Riz Coloured MACDThis is a souped up common or garden MACD . The Histogram is coloured giving a clear visual representation of where we are UpTicking or DownTicking on the Histogram to help support trading decisions.

When colour changes from pink to green market is bullish , and visa versa.

Very useful as a supporting indicator to confirm other strategies, or even as a standalone strategy to some extent.

Alerts are enabled by converting script from a Strategy to a Study, see comments in code.

Centered Oscillators

Psychological line Backtest Psychological line (PSY), as an indicator, is the ratio of the number of

rising periods over the total number of periods. It reflects the buying

power in relation to the selling power.

If PSY is above 50%, it indicates that buyers are in control. Likewise,

if it is below 50%, it indicates the sellers are in control. If the PSY

moves along the 50% area, it indicates balance between the buyers and

sellers and therefore there is no direction movement for the market.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Prime Number Oscillator Backtest Determining market trends has become a science even though a high number or people

still believe it’s a gambling game. Mathematicians, technicians, brokers and investors

have worked together in developing quite several indicators to help them better understand

and forecast market movements.

Developed by Modulus Financial Engineering Inc., the prime number oscillator indicates the

nearest prime number, be it at the top or the bottom of the series, and outlines the

difference between that prime number and the respective series.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Ichimoku + Daily-Candle_X + Gaussian Smooth + MacDI take no credit for this script. I swapped the Hull moving average used the original program made by SeaSide420 for a gaussian smooth function made by jjaskulowski. This script seems to consistently outperform the original strategy for the long condition. I'm mainly focused on crypto, so I removed the "short" option because most crypto exchanges don't have this function as of right now.

Heikin-Ashi Strategy + backtest rangeThis is Heikin-Ashi Strategy + Backtest range that I think useful for BTCUSD pair.

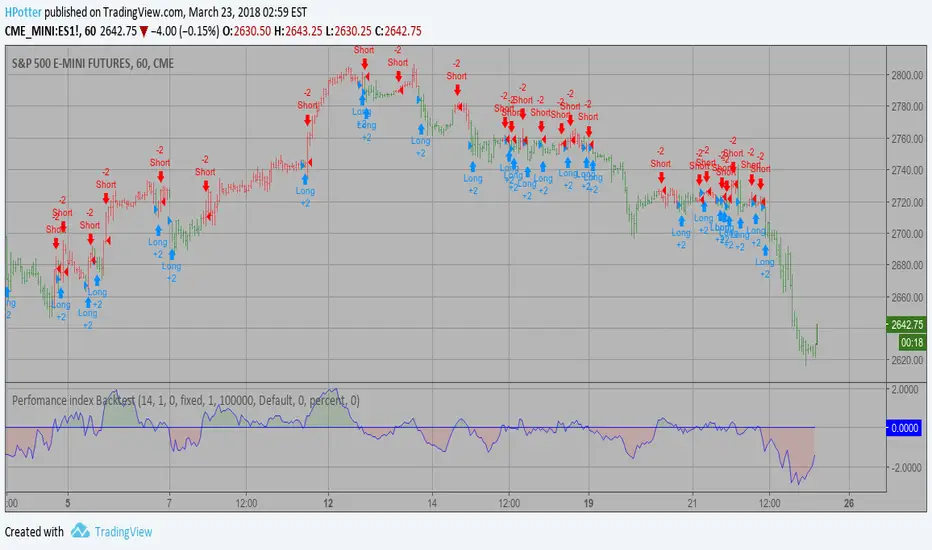

Perfomance index Backtest The Performance indicator or a more familiar term, KPI (key performance indicator),

is an industry term that measures the performance. Generally used by organizations,

they determine whether the company is successful or not, and the degree of success.

It is used on a business’ different levels, to quantify the progress or regress of a

department, of an employee or even of a certain program or activity. For a manager

it’s extremely important to determine which KPIs are relevant for his activity, and

what is important almost always depends on which department he wants to measure the

performance for. So the indicators set for the financial team will be different than

the ones for the marketing department and so on.

Similar to the KPIs companies use to measure their performance on a monthly, quarterly

and yearly basis, the stock market makes use of a performance indicator as well, although

on the market, the performance index is calculated on a daily basis. The stock market

performance indicates the direction of the stock market as a whole, or of a specific stock

and gives traders an overall impression over the future security prices, helping them decide

the best move. A change in the indicator gives information about future trends a stock could

adopt, information about a sector or even on the whole economy. The financial sector is the

most relevant department of the economy and the indicators provide information on its overall

health, so when a stock price moves upwards, the indicators are a signal of good news. On the

other hand, if the price of a particular stock decreases, that is because bad news about its

performance are out and they generate negative signals to the market, causing the price to go

downwards. One could state that the movement of the security prices and consequently, the movement

of the indicators are an overall evaluation of a country’s economic trend.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Chande Forecast Oscillator Backtest The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

SB_CM_MacD_Ult_MTFThis strategy places the order based on the MACD signal.

Original Indicator: MacD Custom Indicator-Multiple Time Frame+All Available Options! by ChrisMoody

Link to the Indicator:

If your risk appetite is high you can replace the first statement with the below statement:

strategy(title="SB_CM_MacD_Ult_MTF", shorttitle="SB_CM_MacD_Ult_MTF", default_qty_type = strategy.percent_of_equity, default_qty_value = 100, pyramiding = 5)

You can check for repainting. Did not check for that.

Message if you think of any modifications/ enhancements/ any opportunities. :)

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

SB_Elder Impulse SystemThe strategy is based on LazyBear's Elder Impulse System

Strategy(in layman terms):

Long: When the green bar in the Elder Impulse System's indicator shows up

Short: When the red bar in the Elder Impulse System's indicator shows up

Close trade/Profit booking: When the blue bar in the Elder Impulse System's indicator shows up

Original Idea:

Message in the script if you think of any modifications/ enhancements.

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

SB_CCI coded OBV StrategyStrategy-

Buy Order: Previous obv value is green and obv_cci coded line crosses over ema line

Sell Order: Previous obv value is red and obv_cci coded line crosses under ema line.

Original Idea:

Preferable for day/week intervals.

For Tips to continue :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Fractal Chaos Oscillator Backtest The value of Fractal Chaos Oscillator is calculated as the difference between

the most subtle movements of the market. In general, its value moves between

-1.000 and 1.000. The higher the value of the Fractal Chaos Oscillator, the

more one can say that it follows a certain trend – an increase in prices trend,

or a decrease in prices trend.

Being an indicator expressed in a numeric value, traders say that this is an

indicator that puts a value on the trendiness of the markets. When the FCO reaches

a high value, they initiate the “buy” operation, contrarily when the FCO reaches a

low value, they signal the “sell” action. This is an excellent indicator to use in

intra-day trading.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Trend'n Stuff_(MA's and Trix)It's a simple trend following system. Play with the setups. Works best on 30min and up timeframes. Look at the code for better understanding.

Smoothened Williams Accumulation/Distribution (Williams AD) Accumulation is a term used to describe a market controlled by buyers;

whereas distribution is defined by a market controlled by sellers.

Williams recommends trading this indicator based on divergences:

Distribution of the security is indicated when the security is making

a new high and the A/D indicator is failing to make a new high. Sell.

Accumulation of the security is indicated when the security is making

a new low and the A/D indicator is failing to make a new low. Buy.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

LFH/ Long positions using MACD histogram, long EMA and short EMADisclaimer: I'm a noob.

Hey there!

I'm trying to implement a script which enter market long position when long EMA crossover short EMA and MACD histogram is positive and histogram at T time is lesser than histogram at T-1.

And when short EMA crossover long EMA, plus MACD histogram is negative and histogram at T is greater than histogram at T-1, I want the script to exit market long position.

Now, I have something pretty close to what I am looking for. What I am missing and can't figure out yet is:

How to moderate entries, ie. I would like it to enter positions when trends are really interesting not just every time the conditions are fulfilled (same for exits) as there is way too much positions

I need to find a way to exit appropriated positions.

Parabolic SAR Strategy with good parametersI tested it on EURUSD with 2% profit:

Set input parameters like here: screenshots.firefox.com

Williams Accumulation/Distribution (Williams AD) Backtest Accumulation is a term used to describe a market controlled by buyers;

whereas distribution is defined by a market controlled by sellers.

Williams recommends trading this indicator based on divergences:

Distribution of the security is indicated when the security is making

a new high and the A/D indicator is failing to make a new high. Sell.

Accumulation of the security is indicated when the security is making

a new low and the A/D indicator is failing to make a new low. Buy.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

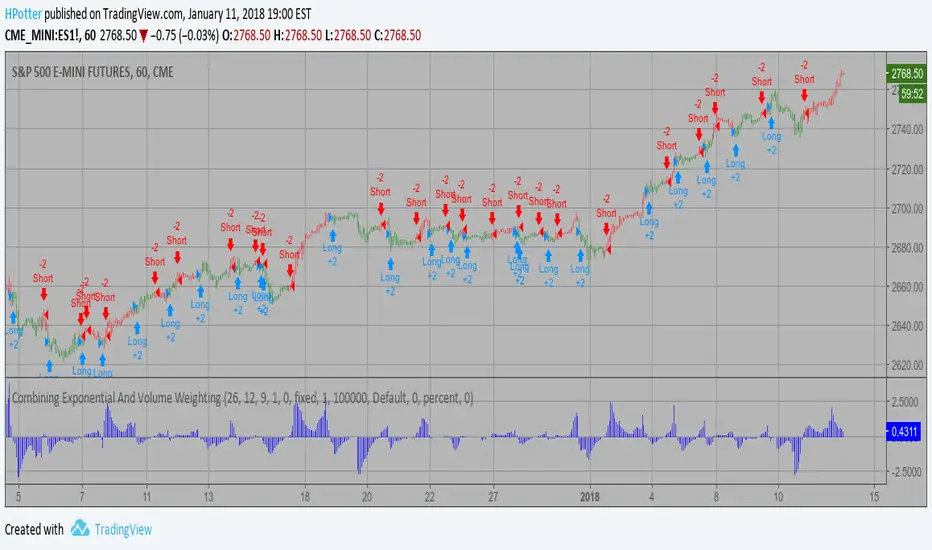

Combining Exponential And Volume Weighting Backtest The related article is copyrighted material from Stocks & Commodities 2009 Oct

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

MovROC (KST indicator) Backtes This indicator really is the KST indicator presented by Martin Pring.

the KST indicator is a weighted summed rate of change oscillator that

is designed to identify meaningful turns. Various smoothed rate of change

indicators can be combined to form different measurements of cycles.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Money Flow Indicator (Chaikin Oscillator) Indicator plots Money Flow Indicator (Chaikin). This indicator looks

to improve on Larry William's Accumulation Distribution formula that

compared the closing price with the opening price. In the early 1970's,

opening prices for stocks stopped being transmitted by the exchanges.

This made it difficult to calculate Williams' formula. The Chaikin

Oscillator uses the average price of the bar calculated as follows

(High + Low) /2 instead of the Open.

The indicator subtracts a 10 period exponential moving average of the

AccumDist function from a 3 period exponential moving average of the

AccumDist function.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Ichimoku Kinko Hyo + HULL-MA_X + MacDThe Ichimoku Kinko Hyo system includes five kinds of signal, of which this strategy uses the most recent of ones i.e. Tenkan Sen / Kijun Sen Cross and price crosses the Kijun Sen. As the Chikou Span, Senkou Span A and Senkou Span B are shifted into the past/future, the trigger signals will be only be used for visual confirmation and not part of the strategy.

The Tenkan Sen, also known as the Turning or Conversion line, is a moving average of the highest high and lowest low over the last 9 periods in this strategy.

The Kijun Sen, also known as the Standard or Base line, is a moving average of the highest high and lowest low over the last 24 periods in this strategy.

The Chikou Span, also known as the Lagging line, is the closing price plotted 24 periods behind in this strategy.

The Senkou Span A, also known as the 1st leading line, is a moving average of the Tenkan Sen and Kijun Sen and is plotted 24 periods ahead in this strategy.

The Senkou Span B, also known as the 2nd leading line, is a moving average of the highest high and lowest low over the last 51 trading days is plotted 24 periods ahead in this strategy.

Moving average convergence divergence (MaCD) is a trend-following momentum indicator that shows the relationship between two moving averages of prices. The MaCD is calculated in this strategy by subtracting the 24-day exponential moving average (EMA) from the 12-day EMA. A nine-day EMA of the MACD, called the "signal line", aMaCD in this case, is then plotted on top of the MaCD. In this strategy, MaCD/ aMaCD Cross is functioning as a trigger for buy and sell signals.

As with most technical analysis methods, Ichimoku is likely to produce frequent conflicting signals in non-trending markets, So in addition to Ichimoku Kinko Hyo, the Hull MA is popular amongst some day traders, as the indicator which in combination with MaCD attempts to give an accurate signal by eliminating lags and improving the smoothness of the line.

Alan Hull, developed this moving average indicator and hence it’s called the Hull MA.

Now, let’s dissect how the Hull moving average is calculated.

The Hull MA involves the weighted moving average (WMA) in its calculation.

First, calculate the WMA with period (n / 2) and multiply this by 2. Remember ‘n’ is the time period configurable based on the trader’s requirement. The default setting is 12 periods in this strategy, fast Hull MA crossing slow Hull MA will generate a circle on charts.

Second, calculate the WMA for period “n” and subtract if from the first step. Thirdly, calculate the weighted moving average with period sqrt (n) using the data from the second step. You can take a look at the below formula:

Hull MA= WMA (2*WMA (n/2) − WMA (n)), sqrt (n))

The Hull MA Cross in combination with Tenkan Sen / Kijun Sen Cross and MaCD tries to give an accurate signal by eliminating lags and improve the smoothness of price activity. Please note that price trends can and do change often, so your readings of the charts and this trading system should be probabilistic, rather than predictive.

MACD Crossover Backtest MACD – Moving Average Convergence Divergence. The MACD is calculated

by subtracting a 26-day moving average of a security's price from a

12-day moving average of its price. The result is an indicator that

oscillates above and below zero. When the MACD is above zero, it means

the 12-day moving average is higher than the 26-day moving average.

This is bullish as it shows that current expectations (i.e., the 12-day

moving average) are more bullish than previous expectations (i.e., the

26-day average). This implies a bullish, or upward, shift in the supply/demand

lines. When the MACD falls below zero, it means that the 12-day moving average

is less than the 26-day moving average, implying a bearish shift in the

supply/demand lines.

A 9-day moving average of the MACD (not of the security's price) is usually

plotted on top of the MACD indicator. This line is referred to as the "signal"

line. The signal line anticipates the convergence of the two moving averages

(i.e., the movement of the MACD toward the zero line).

Let's consider the rational behind this technique. The MACD is the difference

between two moving averages of price. When the shorter-term moving average rises

above the longer-term moving average (i.e., the MACD rises above zero), it means

that investor expectations are becoming more bullish (i.e., there has been an

upward shift in the supply/demand lines). By plotting a 9-day moving average of

the MACD, we can see the changing of expectations (i.e., the shifting of the

supply/demand lines) as they occur.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.