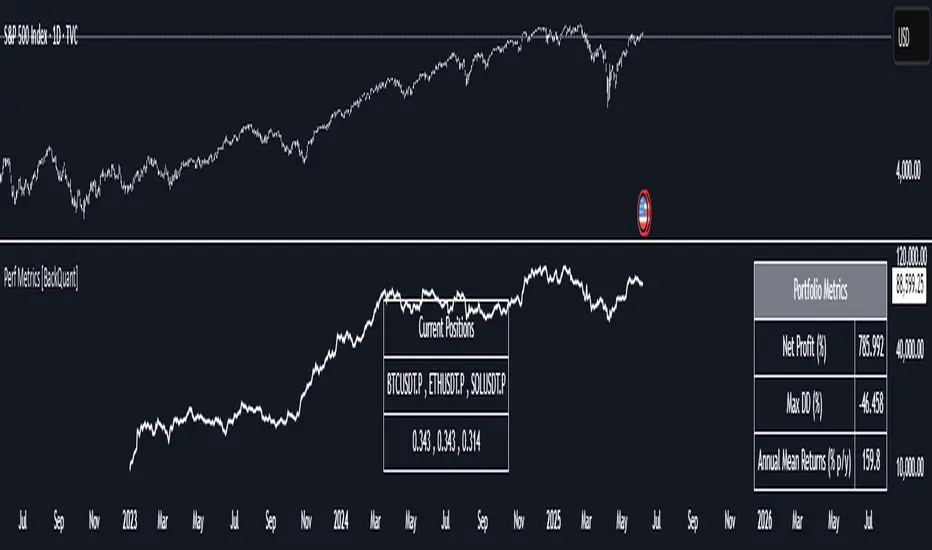

Cross-Sectional Altcoin Portfolio [BackQuant]Cross-Sectional Altcoin Portfolio

Introducing BackQuant's Cross-Sectional Altcoin Portfolio, a sophisticated trading system designed to dynamically rotate among a selection of major altcoins. This portfolio strategy compares multiple assets based on real-time performance metrics, such as momentum and trend strength, to select the strongest-performing coins. It uses a combination of adaptive scoring and regime filters to ensure the portfolio is aligned with favorable market conditions, minimizing exposure during unfavorable trends.

This system offers a comprehensive solution for crypto traders who want to optimize portfolio allocation based on cross-asset performance, while also accounting for market regimes. It allows traders to compare multiple altcoins dynamically and allocate capital to the top performers, ensuring the portfolio is always positioned in the most promising assets.

Key Features

1. Dynamic Asset Rotation:

The portfolio constantly evaluates the relative strength of 10 major altcoins: SOLUSD, RUNEUSD, ORDIUSD, DOGEUSDT, ETHUSD, ENAUSDT, RAYUSDT, PENDLEUSD, UNIUSD, and KASUSDT.

Using a ratio matrix, the system selects the strongest asset based on momentum and trend performance, dynamically adjusting the allocation as market conditions change.

2. Long-Only Portfolio with Cash Reserve:

The portfolio only takes long positions or remains in cash. The system does not enter short positions, reducing the risk of exposure during market downturns.

A powerful regime filter ensures the system is inactive during periods of market weakness, defined by the Universal Trend Performance Indicator (TPI) and other market data.

3. Equity Tracking:

The script provides real-time visualizations of portfolio equity compared to buy-and-hold strategies.

Users can compare the performance of the portfolio against holding individual assets (e.g., BTC, ETH) and see the benefits of the dynamic allocation.

4. Performance Metrics:

The system provides key performance metrics such as:

Sharpe Ratio: Measures risk-adjusted returns.

Sortino Ratio: Focuses on downside risk.

Omega Ratio: Evaluates returns relative to risk.

Maximum Drawdown: The maximum observed loss from a peak to a trough.

These metrics allow traders to assess the effectiveness of the strategy versus simply holding the assets.

5. Regime Filter:

The system incorporates a regime filter that evaluates the overall market trend using the TPI and other indicators. If the market is in a downtrend, the system exits positions and moves to cash, avoiding exposure to negative market conditions.

Users can customize the thresholds for the long and short trends to fit their risk tolerance.

6. Customizable Parameters:

Traders can adjust key parameters, such as the backtest start date, starting capital, leverage multiplier, and visualization options, including equity plot colors and line widths.

The system supports different levels of customizations for traders to optimize their strategies.

7. Equity and Buy-and-Hold Comparisons:

This script enables traders to see the side-by-side comparison of the portfolio’s equity curve and the equity curve of a buy-and-hold strategy for each asset.

The comparison allows users to evaluate the performance of the dynamic strategy versus holding the altcoins in isolation.

8. Forward Test (Out-of-Sample Testing):

The system includes a note that the portfolio provides out-of-sample forward tests, ensuring the robustness of the strategy. This is crucial for assessing the portfolio's performance beyond historical backtesting and validating its ability to adapt to future market conditions.

9. Visual Feedback:

The system offers detailed visual feedback on the current asset allocation and performance. Candles are painted according to the trend of the selected assets, and key metrics are displayed in real-time, including the momentum scores for each asset.

10. Alerts and Notifications:

Real-time alerts notify traders when the system changes asset allocations or moves to cash, ensuring they stay informed about portfolio adjustments.

Visual labels on the chart provide instant feedback on which asset is currently leading the portfolio allocation.

How the Rotation Works

The portfolio evaluates 10 different assets and calculates a momentum score for each based on their price action. This score is processed through a ratio matrix, which compares the relative performance of each asset.

Based on the rankings, the portfolio allocates capital to the top performers, ensuring it rotates between the strongest assets while minimizing exposure to underperforming assets.

If no asset shows strong performance, the system defaults to cash to preserve capital.

Final Thoughts

BackQuant’s Cross-Sectional Altcoin Portfolio provides a dynamic and systematic approach to altcoin portfolio management. By employing real-time performance metrics, adaptive scoring, and regime filters, this strategy aims to optimize returns while minimizing exposure to market downturns. The inclusion of out-of-sample forward tests ensures that the system remains robust in live market conditions, making it an ideal tool for crypto traders seeking to enhance their portfolio's performance with a data-driven, momentum-based approach.

Portfolio management

Performance Metrics With Bracketed Rebalacing [BackQuant]Performance Metrics With Bracketed Rebalancing

The Performance Metrics With Bracketed Rebalancing script offers a robust method for assessing portfolio performance, integrating advanced portfolio metrics with different rebalancing strategies. With a focus on adaptability, the script allows traders to monitor and adjust portfolio weights, equity, and other key financial metrics dynamically. This script provides a versatile approach for evaluating different trading strategies, considering factors like risk-adjusted returns, volatility, and the impact of portfolio rebalancing.

Please take the time to read the following:

Key Features and Benefits of Portfolio Methods

Bracketed Rebalancing:

Bracketed Rebalancing is an advanced strategy designed to trigger portfolio adjustments when an asset's weight surpasses a predefined threshold. This approach minimizes overexposure to any single asset while maintaining flexibility in response to market changes. The strategy is particularly beneficial for mitigating risks that arise from significant asset weight fluctuations. The following image illustrates how this method reacts when asset weights cross the threshold:

Daily Rebalancing:

Unlike the bracketed method, Daily Rebalancing adjusts portfolio weights every trading day, ensuring consistent asset allocation. This method aims for a more even distribution of portfolio weights, making it a suitable option for traders who prefer less sensitivity to individual asset volatility. Here's an example of Daily Rebalancing in action:

No Rebalancing:

For traders who prefer a passive approach, the "No Rebalancing" option allows the portfolio to remain static, without any adjustments to asset weights. This method may appeal to long-term investors or those who believe in the inherent stability of their selected assets. Here’s how the portfolio looks when no rebalancing is applied:

Portfolio Weights Visualization:

One of the standout features of this script is the visual representation of portfolio weights. With adjustable settings, users can track the current allocation of assets in real-time, making it easier to analyze shifts and trends. The following image shows the real-time weight distribution across three assets:

Rolling Drawdown Plot:

Managing drawdown risk is a critical aspect of portfolio management. The Rolling Drawdown Plot visually tracks the drawdown over time, helping traders monitor the risk exposure and performance relative to the peak equity levels. This feature is essential for assessing the portfolio's resilience during market downturns:

Daily Portfolio Returns:

Tracking daily returns is crucial for evaluating the short-term performance of the portfolio. The script allows users to plot daily portfolio returns to gain insights into daily profit or loss, helping traders stay updated on their portfolio’s progress:

Performance Metrics

Net Profit (%):

This metric represents the total return on investment as a percentage of the initial capital. A positive net profit indicates that the portfolio has gained value over the evaluation period, while a negative value suggests a loss. It's a fundamental indicator of overall portfolio performance.

Maximum Drawdown (Max DD):

Maximum Drawdown measures the largest peak-to-trough decline in portfolio value during a specified period. It quantifies the most significant loss an investor would have experienced if they had invested at the highest point and sold at the lowest point within the timeframe. A smaller Max DD indicates better risk management and less exposure to significant losses.

Annual Mean Returns (% p/y):

This metric calculates the average annual return of the portfolio over the evaluation period. It provides insight into the portfolio's ability to generate returns on an annual basis, aiding in performance comparison with other investment opportunities.

Annual Standard Deviation of Returns (% p/y):

This measure indicates the volatility of the portfolio's returns on an annual basis. A higher standard deviation signifies greater variability in returns, implying higher risk, while a lower value suggests more stable returns.

Variance:

Variance is the square of the standard deviation and provides a measure of the dispersion of returns. It helps in understanding the degree of risk associated with the portfolio's returns.

Sortino Ratio:

The Sortino Ratio is a variation of the Sharpe Ratio that only considers downside risk, focusing on negative volatility. It is calculated as the difference between the portfolio's return and the minimum acceptable return (MAR), divided by the downside deviation. A higher Sortino Ratio indicates better risk-adjusted performance, emphasizing the importance of avoiding negative returns.

Sharpe Ratio:

The Sharpe Ratio measures the portfolio's excess return per unit of total risk, as represented by standard deviation. It is calculated by subtracting the risk-free rate from the portfolio's return and dividing by the standard deviation of the portfolio's excess return. A higher Sharpe Ratio indicates more favorable risk-adjusted returns.

Omega Ratio:

The Omega Ratio evaluates the probability of achieving returns above a certain threshold relative to the probability of experiencing returns below that threshold. It is calculated by dividing the cumulative probability of positive returns by the cumulative probability of negative returns. An Omega Ratio greater than 1 indicates a higher likelihood of achieving favorable returns.

Gain-to-Pain Ratio:

The Gain-to-Pain Ratio measures the return per unit of risk, focusing on the magnitude of gains relative to the severity of losses. It is calculated by dividing the total gains by the total losses experienced during the evaluation period. A higher ratio suggests a more favorable balance between reward and risk.

www.linkedin.com

Compound Annual Growth Rate (CAGR) (% p/y):

CAGR represents the mean annual growth rate of the portfolio over a specified period, assuming the investment has been compounding over that time. It provides a smoothed annual rate of growth, eliminating the effects of volatility and offering a clearer picture of long-term performance.

Portfolio Alpha (% p/y):

Portfolio Alpha measures the portfolio's performance relative to a benchmark index, adjusting for risk. It is calculated using the Capital Asset Pricing Model (CAPM) and represents the excess return of the portfolio over the expected return based on its beta and the benchmark's performance. A positive alpha indicates outperformance, while a negative alpha suggests underperformance.

Portfolio Beta:

Portfolio Beta assesses the portfolio's sensitivity to market movements, indicating its exposure to systematic risk. A beta greater than 1 suggests the portfolio is more volatile than the market, while a beta less than 1 indicates lower volatility. Beta is used to understand the portfolio's potential for gains or losses in relation to market fluctuations.

Skewness of Returns:

Skewness measures the asymmetry of the return distribution. A positive skew indicates a distribution with a long right tail, suggesting more frequent small losses and fewer large gains. A negative skew indicates a long left tail, implying more frequent small gains and fewer large losses. Understanding skewness helps in assessing the likelihood of extreme outcomes.

Value at Risk (VaR) 95th Percentile:

VaR at the 95th percentile estimates the maximum potential loss over a specified period, given a 95% confidence level. It provides a threshold value such that there is a 95% probability that the portfolio will not experience a loss greater than this amount.

Conditional Value at Risk (CVaR):

CVaR, also known as Expected Shortfall, measures the average loss exceeding the VaR threshold. It provides insight into the tail risk of the portfolio, indicating the expected loss in the worst-case scenarios beyond the VaR level.

These metrics collectively offer a comprehensive view of the portfolio's performance, risk exposure, and efficiency. By analyzing these indicators, investors can make informed decisions, balancing potential returns with acceptable levels of risk.

Conclusion

The Performance Metrics With Bracketed Rebalancing script provides a comprehensive framework for evaluating and optimizing portfolio performance. By integrating advanced metrics, adaptive rebalancing strategies, and visual analytics, it empowers traders to make informed decisions in managing their investment portfolios. However, it's crucial to consider the implications of rebalancing strategies, as academic research indicates that predictable rebalancing can lead to market impact costs. Therefore, adopting flexible and less predictable rebalancing approaches may enhance portfolio performance and reduce associated costs.

Risk-Adjusted Momentum Oscillator# Risk-Adjusted Momentum Oscillator (RAMO): Momentum Analysis with Integrated Risk Assessment

## 1. Introduction

Momentum indicators have been fundamental tools in technical analysis since the pioneering work of Wilder (1978) and continue to play crucial roles in systematic trading strategies (Jegadeesh & Titman, 1993). However, traditional momentum oscillators suffer from a critical limitation: they fail to account for the risk context in which momentum signals occur. This oversight can lead to significant drawdowns during periods of market stress, as documented extensively in the behavioral finance literature (Kahneman & Tversky, 1979; Shefrin & Statman, 1985).

The Risk-Adjusted Momentum Oscillator addresses this gap by incorporating real-time drawdown metrics into momentum calculations, creating a self-regulating system that automatically adjusts signal sensitivity based on current risk conditions. This approach aligns with modern portfolio theory's emphasis on risk-adjusted returns (Markowitz, 1952) and reflects the sophisticated risk management practices employed by institutional investors (Ang, 2014).

## 2. Theoretical Foundation

### 2.1 Momentum Theory and Market Anomalies

The momentum effect, first systematically documented by Jegadeesh & Titman (1993), represents one of the most robust anomalies in financial markets. Subsequent research has confirmed momentum's persistence across various asset classes, time horizons, and geographic markets (Fama & French, 1996; Asness, Moskowitz & Pedersen, 2013). However, momentum strategies are characterized by significant time-varying risk, with particularly severe drawdowns during market reversals (Barroso & Santa-Clara, 2015).

### 2.2 Drawdown Analysis and Risk Management

Maximum drawdown, defined as the peak-to-trough decline in portfolio value, serves as a critical risk metric in professional portfolio management (Calmar, 1991). Research by Chekhlov, Uryasev & Zabarankin (2005) demonstrates that drawdown-based risk measures provide superior downside protection compared to traditional volatility metrics. The integration of drawdown analysis into momentum calculations represents a natural evolution toward more sophisticated risk-aware indicators.

### 2.3 Adaptive Smoothing and Market Regimes

The concept of adaptive smoothing in technical analysis draws from the broader literature on regime-switching models in finance (Hamilton, 1989). Perry Kaufman's Adaptive Moving Average (1995) pioneered the application of efficiency ratios to adjust indicator responsiveness based on market conditions. RAMO extends this concept by incorporating volatility-based adaptive smoothing, allowing the indicator to respond more quickly during high-volatility periods while maintaining stability during quiet markets.

## 3. Methodology

### 3.1 Core Algorithm Design

The RAMO algorithm consists of several interconnected components:

#### 3.1.1 Risk-Adjusted Momentum Calculation

The fundamental innovation of RAMO lies in its risk adjustment mechanism:

Risk_Factor = 1 - (Current_Drawdown / Maximum_Drawdown × Scaling_Factor)

Risk_Adjusted_Momentum = Raw_Momentum × max(Risk_Factor, 0.05)

This formulation ensures that momentum signals are dampened during periods of high drawdown relative to historical maximums, implementing an automatic risk management overlay as advocated by modern portfolio theory (Markowitz, 1952).

#### 3.1.2 Multi-Algorithm Momentum Framework

RAMO supports three distinct momentum calculation methods:

1. Rate of Change: Traditional percentage-based momentum (Pring, 2002)

2. Price Momentum: Absolute price differences

3. Log Returns: Logarithmic returns preferred for volatile assets (Campbell, Lo & MacKinlay, 1997)

This multi-algorithm approach accommodates different asset characteristics and volatility profiles, addressing the heterogeneity documented in cross-sectional momentum studies (Asness et al., 2013).

### 3.2 Leading Indicator Components

#### 3.2.1 Momentum Acceleration Analysis

The momentum acceleration component calculates the second derivative of momentum, providing early signals of trend changes:

Momentum_Acceleration = EMA(Momentum_t - Momentum_{t-n}, n)

This approach draws from the physics concept of acceleration and has been applied successfully in financial time series analysis (Treadway, 1969).

#### 3.2.2 Linear Regression Prediction

RAMO incorporates linear regression-based prediction to project momentum values forward:

Predicted_Momentum = LinReg_Value + (LinReg_Slope × Forward_Offset)

This predictive component aligns with the literature on technical analysis forecasting (Lo, Mamaysky & Wang, 2000) and provides leading signals for trend changes.

#### 3.2.3 Volume-Based Exhaustion Detection

The exhaustion detection algorithm identifies potential reversal points by analyzing the relationship between momentum extremes and volume patterns:

Exhaustion = |Momentum| > Threshold AND Volume < SMA(Volume, 20)

This approach reflects the established principle that sustainable price movements require volume confirmation (Granville, 1963; Arms, 1989).

### 3.3 Statistical Normalization and Robustness

RAMO employs Z-score normalization with outlier protection to ensure statistical robustness:

Z_Score = (Value - Mean) / Standard_Deviation

Normalized_Value = max(-3.5, min(3.5, Z_Score))

This normalization approach follows best practices in quantitative finance for handling extreme observations (Taleb, 2007) and ensures consistent signal interpretation across different market conditions.

### 3.4 Adaptive Threshold Calculation

Dynamic thresholds are calculated using Bollinger Band methodology (Bollinger, 1992):

Upper_Threshold = Mean + (Multiplier × Standard_Deviation)

Lower_Threshold = Mean - (Multiplier × Standard_Deviation)

This adaptive approach ensures that signal thresholds adjust to changing market volatility, addressing the critique of fixed thresholds in technical analysis (Taylor & Allen, 1992).

## 4. Implementation Details

### 4.1 Adaptive Smoothing Algorithm

The adaptive smoothing mechanism adjusts the exponential moving average alpha parameter based on market volatility:

Volatility_Percentile = Percentrank(Volatility, 100)

Adaptive_Alpha = Min_Alpha + ((Max_Alpha - Min_Alpha) × Volatility_Percentile / 100)

This approach ensures faster response during volatile periods while maintaining smoothness during stable conditions, implementing the adaptive efficiency concept pioneered by Kaufman (1995).

### 4.2 Risk Environment Classification

RAMO classifies market conditions into three risk environments:

- Low Risk: Current_DD < 30% × Max_DD

- Medium Risk: 30% × Max_DD ≤ Current_DD < 70% × Max_DD

- High Risk: Current_DD ≥ 70% × Max_DD

This classification system enables conditional signal generation, with long signals filtered during high-risk periods—a approach consistent with institutional risk management practices (Ang, 2014).

## 5. Signal Generation and Interpretation

### 5.1 Entry Signal Logic

RAMO generates enhanced entry signals through multiple confirmation layers:

1. Primary Signal: Crossover between indicator and signal line

2. Risk Filter: Confirmation of favorable risk environment for long positions

3. Leading Component: Early warning signals via acceleration analysis

4. Exhaustion Filter: Volume-based reversal detection

This multi-layered approach addresses the false signal problem common in traditional technical indicators (Brock, Lakonishok & LeBaron, 1992).

### 5.2 Divergence Analysis

RAMO incorporates both traditional and leading divergence detection:

- Traditional Divergence: Price and indicator divergence over 3-5 periods

- Slope Divergence: Momentum slope versus price direction

- Acceleration Divergence: Changes in momentum acceleration

This comprehensive divergence analysis framework draws from Elliott Wave theory (Prechter & Frost, 1978) and momentum divergence literature (Murphy, 1999).

## 6. Empirical Advantages and Applications

### 6.1 Risk-Adjusted Performance

The risk adjustment mechanism addresses the fundamental criticism of momentum strategies: their tendency to experience severe drawdowns during market reversals (Daniel & Moskowitz, 2016). By automatically reducing position sizing during high-drawdown periods, RAMO implements a form of dynamic hedging consistent with portfolio insurance concepts (Leland, 1980).

### 6.2 Regime Awareness

RAMO's adaptive components enable regime-aware signal generation, addressing the regime-switching behavior documented in financial markets (Hamilton, 1989; Guidolin, 2011). The indicator automatically adjusts its parameters based on market volatility and risk conditions, providing more reliable signals across different market environments.

### 6.3 Institutional Applications

The sophisticated risk management overlay makes RAMO particularly suitable for institutional applications where drawdown control is paramount. The indicator's design philosophy aligns with the risk budgeting approaches used by hedge funds and institutional investors (Roncalli, 2013).

## 7. Limitations and Future Research

### 7.1 Parameter Sensitivity

Like all technical indicators, RAMO's performance depends on parameter selection. While default parameters are optimized for broad market applications, asset-specific calibration may enhance performance. Future research should examine optimal parameter selection across different asset classes and market conditions.

### 7.2 Market Microstructure Considerations

RAMO's effectiveness may vary across different market microstructure environments. High-frequency trading and algorithmic market making have fundamentally altered market dynamics (Aldridge, 2013), potentially affecting momentum indicator performance.

### 7.3 Transaction Cost Integration

Future enhancements could incorporate transaction cost analysis to provide net-return-based signals, addressing the implementation shortfall documented in practical momentum strategy applications (Korajczyk & Sadka, 2004).

## References

Aldridge, I. (2013). *High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems*. 2nd ed. Hoboken, NJ: John Wiley & Sons.

Ang, A. (2014). *Asset Management: A Systematic Approach to Factor Investing*. New York: Oxford University Press.

Arms, R. W. (1989). *The Arms Index (TRIN): An Introduction to the Volume Analysis of Stock and Bond Markets*. Homewood, IL: Dow Jones-Irwin.

Asness, C. S., Moskowitz, T. J., & Pedersen, L. H. (2013). Value and momentum everywhere. *Journal of Finance*, 68(3), 929-985.

Barroso, P., & Santa-Clara, P. (2015). Momentum has its moments. *Journal of Financial Economics*, 116(1), 111-120.

Bollinger, J. (1992). *Bollinger on Bollinger Bands*. New York: McGraw-Hill.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. *Journal of Finance*, 47(5), 1731-1764.

Calmar, T. (1991). The Calmar ratio: A smoother tool. *Futures*, 20(1), 40.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). *The Econometrics of Financial Markets*. Princeton, NJ: Princeton University Press.

Chekhlov, A., Uryasev, S., & Zabarankin, M. (2005). Drawdown measure in portfolio optimization. *International Journal of Theoretical and Applied Finance*, 8(1), 13-58.

Daniel, K., & Moskowitz, T. J. (2016). Momentum crashes. *Journal of Financial Economics*, 122(2), 221-247.

Fama, E. F., & French, K. R. (1996). Multifactor explanations of asset pricing anomalies. *Journal of Finance*, 51(1), 55-84.

Granville, J. E. (1963). *Granville's New Key to Stock Market Profits*. Englewood Cliffs, NJ: Prentice-Hall.

Guidolin, M. (2011). Markov switching models in empirical finance. In D. N. Drukker (Ed.), *Missing Data Methods: Time-Series Methods and Applications* (pp. 1-86). Bingley: Emerald Group Publishing.

Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. *Econometrica*, 57(2), 357-384.

Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. *Journal of Finance*, 48(1), 65-91.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. *Econometrica*, 47(2), 263-291.

Kaufman, P. J. (1995). *Smarter Trading: Improving Performance in Changing Markets*. New York: McGraw-Hill.

Korajczyk, R. A., & Sadka, R. (2004). Are momentum profits robust to trading costs? *Journal of Finance*, 59(3), 1039-1082.

Leland, H. E. (1980). Who should buy portfolio insurance? *Journal of Finance*, 35(2), 581-594.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of technical analysis: Computational algorithms, statistical inference, and empirical implementation. *Journal of Finance*, 55(4), 1705-1765.

Markowitz, H. (1952). Portfolio selection. *Journal of Finance*, 7(1), 77-91.

Murphy, J. J. (1999). *Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications*. New York: New York Institute of Finance.

Prechter, R. R., & Frost, A. J. (1978). *Elliott Wave Principle: Key to Market Behavior*. Gainesville, GA: New Classics Library.

Pring, M. J. (2002). *Technical Analysis Explained: The Successful Investor's Guide to Spotting Investment Trends and Turning Points*. 4th ed. New York: McGraw-Hill.

Roncalli, T. (2013). *Introduction to Risk Parity and Budgeting*. Boca Raton, FL: CRC Press.

Shefrin, H., & Statman, M. (1985). The disposition to sell winners too early and ride losers too long: Theory and evidence. *Journal of Finance*, 40(3), 777-790.

Taleb, N. N. (2007). *The Black Swan: The Impact of the Highly Improbable*. New York: Random House.

Taylor, M. P., & Allen, H. (1992). The use of technical analysis in the foreign exchange market. *Journal of International Money and Finance*, 11(3), 304-314.

Treadway, A. B. (1969). On rational entrepreneurial behavior and the demand for investment. *Review of Economic Studies*, 36(2), 227-239.

Wilder, J. W. (1978). *New Concepts in Technical Trading Systems*. Greensboro, NC: Trend Research.

Money Risk Management with Trade Tracking

Overview

The Money Risk Management with Trade Tracking indicator is a powerful tool designed for traders on TradingView to simplify trade simulation and risk management. Unlike the TradingView Strategy Tester, which can be complex for beginners, this indicator provides an intuitive, beginner-friendly interface to evaluate trading strategies in a realistic manner, mirroring real-world trading conditions.

Built on the foundation of open-source contributions from LuxAlgo and TCP, this indicator integrates external indicator signals, overlays take-profit (TP) and stop-loss (SL) levels, and provides detailed money management analytics. It empowers traders to visualize potential profits, losses, and risk-reward ratios, making it easier to understand the financial outcomes of their strategies.

Key Features

Signal Integration: Seamlessly integrates with external long and short signals from other indicators, allowing traders to overlay TP/SL levels based on their preferred strategies.

Realistic Trade Simulation: Simulates trades as they would occur in real-world scenarios, accounting for initial capital, risk percentage, leverage, and compounding effects.

Money Management Dashboard: Displays critical metrics such as current capital, unrealized P&L, risk amount, potential profit, risk-reward ratio, and trade status in a customizable, beginner-friendly table.

TP/SL Visualization: Plots TP and SL levels on the chart with customizable styles (solid, dashed, dotted) and colors, along with optional labels for clarity.

Performance Tracking: Tracks total trades, win/loss counts, win rate, and profit factor, providing a clear overview of strategy performance.

Liquidation Risk Alerts: Warns traders if stop-loss levels risk liquidation based on leverage settings, enhancing risk awareness.

Benefits for Traders

Beginner-Friendly: Simplifies the complexities of the TradingView Strategy Tester, offering an intuitive interface for new traders to simulate and evaluate trades without confusion.

Real-World Insights: Helps traders understand the actual profit or loss potential of their strategies by factoring in capital, risk, and leverage, bridging the gap between theoretical backtesting and real-world execution.

Enhanced Decision-Making: Provides clear, real-time analytics on risk-reward ratios, unrealized P&L, and trade performance, enabling informed trading decisions.

Customizable and Flexible: Allows customization of TP/SL settings, table positions, colors, and sizes, catering to individual trader preferences.

Risk Management Focus: Encourages disciplined trading by highlighting risk amounts, potential profits, and liquidation risks, fostering better financial planning.

Why This Indicator Stands Out

Many traders struggle to translate backtested strategy results into real-world outcomes due to the abstract nature of percentage-based profitability metrics. This indicator addresses that challenge by providing a practical, user-friendly tool that simulates trades with real-world parameters like capital, leverage, and compounding. Its open-source nature ensures accessibility, while its integration with other indicators makes it versatile for various trading styles.

How to Use

Add to TradingView: Copy the Pine Script code into TradingView’s Pine Editor and add it to your chart.

Configure Inputs: Set your initial capital, risk percentage, leverage, and TP/SL values in the indicator settings. Select external long/short signal sources if integrating with other indicators.

Monitor Dashboards: Use the Money Management and Target Dashboard tables to track trade performance and risk metrics in real time.

Analyze Results: Review win rates, profit factors, and P&L to refine your trading strategy.

Credits

This indicator builds upon the open-source contributions of LuxAlgo and TCP , whose efforts in sharing their code have made this tool possible. Their dedication to the trading community is deeply appreciated.

Macro Context v1 - NobruzeraaaHMacro Context v1

Advanced Multi-Asset Correlation Analysis for Professional Trading

"In institutional trading, correlation is king. This panel puts the crown on your charts."

Overview

This is a sophisticated real-time market analysis tool that monitors critical institutional correlations across traditional and cryptocurrency markets. This indicator provides traders with actionable insights based on academic research and institutional trading patterns.

Features

- **Multi-Asset Correlation Engine**

- **13 Advanced Analysis Layers** covering macro, crypto, and institutional flows

- **Real-time Correlation Detection** between BTC, equities, bonds, and commodities

- **Institutional Divergence Alerts** for early trend identification

- **Risk Sentiment Analysis** using VIX, DXY, and yield curve data

**Professional Grade Analytics**

- **NDX/SPX vs BTC Correlation** - Critical tech-crypto relationship monitoring

- **VIX Breakout Detection** - Institutional panic (>30) and dangerous complacency (<15) alerts

- **Yield Curve Inversion Monitoring** - Recession signal detection via US10Y-US2Y spread

- **Institutional Flow Tracking** - Real proxies using MSTR/COIN performance

- **DXY Critical Levels** - USD dominance (>105) and weakness (<95) thresholds

**Smart Actionable Signals**

- **Opportunity Detection** in altcoins during confirmed risk-on periods

- **Divergence Warnings** when BTC-Tech correlations break down

- **Volatility Preparation** alerts during market complacency

- **Hedge Recommendations** during institutional flight to quality

Correlation Matrix Monitored

**Traditional Markets**

| Asset | Function | Institutional Significance |

|-------|----------|---------------------------|

| **SPX** | Equity benchmark | Risk-on/off sentiment |

| **NDX** | Tech growth proxy | Innovation capital flows |

| **VIX** | Volatility index | Fear/greed institutional gauge |

| **DXY** | Dollar strength | Global liquidity flows |

| **US10Y-US2Y** | Yield curve | Recession probability |

| **Gold** | Safe haven | Inflation hedge demand |

| **Copper** | Industrial metal | Growth expectations |

**Cryptocurrency Markets**

| Asset | Function | Institutional Significance |

|-------|----------|---------------------------|

| **BTC** | Digital store of value | Institutional adoption gauge |

| **ETH** | Smart contract platform | DeFi institutional interest |

| **BTC.D** | Bitcoin dominance | Crypto capital allocation |

| **USDT.D** | Stablecoin dominance | Risk-off crypto indicator |

| **TOTAL3** | Alt market cap | Retail vs institutional flow |

**Institutional Proxies**

| Asset | Function | Why It Matters |

|-------|----------|----------------|

| **MSTR** | MicroStrategy stock | Corporate BTC holdings proxy |

| **COIN** | Coinbase stock | Crypto institutional gateway |

---

Critical Correlations Detected

**1. Tech-Led Risk-On Confirmation**

**Trigger:** NDX outperforming SPX + BTC rising + VIX declining

**Signal:** Strong institutional appetite for growth assets

**Action:** Opportunity in tech and crypto momentum

**2. BTC-Tech Divergence Warning**

**Trigger:** NDX/SPX ratio positive + BTC declining significantly

**Signal:** Potential institutional crypto exit while maintaining tech exposure

**Action:** Monitor for broader crypto weakness

**3. Institutional Panic Mode**

**Trigger:** VIX > 30 + USDT.D rising + BTC/equities declining

**Signal:** Fear-driven liquidations across all risk assets

**Action:** Wait for clarity, prepare for volatility

**4. Dangerous Complacency**

**Trigger:** VIX < 15 + low volatility across assets

**Signal:** Market complacency reaching dangerous levels

**Action:** Prepare for sudden volatility spike

**5. Yield Curve Recession Signal**

**Trigger:** US10Y-US2Y spread deeply inverted (<-0.5%)

**Signal:** Bond market pricing in economic slowdown

**Action:** Defensive positioning, reduce risk exposure

**6. USD Super-Dominance**

**Trigger:** DXY > 105 + gold declining + risk assets under pressure

**Signal:** Extreme USD strength creating global liquidity stress

**Action:** Monitor emerging market stress, dollar-denominated debt concerns

**7. Altseason Confirmation**

**Trigger:** BTC.D declining + USDT.D declining + TOTAL3 outperforming + low VIX

**Signal:** Capital rotating from BTC to altcoins in risk-on environment

**Action:** Opportunity in alternative cryptocurrencies

---

Advanced Analytics Provided

**Risk Sentiment Classification**

- 🔴 **Fear in System** - Multiple fear indicators triggered

- 🟡 **Cautious Mode** - Mixed signals, proceed carefully

- 🟢 **Risk Appetite** - Confirmed risk-on environment

- 🟢 **Strong Risk-On** - Multiple bullish confirmations

- 🟠 **Dangerous Complacency** - Excessive optimism warning

**Macro Context Analysis**

- 💪 **Dollar Dominant** - USD strength driving global flows

- 🌍 **USD Weakening** - Emerging market and commodity positive

- ⚠️ **Market Stress** - Multiple stress indicators active

- 🚀 **Solid Bull Market** - Confirmed uptrend across assets

- 🏭 **Growth Acceleration** - Copper/Gold ratio signaling expansion

- 🛡️ **Defensive Rotation** - Flight to quality assets

**Actionable Intelligence**

- ✅ **Opportunity in Alts** - Multiple confirmations for altcoin exposure

- ⚠️ **Wait for Clarity** - High uncertainty, avoid new positions

- 🏛️ **Consider Hedge** - Defensive positioning recommended

- 📈 **Ride Momentum** - Trend continuation likely

- 🔍 **Monitor Divergence** - Correlation breakdown warning

- ⚠️ **Prepare for Volatility** - Complacency extreme reached

Technical Implementation

**Data Sources**

- **Traditional Markets:** TradingView real-time feeds

- **Cryptocurrency:** Binance spot prices and market cap data

- **Macro Data:** US Treasury yields, volatility indices

- **Update Frequency:** Every minute during market hours

**Calculation Methodology**

- **24-hour percentage changes** for all assets

- **Real-time price levels** for VIX and DXY thresholds

- **Spread calculations** for yield curve analysis

- **Ratio analysis** for relative performance metrics

**Multi-Language Support**

- 🇺🇸 **English** - Full professional terminology

- 🇪🇸 **Spanish** - Complete translation for Latin American markets

- 🇧🇷 **Portuguese** - Brazilian market terminology

---

Academic Foundation

This indicator is built upon peer-reviewed research and institutional trading patterns:

**Research-Based Correlations**

- **Bitcoin-NASDAQ correlation studies** (2024 academic papers)

- **VIX threshold analysis** from institutional trading desks

- **Yield curve inversion** recession prediction models

- **Dollar index breakout** historical analysis

- **Cryptocurrency dominance** flow studies

**Institutional Insights**

- **Fear & Greed Index** methodology adaptation

- **Professional volatility** threshold implementation

- **Corporate treasury** Bitcoin adoption tracking

- **Institutional proxy** correlation validation

---

Quick Start Guide

**Configuration**

- **Language Selection:** Choose your preferred language

- **Asset Selection:** Enable/disable specific asset monitoring

- **Timezone:** Set your preferred timezone for timestamp display

**Interpretation**

- **Green indicators:** Bullish/risk-on signals

- **Red indicators:** Bearish/risk-off signals

- **Yellow indicators:** Neutral/mixed signals

- **Orange indicators:** Warning/extreme conditions

---

Use Cases

**Traders**

- **Portfolio allocation** based on institutional flows

- **Risk management** through correlation monitoring

- **Market timing** using sentiment extremes

- **Divergence trading** opportunities

**Analysts**

- **Multi-asset correlation** research

- **Macro theme** identification

- **Risk sentiment** quantification

- **Flow analysis** across asset classes

**Cryptocurrency Investors**

- **Altseason timing** through dominance analysis

- **Macro correlation** understanding

- **Institutional adoption** tracking

- **Risk-on/off** positioning

---

Important Disclaimers

- **Not Financial Advice:** This tool provides analytical insights, not investment recommendations

- **Market Risk:** All trading involves substantial risk of loss

- **Correlation Changes:** Market correlations can shift rapidly during crisis periods

- **Supplementary Tool:** Should be used alongside other analysis methods

This indicator represents cutting-edge market analysis combining traditional finance and cryptocurrency insights. Regular updates ensure continued accuracy as market structures evolve.

**Version:** 1.0

**Last Updated:** 2025

**Compatibility:** Pine Script v6

**Category:** Multi-Asset Analysis

The LEAP Contest - Symbol & Max Position Table TrackerDescription:

This indicator tracks the maximum contracts allowed to be traded for TradingView’s *"The Leap"* Contest. It displays a horizontal table at the bottom right of your chart showing up to 20 symbols along with their maximum allowable open contract positions.

Use case:

Designed specifically for traders participating in *The Leap* Contest on TradingView.

Users need to enter the symbol and the maximum contracts allowed for that symbol in the settings menu for each new contest.

It provides a quick reference to ensure compliance with contest rules on maximum position sizes.

How it works:

The table shows two rows: the top row displays the symbol name, and the bottom row shows the max contract limit.

If the currently loaded chart symbol matches any symbol in the list, its text color changes to yellow .

Customization:

Symbols and limits must be updated in the indicator’s settings before each contest to reflect the current rules.

PCA Regime-Adjusted MomentumSummary

The PCA Regime-Adjusted Momentum (PCA-RAM) is an advanced market analysis tool designed to provide nuanced insights into market momentum and structural stability. It moves beyond traditional indicators by using Principal Component Analysis (PCA) to deconstruct market data into its most essential patterns.

The indicator provides two key pieces of information:

A smoothed momentum signal based on the market's dominant underlying trend.

A dynamic regime filter that gauges the stability and clarity of the market's structure, advising you when to trust or fade the momentum signals.

This allows traders to not only identify potential shifts in momentum but also to understand the context and confidence behind those signals.

Core Concepts & Methodology

The strength of this indicator lies in its sound, data-driven methodology.

1. Principal Component Analysis (PCA)

At its core, the indicator analyzes a rolling window (default 50 periods) of standardized market data (Open, High, Low, Close, and Volume). PCA is a powerful statistical technique that distills this complex, 5-dimensional data into its fundamental, uncorrelated components of variance. We focus on the First Principal Component (PC1), which represents the single most dominant pattern or "theme" driving the market's behavior in the lookback window.

2. The Momentum Signal

Instead of just looking at price, we project the current market data onto this dominant underlying pattern (PC1). This gives us a raw "projection score" that measures how strongly the current bar aligns with the historically dominant market structure. This raw score is then smoothed using two an exponential moving averages (a fast and a slow line) to create a clear, actionable momentum signal, similar in concept to a MACD.

3. The Dynamic Regime Filter

This is arguably the indicator's most powerful feature. It answers the question: "How clear is the current market picture?"

It calculates the Market Concentration Ratio, which is the percentage of total market variance explained by PC1 alone.

A high ratio indicates that the market is moving in a simple, one-dimensional way (e.g., a clear, strong trend).

A low ratio indicates the market is complex, multi-dimensional, and choppy, with no single dominant theme.

Crucially, this filter is dynamic. It compares the current concentration ratio to its own recent average, allowing it to adapt to any asset or timeframe. It automatically learns what "normal" and "choppy" look like for the specific chart you are viewing.

How to Interpret the Indicator

The indicator is displayed in a separate pane with two key visual elements:

The Momentum Lines (White & Gold)

White Line: The "Fast Line," representing the current momentum.

Gold Line: The "Slow Line," acting as the trend confirmation.

Bullish Signal: A crossover of the White Line above the Gold Line suggests a shift to positive momentum.

Bearish Signal: A crossover of the White Line below the Gold Line suggests a shift to negative momentum.

The Regime Filter (Purple & Dark Red Background)

This is your confidence gauge.

Navy Blue Background (High Concentration): The market structure is stable, simple, and trending. Momentum signals are more reliable and should be given higher priority.

Dark Red Background (Low Concentration): The market structure is complex, choppy, or directionless. Momentum signals are unreliable and prone to failure or "whipsaws." This is a signal to be cautious, tighten stops, or potentially stay out of the market.

Potential Trading Strategies

This tool is versatile and can be used in several ways:

1. Primary Signal Strategy

Condition: Wait for the background to turn Purple, confirming a stable, high-confidence regime.

Entry: Take the next crossover signal from the momentum lines (White over Gold for long, White under Gold for short).

Exit/Filter: Consider exiting positions or ignoring new signals when the background turns Navy.

2. As a Confirmation or Filter for Your Existing Strategy

Do you have a trend-following system? Only enable its long and short signals when the PCA-RAM background is Purple.

Do you have a range-trading or mean-reversion system? It might be most effective when the PCA-RAM background is Navy, indicating a lack of a clear trend.

3. Advanced Divergence Analysis

Look for classic divergences between price and the momentum lines. For example, if the price is making a new high, but the Gold Line is making a lower high, it may indicate underlying weakness in the trend, even on a Purple background. This divergence signal is more powerful because it shows that the new price high is not being confirmed by the market's dominant underlying pattern.

Correlation MA – 15 Assets + Average (Optional)This indicator calculates the moving average of the correlation coefficient between your charted asset and up to 15 user-selected symbols. It helps identify uncorrelated or inversely correlated assets for diversification, pair trading, or hedging.

Features:

✅ Compare your current chart against up to 15 assets

✅ Toggle assets on/off individually

✅ Custom correlation and MA lengths

✅ Real-time average correlation line across enabled assets

✅ Horizontal lines at +1, 0, and -1 for easy visual reference

Ideal for:

Portfolio diversification analysis

Finding low-correlation stocks

Mean-reversion & pair trading setups

Crypto, equities, ETFs

To use: set the benchmark chart (e.g. TSLA), choose up to 15 assets, and adjust settings as needed. Look for assets with correlation near 0 or negative values for uncorrelated performance.

Dr Avinash Talele momentum indicaterTrend and Volatility Metrics

EMA10, EMA20, EMA50:

Show the percentage distance of the current price from the 10, 20, and 50-period Exponential Moving Averages.

Positive values indicate the price is above the moving average (bullish momentum).

Negative values indicate the price is below the moving average (bearish or corrective phase).

Use: Helps traders spot if a stock is extended or pulling back to support.

RVol (Relative Volume):

Compares current volume to the 20-day average.

Positive values mean higher-than-average trading activity (potential institutional interest).

Negative values mean lower activity (less conviction).

Use: High RVol often precedes strong moves.

ADR (Average Daily Range):

Shows the average daily price movement as a percentage.

Use: Higher ADR = more volatility = more trading opportunities.

50D Avg. Vol & 50D Avg. Vol ₹:

The 50-day average volume (in millions) and value traded (in crores).

Use: Confirms liquidity and suitability for larger trades.

ROC (Rate of Change) Section

1W, 1M, 3M, 6M, 12M:

Show the percentage price change over the last 1 week, 1 month, 3 months, 6 months, and 12 months.

Positive values (green) = uptrend, Negative values (red) = downtrend.

Use: Quickly see if the stock is gaining or losing momentum over different timeframes.

Momentum Section

1M, 3M, 6M:

Show the percentage gain from the lowest price in the last 1, 3, and 6 months.

Use: Measures how much the stock has bounced from recent lows, helping find strong rebounds or new leaders.

52-Week High/Low Section

From 52WH / From 52WL:

Show how far the current price is from its 52-week high and low, as a percentage.

Closer to 52WH = strong uptrend; Closer to 52WL = possible value or turnaround setup.

Use: Helps traders identify stocks breaking out to new highs or rebounding off lows.

U/D Ratio

U/D Ratio:

The ratio of up-volume to down-volume over the last 50 days.

Above 1 = more buying volume (bullish), Below 1 = more selling volume (bearish).

Use: Confirms accumulation or distribution.

How This Table Helps Analysts and Traders

Instant Trend Assessment:

With EMA distances and ROC, analysts can instantly see if the stock is trending, consolidating, or reversing.

Momentum Confirmation:

ROC and Momentum sections highlight stocks with strong recent moves, ideal for momentum and breakout traders.

Liquidity and Volatility Check:

Volume and ADR ensure the stock is tradable and has enough price movement to justify a trade.

Relative Positioning:

52-week high/low stats show whether the stock is near breakout levels or potential reversal zones.

Volume Confirmation:

RVol and U/D ratio help confirm if moves are backed by real buying/selling interest.

Actionable Insights:

By combining these metrics, traders can filter for stocks with strong trends, robust momentum, and institutional backing—ideal for swing, position, or even intraday trading.

LTA - Futures Contract Size CalculatorLTA - Futures Contract Size Calculator

This indicator helps futures traders calculate the potential stop-loss (SL) value for their trades with ease. Simply input your entry price, stop-loss price, and number of contracts, and the indicator will compute the ticks moved, price movement, and total SL value in USD.

Key Features:

Supports a wide range of futures contracts, including:

Index Futures: E-mini S&P 500 (ES), Micro E-mini S&P 500 (MES), E-mini Nasdaq-100 (NQ), Micro E-mini Nasdaq-100 (MNQ)

Commodity Futures: Crude Oil (CL), Gold (GC), Micro Gold (MGC), Silver (SI), Micro Silver (SIL), Platinum (PL), Micro Platinum (MPL), Natural Gas (NG), Micro Natural Gas (MNG)

Bond Futures: 30-Year T-Bond (ZB)

Currency Futures: Euro FX (6E), Japanese Yen (6J), Australian Dollar (6A), British Pound (6B), Canadian Dollar (6C), Swiss Franc (6S), New Zealand Dollar (6N)

Displays key metrics in a clean table (bottom-right corner):

Instrument, Entry Price, Stop-Loss Price, Number of Contracts, Tick Size, Ticks Moved, Price Movement, and Total SL Value.

Automatically calculates based on the selected instrument’s tick size and tick value.

User-friendly interface with a dark theme for better visibility.

How to Use:

Add the indicator to your chart.

Select your instrument from the dropdown (ensure it matches your chart’s symbol, e.g., "NG1!" for NATURAL GAS (NG)).

Input your Entry Price, Stop-Loss Price, and Number of Contracts.

View the results in the table, including the Total SL Value in USD.

Ideal For:

Futures traders looking to quickly assess stop-loss risk.

Beginners and pros trading indices, commodities, bonds, or currencies.

Note: Ensure your chart symbol matches the selected instrument for accurate calculations. For best results, test with a few contracts and price levels to confirm the output.

This description is tailored for TradingView’s audience, providing a clear overview of the indicator’s functionality, supported instruments, and usage instructions. It also includes a note to help users avoid common pitfalls (e.g., mismatched symbols). If you’d like to adjust the tone, add more details, or include specific TradingView tags (e.g., , ), let me know!

Zen Lab Checklist - FNSThe Zen Lab Checklist - FNS is a simple yet powerful visual trading assistant designed to help traders maintain discipline and consistency in their trading routines. This provides a customizable on-screen checklist. This indicator allows traders to verify key conditions before entering a trade which will help identify trade quality and promote structured trading habits. This indicator is ideal for discretionary traders who follow a consistent set of entry rules.

✅ Key Features

Customizable Checklist Items:

Define up to 6 checklist labels with on/off toggle switches to track your trade criteria.

Visual Feedback:

Each checklist item displays a ✅ checkmark when conditions are met or a ❌ cross when not. Colors are visually distinct — green for confirmed, red for not confirmed.

Progress Tracker:

A "Trade Score" footer calculates a "trade score" percentage, helping you quickly assess the trade idea quality and readiness.

Table Position Control:

Easily adjust the table’s position on your chart (e.g., top-right, middle-center, bottom-left) using a dropdown menu.

Custom Styling Options:

- Change background and font color of checklist rows.

- Set font size (tiny to huge).

- Set the header and footer colors separately for visual contrast. (default is green background with white font)

📌 How to Use

- Open the indicator settings.

- Label your checklist items to match your personal or strategy-specific rules.

- Toggle the corresponding switches based on your trade setup conditions.

- Review the on-chart checklist and "Trade Score" to confirm your trade decision.

🎯 Why Use This?

- Discipline: Keeps you aligned with your trading plan.

- Clarity: Clear visual indicator of trade readiness.

- Efficiency: Saves time by centralizing your checklist visually on your chart.

- Custom Fit: Adapt the labels and styling to match your strategy or preferences.

⚠️ Notes

This is a manual checklist, meaning you control the toggle switches based on your judgment.

Ideal for discretionary traders who follow a consistent set of entry rules.

Stop Loss & Take Profit For Overlay Indicators[LePasha] Stop Loss & Take Profit For Overlay Indicators

This indicator helps traders easily visualize Stop Loss (SL) and Take Profit (TP) levels based on custom buy and sell signals from any overlay indicators or price-based sources.

Key Features:

Accepts buy and sell signals from any indicator or price source on your chart.

Automatically calculates SL and TP levels using ATR-based volatility for dynamic risk management.

Allows customization of capital, risk percentage per trade, and reward-to-risk ratio.

Displays clear colored boxes on the chart showing potential profit and loss zones.

Calculates position size and required leverage based on your risk settings.

Designed to work with your preferred strategies by simply connecting signal inputs.

Helps you visually manage trades with precise risk control and reward targets.

How to Use:

Connect your buy and sell signals (e.g., from Moving Average crossovers, custom scripts, or price levels) to the indicator’s inputs.

Adjust risk settings to fit your trading style (capital, risk %, reward ratio).

Watch as the indicator draws TP and SL zones on your chart when signals occur.

Use this information to set stops and targets in your trades confidently.

Perfect for traders who want simple, clear, and reliable trade management visuals based on their own strategy signals.

AsturRiskPanelIndicator Summary

ATR Engine

Length & Smoothing: Choose how many bars to use (default 14) and the smoothing method (RMA/SMA/EMA/WMA).

Median ATR: Computes a rolling median of ATR over a user-defined look-back (default 14) to derive a “scalp” target.

Scalp Target

Automatically set at ½ × median ATR, snapped to the nearest tick.

Optional rounding to whole points for simplicity.

Stop Calculation

ATR Multiplier: Scales current ATR by a user input (default 1.5) to produce your stop distance in points (and ticks when appropriate).

Distortion Handling: Switches between point-only and point + tick displays based on contract specifications.

Risk & Sizing

Risk % of account per trade (default 2 %).

Calculates dollar risk per contract and optimal contract count.

Displays all metrics (scalp, stop, risk/contract, max contracts, max risk, account size) in a customizable on-chart table.

ATR-Based Stop Placement Guidelines

Trade Context ATR Multiplier Notes

Tight Range Entry 1.0 × ATR High-conviction, precise entries. Expect more shake-outs.

Standard Trend Entry 1.5 × ATR Balanced for H2/L2, MTR, DT/DB entries.

Breakouts/Microchannels 2.0 × ATR Wide stops through chop—Brooks-style breathing room.

How to Use

Select ATR Settings

Pick an ATR length (e.g. 14) and smoothing (RMA for stability).

Adjust the median length if you want a faster/slower scalp line.

Align Multiplier with Your Setup

For tight-range entries, set ATR Multiplier ≈ 1.0.

For standard trend trades, leave at 1.5.

For breakout/pullback setups, increase to 2.0 or more.

Customize Risk Parameters

Enter your account size and desired risk % per trade (e.g. 2 %).

The table auto-calculates how many contracts you can take.

Read the On-Chart Table

Scalp shows your intraday target.

Stop gives Brooks-style stop distance in points (and ticks).

Risk/Contract is the dollar risk per contract.

Max Contracts tells you maximum position size.

Max Risk confirms total dollar exposure.

Visual Confirmation

Place your entry, then eyeball the scalp and stop levels against chart structure (e.g. swing highs/lows).

Adjust the ATR multiplier if market context shifts (e.g. volatility spikes).

By blending this sizing panel with contextual ATR multipliers, you’ll consistently give your trades the right amount of “breathing room” while keeping risk in check.

Profit Guard ProProfitGuard Pro

ProfitGuard Pro is a risk management and profit calculation tool that helps traders optimize their trades by handling position sizing, risk management, leverage, and take profit calculations. With support for both cumulative and non-cumulative take profit strategies, this versatile indicator provides the insights you need to maximize your trading strategy.

How to Use ProfitGuard Pro:

Load the Indicator: Add ProfitGuard Pro to your chart in TradingView.

Set Your Entry Position: Input your desired entry price.

Define Your Stop Loss: Enter the price at which your trade will exit to minimize losses.

Add Take Profit Levels: Input your TP1, TP2, TP3, and TP4 levels, as needed.

If you want fewer take profit levels, adjust the number of TPs in the settings menu. You can choose between 1 to 4 take profit levels based on your strategy.

Adjust Risk Settings: Specify your account size and risk percentage to calculate position size and leverage.

Choose Cumulative or Non-Cumulative Mode: Toggle cumulative profit mode to either recalculate position sizes as each take profit is hit or keep position sizes static for each TP.

Once set up, ProfitGuard Pro will automatically calculate your position size, leverage, and potential profits for each take profit level, providing a clear visual on your chart to guide your trading decisions.

Key Features:

Risk Management:

Calculate your risk percentage based on account size and stop loss.

Visualize risk in dollar terms and percentage of your account.

Position Size & Leverage:

Automatically calculate the ideal position size and leverage for your trade based on your entry, stop loss, and risk settings.

Ensure you are trading with the appropriate leverage for your account size.

Cumulative vs Non-Cumulative Profit Mode:

Cumulative Mode: Adjusts position size after each take profit is reached, recalculating for remaining contracts.

Non-Cumulative Mode: Treats each take profit as a separate calculation using the full position size.

Take Profit Levels:

Set up to 4 customizable take profit levels.

Adjust percentage values for each TP target, and visualize them on your chart with easy-to-read lines.

Profit Calculation:

Displays potential profits for each take profit level based on whether cumulative or non-cumulative mode is selected.

Calculate your risk-reward ratio dynamically at each TP.

Customizable Visuals:

Easily customize the table's size, position, and color scheme to fit your chart.

Visualize key trade details like leverage, contracts, margin, and profits directly on your chart.

Short and Long Position Support:

Automatically adjusts calculations based on whether you're trading long or short.

Value at Risk (VaR/CVaR) - Stop Loss ToolThis script calculates Value at Risk (VaR) and Conditional Value at Risk (CVaR) over a configurable T-bar forward horizon, based on historical T-bar log returns. It plots projected price thresholds that reflect the worst X% of historical return outcomes, helping set statistically grounded stop-loss levels.

A 95% 5-day VaR of −3% means: “In the worst 5% of all historical 5-day periods, losses were 3% or more.” If you're bullish, and your thesis is correct, price should not behave like one of those worst-case scenarios. So if the market starts trading below that 5-day VaR level, it may indicate that your long bias is invalidated, and a stop-loss near that level can help protect against further downside consistent with tail-risk behavior.

How it's different:

Unlike ATR or standard deviation-based methods, which measure recent volatility magnitude, VaR/CVaR incorporate both the magnitude and **likelihood** (5% chance for example) of adverse moves. This makes it better suited for risk-aware position sizing and exits grounded in actual historical return distributions.

How to use for stop placement:

- Set your holding horizon (T) and confidence level (e.g., 95%) in the inputs.

- The script plots a price level below which only the worst 5% (or chosen %) of T-bar returns have historically occurred (VaR).

- If price approaches or breaches the VaR line, your bullish/bearish thesis may be invalidated.

- CVaR gives a deeper threshold: the average loss **if** things go worse than VaR — useful for a secondary or emergency stop.

FURTHER NOTES FROM SOURCE CODE:

//======================================================================//

// If you're bullish (expecting the price to go up), then under normal circumstances, prices should not behave like they do on the worst-case days.

// If they are — you're probably wrong, or something unexpected is happening. Basically, returns shouldn't be exhibiting downside tail-like behavior if you're bullish.

// VaR(95%, T) gives the threshold below which the price falls only 5% of the time historically, over T days/bars and considering N historical samples.

// CVaR tells you the expected/average price level if that adverse move continues

// Caveats:

// For a variety of reasons, VaR underestimates volatility, despite using historical returns directly rather than making normality assumptions

// as is the case with the standard historicalvol/bollinger band/stdev/ATR approaches)

// Volatility begets volatility (volatility clustering), and VaR is not a conditional probability on recent volatility so it likely underestimates the true volatility of an adverse event

// Regieme shifts occur (bullish phase after prolonged bearish behavior), so upside/short VaR would underestimate the best-case days in the beginning of that move, depending on lookahead horizon/sampling period

// News/events happen, and maybe your sampling period doesn't contain enough event-driven returns to form reliable stats

// In general of course, this tool assumes past return distributions are reflective of forward risk (not the case in non-stationary time series)

// Thus, this tool is not predictive — it shows historical tail risk, not guaranteed outcomes.

// Also, when forming log-returns, overlapping windows of returns are used (to get more samples), but this introduces autocorrelation (if it wasn't there already). This means again, the true VaR is underestimated.

// Description:

// This script calculates and plots both Value at Risk (VaR) and

// Conditional Value at Risk (CVaR) for a given confidence level, using

// historical log returns. It computes both long-side (left tail) and

// short-side (right tail) risk, and converts them into price thresholds (red and green lines respectively).

//

// Key Concepts:

// - VaR: "There is a 95% chance the loss will be less than this value over T days. Represents the 95th-percentile worst empirical returns observed in the sampling period, over T bars.

// - CVaR: "Given that the loss exceeds the VaR, the average of those worst 5% losses is this value. (blue line)" Expected tail loss. If the worst case breached, how bad can it get on average

// - For shorts, the script computes the mirror (right-tail) equivalents.

// - Use T-day log returns if estimating risk over multiple days forward.

// - You can see instances where the VaR for time T, was surpassed historically with the "backtest" boolean

//

// Usage for Stop-Loss:

// - LONG POSITIONS:

// • 95th percentile means, 5% of the time (1 in 20 times) you'd expect to get a VaR level loss (touch the red line), over the next T bars.

// • VaR threshold = minimum price expected with (1 – confidence)% chance.

// • CVaR threshold = expected price if that worst-case zone is breached.

// → Use as potential stop-loss (VaR) or disaster stop (CVaR). If you're bullish (and you're right), price should not be exhibiting returns consistent with the worst 5% of days/T_bars historically.

//======================================================================//

1A Monthly P&L Table - Using Library1A Monthly P&L Table: Track Your Performance Month-by-Month

Overview:

The 1A Monthly P&L Table is a straightforward yet powerful indicator designed to give you an immediate overview of your asset's (or strategy's) percentage performance on a monthly basis. Displayed conveniently in the bottom-right corner of your chart, this tool helps you quickly assess historical gains and losses, making it easier to analyze trends in performance over time.

Key Features:

Monthly Performance at a Glance: Clearly see the percentage change for each past month.

Cumulative P&L: A running total of the displayed monthly P&L is provided, giving you a quick sum of performance over the selected period.

Customizable Display:

Months to Display: Choose how many past months you want to see in the table (from 1 to 60 months).

Text Size: Adjust the text size (Tiny, Small, Normal, Large, Huge) to fit your viewing preferences.

Text Color: Customize the color of the text for better visibility against your chart background.

Intraday & Daily Compatibility: The table is optimized to display on daily and intraday timeframes, ensuring it's relevant for various trading styles. (Note: For very long-term analysis on weekly/monthly charts, you might consider other tools, as this focuses on granular monthly P&L.)

How It Works:

The indicator calculates the percentage change from the close of the previous month to the close of the current month. For the very first month displayed, it calculates the P&L from the opening price of the chart's first bar to the close of that month. This data is then neatly organized into a table, updated on the last bar of the day or session.

Ideal For:

Traders and investors who want a quick, visual summary of monthly performance.

Analyzing seasonal trends or consistent periods of profitability/drawdown.

Supplementing backtesting results with a clear month-by-month breakdown.

Settings:

Text Color: Changes the color of all text within the table.

Text Size: Controls the font size of the table content.

Months to Display: Determines the number of recent months included in the table.

SectorRotationRadarThe Sector Rotation Radar is a powerful visual analysis tool designed to track the relative strength and momentum of a stock compared to a benchmark index and its associated sector ETF. It helps traders and investors identify where an asset stands within the broader market cycle and spot rotation patterns across sectors and timeframes.

🔧 Key Features:

Benchmark Comparison: Measures the relative performance (strength and momentum) of the current symbol against a chosen benchmark (default: SPX), highlighting over- or underperformance.

Automatic Sector Detection: Automatically links stocks to their relevant sector ETFs (e.g., XLK, XLF, XLU), based on an extensive internal symbol map.

Multi-Timeframe Analysis: Supports simultaneous comparison across the current, next, and even third-higher timeframes (e.g., Daily → Weekly → Monthly), providing a bigger-picture perspective of trend shifts.

Tail Visualization: Displays a "trail" of price behavior over time, visualizing how the asset has moved in terms of relative strength and momentum across a user-defined period.

Quadrant-Based Layout: The chart is divided into four dynamic main zones, each representing a phase in the strength/momentum cycle:

🔄 Improving: Gaining strength and momentum

🚀 Leading: High strength and high momentum — top performers

💤 Weakening: Losing momentum while still strong

🐢 Lagging: Low strength and low momentum — underperformers

Clean Chart Visualization:

Background grid with axis labels

Dynamic tails and data points for each symbol

Option to include the associated sector ETF for context

Descriptive labels showing exact strength/momentum values per point

⚙️ Customization Options:

Benchmark Selector: Choose any symbol to compare against (e.g., SPX, Nasdaq, custom index)

Start Date Control: Option to fix a historical start point or use the current data range

Trail Length: Set the number of previous data points to display

Additional Timeframes: Enable analysis of one or two higher timeframes beyond the current

Sector ETF Display: Toggle to show or hide the related sector ETF alongside the asset

📚 Technical Architecture:

The indicator relies on external modules for:

Statistical modeling

Relative strength and momentum calculations

Chart rendering and label drawing

These components work together to compute and display a dynamic, real-time map of asset performance over time.

🧠 Use Case:

Sector Rotation Radar is ideal for traders looking to:

Spot stocks or sectors rotating into strength or weakness

Confirm alignment across multiple timeframes

Identify sector leaders and laggards

Understand how a symbol is positioned relative to the broader market and its peers

This tool is especially valuable for swing traders, sector rotation strategies, and macro-aware investors who want a visual edge in decision-making.

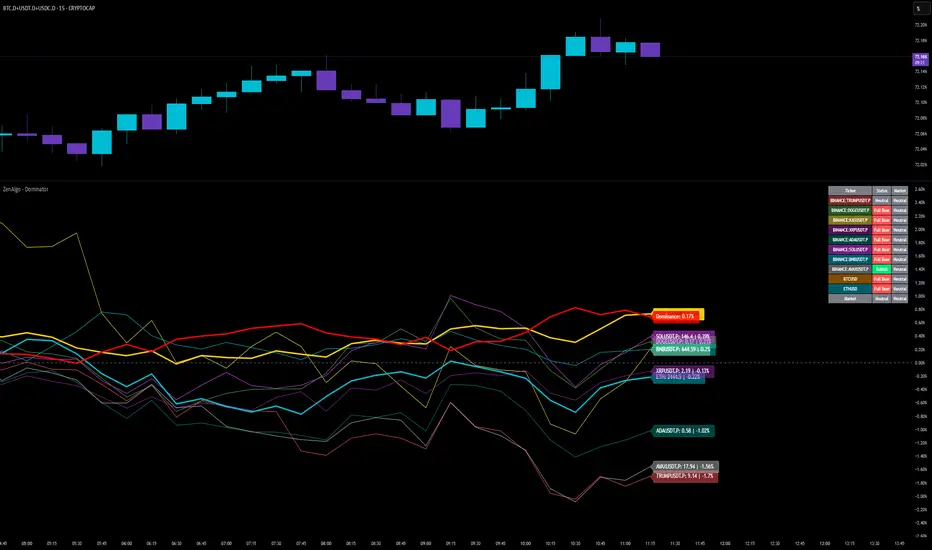

ZenAlgo - DominatorThis indicator provides a structured multi-ticker overview of market momentum and relative strength by analyzing short-term price behavior across selected assets in comparison with broader crypto dominance and Bitcoin/ETH performance.

Ticker and Market Data Handling

The script accepts up to 9 user-defined symbols (tickers) along with BTCUSD and ETHUSD. For each symbol:

It retrieves the current price.

It also requests the daily opening price from the "D" timeframe to compute intraday percentage change.

For BTC, ETH, and dominance (sum of BTC, USDT, and USDC dominance), daily change is calculated using this same method.

This comparison enables tracking relative performance from the daily open, which provides meaningful insight into intraday strength or weakness among different assets.

Dominance Logic

The indicator aggregates dominance data from BTC , USDT , and USDC using TradingView’s CRYPTOCAP indices. This combined dominance is used as a reference in directional and status calculations. ETH dominance is also analyzed independently.

Changes in dominance are used to infer whether market attention is shifting toward Bitcoin/stablecoins (typically indicating risk-off sentiment) or away from them (typically risk-on behavior, benefiting altcoins).

Price Direction Estimation

The script estimates directional bias using an EMA-based deviation technique:

A short EMA (user-defined lookback , default 4 bars) is calculated.

The current close is compared to the EMA to assess directional bias.

Recent candle changes are also inspected to confirm a consistent short-term trend (e.g., 3 consecutive higher closes for "up").

A small threshold is used to avoid classifying flat movements as trends.

This directionality logic is applied separately to:

The selected ticker's price

BTC price

Combined dominance

This allows the script to contextualize the movement of each asset within broader market conditions.

Market Status Evaluation

A custom function analyzes ETH and BTC dominance trends along with their relative strength to define the overall market regime:

Altseason is identified when BTC dominance is declining, ETH dominance rising, and ETH outperforms BTC.

BTC Season occurs when BTC dominance is rising, ETH dominance falling, and BTC outperforms ETH.

If neither condition is met, the state is Neutral .

This classification is shown alongside each ticker's row in the table and helps traders assess whether market conditions favor Bitcoin, Ethereum, or altcoins in general.

Ticker Status Classification

Each ticker is analyzed independently using the earlier directional logic. Its status is then determined as follows:

Full Bull : Ticker is trending up while dominance is declining or BTC is also rising.

Bullish : Ticker is trending up but not supported by broader bullish context.

Bearish : Ticker is trending down but without broader confirmation.

Full Bear : Ticker is trending down while dominance rises or BTC falls.

Neutral : No strong directional bias or conflicting context.

This classification reflects short-term momentum and macro alignment and is color-coded in the results table.

Table Display and Plotting

A configurable table is shown on the chart, which:

Displays the name and status of each selected ticker.

Optionally includes BTC, ETH, and market state.

Uses color-coding for intuitive interpretation.

Additionally, price changes from the daily open are plotted for each selected ticker, BTC, ETH, and combined dominance. These values are also labeled directly on the chart.

Labeling and UX Enhancements

Labels next to the current candle display price and percent change for each active ticker and for BTC, ETH, and combined dominance.

Labels update each bar, and old labels are deleted to avoid clutter.

Ticker names are dynamically shortened by stripping exchange prefixes.

How to Use This Indicator

This tool helps traders:

Spot early rotations between Bitcoin and altcoins.

Identify intraday momentum leaders or laggards.

Monitor which tickers align with or diverge from broader market trends.

Detect possible sentiment shifts based on dominance trends.

It is best used on lower to mid timeframes (15m–4h) to capture intraday to short-term shifts. Users should cross-reference with longer-term trend tools or structural indicators when making directional decisions.

Interpretation of Values