Combo Backtest 123 Reversal & Key Reversal Down This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

A key reversal is a one-day trading pattern that may signal the reversal of a trend.

Other frequently-used names for key reversal include "one-day reversal" and "reversal day."

How Does a Key Reversal Work?

Depending on which way the stock is trending, a key reversal day occurs when:

In an uptrend -- prices hit a new high and then close near the previous day's lows.

In a downtrend -- prices hit a new low, but close near the previous day's highs

WARNING:

- For purpose educate only

- This script to change bars colors.

Trend Analysis

RSI of Ultimate Oscillator [SHORT Selling] StrategyThis is SHORT selling strategy with Ultimate Oscillator. Instead of drectly using the UO oscillator , I have used RSI on UO (as I did in my previous strategies )

Ultimator Oscillator settings are 5, 10 and 15

RSI of UO setting is 5

Short Sell

==========

I have used moving averages from WilliamAlligator indicator --- settings are 10(Lips), 20(teeth) and 50 (Jaw)

when Lips , Teeth and Jaw are aligned to downtrend (that means Lips < Teeth < Jaw )

Look for RSIofUO dropping below 60 ( setting parameter is Sell Line )

Partial Exit

==========

When RSIofUO crossing up Oversold line i.e 30

Cover Short / Exit

=================

When RSIofUO crosisng above overbought line i.e 70

StopLoss

========

StopLoss defaulted to 3 % , Though it is mentioned in settings , it has not been not used to calcuate and StopLoss Exit... Reason is, when RSIofUO already crossed 60 line (for SHORTING) , then it would take more efforts go up beynd 60. There is saying price takes stairs to climb up but it takes elevator to go down. I have not purely depend on this to exit stop loss, however noticed the trades in this stratgey did not get out with loss higher than when RSIofUO reaching 70 level.

Note

======

Williams Alligator is not drawn from the script. It is manually added to chart for illustration purpose. Please add it when you are using this strategy , whch woould give an idea how the strategy is taking Short Trades.

This is tested on Hourly chart for SPY

Bar color changes to purple when the strategy is in SHORT trade

Warning

========

For the eductional purposes only

Pyramiding BTC 5 min no securitySince some say that the script with the security is repaint and the results too preety

i decided to run the same script without it. still the best is when security set to 1 min but without the difference not so much.

it just to show the concept of the strategy that based on linear regression cross hull as buy signal

and the the take profit target. so maybe now its also repaint?:)

based

MavilimW Strategy MTF EMA with HA CandlesThis is a strategy adapted initially for Mavilim moving average indicator, based on WMA MA.

It seems to works amazingly on long term markets, like stocks, some futures, some comodities and so on.

In this strategy, I form initially the candle, using EMA values, so I take the EMA of last 50 closes, open, highs and lows and form the candle

After this I take interally HA and convert the EMA candle to HA.

Then using the moving averages on multiple timeframes, like in this example we have a chart on 4h, but I use 1h and 1d moving averages.

For long condition we have : close is above moving average timeframe1 and oving average timeframe2 and oving average timeframe3

Initially short would be close below ma timeframe1, ma timeframe2 and timeframe3 -> but here I also convert it into a long signal.

So we actually go only long .

And we have 2 different exits : for first long if we have a crossdown of 1h ma with 1 day ma, and for second long if we have a cross up of 1h ma with 1 day ma in this example.

Message me if you have any questions about this strategy.

Heiken Ashi MTF Strategy- IndicatorHello, this is both a strategy and indicator that revolves around Heikin Ashi candles.

In this case we take 3 different time frames, in this example we use daily , weekly and monthly.

The conditions for entry are :

For long : we check that we have a green daily candle, at the same time we check that the weekly and monthly candles are also green.

For short : We check that all candles, daily, weekly and monthly and red.

For exit of long : as soon as 1 of the 3 candles, daily or weekly or monthly converts to red, we exit.

For exit of short : as soon as 1 of the 3 candles converts to green, we exit.

This strategy- indicator can be adapted to any type of market.

Escaping of Rate from Avarage By Mustafa OZVER StrategyI simulated the EoRfA indicator with the gold price

For details about the indicator, visit my profile on tradingview

For Simulation, with default settings, we order

if Eorfa > 1 and change(eorfa) < 0

sell

if Eorfa < -1 and change(eorfa) > 0

buy

And we got

- 2.49 % profit

- 74 % profittable order from all

But only this value can not guarantee good results for trading. BE CAREFUL

Pyramiding BTC 5 minThe pyramide based on this script with his concent

the strategy is the same as BTC 15 script (look at my open scripts) there it without pyramide

you can use the filter if you wish

one trick if you want it to be more accurate (not mean more profit is to reverse the long and short in the filter ' just it will lose less)

about the strategy of pyrimde you can read in detail from the script of Coinrule

i modify only to have 5 step in the pyramide scheme on 20% of equity (seems more logical)

so let me me know what you think:)

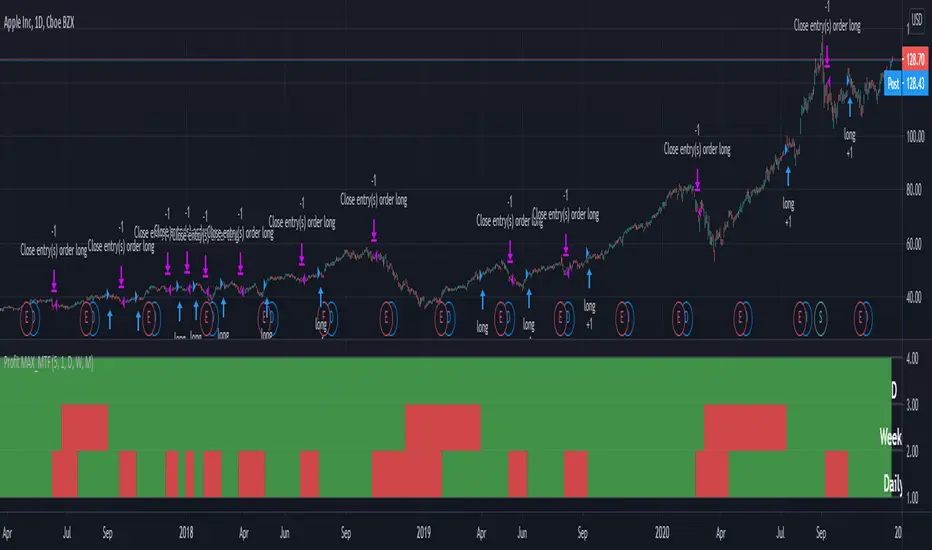

Profit MAX MTF HeatMapThis is a powerfull strategy which is made from combining 3 multi timeframes into one for profit max indicator

In this case we have daily, weekly and montly.

Our long conditions are the next ones :

if we have an uptrend on all 3 at the same time, we go long.

If we have a downtrend on all 3 of them at the same time we go short.

For exit, for long, as soon as one of the 3 converts into downtrend we exit the trade.

For exit, for short, as soon as one of the 3 converts into uptrend we exit the trade.

This tool can be used on all types of markets, and can also be changed the time frames.

Pyramiding Entries On Early Trends (by Coinrule)Pyramiding the entries in a trading strategy may be risky but at the same time very profitable with a proper risk management approach. This strategy seeks to spot early signs of uptrends and increase the position's size while the right conditions persist.

Each trade comes with its stop-loss and take-profit to enforce a proportional risk/reward profile.

The strategy uses a mix of Moving Average based setups to define the buy-signal.

The Moving Average (200) is above the Moving Average (100), which prevents from buying when the uptrend is already in its late stages

The Moving Average (9) is above the Moving Average (100), indicating that the coin is not in a downtrend.

The price crossing above the Moving Average (9) confirms the potential upside used to fire the buy order.

Each entry comes with a stop-loss and a take-profit in a ratio of 1-to-1. After over 400 backtests, we opted for a 3% TP and 3% SL, which provides the best results.

The strategy is optimized on a 1-hour time frame.

The Advantages of this strategy are:

It offers the possibility of adjusting the size of the position proportionally to the confidence in the possibilities that an uptrend will eventually form.

Low drawdowns. On average, the percentage of trades in profit is above 60%, and the stop-loss equal to the take-profit reduces the overall risk.

This strategy returned good returns both with trading pairs with Fiat/stable coins and with BTC. Considering the mixed trends that cryptocurrencies experienced during 2020 vs BTC, this strengthens the strategy's reliability.

The strategy assumes each order to trade 20% of the available capital and pyramids the entries up to 7 times.

A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Keltner Channel [LINKUSDT] 1HThis is a long-only strategy tested on LINK/USDT, 1 hour bar, from Feb 2019. The entry is determined by the breakout of upper Keltnel Channel and when the +DI is higher than 32. Instead of a fixed stop-loss from the original script , I change the exit to the middle band of the Keltnel Channel. 1st profit target will close 20% of the position. 2nd profit target will close 30% of the position. While the remaining 50% position will be closed when the price closes below the middle band of the Keltnel Channel, to take advantage of big trend. All parameters are adjustable. I added another option to enable or disable the ribbon trend filter.

My thoughts: For the same period, LINK appreciated 3000%. So I guess most in and out strategies couldn’t beat a buy and hold strategy during this period. But this doesn’t mean that this strategy is not feasible as each strategy is designed to only take advantage of a certain pattern or behavior of the market. Also, short term strategies allow you to use leverage and hence enable you to use you capital efficiently. Commission is set to 0.1%, taking account of the slippage.

Suggestion: Please perform walk forward analysis before you use real money for trading. Parameters need to be adjusted from time to time depends on your analysis. Can try using ATR for profit targets as over a longer term, the volatility might drop hence a high fixed % profit targets might not be realistic.

Any suggestions are welcome!

OCC Trend Combo 1 day BTC MoonflagRuns on BTC 1 DAY (NOTE USE THIS NOT THE PREVIOUS VERSION - DEFAULTS TUNED TO 1 day BTC HERE)

USE DEFAULT SETTINGS

The strategy is to maximise the profit for OCC longs (ALMA algo)

Longs start when the price action settles around the ALMA OCC, then typically breaks up

Then follow the trend indcator (blue/orange)

Shorts normally happen when the price action crosses below the ALMA OCC, although these initiate faster than the 1 day time setting - so watchout for shorts - are harder to predict than longs

So this catches most of the big move longs at their initiation

CRYPTO HA Strategy money maker long termToday I bring you another amazing strategy.

Its made of 2 EMA in this case 50 and 100.

At the same time, internaly for candles we calculate the candles using the HA system ( while still using in live the normal candles). This way we can assure that even if we use HA candles, we avoid repainting, and its legit.

We first calculate the HA candles based on the EMA 50 values, and after that , we use that candle properties to apply to EMA 100.

Once we have that, for entries we have the next conditions :

sell = o2 > c2 and o2 < c2 and time_cond

buy = o2 < c2 and o2 > c2 and time_cond

For sell : Our open from HA 100 is bigger than Close from ha 100, and the previous open is smaller than previous close

For long : Our open from ha 100 is smaller than close from ha 100 and the previous open is bigger than previous close.

Then we have 2 options :

If we wnat to go only long , which is my prefered version ,or the original one where we go both long and short.

I found that the best results are in general around bigger timeframes, 1h+ , 3h works the best so far on my tests.

For exit we have 2 versions :

1 lets say we had a long signal, as soon as we have a short signal we close the trade. Viceversa for short.

2. Is based on price % movement. In this case I use 7.5% price movement of asset.

We have no TP in use for this system.

For the purpose of this test I use 10.000 $ account. For test I use 100% of it, without any leverage.

I use the SL based on price movement , which is a very risky tool, since it can fluctuate even at 20-30% of our capital.

For comission I used 0.1% for each deal, and a slippage of 5 points.

Be cautious with this system !

If you have any questions , message me.

Crypto MultiTrend multi timeframesHello, today I bring you another crypto strategy which can work with multiple timeframes and most of crypto currencies

Its made entirelly of multiple EMA , of different lengths : like super fast, fast, normal, slow and very slow

We also combine a little bit of price action together with the trend direction both for entry and for exits, to have a more precise control.

The rules for long close is above all EMA's, they are in ascending order and the at same time close is bigger than the previous high, and previous high > second previous high, close > 3rd previous high , close > 4th previous high, close > 5th previous high, 5th high > 6th high.

For short we have the same, but instead of high, we use lows, and instead of > we use < .

As exit we have 2 conditions for long and 2 for short

To exit long we have : super fast ema < fast ema and fast ema < normal and normal < slow ema. For short, they would be the opposite, using > sign.

The second exit for long is when our current low crosses below 4 of ours EMA during the same candle. For short, is when the high crosses above 4 of ours EMA during the same candle.

CAUTIOUS : Currently it uses not risk management system, so in this current condition is extremely risky . Be careful

If you have any questions lets me know

trend Screener List1This is type of custom screener I searched and made to screen bulk stocks any one can modify it, other may get help out of it.

in my code i have made defined

1. uptrend= ema(close,55)> ema(close,144) and ema(close,144)> ema(close,388) and ema(close,388)> ema(close,576) and close>ema(close,388)

2. downtrend = ema(close,55)< ema(close,144) and ema(close,144)< ema(close,388) and ema(close,388)<ema(close,576) and close<ema(close,388)

if the indicator is printing DOWNTREND=TRUE or UPTREND=TRUE then the corresponding stock is in currently in that trend out of the stocks listed in the code

in one code only 40 (max) stocks can be called.

to add more stocks I copied same code and changed the stocks in the code, now you can screen 80 stocks at a time.

This code runs on each bar and checks if the stocks is in uptrend or down trend.

you can customize this screener according to your requirement.

//thanks @QuantNomad from where i solved my problem of screening my top stock for custom trend screener

//idea and motivation taken from

after adding another code you can screen 80 stocks at a time and so on , below following link is how it will look like

MA Strength StrategyThis is based on Aligned Moving Average Index published earlier:

But, instead of scoring trend based on how many moving averages are aligned, we are considering upside score. Higher scores are assigned for slower moving averages and lower scores for faster moving averages to give more stress to long term trend.

Buy/Sell conditions are based on moving average crossover on the upside score sum of Loopback days.

This is a very rough idea which seems to have been working ok on long only trades. Can be further improved.

no diceAllow this strategy to run on it's own and try not to get your emotions involved by manually closing positions. Let the strategy do all the work and you will see good returns every month.

Optimized RSI Strategy - Buy The Dips (by Coinrule)Buy low and sell high is every trader's mantra. While this approach looks straightforward in theory, it's sometimes challenging to put into practice. That requires stress-management to buy when price drops and resolution in selling when the price is rising. RSI is a useful tool to implement long-term and effective trading strategies. The script presents an optimized RSI trading strategy that uses a Moving average to spot the best time to buy the dip.

The strategy buys when the RSI is lower than 35, and at the same time, the price is below the MA100. In this way, the approach helps avoid catching early dips, increasing buying when the bottom approaches.

The position closes when the RSI value is above 65 . Depending on the volatility of the coins that the strategy will trade, it's possible to adjust the RSI exit value to chase larger profits.

The setup is optimized on a 15-minutes time frame and trading cryptocurrencies versus USD or stable coins.

The strategies was backtested over 150 times with multiple setups and coin to assess the best long-term system.

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

RSI of VWAP [SHORT selling]This is SHORT selling version of RSIofVWAP strategy. Settings and Logic are totally different from LONG side version , hence I am publishing it as a new strategy.

Settings

============

VWAP of RSI Length 15

Slow EMA Length 200

Short entry level 25

Cover short level 70

stop loss 5

SHORT Entry

============

condition1 : When RSIofVWAP crossdown below 25 and VWAP is below ema200

condition2: When weekly RSIofVWAP crossdown 70 and VWAP (note : session vwap , not weekly vwap) is below ema200

condition3: Use VIX value , if you want to short when the price is above ema200

vwap RSI crossing down 70 and VIX RSI is cossing up 70

enter short ... This is like falling knife :-)

I need to add the code -- later

if any of above condition is TRUE , SHORT entry will be taken

Take Profit

============

When close less than short entry price and RSIofVWAp is crossing up 25 , take profit ...close 1/3 of the position

Exit

============

When RSIofVWAP crossing up 70 level

Stop Loss

============

Stop Loss is set to 5%

Note:

1. When strategy is in SHORT position , background and bar color changes to gray

2. When strategy is already in short position , possible entries are shown in yellow background

3. RSI Length 15 is working most of the equities on hourly chart. ( RSI length 9 and 14 also works good , but not for all ... You may want to try which setting works for your symbol)

4. weekly VWAP (blue color) is also plotted by default ... you can disable it if you dont want to see it. But there is advantage keeping it on the chart , you can notice whenever weekly VWAP crosses above 70 line , trend is UP ... if you have LONG position you can hold on it ... Hurray :-)

Warning

============

For the educational purposes only

MACD Strategy with trailing ATR stopThis is a trend based strategy that uses EMA and SMA intersection for determining the direction of the trend and MACD for the entry signal. At the same time, the strategy uses ATR, which is working as a trailing stop.

The strategy entry will work when the Trend ribbon will turn green and MACD line will crossover the signal line. This strategy also takes into account the pyramiding and allows to enter the second time if the signal will repeat itself.

There are 3 exit points. The first 10% of the position will be closed when the price will increase by 1%. The second portion of 50% will be closed when the price reaches 5% Take profit target. The remaining 40 % of the position will wait for the exit signal which will occur when the price closes below the ATR line.

The strategy is using a fixed amount in dollars, each time the entry occurs the strategy will enter with 100$ in the order.

The strategy can be applied to other crypto assets. However, they will require input changes.

Best of luck with your trading.

Multi MA MTF SandBox StrategyA moving averages SandBox strategy where you can experiment using two different moving averages (like KAMA, ALMA, HMA, JMA, VAMA and more) on different time frames to generate BUY and SELL signals, when they cross.

Great sandbox for experimenting with different moving averages and different time frames.

== How to use ==

We select two types of moving averages on two different time frames (or the same time frame):

First is the FAST moving average that should be at the same time frame or higher.

Second is the SLOW moving average that should be on the same time frame or higher.

== Buy and Sell Signals ==

When FAST moving average cross over the SLOW moving average we have a BUY signal (for LONG)

When FAST moving average cross under the SLOW moving average we have a SELL signal (for SHORT)

WARNING: Using a lower time frame than your chart time frame will result in unrealistic results in your backtesting and bar replay.

== NOTES ==

You can select BOTH, LONG, SHORT or NONE in the strategy settings.

You can also enable Stop Loss and Take Profit.

More sandboxes to come, Follow to get notified.

Like if you like and Enjoy!

Can also act as indicator by setting 'What trades should be taken' to 'NONE':

MartingaleBecause market has random wlak but also a martingale property: after a good day, there is a higher probability that another good day will follow than a bad one.

System goes long only: it does not operate when the variation close-to-close in percentage (%) in under a certain buffer (i.e. very little movements are not considered).

There are also rules of money management in fixed percentages

Combo Backtest 123 Reversal & Kase Dev Stops This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Kase Dev Stops system finds the optimal statistical balance between letting profits run,

while cutting losses. Kase DevStop seeks an ideal stop level by accounting for volatility (risk),

the variance in volatility (the change in volatility from bar to bar), and volatility skew

(the propensity for volatility to occasionally spike incorrectly).

Kase Dev Stops are set at points at which there is an increasing probability of reversal against

the trend being statistically significant based on the log normal shape of the range curve.

Setting stops will help you take as much risk as necessary to stay in a good position, but not more.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

WARNING:

- For purpose educate only

- This script to change bars colors.

HTF High/Low Repaint StrategyHere is an another attempt to demonstrate repainting and how to avoid them. It happened few times to me that I develop a strategy which is giving immense returns - only to realize after few forward testing that it is repainting. Sometimes, it is well disguised even during forward testing.

In this simple strategy, conditions are as below:

Buy : When a 3M bar produces high and low higher than it's previous 3M bar high, low

Sell : When a 3M bar produces high and low lower than its previous 3M bar high, low.

Default setting is : lookahead = on and offset = 0

This means current 3M bar high low is plotted for all the daily bars within this month. Which means, strategy looks ahead of time to see this 3M bar high is higher than previous 3M bar high during the start of the first daily bar. Hence, this combination leads to massive repaint.

For example, trade made on October 2nd 2018 already knows well ahead of time that price is going to go down in next 3 months:

Similarly, after 2 years on October 2nd 2020 - the strategy already knows that last 3M high is going to be breached on 7th December 2020

Solution: If you are using security for higher timeframes, safer option is always to use offset 1. Further details in the trading view script:

BUT

It may still repaint if we are passing function to security.

For example:

f_secureSecurity(_symbol, _res, _src) => security(_symbol, _res, _src , lookahead = barmerge.lookahead

This function will likely avoid any repainting with Higher timeframe if we are passing in built variables such as high, low, close, open etc. But, if we try to pass supertrend, this will not produce right results. This is because supertrend calculation in turn uses high/low/close values which do not consider the offset while calculating. Hence, even with offset 1, this will still produce issues.

Hence, the call:

= f_secureSecurity(syminfo.tickerid, derivedResolution, supertrend(3,10), offset) will again lead to massive repainting. Solution to this is to implement supertrend function and use high, low, close values derived from secureSecurity.

Quick tips to identify or be suspicious about repainting

Unbelievable results on all timeframes and all instruments with both long and short trades

Lower timeframes giving significantly higher returns on backtest when compared to higher timeframe

If these things happen, be wary about repainting and do a through check of all security function usage in your strategy.

All the best :)

PS: Apply 3-5 days resolution and see the fun. Also, WHC is one hell of a Christmas tree. Could have made immense profit in the same strategy even without repainting.