MathProbabilityDistributionLibrary "MathProbabilityDistribution"

Probability Distribution Functions.

name(idx) Indexed names helper function.

Parameters:

idx : int, position in the range (0, 6).

Returns: string, distribution name.

usage:

.name(1)

Notes:

(0) => 'StdNormal'

(1) => 'Normal'

(2) => 'Skew Normal'

(3) => 'Student T'

(4) => 'Skew Student T'

(5) => 'GED'

(6) => 'Skew GED'

zscore(position, mean, deviation) Z-score helper function for x calculation.

Parameters:

position : float, position.

mean : float, mean.

deviation : float, standard deviation.

Returns: float, z-score.

usage:

.zscore(1.5, 2.0, 1.0)

std_normal(position) Standard Normal Distribution.

Parameters:

position : float, position.

Returns: float, probability density.

usage:

.std_normal(0.6)

normal(position, mean, scale) Normal Distribution.

Parameters:

position : float, position in the distribution.

mean : float, mean of the distribution, default=0.0 for standard distribution.

scale : float, scale of the distribution, default=1.0 for standard distribution.

Returns: float, probability density.

usage:

.normal(0.6)

skew_normal(position, skew, mean, scale) Skew Normal Distribution.

Parameters:

position : float, position in the distribution.

skew : float, skewness of the distribution.

mean : float, mean of the distribution, default=0.0 for standard distribution.

scale : float, scale of the distribution, default=1.0 for standard distribution.

Returns: float, probability density.

usage:

.skew_normal(0.8, -2.0)

ged(position, shape, mean, scale) Generalized Error Distribution.

Parameters:

position : float, position.

shape : float, shape.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.ged(0.8, -2.0)

skew_ged(position, shape, skew, mean, scale) Skew Generalized Error Distribution.

Parameters:

position : float, position.

shape : float, shape.

skew : float, skew.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.skew_ged(0.8, 2.0, 1.0)

student_t(position, shape, mean, scale) Student-T Distribution.

Parameters:

position : float, position.

shape : float, shape.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.student_t(0.8, 2.0, 1.0)

skew_student_t(position, shape, skew, mean, scale) Skew Student-T Distribution.

Parameters:

position : float, position.

shape : float, shape.

skew : float, skew.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.skew_student_t(0.8, 2.0, 1.0)

select(distribution, position, mean, scale, shape, skew, log) Conditional Distribution.

Parameters:

distribution : string, distribution name.

position : float, position.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

shape : float, shape.

skew : float, skew.

log : bool, if true apply log() to the result.

Returns: float, probability.

usage:

.select('StdNormal', __CYCLE4F__, log=true)

Indicators and strategies

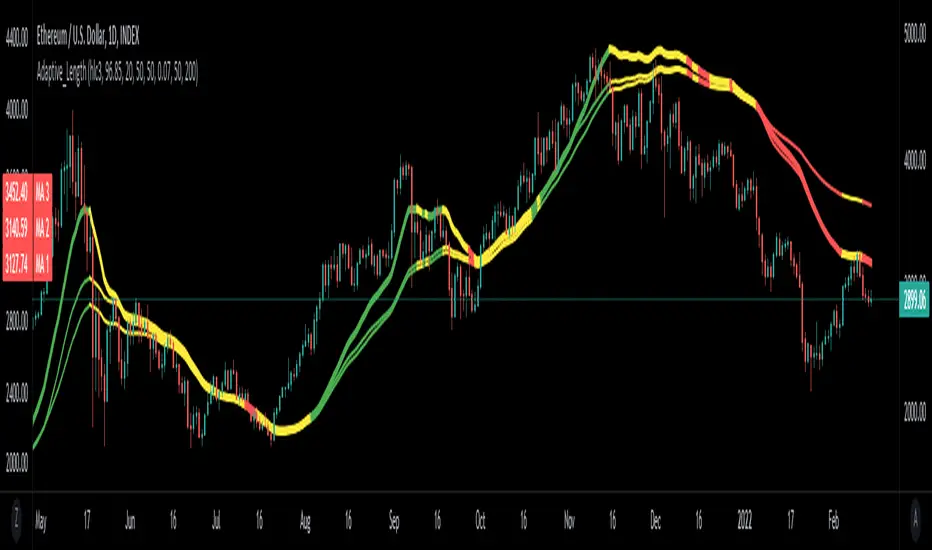

Adaptive_LengthLibrary "Adaptive_Length"

This library contains functions to calculate Adaptive dynamic length which can be used in Moving Averages and other indicators.

Two Exponential Moving Averages (EMA) are plotted. Coloring in plot is derived from Chikou filter and Dynamic length of MA1 is adapted using Signal output from Chikou library.

dynamic(para, adapt_Pct, minLength, maxLength) Adaptive dynamic length based on boolean parameter

Parameters:

para : Boolean parameter; if true then length would decrease and would increase if its false

adapt_Pct : Percentage adaption based on parameter

minLength : Minimum allowable length

maxLength : Maximum allowable length

Returns: Adaptive Dynamic Length based on Boolean Parameter

auto_alpha(src, a) Adaptive length based on automatic alpha calculations from source input

Parameters:

src : Price source for alpha calculations

a : Input Alpha value

Returns: Adaptive Length calculated from input price Source and Alpha

MovingAveragesLibrary "MovingAverages"

Contains utilities for generating moving average values including getting a moving average by name and a function for generating a Volume-Adjusted WMA.

sma(_D, _len) Simple Moving Avereage

Parameters:

_D : The series to measure from.

_len : The number of bars to measure with.

ema(_D, _len) Exponential Moving Avereage

Parameters:

_D : The series to measure from.

_len : The number of bars to measure with.

rma(_D, _len) RSI Moving Avereage

Parameters:

_D : The series to measure from.

_len : The number of bars to measure with.

wma(_D, _len) Weighted Moving Avereage

Parameters:

_D : The series to measure from.

_len : The number of bars to measure with.

vwma(_D, _len) volume-weighted Moving Avereage

Parameters:

_D : The series to measure from. Default is 'close'.

_len : The number of bars to measure with.

alma(_D, _len) Arnaud Legoux Moving Avereage

Parameters:

_D : The series to measure from. Default is 'close'.

_len : The number of bars to measure with.

cma(_D, _len, C, compound) Coefficient Moving Avereage (CMA) is a variation of a moving average that can simulate SMA or WMA with the advantage of previous data.

Parameters:

_D : The series to measure from. Default is 'close'.

_len : The number of bars to measure with.

C : The coefficient to use when averaging. 0 behaves like SMA, 1 behaves like WMA.

compound : When true (default is false) will use a compounding method for weighting the average.

dema(_D, _len) Double Exponential Moving Avereage

Parameters:

_D : The series to measure from. Default is 'close'.

_len : The number of bars to measure with.

zlsma(_D, _len) Arnaud Legoux Moving Avereage

Parameters:

_D : The series to measure from. Default is 'close'.

_len : The number of bars to measure with.

zlema(_D, _len) Arnaud Legoux Moving Avereage

Parameters:

_D : The series to measure from. Default is 'close'.

_len : The number of bars to measure with.

get(type, len, src) Generates a moving average based upon a 'type'.

Parameters:

type : The type of moving average to generate. Values allowed are: SMA, EMA, WMA, VWMA and VAWMA.

len : The number of bars to measure with.

src : The series to measure from. Default is 'close'.

Returns: The moving average series requested.

ChikouLibrary "Chikou"

This library contains Chikou Filter function to enhances functionality of Chikou-Span from Ichimoku Cloud using a simple trend filter.

Chikou is basically close value of ticker offset to close and it is a good for indicating if close value has crossed potential Support/Resistance zone from past. Chikou is usually used with 26 period.

Chikou filter uses a lookback length calculated from provided lookback percentage and checks if trend was bullish or bearish within that lookback period.

Bullish : Trend is bullish if Chikou span is above high values of all candles within defined lookback period. Bull color shows bullish trend .

Bearish : Trend is bearish if Chikou span is below low values of all candles within defined lookback period. This is indicated by Bearish color.

Reversal / Choppiness : Reversal color indicates that Chikou are swinging around candles within defined lookback period which is an indication of consolidation or trend reversal.

chikou(src, len, perc, _high, _low, bull_col, bear_col, r_col) Chikou Filter for Ichimoku Cloud with Color and Signal Output

Parameters:

src : Price Source (better to use (OHLC4+high+low/3 instead of default close value)

len : Chikou Legth (displaced source value)

perc : Percentage lookback period for Chikou Filter with defined how much candels of total length should be considered for backward filteration

_high : Ticker High Value

_low : Ticker Low Value

bull_col : Color to be returned if source value is greater than all candels within provided lookback percentage.

bear_col : Color to be returned if source value is lower than all candels within provided lookback percentage.

r_col : Color to be returned if source value is swinging around candles within defined lookback period which is an indication of consolidation or trend reversal.

Returns: Color based on trend. 'bull_col' if trend is bullish, 'bear_col' if trend is bearish. 'r_col' if no prominent trend. Integer Signal is also returned as 1 for Bullish, -1 for Bearish and 0 for no prominent trend.

HA_CandlesLibrary "HA_Candles"

Heikin Ashi Candles

HA_Close() Heikin Ashi Modified Close

Returns: Heikin Ashi Modified Close

HA_Open() Heikin Ashi Modified Open

Returns: Heikin Ashi Modified Open

HA_High() Heikin Ashi Modified High

Returns: Heikin Ashi Modified High

HA_Low() Heikin Ashi Modified Low

Returns: Heikin Ashi Modified Low

HA_Delta(Heikin) Heikin Ashi Delta

Parameters:

Heikin : Ashi Close, Heikin Ashi Open

Returns: Heikin Ashi Delta

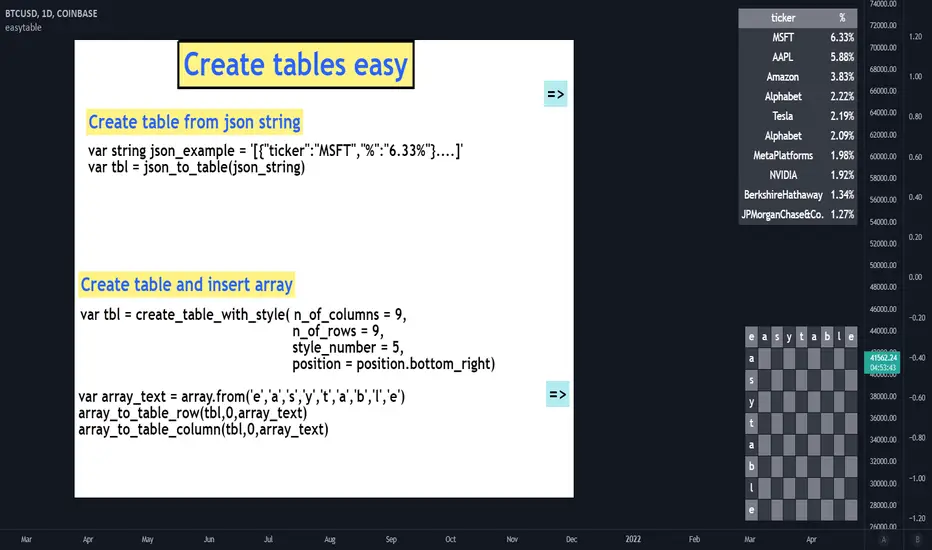

easytableLibrary "easytable"

Create tables easily, with minimal code

▦ FEATURES ▦

█ Create tables █ JSON To Table █ Change Colors █ Array to Rows/Columns █ Pre-Styles █ Change Text Size █ Delete Rows/Columns █ Blink Cells

indentify_table_id() Identifies all tables ID number in each cell(0,0).

get_table_by_id(id_number) Get table object by ID number.

Parameters:

id_number : (int) ID number of the table to fetch.

Returns: table.

change_cells_color(table_object, cells_color, start_column, end_column, start_row, end_row) Change cells background colors.

Parameters:

table_object : (table) table object to be changed.

cells_color : (color) Cells color.

start_column : (int) Start column.

end_column : (int) End column.

start_row : (int) Start Row.

end_row : (int) End Row to change.

Returns: Void.

change_cells_text_color(table_object, text_color, start_column, end_column, start_row, end_row) Change cells text colors.

Parameters:

table_object : (table) table object to be changed.

text_color : (color) Text color.

start_column : (int) Start column.

end_column : (int) End column.

start_row : (int) Start Row.

end_row : (int) End Row.

Returns: Void.

change_all_table_text_color(table_object, text_color, table_column_size, table_row_size) Change All table text color.

Parameters:

table_object : (table) table object to be changed.

text_color : (color) Text color.

table_column_size : (int) Size of the table columns.

table_row_size : (int) Size of the table rows.

Returns: Void.

change_table_size(table_object, n_of_columns, n_of_rows, tbl_size) Change table size.

Parameters:

table_object : (table) table object to be changed.

n_of_columns : (int) Size of the table columns.

n_of_rows : (int) Size of the table rows.

tbl_size : (string) size of the table.

Returns: Void.

change_cells_text_size(text_size, start_column, end_column, start_row, end_row, table_id) Change table cells text size .

Parameters:

text_size : (string) Text size.

start_column : (int) Start column.

end_column : (int)(optional) End column.

start_row : (int)(optional) Start Row.

end_row : (int)(optional) End Row.

table_id : (int)(optional) Number of the ID of the table.

Returns: Void.

table_delete_row(table_object, table_column_size, start_row, end_row) Delete specified rows from table.

Parameters:

table_object : (table) table object to be changed.

table_column_size : (int) Table columns max size.

start_row : (int) Start row to delete.

end_row : (int)(optional) End row to delete (optional — Assumes start_row value).

Returns: Void.

table_delete_column(table_object, table_row_size, start_column, end_column) Delete specified columns from table.

Parameters:

table_object : (table) table object to be changed.

table_row_size : (int) Table rows max size.

start_column : (int) Start column to delete.

end_column : (int)(optional) End column to delete (optional — Assumes start_column value).

Returns: Void.

array_to_table_column_auto(column_to_insert, array_to_insert, table_id) Insert string array to table column without passing table object.

Parameters:

column_to_insert : (int) Column to be inserted.

array_to_insert : (string array) Start column to delete.

table_id : (int)(optional) Number of the ID of the table.

Returns: Void.

array_to_table_row_auto(row_to_insert, array_to_insert, table_id) Insert string array to table row without passing table object.

Parameters:

row_to_insert : (int) Column to be inserted.

array_to_insert : (string array) Start column to delete.

table_id : (int)(optional) Number of the ID of the table.

Returns: Void.

array_to_table_row(table_object, row_to_insert, array_to_insert) Insert string array to table row by passing table object.

Parameters:

table_object : (table) table object to be changed.

row_to_insert : (int) Row to be inserted.

array_to_insert : (string array) Start column to delete.

Returns: Void.

array_to_table_column(table_object, column_to_insert, array_to_insert) Insert string array to table column by passing table object.

Parameters:

table_object : (table) table object to be changed.

column_to_insert : (int) Column to be inserted.

array_to_insert : (string array) Start column to delete.

Returns: Void.

blink_cell(cell_column, cell_row, c_color, blink_interval_ms, table_id) Changes cell color at set intervals (blink).

Parameters:

cell_column : (int) Cell column position.

cell_row : (int) Cell row position.

c_color : (color) Color to blink.

blink_interval_ms : (int)(opt) Interval in milliseconds.

table_id : (int)(opt) Table ID number.

change_table_style(table_object, number_of_columns, number_of_rows, color) Changes table pre-style by selecting a pre-style number.

Parameters:

table_object : (table) table object to be changed.

number_of_columns : (int) Table column size.

number_of_rows : (int) Table row size.

color : 1 (color) Color of .

Returns: Void.

create_table_clean(n_of_columns, n_of_rows, position) Create a simple(blank) table without any styling.

Parameters:

n_of_columns : (int) Numbers of columns in the table.

n_of_rows : (int) Number of rows in the table.

position : (string) table position.

Returns: table object.

create_table_with_style(n_of_columns, n_of_rows, style_number, position) Create table with a pre-set style.

Parameters:

n_of_columns : (int) Numbers of columns in the table.

n_of_rows : (int) Number of rows in the table.

style_number : (int) Style number.

position : (string) table position.

Returns: table object.

json_to_table(raw_json) Create table based on input raw json string.

Parameters:

raw_json : (int) Raw json string.

Returns: table object.

json_example() Example function that display a table based on a json

example_create_table()

jsonLibrary "json"

Convert JSON strings to tradingview

▦ FEATURES ▦

█ Json to array █ Get json key names █ Get json key values █ Size of json

get_json_keys_names(raw_json) Returns string array with all key names

Parameters:

raw_json : (string) Raw JSON string

Returns: (string array) Array with all key names

get_values_by_id_name(raw_json, key_name) Returns string array with values of the input key name

Parameters:

raw_json : (string) Raw JSON string

key_name : (string) Name of the key to be fetched

Returns: (string array) Array with values of the input key name

size_of_json_string(raw_json) Returns size of raw JSON string

Parameters:

raw_json : (string) Raw JSON string

Returns: Size of n_of_values, size of n_of_keys_names

timeUtilsLibrary "timeUtils"

Utils for time series

tradingDaysTillEndOfMonth() Calculates how many full trading days left until the end of the current month. (It doesn't take into account market holidays)

Returns: int series of the remaining trading days until the end of the month.

insideRange()

utilsLibrary "utils"

ma_smooth(alg, src, len) Calculates various moving averages

Parameters:

alg : Smoothing algorithm to use

src : Source data

len : Length of moving average

RVSILibrary "RVSI"

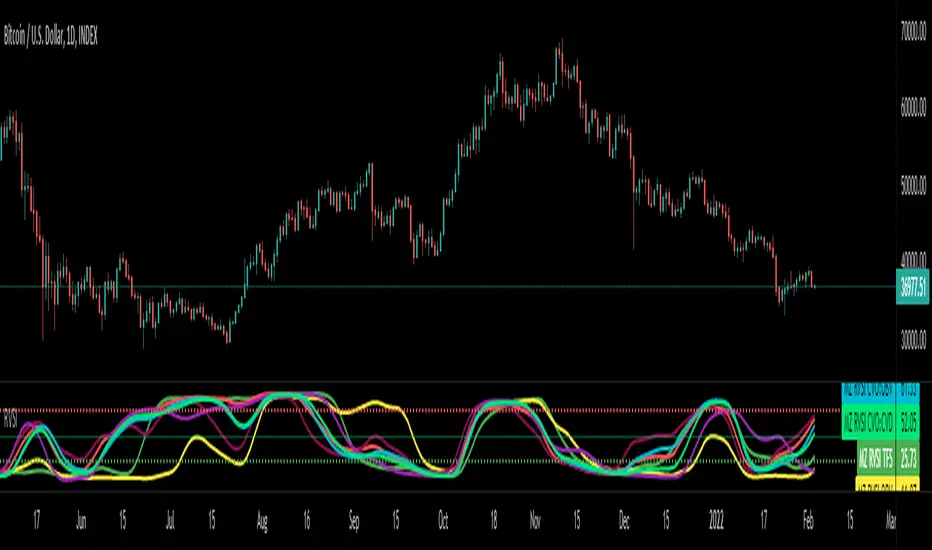

This Library contains functions that calculate all types of " Relative Volume Strength Index (MZ RVSI ) " depending upon unique volume oscillator. Achieved RVSI value can be used for divergence detection in volume or to adapt dynamic length in Moving Averages or other functions.

rvsi_tfs(vol_src, vol_Len, rvsiLen, _open, _close) Relative Volume Strength Index based on TFS Volume Oscillator

Parameters:

vol_src : Volume Source

vol_Len : Volume Legth for TFS Volume Oscillato

rvsiLen : Period of Relative Volume Strength Index

_open : Ticker Open Value

_close : Ticker Close Value

Returns: Relative Volume Strength Index value based on TFS Volume Oscillator

rvsi_obv(vol_src, rvsiLen, _close) Relative Volume Strength Index based on On Balance Volume

Parameters:

vol_src : Volume Source to Calculate On Balance Volume

rvsiLen : Period of Relative Volume Strength Index

_close : Ticker Close Value

Returns: Relative Volume Strength Index value based on On Balance Volume

rvsi_kvo(vol_src, FastX, SlowX, rvsiLen, _close) Relative Volume Strength Index based on Klinger Volume Oscillator

Parameters:

vol_src : Volume Source

FastX : Volume Fast Length

SlowX : Volume Slow Length

rvsiLen : Period of Relative Volume Strength Index

_close : Ticker Close Value

Returns: Relative Volume Strength Index value based on Klinger Volume Oscillator

rvsi_vzo(vol_src, zLen, rvsiLen, _close) Relative Volume Strength Index based on Volume Zone Oscillator

Parameters:

vol_src : Volume Source

zLen : Volume Legth for Volume Zone Oscillator

rvsiLen : Period of Relative Volume Strength Index

_close : Ticker Close Value

Returns: Relative Volume Strength Index value based on Volume Zone Oscillator

rvsi_cvo_obv(vol_src, ema1len, ema2len, rvsiLen) Relative Volume Strength Index based on Cumulative Volume Oscillator with On Balance Volume as Calculations Source

Parameters:

vol_src : Volume Source

ema1len : EMA Fast Length

ema2len : EMA Slow Length

rvsiLen : Period of Relative Volume Strength Index

Returns: Relative Volume Strength Index value based on Cumulative Volume Oscillator with On Balance Volume as Calculations Source

rvsi_cvo_pvt(vol_src, FastX, SlowX, rvsiLen) Relative Volume Strength Index based on Cumulative Volume Oscillator with Price Volume Trend as Calculations Source

Parameters:

vol_src : Volume Source

FastX : EMA Fast Length

SlowX : EMA Slow Length

rvsiLen : Period of Relative Volume Strength Index

Returns: Relative Volume Strength Index value based on Cumulative Volume Oscillator with Price Volume Trend as Calculations Source

rvsi_cvo_cvd(vol_src, FastX, SlowX, rvsiLen, _open, _close, _high, _low) Relative Volume Strength Index based on Cumulative Volume Oscillator with Cumulative Volume Delta as Calculations Source

Parameters:

vol_src : Volume Source

FastX : EMA Fast Length

SlowX : EMA Slow Length

rvsiLen : Period of Relative Volume Strength Index

_open : Ticker Open Value

_close : Ticker Close Value

_high : Ticker High Value

_low : Ticker Low Value

Returns: Relative Volume Strength Index value based on Cumulative Volume Oscillator with Cumulative Volume Delta as Calculations Source

eStrategyLibrary "eStrategy"

Library contains methods which can help build custom strategy for continuous investment plans and also compare it with systematic buy and hold.

sip(startYear, initialDeposit, depositFrequency, recurringDeposit, buyPrice) Depicts systematic buy and hold over period of time

Parameters:

startYear : Year on which SIP is started

initialDeposit : Initial one time investment at the start

depositFrequency : Frequency of recurring deposit - can be monthly or weekly

recurringDeposit : Recurring deposit amount

buyPrice : Indicatinve buy price. Use high to be conservative. low, close, open, hl2, hlc3, ohlc4, hlcc4 are other options.

Returns: totalInvestment - initial + recurring deposits

totalQty - Quantity of units held for given instrument

totalEquity - Present equity

customStrategy(startYear, initialDeposit, depositFrequency, recurringDeposit, buyPrice, sellPrice, initialInvestmentPercent, recurringInvestmentPercent, signal, tradePercent) Allows users to define custom strategy and enhance systematic buy and hold by adding take profit and reloads

Parameters:

startYear : Year on which SIP is started

initialDeposit : Initial one time investment at the start

depositFrequency : Frequency of recurring deposit - can be monthly or weekly

recurringDeposit : Recurring deposit amount

buyPrice : Indicatinve buy price. Use high to be conservative. low, close, open, hl2, hlc3, ohlc4, hlcc4 are other options.

sellPrice : Indicatinve sell price. Use low to be conservative. high, close, open, hl2, hlc3, ohlc4, hlcc4 are other options.

initialInvestmentPercent : percent of amount to invest from the initial depost. Keep rest of them as cash

recurringInvestmentPercent : percent of amount to invest from recurring deposit. Keep rest of them as cash

signal : can be 1, -1 or 0. 1 means buy/reload. -1 means take profit and 0 means neither.

tradePercent : percent of amount to trade when signal is not 0. If taking profit, it will sell the percent from existing position. If reloading, it will buy with percent from cash reserve

Returns: totalInvestment - initial + recurring deposits

totalQty - Quantity of units held for given instrument

totalCash = Amount of cash held

totalEquity - Overall equity = totalQty*close + totalCash

JohnEhlersFourierTransformLibrary "JohnEhlersFourierTransform"

Fourier Transform for Traders By John Ehlers, slightly modified to allow to inspect other than the 8-50 frequency spectrum.

reference:

www.mesasoftware.com

high_pass_filter(source) Detrended version of the data by High Pass Filtering with a 40 Period cutoff

Parameters:

source : float, data source.

Returns: float.

transformed_dft(source, start_frequency, end_frequency) DFT by John Elhers.

Parameters:

source : float, data source.

start_frequency : int, lower bound of the frequency window, must be a positive number >= 0, window must be less than or 30.

end_frequency : int, upper bound of the frequency window, must be a positive number >= 0, window must be less than or 30.

Returns: tuple with float, float array.

db_to_rgb(db, transparency) converts the frequency decibels to rgb.

Parameters:

db : float, decibels value.

transparency : float, transparency value.

Returns: color.

windowing_taAll Signals Are the Sum of Sines. When looking at real-world signals, you usually view them as a price changing over time. This is referred to as the time domain. Fourier’s theorem states that any waveform in the time domain can be represented by the weighted sum of sines and cosines. For example, take two sine waves, where one is three times as fast as the other–or the frequency is 1/3 the first signal. When you add them, you can see you get a different signal.

Although performing an FFT on a signal can provide great insight, it is important to know the limitations of the FFT and how to improve the signal clarity using windowing. When you use the FFT to measure the frequency component of a signal, you are basing the analysis on a finite set of data. The actual FFT transform assumes that it is a finite data set, a continuous spectrum that is one period of a periodic signal. For the FFT, both the time domain and the frequency domain are circular topologies, so the two endpoints of the time waveform are interpreted as though they were connected together. When the measured signal is periodic and an integer number of periods fill the acquisition time interval, the FFT turns out fine as it matches this assumption. However, many times, the measured signal isn’t an integer number of periods. Therefore, the finiteness of the measured signal may result in a truncated waveform with different characteristics from the original continuous-time signal, and the finiteness can introduce sharp transition changes into the measured signal. The sharp transitions are discontinuities.

When the number of periods in the acquisition is not an integer, the endpoints are discontinuous. These artificial discontinuities show up in the FFT as high-frequency components not present in the original signal. These frequencies can be much higher than the Nyquist frequency and are aliased between 0 and half of your sampling rate. The spectrum you get by using a FFT, therefore, is not the actual spectrum of the original signal, but a smeared version. It appears as if energy at one frequency leaks into other frequencies. This phenomenon is known as spectral leakage, which causes the fine spectral lines to spread into wider signals.

You can minimize the effects of performing an FFT over a noninteger number of cycles by using a technique called windowing. Windowing reduces the amplitude of the discontinuities at the boundaries of each finite sequence acquired by the digitizer. Windowing consists of multiplying the time record by a finite-length window with an amplitude that varies smoothly and gradually toward zero at the edges. This makes the endpoints of the waveform meet and, therefore, results in a continuous waveform without sharp transitions. This technique is also referred to as applying a window.

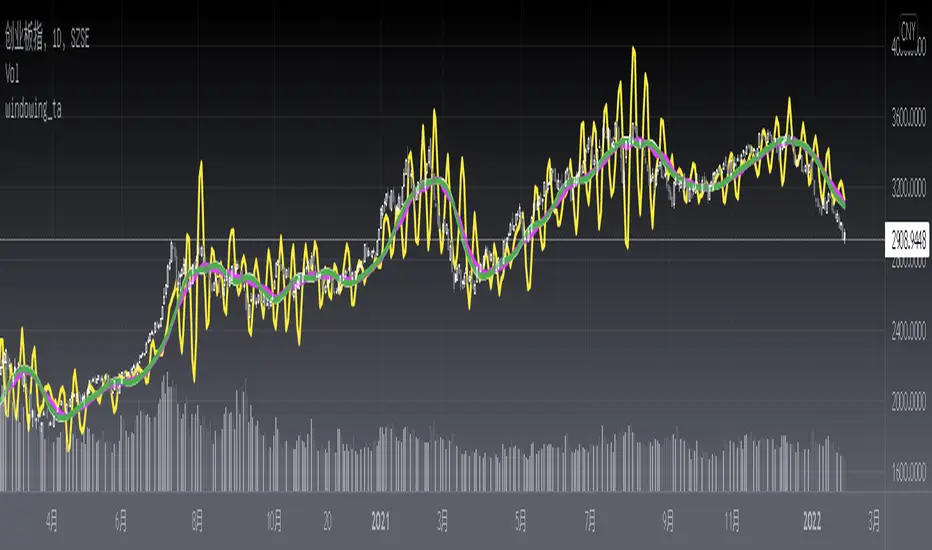

Here is a windowing_ta library with J.F Ehlers Windowing functions proposed on Sep, 2021.

Library "windowing_ta"

hann()

hamm()

fir_sma()

fir_triangle()

harmonicpatterns1Library "harmonicpatterns1"

harmonicpatterns: methods required for calculation of harmonic patterns. Correction for library (missing export in line 303)

isGartleyPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isGartleyPattern: Checks for harmonic pattern Gartley

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Gartley. False otherwise.

isBatPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isBatPattern: Checks for harmonic pattern Bat

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Bat. False otherwise.

isButterflyPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isButterflyPattern: Checks for harmonic pattern Butterfly

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Butterfly. False otherwise.

isCrabPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isCrabPattern: Checks for harmonic pattern Crab

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Crab. False otherwise.

isDeepCrabPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isDeepCrabPattern: Checks for harmonic pattern DeepCrab

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is DeepCrab. False otherwise.

isCypherPattern(xabRatio, axcRatio, xadRatio, err_min, err_max) isCypherPattern: Checks for harmonic pattern Cypher

Parameters:

xabRatio : AB/XA

axcRatio : XC/AX

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Cypher. False otherwise.

isSharkPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isSharkPattern: Checks for harmonic pattern Shark

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Shark. False otherwise.

isNenStarPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isNenStarPattern: Checks for harmonic pattern Nenstar

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Nenstar. False otherwise.

isAntiNenStarPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isAntiNenStarPattern: Checks for harmonic pattern Anti NenStar

Parameters:

xabRatio : - AB/XA

abcRatio : - BC/AB

bcdRatio : - CD/BC

xadRatio : - AD/XA

err_min : - Minumum error threshold

err_max : - Maximum error threshold

Returns: True if the pattern is Anti NenStar. False otherwise.

isAntiSharkPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isAntiSharkPattern: Checks for harmonic pattern Anti Shark

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Anti Shark. False otherwise.

isAntiCypherPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isAntiCypherPattern: Checks for harmonic pattern Anti Cypher

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Anti Cypher. False otherwise.

isAntiCrabPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isAntiCrabPattern: Checks for harmonic pattern Anti Crab

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Anti Crab. False otherwise.

isAntiButterflyPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isAntiButterflyPattern: Checks for harmonic pattern Anti Butterfly

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Anti Butterfly. False otherwise.

isAntiBatPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isAntiBatPattern: Checks for harmonic pattern Anti Bat

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Anti Bat. False otherwise.

isAntiGartleyPattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isAntiGartleyPattern: Checks for harmonic pattern Anti Gartley

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Anti Gartley. False otherwise.

isNavarro200Pattern(xabRatio, abcRatio, bcdRatio, xadRatio, err_min, err_max) isNavarro200Pattern: Checks for harmonic pattern Navarro200

Parameters:

xabRatio : AB/XA

abcRatio : BC/AB

bcdRatio : CD/BC

xadRatio : AD/XA

err_min : Minumum error threshold

err_max : Maximum error threshold

Returns: True if the pattern is Navarro200. False otherwise.

isHarmonicPattern(x, a, c, c, d, flags, errorPercent) isHarmonicPattern: Checks for harmonic patterns

Parameters:

x : X coordinate value

a : A coordinate value

c : B coordinate value

c : C coordinate value

d : D coordinate value

flags : flags to check patterns. Send empty array to enable all

errorPercent : Error threshold

Returns: Array of boolean values which says whether valid pattern exist and array of corresponding pattern names

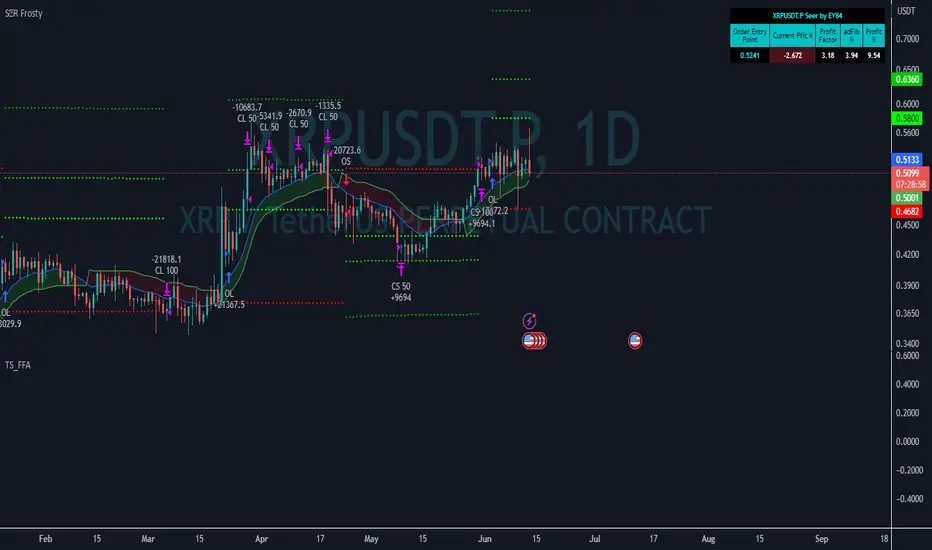

TS_FFALibrary "TS_FFA"

Splits the ticker and generates best configs for FP and PP

splitter(x) Splits the ticker and found the configuration regarding to name.

Parameters:

_x: ticker

Returns: Fib and Profit percent values

- Splitter had been added.

- USDTPERP coins on Binance had been added

- timeFrameMultiplier() timeframe multiplier had been added to the library

- timeframe period value fixed

- Changed timezone multiplier

- Changed VWMA Percent values

bytimeLibrary "bytime"

TODO: to do something at the specified time.

////Return =>> ht = hour , mt = minute , st = second ,Dt = Day, Mt = month, Yt = year , dateTime = full time format./////////////

Note : Remember to always add import when you call our library and change Gtime() to Timeset.Gtime() is used to access internal data.

import hapharmonic/bytime/1 as Timeset

=Timeset.Gtime()

/////////////Set a time to trigger an alert./////////////

ck = false

///hour : minute : second

if ht == TH and mt == TM and st == TS

//some action

//...

//.

ck := true

Gtime()

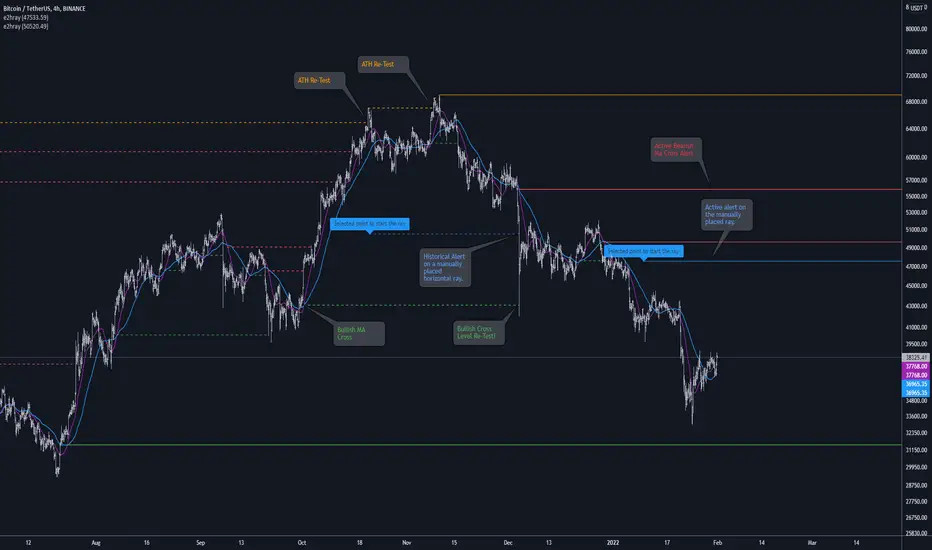

[e2] Drawing Library :: Horizontal Ray█ OVERVIEW

Library "e2hray"

A drawing library that contains the hray() function, which draws a horizontal ray/s with an initial point determined by a specified condition. It plots a ray until it reached the price. The function let you control the visibility of historical levels and setup the alerts.

█ HORIZONTAL RAY FUNCTION

hray(condition, level, color, extend, hist_lines, alert_message, alert_delay, style, hist_style, width, hist_width)

Parameters:

condition : Boolean condition that defines the initial point of a ray

level : Ray price level.

color : Ray color.

extend : (optional) Default value true, current ray levels extend to the right, if false - up to the current bar.

hist_lines : (optional) Default value true, shows historical ray levels that were revisited, default is dashed lines. To avoid alert problems set to 'false' before creating alerts.

alert_message : (optional) Default value string(na), if declared, enables alerts that fire when price revisits a line, using the text specified

alert_delay : (optional) Default value int(0), number of bars to validate the level. Alerts won't trigger if the ray is broken during the 'delay'.

style : (optional) Default value 'line.style_solid'. Ray line style.

hist_style : (optional) Default value 'line.style_dashed'. Historical ray line style.

width : (optional) Default value int(1), ray width in pixels.

hist_width : (optional) Default value int(1), historical ray width in pixels.

Returns: void

█ EXAMPLES

• Example 1. Single horizontal ray from the dynamic input.

//@version=5

indicator("hray() example :: Dynamic input ray", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

inputTime = input.time(timestamp("20 Jul 2021 00:00 +0300"), "Date", confirm = true)

inputPrice = input.price(54, 'Price Level', confirm = true)

e2draw.hray(time == inputTime, inputPrice, color.blue, alert_message = 'Ray level re-test!')

var label mark = label.new(inputTime, inputPrice, 'Selected point to start the ray', xloc.bar_time)

• Example 2. Multiple horizontal rays on the moving averages cross.

//@version=5

indicator("hray() example :: MA Cross", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

float sma1 = ta.sma(close, 20)

float sma2 = ta.sma(close, 50)

bullishCross = ta.crossover( sma1, sma2)

bearishCross = ta.crossunder(sma1, sma2)

plot(sma1, 'sma1', color.purple)

plot(sma2, 'sma2', color.blue)

// 1a. We can use 2 function calls to distinguish long and short sides.

e2draw.hray(bullishCross, sma1, color.green, alert_message = 'Bullish Cross Level Broken!', alert_delay = 10)

e2draw.hray(bearishCross, sma2, color.red, alert_message = 'Bearish Cross Level Broken!', alert_delay = 10)

// 1b. Or a single call for both.

// e2draw.hray(bullishCross or bearishCross, sma1, bullishCross ? color.green : color.red)

• Example 3. Horizontal ray at the all time highs with an alert.

//@version=5

indicator("hray() example :: ATH", overlay = true)

import e2e4mfck/e2hray/1 as e2draw

var float ath = 0, ath := math.max(high, ath)

bool newAth = ta.change(ath)

e2draw.hray(nz(newAth ), high , color.orange, alert_message = 'All Time Highs Tested!', alert_delay = 10)

TAExtLibrary "TAExt"

Indicator functions can be used in other indicators and strategies. This will be extended by time with indicators I use in my strategies and studies.

atrwo(length, stdev_length, stdev_mult) ATR without outliers

Parameters:

length : The length of the ATR

stdev_length : The length of the standard deviation, used for detecting outliers

stdev_mult : The multiplier of the standard deviation, used for detecting outliers

Returns: The ATR value

atrwma(src, period, type, atr_length, stdev_length, stdev_mult) ATR without outlier weighted moving average

Parameters:

src : The source of the moving average

period : The period of the moving average

type : The type of the moving average, possible values: SMA, EMA, RMA

atr_length : The length of the ATR

stdev_length : The length of the standard deviation, used for detecting outliers

stdev_mult : The multiplier of the standard deviation, used for detecting outliers

Returns: The moving average value

jma(src, period, phase, power) Jurik Moving Average

Parameters:

src : The source of the moving average

period : The period of the moving average calculation

phase : The phase of jurik MA calculation (-100..100)

power : The power of jurik MA calculation

Returns: The Jurik MA series

anyma(src, period, type, offset, sigma, phase, power) Moving Average by type

Parameters:

src : The source of the moving average

period : The period of the moving average calculation

type : The type of the moving average

offset : Used only by ALMA, it is the ALMA offset

sigma : Used only by ALMA, it is the ALMA sigma

phase : The phase of jurik MA calculation (-100..100)

power : The power of jurik MA calculation

Returns: The moving average series

wae(macd_src, macd_fast_length, macd_slow_length, macd_sensitivity, bb_base_src, bb_upper_src, bb_lower_src, bb_length, bb_mult, dead_zone_length, dead_zone_mult) Waddah Attar Explosion (WAE)

Parameters:

macd_src : The source series used by MACD

macd_fast_length : The fast MA length of the MACD

macd_slow_length : The slow MA length of the MACD

macd_sensitivity : The MACD diff multiplier

bb_base_src : The source used by stdev

bb_upper_src : The source used by the upper Bollinger Band

bb_lower_src : The source used by the lower Bollinger Band

bb_length : The lenth for Bollinger Bands

bb_mult : The multiplier for Bollinger Bands

dead_zone_length : The ATR length for dead zone calculation

dead_zone_mult : The ATR multiplier for dead zone

Returns:

ssl(length, high_src, low_src) Semaphore Signal Level channel (SSL)

Parameters:

length : The length of the moving average

high_src : Source of the high moving average

low_src : Source of the low moving average

Returns:

adx(atr_length, di_length, adx_length, high_src, low_src, atr_ma_type, di_ma_type, adx_ma_type) Average Directional Index + Direction Movement Index (ADX + DMI)

Parameters:

atr_length : The length of ATR

di_length : DI plus and minus smoothing length

adx_length : ADX smoothing length

high_src : Source of the high moving average

low_src : Source of the low moving average

atr_ma_type : MA type of the ATR calculation

di_ma_type : MA type of the DI calculation

adx_ma_type : MA type of the ADX calculation

Returns:

FunctionCosineSimilarityLibrary "FunctionCosineSimilarity"

Cosine Similarity method.

function(sample_a, sample_b) Measure the similarity of 2 vectors.

Parameters:

sample_a : float array, values.

sample_b : float array, values.

Returns: float.

diss(cosim) Dissimilarity helper function.

Parameters:

cosim : float, cosine similarity value (0 > 1)

Returns: float

historicalrangeLibrary "historicalrange"

Library provices a method to calculate historical percentile range of series.

hpercentrank(source) calculates historical percentrank of the source

Parameters:

source : Source for which historical percentrank needs to be calculated. Source should be ranging between 0-100. If using a source which can beyond 0-100, use short term percentrank to baseline them.

Returns: pArray - percentrank array which contains how many instances of source occurred at different levels.

upperPercentile - percentile based on higher value

lowerPercentile - percentile based on lower value

median - median value of the source

max - max value of the source

distancefromath(source) returns stats on historical distance from ath in terms of percentage

Parameters:

source : for which stats are calculated

Returns: percentile and related historical stats regarding distance from ath

distancefromma(maType, length, source) returns stats on historical distance from moving average in terms of percentage

Parameters:

maType : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length : Moving Average Length

source : for which stats are calculated

Returns: percentile and related historical stats regarding distance from ath

bpercentb(source, maType, length, multiplier, sticky) returns percentrank and stats on historical bpercentb levels

Parameters:

source : Moving Average Source

maType : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length : Moving Average Length

multiplier : Standard Deviation multiplier

sticky : - sticky boundaries which will only change when value is outside boundary.

Returns: percentile and related historical stats regarding Bollinger Percent B

kpercentk(source, maType, length, multiplier, useTrueRange, sticky) returns percentrank and stats on historical kpercentk levels

Parameters:

source : Moving Average Source

maType : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length : Moving Average Length

multiplier : Standard Deviation multiplier

useTrueRange : - if set to false, uses high-low.

sticky : - sticky boundaries which will only change when value is outside boundary.

Returns: percentile and related historical stats regarding Keltener Percent K

dpercentd(useAlternateSource, alternateSource, length, sticky) returns percentrank and stats on historical dpercentd levels

Parameters:

useAlternateSource : - Custom source is used only if useAlternateSource is set to true

alternateSource : - Custom source

length : - donchian channel length

sticky : - sticky boundaries which will only change when value is outside boundary.

Returns: percentile and related historical stats regarding Donchian Percent D

oscillator(type, length, shortLength, longLength, source, highSource, lowSource, method, highlowLength, sticky) oscillator - returns Choice of oscillator with custom overbought/oversold range

Parameters:

type : - oscillator type. Valid values : cci, cmo, cog, mfi, roc, rsi, stoch, tsi, wpr

length : - Oscillator length - not used for TSI

shortLength : - shortLength only used for TSI

longLength : - longLength only used for TSI

source : - custom source if required

highSource : - custom high source for stochastic oscillator

lowSource : - custom low source for stochastic oscillator

method : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength : - length on which highlow of the oscillator is calculated

sticky : - overbought, oversold levels won't change unless crossed

Returns: percentile and related historical stats regarding oscillator

ZxLibraryLibrary "ZxLibrary"

ZxLibrary is an easy with more than 130 Indicators and more than 60 Candlestick Patterns.

dc_taAdaptive technical indicators are importants in a non stationary market, the ability to adapt to a situation can boost the efficiency of your strategy. A lot of methods have been proposed to make technical indicators "smarters", the dominant cycle tuned indicators are one of them which are based on J.F.Ehlers theory. Here is a collections of algorithms to calculate dominant cycles. ENJOY!

Library "dc_ta"

bton()

EhlersHoDyDC()

EhlersPhAcDC()

EhlersDuDiDC()

EhlersCycPer()

EhlersCycPer2()

EhlersBPZC()

EhlersAutoPer()

EhlersHoDyDCE()

EhlersPhAcDCE()

EhlersDuDiDCE()

EhlersDFTDC()

EhlersDFTDC2()

ArrayOperationsLibrary "ArrayOperations"

Array element wise basic operations.

add(sample_a, sample_b) Adds sample_b to sample_a and returns a new array.

Parameters:

sample_a : values to be added to.

sample_b : values to add.

Returns: array with added results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

subtract(sample_a, sample_b) Subtracts sample_b from sample_a and returns a new array.

sample_a : values to be subtracted from.

sample_b : values to subtract.

Returns: array with subtracted results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

multiply(sample_a, sample_b) multiply sample_a by sample_b and returns a new array.

sample_a : values to multiply.

sample_b : values to multiply with.

Returns: array with multiplied results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

divide(sample_a, sample_b) Divide sample_a by sample_b and returns a new array.

sample_a : values to divide.

sample_b : values to divide with.

Returns: array with divided results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

power(sample_a, sample_b) power sample_a by sample_b and returns a new array.

sample_a : values to power.

sample_b : values to power with.

Returns: float array with power results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

remainder(sample_a, sample_b) Remainder sample_a by sample_b and returns a new array.

sample_a : values to remainder.

sample_b : values to remainder with.

Returns: array with remainder results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

equal(sample_a, sample_b) Check element wise sample_a equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

not_equal(sample_a, sample_b) Check element wise sample_a not equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

over_or_equal(sample_a, sample_b) Check element wise sample_a over or equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

under_or_equal(sample_a, sample_b) Check element wise sample_a under or equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

over(sample_a, sample_b) Check element wise sample_a over sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

under(sample_a, sample_b) Check element wise sample_a under sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

and_(sample_a, sample_b) Check element wise sample_a and sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

or_(sample_a, sample_b) Check element wise sample_a or sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

all(sample) Check element wise if all numeric samples are true (!= 0).

sample : values to check.

Returns: int.

any(sample) Check element wise if any numeric samples are true (!= 0).

sample : values to check.

Returns: int.