Portfolio TableA tool to manage your invested assets (stocks, crypto currencies, ...).

- Show profit of every asset as well as the total profit.

- Show/hide a bought price line on the chart if the current selected ticker is on your portfolio.

Portfolio management

Trade Information BoxThis script is a TradingView indicator written in Pine Script. It creates an information box on the chart that provides details related to a trade, including entry plan, stop loss, take profit, and position sizing. Let's break down the components:

1. **Input Parameters:**

- `entryPrice`: The entry price for the trade. This is a manually input value, and the default is set to 100.

- `smaLength`: The length parameter for the Simple Moving Average (SMA) calculation. Default is set to 20.

- `smaMultiplier`: The multiplier used to calculate the stop loss and take profit based on the SMA. Default is set to 1.5.

- `riskPerTradePercent`: The percentage of risk per trade as a decimal. Default is set to 2.

- `capital`: The total capital available for trading. Default is set to 10,000.

2. **Calculations:**

- `smaValue`: Calculates the Simple Moving Average based on the closing prices with the specified length (`smaLength`).

- `stopLoss`: Calculates the stop loss level by subtracting the product of the SMA value and the multiplier (`smaMultiplier`) from the entry price.

- `takeProfit`: Calculates the take profit level by adding the product of the SMA value and the multiplier (`smaMultiplier`) to the entry price.

- `riskPerTrade`: Calculates the actual risk amount per trade based on the specified percentage of capital.

- `maxQuantity`: Calculates the maximum quantity of shares or contracts that can be bought based on the specified risk percentage and the difference between entry price and stop loss.

- `buyValue`: Calculates the total value of the position based on the maximum quantity and entry price.

3. **Info Box:**

- `labelBox`: Defines a label box on the chart.

- `label.set_xy(labelBox, bar_index, high)`: Sets the position of the label box to the high of the current bar.

- `label.set_text(...)`: Defines the text content of the label box, providing details on the trading plan, entry, stop loss, take profit, capital, risk per trade, maximum quantity, and buy value.

Overall, this indicator is designed to provide traders with key information related to their trade plan, risk management, and position sizing directly on the chart. The displayed values are formatted with three decimal places for clarity.

CAPM Calculator [TrendX_]CAPM calculator is a powerful tool that helps find the cost of equity, which is the minimum return that shareholders require to invest in a company.

With the CAPM calculator, you can assess how well your trading strategy performs compared to the market. The goal of your strategy is to earn higher returns than what you would get by investing in the market with the same level of risk. This is called the risk-adjusted cost of capital, and it represents the minimum return that you should accept for your investment.

USAGE

A simple way to measure this is to compare the Compound annual growth rate (CAGR) of the trading strategy with the “Compound CAPM”, which is the CAGR of investing in the market with the same beta as the strategy.

If the trading strategy has a higher CAGR than the “Compound CAPM”, it means that it has outperformed the market on a risk-adjusted basis.

This is a sign of an effective trading strategy.

DISCLAIMER

The results achieved in the past are not all reliable sources of what will happen in the future. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur.

Therefore, you should always exercise caution and judgment when making decisions based on past performance.

Custom Lot Size Table with Calculator This TradingView script, is designed to empower traders with precise risk management tools. It allows for input of key parameters such as account balance, desired risk percentage, and a range for stop-loss pips, ensuring that the lot sizes calculated are perfectly aligned with risk tolerances.

The script dynamically adjusts the table size based on the user's input, offering a clear and concise visualization of the appropriate lot sizes..

Anchored Chandelier ExitThe Chandelier Exit is a popular tool among traders used to help determine appropriate stop loss levels. Originally developed by Chuck LeBeau, the Chandelier Exit takes into account market volatility and adjusts the stop loss level dynamically. This indicator builds upon the original Chandelier Exit by allowing the trader to select an anchor date or starting point for the indicator to begin calculating from.

The Original Chandelier Exit

Before we get into the details of the Anchored Chandelier Exit, let's review the original. Essentially a dynamic ATR stop loss, the Chandelier Exit provides a trailing stop that moves higher or lower based on volatility.

The Chandelier Exit is calculated based on the following criteria:

🔶ATR - The ATR is used to measure the volatility of a security over a lookback period. The ATR length determines the number of bars to consider when calculating the average true range. The shorter the length, the more responsive the level will be.

🔶ATR Multiplier - The default multiplier is set to 3. This is used to determine the sensitivity of the Chandelier Exit. The higher the ATR multiplier the wider the stop levels will be. A lower multiplier will tighten stop levels.

🔶Highest / Lowest Points - Determine the highest high (bullish trade) or lowest low (bearish trade) during the lookback period. The default length is 22 bars.

Calculating the Chandelier Exit

Bullish trades - Highest High - ATR * Multiplier

Bearish trades - Lowest Low + ATR * Multiplier

The Anchored Chandelier Exit

The Anchored Chandelier Exit is a new twist on the original, allowing traders to adapt their stop loss levels based on specific market events, levels or bars.

Similar to the original, traders can select the ATR length and multiplier, however, the high or low from which the ATR is subtracted or added is first determined at the anchor bar.

As new bars form, the indicator checks for the previous high/low to be breached. If the high or low is exceeded, the highest/lowest point is updated and the Chandelier Exit is recalculated.

When the indicator is first loaded to your chart, it will ask you to select an anchor bar and choose the bias for the trade.

A bullish (long) bias trade will plot the Chandelier Exit below price action, while a bearish (short) bias trade will plot the Chandelier Exit above price action.

Indicator Features

🔶Custom Start Date

🔶Bullish or Bearish Bias

🔶Selectable ATR Length & Multiplier

🔶Custom Colors

🔶Exit With Close or Wicks

🔶Exit Alerts

With careful parameter optimization, the Anchored Chandelier Exit can be a useful tool for helping traders manage risk based on market volatility.

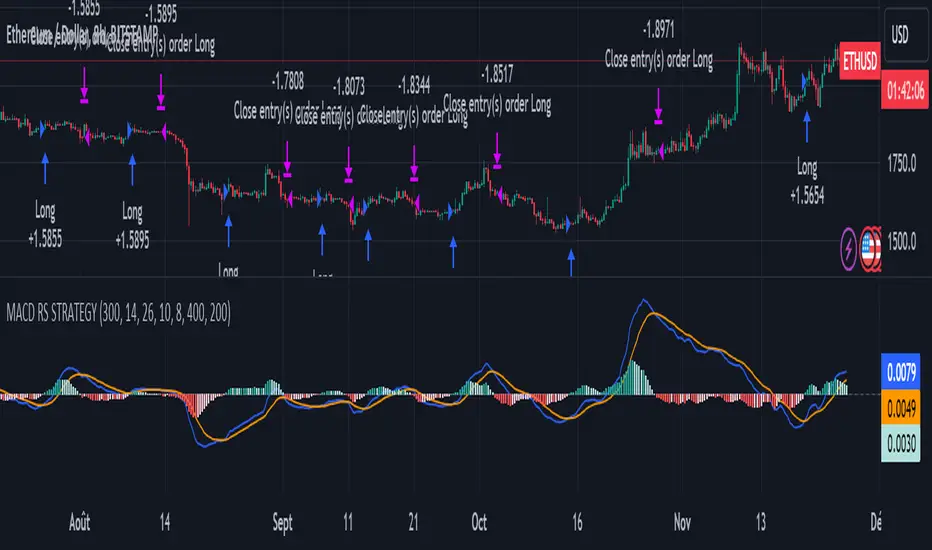

MACD of Relative Strenght StrategyMACD Relative Strenght Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators: MACD and Relative Strenght (RS). By coupling them, we obtain powerful buy signals. In fact, the special feature of this strategy is that it creates an indicator from an indicator. Thus, we construct a MACD whose source is the value of the RS. The strategy only takes buy signals, ignoring SHORT signals as they are mostly losers. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RELATIVE STRENGHT :

RS is an indicator that measures the anomaly between momentum and the assumption of market efficiency. It is used by professionals and is one of the most robust indicators. The idea is to own assets that do better than average, based on their past performance. We calculate RS using this formula :

RS = close/highest_high(RS_Length)

Where highest_high(RS_Length) = highest value of the high over a user-defined time period (which is the RS_Length).

We can thus situate the current price in relation to its highest price over this user-defined period.

MACD (Moving Average Convergence - Divergence) :

This is one of the best-known indicators, measuring the distance between two exponential moving averages : one fast and one slower. A wide distance indicates fast momentum and vice versa. We'll plot the value of this distance and call this line macdline. The MACD uses a third moving average with a lower period than the first two. This last moving average will give a signal when it crosses the macdline. It is therefore constructed using the values of the macdline as its source.

It's important to note that the first two MAs are constructed using RS values as their source. So we've just built an indicator of an indicator. This kind of method is very powerful because it is rarely used and brings value to the strategy.

PARAMETERS :

RS Length : Relative Strength length i.e. the number of candles back to find the highest high and compare the current price with this high. Default is 300.

MACD Fast Length : Relative Strength fast EMA length used to plot the MACD. Default is 14.

MACD Slow Length : Relative Strength slow EMA length used to plot the MACD. Default is 26.

MACD Signal Smoothing : Macdline SMA length used to plot the MACD. Default is 10.

Max risk per trade (in %) : The maximum loss a trade can incur (in percentage of the trade value). Default is 8%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD in 8h timeframe with the parameters set by default.

ENTER RULES :

The entry rules are very simple : we open a long position when the MACD value turns positive. You are therefore LONG when the MACD is green.

EXIT RULES :

We exit a position (whether losing or winning) when the MACD becomes negative, i.e. turns red.

RISK MANAGEMENT :

This strategy can incur losses, so it's important to manage our risks well. If the position is losing and has incurred a loss of -8%, our stop loss is activated to limit losses.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

Ceres Trader Position and Risk Management ToolNOTE: It won't properly scale until you enter an entry point that is located on the chart. It's a feature not a bug. After that, you will see the entry, s/l, and target price lines properly displayed on the chart.

The "Ceres Trader Position and Risk Management Tool" is a comprehensive indicator designed for TradingView, meticulously crafted for traders who prioritize effective risk management and clear position visualization. This tool seamlessly integrates with your trading strategy, providing crucial information about your trades directly on your chart.

Key Features:

Position Type Visualization: Displays long or short positions with distinct color-coded lines and boxes for easy recognition.

Entry, Stop Loss, and Target Levels: Visual markers for entry price, stop loss, and target price, enabling you to track your trade setup at a glance.

Risk Assessment: Calculates and displays the amount at risk based on the stop loss distance and the percentage of risk capital.

Profit Potential: Shows the potential profit in dollar terms if the target is reached, helping you understand the reward prospects of your trade.

Reward to Risk Ratio: Indicates the ratio of potential reward to risk, an essential metric for evaluating the efficiency of your trade setup.

Current P&L Tracking: Continuously updates the open profit and loss based on the current market price, giving you real-time insight into your trade's performance.

Customizable Risk and Reward Boxes: Allows personalization of the risk and reward zones with color options, enhancing chart clarity and visual appeal.

How to Use:

Setting Up Your Trade:

Input your trade details including position type (long or short), entry price, risk capital, risk percentage, reward-risk ratio, and stop loss distance.

Visualize Your Trade:

The tool will automatically plot the entry, stop loss, and target prices on the chart.

Risk and reward areas will be highlighted with customizable color boxes.

Monitor Your Risk and Reward:

View the amount risked and potential profit in dollar terms directly on the chart.

Keep track of the reward to risk ratio to assess trade efficiency.

Stay Informed of Real-time Performance:

The current P&L of your open position will be updated in real-time, helping you make informed decisions.

This tool is ideal for traders who follow disciplined risk management practices and want to keep essential trade information easily accessible. With the "Ceres Trader Position and Risk Management Tool," you are equipped to make strategic trading decisions backed by clear visual cues and critical data.

Capital Accumulation Plan (CAP) Simulator 2.0Description:

This indicator serves as a simulation tool for the Capital Accumulation Plan (CAP). The CAP is an investment strategy involving regular contributions of a fixed amount at consistent intervals, regardless of market fluctuations. This simulator allows you to visualize how your invested capital might grow over time, considering a fixed monthly investment in a given financial instrument.

How to Use:

Customize the monthly investment amount, the day of the month for the investment, and the simulation period. Also, input the percentage of taxation on potential dividends and the Total Expense Ratio (TER) of the financial instrument. The indicator calculates the portfolio value over time, the invested capital, and the average cost. If applicable, it also calculates the dividend amounts over time and the corresponding taxes to be paid.

The indicator displays how these metrics would change over time following the PAC strategy.

Important Notes:

Apply exclusively to the daily chart; a fix for the chosen day absence will be implemented shortly.

EntryPrice Gain&Loss IndicatorThis indicator takes (1) an entry price or average position price and (2) position size (denominator) to calculate current gain or loss and returns those as well as the position change in percent. It will also draw into the Chart and show relevant data in a table.

It is mainly supposed to help tracking an (average) spot position easily.

It is recommended to switch it to invisible when switching to other charts.

You can also use several instances of the indicator to track your positions in different assets.

Features:

- table position and text size can be adjusted

- colors can be changed

(recommending 25% opacity for plot backgrounds)

- several instances possible

(recommended to tuen indicator invisible when switching to other charts or analyzing

Version 1.0

Trailing stopHi all!

This script helps to alert you when a trailing stop is hit. More specifically it alerts you when the low of the candle crosses below your trailing stop. A trailing stop follows a price positive movements. It raises your stop when price goes up, but keeps it at the same level if price goes down, so it "locks" in your profit. You define your long entry bar and choose one of the following methods for the stop:

ATR

The Average True Range (ATR) is popular to trail stops. The trailing stop is raised by the low minus the ATR (times a factor that can be set under the settings for ATR).

EMA

The Exponential Moving Average (EMA) can be used to trail your stop. When the low goes below the EMA an alert is sent about the stop. Its length can be set in the settings.

SMA

The Simple Moving Average (SMA) can be used to trail your stop. When the low goes below the SMA an alert is sent about the stop. Its length can be set in the settings.

Source

An external source can be useful as a stop signal. You can use this option that will stop you out when the signal returns anything else than "na". E.g. if you want a stop when KivancOzbilgic script "SuperTrend" () turns red, you set the source to "Supertrend: Down Trend". This option will not draw pretty things on the chart, but it will alert you!

Please note that this is for long entries only.

Best of trading luck!

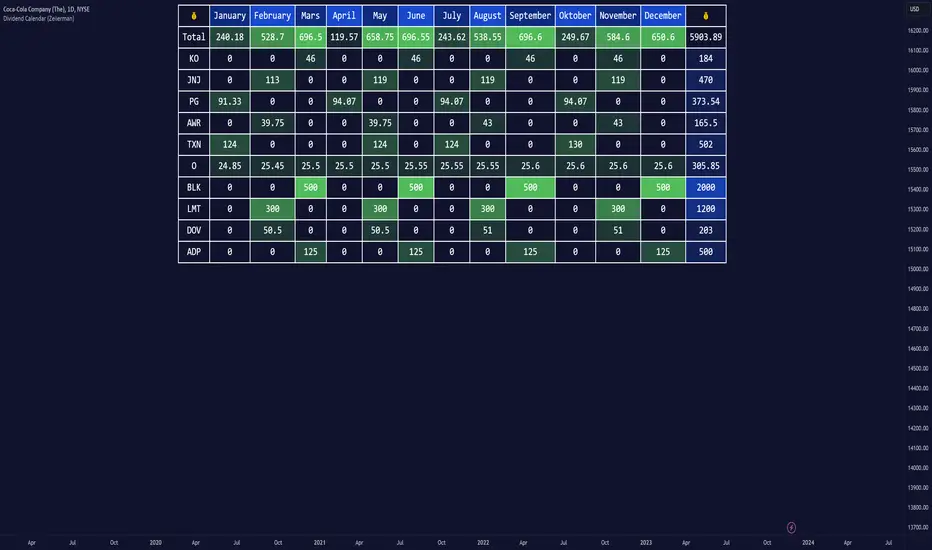

Dividend Calendar (Zeiierman)█ Overview

The Dividend Calendar is a financial tool designed for investors and analysts in the stock market. Its primary function is to provide a schedule of expected dividend payouts from various companies.

Dividends, which are portions of a company's earnings distributed to shareholders, represent a return on their investment. This calendar is particularly crucial for investors who prioritize dividend income, as it enables them to plan and manage their investment strategies with greater effectiveness. By offering a comprehensive overview of when dividends are due, the Dividend Calendar aids in informed decision-making, allowing investors to time their purchases and sales of stocks to optimize their dividend income. Additionally, it can be a valuable tool for forecasting cash flow and assessing the financial health and dividend-paying consistency of different companies.

█ How to Use

Dividend Yield Analysis:

By tracking dividend growth and payouts, traders can identify stocks with attractive dividend yields. This is particularly useful for income-focused investors who prioritize steady cash flow from their investments.

Income Planning:

For those relying on dividends as a source of income, the calendar helps in forecasting income.

Trend Identification:

Analyzing the growth rates of dividends helps in identifying long-term trends in a company's financial health. Consistently increasing dividends can be a sign of a company's strong financial position, while decreasing dividends might signal potential issues.

Portfolio Diversification:

The tool can assist in diversifying a portfolio by identifying a range of dividend-paying stocks across different sectors. This can help mitigate risk as different sectors may react differently to market conditions.

Timing Investments:

For those who follow a dividend capture strategy, this indicator can be invaluable. It can help in timing the buying and selling of stocks around their ex-dividend dates to maximize dividend income.

█ How it Works

This script is a comprehensive tool for tracking and analyzing stock dividend data. It calculates growth rates, monthly and yearly totals, and allows for custom date handling. Structured to be visually informative, it provides tables and alerts for the easy monitoring of dividend-paying stocks.

Data Retrieval and Estimation: It fetches dividend payout times and amounts for a list of stocks. The script also estimates future values based on historical data.

Growth Analysis: It calculates the average growth rate of dividend payments for each stock, providing insights into dividend consistency and growth over time.

Summation and Aggregation: The script sums up dividends on a monthly and yearly basis, allowing for a clear view of total payouts.

Customization and Alerts: Users can input custom months for dividend tracking. The script also generates alerts for upcoming or current dividend payouts.

Visualization: It produces various tables and visual representations, including full calendar views and income tables, to display the dividend data in an easily understandable format.

█ Settings

Overview:

Currency:

Description: This setting allows the user to specify the currency in which dividend values are displayed. By default, it's set to USD, but users can change it to their local currency.

Impact: Changing this value alters the currency denomination for all dividend values displayed by the script.

Ex-Date or Pay-Date:

Description: Users can select whether to show the Ex-dividend day or the Actual Payout day.

Impact: This changes the reference date for dividend data, affecting the timing of when dividends are shown as due or paid.

Estimate Forward:

Description: Enables traders to predict future dividends based on historical data.

Impact: When enabled, the script estimates future dividend payments, providing a forward-looking view of potential income.

Dividend Table Design:

Description: Choose between viewing the full dividend calendar, just the cumulative monthly dividend, or a summary view.

Impact: This alters the format and extent of the dividend data displayed, catering to different levels of detail a user might require.

Show Dividend Growth:

Description: Users can enable dividend growth tracking over a specified number of years.

Impact: When enabled, the script displays the growth rate of dividends over the selected number of years, providing insight into dividend trends.

Customize Stocks & User Inputs:

This setting allows users to customize the stocks they track, the number of shares they hold, the dividend payout amount, and the payout months.

Impact: Users can tailor the script to their specific portfolio, making the dividend data more relevant and personalized to their investments.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

THISMA btccorrelationDescription:

This is a tool designed for traders who want to analyze correlation between any traded crypto's price in USD and the price of Bitcoin in USD.

Key Features:

Adjustable Correlation Window: The script features an input parameter that allows traders to set the length of the correlation window, with a default value of 14. Lower if you want faster granularity.

Clear Visualization: The correlation coefficient is plotted in a distinct pane below the main trading chart.

Reference Lines for Interpretation: Horizontal reference lines are included at 0.5 (indicating weak positive correlation), -0.5 (indicating weak negative correlation), and 0 (indicating no correlation). These lines, color-coded in green, red, and gray respectively, assist traders in quickly interpreting the correlation coefficient's value.

Applications:

Market Insight: If you want to be able to monitor if you should enter a trade on an altcoin or if its better to stick to Bitcoin to avoid being double exposed.

Risk Management: Identifying the correlation can help in assessing and managing the systemic risk associated with market movements, especially in cryptocurrency markets where Bitcoin's influence is significant.

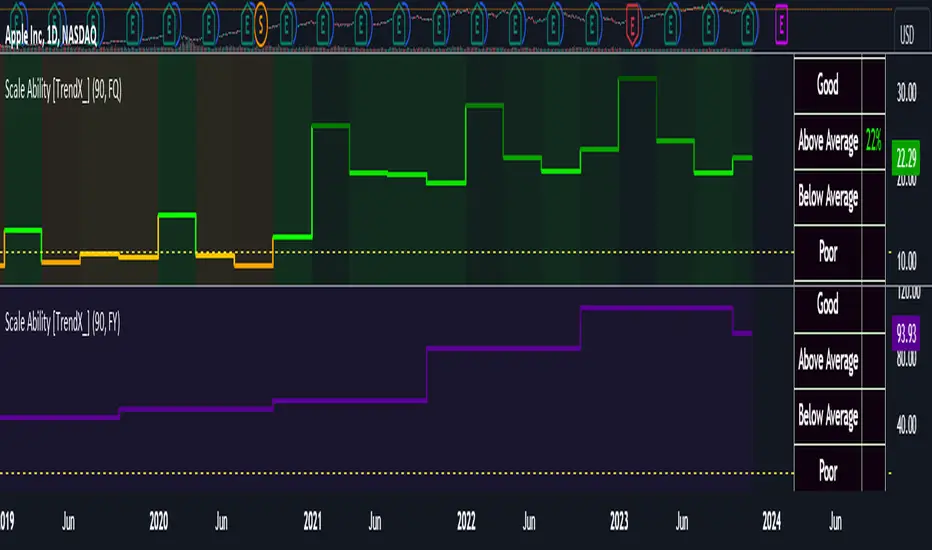

Scale Ability [TrendX_]Scale Ability indicator can indicate a company’s potential for future growth and profitability.

A scalable company is one that can increase its revenue and market share without increasing its costs proportionally, which can benefit from economies of scale. Therefore, the high-scale ability can generate more value for its shareholders - which is important for investment decisions.

Scale Ability indicator consists of 3 financial components:

Cash Flow from Investing Activities to Total Assets Ratio (CFIA / TA)

Net Income to Total Debt Ratio (NI / TD)

Earnings Before Interest, Taxes, Depreciation and Amortization to Equity Ratio (EBITDA / E)

These measures can help investors assess how efficiently and effectively a company uses its resources to generate revenue and profit.

Note:

This can be customizable between Fiscal Quarter (FQ) and Fiscal Year (Fy)

This is suitable for companies in fast-growing industries.

FUNCTION

CFIA / TA Ratio

A company with a net income to total debt of 9% could indicate that it is investing in its assets to keep up with the market demand and the technological changes which can create competitive advantages.

NI/ TD Ratio

A company with a net income to total debt of 9% could show that it is profitable and has a strong financial position, which can easily cover its debt payments.

EBITDA / E Ratio

A company with a net income to total debt of 14% illustrates that it is generating a high return on its equity.

USAGE

Scale index division:

> 43 : Excellent

32 - 43 : Good

12 - 31 : Above Average

= 11 : Average

8 - 10 : Below Average

5 - 7 : Poor

< 4 : Very Poor

DISCLAIMER

This is only a rough estimate, and the actual ratio may differ significantly depending on the stage of the business cycle and the company’s strategy, and the comparison of each company and its peers.

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur.

Therefore, one should always exercise caution and judgment when making decisions based on past performance.

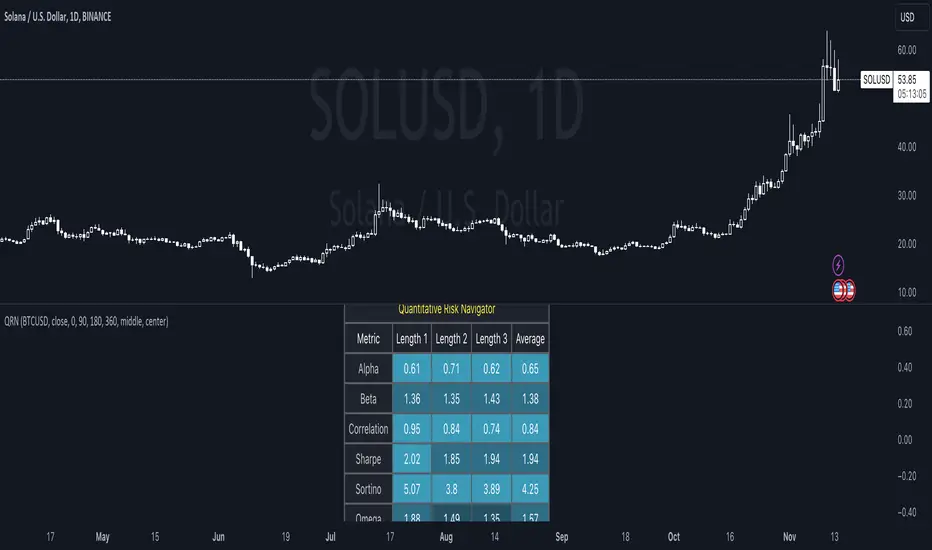

Quantitative Risk Navigator [kikfraben]📊 Quantitative Risk Navigator - Your Financial Performance GPS

Navigate the complexities of financial markets with confidence using the Quantitative Risk Navigator. This indicator provides you with a comprehensive dashboard to assess and understand the risk and performance of your chosen asset.

📈 Key Features:

Alpha and Beta Analysis: Uncover the outperformance (Alpha) and risk exposure (Beta) of your asset compared to a selected benchmark. Know where your investment stands in the market.

Correlation Insights: Understand the relationship between your asset and its benchmark through a clear visualization of correlation trends over different time lengths.

Risk-Return Metrics: Evaluate risk and return simultaneously with Sharpe and Sortino ratios. Make informed decisions by assessing the reward-to-risk ratio of your investment.

Omega Ratio: Gain deeper insights into your asset's performance by analyzing the Omega Ratio, which highlights the distribution of positive and negative returns.

Customizable Visualization: Tailor your chart to focus on specific metrics and time frames. Choose which metrics to display, allowing you to concentrate on the aspects that matter most to you.

Interactive Metrics Table: A user-friendly metrics table provides a quick overview of key values, including average metrics, enabling you to grasp the financial health of your asset at a glance.

Color-Coded Clarity: The indicator employs color-coded visualizations, making it easy to identify bullish and bearish trends, helping you make rapid and informed decisions.

🛠️ How to Use:

Symbol Selection: Choose your base symbol and preferred data source for analysis.

Risk-Free Rate: Input your risk-free rate to fine-tune calculations.

Length Customization: Adjust the lengths for different metrics to align with your analysis preferences.

Whether you're a seasoned trader or just stepping into the financial world, the Quantitative Risk Navigator empowers you to make strategic decisions by providing a comprehensive view of your asset's risk and return profile. Stay in control of your investments with this powerful financial GPS.

🚀 Start Navigating Your Financial Journey Today!

Rate of Change StrategyRate of Change Strategy :

INTRODUCTION :

This strategy is based on the Rate of Change indicator. It compares the current price with that of a user-defined period of time ago. This makes it easy to spot trends and even speculative bubbles. The strategy is long term and very risky, which is why we've added a Stop Loss. There's also a money management method that allows you to reinvest part of your profits or reduce the size of your orders in the event of substantial losses.

RATE OF CHANGE (ROC) :

As explained above, the ROC is used to situate the current price compared to that of a certain period of time ago. The formula for calculating ROC in relation to the previous year is as follows :

ROC (365) = (close/close (365) - 1) * 100

With this formula we can find out how many percent the change in the current price is compared with 365 days ago, and thus assess the trend.

PARAMETERS :

ROC Length : Length of the ROC to be calculated. The current price is compared with that of the selected length ago.

ROC Bubble Signal : ROC value indicating that we are in a bubble. This value varies enormously depending on the financial product. For example, in the equity market, a bubble exists when ROC = 40, whereas in cryptocurrencies, a bubble exists when ROC = 150.

Stop Loss (in %) : Stop Loss value in percentage. This is the maximum trade value percentage that can be lost in a single trade.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by an amount chosen by the user.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:BTCUSD in 1D timeframe with the following parameters :

ROC Length = 365

ROC Bubble Signal = 180

Stop Loss (in %) = 6

LONG CONDITION :

We are in a LONG position if ROC (365) > 0 for at least two days. This allows us to limit noise and irrelevant signals to ensure that the ROC remains positive.

SHORT CONDITION :

We are in a SHORT position if ROC (365) < 0 for at least two days. We also open a SHORT position when the speculative bubble is about to burst. If ROC (365) > 180, we're in a bubble. If the bubble has been in existence for at least a week and the ROC falls back below this threshold, we can expect the asset to return to reasonable prices, and thus a downward trend. So we're opening a SHORT position to take advantage of this upcoming decline.

EXIT RULES FOR WINNING TRADE :

The strategy is self-regulating. We don't exit a LONG trade until a SHORT signal has arrived, and vice versa. So, to exit a winning position, you have to wait for the entry signal of the opposite position.

RISK MANAGEMENT :

This strategy is very risky, and we can easily end up on the wrong side of the trade. That's why we're going to manage our risk with a Stop Loss, limiting our losses as a percentage of the trade's value. By default, this percentage is set at 6%. Each trade will therefore take a maximum loss of 6%.

If the SL has been triggered, it probably means we were on the wrong side. This is why we change the direction of the trade when a SL is triggered. For example, if we were SHORT and lost 6% of the trade value, the strategy will close this losing trade and open a long position without taking into account the ROC value. This allows us to be in position all the time and not miss the best opportunities.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

NOTE :

Please note that the strategy is backtested from 2017-01-01. As the timeframe is 1D, this strategy is a medium/long-term strategy. That's why only 34 trades were closed. Be careful, as the test sample is small and performance may not necessarily reflect what may happen in the future.

Enjoy the strategy and don't forget to take the trade :)

Absolute Momentum (Time Series Momentum)Absolute momentum , also known as time series momentum , focuses on the trend of an asset's own past performance to predict its future performance. It involves analyzing an asset's own historical performance, rather than comparing it to other assets.

The strategy determines whether an asset's price is exhibiting an upward (positive momentum) or downward (negative momentum) trend by assessing the asset's return over a given period (standard look-back period: 12 months or approximately 250 trading days). Some studies recommend calculating momentum by deducting the corresponding Treasury bill rate from the measured performance.

Absolute Momentum Indicator

The Absolute Momentum Indicator displays the rolling 12-month performance (measured over 250 trading days) and plots it against a horizontal line representing 0%. If the indicator crosses above this line, it signifies positive absolute momentum, and conversely, crossing below indicates negative momentum. An additional, optional look-back period input field can be accessed through the settings.

Hint: This indicator is a simplified version, as some academic approaches measure absolute momentum by subtracting risk-free rates from the 12-month performance. However, even with higher rates, the values will still remain close to the 0% line.

Benefits of Absolute Momentum

Absolute momentum, which should not be confused with relative momentum or the momentum indicator, serves as a timing instrument for both individual assets and entire markets.

Gary Antonacci , a key contributor to the absolute momentum strategy (find study below), emphasizes its effectiveness in multi-asset portfolios and its importance in long-only investing. This is particularly evident in a) reducing downside volatility and b) mitigating behavioral biases.

Moskowitz, Ooi, and Pedersen document significant 'time series momentum' across various asset classes, including equity index, currency, commodity, and bond futures, in 58 liquid instruments (find study below). There's a notable persistence in returns ranging from one to 12 months, which tends to partially reverse over longer periods. This pattern aligns with sentiment theories suggesting initial under-reaction followed by delayed over-reaction.

Despite its surprising ease of implementation, the academic community has successfully measured the effects of absolute momentum across decades and in every major asset class, including stocks, bonds, commodities, and foreign exchange (FX).

Strategies for Implementing Absolute Momentum:

To Buy a Stock:

Select a Look-Back Period: Choose a historical period to analyze the stock's performance. A common period is 12 months, but this can vary based on your investment strategy.

Calculate Excess Return: Determine the stock's excess return over this period. You can also assume a risk-free rate of "0" to simplify the process.

Evaluate Momentum:

If the excess return is positive, it indicates positive absolute momentum. This suggests the stock is in an upward trend and could be a good buying opportunity.

If the excess return is negative, it suggests negative momentum, and you might want to delay buying.

Consider further conditions: Align your decision with broader market trends, economic indicators, or fundamental analysis, for additional context.

To Sell a Stock You Own:

Regularly Monitor Performance: Use the same look-back period as for buying (e.g., 12 months) to regularly assess the stock's performance.

Check for Negative Momentum: Calculate the excess return for the look-back period. Again, you can assume a risk-free rate of "0" to simplify the process. If the stock shows negative momentum, it might be time to consider selling.

Consider further conditions:Align your decision with broader market trends, economic indicators, or fundamental analysis, for additional context.

Important note: Note: Entering a position (i.e., buying) based on positive absolute momentum doesn't necessarily mean you must sell it if it later exhibits negative absolute momentum. You can initiate a position using positive absolute momentum as an entry indicator and then continue holding it based on other criteria, such as fundamental analysis.

General Tips:

Reassessment Frequency: Decide how often you will reassess the momentum (monthly, quarterly, etc.).

Remember, while absolute momentum provides a systematic approach, it's recommendable to consider it as part of a broader investment strategy that includes diversification, risk management, fundamental analysis, etc.

Relevant Capital Market Studies:

Antonacci, Gary. "Absolute momentum: A simple rule-based strategy and universal trend-following overlay." Available at SSRN 2244633 (2013)

Moskowitz, Tobias J., Yao Hua Ooi, and Lasse Heje Pedersen. "Time series momentum." Journal of financial economics 104.2 (2012): 228-250

Narrow Range StrategyNarrow Range Strategy :

INTRODUCTION :

This strategy is based on the Narrow Range Day concept, implying that low volatility will generate higher volatility in the days ahead. The strategy sends us buy and sell signals with well-defined profit targets. It's a medium/long-term strategy. There's also a money management method that allows us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

NARROW RANGE (NR) DAY :

A Narrow Range Day is a day in which price variations are included in those of a specific day some time before. The high and low of this specific day form the "reference range". In general, we compare these variations with those of 4 or 7 days ago. The mathematical formula for finding an NR4 is :

If low > low(4) and high < high(4) :

nr = true

This implies that the current low is greater than the low of 4 days ago, and the current high is smaller than the high of 4 days ago. So today's volatility is lower than that of 4 days ago, and may be a sign of high volatility to come.

PARAMETERS :

Narrow Range Length : Corresponds to the number of candles back to compare current volatility. The default is 4, allowing comparison of current volatility with that of 4 candles ago.

Stop Loss : Percentage of the reference range on which to set an exit order to limit losses. The minimum value is 0.001, while the maximum is 1. The default value is 0.35.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by an amount chosen by the user.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot was used to test NR4 and NR7 with all possible Stop Losses in order to find out which combination generates the highest return on BITSTAMP:ETHUSD while limiting the drawdown. This strategy is the most optimal with an NR4 and a SL of 35% of the reference range size in 5D timeframe.

BUY AND SHORT SIGNALS :

When an NR is spotted, we create two stop orders on the high and low of the reference range. As soon as there's a breakout from this reference range (shown in blue on the chart), we open a position. We're LONG if there's a breakout on the high and SHORT if there's a breakout on the low. Executing a stop order cancels the second stop order.

RISK MANAGEMENT :

This strategy is subject to losses. We manage our risk with Stop Losses. The user is free to enter a SL as a percentage of the reference range. The maximum amount risked per trade therefore depends on the size of the range. The larger the range, the greater the risk. That's why we have set a maximum Stop Loss to 10% to limiting risks per trade.

The special feature of this strategy is that it targets a precise profit objective. This corresponds to the size of the reference range at the top of the high if you're LONG, or at the bottom of the low if you're short. In the same way, the larger the reference range, the greater the potential profits.

The risk reward remains the same for all trades and amounts to : 100/35 = 2.86. If the reference range is too high, we have set a SL to 10% of the trade value to limit losses. In that case, the risk reward is less than 2.86.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

NOTE :

Please note that the strategy is backtested from 2017-01-01. As the timeframe is 5D, this strategy is a medium/long-term strategy. That's why only 37 trades were closed. Be careful, as the test sample is small and performance may not necessarily reflect what may happen in the future.

Enjoy the strategy and don't forget to take the trade :)

Liquidations Meter [LuxAlgo]The Liquidation Meter aims to gauge the momentum of the bar, identify the strength of the bulls and bears, and more importantly identify probable exhaustion/reversals by measuring probable liquidations.

🔶 USAGE

This tool includes many features related to the concept of liquidation. The two core ones are the liquidation meter and liquidation price calculator, highlighted below.

🔹 Liquidation Meter

The liquidation meter presents liquidations on the price chart by measuring the highest leverage value of longs and shorts that have been potentially liquidated on the last chart bar, hence allowing traders to:

gauge the momentum of the bar.

identify the strength of the bulls and bears.

identify probable reversal/exhaustion points.

Liquidation of low-leveraged positions can be indicative of exhaustion.

🔹 Liquidation Price Calculator

A liquidation price calculator might come in handy when you need to calculate at what price level your leveraged position in Crypto, Forex, Stocks, or any other asset class gets liquidated to add a protective stop to mitigate risk. Monitoring an open position gets easier if the trader can calculate the total risk in order for them to choose the right amount of margin and leverage.

Liquidation price is the distance from the trader's entry price to the price where trader's leveraged position gets liquidated due to a loss. As the leverage is increased, the distance from trader's entry price to the liquidation price shrinks.

While you have one or several trades open you can quickly check their liquidation levels and determine which one of the trades is closest to their liquidation price.

If you are a day trader that uses leverage and you want to know which trade has the best outlook you can calculate the liquidation price to see which one of the trades looks best.

🔹 Dashboard

The bar statistics option enables measuring and presenting trading activity, volatility, and probable liquidations for the last chart bar.

🔶 DETAILS

It's important to note that liquidation price calculator tool uses a formula to calculate the liquidation price based on the entry price + leverage ratio.

Other factors such as leveraged fees, position size, and other interest payments have been excluded since they are variables that don’t directly affect the level of liquidation of a leveraged position.

The calculator also assumes that traders are using an isolated margin for one single position and does not take into consideration the additional margin they might have in their account.

🔹Liquidation price formula

the liquidation distance in percentage = 100 / leverage ratio

the liquidation distance in price = current asset price x the liquidation distance in percentage

the liquidation price (longs) = current asset price – the liquidation distance in price

the liquidation price (shorts) = current asset price + the liquidation distance in price

or simply

the liquidation price (longs) = entry price * (1 – 1 / leverage ratio)

the liquidation price (shorts) = entry price * (1 + 1 / leverage ratio)

Example:

Let’s say that you are trading a leverage ratio of 1:20. The first step is to calculate the distance to your liquidation point in percentage.

the liquidation distance in percentage = 100 / 20 = 5%

Now you know that your liquidation price is 5% away from your entry price. Let's calculate 5% below and above the entry price of the asset you are currently trading. As an example, we assume that you are trading bitcoin which is currently priced at $35000.

the liquidation distance in price = $35000 x 0.05 = $1750

Finally, calculate liquidation prices.

the liquidation price (longs) = $35000 – $1750 = $33250

the liquidation price (short) = $35000 + $1750 = $36750

In this example, short liquidation price is $36750 and long liquidation price is $33250.

🔹How leverage ratio affects the liquidation price

The entry price is the starting point of the calculation and it is from here that the liquidation price is calculated, where the leverage ratio has a direct impact on the liquidation price since the more you borrow the less “wiggle-room” your trade has.

An increase in leverage will subsequently reduce the distance to full liquidation. On the contrary, choosing a lower leverage ratio will give the position more room to move on.

🔶 SETTINGS

🔹Liquidations Meter

Base Price: The option where to set the reference/base price.

🔹Liquidation Price Calculator

Liquidation Price Calculator: Toggles the visibility of the calculator. Details and assumptions made during the calculations are stated in the tooltip of the option.

Entry Price: The option where to set the entry price, a value of 0 will use the current closing price. Details are given in the tooltip of the option.

Leverage: The option where to set the leverage value.

Show Calculated Liquidation Prices on the Chart: Toggles the visibility of the liquidation prices on the price chart.

🔹Dashboard

Show Bar Statistics: Toggles the visibility of the last bar statistics.

🔹Others

Liquidations Meter Text Size: Liquidations Meter text size.

Liquidations Meter Offset: Liquidations Meter offset.

Dashboard/Calculator Placement: Dashboard/calculator position on the chart.

Dashboard/Calculator Text Size: Dashboard text size.

🔶 RELATED SCRIPTS

Here are some of the scripts that are related to the liquidation and liquidity concept, for more and other conceptual scripts you are kindly invited to visit LuxAlgo-Scripts .

Liquidation-Levels

Liquidations-Real-Time

Buyside-Sellside-Liquidity

Cryptocurrency Cointegration Matrix (SpiritualHealer117)This indicator plots a cointegration matrix for the pairings of 100 cryptocurrencies. The matrix is populated with ADF t-stats (from an ADF-test with 1 lag). An ADF-test (Augmented Dickey-Fuller test) tests the null hypothesis that an AR process has a unit root. If rejected, the alternative hypothesis is usually that the AR process is either stationary or trend-stationary. This model extends upon Lejmer's Cointegration Matrix for forex by enabling the indicator to use cryptocurrency pairs and allows for significantly more pairs to be analyzed using the group selection feature. This indicator arose from collaboration with TradingView user CryptoJuju.

This indicator runs an ADF-test on the residuals (spread) of each pairing (i.e. a cointegration test). It tests if there is a unit root in the spread between the two assets of a pairing. If there is a unit root in the spread, it means the spread varies randomly over time, and any mean reversion in the spread is very hard to predict. By contrast, if a unit root does not exist, the spread (distance between the assets) should remain more or less constant over time, or rise/fall in close to the same rate over time. The more negative the number from an ADF-test, the stronger the rejection of the idea that the spread has a unit root. In statistics, there are different levels which correspond with the confidence level of the test. For this indicator, -3.238 equals a confidence level of 90%, -3.589 equals a confidence level of 95% and -4.375 equals a confidence level of 99% that there is not a unit root. So the colors are based on the confidence level of the test statistic (the t-stat, i.e. the number of the pairing in the matrix). So if the number is greater than -3.238 it is green, if it's between -3.238 and -3.589 it's yellow, if it's between -3.589 and -4.375 it's orange, and if its lower than -4.375 it's red.

There are multiple ways to interpret the results. A strong rejection of the presence of a unit root (i.e. a value of -4.375 or below) is not a guarantee that there is no unit root, or that any of the two alternative hypotheses (that the spread is stationary or trend-stationary) are correct. It only means that in 99% of the cases, if the spread is an AR process, the test is right, and there is no unit root in the spread. Therefore, the results of this test is no guarantee that the result proves one of the alternative solutions. Green therefore means that a unit root cannot be ruled out (which can be interpreted as "the two cryptocurrencies probably don't move together over time"), and red means that a unit root is likely not present (which can be interpreted as "the two cryptocurrencies may move together over time").

One possible way to use this indicator is to make sure you don't trade two pairs that move together at the same time. So basically the idea is that if you already have a trade open in one of the currency pairs of the pairing, only enter a trade in the other currency pair of that pairing if the color is green, or you may be doubling your risk. Alternatively, you could implement this indicator into a pairs trading system, such as a simple strategy where you buy the spread between two cryptocurrencies with a red result when the spread's value drops one standard deviation away from its moving average, and conversely sell when it moves up one standard deviation above the moving average. However, this strategy is not guaranteed to work, since historical data does not guarantee the future.

Specific to this indicator, there are 100 different cryptocurrency tickers which are included in the matrix, and the cointegration matrices between all the tickers can be checked by switching asset group 1 and asset group 2 to different asset groups. The ADF test is computed using a specified length, and if there is insufficient data for the length, the test produces a grayed out box.

NOTE: The indicator can take a while to load since it computes the value of 400 ADF tests each time it is run.

Leading Industry [TrendX__]Leading Industry indicator functions like an Industry-meter, a tool that measures the strength of different industries in a country or region.

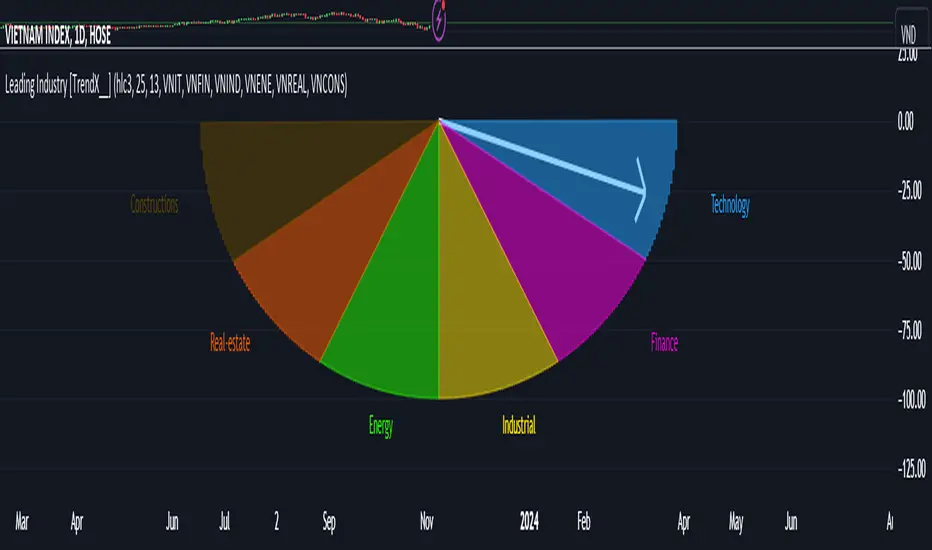

It consists of the fields of Technology, Finance, Industrial, Energy, Real-estate, and Construction.

USAGE

The Industry-meter indicates which industry is the strongest by using an arrow that points to the field with the highest score.

The default fields are set for Vietnam’s industry, but the user can customize them according to their preferences and needs.

The Industry-meter is a useful way to visualize the economic landscape and identify the opportunities and challenges in various sectors.

DISCLAIMER

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur.

Therefore, one should always exercise caution and judgment when making decisions based on past performance.

Martingale + Grid DCA Strategy [YinYangAlgorithms]This Strategy focuses on strategically Martingaling when the price has dropped X% from your current Dollar Cost Average (DCA). When it does Martingale, it will create a Purchase Grid around this location to likewise attempt to get you a better DCA. Likewise following the Martingale strategy, it will sell when your Profit has hit your target of X%.

Martingale may be an effective way to lower your DCA. This is due to the fact that if your initial purchase; or in our case, initial Grid, all went through and the price kept going down afterwards, that you may purchase more to help lower your DCA even more. By doing so, you may bring your DCA down and effectively may make it easier and quicker to reach your target profit %.

Grid trading may be an effective way of reducing risk and lowering your DCA as you are spreading your purchases out over multiple different locations. Likewise we offer the ability to ‘Stack Grids’. What this means, is that if a single bar was to go through 20 grids, the purchase amount would be 20x what each grid is valued at. This may help get you a lower DCA as rather than creating 20 purchase orders at each grid location, we create a single purchase order at the lowest grid location, but for 20x the amount.

By combining both Martingale and Grid DCA techniques we attempt to lower your DCA strategically until you have reached your target profit %.

Before we start, we just want to make it known that first off, this Strategy features 8% Commission Fees, you may change this in the Settings to better reflect the Commission Fees of your exchange. On a similar note, due to Commission Fees being one of the number one profit killers in fast swing trade strategies, this strategy doesn’t focus on low trades, but the ideology of it may result in low amounts of trades. Please keep in mind this is not a bad thing. Since it has the ability to ‘Stack Grid Purchases’ it may purchase more for less and result in more profit, less commission fees, and likewise less # of trades.

Tutorial:

In this example above, we have it set so we Martingale twice, and we use 100 grids between the upper and lower level of each martingale; for a total of 200 Grids. This strategy will take total capital (initial capital + net profit) and divide it by the amount of grids. This will result in the $ amount purchased per grid. For instance, say you started with $10,000 and you’ve made $2000 from this Strategy so far, your total capital is $12,000. If you likewise are implementing 200 grids within your Strategy, this will result in $12,000 / 200 = $60 per grid. However, please note, that the further down the grid / martingale is, the more volume it is able to purchase for $60.

The white line within the Strategy represents your DCA. As the Strategy makes purchases, this will continue to get lower as will your Target Profit price (Blue Line). When the Close goes above your Target Profit price, the Strategy will close all open positions and claim the profit. This profit is then reinvested back into the Strategy, which may exponentially help the Strategy become more profitable the longer it runs for.

In the example above, we’ve zoomed in on the first example. In this we want to focus on how the Strategy got back into the trades shortly after it sold. Currently within the Settings we have it set so our entry is when the Lowest with a length of 3 is less than the previous Lowest with a length of 3. This is 100% customizable and there are multiple different entry options you can choose from and customize such as:

EMA 7 Crossover EMA 21

EMA 7 Crossunder EMA 21

RSI 14 Crossover RSI MA 14

RSI 14 Crossunder RSI MA 14

MFI 14 Crossover MFI MA 14

MFI 14 Crossunder MFI MA 14

Lowest of X Length < Previous Lowest of X Length

Highest of X Length > Previous Highest of X Length

All of these entry options may be tailored to be checked for on a different Time Frame than the one you are currently using the Strategy on. For instance, you may be running the Strategy on the 15 minute Time Frame yet decide you want the RSI to cross over the RSI MA on the 1 Day to be a valid entry location.

Please keep in mind, this Strategy focuses on DCA, this means you may not want the initial purchase to be the best location. You may want to buy when others think it is a good time to sell. This is because there may be strong bearish momentum which drives the price down drastically and potentially getting you a good DCA before it corrects back up.

We will continue to add more Entry options as time goes on, and if you have any in mind please don’t hesitate to let us know.

Now, back to the example above, if we refer to the Yellow circle, you may see that the Lowest of a length of 3 was less than its previous lowest, this triggered the martingales to create their grids. Only a few bars later, the price went into the first grid and went a little lower than its midpoint (Yellow line). This caused about 60% of the first grid to be purchased. Shortly after the price went even lower into this grid and caused the entire first martingale grid to be purchased. However, if you notice, the white line (your DCA) is lower than the midpoint of the first grid. This is due to the fact that we have ‘Stack Grid Purchases’ enabled. This allows the Strategy to purchase more when a single bar crosses through multiple grid locations; and effectively may lower your average more than if it simply executed a purchase order at each grid.

Still looking at the same location within our next example, if we simply increase the Martingale amount from 2 to 3 we can see something strange happens. What happened is our Target Profit price was reached, then our entry condition was met, which caused all of the martingale grids to be formed; however, the price continued to increase afterwards. This may not be a good thing, sure the price could correct back down to these grid locations, but what if it didn’t and it just kept increasing? This would result in this Strategy being stuck and unable to make any trades. For this reason we have implemented a Failsafe in the Settings called ‘Reset Grids if no purchase happens after X bars’.

We have enabled our Failsafe ‘Reset Grids if no purchase happens after X bars’ in this example above. By default it is set to 100 bars, but you can change this to whatever works best for you. If you set it to 0, this Failsafe will be disabled and act like the example prior where it is possible to be stuck with no trades executing.

This Failsafe may be an important way to ensure the Strategy is able to make purchases, however it may also mean the Grids increase in price when it is used, and if a massive correction were to occur afterwards, you may lose out on potential profit.

This Strategy was designed with WebHooks in mind. WebHooks allow you to send signals from the Strategy to your exchange. Simply set up a Custom TradingView Bot within the OKX exchange or 3Commas platform (which has your exchange API), enter the data required from the bot into the settings here, select your bot type in ‘Webhook Alert Type’, and then set up the alert. After that you’re good to go and this Strategy will fully automate all of its trades within your exchange for you. You need to format the Alert a certain way for it to work, which we will go over in the next example.

Add an alert for this Strategy and simply modify the alert message so all it says is:

{{strategy.order.alert_message}}

Likewise change from the Alert ‘Settings’ to Alert ‘Notifications’ at the top of the alert popup. Within the Notifications we will enable ‘Webhook URL’ and then we will pass the URL we are sending the Webhook to. In this example we’ve put OKX exchange Webhook URL, however if you are using 3Commas you’ll need to change this to theirs.

OKX Webhook URL:

www.okx.com

3Commas Webhook URL:

app.3commas.io

Make sure you click ‘Create’ to actually create this alert. After that you’re all set! There are many Tutorials videos you can watch if you are still a little confused as to how Webhook trading works.

Due to the nature of this Strategy and how it is designed to work, it has the ability to never sell unless there it will make profit. However, because of this it also may be stuck waiting in trades for quite a long period of time (usually a few months); especially when your Target Profit % is 15% like in the example above. However, this example above may be a good indication that it may maintain profitability for a long period of time; considering this ‘Deep Backtest’ is from 2017-8-17.

We will conclude the tutorial here. Hopefully you understand how this Strategy has the potential to make calculated and strategic DCA Grid purchases for you and then based on a traditional Martingale fashion, bulk sell at the desired Target Profit Percent.

Settings:

Purchase Settings:

Only Purchase if its lower than DCA: Generally speaking, we want to lower our Average, and therefore it makes sense to only buy when the close is lower than our current DCA and a Purchase Condition is met.

Purchase Condition: When creating the initial buy location you must remember, you want to Buy when others are Fearful and Sell when others are Greedy. Therefore, many of the Buy conditions involve times many would likewise Sell. This is one of the bonuses to using a Strategy like this as it will attempt to get you a good entry location at times people are selling.

Lower / Upper Change Length: This Lower / Upper Length is only used if the Purchase Condition is set to 'Lower Changed' or 'Upper Changed'. This is when the Lowest or Highest of this length changes. Lowest would become lower or Highest would become higher.

Purchase Resolution: Purchase Resolution is the Time Frame that the Purchase Condition is calculated on. For instance, you may only want to start a new Purchase Order when the RSI Crosses RSI MA on the 1 Day, but yet you run this Strategy on the 15 minutes.

Sell Settings:

Trailing Take Profit: Trailing Take Profit is where once your Target Profit Percent has been hit, this will trail up to attempt to claim even more profit.

Target Profit Percent: What is your Target Profit Percent? The Strategy will close all positions when the close price is greater than your DCA * this Target Profit Percent.

Grid Settings:

Stack Grid Purchases: If a close goes through multiple Buy Grids in one bar, should we amplify its purchase amount based on how many grids it went through?

Reset Grids if no purchase happens after X Bars: Set this to 0 if you never want to reset. This is very useful in case the price is very bullish and continues to increase after our Target Profit location is hit. What may happen is, Target Profit location is hit, then the Entry condition is met but the price just keeps increasing afterwards. We may not want to be sitting waiting for the price to drop, which may never happen. This is more of a failsafe if anything. You may set it very large, like 500+ if you only want to use it in extreme situations.

Grid % Less than Initial Purchase Price: How big should our Buy Grid be? For instance if we bought at 0.25 and this value is set to 20%, that means our Buy Grid spans from 0.2 - 0.25.

Grid Amounts: How many Grids should we create within our Buy location?

Martingale Settings:

Amount of Times 'Planned' to Martingale: The more Grids + the More Martingales = the less $ spent per grid, however the less risk. Remember it may be better to be right and take your time than risk too much and be stuck too long.

Martingale Percent: When the current price is this percent less than our DCA, lets create another Buy Grid so we can lower our average more. This will make our profit location less.

Webhook Alerts:

Webhook Alert Type: How should we format this Alert? 3Commas and OKX take their alerts differently, so please select the proper one or your webhooks won't work.

3Commas Webhook Alerts:

3Commas Bot ID: The 3Commas Bot ID is needed so we know which BOT ID we are sending this webhook too.

3Commas Email Token: The 3Commas Email Token is needed for your webhooks to work properly as it is linked to your account.

OKX Webhook Alerts:

OKX Signal Token: This Signal Token is attached to your OKX bot and will be used to access it within OKX.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

2 Moving Averages | Trend FollowingThe trading system is a trend-following strategy based on two moving averages (MA) and Parabolic SAR (PSAR) indicators.

How it works:

The strategy uses two moving averages: a fast MA and a slow MA.

It checks for a bullish trend when the fast MA is above the slow MA and the current price is above the fast MA.

It checks for a bearish trend when the fast MA is below the slow MA and the current price is below the fast MA.

The Parabolic SAR (PSAR) indicator is used for additional trend confirmation.

Long and short positions can be turned on or off based on user input.

The strategy incorporates risk management with stop-loss orders based on the Average True Range (ATR).

Users can filter the backtest date range and display various indicators.

The strategy is designed to work with the date range filter, risk management, and user-defined positions.

Features:

Trend-following strategy.

Two customizable moving averages.

Parabolic SAR for trend confirmation.

User-defined risk management with stop-loss based on ATR.

Backtest date range filter.

Flexibility to enable or disable long and short positions.

This trading system provides a comprehensive approach to trend-following and risk management, making it suitable for traders looking to capture trends with controlled risk.

Renko StrategyRENKO STRATEGY

CAUTION : This strategy must be applied to a candlestick chart (not a Renko chart).

INTRODUCTION :

The Traditional Renko chart has been reproduced and is plotted according to the evolution of the price. It will enable us to receive buy or sell signals and follow major trends. This is a medium/long term strategy and depends a lot on the box size chosen in the parameters. There's also a money management method allowing us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RENKO CHART :

Renko chart construction methodology :

The user must first choose the box size. The minimum is 0.00001 and there is no maximum. The default is 10. The user must then choose the source that will define the data on which the calculations will be based (high, low, open, close). By default, close is selected. The first candle on the chart is used to draw the first box with its high and low.

Each time the price changes by the amount of the box size relative to the high or low of the last box, a new box is added above or below the previous one. If price variations are less than the box size, the same box is added next to the previous one. If price variations are N (integer number) times greater than box size, N boxes are added above or below the previous one. Each box added above the previous one is a green box, while each box added below the previous one is a red box.

Conditions for drawing a green box above the previous one :

(source - high_of_the_last_box) / box_size > 1

Condition for drawing a red box below the previous one :

(low_of_the_last_box - source) / box_size > 1

If neither condition is triggered, the same box is drawn next to the previous one.

Example :

The last candle has drawn a box with low 12 and high 14. The box size is therefore 2. The strategy will look at the value of the close each time a candle ends. The current candle closes with a close equal to 15.5. As the variation from the previous high is only 1.5 (which is less than the box size), the same box is added next to the previous one. The next candle closes at 16.2. The price variation is therefore 2.2 compared with the previous high. We can now add a new green box just above the previous one, with a low of 14 and a high of 16. The same process applies if the candle's close is at least one box size below the low of the last box. In this case, a new red box is placed below the previous one.

PARAMETERS :

Source : Allows you to specify which data will be taken into account by the strategy when performing calculations. The default is close.

Box size : Size of Renko graph boxes. This is a very important parameter to choose carefully, as it has a strong impact on the strategy's performance. Defaults to 10.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test all possible box sizes to find out which one generates the highest return on BITSTAMP:LTCUSD while limiting the drawdown. This strategy is the most optimal with a box size equal to 5.08 in 8h timeframe.

BUY AND SHORT SIGNALS :

As the aim of this strategy is to follow major trends based on price movements, we need to be on the right side of price fluctuation. We trade every box reversal, i.e. we are LONG when the boxes are green indicating an uptrend and SHORT when they are red indicating a downtrend.

RISK MANAGEMENT :

This strategy can incur losses. The size of the box is decisive, as it is used to plot the RENKO chart and thus trigger buy or sell signals. It's also what allows us to manage risk. For every trade, we risk a maximum amount equal to 2 times the size of the box, i.e. :(5.08*2*nb_contract)/trade_value.

MONEY MANAGEMENT :

The fixed ratio method has been used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy not only increases our performance, but also our drawdown.

Enjoy the strategy and don't forget to take the trade :)