EC_2025_Q4_ENLibrary "EC_2025_Q4_EN"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

Indicators and strategies

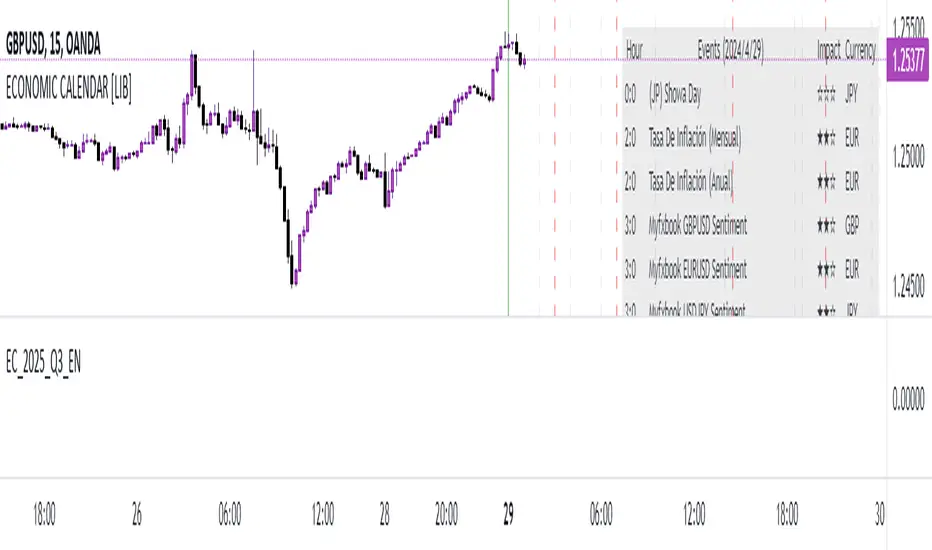

EC_2025_Q3_ENLibrary "EC_2025_Q3_EN"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2025_Q2_ENLibrary "EC_2025_Q2_EN"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2025_Q1_ENLibrary "EC_2025_Q1_EN"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2025_Q4_SPLibrary "EC_2025_Q4_SP"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2025_Q3_SPLibrary "EC_2025_Q3_SP"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2025_Q2_SPLibrary "EC_2025_Q2_SP"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2025_Q1_SPLibrary "EC_2025_Q1_SP"

output2025()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2025()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2025()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2025()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q4_SPLibrary "EC_2024_Q4_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q3_SPLibrary "EC_2024_Q3_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q4_ENLibrary "EC_2024_Q4_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q3_ENLibrary "EC_2024_Q3_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q2_ENLibrary "EC_2024_Q2_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q2_SPLibrary "EC_2024_Q2_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q1_SPLibrary "EC_2024_Q1_SP"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2024_Q1_ENLibrary "EC_2024_Q1_EN"

output2024()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2024()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2024()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2024()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q4_SPLibrary "EC_2023_Q4_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q3_SPLibrary "EC_2023_Q3_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q2_SPLibrary "EC_2023_Q2_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q1_SPLibrary "EC_2023_Q1_SP"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q4_ENLibrary "EC_2023_Q4_EN"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q3_ENLibrary "EC_2023_Q3_EN"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text

EC_2023_Q2_ENLibrary "EC_2023_Q2_EN"

output2023()

Returns the list of events during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;;; ...

Where: is expressed as date + characteristics: YYYY,MM,DD,hh,mm,ss,x,y,z

x impact in numbers

y event name in numbers

z currency in numbers

name2023()

Returns the list of event names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, name

index: related to event name y

name event: event name related to y text

impact2023()

Returns the list of impact names during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, impact

index: related to impact name x

impact: impact name related to x text

currency2023()

Returns the list of currencies during the period.

Returns: array: (week1,week2, ... week_n)

week_n= ;; ...

Where: is expressed as: index, currency

index: related to currency name z

currency: currency name related to z text