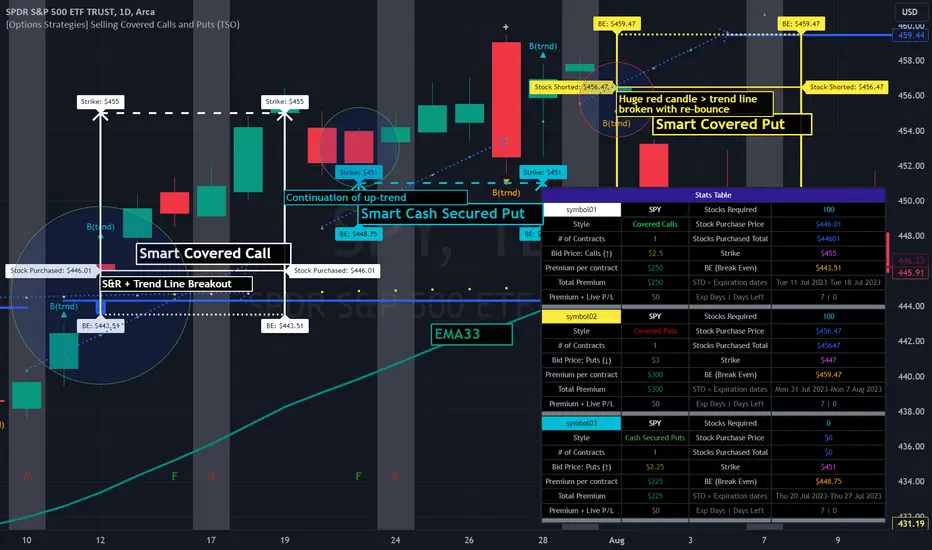

[Options Strategies] Selling Covered Calls and Puts (TSO) This trading indicator assists with traditional covered options trading strategies like Covered Calls, Covered Puts, and Cash Secured Puts. It also offers advanced features for trading options intelligently by utilizing options specific levels, such as BE (Break Even) and Strike (all visually shown on chart) in combination with S&R (Support and Resistance), Trend Lines, and other technical analysis tools such as MA (Moving Averages) and ATR Average True Range, all integrated within the indicator.

* Covered options approach over trading shares or options separately offers distinct advantages:

- Reduced Risk and Flexibility : Covered options strategy provides a more conservative approach by combining stock ownership with options trading. It reduces risk exposure compared to buying options outright or trading shares alone. Additionally, it offers flexibility in various market conditions.

- Profitability in Sideways Markets: Covered options allow for profitability in scenarios where the stock price is either moving optimally or remaining sideways. In contrast, just holding stocks might not yield significant gains in a sideways market, and buying options can result in losses due to time decay.

- Protection Against Price Movements: In covered options, if the stock price goes against the trade, the loss is mitigated by the premium received from selling the options. This provides a level of protection compared to other trading strategies where losses can accumulate more rapidly.

==============================================================

Strategies / Visual Examples:

---------------------------------------------------------------------------

---------------------------------------------------------------------------

Up to 3 Symbols can be monitored at the same time with alerts for each Symbol and a Stats Table. To see Symbol's visuals (Date Range, Strike, BE, etc.) - the chart has to be loaded with that Symbol. Here is an example of trading multiple stocks at same layout on different charts trading AAPL, BAC and TSLA.

---------------------------------------------------------------------------

---------------------------------------------------------------------------

An example of a Smart Covered Calls trading SPY.

STRATEGY EXPLANATION:

* Trade Open Trigger (Bullish/Sideway)

>>> S&R (Support and Resistance) or Trend Line broken, bounced off or simply near (if price is near/slightly crossing S&R/Trend Line > a bounce often takes place)

>>> Confirmation by additional TA (Technical Analysis) tools.

>>> EXAMPLE: Broken Resistance combined with a Trend Line up-bounce, confirmed by bullish 200EMA.

* TP (Take-Profit)

>>> Contracts Expire at Expiration date: Premium received for selling contracts kept.

>>> Assignment: Premium received for selling contracts kept + stock assigned/sold at a higher price than it was purchased.

* BE/SL (Break Even Stop-Loss) |

>>> BE/SL hit: stock sold at a slight loss with options contracts bought out (BTC - Buy to Close) at a lower price than initially sold (since price went down and these are calls), so technically the loss is reduced by the partial Premium still kept from initially sold contracts at trade open.

>>> Increasing the BE/SL distance: for wider BE/SL > Bid Price needs to be increased:

- Set longer Expiration date.

- Set closer Strike price.

NOTE: With longer Expiration date and closer Strike, chances of assignment increase as well. It's best to find an optimal level, where BE/SL is behind a Support/Resistance level and/or an established trend line and/or Large Length Moving Average, yet not extremely far away.

---------------------------------------------------------------------------

---------------------------------------------------------------------------

An example of a Smart Covered Puts trading SPY.

STRATEGY EXPLANATION:

* Trade Open Trigger (Bearish/Sideway)

>>> S&R (Support and Resistance) or Trend Line broken, bounced off or simply near (if price is near/slightly crossing S&R/Trend Line > a bounce often takes place)

>>> Confirmation by additional TA (Technical Analysis) tools.

>>> EXAMPLE: Broken Resistance combined with a Trend Line down-bounce, confirmed by bearish 200EMA.

* TP (Take-Profit)

>>> Contracts Expire at Expiration date: Premium received for selling contracts kept.

>>> Assignment: Premium received for selling contracts kept + stock assigned/bought-to-cover at a lower price than it was shorted.

* BE/SL (Break Even Stop-Loss) |

>>> BE/SL hit: stock bought-to-cover at a slight loss with options contracts bought out (BTC - Buy to Close) at a lower price than initially sold (since price went up and these are puts), so technically the loss is reduced by the partial Premium still kept from initially sold contracts at trade open.

>>> Increasing the BE/SL distance: for wider BE/SL > Bid Price needs to be increased:

- Set longer Expiration date.

- Set closer Strike price.

NOTE: With longer Expiration date and closer Strike, chances of assignment increase as well. It's best to find an optimal level, where BE/SL is behind a Support/Resistance level and/or an established trend line and/or Large Length Moving Average, yet not extremely far away.

---------------------------------------------------------------------------

---------------------------------------------------------------------------

An example of a Smart Secured Cash Puts trading SPY.

STRATEGY EXPLANATION:

* Trade Open Trigger (Bullish/Sideway)

>>> Bullish steady trend.

>>> Confirmation by additional TA (Technical Analysis) tools.

>>> EXAMPLE: Slowly rising price action above 200EMA.

* TP (Take-Profit)

>>> Early BTC: BTC (Buy to Close) before Expiration date if options premium/contract price already reduced by at least 50-90% (the reduced price is the profit, if premium lost 90% - only 10% will need to be paid to buy options out to close the trade) and if the stock price is nearing Resistance, Trend Line or big length moving average (like 200EMA) as a bounce may happen or even a potential reverse of the trend. If there is no trend reversal or a small correction bounce occurs, with further trend continuation > another Cash Secured Puts trade can be opened with new Expiration date and Strike.

>>> Contracts Expire at Expiration date: Premium received for selling contracts kept, considering the Strike was never hit.

>>> Assignment with stock closing below Strike and above/near BE (Break Even): Premium received for selling contracts kept. NOTE: It is best to get rid of the stock ASAP to then open a new Cash Secured Puts trade with lower Strike and a new Expiration date.

* BE/SL (Break Even Stop-Loss) |

>>> BE/SL hit: contracts bought out (BTC - Buy to Close) at a higher price than initially sold (since price went down and these are puts), the amount/difference in current contract price is the loss (as premium received + contract price increase is the total cost, which will have to be paid to buy the countracts out).

>>> Increasing the BE/SL distance: for wider BE/SL > Bid Price needs to be increased:

- Set longer Expiration date.

- Set closer Strike price.

NOTE: With longer Expiration date and closer Strike, chances of assignment increase as well. It's best to find an optimal level, where BE/SL is behind a Support/Resistance level and/or an established trend line and/or Large Length Moving Average, yet not extremely far away.

---------------------------------------------------------------------------

---------------------------------------------------------------------------

An example of Options Wheel strategy trading TQQQ. See how Strike and BE (Break Even) hits are displayed every time they occur.

STRATEGY EXPLANATION:

* Trade Open Trigger (Bullish/Sideway)

>>> Options Wheel strategy combines Cash Secured Puts with Covered Calls, so a steady bullish trend is preferred with lower volatility.

>>> It's best to start with Cash Secured Puts until assignment hits (stocks purchased), then switch to Covered Calls until assignment hits (stocks sold) and so on.

* TP (Take-Profit)

>>> Contracts Expire at Expiration date: Premium received for selling contracts kept.

>>> Assignment: Premium received for selling contracts kept. Stock is assigned (purchased if Cash Secured Puts were sold | sold if Covered Calls were sold ).

* BE/SL (Break Even Stop-Loss)

>>> Assignment is the stop-loss for this strategy, which ends current trade and starts next one. It is not a direct loss, but could result a long unrealized losses if after stock purchase assignment it goes down for a while or even a complete loss if low-cap company is used and it goes out of business.

>>> BE/SL distance can still be increased/kept optimal: for wider BE/SL > Bid Price needs to be increased:

- Set longer Expiration date.

- Set closer Strike price.

NOTE: With longer Expiration date and closer Strike, chances of assignment increase as well. It's best to find an optimal level, where BE/SL is behind a Support/Resistance level and/or an established Trend Line and/or Large Length Moving Average, yet not extremely far away.

| 3.0_wheel_strategy_tqqq_example.png

===========================================================================

Trading open/close/TP/SL labels, plots and colors explanations:

---------------------------------------------------------------------------

There are 3 approaches: Cashed Secured Puts, Covered Puts, Covered Calls. Here is an example showing all 3 (the Strikes, Bid prices, Expirations were chosen realistically).

>>> There are 3 symbol templates, the color can be changed for each and each symbol template can be unchecked to be fully hidden or all 3 can be used.

>>> Strike: dashed horizontal line plotted at chosen Strike, if Strike is hit within the Date Range - there will be a label shown.

>>> BE (Break Even): dotted horizontal line plotted at calculated BE, if BE is hit within the Date Range - there will be a label shown.

>>> Stock Purchased: solid horizontal line plotted at input price at which the stock was purchased.

>>> Date Range (STO >>> Expiration ): vertical lines with arrows (arrows direction is based on the approach), which connect Strike, BE (Break Even) and Stock Purchased creating an square/rectangle of the whole trade, making it easy to see everything at once.

>>> Stats Table: shows all the necessary data for each symbol.

===========================================================================

GLOBAL SETTINGS ///////////////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Show: week divider vertical lines: Will show vertical divider lines separating each week.

>>> Show: Mondays and Fridays: Will show M - for Monday, F - for Friday, T - for Tuesday (Tuesday will be shown if there is a Holiday on Monday)

---------------------------------------------------------------------------

OPTIONS SETUP: SYMBOL0X /////////////////////////////////////////////////// | (identical for all 3 symbols)

---------------------------------------------------------------------------

>>> Symbol0X | Show Table: Turns on symbol01, all visuals on chart, calculations, etc. Table can be separately hidden if desired.

>>> Label Size: Size of the labels on chart showing Strike, BE (Break Even), etc.

>>> Label Color: Color for all symbol0X labels.

>>> Text Color: Text color for all symbol0X labels.

>>> Options Trading Style: 1)Covered Calls: Bullish-sideways market approach (need to own 100 shares of stock per each contract sold), Strike price has to be set above the current stock price | 2)Covered Puts: Bearish-sideways market approach (need to own 100 shares of stock per each contract sold), Strike price has to be set below the current stock price | 3)Cash Secured Puts: Bullish-sideways approach (need to have enough cash to acquire shares at Strike price if hit), Strike price has to be set below the current stock price.

>>> # of contracts sold (1 contract > 100shares): # of contracts sold per trade, for Covered Calls and Covered Puts, every contract must be backed up by 100shares of the underlying stock.

>>> Price per 1 contract (Bid): Premium received per each contract sold.

>>> Strike Price.

>>> Stock Purchase Price: Stock purchase price (NOTE: This is only for Covered Call and Covered Puts, for Secured Cash Puts - stock is only purchased if at Expiration it closes beyond Strike price).

>>> STO (Sell to Open) Date: date at which the contracts were sold and Premium received.

>>> Exp (Expiration) Date: date at which contracts expire, if price never breaks the Strike at Expiration - contracts become worthless!

>>> Alert/Label: Futures Expire Soon: With this setting turned on, an Alert will trigger and a Label will be shown at opening of the first candle bar on the Expiration date. It will certainly be before the end of the day, however depending on the chart TimeFrame during alert creation - it may trigger at a different time. For Example: On a Daily chart TimeFrame SPY (S&P500) will trigger such alert at 9:30AM ET. ||| NOTE: Due to difference in timezones - the solid lines representing the STO >>> Exp range may be off by 1 business day from the date input in the indicator Settings > Inputs, so double check and calibrate the date by setting it 1 day behind/ahead from actual dates so that Alert is received on the actual Expiration date.

>>> Strike price Broken - Style: 'Close': Show/Alert Strike price broken only once candle bar is closed | 'Live': Show/Alert Strike price broken immediately once it happens, before candle bar is closed.

>>> Show: Strike price Broken: will show a label near candle bar breaking the Strike price.

>>> Alert: Strike price Broken: will alert at price breaking the Strike price.

>>> BE (Break Even) price Broken - Alert Style: 'Close': Show/Alert BE (Break Even) price broken only once candle bar is closed | 'Live': Show/Alert BE (Break Even) price broken immediately once it happens, before candle bar is closed.

>>> Show: BE (Break Even) price Broken: will show a label near candle bar breaking the BE price.

>>> Alert: BE (Break Even) price Broken: will alert at price breaking the BE price.

---------------------------------------------------------------------------

TA: TREND LINES ///////////////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Trend Lines - Uptrend/downtrend colors

>>> Show: Trend Lines: Show/Hide trend lines

>>> Show: Trend Line Breaks: Show/Hide labels where trend lines were broken

>>> Alert: Trend Line Breaks: Alert when trend line is broken

>>> Trend Lines - Search - Left Bars / Trend Lines - Search - Right Bars: how many candle bars will be used to calculate Trend Lines, the bigger the number > the more precise and less amount of trend lines will be found

>>> Trend Lines - Extend Setting

---------------------------------------------------------------------------

TA: S&R (SUPPORT AND RESISTANCE) //////////////////////////////////////////

---------------------------------------------------------------------------

>>> S&R (Support and Resistance) - Support/Resistance colors.

>>> Show: S&R (Support and Resistance) Top/Bottom Levels.

>>> Show: S&R (Support and Resistance) Top/Bottom Level Breaks: Show/Hide labels where support/resistance levels were broken

>>> Alert: S&R (Support and Resistance) Top/Bottom Level Breaks: Alert when S&R (Support and Resistance) level is broken

>>> S&R (Support and Resistance) - Search - Left Bars / S&R (Support and Resistance) - Search - Right Bars: how many candle bars will be used to calculate S&R (Support & Resistance) Levels, the bigger the number > the more precise and less amount of support and resistance levels will be found.

>>> S&R Search - Custom Resolution: This is a custom timeframe setting specifically for S&R Search, it disregards current chart timeframe. This is great to use for scalping, for example: with main chart set to 1min and the custom timeframe set to 3min or 5min - there will be stronger support/resistance levels with more detailed price action.

---------------------------------------------------------------------------

TA: ADDITIONAL TOOLS //////////////////////////////////////////////////////

>>> Show - MA (Moving Average).

>>> Show - ATR (Average True Range).

---------------------------------------------------------------------------

---------------------------------------------------------------------------

STATS TABLE ///////////////////////////////////////////////////////////////

Stats Table displays all the necessary date about each options setup.

>>> Table positioning

---------------------------------------------------------------------------

===========================================================================

Adding Alerts in TradngView

---------------------------------------------------------------------------

-Add indicator to chart and make sure to check/uncheck which alerts are required, then simply create it.

-Right-click anywhere on the TradingView chart

-Click on Add alert

-Condition: Select this indicator by it’s name

-Immediately below, change it to "alert() function calls only"

-Expiration: Open-ended (that may require higher tier TradingView account, otherwise the alert will need to be occasionally re-triggered)

-Alert name: Whatever you desire

-Hit “Create”

-Note: If you change ANY Settings within the indicator – you must DELETE the current alert and create a new one per steps above, otherwise it will continue triggering alerts per old Settings!

===========================================================================

If you have any questions or issues with the indicator, please message me directly via TradingView.

---------------------------------------------------------------------------

Good Luck! (NOTE: Trading is very risky, past performance is not necessarily indicative of future results, so please trade responsibly!)

Options

BetaBeta , also known as the Beta coefficient, is a measure that compares the volatility of an individual underlying or portfolio to the volatility of the entire market, typically represented by a market index like the S&P 500 or an investible product such as the SPY ETF (SPDR S&P 500 ETF Trust). A Beta value provides insight into how an asset's returns are expected to respond to market swings.

Interpretation of Beta Values

Beta = 1: The asset's volatility is in line with the market. If the market rises or falls, the asset is expected to move correspondingly.

Beta > 1: The asset is more volatile than the market. If the market rises or falls, the asset's price is expected to rise or fall more significantly.

Beta < 1 but > 0: The asset is less volatile than the market. It still moves in the same direction as the market but with less magnitude.

Beta = 0: The asset's returns are not correlated with the market's returns.

Beta < 0: The asset moves in the opposite direction to the market.

Example

A beta of 1.20 relative to the S&P 500 Index or SPY implies that if the S&P's return increases by 1%, the portfolio is expected to increase by 12.0%.

A beta of -0.10 relative to the S&P 500 Index or SPY implies that if the S&P's return increases by 1%, the portfolio is expected to decrease by 0.1%. In practical terms, this implies that the portfolio is expected to be predominantly 'market neutral' .

Calculation & Default Values

The Beta of an asset is calculated by dividing the covariance of the asset's returns with the market's returns by the variance of the market's returns over a certain period (standard period: 1 years, 250 trading days). Hint: It's noteworthy to mention that Beta can also be derived through linear regression analysis, although this technique is not employed in this Beta Indicator.

Formula: Beta = Covariance(Asset Returns, Market Returns) / Variance(Market Returns)

Reference Market: Essentially any reference market index or product can be used. The default reference is the SPY (SPDR S&P 500 ETF Trust), primarily due to its investable nature and broad representation of the market. However, it's crucial to note that Beta can also be calculated by comparing specific underlyings, such as two different stocks or commodities, instead of comparing an asset to the broader market. This flexibility allows for a more tailored analysis of volatility and correlation, depending on the user's specific trading or investment focus.

Look-back Period: The standard look-back period is typically 1-5 years (250-1250 trading days), but this can be adjusted based on the user's preference and the specifics of the trading strategy. For robust estimations, use at least 250 trading days.

Option Delta: An optional feature in the Beta Indicator is the ability to select a specific Delta value if options are written on the underlying asset with Deltas less than 1, providing an estimation of the beta-weighted delta of the position. It involves multiplying the beta of the underlying asset by the delta of the option. This addition allows for a more precise assessment of the underlying asset's correspondence with the overall market in case you are an options trader. The default Delta value is set to 1, representing scenarios where no options on the underlying asset are being analyzed. This default setting aligns with analyzing the direct relationship between the asset itself and the market, without the layer of complexity introduced by options.

Calculation: Simple or Log Returns: In the calculation of Beta, users have the option to choose between using simple returns or log returns for both the asset and the market. The default setting is 'Simple Returns'.

Advantages of Using Beta

Risk Management: Beta provides a clear metric for understanding and managing the risk of a portfolio in relation to market movements.

Portfolio Diversification: By knowing the beta of various assets, investors can create a balanced portfolio that aligns with their risk tolerance and investment goals.

Performance Benchmarking: Beta allows investors to compare an asset's risk-adjusted performance against the market or other benchmarks.

Beta-Weighted Deltas for Options Traders

For options traders, understanding the beta-weighted delta is crucial. It involves multiplying the beta of the underlying asset by the delta of the option. This provides a more nuanced view of the option's risk relative to the overall market. However, it's important to note that the delta of an option is dynamic, changing with the asset's price, time to expiration, and other factors.

FalconRed 3 Candlestick LevelsThis Pine Script indicator is designed to enhance price action analysis by identifying specific candle patterns that signal potential buying and selling levels. The analysis is based on the characteristics of the current candle and its two immediate predecessors.

For identifying buying levels, the script examines the wicks of the candles, highlighting areas where buying and selling struggle is evident. The indicator recognizes significant breaks above wick levels, especially when followed by a subsequent candle with a lower wick. This combination suggests that previous selling pressure has been challenged and overcome.

Buy breakout and retest levels are highlighted with green color, providing a clear visual indication of potential buying opportunities. The indicator draws horizontal lines that extend to the right, offering insights into the frequency of retests and the recurrence of similar patterns in specific price zones, thereby confirming and reinforcing the observed price action.

Similarly, the indicator scrutinizes the selling side, pinpointing breakdown and retest levels. These areas are highlighted with red color, aiding in the identification of potential selling opportunities.

This indicator serves as a valuable tool for analyzing price action levels and visualizing buying and selling areas. It can be effectively combined with other technical indicators to enhance confidence in trading decisions. Gain deeper insights into market dynamics and improve decision-making by integrating this candle pattern analysis indicator into your trading strategy.

Open Interest by strikeOverview :

What is open interest (OI)? Is the total number of open derivative contracts, such as options, that have not been settled. These positions have been opened, but have not been closed out, expired, or exercised. This indicator helps with giving the open interest of selected equities on the market. It will give you the current weekly expiration date and has also the option to give the monthly expiration date (3rd Friday of the month).

How it works/Calculations :

This indicator will bring the data from an outside source and will have the closest options strikes to the current spot price of the underlying. The bars size will be equivalent to the amount of open interest. In the settings, you can see current weekly expiration options OI or have the option to see monthly expiration. When the weekly expiration is the monthly expiration week, then monthly expiration will show the next monthly expiration. (Example: On December 6, 2023 you will see weekly expiration of Dec 8, 2023 and monthly expiration will be Dec 15, 2023. On December 11, 2023 you will see weekly expiration of Dec 15, 2023 and monthly expiration will be Jan 19, 2024). You will also have the option to see the values or hide them. Also can see delta OI (for each strike subtract the calls and puts and display the remaining values). Open Interest updaters once a day, this indicator will update as well to give the most current values.

Current equities available for the data :

1. XLK 2. XLY 3. XLV 4. XLI 5. XLF 6. AAPL 7. MSFT 8. NVDA 9. AMD 10. V 11. Crm 12. Meta 13. Goog 14. NFLX 15. Amzn 16. Tsla 17. HD 18. Low 19. TGT 20. Wmt 21. XOM 22. Cvx 23. JPM 24. AXP 25. GS 26. ABBV 27. Cat 28. DE 29. BA 30. Fdx 31. UPS 32. Shop 33. SQ 34. Abnb 35. Snow 36. Coin 37. Crwd 38. Uber 39. SBUX 40. ENPH 41. XLP 42. XLE 43. XLB 44. NKE 45. UPS

How to use :

You should not be using this indicator for entries or stop. This indicator will help you see where there are possible levels that will serve as imaginary support and resistance.

Settings:

As above, you can choose weekly or monthly expiration date as explained above. Also you can choose to see the values or delta OI or no values.

Disclaimer:

This is still an indicator that in no way should be used alone.

The information contained in this script does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts are only for educational purposes!

Tips,Notes,RulesEasy Annotation:

Quickly create custom annotations during your trading sessions to capture important ideas, strategies and observations as you go.

User-friendly Interface:

The indicator offers an intuitive interface, ensuring a smooth experience for adding notes to your chart.

Custom Appearance:

Personalize your annotations according to your preferences.

Adjust the text size to make your notes easily readable and tailored to your visual preferences.

Choose from a variety of colors to make your annotations visually distinct and recognizable.

Align your text according to your preferences to create a visually appealing graphic.

Flexible Positioning:

Place your annotations at the top, middle, or bottom of the chart, providing flexibility without obstructing your view of the price action.

Clear View of Price Action:

Make sure your personalized notes don't interfere with your analysis of market movements.

Tracking Trading Rules:

Use the indicator to record your trading rules, ensuring that you follow your established strategies consistently.

Implement and follow your risk management plans, helping you maintain control over your transactions.

Capture and examine the psychological cues that influence your decisions, promoting greater discipline in your approach to trading.

Improved Trading Experience:

The Trading Notes indicator integrates seamlessly into your trading workflow, allowing you to focus on market analysis and decision-making.

Develop a complete record of your trading sessions, facilitating post-analysis and continuous improvement.

OmniSessions [WinWorld]The indicator shows the range of 4 most popular sessions (New York, Tokyo, London, Sydney). Sessions are used to identify zones with maximum volatility, as well as to find entry points. Session boundaries can act as POI no worse than OrderBlock.

In addition to sessions, you can use settings with KillZones - a range within a session that has potentially high volatility.

Silver Bullet is a more advanced range that allows you to identify the potential for maximum volatility. Excellent entry points can be obtained on the sweep of the range or from the nearest orderblock. We will explain it a bit deeply below.

Why use sessions?

During specific sessions big financial instutions from specific parts of the world enter the market, and this fact alone let us find the most "liquid" sessions in order to catch the best price movements. If talking about orderblocks, it is just a point of interest (more precisely, it is actually a zone of interest), which usually is a zone where the signficant amount of limit orders lies, and when price enter such zone, it immediately shows a strong reaction with either breakout from this zone or it bounces against this zone.

How is this indicator different from others?

There a lot of orderblocks indicator out here publicly available, but huge portion of them doesn't take into calculation important smart money concepts, such as valid pullbacks, for example. Valid pullbacks is a concept of price movement, which lets us indentify quite precisely price's impulses. Based on this impulses, we search our orderblocks. This approach allows to catch the most relevant and highly liquid orderblocks, which present traders with best trade entry opportunities, because usually, when entering with these orderblocks, you follow the moves of big money players, and that gives trader an edge in trading. None of open-source indicators uses such approach ( we've studied all of them ). Also an important notice: no public code is utilized in this indicato whatsoever. We've build our own flexible session mechanism, which allows you to quickly change between different type of sessions and also choose which session to use. And the big thing is our own alorithm to deal with asset, trading sessions of which are quite exotic (such as DAX and MEOX indexes, which close and open at different times of the day, which makes it hard for indicator to catch by default), so with indicator you can enjoy trading by sessions with no "bugs".

And the most user-desired and important thing: we've implemented feature to set winter and summer seasons for sessions, and this solves life-long struggle of traders to set correct trading session time, when forex exchanges switch trading hours, so now you don't need to info which our summer or winter is traded by, but just switch between seasons by one button in our indicator. And we can proudly state, no sesions indicator in the TradingView has such feature , so feel free to use it now on our indicator.

How orderblocks are built?

When London, New York or Asia ends, we find the closest orderblocks above and below closed session's high and low respectively. We do it by finding so called valid pullbacks ( was explained above ), then searching for valid fair value gap (FVG), that is inside of some valid pullbacks, and if we find it, then the orderblock is established and you will live orderblock and fair value gap (FVG) box ( both are colored in closed session's colour ).

How are orderblocks and FVG displayed on the chart?

Live orderblock and FVG are displayed as boxes on the chart, that are plolonged each bar if price didn't reach the orderblock.

Some important details:

When price touches FVG, FVG then is modified to reflect how much of untouched FVG is left. You will see it as decreasing of FVG box size in live mode. If price fully takes over FVG, FVG deletes;

When price touches orderblock, orderblock stops being prolonged and stays on the chart and is considered as worked-out.

These featues allow you to fully see live orderblocks and FVGs (if they exist) and already worked-out orderblocks to see how useful they were in the history.

Is that it?

No, because our indicator also shows sessions sweeps, which is historically a good indication that price grabbed the liquidity of previously closed sessions and now has enough "power" to do big movements, which is a good thing for traders, because it allows them to catch big movements and profit big.

Ok, we've covered the basics, now let's talk about what exactly this indicator can do.

OmnISessions is all-in-one sessions' indicator, that cointain:

Sessions (Automatic adaptation to your time zone)

Kill Zones

Silver Bullets

Session Sweeps

Order Blocks (Session, Killzone, SilverBullet)

Easily switch between summer and winter seasons

Now you don't need to look for opening and closing times of stock exchanges: the algorithm itself adjusts the session times according to your timezone. Just change the seasonality: winter/summer and the session times will be clearly displayed on your chart.

A quick view of the settings:

Show: Sessions, KillZones or SilverBullet

Season selection: Winter/Summer

Session Color Selection

Visuals:

Show/Hide session name - displays session name (ex.: London, New York, Silver Bullet and etc.) on the chart;

Show/Hide session box - displays session range as box with coloured background on the chart;

Show/Hide High/Low sessions - displays two horizontal lines for higher and lower borders of the session;

Show/Hide OrderBlocks - displays worked-out orderblocks in the history with live orderblocks and their fair value gaps (FVGs);

Show/Hide live Session High/Low - displays higher and lower border of the session as lines, that are prolonged each bar even after the session ends;

Show/Hide Session Sweeps - displays session sweeps of higher and lower border as dotted line;

Dividers (alternative session display):

Horizontal Divider

Backgrounder coloring

Customization: choose the display type: Sessions, Killzones or Silver Bullet.

The indicator displays orders that are above or below the previous session boundaries.

Below are Killzones with Order Blocks:

And this is Silver Bullet with Order Blocks:

Overall, you can clearly see that orderblocks, sessions sweeps and different type of sessions in one indicator allow you to fully utilize your time and mental energy, because finding orderblocks with valid pullbacks by hand is quite time-costly task, but finding them on different type of sessions, while not knowing trading hours of current trading session, is the true hell of work. OmniSessions indicator performs all of these calculations by itself, so you can focus on finding the best entries, while checking the situation on different sessions at the same time.

We hope that you will find great use of OmniSessions!

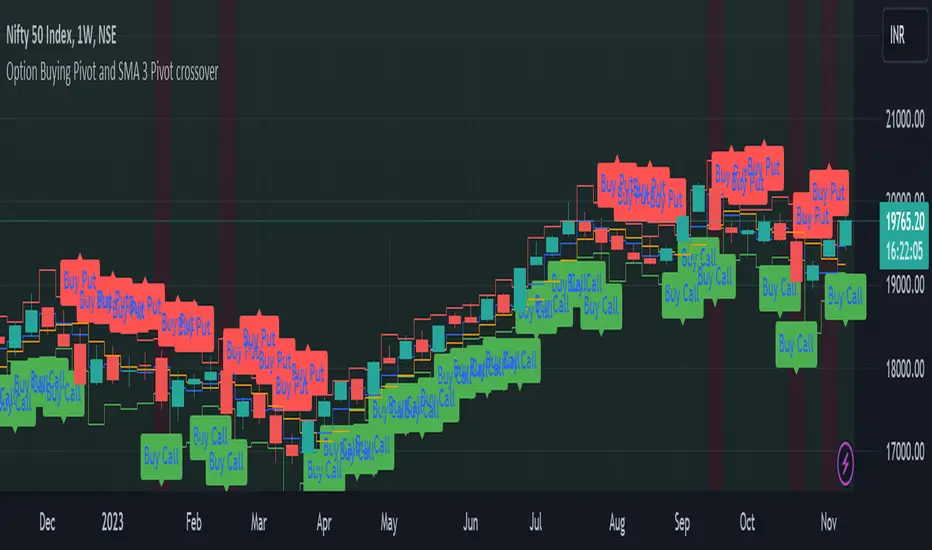

Option Buying Pivot and SMA 3 Pivot crossoverThis script is designed as a visual aid for options trading specifically for option buying, providing information about potential entry points, Option levels, and trade outcomes. Here's a summary of the key elements:

1. Pivot Point and True Range:*

- The script calculates the current candle's pivot point, representing an average of high, low, and close prices from the previous candle.

- True range, a measure of volatility, is determined using the high, low, and close prices of the last two candles.

2. Option Levels:

- Downside (PutValue - Red colour line) and upside (CallValue - Green Colour line) are calculated based on the current pivot point and true range.

PutValue = currentCandlePivot + currentCandleTrueRange

CallValue = currentCandlePivot - currentCandleTrueRange

3. Simple Moving Average (SMA) of Pivot Point:

- A 3-period SMA is applied to the pivot point to smooth out fluctuations.

4. Trade Entry Logic:

- Long entry is signalled when the current pivot point is above the SMA. (longEntry = currentCandlePivot > smaPivot)

- At the time of long entry BUY THE CALL OPTION OR SELL THE PUT OPTION near the CallValue Green line

- Short entry is signalled when the current pivot point is below the SMA. (shortEntry = currentCandlePivot < smaPivot)

- At the time of Short entry BUY THE PUT OPTION OR SELL THE CALL OPTION near the PutValue Red line

The indicator having option to change the background of the candle as a green for long; and change the background of the candle as red for short. Also, Having the option to plot as label.

5. Win and Loss Logic:

- Winning conditions are assessed based on the close price relative to CallValue (for Long) and PutValue (for Short).

- Losing conditions are determined similarly.

- winLong = close > CallValue and longEntry

- winShort = close < PutValue and shortEntry

-lossLong = close < CallValue and longEntry

-lossShort = close > PutValue and shortEntry

The indicator having option to change the background of the candle as a green for win; and change the background of the candle as red for loss. Also, Having the option to plot as label.

6. Background Coloring and Plots:

- The script uses background colors to highlight Long, Short, Win, and Loss scenarios.

- Shapes and labels are plotted on the chart to visually represent entry points, stop-loss levels, and trade outcomes.

The overall purpose is to provide traders with a clear visual representation of potential trading opportunities and outcomes, helping them make informed decisions in the options market.

User Defined Range Selector and Color Changing EMA LineThe "User Defined Range Selector and Color Changing EMA Line," stands out in the crowded field of trading indicators due to its unique blend of visual clarity and customizable functionality. Unlike traditional indicators, this tool not only tracks the Exponential Moving Average (EMA) but enhances it with a user-defined mirrored line to visually denote a range based on a percentage distance from the EMA.

Key Features:

- Dynamic Color-Changing EMA: The EMA line changes color based on its slope, providing instant visual cues about the market trend. Blue signifies an upward trend, red indicates a downward trend, and gray represents a sideways market.

- Customizable Range Selector: A mirrored EMA line is plotted, which can be set at a user-defined percentage away from the primary EMA. This feature allows traders to visualize a potential price range or channel, adding an extra layer of analysis for potential support and resistance zones.

- User-Driven Inputs: With inputs like EMA length, slope length, source, and the percentage distance for the mirrored line, the indicator offers a high level of customization, catering to various trading styles and strategies.

- Enhanced Trading Strategy Development: This combination of trend visualization and range identification aids in refining entry and exit points, making it an invaluable tool for developing more nuanced trading strategies.

Why It's Unique:

- Dual Functionality: The combination of trend indication (via color changes) and range visualization (through the mirrored line) sets this indicator apart from traditional EMA-based tools.

- Customization and Flexibility: The ability to tailor key parameters like EMA length and the percentage away for the mirrored line empowers traders to adapt the tool to fit their specific trading approach and market conditions.

- Visual Simplicity: Despite its multifaceted capabilities, the indicator maintains a clean and intuitive visual presentation, ensuring ease of use and interpretation.

License: This source code is subject to the terms of the Mozilla Public License 2.0. More details can be found at (mozilla.org). However, the code is public so use it as you see fit.

SPX Daily Probability Predictor_MFCDescription:

The SPX Daily Probability Predictor is a powerful trading indicator designed exclusively for TradingView, providing traders with valuable insights into the potential movement of the S&P 500 index (SPX) on a daily basis. This indicator utilizes a sophisticated calculation method based on historical price movements, including gaps, to estimate the probability of the index's future direction.

Key Features:

Daily Probability Calculation:

The indicator calculates the daily probability of the SPX movement by analyzing the standard deviation of historical price changes. This statistical approach offers a comprehensive understanding of the market's volatility and aids traders in making more informed decisions.

Historical Movement Inclusion:

Unlike traditional indicators that only consider the closing prices, the SPX Daily Probability Predictor goes a step further by incorporating the full spectrum of daily movements, including gaps. This inclusive approach provides a more accurate representation of market dynamics, enhancing the reliability of the probability predictions.

Real-Time Analysis:

Stay ahead of the market with real-time analysis that adapts to the current trading session. The SPX Daily Probability Predictor dynamically adjusts its calculations throughout the trading day, ensuring that traders receive the most up-to-date and relevant information for their decision-making process.

Customizable Parameters:

Tailor the indicator to your trading preferences with customizable parameters. Adjust the lookback period or fine-tune other settings to align the probability predictions with your individual trading strategy.

By incorporating historical price movements, including gaps, and employing statistical analysis to calculate daily probabilities, the SPX Daily Probability Predictor equips traders with a valuable tool for anticipating potential market directions. Whether you are a seasoned investor or a newcomer to the world of trading, this indicator provides actionable insights that can contribute to more informed decision-making in the dynamic environment of the stock market.

Upcoming Enhancements:

Please note that while the SPX Daily Probability Predictor currently offers a robust set of features for daily market analysis, we are committed to continuous improvement and the development of additional functionalities. In future updates, users can look forward to exciting enhancements, including the capability to forecast future probabilities of market movements. This forward-looking feature will provide traders with a valuable glimpse into potential trends, aiding in more proactive decision-making.

Furthermore, we are actively working on expanding the indicator's scope to accommodate different time frames. Soon, traders will have the option to obtain probability data not only on a daily basis but also for monthly or weekly intervals. This extended flexibility allows for a more comprehensive analysis, catering to various trading styles and preferences.

As we strive to create a versatile and powerful tool for the TradingView community, we welcome user feedback and suggestions for additional features. Your insights play a crucial role in shaping the future evolution of the SPX Daily Probability Predictor, ensuring it remains a valuable asset in the dynamic landscape of financial markets. Stay tuned for updates as we continue to enhance and refine this innovative trading indicator.

[ETNX] BTC CME OI L/SOVERVIEW

This indicator displays how many traders have Long and Short positions opened on CME Bitcoin Futures and Options. The data is provided from the CFTC Commitments of Traders Reports. These reports are given weekly. Therefore, this indicator works better on weekly timeframes.

The COT reports are separated into 5 categories:

Dealer/Intermediary - These participants are typically described as the “sell side” of the market. Though they may not predominately sell futures, they design and sell various financial assets to clients. They tend to have matched books or offset their risk across markets and clients. Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities. These include large banks (U.S. and non-U.S.) and dealers in securities, swaps, and other derivatives.

Asset Manager/Institutional - These are institutional investors, including pension funds, endowments, insurance companies, mutual funds, and portfolio/investment managers whose clients are predominantly institutional.

Leveraged Funds - These are typically hedge funds and various types of money managers, including registered commodity trading advisors (CTAs); registered commodity pool operators (CPOs), or unregistered funds identified by CFTC. The strategies may involve taking outright positions or arbitrage within and across markets. The traders may be engaged in managing and conducting proprietary futures trading and trading on behalf of speculative clients.

Other Reportables - Reportable traders not placed into one of the first three categories are placed into the “other reportables” category. The traders in this category mostly use markets to hedge business risk, whether that risk is related to foreign exchange, equities, or interest rates. This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

Non Reportable

INPUT DISPLAY

The Open Interest can be displayed in three ways:

Contracts - How many contracts are opened on CME

BTC - How many BTC the contracts worth

Billions USD - How much is worth in USD based on the CME BTC Price

The Open Interest is calculated for:

Futures - The Futures Short and Long Positions Opened

Futures & Options - The Futures & Options Short and Long Positions Opened

[ETNX] BTC CME TradersOVERVIEW

This indicator displays how many traders have Long and Short positions opened on CME Bitcoin Futures and Options. The short traders have negative values only for display purposes. Therefore, if the short value is displayed as -56, that means that there are 56 traders that have short positions opened. The total of traders is the sum of short and long traders. The data is provided from the CFTC Commitments of Traders Reports. These reports are given weekly. Therefore, this indicator works better on weekly timeframes.

The COT reports are separated into 5 categories:

Dealer/Intermediary - These participants are typically described as the “sell side” of the market. Though they may not predominately sell futures, they design and sell various financial assets to clients. They tend to have matched books or offset their risk across markets and clients. Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities. These include large banks (U.S. and non-U.S.) and dealers in securities, swaps, and other derivatives.

Asset Manager/Institutional - These are institutional investors, including pension funds, endowments, insurance companies, mutual funds, and portfolio/investment managers whose clients are predominantly institutional.

Leveraged Funds - These are typically hedge funds and various types of money managers, including registered commodity trading advisors (CTAs); registered commodity pool operators (CPOs), or unregistered funds identified by CFTC. The strategies may involve taking outright positions or arbitrage within and across markets. The traders may be engaged in managing and conducting proprietary futures trading and trading on behalf of speculative clients.

Other Reportables - Reportable traders not placed into one of the first three categories are placed into the “other reportables” category. The traders in this category mostly use markets to hedge business risk, whether that risk is related to foreign exchange, equities, or interest rates. This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

Non Reportable

INPUT DISPLAY

The Open Interest can be displayed in three ways:

Futures - The Futures Short and Long Positions Opened

Options - The Options Short and Long Positions Opened

Futures & Options - The Futures & Options Short and Long Positions Opened

[ETNX] BTC CME OI RatioOVERVIEW

This indicator displays the Ratio between the Long and Short positions opened on CME Bitcoin Futures and Options. The data is provided from the CFTC Commitments of Traders Reports. These reports are given weekly. Therefore, this indicator works better on weekly timeframes.

The COT reports are separated into 5 categories:

Dealer/Intermediary - These participants are typically described as the “sell side” of the market. Though they may not predominately sell futures, they design and sell various financial assets to clients. They tend to have matched books or offset their risk across markets and clients. Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities. These include large banks (U.S. and non-U.S.) and dealers in securities, swaps, and other derivatives.

Asset Manager/Institutional - These are institutional investors, including pension funds, endowments, insurance companies, mutual funds, and portfolio/investment managers whose clients are predominantly institutional.

Leveraged Funds - These are typically hedge funds and various types of money managers, including registered commodity trading advisors (CTAs); registered commodity pool operators (CPOs) or unregistered funds identified by CFTC. The strategies may involve taking outright positions or arbitrage within and across markets. The traders may be engaged in managing and conducting proprietary futures trading and trading on behalf of speculative clients.

Other Reportables - Reportable traders not placed into one of the first three categories are placed into the “other reportables” category. The traders in this category mostly use markets to hedge business risk, whether that risk is related to foreign exchange, equities, or interest rates. This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

Non Reportable

IMPORTANT

The SPREADS are excluded. “Spreading” is a computed amount equal to offsetting long and short positions held by a trader. The computed amount of spreading is calculated as the amount of offsetting futures in different calendar months or offsetting futures and options in the same or different calendar months. Any residual long or short position is reported in the long or short column. Inter-market spreads are not considered.

INPUT INCLUDE Non-Reportable

This ratio excludes by default the Non-Reportable category. If this input is enabled, the ratio between Longs and Shorts should flatten.

INPUT DISPLAY

The Open Interest can be displayed in three ways:

Futures - The Futures Short and Long Positions Opened

Options - The Options Short and Long Positions Opened

Futures & Options - The Futures & Options Short and Long Positions Opened

[ETNX] BTC CME OIOVERVIEW

This indicator displays the Open Interest based on CME Bitcoin Futures & Options. The data is provided from the CFTC Commitments of Traders Reports. These reports are given weekly. Therefore, this indicator works better on W timeframes.

INPUTS

The Open Interest can be displayed in three ways:

Contracts - How many contracts are opened on CME

BTC - How many BTC the contracts worth

Billions USD - How much is worth in USD based on the CME BTC Price

Expected Move by Option's Implied Volatility High Liquidity

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols with high option liquidity.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options.There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry. This script will display Expected Move data for Symbols within the range of JBL-NOTE in alphabetical order.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Expected Move by Option's Implied Volatility Symbols: B - CLF

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of B - CLF in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Open-Close Difference Signalopen close signal This code will plot an upward triangle shape at the low of the candle when either the difference between open and close or the difference between close and open is above 45 points. This can be considered a buy signal. Adjust the threshold value as needed using the script's settings on TradingView.

Expected Move by Option's Implied Volatility Symbols: A - AZZ

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of A - AZZ in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Session highlighter [Digit23]This Pine Script indicator, crafted by Digit23, serves as a session highlighter to enrich your TradingView trading experience. It offers a visual representation of a specified trading session, aiding traders in identifying and concentrating on pivotal time intervals.

Key Features:

User-Defined Session: Tailor the trading session by setting specific start and end times, allowing traders to align the indicator with their preferred timeframes.

Day of Week Filter: Optionally, refine the highlighted session by selecting a specific day of the week, providing flexibility to accommodate diverse trading strategies.

Visual Clarity: The indicator employs a customizable background color during the defined trading session, ensuring quick recognition and differentiation of the highlighted timeframe.

How to Use:

Session Configuration: Adjust the start and end times to define your preferred trading session.

Day of Week Filter (Optional): Fine-tune the indicator by specifying a particular day of the week to apply the session highlight.

Visual Enhancement: The indicator visually highlights the specified trading session, offering a clear and intuitive representation on your TradingView chart.

Compatibility:

This indicator seamlessly integrates with all markets and timeframes available on TradingView, providing versatility for traders across different instruments.

Note:

Use this indicator alongside other technical analysis tools for a comprehensive trading strategy.

This indicator is shared for educational and informational purposes only. Trading involves risk, and it's crucial to conduct thorough research and analysis before making trading decisions.

Disclaimer: This script is provided for educational and informational purposes only. Trading involves risk, and it is essential to conduct thorough research and analysis before making trading decisions.

Spot-Vol CorrelationSpot-Vol Correlation Script Guide

Purpose:

This TradingView script measures the correlation between percentage changes in the spot price (e.g., for SPY, an ETF that tracks the S&P 500 index) and the changes in volatility (e.g., as indicated by the VIX, the Volatility Index). Its primary objective is to discern whether the relationship between spot price and volatility behaves as expected ("normal" condition) or diverges from the expected pattern ("abnormal" condition).

Normal vs. Abnormal Correlation:

Normal Correlation: Historically, the VIX (or volatility) and the spot price of major indices like the S&P 500 have an inverse relationship. When the spot price of the index goes up, the VIX tends to go down, indicating lower volatility. Conversely, when the index drops, the VIX generally rises, signaling increased volatility.

Abnormal Correlation: There are instances when this inverse relationship doesn't hold, and both the spot price and the VIX move in the same direction. This is considered an "abnormal" condition and might indicate unusual market dynamics, potential uncertainty, or impending shifts in market sentiment.

Using the Script:

Inputs:

First Symbol: This is set by default to VIX, representing volatility. However, users can input any other volatility metric they prefer.

Second Symbol: This is set to SPY by default, representing the spot price of the S&P 500 index. Like the first symbol, users can substitute SPY with any other asset or index of their choice.

Length of Calculation Period: Users can define the lookback period for the correlation calculation. By default, it's set to 10 periods (e.g., days for a daily chart).

Upper & Lower Bounds of Normal Zone: These parameters define the range of correlation values that are considered "normal" or expected. By default, this is set between -0.60 and -1.00.

Visuals:

Correlation Line: The main line plot shows the correlation coefficient between the two input symbols. When this line is within the "normal zone", it indicates that the spot price and volatility are inversely correlated. If it's outside this zone, the correlation is considered "abnormal".

Green Color: Indicates a period when the spot price and VIX are behaving as traditionally expected (i.e., one rises while the other falls).

Red Color: Denotes a period when the spot price and VIX are both moving in the same direction, which is an abnormal condition.

Shaded Area (Normal Zone): The area between the user-defined upper and lower bounds is shaded in green, highlighting the range of "normal" correlation values.

Interpretation:

Monitor the color and position of the correlation line relative to the shaded area:

If the line is green and within the shaded area, the market dynamics are as traditionally expected.

If the line is red or outside the shaded area, users should exercise caution as this indicates a divergence from typical behavior, which can precede significant market moves or heightened uncertainty.

Advanced Market Opening Gap DetectorThe Advanced Market Opening Gap Detector (AMOGD) is a Pine Script indicator designed to help you identify market gaps at the opening of a new trading day. Gaps are areas on a chart where the price of a security moves sharply up or down with little or no trading in between. They are significant as they may indicate a change in market sentiment. This indicator highlights the size and direction of the opening gap, allowing you to potentially adjust your strategies accordingly.

By setting a minimum gap size, you can filter out smaller, less significant gaps, focusing only on larger gaps which may have more substantial implications. You can define the minimum gap size in points or pips, providing flexibility based on your trading preferences and the asset being traded.

How-to Use:

Apply the AMOGD indicator to your TradingView chart.

Configure the minimum gap size and unit (points or pips) based on your preference using the settings panel.

At the opening of each new trading day, the indicator will check for a gap between the previous close and the opening price.

If a valid gap is detected (i.e., the gap size meets or exceeds the minimum gap size specified), the indicator will:

Draw lines to indicate the opening price and previous close.

Display a label indicating the size of the gap.

Highlight the gap on the chart for better visibility.

Importance:

Market gaps can be pivotal points indicating a possible new trend or a continuation of the current trend. Being able to identify and analyze these gaps is crucial for making informed trading decisions. The AMOGD indicator automates the process of identifying and visualizing opening market gaps, saving traders time and allowing for quick assessment of market conditions at the start of each trading day. By setting a minimum gap size, traders can also filter out less significant price movements, allowing them to focus on potentially trend-changing gaps. This tool can be a valuable addition to a trader's toolkit, aiding in the analysis and interpretation of market behavior at the open, which is often a very volatile and crucial period in the trading day.

DISCLAIMER! RISK WARNING!

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. TRADERS SHOULD NOT BASE THEIR DECISION ON INVESTING IN ANY TRADING PROGRAM SOLELY ON THE PAST PERFORMANCE PRESENTED, ADDITIONALLY, IN MAKING AN INVESTMENT DECISION, TRADERS MUST ALSO RELY ON THEIR OWN EXAMINATION OF THE PERSON OR ENTITY MAKING THE TRADING DECISIONS.

[BCT] Option Pricing via Markov Chain Monte Carlo SimulationOverview:

This script offers a toolkit for quantitative options trading, using Monte Carlo simulations based on actual historical returns to model potential future price paths for underlying assets. A range of metrics related to options trading are also provided.

Monte Carlo Simulations:

The script employs Monte Carlo simulations to model future price paths based on the historical returns of the underlying asset. These simulated paths are represented as parabolas at the 2-sigma, 25th percentile, and median levels for quick reference.

Methodologies:

For calculating options prices at At-the-Money (or any user-selected strike), two methodologies are used:

Simple Averaging: Takes the mean of the simulated asset price paths.

Kernel Density Estimation (KDE): Applied to the simulated asset price paths to produce a smoothed estimate of its probability density function, thereby aiding in a more nuanced option price calculation.

Bootstrap Resampling:

Bootstrap resampling is specifically applied to the simulated asset price paths to generate an estimate of the standard deviation of the options prices. Note that while bootstrap methods are employed, they serve as statistical tools and do not guarantee statistical reliability.

Metrics Displayed:

Model-Estimated At-the-Money (or selected strike) Straddle Price

Model-Estimated At-the-Money (or selected strike) Call Price

Model-Estimated At-the-Money (or selected strike) Put Price

Model-Estimated Standard deviation for Option Prices from simulated price paths

Underlying Monte Carlo Simulation Results (represented as parabolas at the 2 sigma, 25 percentile and median)

This is not financial advice. Use at your own risk.

Disclaimer: Options trading carries a high level of risk and may not be suitable for all investors. This script is intended to serve as an educational tool and should not be considered financial advice. While designed to aid in decision-making, the script's indicators are not guarantees of performance or outcomes. Always conduct your own due diligence before making trading decisions.

Auto Trailing stoploss By InvestYourAsset💥The Auto Trailing Stop-Loss indicator is a technical indicator that uses the ATR (Average True Range) to calculate a trailing stop-loss for both long and short positions.

💥The signals according to the indicator allows traders to exit from the position before its too late! The indicator can be used to determine when to enter and exit trades.

💥To use the indicator, you simply need to set the input parameters to suit your trading style and risk tolerance. The default values for the parameters are:

p: The ATR period (14)

q: The stop period (20)

x: The multiplier used to calculate the initial high and initial low (1.5)

Calculations:

📈Calculates the ATR using the specified period you can modify ATR period according to your trading style.

📈Calculates the initial high and low stop levels based on the highest high and lowest low over the user defined ATR period.

📈Calculates short and long stoploss levels using the initial high and low stops.

💥Once you have set the input parameters according to your trading style whether you are a day trader or a swing trader, the indicator will plot the short stoploss, long stoploss, and stoploss hit signals on your chart.

💥You can use the indicator to enter and exit trades in a various ways.

For example,

🚀 you could enter a long trade when the price crosses above both red and green lines plotted on the chart. (or when price crosses over both short stoploss and long stoploss.) You could also use the indicator to secure your profits by moving your stop-loss up as the price moves in your favor.

Here is an example of how you could use the indicator to enter and exit trades:

🚀Enter a long trade when the price crosses above the red line or short stoploss.

✅keep Moving your stop-loss upward with the long stoploss or green line.

✅Exit the trade when the price crosses below the long stoploss or green line.

💥You can also use the indicator to protect your existing trades. For example, if you are already in a long trade, you could move your stop-loss up to the short stop when the price moves up 10%. This will help you to protect your profits in case the price starts to move against you.

💥💥some additional tips for using the Auto Trailing Stop-Loss indicator:

✅Use the indicator in conjunction with other technical indicators or your own trading strategy to generate entry and exit signals.

✅Backtest your trading strategy before using it live to make sure that it is profitable.

✅Use the indicator to protect your profits by moving your stop-loss up as the price moves in your favor.

✅ Always follow risk management rules and manage your position sizing according to your risk appetite.

✅ Be aware of the overall trend direction. If the trend is up, you should be looking for bullish reversals or continuations. If the trend is down, you should be looking for bearish reversals or continuations.

This script essentially provides a visual representation of a trading strategy that automatically adjusts stop-loss levels based on market volatility (ATR). It also includes signals for entering long or short positions and visually highlights these signals on the chart.

📣📣Follow us for timely updates regarding future indicators and give it a like if you appreciate the work.📣📣

Highlight Day of WeekA simple indicator that highlights certain days of the week by changing the background color of the chart to a specified color. Each day can be highlighted its own respective color.

This can be used to visually search for patterns based on day of the week.