Digital Clock with Market Status and AlertsDigital Clock with Market Status and Alerts - 日本語解説は下記

Overview:

The Digital Clock with Market Status and Alerts indicator is designed to display the current time in various global time zones while also providing the status of major financial markets such as Tokyo, London, and New York. This indicator helps traders monitor the open and close times of different markets and alerts them when a market opens. Customizable options are provided for table positioning, background, text colors, and font size.

Key Features:

Real-Time Digital Clock: The indicator shows the current time in your selected time zone (Asia/Tokyo, America/New_York, Europe/London, Australia/Sydney). The time updates in real-time and includes hours, minutes, and seconds, providing a convenient and accurate way to monitor time across different trading sessions.

Global Market Status: Displays the open or closed status of major financial markets.

・Tokyo Market: Open from 9:00 AM to 3:00 PM (JST).

・London Market: Open from 16:00 to 24:00 during summer time and from 17:00 to 1:00 during winter time (JST).

・New York Market: Open from 21:00 to 5:00 during summer time and from 22:00 to 6:00 during winter time (JST).

Customizable Display:

・Background Color: The indicator allows you to set the background color for the clock display, while the leftmost empty cell can be independently customized with its own background color for table alignment.

・Clock and Market Status Colors: Separate color options are available for the clock text, market status during open, and market status during closed periods.

・Text Size: You can adjust the size of the text (small, normal, large) to fit your preferences.

・Table Position: You can position the digital clock and market status table in different locations on the chart: top left, top center, top right, bottom left, bottom center, and bottom right.

Alerts for Market Opening: The indicator will trigger alerts when a market (Tokyo, London, or New York) opens, notifying traders in real-time. This can help ensure that you don't miss any important market openings.

How to Use:

Setup:

Apply the Indicator: Add the Digital Clock with Market Status and Alerts indicator to your chart. Customize the time zone, text size, background colors, and table position based on your preferences.

Monitor Market Status: Watch the market status displayed for Tokyo, London, and New York to keep track of market openings and closings in real-time.

Receive Alerts: The indicator provides built-in alerts for market openings, helping you stay informed when a key market opens for trading.

Time Monitoring:

・Real-Time Clock: The current time is displayed with hours, minutes, and seconds for accurate tracking. The clock updates every second and reflects the selected time zone.

・Global Time Zones: Choose your desired time zone (Tokyo, New York, London, Sydney) to monitor the time most relevant to your trading strategy.

Market Status:

・Tokyo Market: The status will display "Tokyo OPEN" when the Tokyo market is active, and "Tokyo CLOSED" when it is outside of trading hours.

・London Market: Similarly, the indicator will show "London OPEN" or "London CLOSED" depending on whether the London market is currently active.

・New York Market: The New York market status follows the same structure, showing "NY OPEN" or "NY CLOSED."

Customization:

・Table Positioning: Easily move the table to the desired location on the chart to avoid overlap with other chart elements. The leftmost empty cell helps with alignment.

・Text and Background Color: Adjust the text and background colors to suit your personal preferences. You can also set independent colors for open and closed market statuses to easily distinguish between them.

Cautions and Disclaimer:

・Indicator Modifications: This indicator may be updated without prior notice, which could change or remove certain features.

・Trade Responsibility: This indicator is a tool to assist your trading, but responsibility for all trades remains with you. No guarantee of profit or success is implied, and losses can occur. Use it alongside your own analysis and strategy.

Digital Clock with Market Status and Alerts - 解説と使い方

概要:

Digital Clock with Market Status and Alerts インジケーターは、さまざまな世界のタイムゾーンで現在の時刻を表示し、東京、ロンドン、ニューヨークなどの主要な金融市場のステータスを提供します。このインジケーターにより、複数の市場のオープンおよびクローズ時間をリアルタイムで監視でき、市場がオープンする際にアラートを受け取ることができます。テーブルの位置、背景色、テキストカラー、フォントサイズなどのカスタマイズが可能です。

主な機能:

リアルタイムデジタル時計: 選択したタイムゾーン(東京、ニューヨーク、ロンドン、シドニー)の現在時刻を表示します。リアルタイムで更新され、時間、分、秒を正確に表示します。

世界の市場ステータス: 主要な金融市場のオープン/クローズ状況を表示します。

・東京市場: 午前9時~午後3時(日本時間)。

・ロンドン市場: 夏時間では16時~24時、冬時間では17時~1時(日本時間)。

・ニューヨーク市場: 夏時間では21時~5時、冬時間では22時~6時(日本時間)。

カスタマイズ可能な表示設定:

・背景色: 時計表示の背景色を設定できます。また、テーブルの左側に空白のセルを配置し、独立した背景色を設定することでテーブルの配置調整が可能です。

・時計と市場ステータスの色: 時計テキスト、オープン市場、クローズ市場の色を個別に設定できます。

・テキストサイズ: 小、標準、大から選択し、テキストサイズをカスタマイズ可能です。

・テーブル位置: デジタル時計と市場ステータスのテーブルをチャートのさまざまな場所(左上、中央上、右上、左下、中央下、右下)に配置できます。

市場オープン時のアラート: 市場(東京、ロンドン、ニューヨーク)がオープンするときにアラートを発し、リアルタイムで通知されます。これにより、重要な市場のオープン時間を逃さないようサポートします。

使い方:

セットアップ:

インジケーターを適用: チャートに「Digital Clock with Market Status and Alerts」インジケーターを追加し、タイムゾーン、テキストサイズ、背景色、テーブル位置を好みに応じてカスタマイズします。

市場ステータスを確認: 東京、ロンドン、ニューヨークの市場ステータスをリアルタイムで表示し、オープン/クローズ時間を把握できます。

アラートを受け取る: 市場オープン時のアラート機能により、重要な市場のオープンを見逃さないように通知が届きます。

時間管理:

・リアルタイム時計: 現在の時刻が秒単位で表示され、選択したタイムゾーンに基づいて正確に追跡できます。

・グローバルタイムゾーン: 東京、ニューヨーク、ロンドン、シドニーなど、トレードに関連するタイムゾーンを選択して監視できます。

市場ステータス:

・東京市場: 東京市場が開いていると「Tokyo OPEN」と表示され、閉じている場合は「Tokyo CLOSED」と表示されます。

・ロンドン市場: 同様に、「London OPEN」または「London CLOSED」が表示され、ロンドン市場のステータスを確認できます。

・ニューヨーク市場: ニューヨーク市場も「NY OPEN」または「NY CLOSED」で現在の状況が表示されます。

カスタマイズ:

・テーブル位置の調整: テーブルの位置を簡単に調整し、チャート上の他の要素と重ならないように配置できます。左側の空白セルで位置調整が可能です。

・テキストと背景色のカスタマイズ: テキストと背景の色を自分の好みに合わせて調整できます。また、オープン時とクローズ時の市場ステータスを区別するため、独立した色設定が可能です。

注意事項と免責事項:

・インジケーターの変更: このインジケーターは、予告なく変更や機能の削除が行われる場合があります。

・トレード責任: このインジケーターはトレードをサポートするツールであり、トレードに関する全責任はご自身にあります。利益を保証するものではなく、損失が発生する可能性があります。自分の分析や戦略と組み合わせて使用してください。

Options

Line Chart ShiftedThis indicator is designed to assist traders who rely on both line charts and candlestick patterns in their technical analysis. By plotting the closing price from previous bars and shifting it left by a customizable amount, this indicator overlays a line chart directly onto a candlestick chart, giving traders a clearer view of trends and key levels.

Key Features:

Shifted Close Price: The line is plotted based on the closing prices of the previous 3 candles, providing an advanced view of the market's price movements.

Customizable Line Width and Color: Traders can easily modify the thickness and color of the line to match their charting style or improve visibility when analyzing price action.

How It Helps:

Combines Line and Candlestick Charts: For traders who analyze both line and candlestick charts, this indicator provides an effective way to see how price has been evolving, helping to identify support, resistance, and trend lines more easily.

Enhanced Visualization: By shifting the line slightly to the left, the overlay offers a clean separation between the current candlestick and the historical line, improving clarity and making it easier to spot trends.

US Market Support & ResistanceUS Market Support & Resistance Indicator (For 5-30 Minute Timeframes)

This indicator plots key support and resistance levels for the US market based on the high and low of the first candle at the market open. It also shades the area between these levels with a color that dynamically changes to indicate the current trend:

* Green: Price is above the resistance level, suggesting a potential uptrend.

* Red: Price is below the support level, suggesting a potential downtrend.

* Gray: Price is trading between the support and resistance levels, suggesting a sideways trend.

Additionally, the indicator displays a small dashboard in the top right corner of the chart showing the current trend ("Upward", "Downward", or "Sideways") in the corresponding color.

Key Features:

* US Market Time Identification: Accurately identifies US market open and close times in UTC and colors candles red during these times.

* Support & Resistance Plotting: Plots support and resistance lines at the high and low of the first candle at the market open and extends them infinitely on the chart.

* Shaded Area Between Levels: Shades the area between the support and resistance lines with a color that dynamically changes based on the current price location relative to these levels.

* Trend Display: Displays a dashboard showing the current trend based on the shaded area's color.

* Open Alert: Issues an alert when the US market opens.

* Supported Timeframes: Works on timeframes less than 30 minutes and greater than 5 minutes.

* Economic News: Not recommended for use during periods of sporadic economic news releases, as sudden price fluctuations may cause false signals.

How to Use:

* Add the indicator to your chart, ensuring the timeframe is between 5 and 30 minutes.

* Wait for the US market to open.

* Observe the shaded area's color and the dashboard to identify the current trend.

* Use the support and resistance levels to make trading decisions, keeping in mind not to rely solely on it during news releases.

Caution: This indicator relies on support and resistance levels drawn at the US market open and may not always be accurate, especially during periods of high volatility. It should be used in conjunction with other technical analysis tools to confirm the trend and make informed trading decisions.

Note: This description is designed to be compliant with TradingView's policies on indicator publishing.

Tomorrow Floor Pivots with CPR By Nifty ZThe colors for resistance and support levels have been updated to gradient reds and greens for clearer distinction.

The CPR band uses light blue and purple to stand out more effectively.

Here's a detailed explanation of the user inputs and the typical use of **Floor Pivots for Tomorrow’s Market Range** in a trading context, focusing on support, resistance, and breakout scenarios:

The script allows traders to customize key parameters for their analysis:

1. Pivot Timeframe:

- Users can select different timeframes for calculating floor pivots, such as 1 hour, 4 hours, daily, weekly, monthly, etc.

- This is crucial because the timeframe selection influences the granularity of the support and resistance levels for the next trading day.

- For instance, selecting a **Daily** timeframe will calculate floor pivots for the next trading day, while selecting **Weekly** will give levels for the upcoming week.

2. Show Floor Pivots:

- Users can toggle the visibility of the calculated **Floor Pivots**, which include resistance levels (R1, R2, R3, R4) and support levels (S1, S2, S3, S4).

3. Show CPR (Central Pivot Range):

- CPR (Central Pivot Range) is a key area where the price tends to consolidate.

- The script allows users to enable or disable the visibility of CPR, which consists of the BC (Bottom Central Pivot) and TC (Top Central Pivot).

4. Show Labels:

- Users can choose whether or not to display labels indicating the **Pivot**, **Support**, and Resistance levels on the chart. This can be helpful for visual analysis when day trading.

Understanding Floor Pivots

The Floor Pivots (Pivot, Resistance, and Support levels) for tomorrow's market range are calculated based on today’s high, low, and close. These levels help traders anticipate how the market may behave in the upcoming session.

1. Pivot:

- The Pivot Point is a central level, calculated as the average of the high, low, and close. It’s considered a reference point that determines the market’s overall bias.

- If the price is trading **above the pivot**, it generally suggests a **bullish** sentiment for the day.

- If the price is trading **below the pivot**, it suggests a **bearish** sentiment.

2. Resistance Levels (R1, R2, R3, R4):

- R1 is often the first area where price may stall in an uptrend. It represents the first major resistance level.

- **R2**, **R3**, and **R4** mark additional levels of resistance, progressively further away from the current price. These are used to project potential upward targets.

- These resistance levels are areas where the price might encounter selling pressure, especially during day trading.

3. **Support Levels (S1, S2, S3, S4):**

- Similarly, **S1** is the first area where the price might find support in a downtrend.

- **S2**, **S3**, and **S4** provide deeper support levels where the price may bounce from.

- These support zones are used by day traders to anticipate where the price might reverse upward.

### **Role of Resistance and Support in Day Trading**

- **Resistance Levels (R1, R2, R3, R4)** indicate potential areas where price could **stall** during an uptrend. These levels are useful for **short-term traders** looking to set exit points or identify reversal zones.

- **Support Levels (S1, S2, S3, S4)** highlight areas where the price could **find support** and potentially **bounce** higher. These levels are particularly helpful for identifying buy zones in a downtrend.

- If a price **breaks out** above the resistance levels or **breaks down** below the support levels, it often signals a strong trend continuation.

### **Understanding the Central Pivot Range (CPR)**

The **CPR** is formed by two key levels:

- **BC (Bottom Central Pivot):** The midpoint of the day’s high and low.

- **TC (Top Central Pivot):** The difference between the pivot and BC.

The CPR acts as a region of **consolidation** or **indecision** where the market is likely to stay within a narrow range. The width of the CPR gives traders a sense of volatility:

- A **narrow CPR** often signals that a **breakout** is imminent.

- A **wider CPR** suggests that the market could remain range-bound.

### **Market Sentiment Based on Floor Pivots**

The relationship between **today’s** and **tomorrow’s pivots** is crucial in determining the market sentiment for the next day.

1. **Bullish Case (Higher Highs):**

- If **tomorrow's pivot** is higher than **today's pivot**, it indicates a **bullish sentiment**. This suggests that the market is likely to trend upward in the next session.

- In a **bullish overlapping pivot range**, if **Day 1 (today)** is higher than **Day 2 (tomorrow)**, traders expect continued upward momentum.

2. **Bearish Case (Lower Lows):**

- Conversely, if **tomorrow's pivot** is lower than **today's pivot**, it suggests a **bearish sentiment** and that the market could trend downward in the next session.

- In a **bearish overlapping pivot range**, if **Day 1 (today)** is lower than **Day 2 (tomorrow)**, traders expect continued downward pressure.

### **Breakout Scenarios**

A breakout occurs when the price **violates either the support or resistance levels** significantly, indicating that the price is moving in the direction of the breakout.

1. **Bullish Breakout:**

- If the price consistently stays **above the CPR** and **resistance levels (R1, R2)**, it indicates a strong **bullish breakout**.

- This is especially true when the **CPR is narrow** for both days, signaling a buildup in price action and a potential breakout to the upside.

2. **Bearish Breakout:**

- If the price breaks **below the CPR** and **support levels (S1, S2)**, it indicates a **bearish breakout**.

- A narrow CPR on **both days** suggests that a breakout to the downside could be imminent.

3. **Neutral or Ranging Days:**

- Sometimes, the CPR stays **unchanged** for 4-5 days, indicating a period of **consolidation** where the price is moving within a tight range. This often leads to a significant breakout once the consolidation ends.

Strategic Application of Floor Pivots for Tomorrow

Traders use floor pivots to plan their next-day trades by:

- **Aligning with Market Sentiment:** Based on whether tomorrow’s pivot is higher or lower than today’s, traders can align their trades in the direction of the market’s overall bias.

- **Identifying Entry and Exit Points:** Resistance and support levels provide well-defined areas to enter or exit trades, making pivots essential for day trading strategies.

- **Anticipating Breakouts:** Monitoring the width of the CPR and the relation between pivots helps traders anticipate potential breakouts, allowing them to react quickly to sudden price movements.

By effectively using these pivots and understanding their significance, traders can improve their decision-making for short-term trades in the stock or futures markets.

Volume-Price PercentileDescription:

The "Volume-Price Percentile Live" indicator is designed to provide real-time analysis of the relationship between volume percentiles and price percentiles on any given timeframe. This tool helps traders assess market activity by comparing how current volume levels rank relative to historical volume data and how current price movements (specifically high-low ranges) rank relative to historical price data. The indicator visualizes the ratio of volume percentile to price percentile as a histogram, allowing traders to gauge the relative strength of volume against price movements in real time.

Functionality:

Volume Percentile: Calculates the percentile rank of the current volume within a user-defined rolling period (default is 30 bars). This percentile indicates where the current volume stands in comparison to historical volumes over the specified period.

Price Percentile: Calculates the percentile rank of the current candle's high-low difference within a user-defined rolling period (default is 30 bars). This percentile reflects the current price movement's strength relative to past movements over the specified period.

Percentile Ratio (VP Ratio): The indicator plots the ratio of the volume percentile to the price percentile. This ratio helps identify periods when volume is significantly higher or lower relative to price movement, providing insights into potential market imbalances or strength.

Real-Time Data: By fetching data from a lower timeframe (e.g., 1-minute), the indicator updates continuously within the current timeframe, offering live, intra-candle updates. This ensures that traders can see the histogram change in real-time as new data becomes available, without waiting for the current candle to close.

How to Use:

Adding the Indicator: To use this indicator, add it to your chart on TradingView by selecting it from the Indicators list once it is published publicly.

Setting Parameters:

Volume Period Length: This input sets the rolling window length for calculating the volume percentile (default is 30). You can adjust it based on the desired sensitivity or historical period relevance.

Candle Period Length: This input sets the rolling window length for calculating the price percentile based on the high-low difference of candles (default is 30). Adjust this to match your trading style or analysis period.

Interpreting the Histogram:

The histogram represents the volume percentile divided by the price percentile.

Above 1: A value greater than 1 indicates that volume is relatively strong compared to price movement, which may suggest high activity or potential accumulation/distribution phases.

Below 1: A value less than 1 suggests that price movement is relatively stronger than volume, indicating potential weakness in volume relative to price moves.

Near 1: Values close to 1 suggest a balanced relationship between volume and price movement.

Application: Use this indicator to identify potential breakout or breakdown scenarios, assess the strength of price movements, and confirm trends. When volume percentile consistently leads price percentile, it might signal sustained interest and support for the current price trend. Conversely, if volume percentile lags significantly, it might warn of potential trend weakness.

Best Practices:

Multiple Timeframe Analysis: While the indicator provides real-time updates on any timeframe, consider using it alongside higher timeframe analysis to confirm trends and volume behavior across different periods.

Customization: Adjust the period lengths based on the asset’s typical volume and price behavior, as well as your trading strategy (e.g., short-term scalping vs. long-term trend following).

Complement with Other Indicators: Use this indicator in conjunction with other volume-based tools, trend indicators, or momentum oscillators to gain a comprehensive view of market dynamics.

Fixed Straddle with dynamic Res/Sup [BlueChip Algos]Fixed Straddle/Strangle with Dynamic Resistance and Support indicator is designed for options traders focusing on combined straddle and strangle premiums of particular strikes (without rolling). This script offers dynamic charting capabilities with integrated technical indicators, making it a valuable tool for traders in the Indian options market.

About the Indicator

This indicator allows traders to analyze straddle and strangle positions using pre-set strike prices. It dynamically plots resistance and support levels based on price movements using swing HIGHs and LOWs, plots potential stop-loss levels using ATR Stop Loss combined with other customizable indicators like Moving Averages, SuperTrend and VWAP

Features

Straddle and Strangle Analysis: Users can analyze options straddle or custom strangle positions by specifying the exact strike prices for both CE (Call) and PE (Put) options. Please note that one needs to give required strike in all 3 fields mandatorily (Fixes staddle, CE and PE) irrespective of whether you select straddle or strangle in the dropdown.

Dynamic Resistance and Support: The script dynamically adjusts support and resistance levels based on price movements, providing insights into potential price reversal points.

Comprehensive Indicator Suite: Includes popular indicators like Moving Averages, SuperTrend, ATR Stop Loss, and VWAP, each customizable to fit the trader's strategy.

Input Parameters

Chart Type: Choose between "Fixed Straddle" and "Fixed Strangle" for the analysis.

Symbol Selection: Select from various Indian indices such as NIFTY, BANKNIFTY, MIDCAP, FINNIFTY, SENSEX, BANKEX, or input a custom symbol.

Strike Prices: Set the exact strike prices for the fixed straddle or strangle analysis. Note to enter value in all 3 strike fields irrespective of straddle or strangle selection.

Expiry Date: Select the expiry date for the options.

Indicator Settings: Customize each indicator’s parameters, including Moving Averages, SuperTrend, ATR Stop Loss, VWAP, and Swing High/Low levels.

Understanding the Indicator

1. Dynamic Resistance and Support Levels using swing H/Ls

Purpose: This indicator identifies significant swing highs and lows, which are key levels for potential price reversals or continuation.

Parameters:

Swing Length: Number of bars used to confirm swing highs and lows.

How It Works: The Swing High/Low Levels are plotted based on past price action, marking the areas where the price has previously reversed, helping traders set their stop-loss or take-profit levels.

2. VWAP (Volume Weighted Average Price)

Purpose: VWAP provides the average price weighted by volume over a specified period. It is widely used by traders to identify the true average price of a security.

How It Works: VWAP is plotted as a line on the chart, which helps in understanding the price direction in relation to the day's volume-weighted average price.

3. ATR Stop Loss

Purpose: The ATR Stop Loss dynamically adjusts stop-loss levels based on the market’s volatility, calculated through the ATR.

Parameters:

ATR Period: Number of periods over which ATR is calculated.

Multiplier: Factor that determines the distance of the stop-loss from the current price.

How It Works: This indicator adjusts the stop-loss level to protect against large market swings, moving closer or further away based on the ATR value.

4. Moving Average (MA)

Purpose: The Moving Average smooths price data to help identify trends and reversals. It is useful for understanding the overall market direction.

Parameters:

MA Source: Data source for the Moving Average calculation (e.g., Close price).

MA Length: The number of periods used to calculate the Moving Average.

MA Smoothing: The type of smoothing applied, such as SMA, EMA, WMA, or RMA.

5. SuperTrend

Purpose: SuperTrend is a trend-following indicator that helps traders identify the prevailing market trend and potential entry/exit points.

Parameters:

Factor: The multiplier applied to the ATR (Average True Range) for calculating the SuperTrend bands.

ATR Period: The number of periods used for calculating the ATR.

How It Works: The SuperTrend line acts as a support or resistance level. A price above the SuperTrend line indicates a bullish trend, while a price below it indicates a bearish trend.

Smooth Trailing Stop

Trading indicator designed to provide traders with a dynamic and responsive stop-loss mechanism, leveraging a combination of Zero Lag Exponential Moving Averages (ZEMA) and the Average True Range (ATR). This indicator is particularly useful for traders looking to capture trends while managing risk effectively. Future notes: will add MTF analysis. First

Key Features:

Zero Lag EMA (ZEMA): This indicator uses a Zero Lag EMA, which helps to reduce the lag traditionally associated with moving averages, providing a more accurate reflection of price action.

ATR-Based Trailing Stop: The stop-loss level is dynamically calculated using a multiplier of the ATR, which adjusts to the volatility of the market, ensuring that the stop-loss distance is neither too tight nor too loose.

Position Tracking: The indicator tracks the position (long or short) based on the relationship between the price and the trailing stop, coloring the stop line green for a long position and red for a short position.

Candle Coloring: Candles are colored green when a buy signal is generated and red otherwise, giving a visual cue to the trader.

Customizable Inputs:

Period: Define the number of periods used for the ZEMA calculation.

ATR Period & Multiplier: Adjust the period and multiplier used for ATR, allowing for customization based on the trader’s risk tolerance and market conditions.

Line Width: Customize the width of the trailing stop line for better visibility on the chart.

This indicator is suitable for traders of all experience levels who are looking for a smooth trailing stop system for their trading strategy.

Theta Shield | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Theta Shield indicator! Theta is the options risk factor concerning how fast there is a decline in the value of an option over time. This indicator aims to help the trader avoid sideways market phases in the current ticker, to minimize the risk of theta decay. For more information, please check the "How Does It Work" section.

Features of the new Theta Shield Indicator :

Foresight Of Accumulation Zones

Decrease Risk Of Theta Decay

Clear "Valid" & "Non-Valid" Signals

Validness Trail

Alerts

📌 HOW DOES IT WORK ?

In options trading, theta is defined as the rate of decline in the value of an option due to the passage of time. Traders want to avoid this kind of decay in the value of an option. One of the best ways to avoid it is not holding an option contract when the market is going sideways. This indicator uses a stochastic oscillator to try to get a foresight of sideways markets, warning the trader to not hold an option contract while the price is in a range.

The indicator starts by calculating the stochastic value using close, high & low prices of the candlesticks. Then a stoch threshold & a theta length are determined depending on the option contract type defined by the user in the settings of the indicator. Each candlestick that falls above or below the stoch threshold value is counted, and a "theta valid strength" is calculated using the counted candlesticks, which has a value between -100 & 100. Here is the formula of the "theta valid strength" value :

f_lin_interpolate(float x0, float x1, float y0, float y1, float x) =>

y0 + (x - x0) * (y1 - y0) / (x1 - x0)

thetaValid = Total Candlesticks That Fall Above & Below The Threshold In Last "Theta Length" bars.

thetaValidStrength = f_lin_interpolate(0, thetaLength, -100, 100, thetaValid)

Then a trail is rendered, and "Valid" & "Non-Valid" signals are given using this freshly calculated strength value. Valid means that the indicator currently thinks that no accumulation will happen in the near future, so the option positions in the current ticker are protected from the theta decay. Non-Valid means that the indicator thinks the ticker has entered the accumulation phase, so holding any option position is not recommended, as they may be affected by the theta decay.

🚩 UNIQUENESS

This indicator offers a unique way to avoid theta decay in options trading. It uses a stochastic oscillator and thresholds to calculate a "theta strength" value, which is used for rendering validness signals and a trail. Traders can follow the valid & non-valid signals when deciding to hold their options position or not. The indicator also has an alerts feature, so you can get notified when a ticker is about to enter a range, or when it's about to get out of it.

⚙️ SETTINGS

1. General Configuration

Contract Type -> You can set the option contract type here. The indicator will adjust itself to get a better foresight depending on the contract length.

2. Style

Fill Validness -> Will render a trail based on "theta strength" value.

[1] Dynamic Support and Resistance with breakout [Dr Future]This script appears to be designed to identify and visualize dynamic support and resistance levels on a price chart, along with potential breakout signals.

Key Components & Functionality (Inferred):

Dynamic Support and Resistance: The script likely employs algorithms to calculate and plot support and resistance levels that adjust in real-time as price action evolves.

Breakout Detection: The script probably incorporates logic to recognize when the price breaks out of these dynamic support or resistance zones. This could trigger alerts or visual cues on the chart.

Dr Future's Approach: It's worth noting the " " tag, suggesting the script might be based on specific methodologies or insights associated with a trader or analyst known as "Dr Future." Without more context on their strategies, it's difficult to pinpoint the exact techniques used.

Potential Benefits:

Adaptive Levels: Dynamic support and resistance can offer a more responsive approach compared to static levels, as they account for changing market conditions.

Breakout Opportunities: Identifying breakouts can help traders spot potential entry or exit points.

Visual Clarity: Plotting these levels directly on the chart can provide a clearer picture of the current market structure and potential turning points.

Caveats:

False Signals: Like any technical tool, dynamic support and resistance can generate false signals. Breakouts might not always lead to sustained trends.

Parameter Sensitivity: The script's effectiveness likely depends on how its parameters are configured. Fine-tuning might be required to suit different markets or timeframes.

"Dr Future" Factor: The script's performance could be tied to the specific strategies of "Dr Future," which might not be universally applicable.

Important Note:

Without access to the actual code and a deeper understanding of "Dr Future's" methods, this description is based on inference and general knowledge of technical analysis.

Recommendation:

If you're considering using this script, it would be prudent to:

Backtest Thoroughly: Test the script on historical data to assess its performance and identify potential pitfalls.

Understand the Parameters: Familiarize yourself with the script's settings and how they impact the plotted levels and breakout signals.

Combine with Other Tools: Use this script in conjunction with other technical indicators and risk management strategies for a more holistic trading approach.

Daily Bias Engine | PDH/PDL Range This program is designed to track the previous day range and interactions with the mean threshold on the following day.

The bias strategy is simple:

If you create new range highs over a PDH, you will lean towards calls.

If you create new range lows over a PDL, you will learn towards puts.

If neither event happens, no bias can be determined and therefore no trades taken.

If by 12:00pm there still is no bias determined, it will show moderate strength based on the trend.

Remember, use this strategy to outline your bias and find a cheap entry model to take advantage of.

Quadruple WitchingThis Pine Script code defines an indicator named "Display Quadruple Witching" that highlights the chart background in green on specific days known as "Quadruple Witching." Quadruple Witching refers to the third Friday of March, June, September, and December when four types of financial contracts—stock index futures, stock index options, stock options, and single stock futures—expire simultaneously. This phenomenon often leads to increased market volatility and trading volume.

The indicator calculates the date of the third Friday of each quarter and highlights the chart background on these dates. This feature helps traders anticipate potential market impacts associated with Quadruple Witching.

Importance of Quadruple Witching

Quadruple Witching is significant in financial markets for several reasons:

Increased Market Activity: On these dates, the market often experiences a surge in trading volume as traders and institutions adjust their positions in response to the expiration of multiple derivative contracts (CFA Institute, 2020).

Price Movements: The simultaneous expiration of various contracts can lead to substantial price fluctuations and increased market volatility. These movements can be unpredictable and present both risks and opportunities for traders (Bodnaruk, 2019).

Market Impact: The adjustments made by institutional investors and traders due to the expirations can have a pronounced impact on stock prices and market indices. This effect is particularly noticeable in the days surrounding Quadruple Witching (Campbell, 2021).

References

CFA Institute. (2020). The Impact of Quadruple Witching on Financial Markets. CFA Institute Research Foundation. Retrieved from CFA Institute.

Bodnaruk, A. (2019). The Effect of Option Expiration on Stock Prices. Journal of Financial Economics, 131(1), 45-64. doi:10.1016/j.jfineco.2018.08.004

Campbell, J. Y. (2021). The Behaviour of Stock Prices Around Expiration Dates. Journal of Financial Economics, 141(2), 577-600. doi:10.1016/j.jfineco.2021.01.001

These references provide a deeper understanding of how Quadruple Witching influences market dynamics and why being aware of these dates can be crucial for trading strategies.

Rolling Straddle with swing High/Low [Bluechip Algos]The Rolling Straddle and Strangle indicator is designed for options traders, particularly those trading in Indian indices such as NIFTY, BANKNIFTY, and others. This script not only allows users to analyze rolling straddle and strangle strategies by plotting various metrics but also has several indicators to apply on top of straddle/strangle charts. Especially indicators like swing high/low and ATR stop loss help you identify potential entry and exit points respectively.

About the Indicator

This indicator plots rolling straddles and strangles based on the selected symbol, strike prices, and expiry dates. Users can choose between analyzing single or multiple charts, and the script dynamically adjusts for different symbols, including NIFTY, BANKNIFTY, and other indices. Additionally, it incorporates several popular technical indicators to assist in decision-making.

Features

Dynamic Strike Price Calculation: Automatically adjusts strike prices based on the selected symbol and ATM (At-The-Money) reference.

Straddle and Strangle Analysis: Offers both rolling straddle and rolling strangle options, providing detailed views of option prices.

Table Plotting: Displays a table with the strike prices and corresponding CE (Call) and PE (Put) prices, including combined values.

Integrated Indicators: Includes customizable indicators such as Swing High/Low levels, ATR Stop Loss, Moving Averages, SuperTrend, and VWAP each designed to enhance strategy analysis.

Understanding the Indicator

1. Swing High/Low Levels

Purpose: This indicator identifies swing highs and lows in the price data, which are key levels that traders often use for placing stop-loss orders or for identifying potential reversal points.

Parameters:

Swing Length: The number of bars before and after the current bar that must be lower/higher to confirm a swing high/low.

How It Works: The indicator marks the highest high and lowest low over the specified period, helping traders to identify key support and resistance levels.

2. ATR Stop Loss

Purpose: The ATR Stop Loss is used to determine a dynamic stop-loss level based on the volatility of the asset. It adjusts the stop-loss level as the market conditions change.

Parameters:

ATR Period: The number of periods over which the ATR is calculated.

Multiplier: Factor used to adjust the stop-loss distance from the current price.

How It Works: The stop-loss level is adjusted dynamically based on the ATR value, providing protection against large, unexpected moves.

3. Moving Average (MA)

Purpose: The Moving Average is used to smooth out price data, providing a clearer view of the price trend over time. It is particularly useful for identifying the direction of the trend.

Parameters:

MA Source: The data series used for calculating the Moving Average (e.g., Close price).

MA Length: The number of periods over which the Moving Average is calculated.

MA Smoothing: The method used for smoothing the data, such as SMA (Simple Moving Average), EMA (Exponential Moving Average), WMA (Weighted Moving Average), or RMA (Running Moving Average).

4. SuperTrend

Purpose: The SuperTrend indicator is a trend-following indicator that helps traders identify the prevailing trend. It is based on the ATR (Average True Range) and provides clear buy/sell signals.

Parameters:

Factor: Multiplier applied to the ATR to calculate the upper and lower bands.

ATR Period: The period over which the ATR is calculated.

How It Works: When the price is above the SuperTrend line, it indicates a bullish trend, and when the price is below, it indicates a bearish trend.

5. VWAP (Volume Weighted Average Price)

Purpose: VWAP is a trading benchmark used by traders that gives the average price a security has traded at throughout the day, based on both volume and price. It is often used to determine the general direction of the market and as a basis for intraday trading strategies.

How It Works: VWAP calculates the cumulative price-volume divided by the cumulative volume over a specified period, providing a weighted average price that is more reflective of true market activity.

Input Parameters

Chart Type: Select between "Rolling Straddle" and "Rolling Strangle."

Symbol Selection: Choose from NIFTY, BANKNIFTY, MIDCAP, FINNIFTY, SENSEX, BANKEX, or a custom symbol.

Strike Interval: Customize strike intervals for different indices.

Expiry Date: Select the option expiry date.

Table Settings: Configure the table's position and colors for better visibility.

Indicator Settings: Customize each indicator’s parameters to suit your trading strategy, including lengths, smoothing methods, and colors.

VIX Opening GapOverview

This simple script generates alerts based on the difference between the previous trading day's VIX close and the current trading day's opening bar. It is designed for use on the TVC version of the VIX chart, with 1-minute bars.

Features

The script flags one of four conditions based on the difference between the previous day's close and the current day's open: (1) open up; (2) open down; (3) gap up; and (4) gap down. The thresholds for gaps up and down are expressed as percentages and can be changed in the input settings.

The script can assess the gap at the first bar of the premarket session or at the first bar printed after market open. Change this by toggling the "Use Premarket Hours" feature in the input settings.

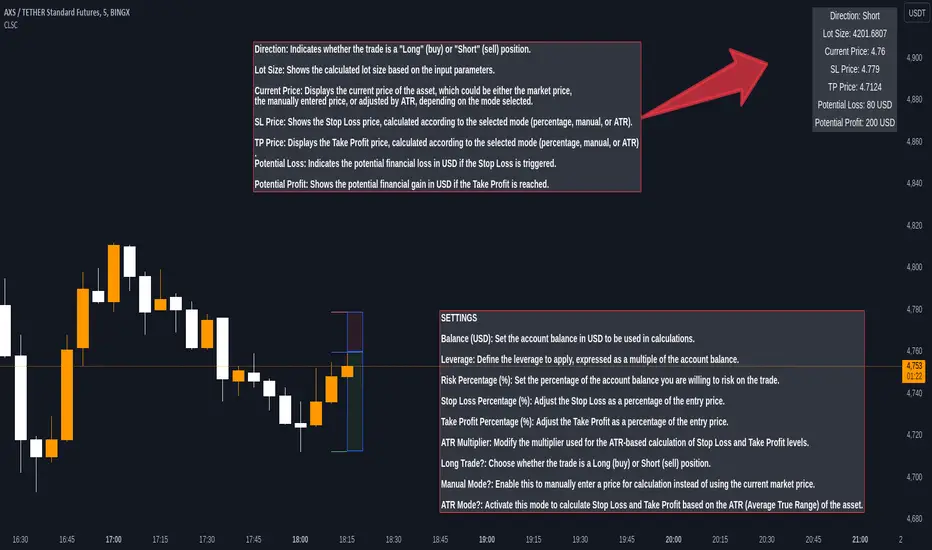

Lot Size Calculator [SCRIPTS INVERSIONES]1. Balance (USD)

Description: This input allows you to set your trading account balance in USD. The balance is used to calculate the amount of money you are risking on a trade.

How to Use: Enter the total balance of your trading account. For example, if you have $1,000 in your account, you would input 1000.

2. Leverage

Description: Leverage multiplies your purchasing power, allowing you to control a larger position than your account balance would normally allow.

How to Use: Set the leverage level you are using. For example, if your broker offers 20x leverage, you would input 20. This will affect the size of your positions and the potential risk and reward.

3. Risk Percentage (%)

Description: This is the percentage of your account balance that you are willing to risk on a single trade.

How to Use: Enter the percentage of your balance you want to risk. For instance, if you want to risk 1% of your $1,000 balance, you would input 1. The script will then calculate the maximum amount of money you can lose on the trade.

4. Stop Loss Percentage (%)

Description: This is the percentage distance from your entry price at which your Stop Loss (SL) will be set.

How to Use: Input the percentage you want for the Stop Loss. For example, if you want the SL to be set 1% below the entry price, you would input 1. This is used when not in manual or ATR mode.

5. Take Profit Percentage (%)

Description: This is the percentage distance from your entry price at which your Take Profit (TP) will be set.

How to Use: Input the percentage for the Take Profit. For example, if you want the TP to be set 2% above the entry price, you would input 2. This is used when not in manual or ATR mode.

6. ATR Multiplier

Description: The Average True Range (ATR) is a measure of volatility, and this multiplier adjusts how far your Stop Loss and Take Profit are set based on ATR.

How to Use: If you're using ATR mode, set the multiplier to adjust the distance of your SL and TP. For example, if the ATR is 10 and you set a multiplier of 1.5, the SL and TP will be set 15 units away from the entry price.

7. Long Trade?

Description: This option determines whether your trade is a "Long" (buy) or "Short" (sell) position.

How to Use: Select true if you are going long (expecting the price to rise), or false if you are going short (expecting the price to fall). This will influence how the SL and TP are calculated.

8. Manual Mode?

Description: In Manual Mode, you can manually input an entry price instead of using the current market price for calculations.

How to Use: Enable this mode by setting it to true if you want to manually enter a specific price. You will then need to input your desired entry price in the "Manual Price" field.

9. ATR Mode?

Description: When ATR Mode is enabled, the script uses the ATR to calculate Stop Loss and Take Profit levels instead of using fixed percentages.

How to Use: Enable this mode by setting it to true to calculate SL and TP based on ATR. The SL and TP will then be adjusted automatically based on market volatility.

How to Use the Script with Different Modes

Automatic Mode with Percentages:

When to Use: If you want SL and TP to be set as a fixed percentage of the entry price.

Setup: Set Manual Mode to false and ATR Mode to false. Input your desired percentages for SL and TP.

Manual Mode:

When to Use: If you want to manually set the entry price and calculate SL and TP based on that price.

Setup: Set Manual Mode to true. Enter the manual price you want to use for calculations in the "Manual Price" field. SL and TP will be calculated based on this price.

ATR Mode:

When to Use: If you want SL and TP to adjust automatically based on market volatility.

Setup: Set ATR Mode to true and adjust the ATR Multiplier according to your preference. SL and TP will be set according to the ATR value multiplied by the chosen multiplier.

Custom Text DisplayThe "Custom Text Display" indicator allows users to display customizable text in a fixed position in the bottom-right corner of their chart. Each text entry can have its own color, which can be set in the indicator's settings. Follow these steps to set up and use the indicator effectively:

Adding the Indicator to Your Chart:

Apply the "Custom Text Display" indicator to your chart from the indicators list.

Configuring Text and Colors:

Open the settings for the indicator.

Enter the desired text for each of the five text fields labeled "Text 1", "Text 2", etc.

Choose a color for each text entry using the color pickers labeled "Color 1", "Color 2", etc.

Selecting the Active Text:

In the indicator settings, find the "Select Active Text" dropdown menu.

This menu offers six options: "0" (None), "1" (Text 1), "2" (Text 2), "3" (Text 3), "4" (Text 4), and "5" (Text 5).

Select the number corresponding to the text you want to activate. Only one text can be active at a time.

Viewing the Active Text on the Chart:

The selected active text will be displayed in the bottom-right corner of the chart with the corresponding background color.

If no text is selected (option "0"), no text will be displayed.

[SGM Geometric Brownian Motion]Description:

This indicator uses Geometric Brownian Motion (GBM) simulations to predict possible price trajectories of a financial asset. It helps traders visualize potential price movements, assess risks, and make informed decisions.

Geometric Brownian Motion:

Geometric Brownian Motion is an extension of standard Brownian motion (or Wiener process) used to model the random behavior of particles in physics. In finance, this concept is used to model the evolution of asset prices over time in a continuous manner. The basic idea is that the price of an asset does not only change randomly but also exponentially depending on certain parameters.

Basic formula

The formula for the evolution of the price of an asset S(t) under MBG is given by the following stochastic differential equation:

𝑑𝑆(𝑡) = 𝜇𝑆(𝑡)𝑑𝑡 + 𝜎𝑆(𝑡)𝑑𝑊(𝑡)

where:

S(t) is the price of the asset at time

μ is the expected growth rate (or drift).

σ is the volatility of the price of the asset.

dW(t) represents the noise term, i.e. the standard Brownian motion.

Explanations of the terms

Expected growth rate (μ):

This is the expected average return on the asset. If you think your asset will grow by 5% per year,

μ will be 0.05.

Volatility (σ):

It is a measure of the uncertainty or risk associated with the asset. If the asset price varies a lot, σ will be high.

Noise term (dW(t)):

It represents the randomness of the price change, modeled by a Wiener process.

Features:

Customizable number of simulations: Choose the number of price trajectories to simulate to get a better estimate of future movements.

Adjustable simulation length: Set the duration of the simulations in number of periods to adapt the indicator to your trading horizons.

Trajectory display: Visualize the simulated price trajectories directly on the chart to better understand possible future scenarios.

Dispersion calculations: Display the distribution of simulated final prices to assess dispersion and potential variations.

Sharpe ratio distribution: Analyze the risk-adjusted performance of simulations using the Sharpe ratio distribution.

Risk Statistics: Get key risk metrics like maximum drawdown, average return, and Value at Risk (VaR) at different confidence levels.

User Inputs:

Number of Simulations: 200 by default.

Simulation Length: 10 periods by default.

Brownian Motion Transparency: Adjust the transparency of simulated lines for better visualization.

Brownian Motion Display: Enable or disable the display of simulated paths.

Brownian Dispersion Display: Display the distribution of simulated final prices.

Sharpe Dispersion Display: Display the distribution of Sharpe ratios.

Customizable Colors: Choose colors for lines and tables.

Usage:

Configure Settings: Adjust the number of simulations, simulation length, and display preferences to suit your needs.

Analyze Simulated Paths: Simulated path lines appear on the chart, representing possible price developments.

Review Dispersion Charts: Review the charts to understand the distribution of final prices and Sharpe ratios, as well as key risk statistics. This indicator is ideal for traders looking to anticipate future price movements and assess the associated risks. With its detailed simulations and dispersion analyses, it provides valuable insight into the financial markets.

[SGM Return Distribution]Code Description

This Pine Script™ is designed to analyze the distribution of historical returns of a financial asset and project future confidence levels. It uses statistical techniques to estimate the probability of winning and losing as well as displaying confidence bands and distribution statistics.

User Entries

Length (252): The number of days used to calculate statistics.

Offset (20): Offset used to project future values.

Projection Days (10): Number of days projected into the future.

Smoothing Confidence Levels (10): Smoothing confidence bands.

Display Settings

Plot Distribution: Shows the distribution of returns.

Show Probabilities: Shows winning and losing probabilities.

Show Distribution Stats: Shows distribution statistics.

Show Confidence Bands: Shows confidence bands.

Show Confidence Lines: Shows confidence lines.

Calculations and Features

Distribution of Yields:

Calculates logarithmic returns and their statistics (average, volatility, skewness, kurtosis).

Projects the average and volatility over the projected number of days.

Displays the distribution of returns as a histogram.

Confidence Interval:

Uses the inv_norm function to calculate Z scores for different confidence levels.

Calculates the upper and lower bounds of the confidence bands.

Probability Display:

Calculates and displays win and loss probabilities based on the distribution of returns.

Statistics Display:

Shows key statistics such as mean, volatility, skewness and kurtosis.

Trust Bands and Lines:

Shows confidence bands and lines based on calculated confidence levels.

Mathematical Assumptions Used

Logarithmic Returns: Returns are calculated using the logarithm of prices, which is common for financial time series because it makes returns independent of price level.

Normal Distribution for Confidence Bands: Confidence interval calculations are based on the assumption that returns follow a normal distribution.

Average and Volatility Projection: Average returns and volatility are projected over a future period assuming they remain constant.

Skewness and Kurtosis: Although these measures are calculated for understanding the distribution of returns, they are not used in box projections but can provide additional information about the distribution of historical returns.

Use in Trading

Risk Estimation: Confidence bands can help estimate likely future price levels, which is crucial for determining strike levels and risk management.

Risk Management: Use confidence bands to set stop-loss and take-profit levels.

Probability Analysis: Win and loss probabilities can help assess a position's likelihood of success.

Potential Problems

Assumption of Normality for Confidence Bands: Financial returns do not always follow a normal distribution, especially in the presence of extreme events (fat tails).

Stationarity: Assuming that return statistics (average, volatility) remain constant over time can be erroneous in volatile market periods.

Limited Historical Data: Using a limited history (252 days) may not capture all possible behaviors of the asset.

Input Parameters: Results can be sensitive to the input parameters chosen (length, offset, etc.).

SparkPlusSparkPlus Indicator

The SparkPlus indicator is an advanced tool designed for real-time options trading, leveraging a unique combination of candlestick patterns and custom trade management logic. Unlike standard candlestick pattern indicators, SparkPlus integrates multiple layers of functionality to provide traders with actionable insights and comprehensive trade management. Here are the key features that set SparkPlus apart:

1. Unique Candlestick Patterns:

- Bullish Spark Pattern: Detects specific bullish candlestick formations over three bars, ensuring higher reliability in identifying upward trends.

- Bearish Spark Pattern: Identifies bearish formations over three bars, providing precise signals for potential downward movements.

2. Integrated Trade Management:

- The indicator not only signals potential trades but also manages them by setting entry points, stop loss, and multiple target levels.

- Dynamic Stop Loss and Target Calculation: The stop loss and target levels are dynamically calculated based on the volatility (using ATR), ensuring they adapt to market conditions.

3. Real-time Alerts:

- Provides real-time alerts for trade setups, entry points, stop loss hits, and target achievements, keeping traders informed and ready to act.

4. Detailed Trade Dashboard:

- A comprehensive dashboard is integrated into the chart to track the number of trades triggered, wins, losses, and points gained or lost for both long and short trades.

- This dashboard updates in real-time, providing an at-a-glance overview of the trading performance.

5. Visual Trade Representation:

- The script draws lines for entry, stop loss, and target levels on the chart, offering a clear visual representation of each trade.

- This feature helps traders easily track and manage active trades directly from the chart.

6. Enhanced User Control:

- Users can toggle specific features such as stop loss/target display and Spark alerts, allowing for a customizable trading experience.

By combining these elements, SparkPlus offers a robust and versatile tool for traders, enhancing their ability to make informed decisions and manage trades effectively.

BE-NSE-Distributed Straddle Intraday Trading StrategyHerewith publishing the script (not the Indicator!) for the benift of Option Traders. I call this a script as this doesn't perform any kind of analysis of candle data and provide general BUY | SELL information. This Script is based on the TRUE VALUES concept which is nothing but LTP.

Idea Behind this Script:

As an option seller i need the lower risk option premium to trade. so that, time can work in our favor. basic question which we get at the first is which option to choose out of many available.

If traders feel the question is apt then this script is for them.

Logic Behind this script:

Upon Market Open, script in the BACKEND ( Under the hood ) deployes 60 possible combinations of STRADDLES for sampling, and continue to monitor the LTP movements and compares it against opposite pairs. lets say out of 30 Straddle options one of the Straddle it picked is ATM CE VS ATM PE. for 1 rs move in underlying how much impact is happening in CE VS PE.

This simple anlysis is done at every 30 seconds. once the Analysis is complete it picks 4 options 2 on the CALL side and 2 on the PUT side, which script feels the movement of prices are smooth. SMOOTH refers that time decay that can work in our favor..

Calculations behid the script:

lets say BNF LTP is 52000 at 9:20 AM, and one of the pair script took for sampling was ATM CE vs PE which are having the LTP of 100 each.

At 9:35 AM, BNF is trading at 52075, and ATM CE is reading the LTP of 122 and ATM PUT is reading the LTP of 70. ideally LTP of Call should be around 135 and Put should be around 65 considering the usual delta of 0.48 . Net Money Index for this Pair Sample is 8

Call Side => 100 - 122 = -22

Put Side => 100 - 70 = 30

Money Index => 30 - 22 = 8 for 15 Min

This Money index is calculated across choosen samples and the Option strikes is provided as an output which has mere possiblity of working in Options Seller's favor.

How to Read the Output:

For the choosen strikes from the time of Entry (Suggested Entry time by script) till the current time, the bottom pane plots the Money index as columns. Green Columns indicate that how much option premium eroded due to time decay. Red Columns indicate that how much Option premium increased during the time.

Note: Script dynamically calculate the strikes and suggests in realtime.

WARNING or a Humble Request:

For those who don't understand the word "Repaint" how it works in Pine Script. plz don't consider using this script. For those who wish to understand I have kept the Observer mode in the settings which shall guide you on why the Money Index shown on the chart when the MARKET IS CLOSED is different than when the MARKET IS OPEN (Realtime).

Disclaimer:

I have tested the script only in BNF and not sure if this works on Nifty, FinNifty or others. you may still try and plz do provide the feedback for improvising the script.

----- BreathEasy --------

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

Tradingnomy Options Dashboard

**Tradingnomy Options Dashboard**

The "Tradingnomy Options Dashboard" is a sophisticated indicator developed, tailored for traders focusing on options trading in the Indian market. This powerful tool offers a comprehensive analysis of options premiums across various indices, enhancing decision-making capabilities.

**Key Features and Functionality:**

1. **Data Source Selection**: Users can select the data source (defaulting to the closing price) for precise calculations, ensuring accurate analysis.

2. **Index Selection**: Choose from prominent Indian indices including NIFTY, BANKNIFTY, MIDCPNIFTY, FINNIFTY, SENSEX, and BANKEX. Each selection dynamically maps to its corresponding spot symbol for data retrieval.

3. **Strike Prices and Expiry Date Customization**: Customize strike prices (`strike_ce` for calls and `strike_pe` for puts) and set the expiration date (day, month, year) of the options contracts. This flexibility allows traders to simulate various trading scenarios.

4. **Symbol Construction**: The script constructs unique symbols (`symbol_CE` for call options and `symbol_PE` for put options) based on the chosen index, expiry date, and strike prices. This automated process simplifies data fetching and analysis.

5. **Real-Time Data Retrieval**: Utilizing TradingView's `request.security` function, the script fetches real-time closing prices for the constructed option symbols (`symbol_CE` and `symbol_PE`), ensuring up-to-date market information.

6. **Straddle and Premium Calculation**: The indicator calculates the straddle value by combining the closing prices of both call and put options (`straddle_close`). Additionally, it separately plots the call premium (`Call_Premium`) and put premium (`Put_Premium`) for visual clarity.

7. **User-Driven Visualization**: Users can easily toggle visibility settings to display or hide the straddle, call premiums, and put premiums based on their analytical needs. This feature-rich customization enhances usability and focus on relevant trading insights.

**Usage and Originality:**

- **Educational Tool**: Designed primarily for educational purposes, the "Tradingnomy Options Dashboard" helps traders understand options pricing dynamics and formulate informed trading strategies.

- **Original Script**: Developed exclusively by tradingnomy_algo, this script adheres to the Mozilla Public License 2.0, ensuring transparency and respect for intellectual property rights. It stands out as an original contribution to the TradingView community, offering unique insights into the Indian options market.

This has been possible due to the Newly Added Options Data provided by Tradingview for Indian Markets

**How to Use:**

1. **Select Index**: Choose your preferred index (e.g., NIFTY, BANKNIFTY) from the dropdown menu.

2. **Set Parameters**: Customize strike prices (`strike_ce` and `strike_pe`) and choose the expiration date (`_day`, `_month`, `_year`) using intuitive input controls.

3. **Visualize Data**: Toggle the visibility of straddle/strangle values, call premiums, and put premiums to focus on specific metrics relevant to your trading strategy.

4. **Interpret Results**: Analyze the plotted data to understand options premiums trends and make informed trading decisions based on current market conditions.

**Disclaimer**: While this indicator provides valuable insights, it is important to conduct thorough research and consider multiple factors before making trading decisions. The "Tradingnomy Options Dashboard" is a tool for educational purposes and does not constitute financial advice.

Options Overlay [Pro] IVR IV Skew Delta Exp.mv MurreyMath Expiry

𝗧𝗵𝗲 𝗳𝗶𝗿𝘀𝘁 𝗿𝗲𝗮𝗹 𝗼𝗽𝘁𝗶𝗼𝗻𝘀 𝗱𝗮𝘁𝗮 𝗶𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿 𝗼𝗻 𝗧𝗿𝗮𝗱𝗶𝗻𝗴𝗩𝗶𝗲𝘄, 𝗮𝘃𝗮𝗶𝗹𝗮𝗯𝗹𝗲 𝗳𝗼𝗿 𝗼𝘃𝗲𝗿 𝟭𝟱𝟬+ 𝗹𝗶𝗾𝘂𝗶𝗱 𝗨𝗦 𝗺𝗮𝗿𝗸𝗲𝘁 𝘀𝘆𝗺𝗯𝗼𝗹𝘀.

🔃 Auto-Updating Option Metrics without refresh!

🍒 Developed and maintained by option traders for option traders.

📈 Specifically designed for TradingView users who trade options.

Our indicator provides essential key metrics such as:

✅ IVRank

✅ IVx

✅ 5-Day IVx Change

✅ Delta curves and interpolated distances

✅ Expected move curve

✅ Standard deviation (STD1) curve

✅ Vertical Pricing Skew

✅ Horizontal IVx Skew

✅ Delta Skew

like TastyTrade, TOS, IBKR etc, but in a much more visually intuitive way. See detailed descriptions below.

If this isn't enough, we also include a unique grid system designed specifically for options traders. This package features our innovative dynamic grid system:

✅ Enhanced Murrey Math levels (horizontal scale)

✅ Options expirations (vertical scale)

Designed to help you assess market conditions and make well-informed trading decisions, this tool is an essential addition for every serious options trader!

Ticker Information:

This indicator is currently implemented for more than 150 liquid US market tickers and we are continuously expanding the list:

SP:SPX AMEX:SPY NASDAQ:QQQ NASDAQ:TLT AMEX:GLD

NYSE:AA NASDAQ:AAL NASDAQ:AAPL NYSE:ABBV NASDAQ:ABNB NASDAQ:AMD NASDAQ:AMZN AMEX:ARKK NASDAQ:AVGO NYSE:AXP NYSE:BA NYSE:BABA NYSE:BAC NASDAQ:BIDU AMEX:BITO NYSE:BMY NYSE:BP NASDAQ:BYND NYSE:C NYSE:CAT NYSE:CCJ NYSE:CCL NASDAQ:COIN NYSE:COP NASDAQ:COST NYSE:CRM NASDAQ:CRWD NASDAQ:CSCO NYSE:CVNA NYSE:CVS NYSE:CVX NYSE:DAL NASDAQ:DBX AMEX:DIA NYSE:DIS NASDAQ:DKNG NASDAQ:EBAY NASDAQ:ETSY NASDAQ:EXPE NYSE:F NYSE:FCX NYSE:FDX AMEX:FXI AMEX:GDX AMEX:GDXJ NYSE:GE NYSE:GM NYSE:GME NYSE:GOLD NASDAQ:GOOG NASDAQ:GOOGL NYSE:GPS NYSE:GS NASDAQ:HOOD NYSE:IBM NASDAQ:IEF NASDAQ:INTC AMEX:IWM NASDAQ:JD NYSE:JNJ NYSE:JPM NYSE:JWN NYSE:KO NYSE:LLY NYSE:LOW NYSE:LVS NYSE:MA NASDAQ:MARA NYSE:MCD NYSE:MET NASDAQ:META NYSE:MGM NYSE:MMM NYSE:MPC NYSE:MRK NASDAQ:MRNA NYSE:MRO NASDAQ:MRVL NYSE:MS NASDAQ:MSFT AMEX:MSOS NYSE:NCLH NASDAQ:NDX NYSE:NET NASDAQ:NFLX NYSE:NIO NYSE:NKE NASDAQ:NVDA NASDAQ:ON NYSE:ORCL NYSE:OXY NASDAQ:PEP NYSE:PFE NYSE:PINS NYSE:PLTR NASDAQ:PTON NASDAQ:PYPL NASDAQ:QCOM NYSE:RBLX NYSE:RCL NASDAQ:RIOT NASDAQ:RIVN NASDAQ:ROKU NASDAQ:SBUX NYSE:SHOP AMEX:SLV NASDAQ:SMCI NASDAQ:SMH NYSE:SNAP NYSE:SQ NYSE:T NYSE:TGT NASDAQ:TQQQ NASDAQ:TSLA NYSE:TSM NASDAQ:TTD NASDAQ:TXN NYSE:U NASDAQ:UAL NYSE:UBER AMEX:UNG NYSE:UPS NASDAQ:UPST AMEX:USO NYSE:V AMEX:VXX NYSE:VZ NASDAQ:WBA NYSE:WFC NYSE:WMT NASDAQ:WYNN NYSE:X AMEX:XHB AMEX:XLE AMEX:XLF AMEX:XLI AMEX:XLK AMEX:XLP AMEX:XLU AMEX:XLV AMEX:XLY NYSE:XOM NYSE:XPEV CBOE:XSP NASDAQ:ZM

How does the indicator work and why is it unique?

This Pine Script indicator is a complex tool designed to provide various option metrics and visualization tools for options market traders. The indicator extracts raw options data from an external data provider (ORATS), processes and refines the delayed data package using pineseed, and sends it to TradingView, visualizing the data using specific formulas (see detailed below) or interpolated values (e.g., delta distances). This method of incorporating options data into a visualization framework is unique and entirely innovative on TradingView.

The indicator aims to offer a comprehensive view of the current state of options for the implemented instruments, including implied volatility (IV), IV rank (IVR), options skew, and expected market movements, which are objectively measured as detailed below.

The options metrics we display may be familiar to options traders from various major brokerage platforms such as TastyTrade, IBKR, TOS, Tradier, TD Ameritrade, Schwab, etc.

🟨 𝗗𝗘𝗧𝗔𝗜𝗟𝗘𝗗 𝗗𝗢𝗖𝗨𝗠𝗘𝗡𝗧𝗔𝗧𝗜𝗢𝗡 🟨

🔶 Auto-Updating Option Metrics and Curved Lines

🔹 Interpolated DELTA Curves (16,20,25,30,40)

In our indicator, the curve layer settings allow you to choose the delta value for displaying the delta curve: 16, 20, 25, 30, or even 40. The color of the curve can be customized, and you can also hide the delta curve by selecting the "-" option.

It's important to mention that we display interpolated deltas from the actual option chain of the underlying asset using the Black-Scholes model. This ensures that the 16 delta truly reflects the theoretical, but accurate, 16 delta distance. (For example, deltas shown by brokerages for individual strikes are rounded; a 0.16 delta might actually be 0.1625.)

🔹 Expected Move Curve (Exp.mv)

The expected move is the predicted dollar change in the underlying stock's price by a given option's expiration date, with 68% certainty. It is calculated using the expiration's pricing and implied volatility levels. We chose the TastyTrade method for calculating expected move, as we found it to be the most expressive.

Expected Move Calculation

Expected Move = (ATM straddle price x 0.6) + (1st OTM strangle price x 0.3) + (2nd OTM strangle price x 0.1)

For example , if stock XYZ is trading at 121 and the ATM straddle is 4.40, the 120/122 strangle is 3.46, and the 119/123 strangle is 2.66, the expected move is calculated as follows: 4.40 x 0.60 = 2.64; 3.46 x 0.30 = 1.04; 2.66 x 0.10 = 0.27; Expected move = 2.64 + 1.04 + 0.27 = ±3.9

In this example below, the TastyTrade platform indicates the expected move on the option chain with a brown color, and the exact value is displayed behind the ± symbol for each expiration. By default, we also use brown for this indication, but this can be changed or the curve display can be turned off.

🔹 Standard Deviation Curve (1 STD)

One standard deviation of a stock encompasses approximately 68.2% of outcomes in a distribution of occurrences based on current implied volatility.

We use the expected move formula to calculate the one standard deviation range of a stock. This calculation is based on the days-to-expiration (DTE) of our option contract, the stock price, and the implied volatility of a stock:

Calculation:

Standard Deviation = Closing Price * Implied Volatility * sqrt(Days to Expiration / 365)

According to options literature, there is a 68% probability that the underlying asset will fall within this one standard deviation range at expiration.

If the 1 STD and Exp.mv displays are both enabled, the indicator fills the area between them with a light gray color. This is because both represent probability distributions that appear as a "bell curve" when graphed, making it visually appealing.

Tip and Note:

The 1 STD line might appear jagged at times , which does not indicate a problem with the indicator. This is normal immediately after market open (e.g., during the first data refresh of the day) or if the expirations are illiquid (e.g., weekly expirations). The 1 STD value is calculated based on the aggregated IVx for the expirations, and the aggregated IVx value for weekly expirations updates less frequently due to lower trading volume. In such cases, we recommend enabling the "Only Monthly Expirations" option to smooth out the bell curve.

∑ Quant Observation:

The values of the expected move and the 1st standard deviation (1STD) will not match because they use different calculation methods, even though both are referred to as representing 68% of the underlying asset's movement in options literature. The expected move is based on direct market pricing of ATM options. The 1STD, on the other hand, uses the averaged implied volatility (IVX) for the given expiration to determine its value. Based on our experience, it is better to consider the area between the expected move and the 1STD as the true representation of the original 68% rule.

🔶 IVR Dashboard Panel Rows

🔹 IVR (IV Rank)

The Implied Volatility Rank (IVR) indicator helps options traders assess the current level of implied volatility (IV) in comparison to the past 52 weeks. IVR is a useful metric to determine whether options are relatively cheap or expensive. This can guide traders on whether to buy or sell options. We calculate IVrank, like TastyTrade does.

IVR Calculation:

IV Rank = (current IV - 52 week IV low) / (52 week IV high - 52 week IV low)

IVR Levels and Interpretations:

IVR 0-10 (Green): Very low implied volatility rank. Options might be "cheap," potentially a good time to buy options.

IVR 10-35 (White): Normal implied volatility rank. Options pricing is relatively standard.

IVR 35-50 (Orange): Almost high implied volatility rank.

IVR 50-75 (Red): Definitely high implied volatility rank. Options might be "expensive," potentially a good time to sell options for higher premiums.

IVR above 75 (Highlighted Red): Ultra high implied volatility rank. Indicates very high levels, suggesting a favorable time for selling options.

The panel refreshes automatically if the symbol is implemented. You can hide the panel or change the position and size.

🔹IVx (Implied Volatility Index)

The Implied Volatility Index (IVx) displayed in the option chain is calculated similarly to the VIX. The Cboe uses standard and weekly SPX options to measure the expected volatility of the S&P 500. A similar method is utilized to calculate IVx for each option expiration cycle.

For our purposes on the IVR Panel, we aggregate the IVx values specifically for the 35-70 day monthly expiration cycle . This aggregated value is then presented in the screener and info panel, providing a clear and concise measure of implied volatility over this period.

IVx Color coding:

IVx above 30 is displayed in orange.

IVx above 60 is displayed in red

IVx on curve:

The IVx values for each expiration can be viewed by hovering the mouse over the colored tooltip labels above the Curve.

IVx avg on IVR panel :

If the option is checked in the IVR panel settings, the IVR panel will display the average IVx values up to the optimal expiration.

Important Note:

The IVx value alone does not provide sufficient context. There are stocks that inherently exhibit high IVx values. Therefore, it is crucial to consider IVx in conjunction with the Implied Volatility Rank (IVR), which measures the IVx relative to its own historical values. This combined view helps in accurately assessing the significance of the IVx in relation to the specific stock's typical volatility behavior.

This indicator offers traders a comprehensive view of implied volatility, assisting them in making informed decisions by highlighting both the absolute and relative volatility measures.

🔹IVx 5 days change %

We are displaying the five-day change of the IV Index (IVx value). The IV Index 5-Day Change column provides quick insight into recent expansions or decreases in implied volatility over the last five trading days.

Traders who expect the value of options to decrease might view a decrease in IVX as a positive signal. Strategies such as Strangle and Ratio Spread can benefit from this decrease.

On the other hand, traders anticipating further increases in IVX will focus on the rising IVX values. Strategies like Calendar Spread or Diagonal Spread can take advantage of increasing implied volatility.

This indicator helps traders quickly assess changes in implied volatility, enabling them to make informed decisions based on their trading strategies and market expectations.

🔹 Vertical Pricing Skew

At TanukiTrade, Vertical Pricing Skew refers to the difference in pricing between put and call options with the same expiration date at the same distance (at expected move). We analyze this skew to understand market sentiment. This is the same formula used by TastyTrade for calculations.

We calculate the interpolated strike price based on the expected move , taking into account the neighboring option prices and their distances. This allows us to accurately determine whether the CALL or PUT options are more expensive.

PUT Skew (red): Put options are more expensive than call options, indicating the market expects a downward move (▽). If put options are more expensive by more than 20% at the same expected move distance, we color it lighter red.

CALL Skew (green): Call options are more expensive than put options, indicating the market expects an upward move (△). If call options are priced more than 30% higher at the examined expiration, we color it lighter green.

Vertical Skew on Curve:

The degree of vertical pricing skew for each expiration can be viewed by hovering over the points above the curve. Hover with mouse for more information.

Vertical Skew on IVR panel:

We focus on options with 35-70 days to expiration (DTE) for optimal analysis in case of vertical skew. Hover with mouse for more information.

This approach helps us gauge market expectations accurately, providing insights into potential price movements. Remember, we always evaluate the skew at the expected move using linear interpolation to determine the theoretical pricing of options.

🔹 Delta Skew 🌪️ (Twist)

We have a new metric that examines which monthly expiration indicates a "Delta Skew Twist" where the 16 delta deviates from the monthly STD. This is important because, under normal circumstances, the 16 delta is positioned between the expected move and the standard deviation (STD1) line (see Exp.mv & 1STD exact definitions above). However, if the interpolated 16 delta line exceeds the STD1 line either upwards or downwards, it represents a special case of vertical skew on the option chain.

Normal case : exp.move < delta16 < std1

Delta Skew Twist: exp.move < std1 < delta16

We indicate this with direction-specific colors (red/green) on the delta line. We also color the section of the delta curve affected by the delta skew in this case, even if you choose to display a lower delta, such as 30, instead of 16.

If "Colored Labels with Tooltips" is enabled, we also display a 🌪️ symbol in the tooltip for the expirations affected by Delta Skew.

If you have enabled the display of 'Vertical Pricing Skew' on the IVR Panel, a 🌪️ symbol will also appear next to the value of the vertical skew, and the tooltip will indicate from which expiration Delta Skew is observed.

🔹 Horizontal IVx Skew

In options pricing, it is typically expected that the implied volatility (IVx) increases for options with later expiration dates. This means that options further out in time are generally more expensive. At TanukiTrade, we refer to the phenomenon where this expectation is reversed—when the IVx decreases between two consecutive expirations—as Horizontal Skew or IVx Skew.

Horizontal IVx Skew occurs when: Front Expiry IVx < Back Expiry IVx

This scenario can create opportunities for traders who prefer diagonal or calendar strategies . Based on our experience, we categorize Horizontal Skew into two types:

Weekly Horizontal Skew:

When IVx skew is observed between two consecutive non-monthly expirations, the displayed value is the rounded-up percentage difference. On hover, the approximate location of this skew is also displayed. The precise location can be seen on this indicator.

Monthly Horizontal Skew: