Apex Edge SMC Tactical Suite

🛰 Apex Edge SMC Tactical Suite

Apex Edge SMC Tactical Suite is a precision-engineered multi-signal tool designed for advanced traders who demand real-time edge detection, breakout identification, and smart volatility-based risk placement. Built to blend seamlessly into any price action, SMC, or momentum-based strategy.

🔧 Core Features:

📍 Entry Signals

Green & red arrows appear only when a candle meets strict "Power Candle" criteria:

High momentum breakout

Volume spike confirmation

OBV spike divergence

Trend & HTF filter optional

Volatility-adjusted stop placement

💥 Power Candles

Smart detection of explosive volume+range candles

Custom "fuel score" system ranks their momentum potential

Displays as either candle highlights or subtle labels

📊 Fuel Meter

RSI-based energy tracker with customizable threshold

Plots real-time bar strength on a mini histogram

🧠 Trap Detection + Reversals

Detects stop hunt wicks or "liquidity traps"

Shows reversal diamonds on potential reclaim setups

Built-in swing logic confirms trap reversals

🧮 HTF Filtering

Optional higher-timeframe trend filter via Hull MA

Keeps signals aligned with broader market direction

📦 TP/SL Zones

Risk is calculated using volatility clustering (recent swing zones)

TP auto-calculated using ATR-based expansion

🔔 Alerts Included:

✅ Power Candle Detection

✅ Long/Short Entry Alerts

✅ Exit Signal Alerts

✅ Trap Defense Alerts

✅ Trap Reversal Confirmations

🎯 Ideal For:

SMC / ICT traders

Breakout traders

Trend followers

Scalpers / intraday setups

Momentum + volume combo traders

⚠️ Tip: Best paired with clean chart layouts, market structure, or order block frameworks. Can be combined with internal/external liquidity sweep logic for extra confluence.

Feel free to play around with the code and if you're a professional coder (unlike me) then please tag me into any versions that you can make better. Enjoy!

Disclaimer - This script was created entirely with many hours using the assistance of ChatGPT

Volatility

VPSRVP Sovereign Reign (VPSR) - Advanced Volume Profile Analysis

A sophisticated volume analysis tool that provides deep insights into market participation and momentum through an intuitive visual interface. This indicator helps traders identify significant market moves, potential reversals, and institutional activity.

Key Features:

1. Smart Volume Analysis

• Dynamic volume profiling

• Institutional participation detection

• Abnormal volume identification

• Real-time momentum tracking

2. Advanced Visual System

• Color-coded volume bars

• Adaptive cloud formation

• Reversal pattern detection

• Fake-out warning system

Visual Components:

1. Volume Bars

• Green: Bullish pressure with normal volume

• Purple: Bearish pressure with normal volume

• White: Significant bullish participation

• Pink: Significant bearish participation

• Orange: High-probability reversal zones

2. Dynamic Cloud

• White Cloud: Bullish control zone

• Purple Cloud: Bearish control zone

• Cloud density indicates participation strength

• Adaptive to market conditions

Signal Interpretation:

1. Normal Market Conditions

• Green/Purple bars show directional pressure

• Cloud color indicates dominant force

• Cloud height shows average participation

2. Significant Events

• White/Pink bars signal major moves

• Orange bars highlight potential reversals

• Cloud expansion shows increasing activity

• Cloud contraction indicates consolidation

Customization Options:

• Volume MA Length: Smoothing factor

• Abnormal Volume Threshold: Sensitivity

• Cloud Display: Toggle visualization

• Color scheme optimization

Best Practices:

1. Multiple Timeframe Analysis

• Start with higher timeframes

• Confirm on lower timeframes

• Watch for confluence

2. Volume Analysis

• Compare to historical levels

• Monitor abnormal spikes

• Track participation trends

3. Trade Management

• Use as confirmation tool

• Wait for clear signals

• Monitor fake-out warnings

• Combine with price action

Trading Applications:

1. Trend Analysis

• Identify strong moves

• Spot weakening trends

• Detect consolidation

2. Reversal Detection

• Spot potential turning points

• Identify fake-outs

• Monitor institutional activity

3. Risk Management

• Volume-based position sizing

• Stop loss placement

• Profit target selection

The VP Sovereign Reign indicator excels at:

• Identifying significant market moves

• Detecting institutional participation

• Warning of potential reversals

• Highlighting fake-outs

• Providing clear market context

Risk Warning:

This indicator is designed as a technical analysis tool and should be used as part of a complete trading strategy. Past performance does not guarantee future results. Always employ proper risk management techniques.

Note: For optimal results, use in conjunction with price action analysis and other complementary indicators.

Bounty SeekerBounty Seeker - Advanced Market Structure & Order Block Detection

A sophisticated indicator that identifies high-probability reversal zones through the analysis of market structure, volume patterns, and institutional order blocks. This tool helps traders spot potential reversals and fake-outs with precision.

Core Components:

1. Pivot Detection System

• Smart pivot high/low identification

• Volume-enhanced confirmation

• RSI confluence validation

• Real-time market structure analysis

2. Order Block Detection

• Institutional buying/selling zones

• Historical support/resistance levels

• Smart volume threshold analysis

• Dynamic level adaptation

Signal Types:

1. Bull Pivots (White X)

• Strong volume confirmation

• RSI oversold conditions

• Price action validation

• Order block confluence

2. Bear Pivots (Purple X)

• Volume surge confirmation

• RSI overbought alignment

• Bearish price action

• Resistance zone validation

3. Fake Pivots (Orange X)

• Low volume warning signals

• Trap zone identification

• False breakout detection

• Risk management guide

Visual Elements:

• Dashed Lines: Order block zones

• White/Purple X's: Major pivot points

• Orange X's: Potential fake moves

• Dynamic support/resistance levels

Best Usage Practices:

• Most effective on 1H+ timeframes

• Focus on major market pairs

• Wait for complete signal formation

• Combine with trend direction

• Monitor volume confirmation

• Use proper position sizing

The indicator excels at:

1. Identifying potential reversal zones

2. Detecting institutional order blocks

3. Warning of potential fake moves

4. Providing clear entry/exit levels

5. Highlighting strong volume zones

Risk Management:

• Always wait for signal confirmation

• Use appropriate stop loss levels

• Consider multiple timeframe analysis

• Don't trade against major trends

• Monitor volume for validation

This indicator combines advanced market structure analysis with volume profiling to help traders identify high-probability trading opportunities while warning of potential traps and fake-outs.

Note: Past performance does not guarantee future results. Always use proper risk management techniques.

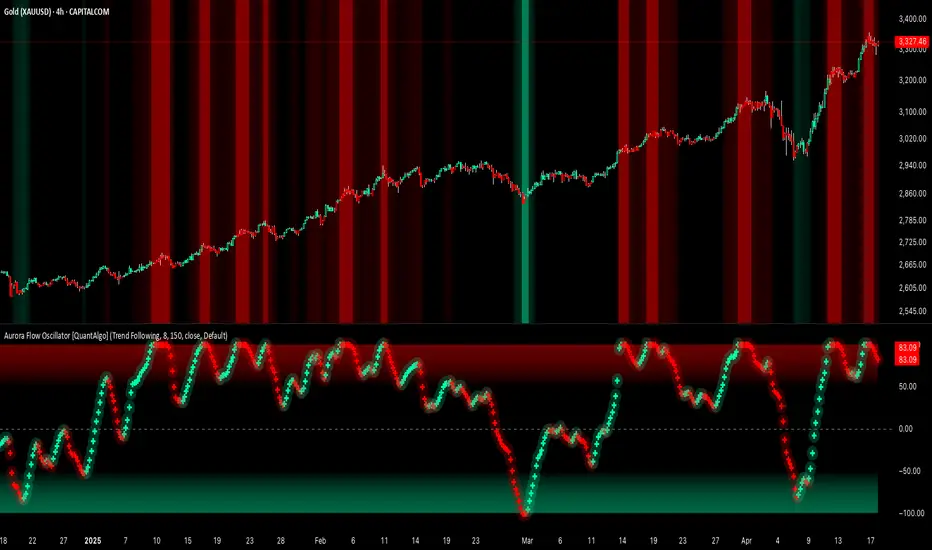

Aurora Flow Oscillator [QuantAlgo]The Aurora Flow Oscillator is an advanced momentum-based technical indicator designed to identify market direction, momentum shifts, and potential reversal zones using adaptive filtering techniques. It visualizes price momentum through a dynamic oscillator that quantifies trend strength and direction, helping traders and investors recognize momentum shifts and trading opportunities across various timeframes and asset class.

🟢 Technical Foundation

The Aurora Flow Oscillator employs a sophisticated mathematical approach with adaptive momentum filtering to analyze market conditions, including:

Price-Based Momentum Calculation: Calculates logarithmic price changes to measure the rate and magnitude of market movement

Adaptive Momentum Filtering: Applies an advanced filtering algorithm to smooth momentum calculations while preserving important signals

Acceleration Analysis: Incorporates momentum acceleration to identify shifts in market direction before they become obvious

Signal Normalization: Automatically scales the oscillator output to a range between -100 and 100 for consistent interpretation across different market conditions

The indicator processes price data through multiple filtering stages, applying mathematical principles including exponential smoothing with adaptive coefficients. This creates an oscillator that dynamically adjusts to market volatility while maintaining responsiveness to genuine trend changes.

🟢 Key Features & Signals

1. Momentum Flow and Extreme Zone Identification

The oscillator presents market momentum through an intuitive visual display that clearly indicates both direction and strength:

Above Zero: Indicates positive momentum and potential bullish conditions

Below Zero: Indicates negative momentum and potential bearish conditions

Slope Direction: The angle and direction of the oscillator provide immediate insight into momentum strength

Zero Line Crossings: Signal potential trend changes and new directional momentum

The indicator also identifies potential overbought and oversold market conditions through extreme zone markings:

Upper Zone (>50): Indicates strong bullish momentum that may be approaching exhaustion

Lower Zone (<-50): Indicates strong bearish momentum that may be approaching exhaustion

Extreme Boundaries (±95): Mark potentially unsustainable momentum levels where reversals become increasingly likely

These zones are displayed with gradient intensity that increases as the oscillator moves toward extremes, helping traders and investors:

→ Identify potential reversal zones

→ Determine appropriate entry and exit points

→ Gauge overall market sentiment strength

2. Customizable Trading Style Presets

The Aurora Flow Oscillator offers pre-configured settings for different trading approaches:

Default (80,150): Balanced configuration suitable for most trading and investing situations.

Scalping (5,80): Highly responsive settings for ultra-short-term trades. Generates frequent signals and catches quick price movements. Best for 1-15min charts when making many trades per day.

Day Trading (8,120): Optimized for intraday movements with faster response than default settings while maintaining reasonable signal quality. Ideal for 5-60min or 4h-12h timeframes.

Swing Trading (10,200): Designed for multi-day positions with stronger noise filtering. Focuses on capturing larger price swings while avoiding minor fluctuations. Works best on 1-4h and daily charts.

Position Trading (14,250): For longer-term position traders/investors seeking significant market trends. Reduces false signals by heavily filtering market noise. Ideal for daily or even weekly charts.

Trend Following (16,300): Maximum smoothing that prioritizes established directional movements over short-term fluctuations. Best used on daily and weekly charts, but can also be used for lower timeframe trading.

Countertrend (7,100): Tuned to detect potential reversals and exhaustion points in trends. More sensitive to momentum shifts than other presets. Effective on 15min-4h charts, as well as daily and weekly charts.

Each preset automatically adjusts internal parameters for optimal performance in the selected trading context, providing flexibility across different market approaches without requiring complex manual configuration.

🟢 Practical Usage Tips

1/ Trend Analysis and Interpretation

→ Direction Assessment: Evaluate the oscillator's position relative to zero to determine underlying momentum bias

→ Momentum Strength: Measure the oscillator's distance from zero within the -100 to +100 range to quantify momentum magnitude

→ Trend Consistency: Monitor the oscillator's path for sustained directional movement without frequent zero-line crossings

→ Reversal Detection: Watch for oscillator divergence from price and deceleration of movement when approaching extreme zones

2/ Signal Generation Strategies

Depending on your trading approach, multiple signal strategies can be employed:

Trend Following Signals:

Enter long positions when the oscillator crosses above zero

Enter short positions when the oscillator crosses below zero

Add to positions on pullbacks while maintaining the overall trend direction

Countertrend Signals:

Look for potential reversals when the oscillator reaches extreme zones (±95)

Enter contrary positions when momentum shows signs of exhaustion

Use oscillator divergence with price as additional confirmation

Momentum Shift Signals:

Enter positions when oscillator changes direction after establishing a trend

Exit positions when oscillator direction reverses against your position

Scale position size based on oscillator strength percentage

3/ Timeframe Optimization

The indicator can be effectively applied across different timeframes with these considerations:

Lower Timeframes (1-15min):

Use Scalping or Day Trading presets

Focus on quick momentum shifts and zero-line crossings

Be cautious of noise in extreme market conditions

Medium Timeframes (30min-4h):

Use Default or Swing Trading presets

Look for established trends and potential reversal zones

Combine with support/resistance analysis for entry/exit precision

Higher Timeframes (Daily+):

Use Position Trading or Trend Following presets

Focus on major trend identification and long-term positioning

Use extreme zones for position management rather than immediate reversals

🟢 Pro Tips

Price Momentum Period:

→ Lower values (5-7) increase sensitivity to minor price fluctuations but capture more market noise

→ Higher values (10-16) emphasize sustained momentum shifts at the cost of delayed response

→ Adjust based on your timeframe (lower for shorter timeframes, higher for longer timeframes)

Oscillator Filter Period:

→ Lower values (80-120) produce more frequent directional changes and earlier response to momentum shifts

→ Higher values (200-300) filter out shorter-term fluctuations to highlight dominant market cycles

→ Match to your typical holding period (shorter holding time = lower filter values)

Multi-Timeframe Analysis:

→ Compare oscillator readings across different timeframes for confluence

→ Look for alignment between higher and lower timeframe signals

→ Use higher timeframe for trend direction, lower for earlier entries

Volatility-Adaptive Trading:

→ Use oscillator strength to adjust position sizing (stronger = larger)

→ Consider reducing exposure when oscillator reaches extreme zones

→ Implement tighter stops during periods of oscillator acceleration

Combination Strategies:

→ Pair with volume indicators for confirmation of momentum shifts

→ Use with support/resistance levels for strategic entry and exit points

→ Combine with volatility indicators for comprehensive market context

Exponential Trend [AlgoAlpha]OVERVIEW

This script plots an adaptive exponential trend system that initiates from a dynamic anchor and accelerates based on time and direction. Unlike standard moving averages or trailing stops, the trend line here doesn't follow price directly—it expands exponentially from a pivot determined by a modified Supertrend logic. The result is a non-linear trend curve that starts at a specific price level and accelerates outward, allowing traders to visually assess trend strength, persistence, and early-stage reversal points through both base and volatility-adjusted extensions.

CONCEPTS

This indicator builds on the idea that trend-following tools often need dynamic, non-static expansion to reflect real market behavior. It uses a simplified Supertrend mechanism to define directional context and anchor levels, then applies an exponential growth function to simulate trend acceleration over time. The exponential growth is unidirectional and resets only when the direction flips, preserving trend memory. This method helps avoid whipsaws and adds time-weighted confirmation to trends. A volatility buffer—derived from ATR and modifiable by a width multiplier—adds a second layer to indicate zones of risk around the main trend path.

FEATURES

Exponential Trend Logic : Once a directional anchor is set, the base trend line accelerates using an exponential formula tied to elapsed bars, making the trend stronger the longer it persists.

Volatility-Adjusted Extension : A secondary band is plotted above or below the base trend line, widened by ATR to visualize volatility zones, act as soft stop regions or as a better entry point (Dynamic Support/Resistance).

Color-Coded Visualization : Clear green/red base and extension lines with shaded fills indicate trend direction and confidence levels.

Signal Markers & Alerts : Triangle markers indicate confirmed trend reversals. Built-in alerts notify users of bullish or bearish direction changes in real-time.

USAGE

Use this script to identify strong trends early, visually measure their momentum over time, and determine safe areas for entries or exits. Start by adjusting the *Exponential Rate* to control how quickly the trend expands—the higher the rate, the more aggressive the curve. The *Initial Distance* sets how far the anchor band is placed from price initially, helping filter out noise. Increase the *Width Multiplier* to widen the volatility zone for more conservative entries or exits. When the price crosses above or below the base line, a new trend is assumed and the exponential projection restarts from the new anchor. The base trend and its extension both shift over time, but only reset on a confirmed reversal. This makes the tool especially useful for momentum continuation setups or trailing stop logic in trending markets.

Relative ATRThis indicator enhances the standard Average True Range (ATR) by providing context about current volatility relative to its recent historical average. It highlights periods where ATR is significantly higher or lower than its own recent norm.

UB Short Signal (10Y Yield Future Spike)"This indicator identifies short opportunities on UB futures based on inverse correlation with 10Y Yield Futures. A macro trading tool to be used with additional confirmations."

🎯 Indicator Strategy

This tool generates sell signals for Ultra Bond (UB) futures when:

The Micro 10-Year Yield Future shows an upward spike (> adjustable threshold)

Trading volume is significant (false signal filter)

Inverse correlation is confirmed (UB falls when 10Y rises)

⚙️ Parameters

Spike Threshold: Sensitivity adjustment (e.g., 0.08% for swing trading)

Minimum Volume: Default 100 (optimized for Micro 10Y contracts)

📊 Recent Backtest

06/15/2024: +0.10% spike → UB dropped -0.3% within 15 minutes

06/18/2024: Valid signal post-CPI release

⚠️ Disclaimer

Analytical tool only – not financial advice

Must be combined with proper risk management

Money Flow Pulse💸 In markets where volatility is cheap and structure is noisy, what matters most isn’t just the move — it’s the effort behind it. Money Flow Pulse (MFP) offers a compact, color-coded readout of real-time conviction by scoring volume-weighted price action on a five-tier scale. It doesn’t try to predict reversals or validate trends. Instead, it reveals the quality of the move in progress: is it fading , driving , exhausting , or hollow ?

🎨 MFP draws from the traditional Money Flow Index (MFI), a volume-enhanced momentum oscillator, but transforms it into a modular “pressure readout” that fits seamlessly into any structural overlay. Rather than oscillating between extremes with little interpretive guidance, MFP discretizes the flow into clean, color-coded regimes ranging from strong inflow (+2) to strong outflow (–2). The result is a responsive diagnostic layer that complements, rather than competes with, tools like ATR and/or On-Balance Volume.

5️⃣ MFP uses a normalized MFI value smoothed over 13 periods and classified into a 5-tier readout of Volume-Driven Conviction :

🍆 Exhaustion Inflow — usually a top or blowoff; not strength, but overdrive (+2)

🥝 Active Inflow — supportive of trend continuation (+1)

🍋 Neutral — chop, coil, or fakeouts (0)

🍑 Selling Intent — weakening structure, possible fade setups (-1)

🍆 Exhaustion Outflow — often signals forced selling or accumulation traps (-2)

🎭 These tiers are not arbitrary. Each one is tuned to reflect real capital behavior across timeframes. For instance, while +1 may support continuation, +2 often precedes exhaustion — especially on the lower timeframes. Similarly, a –1 reading during a pullback suggests sell-side pressure is building, but a shift to –2 may mean capitulation is already underway. The difference between the two can define whether a move is tradable continuation or strategic exhaustion .

🌊 The MFI ROC (Rate of Change) feature can be toggled to become a volatility-aware pulse monitor beneath the derived MFI tier. Instead of scoring direction or structure, ROC reveals how fast conviction is changing — not just where it’s headed, but how hard it's accelerating or decaying. It measures the raw Δ between the current and previous MFI values, exposing bursts of energy, fading pressure, or transitional churn .

🎢 Visually, ROC appears as a low-opacity area fill, anchored to a shared lemon-yellow zero line. When the green swell rises, buying pressure is accelerating; when the red drops, flow is actively deteriorating. A subtle bump may signal early interest — while a steep wave hints at an emotional overreaction. The ROC value itself provides numeric insight alongside the raw MFI score. A reading of +3.50 implies strong upside momentum in the flow — often supporting trend ignition. A score of –6.00 suggests rapid deceleration or full exhaustion — often preceding reversals or failed breakouts.

・ MFI shows you where the flow is

・ ROC tells you how it’s behaving

😎 This blend reveals not just structure or intent — but also urgency . And in flow-based trading, urgency often precedes outcome.

🧩 Divergence isn’t delay — it’s disagreement . One of the most revealing features of MFP is how it exposes momentum dissonance — situations where price and flow part ways. These divergences often front-run pivots , traps , or velocity stalls . Unlike RSI-style divergence, which whispers of exhaustion, MFI divergence signals a breakdown in conviction. The structure may extend — but the effort isn’t there.

・ Price ▲ MFI ▼ → Effortless Markup : Often signals distribution or a grind into liquidity. Without rising MFI, the rally lacks true flow participation — a warning of fragility.

・ Price ▼ MFI ▲ → Absorption or Early Accumulation : Price breaks down, but money keeps flowing in — a hidden bid. Watch for MFI tier shifts or ROC bursts to confirm a reversal.

🏄♂️ These moments don’t require signal overlays or setup hunting. MFP narrates the imbalance. When price breaks structure but flow does not — or vice versa — you’re not seeing trend, you’re seeing disagreement, and that's where edge begins.

💤 MFP is especially effective on intraday charts where volume dislocations matter most. On the 1H or 15m chart, it helps distinguish between breakouts with conviction versus those lacking flow. On higher timeframes, its resolution softens — it becomes more of a drift indicator than a trigger device. That’s by design: MFP prioritizes pulse, not position. It’s not the fire, it’s the heat.

📎 Use MFP in confluence with structural overlays to validate price behavior. A ribbon expansion with rising MFP is real. A compression breakout without +1 flow is "fishy". Watch how MFP behaves near key zones like anchored VWAP, MAs or accumulation pivots. When MFP rises into a +2 and fails to sustain, the reversal isn’t just technical — it’s flow-based.

🪟 MFP doesn’t speak loudly, but it never whispers without reason. It’s the pulse check before action — the breath of the move before the breakout. While it stays visually minimal on the chart, the true power is in the often overlooked Data Window, where traders can read and interpret the score in real time. Once internalized, these values give structure-aware traders a framework for conviction, continuation, or caution.

🛜 MFP doesn’t chase momentum — it confirms conviction. And in markets defined by noise, that signal isn’t just helpful — it’s foundational.

Dskyz (DAFE) Turning Point Indicator - Dskyz (DAFE) Turning Point Indicator — Smart Reversal Signals

Inspired by the intelligent logic of a pervious indicator I saw. This script represents a next-generation reversal detection system—completely re-engineered with cutting-edge filters, adaptive logic, and intelligent dashboards.

The Dskyz (DAFE) Turning Point Indicator

🧠 What Is It?

is designed to identify key market reversal zones with extraordinary accuracy by combining trend direction, volatility confirmation, price action patterns, and smart filtering layers—all visualized in a highly interactive and informative chart overlay.

This isn’t just a signal generator—it’s a decision-making assistant.

⚙️ Inputs & How to Use Them

All input fields are grouped for ease-of-use and explanation:

🔸 Reversal Logic Settings

Source: The price source used for signal generation (default: hlcc4). Can be changed to any standard price formula (open, close, hl2, etc.).

ATR Period: Used for determining volatility and dynamic trailing stop logic.

Supertrend Factor / Period: Calculates directional movement to detect trending vs choppy zones.

Reversal Sensitivity Thresholds: Internal logic filters minor pullbacks from true reversals.

🔸 Filters

Trend Filter: Enables trend-only signals (optional).

Volume Spike Filter: Confirms reversals with significant volume activity.

Volatility Zone Coloring: Visually highlights high-volatility areas to avoid late entries or fakeouts.

Custom High/Low Detection: Smart local top/bottom scanning to reinforce accuracy.

🔸 Visual & Dashboard Options

Signal Labels: Toggle signal labels on the chart.

Color Theme: Choose your visual theme for easier visibility.

Dashboard Toggle: Activate a compact dashboard summarizing strategy health (win rate, drawdown, trend state, volatility).

🧩 Functions Used

ta.supertrend(): Determines trend direction for signal confirmation and filtering.

ta.atr(): Calculates real-time volatility to determine trailing stop exits and visual zones.

ta.rsi() (internally optimized): Helps filter overbought/oversold conditions.

Local High/Low Scanner: Tracks recent pivots using a custom dynamic lookback.

Signal Engine: Consolidates multiple confirmation layers before plotting.

🚀 What Makes It Unique?

Unlike traditional reversal indicators, this one combines:

Multi-factor signal validation: No single indicator makes the call—volume, trend, price action, and volatility all contribute.

Adaptive filtering: The indicator evolves with the market—less noise, smarter signals.

Visual volatility heatmap zones: Avoid entering during uncertainty or manipulation spikes.

Interactive trend dashboard: Immediate insight into the strength and condition of the current market phase.

Highly customizable: Turn features on/off to match your trading style—scalping, swing, or trend-following.

Precision timing: Uses optimized versions of RSI and ATR that adjust automatically with price context.

🧬 Recommended for:

Commodity: Futures, Forex, Crypto

Timeframes: 1m to 1h for active traders. 4h+ for swing trades.

Pair With: Support/resistance zones, Fibonacci levels, and smart money concepts for additional confluence.

🎯 Why It Works

- Traditional reversal signals suffer from lag and noise. This system filters both by:

- Using multi-source confirmation, not just price movement.

-Tracking volatility directly, not assuming static markets.

-Detecting exhaustion, not just divergence.

-Keeping your screen clean, with only the most relevant data shown.

🧾 Credit & Acknowledgement

🧠 Original Concept Inspiration: This project was deeply inspired by the work of Enes_Yetkin_ and their approach to reversal detection. This version expands on the concept with additional technical layers, updated visuals, and real-time adaptability.

📌 Final Thoughts

This is more than a reversal tool. It's a market condition interpreter, entry/exit planner, and risk assistant all in one. Every aspect is engineered to give you an edge—especially when timing means everything.

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

-Dskyz

FeraTrading Relative Volume IndicatorThis FeraTrading Relative Volume Indicator measures relative volume pressure by comparing buying and selling activity, smoothed using a configurable average. It helps traders identify volume-driven momentum shifts, offering dynamic buy and sell signals based on weighted pressure values.

Key Features:

📈 Relative Volume (RV) Line: Measures net buying/selling pressure using volume-weighted price action.

🟢 Buy Signals: Triggered when RV crosses above a smoothed moving average (SMA 1).

🔴 Sell Signals (optional): Triggered when RV crosses below a separate SMA (SMA 2).

🔍 Customizable Inputs: Adjust smoothing length, weight, and signal sensitivity.

🕯️ Weighted Candles (optional): Visualizes custom OHLC based on volume-weighted volatility.

📊 Two SMAs: Use separate or combined moving averages to analyze trends in pressure.

🎨 Flexible Styling: Customize line and signal colors to match your chart setup.

Use Cases:

Spotting accumulation/distribution phases

Timing entries during volume surges

Confirming breakout momentum with underlying volume pressure

This indicator was developed by FeraTrading to visualize relative volume pressure.

Volume Flow RatioVolume Flow Ratio (VFR) Indicator

Overview

The Volume Flow Ratio (VFR) is a sophisticated volume analysis tool that measures current trading volume relative to the maximum volume of the previous period. Unlike traditional volume indicators that show raw volume or simple moving averages, VFR provides context by comparing current activity to recent maximum activity levels.

Core Features

1. Split Period Analysis

- Multiple Timeframe Options:

- Daily: Compares to previous day's maximum

- Weekly: Week-to-week comparison

- NYSE Weekly: Specialized for stock market trading (Monday-Friday only)

- Monthly: Month-to-month analysis

- Quarterly: Quarter-to-quarter perspective

- Yearly: Year-over-year volume comparison

2. Ratio-Based Measurement

- Displays volume as a ratio (0 to 1+) rather than raw numbers

- 1.0 represents volume equal to previous period's maximum

- Example: If previous max was 50,000 contracts:

- Current volume of 25,000 shows as 0.5

- Current volume of 75,000 shows as 1.5

3. Triple Coloring Modes

- Moving Average Based:

- Compares current ratio to its moving average

- Customizable MA period

- Green: Above MA (higher than average activity)

- Red: Below MA (lower than average activity)

- Previous Candle Comparison:

- Simple increase/decrease from previous bar

- Green: Higher than previous bar

- Red: Lower than previous bar

- Candle Color Based:

- Syncs with price action

- Green: Bullish candles (close > open)

- Red: Bearish candles (close < open)

Primary Use Cases

1. Volume Profile Analysis

- Perfect for traders who need to understand when markets are most active

- Helps identify unusual volume spikes relative to recent history

- Useful for timing entries and exits based on market participation

2. Market Activity Traders

Ideal for traders who:

- Need to identify high-liquidity periods

- Want to avoid low-volume periods

- Look for volume breakouts or divergences

- Trade based on institutional participation levels

3. Mean Reversion Traders

Helps identify:

- Overextended volume conditions (potential reversals)

- Volume exhaustion points

- Return to normal volume levels after spikes

4. Momentum Traders

Useful for:

- Confirming trend strength through volume

- Identifying potential trend exhaustion

- Validating breakouts with volume confirmation

Advantages Over Traditional Volume Indicators

1. Contextual Analysis

- Shows relative strength rather than raw numbers

- Easier to compare across different time periods

- Automatically adjusts to changing market conditions

2. Period-Specific Insights

- Respects natural market cycles (daily, weekly, monthly)

- Special handling for NYSE trading days

- Eliminates weekend noise in stock market analysis

3. Flexible Visualization

- Three distinct coloring methods for different trading styles

- Clear reference line at 1.0 for quick analysis

- Histogram style for easy pattern recognition

Best Practices

For Day Traders

- Use Daily split for intraday volume patterns

- MA coloring mode with shorter periods (5-10)

- Focus on ratios during market hours

For Swing Traders

- Weekly or NYSE Weekly splits

- Longer MA periods (15-20)

- Look for sustained volume patterns

For Position Traders

- Monthly or Quarterly splits

- Candle color mode for trend confirmation

- Focus on major volume shifts

Limitations

- Requires one full period to establish baseline

- May be less effective in extremely low volume conditions

- NYSE Weekly mode specific to stock market hours

This indicator is particularly valuable for traders who understand that volume is a crucial component of price action but need a more sophisticated way to analyze it than simple volume bars. It's especially useful for those who trade based on market participation levels and need to quickly identify whether current volume is significant relative to recent history.

Intraday Uncertainty [PhenLabs]📊 Intraday Uncertainty

Version: PineScript™ v6

📌 Description

The Intraday Uncertainty indicator offers traders a visual representation of market certainty/uncertainty during trading sessions. By comparing each price bar’s range to the Average True Range (ATR), it provides an intuitive way to gauge market conviction through a color gradient system.

This tool helps traders identify periods of high certainty (potentially trending markets) versus high uncertainty (potentially choppy or volatile markets) without complex calculations or multiple indicators. The color-coded bars create an immediate visual cue to support decision-making in varying market conditions.

🚀 Points of Innovation

Automated range-to-ATR ratio calculation that adapts to changing market volatility

Dynamic color gradient system that visually distinguishes between certain and uncertain price action

Customizable gradient clamping to fine-tune sensitivity to market conditions

Integrated dashboard that provides clear interpretation guidance

Position-flexible legend that accommodates different chart layouts

Highly optimized for performance with minimal calculation overhead

🔧 Core Components

ATR Calculation: Measures market volatility using a configurable lookback period

Range-to-ATR Ratio: Compares current bar’s high-low range against average volatility

Gradient Mapping System: Converts numerical uncertainty values into an intuitive color scale

Dashboard Legend: Provides clear interpretation guidance with customizable positioning

🔥 Key Features

Bar Coloring: Instantly identifies market certainty levels through intuitive color gradients

Customizable ATR Period: Adjust sensitivity to historical volatility based on trading style

Gradient Clamping: Fine-tune the color sensitivity using the Range/ATR multiplier

Color Customization: Personalize the color scheme to match your chart aesthetics

Informative Dashboard: Quickly interpret color meanings with the optional on-chart legend

Flexible Display Options: Customize dashboard position and text size for your chart layout

🎨 Visualization

Color Gradient: Bars colored on a spectrum from green (high certainty) to red (high uncertainty)

Dashboard Legend: Optional on-chart guide explaining the color interpretation

Color Intensity: Stronger colors indicate more extreme certainty/uncertainty levels

At-a-glance Interpretation: Quickly identify market conviction without analyzing numbers

📖 Usage Guidelines

Calculation Settings

ATR Period

Default: 14

Range: 1+

Description: Controls the lookback period for ATR calculation. Lower values increase sensitivity to recent volatility, while higher values provide more stability.

Gradient Clamp (Range/ATR Multiplier)

Default: 2.0

Range: 0.1+

Description: Sets the maximum Range/ATR ratio for gradient scaling. Ranges above this value display the end color (high uncertainty).

Color Settings

Gradient Start Color (High Certainty)

Default: Green

Description: Color representing high market certainty (low Range/ATR ratio)

Gradient End Color (Low Certainty)

Default: Red

Description: Color representing low market certainty (high Range/ATR ratio)

Dashboard Settings

Show Dashboard Legend

Default: True

Description: Toggles the visibility of the on-chart interpretation guide

Dashboard Position

Options: top_right, top_left, bottom_right, bottom_left, middle_right, middle_left

Default: bottom_right

Description: Controls the placement of the dashboard on your chart

Dashboard Text Size

Options: tiny, small, normal, large, huge

Default: normal

Description: Adjusts the text size of the dashboard for readability

✅ Best Use Cases

Identifying potential trend shifts when certainty levels change dramatically

Confirming trend strength through consistent certainty levels

Detecting choppy/sideways markets with persistent high uncertainty

Filtering trading signals from other indicators based on certainty levels

Gauging market conviction behind price breakouts or pullbacks

Optimizing entry/exit timing based on certainty/uncertainty transitions

⚠️ Limitations

Does not predict future price direction, only measures current bar certainty

May provide false signals during news events or unexpected volatility spikes

Requires context within the broader market environment for optimal interpretation

Color interpretation is relative rather than absolute across different securities

ATR-based calculation means sensitivity varies across different timeframes

💡 What Makes This Unique

Simplicity: Single visual indicator that doesn’t require multiple technical tools

Adaptability: Automatically adjusts to changing market volatility conditions

Contextual Analysis: Provides market conviction context beyond just price movement

Intuitive Design: Color-based system that requires minimal learning curve

Efficiency: Lightweight calculation that doesn’t impact chart performance

🔬 How It Works

1. ATR Calculation:

Calculates the Average True Range using the specified period

Establishes a baseline for normal market volatility

2. Range Analysis:

Measures each bar’s high-low range

Compares this range to the current ATR value to create a ratio

3. Gradient Mapping:

Converts the Range/ATR ratio to a normalized value between 0 and 1

Maps this value onto a color gradient between the start and end colors

Applies the resulting color to the price bar

4. Dashboard Creation:

Constructs an information panel on the last visible bar

Populates it with color samples and interpretation guidance

💡 Note:

This indicator works best when used in conjunction with other technical analysis tools rather than in isolation. The certainty/uncertainty measure provides context for your trading decisions but should not be the sole basis for entries and exits. Consider using higher certainty periods for trend-following strategies and exercise caution during periods of high uncertainty.

ATR % + Pump Detector📘 **ATR % + Pump Detector (Fixed 0.10%)**

This indicator combines two powerful volatility tools in one:

- **ATR % Display (Blue):**

Calculates the Average True Range as a percentage of price. Triggers an alert when ATR % exceeds **0.10%**, signaling rising volatility and potential breakout conditions.

- **Pump % Detector (Red):**

Measures the percentage change from **open to close** of the current candle. Triggers alerts when the move exceeds **+0.10%** (pump) or **–0.10%** (dump), helping you catch sudden price spikes in real time.

🔹 **Top-right display** shows both metrics in a clean table

🔹 Works on **any timeframe**

🔹 Ideal for **momentum trading, breakout entries**, or filtering low-vol setups

Volume and Volatility Ratio Indicator-WODI该指标名为“交易量与波动率比例指标-WODI”,主要基于交易量和价格波动率构造一个复合指数,帮助识别市场内可能存在的异常或转折信号。具体实现如下:

用户自定义参数

用户可以设置交易量均线长度(vol_length)、指数的短期与长期均线长度(index_short_length、index_long_length)、均线敏感度(index_magnification)、阈值放大因子(index_threshold_magnification)以及检测K线形态的区间(lookback_bars)。这些参数为后续计算提供了灵活性,允许用户根据不同市场环境自定义指标的敏感度和响应速度。

交易量均线与百分比计算

首先通过 ta.sma 计算指定长度的交易量简单均线(vol_ma)。

接下来,将当前交易量与均线进行比较,计算出当前交易量占均线的百分比(vol_percent),这反映了短期内交易量的相对活跃程度。

波动率的衡量

使用当前K线的最高价和最低价计算振幅,再除以收盘价乘以100得到波动率(volatility),从而反映市场价格波动的幅度。

构建交易量/波动率指数

将交易量百分比与波动率相乘,形成了“交易量/波动率指数”(volatility_index)。该指数能够同时反映市场的交易活跃度和价格波动性,两者的联合作用帮助捕捉市场的“热度”。

计算指标均线与阈值

对交易量/波动率指数分别计算短期均线(index_short_ma)和长期均线(index_long_ma),并通过乘以一个敏感度参数(index_magnification)进行调整。

同时,依据长期均线计算一个阈值(index_threshold),起到过滤噪音的作用。当指数突破该阈值时,可能预示着市场的重要变化。

K线形态与反转模式检测

通过遍历最近几根K线(由lookback_bars控制),指标会检测是否符合一系列预定条件(涉及交易量、价格振幅、K线形态等),以判断是否存在反转模式。若符合条件,则标记为反转模式,从而为潜在的转折点提供提示。

图表展示

最终在独立窗口中绘制多个元素:

指数短均线与长均线:经过敏感度调整后显示,用于分析指数趋势。

交易量/波动率指数:采用阶梯线风格绘制,直观展示指数变化。

阈值线:作为参考水平,便于判断指数是否突破常规范围。

交易量柱状图:当当前交易量高于均线时,通过不同颜色显示;当检测到反转模式时,颜色会进一步强化,帮助用户迅速识别潜在信号。

English Description

This indicator, titled “Volume and Volatility Ratio Indicator - WODI”, is designed to construct a composite index based on trading volume and price volatility, aiding in the identification of abnormal market conditions or potential reversal signals. Its functionality is broken down as follows:

User-Defined Parameters

The indicator allows users to set parameters such as the moving average length for volume (vol_length), the short and long moving average lengths for the index (index_short_length and index_long_length), a sensitivity multiplier (index_magnification), a threshold magnification factor (index_threshold_magnification), and the number of bars for pattern detection (lookback_bars). These parameters provide flexibility to adjust the sensitivity and responsiveness of the indicator based on different market conditions.

Volume Moving Average and Percentage Calculation

A simple moving average (SMA) of volume is computed over the specified length (vol_ma) using the ta.sma function.

The current volume is then compared to its moving average to calculate the volume percentage (vol_percent), reflecting the relative trading intensity in the short term.

Measuring Volatility

Volatility is calculated based on the current bar’s high and low prices, normalized by the closing price and multiplied by 100, which provides a measure of the market’s price fluctuation magnitude.

Constructing the Volume/Volatility Index

The index (volatility_index) is derived by multiplying the volume percentage by the calculated volatility. This composite metric reflects both market activity and price movement, effectively capturing the overall “heat” of the market.

Calculating the Index Moving Averages and Threshold

Two moving averages for the volatility_index are computed: one short-term (index_short_ma) and one long-term (index_long_ma). These are then adjusted by the sensitivity multiplier (index_magnification).

A threshold level (index_threshold) is calculated based on the long-term moving average multiplied by the threshold magnification factor, serving to filter out market noise. When the index exceeds this threshold, it may signal significant market shifts.

Detection of Reversal Patterns

The indicator iterates through the recent bars (as determined by lookback_bars) to check whether a set of predetermined conditions (involving trends in the volatility_index, volume comparisons, price closes, and K-line patterns) are met. If these conditions are satisfied, it flags a reversal pattern, which may serve as a warning for a potential market turnaround.

Visualization on the Chart

The final display includes several elements plotted in a separate indicator window:

The short-term and long-term moving averages of the index (after sensitivity adjustment) which help visualize the trend of the composite index.

The volatility index itself is drawn using a step-line style for clarity.

A threshold line is plotted to provide a reference level against which index movements can be compared.

A volume histogram is also displayed, where bars are colored differently when the current volume exceeds the moving average; the color is further enhanced if a reversal pattern is detected, making it easy for users to quickly spot potential signals.

3M-10Y Yield Spread3M-10Y Yield Spread Indicator Description

What It Is:

This indicator calculates the difference (spread) between the 3-month and 10-year US Treasury yields, plotted as a line with a zero reference. The background turns red when the spread inverts (falls below zero), signaling when the 3-month yield exceeds the 10-year yield.

What It Helps Understand:

Economic Health: An inverted yield curve (spread < 0) often predicts recessions, as it reflects market expectations of future economic slowdown, typically preceding downturns by 6-18 months.

Fed Policy Impact: Fed rate hikes can push short-term yields (like the 3-month) higher, potentially causing inversion if long-term yields (10-year) don’t rise as much due to growth concerns. Conversely, Fed rate cuts can lower short-term yields, steepening the curve (spread > 0), signaling economic stimulus or recovery expectations.

Rogue ORB PRORogue ORB Pro is a precision-engineered Opening Range Breakout (ORB) indicator built for active intraday traders who need real signals, not noise.

This tool identifies high-probability breakout entries from the opening range, enhanced with optional ATR-based stop loss levels, deviation targets, cooldown filters, and a relative volume gate to filter weak setups.

🔍 Key Features:

Opening Range High/Low: Drawn from a user-defined time window and locked for the day

Deviations: Automatically plots target zones above and below the OR range (e.g. 1, 2 deviations)

Pre-Market Levels: Automatically draws pre market high and low lines at the end of pre market session

Buy/Sell Signals: Triggered on breakout of the OR High/Low with configurable breakout logic (touch or close)

ATR Stop Loss Line: Dynamically drawn at a fixed ATR distance from breakout candle, with optional SL label

Cooldown Period: Prevents back-to-back signals by enforcing a user-defined bar delay between entries, can help with overtrading

Volume Filter: Optional relative volume filter that requires breakout candles to exceed a custom volume threshold

VWAP Overlay: Visual VWAP for directional bias and confluence

Gradient Range [BigBeluga]

This indicator highlights range-bound market conditions by dynamically plotting gradient-colored candlesticks within a defined price box. It detects whether the market is ranging or trending using ADX and can identify mean reversion points when price steps outside the established range.

🔵KEY FEATURES:

Range Detection Box:

➣ A transparent box is drawn based on the highest and lowest price close over a user-defined period.

➣ Helps visualize range boundaries and the midline for support/resistance reference.

Gradient Candlestick Coloring:

➣ Candles inside the range are colored with a gradient from top to bottom based on proximity to the midline.

➣ Top range candles are shaded with bearish tones, while bottom range candles use bullish tones.

Ranging/Trending State Detection:

➣ Uses ADX to determine if the market is currently in a ranging or trending state.

➣ A label in the bottom right corner shows a real-time status (🟢 Ranging / 🟡 Trending).

Mean Reversion Signal Circles:

➣ When the market is ranging, white circles are plotted at highs/lows that breach the box boundary, indicating potential mean reversion points.

➣ These levels can act as fade trade setups or exhaustion markers.

🔵USAGE:

Range Trading: Trade between the upper and lower boundaries during range-bound conditions with clearer visual feedback.

Mean Reversion Plays: Use circle signals as early alerts to identify when price extends beyond the range and may revert to the mean.

Visual Trend Strength: Instantly recognize where price is concentrated inside the range via the color gradient system.

Ranging Filter: Use the ADX label to avoid false setups during strong trending periods.

Gradient Range provides an elegant and data-driven approach to range-bound market analysis. With its gradient visualization and smart reversion detection, it empowers traders to better time entries and exits within consolidation zones.

ATR Stop-Loss & TargetsATR and Supertrend-based SL/TP & Trailing System

This indicator combines Average True Range (ATR) and Supertrend logic to help traders define precise stop-loss, first target, and trailing stop-loss (TSL) levels.

⚙️ Key Features:

📏 ATR-based Stop-Loss & Target Lines:

Uses ATR (default period: 5) based on the previous day's candle for more stable risk management.

Traders can choose the price source: Close, Open, or enter a manual price.

SL and first target are calculated using multipliers:

Multiplier 1 = Stop Loss

Multiplier 2 = First Target

📉 Supertrend for Trailing Stop:

Built-in Supertrend logic for trailing stop-loss management.

Uses ATR(10) with a multiplier of 2.1, based on HL2.

Supertrend can be toggled ON/OFF from the settings.

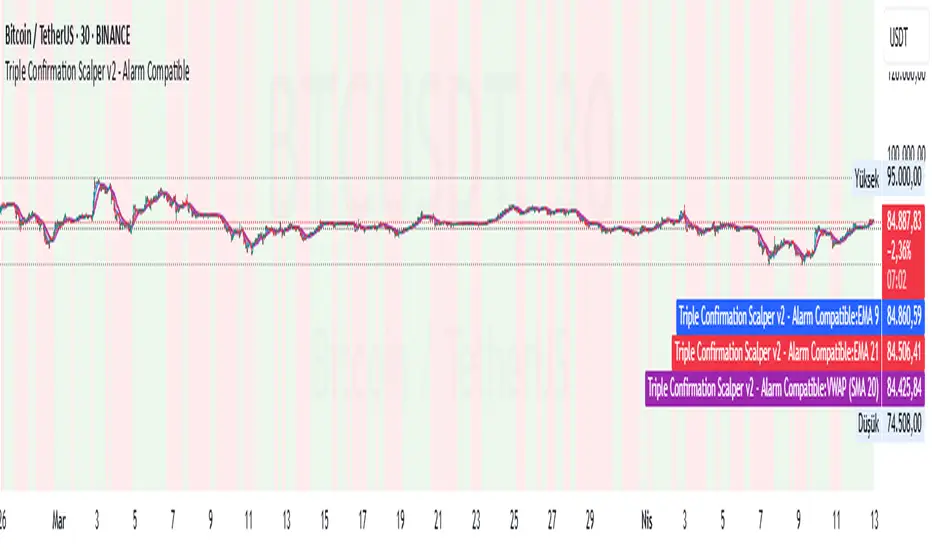

Triple Confirmation Scalper v2 - Alarm CompatibleTriple Confirmation Scalper Strategy

A high-probability scalping strategy combining trend momentum, overbought/sold conditions, and volume confirmation to filter low-noise signals.

📊 Strategy Logic

Trend Direction

Dual EMA crossover (9 & 21 periods) for momentum and trend bias.

Overbought/Oversold Zones

RSI (14-period) to avoid entries at extremes.

Volume Spike Filter

OBV + 20-period volume average to confirm breakout validity.

Dynamic Risk Management

Stop-loss: Adaptive to recent price action (5-candle low/high ±1%).

Take-profit: 1.5% target (1.5:1 risk/reward).

🔍 Advanced Features

Precision VWAP (20-period, HLC3-based) for dynamic S/R levels.

Visual Aids:

EMA/VWAP bands + trend-colored background.

Volume spike alerts.

TradingView Alerts pre-configured for long/short signals.

⚙️ Default Settings

Commission: 0.1% factored into backtests.

Mode: Supports both long/short positions.

⚠️ Disclaimer

This is a technical analysis tool, not financial advice.

Past performance ≠ future results. Test thoroughly in a demo account.

Adjust parameters (e.g., EMA periods, RSI thresholds) to match your risk tolerance.

✅ TradingView Compliance Notes:

No exaggerated claims (e.g., "100% win rate").

Clear disclaimer included.

Focus on objective strategy logic (no promotional language).

Visualisation tendancesThis script allows you to visualize the current trend of a financial asset.

It has two colors:

- Green for bullish phases

- Red for bearish phases

This allows you to instantly position yourself in the direction of the trend.

It also integrates Bollinger Bands, a volatility indicator.

This allows you to display two different indicators in a single indicator.

SR Intensity CandleThis is a very simple script intended to find just what the title says, "Intensity Candles" is what i am calling them. A bullish intensity candle is taking the low of the previous candle and the close is above the previous candle high. Bearish intensity candle is the opposite, a candle that takes the high of the previous candle and the close is below the low of the previous candle.

Alternatively, if a "bullish" intensity candle is the mitigated and price pushes below, you can expect a back test short of the "bullish" intensity candle. They will act as SR zones for the future price action.

The BEST and most ideal spot for the intensity candles to happen is the see a bullish candle at the low of a move and a bearish candle at the highs indicating strong movement for reversal.

Liquidity Zones Alerts"Liquidity Zones Alerts" is a powerful smart-money-based indicator designed to detect key liquidity grabs and provide high-probability reversal signals using a combination of market structure, volume, volatility, and candlestick confirmation.

🧠 How It Works

The core logic of this indicator is built around the Smart Money Concepts:

🔺 Liquidity Sweeps: Detects when price takes out previous daily or weekly highs/lows, suggesting stop hunts or engineered liquidity moves by institutional players.

📈 Volume Filter: Ensures signals only appear during above-average volume, filtering out noise and low-interest moves.

⚡ Volatility Filter: Flags high-range candles relative to the average, catching flash crashes/spikes that often precede strong reversals.

🔄 Engulfing Candle Confirmation: Confirms entry with a bullish or bearish engulfing pattern after liquidity is taken — increasing signal reliability.

🧭 Premium/Discount Zone Logic: Trades are filtered to ensure longs are only taken in discount zones, and shorts in premium zones, using a 20-period market range for context.

📌 Features

✅ Daily & Weekly liquidity zones toggle

✅ Visual signals with clean 🔻(short) & 🔺(long) arrows

✅ Auto-detection of flash crashes

✅ Alerts on both long and short setups

✅ Optional previous high/low level plotting for context

✅ Background highlighting of valid signal candles

✅ Multi-timeframe friendly and compatible with any asset

🛠️ Use Case

Whether you're a scalper or a swing trader, this tool helps you spot institutional entry zones before the move happens. It works especially well when combined with your existing bias or supply/demand zones.

💬 “Price doesn't move randomly — it hunts liquidity. This indicator shows you where and when it happens.”

ATR % Oscillator - DolphinTradeBot1️⃣ Overview

🔸 This is a simplified version of ATR and TR that shows volatility as percentage changes , making it easier to compare two symbols.

🔸 The indicator compares the volatility of two different assets by calculating the percentage-based price ranges and their moving averages .

📌 This is especially useful for pair traders, as it helps identify which symbol is more volatile, allowing for strategic decisions based on relative movement rather than overall market direction.

2️⃣ How Is It Work?

🔸 For each symbol, it calculates the absolute percentage difference between either:

• Close and Open (net price change), or

• High and Low (daily price range).

🔸 The results are visualized as column bars — the taller the bar, the higher the volatility.

🔸 It also plots a moving average line (SMA) based on the selected range length.

📌 These calculations are independent of the chart you're on — they work purely based on the two selected symbols.

If no symbols are selected, it defaults to using the current chart's symbol.

3️⃣ How to Use It?

With this indicator, you can:

🔸 Compare the volatility between two assets.

🔸 Detect sudden volatility spikes that may signal upcoming momentum.

🔸 Support spread, arbitrage, or correlation-based strategies .

🔸 See which symbol is gaining market attention (a larger difference = more activity).

Example: Compare BTC vs ETH to see which one is dominating in terms of price action or volatility.

4️⃣⚙️ Settings

🔸 Symbol Settings

• Symbol-1 / Symbol-2: Choose the two assets to compare.

• Checkboxes: Enable/disable visibility for each symbol's data.

🔸 Calculation Settings

• Range Average: The number of bars used for the moving average.

• Calculation Source:

- Close-Open: Measures net price movement.

- High-Low: Measures total price range.