor:

This parameter is the multiplier for the Average True Range (ATR) in SuperTrend calculation. By adjusting the factor, you can control the distance of the SuperTrend from the price. A higher factor makes the SuperTrend further from the price, giving more room for price movement but possibly missing shorter-term signals. A lower factor brings the SuperTrend closer to the price, making it more reactive but possibly more prone to false signals.

Moving Average Source:

This setting lets you choose the type of moving average used for the SuperTrend calculation, such as Simple Moving Average (SMA), Exponential Moving Average (EMA), etc.

Different types of moving averages provide various characteristics to the SuperTrend, enabling customization to align with individual trading strategies and market conditions.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!