Share SizePurpose: The "Share Size" indicator is a powerful risk management tool designed to help traders quickly determine appropriate share/contract sizes based on their predefined risk per trade and the current market's volatility (measured by ATR). It calculates potential dollar differences from recent highs/lows and translates them into a recommended share/contract size, accounting for a user-defined ATR-based offset. This helps you maintain consistent risk exposure across different instruments and market conditions.

How It Works: At its core, the indicator aims to answer the question: "How many shares/contracts can I trade to keep my dollar risk within limits if my stop loss is placed at a recent high or low, plus an ATR-based buffer?"

Price Difference Calculation: It first calculates the dollar difference between the current close price and the high and low of the current bar (Now) and the previous 5 bars (1 to 5).

Tick Size & Value Conversion: These price differences are then converted into dollar values using the instrument's specific tickSize and tickValue. You can select common futures contracts (MNQ, MES, MGC, MCL), a generic "Stock" setting, or define custom values.

ATR Offset: An Average True Range (ATR) based offset is added to these dollar differences. This offset acts as a buffer, simulating a stop loss placed beyond the immediate high/low, accounting for market noise or volatility.

Risk-Based Share Size: Finally, using your Default Risk ($) input, the indicator calculates how many shares/contracts you can take for each of the 6 high/low scenarios (current bar, 5 previous bars) to ensure your dollar risk per trade remains constant.

Dynamic Table: All these calculations are presented in a clear, real-time table at the bottom-left of your chart. The table dynamically adjusts its "Label" to show the selected symbol preset, making it easy to see which instrument's settings are currently being used. The "Shares" rows indicate the maximum shares/contracts you can trade for a given risk and stop placement. The cells corresponding to the largest dollar difference (and thus smallest share size) for both high and low scenarios are highlighted, drawing your attention to the most conservative entry points.

Key Benefits:

Consistent Risk: Helps maintain a consistent dollar risk per trade, regardless of the instrument or its current price/volatility.

Dynamic Sizing: Automatically adjusts share/contract size based on market volatility and your chosen stop placement.

Quick Reference: Provides a real-time, easy-to-read table directly on your chart, eliminating manual calculations.

Informed Decision Making: Assists in quickly assessing trade opportunities and potential position sizes.

Setup Parameters (Inputs)

When you add the "Share Size" indicator to your chart, you'll see a settings dialog with the following parameters:

1. Symbol Preset:

Purpose: This is the primary setting to define the tick size and value for your chosen trading instrument.

Options:

MNQ (Micro Nasdaq 100 Futures)

MES (Micro E-mini S&P 500 Futures)

MGC (Micro Gold Futures)

MCL (Micro Crude Oil Futures)

Stock (Generic stock setting, with tick size/value of 0.01)

Custom (Allows you to manually input tick size and value)

Default: MNQ

Importance: Crucial for accurate dollar calculations. Ensure this matches the instrument you are trading.

2. Tick Size (Manual Override):

Purpose: Only used if Symbol Preset is set to Custom. This defines the smallest price increment for your instrument.

Type: Float

Default: 0.25

Hidden: This input is hidden (display=display.none) unless "Custom" is selected. You might need to change display=display.none to display=display.inline in the code if you want to see and adjust it directly in the settings for "Custom" mode.

3. Tick Value (Manual Override):

Purpose: Only used if Symbol Preset is set to Custom. This defines the dollar value of one tickSize increment.

Type: Float

Default: 0.50

Hidden: This input is hidden (display=display.none) unless "Custom" is selected. Similar to Tick Size, you might need to adjust its display property if you want it visible.

4. Default Risk ($):

Purpose: This is your maximum desired dollar risk per trade. All share size calculations will be based on this value.

Type: Float

Default: 50.0

Hidden: This input is hidden (display=display.none). It's a critical setting, so consider making it visible by changing display=display.none to display=display.inline in the code if you want users to easily adjust their risk.

ATR Offset Settings (Group): This group of settings allows you to fine-tune the ATR-based buffer added to your potential stop loss.

5. ATR Offset Length:

Purpose: Defines the lookback period for the Average True Range (ATR) calculation used for the offset.

Type: Integer

Default: 7

Hidden: This input is hidden (display=display.none).

6. ATR Offset Timeframe:

Purpose: Specifies the timeframe on which the ATR for the offset will be calculated. This allows you to use ATR from a higher timeframe for your stop buffer, even if your chart is on a lower timeframe.

Type: Timeframe string (e.g., "1" for 1 minute, "60" for 1 hour, "D" for Daily)

Default: "1" (1 Minute)

Hidden: This input is hidden (display=display.none).

7. ATR Offset Multiplier (x ATR):

Purpose: Multiplies the calculated ATR value to determine the final dollar offset added to your high/low price difference. A value of 1.0 means one full ATR is added. A value of 0.5 means half an ATR is added.

Type: Float

Minimum Value: 0 (no offset)

Default: 1.0

Hidden: This input is hidden (display=display.none).

Portfolio management

Multi-Session MarkerMulti-Session Marker is a flexible visual tool for traders who want to highlight up to 10 custom trading sessions directly on their chart’s background.

Custom Sessions: Enter up to 10 time ranges (in HHMM-HHMM format) to mark any market session, news window, or personal focus period.

Visual Clarity: For each session, toggle the highlight on or off and select a unique background color and opacity, making it easy to distinguish active trading windows at a glance.

Universal Time Handling: Session times automatically follow your chart’s time zone—no manual adjustment required.

Efficient and Fast: Utilizes TradingView’s bgcolor() for smooth performance, even on fast timeframes like 1-second charts.

Clean Interface: All session controls are grouped for easy editing in the indicator’s settings panel.

How to use:

In the indicator settings, enter your desired session times (e.g., 0930-1130) for each session you want to highlight.

Toggle “Show Session” and pick a color for each session.

The background will automatically highlight those periods on your chart.

This indicator is ideal for day traders, futures traders, or anyone who wants to visually segment their trading day for better focus and analysis.

Hidden Markov Model [Extension] | FractalystWhat's the indicator's purpose and functionality?

The Hidden Markov Model is specifically designed to integrate with the Quantify Trading Model framework, serving as a probabilistic market regime identification system for institutional trading analysis.

Hidden Markov Models are particularly well-suited for market regime detection because they can model the unobservable (hidden) state of the market, capture probabilistic transitions between different states, and account for observable market data that each state generates.

The indicator uses Hidden Markov Model mathematics to automatically detect distinct market regimes such as low-volatility bull markets, high-volatility bear markets, or range-bound consolidation periods.

This approach provides real-time regime probabilities without requiring optimization periods that can lead to overfitting, enabling systematic trading based on genuine probabilistic market structure.

How does this extension work with the Quantify Trading Model?

The Hidden Markov Model | Fractalyst serves as a probabilistic state estimation engine for systematic market analysis.

Instead of relying on traditional technical indicators, this system automatically identifies market regimes using forward algorithm implementation with three-state probability calculation (bullish/neutral/bearish), Viterbi decoding process for determining most likely regime sequence without repainting, online parameter learning with adaptive emission probabilities based on market observations, and multi-feature analysis combining normalized returns, volatility comprehensive regime assessment.

The indicator outputs regime probabilities and confidence levels that can be used for systematic trading decisions, portfolio allocation, or risk management protocols.

Why doesn't this use optimization periods like other indicators?

The Hidden Markov Model | Fractalyst deliberately avoids optimization periods to prevent overfitting bias that destroys out-of-sample performance.

The system uses a fixed mathematical framework based on Hidden Markov Model theory rather than optimized parameters, probabilistic state estimation using forward algorithm calculations that work across all market conditions, online learning methodology with adaptive parameter updates based on real-time market observations, and regime persistence modeling using fixed transition probabilities with 70% diagonal bias for realistic regime behavior.

This approach ensures the regime detection signals remain robust across different market cycles without the performance degradation typical of over-optimized traditional indicators.

Can this extension be used independently for discretionary trading?

No, the Hidden Markov Model | Fractalyst is specifically engineered for systematic implementation within institutional trading frameworks.

The indicator is designed to provide regime filtering for systematic trading algorithms and risk management systems, enable automated backtesting through mathematical regime identification without subjective interpretation, and support institutional-level analysis when combined with systematic entry/exit models.

Using this indicator independently would miss the primary value proposition of systematic regime-based strategy optimization that institutional frameworks provide.

How do I integrate this with the Quantify Trading Model?

Integration enables institutional-grade systematic trading through advanced machine learning and statistical validation:

- Add both HMM Extension and Quantify Trading Model to your chart

- Select HMM Extension as the bias source using input.source()

- Quantify automatically uses the extension's bias signals for entry/exit analysis

- The built-in machine learning algorithms score optimal entry and exit levels based on trend intensity, and market structure patterns identified by the extension

The extension handles all bias detection complexity while Quantify focuses on optimal trade timing, position sizing, and risk management along with PineConnector automation

What markets and assets does the indicator Extension work best on?

The Hidden Markov Model | Fractalyst performs optimally on markets with sufficient price movement since the system relies on statistical analysis of returns, volatility, and momentum patterns for regime identification.

Recommended asset classes include major forex pairs (EURUSD, GBPUSD, USDJPY) with high liquidity and clear regime transitions, stock index futures (ES, NQ, YM) providing consistent regime behavior patterns, individual equities (large-cap stocks with sufficient volatility for regime detection), cryptocurrency markets (BTC, ETH with pronounced regime characteristics), and commodity futures (GC, CL showing distinct market cycles and regime transitions).

These markets provide sufficient statistical variation in returns and volatility patterns, ensuring the HMM system's mathematical framework can effectively distinguish between bullish, neutral, and bearish regime states.

Any timeframe from 15-minute to daily charts provides sufficient data points for regime calculation, with higher timeframes (4H, Daily) typically showing more stable regime identification with fewer false transitions, while lower timeframes (30m, 1H) provide more responsive regime detection but may show increased noise.

Acceptable Timeframes and Portfolio Integration:

- Any timeframe that can be evaluated within Quantify Trading Model's backtesting engine is acceptable for live trading implementation.

Legal Disclaimers and Risk Acknowledgments

Trading Risk Disclosure

The HMM Extension is provided for informational, educational, and systematic bias detection purposes only and should not be construed as financial, investment, or trading advice. The extension provides institutional analysis but does not guarantee profitable outcomes, accurate bias predictions, or positive investment returns.

Trading systems utilizing bias detection algorithms carry substantial risks including but not limited to total capital loss, incorrect bias identification, market regime changes, and adverse conditions that may invalidate analysis. The extension's performance depends on accurate data, TradingView infrastructure stability, and proper integration with Quantify Trading Model, any of which may experience data errors, technical failures, or service interruptions that could affect bias detection accuracy.

System Dependency Acknowledgment

The extension requires continuous operation of multiple interconnected systems: TradingView charts and real-time data feeds, accurate reporting from exchanges, Quantify Trading Model integration, and stable platform connectivity. Any interruption or malfunction in these systems may result in incorrect bias signals, missed transitions, or unexpected analytical behavior.

Users acknowledge that neither Fractalyst nor the creator has control over third-party data providers, exchange reporting accuracy, or TradingView platform stability, and cannot guarantee data accuracy, service availability, or analytical performance. Market microstructure changes, reporting delays, exchange outages, and technical factors may significantly affect bias detection accuracy compared to theoretical or backtested performance.

Intellectual Property Protection

The HMM Extension, including all proprietary algorithms, classification methodologies, three-state bias detection systems, and integration protocols, constitutes the exclusive intellectual property of Fractalyst. Unauthorized reproduction, reverse engineering, modification, or commercial exploitation of these proprietary technologies is strictly prohibited and may result in legal action.

Liability Limitation

By utilizing this extension, users acknowledge and agree that they assume full responsibility and liability for all trading decisions, financial outcomes, and potential losses resulting from reliance on the extension's bias detection signals. Fractalyst shall not be liable for any unfavorable outcomes, financial losses, missed opportunities, or damages resulting from the development, use, malfunction, or performance of this extension.

Past performance of bias detection accuracy, classification effectiveness, or integration with Quantify Trading Model does not guarantee future results. Trading outcomes depend on numerous factors including market regime changes, pattern evolution, institutional behavior shifts, and proper system configuration, all of which are beyond the control of Fractalyst.

User Responsibility Statement

Users are solely responsible for understanding the risks associated with algorithmic bias detection, properly configuring system parameters, maintaining appropriate risk management protocols, and regularly monitoring extension performance. Users should thoroughly validate the extension's bias signals through comprehensive backtesting before live implementation and should never base trading decisions solely on automated bias detection.

This extension is designed to provide systematic institutional flow analysis but does not replace the need for proper market understanding, risk management discipline, and comprehensive trading methodology. Users should maintain active oversight of bias detection accuracy and be prepared to implement manual overrides when market conditions invalidate analysis assumptions.

Terms of Service Acceptance

Continued use of the HMM Extension constitutes acceptance of these terms, acknowledgment of associated risks, and agreement to respect all intellectual property protections. Users assume full responsibility for compliance with applicable laws and regulations governing automated trading system usage in their jurisdiction.

TradePlanner ProPlan smarter. Trade with precision.

TradePlanner Pro is a professional-grade overlay tool designed to streamline your trading decisions by visually organizing your trade plans directly on the chart. Built for traders who value preparation and clarity, this script enables precise entry planning, risk management, and target visualization—all tailored per symbol.

Core Purpose

TradePlanner Pro helps you map out potential trades using pre-defined symbol-based presets. It dynamically calculates position sizes based on your account size or fixed risk, then visualizes key trade levels (Entry, Take Profits, Stop Loss) with profit/loss metrics in both dollar and percentage terms. It's the perfect companion for traders who prepare their setups in advance and want their plans clearly represented on the chart.

Key Features

🔹 Per-Symbol Presets: Define entries, up to 3 take-profit levels, and stop-losses for each ticker.

🔹 Dynamic Risk Sizing: Choose between percentage-based risk or fixed dollar risk per trade.

🔹 Visual Trade Mapping: Automatically plots Entry, TP1–TP3, and SL lines on your chart.

🔹 Real-Time P&L Labels: Displays profit/loss amounts and percentages, with optional R/R ratios.

🔹 Custom Investment Display: Shows how much capital is allocated per trade.

🔹 Clean, Configurable UI: Adjust label positions, font sizes, opacity, and label visibility to match your style.

Whether you're swing trading or day trading, TradePlanner Pro helps you stay disciplined, organized, and confident in your execution.

How to Use TradePlanner Pro – Step-by-Step Guide

TradePlanner Pro is designed to be easy to set up while giving you full control over how your trades are visualized and calculated. Here’s how to get started:

1. Start with Default Settings

By default, the script assumes:

Account Size: $10,000

Max Money per Trade (%): 1.0%

Max Risk (USD): 0 (disabled; only percentage risk is used)

This means the script will size each trade to risk 1% of your account balance per trade unless you override it with a fixed USD risk amount.

2. Set Up Your Symbol Presets

The "Symbol Presets" input is a flexible text area where you define trade setups for each ticker.

Format (one per line):

SYMBOL:Entry,TP1 ,SL

Example:

AAPL:250,260,270,240

MSFT:100,110,90

TSLA:180,200,170

You can include 1 to 3 take-profit levels.

The script will only activate for the current chart’s symbol, matching what's listed.

3. Customize Risk Parameters

You can use:

Account % Risk – Based on account size and % risk.

Fixed USD Risk – When a dollar amount is entered (>0), it takes priority and calculates share size based on the risk per share.

There's also an option to round share quantities down to whole units, which is useful for stock or crypto trading platforms that only allow whole-number units.

4. Choose What to Display

Toggle on/off these elements as needed:

Show Entry/TP/SL Lines

Show P&L Labels – Profit/loss amounts at each target and SL.

Show Amount Invested – Includes total dollar value in the quantity label.

Show Percentages – Adds % gain/loss to each label.

Show Risk/Reward Ratios – Optionally displayed beside or below TP labels.

You can further adjust:

Font size and label opacity

Label position offset – In percent of price range, so they don’t overlap the actual levels.

5. Read the Visual Outputs

Once the preset matches the current chart symbol:

Lines will appear for Entry, TP1-TP3, and Stop Loss.

Labels will display your:

Trade quantity (and invested amount)

Dollar and % profit at each target

Total loss at stop loss

Optional R/R ratios

Everything updates dynamically and adjusts to your current chart scale and bar availabilit

VWAP/VOL [Extension] | FractalystWhat's the indicator's purpose and functionality?

The VWAP/VOL Extension is designed specifically as a bias identification system for the Quantify Trading Model.

This extension uses volume-weighted average price analysis combined with institutional volume classification to automatically detect market bias without requiring optimization periods that lead to overfitting.

The system provides real-time bias signals (bullish/bearish/neutral) that integrate directly with Quantify's machine learning algorithms, enabling institutional-level backtesting and automated entry/exit identification based on genuine market structure rather than curve-fitted parameters.

How does this extension work with the Quantify Trading Model?

The VWAP/VOL Extension serves as the bias detection engine for Quantify's automated trading system.

Instead of manually selecting bias direction, this extension automatically identifies market bias using:

- Volume-weighted VWAP analysis with three-state detection (bullish/bearish/neutral)

- Institutional volume classification using relative volume thresholds without optimization

- Non-repainting architecture ensuring consistent bias signals for Quantify's machine learning

The extension outputs bias signals that Quantify uses as input through the `input.source()` function, allowing the Trading Model to focus on optimal entry/exit timing while the extension handles bias identification.

Why doesn't this use optimization periods like other indicators?

The VWAP/VOL Extension deliberately avoids optimization periods to prevent overfitting bias that destroys out-of-sample performance. The system uses:

- Fixed mathematical thresholds based on market structure principles rather than optimized parameters

- Relative volume analysis using standard 2.0x/0.5x ratios that work across all market conditions

- VWAP distance calculations based on percentage thresholds without curve-fitting

- Gap enforcement using fixed 5-bar minimums for disciplined bias detection

This approach ensures the bias signals remain robust across different market regimes without the performance degradation typical of over-optimized systems.

Can this extension be used independently for discretionary trading?

No, the VWAP/VOL Extension is specifically engineered to work as a component within the Quantify ecosystem. The extension is designed to:

- Provide bias input for Quantify's machine learning algorithms

- Enable automated backtesting through systematic bias identification

- Support institutional-level analysis when combined with Quantify's ML entry model

Using this extension independently would miss the primary value proposition of systematic entry/exit optimization that Quantify provides.

The extension handles bias detection so Quantify can focus on probability-based trade timing and risk management.

How does this enable institutional-level backtesting?

The extension transforms discretionary bias identification into systematic institutional analysis by:

- Eliminating subjective bias selection through automated VWAP/volume analysis

- Providing consistent historical signals with non-repainting architecture for accurate backtesting

- Integrating with Quantify's algorithms to identify optimal entry patterns based on objective bias states

- Enabling performance analysis across multiple market regimes without optimization bias

This combination allows Quantify to run institutional-grade backtests with consistent bias identification, generating reliable performance statistics and risk metrics that reflect genuine market edge rather than curve-fitted results.

How do I integrate this with the Quantify Trading Model?

Integration enables institutional-grade systematic trading through advanced machine learning and statistical validation:

- Add both VWAP/VOL Extension and Quantify Trading Model to your chart

- Select VWAP/VOL Extension as the bias source using input.source()

- Quantify automatically uses the extension's bias signals for entry/exit analysis

- The built-in machine learning algorithms score optimal entry and exit levels based on trend intensity, volume conviction, and market structure patterns identified by the extension

The extension handles all bias detection complexity while Quantify focuses on optimal trade timing, position sizing, and risk management along with PineConnector automation

What markets and assets does the VWAP/VOL Extension work best on?

The VWAP/VOL Extension performs optimally on markets with consistent, high-volume participation since the system relies on institutional volume analysis for bias detection. Futures markets provide the most reliable performance due to their centralized volume data and continuous institutional participation.

Recommended Futures Markets:

- ES (S&P 500 E-mini) - Over 2 million contracts daily volume, excellent liquidity depth

- NQ (NASDAQ-100 E-mini) - Around 600,000 contracts daily, strong tech sector representation

- YM (Dow Jones E-mini) - Consistent institutional flow and volume patterns

- RTY (Russell 2000 E-mini) - Small-cap exposure with reliable volume data

- GC (Gold Futures) - High volume commodity with institutional participation

- CL (Crude Oil Futures) - Energy sector representation with strong volume consistency

Why Futures Markets Excel:

- Futures markets provide centralized volume reporting, ensuring the extension's volume classification system receives accurate institutional participation data. The standardized contract specifications and continuous trading hours create consistent volume patterns that the extension's algorithms can analyze effectively.

Acceptable Timeframes and Portfolio Integration:

- Any timeframe that can be evaluated within Quantify Trading Model's backtesting engine is acceptable for live trading implementation.

The extension is specifically designed to integrate with Quantify's portfolio management system, allowing multiple strategies across different timeframes and assets to operate simultaneously while maintaining consistent bias identification methodology across the entire automated trading portfolio.

Legal Disclaimers and Risk Acknowledgments

Trading Risk Disclosure

The VWAP/VOL Extension is provided for informational, educational, and systematic bias detection purposes only and should not be construed as financial, investment, or trading advice. The extension provides volume-weighted institutional analysis but does not guarantee profitable outcomes, accurate bias predictions, or positive investment returns.

Trading systems utilizing bias detection algorithms carry substantial risks including but not limited to total capital loss, incorrect bias identification, market regime changes, and adverse conditions that may invalidate volume-based analysis. The extension's performance depends on accurate volume data, TradingView infrastructure stability, and proper integration with Quantify Trading Model, any of which may experience data errors, technical failures, or service interruptions that could affect bias detection accuracy.

System Dependency Acknowledgment

The extension requires continuous operation of multiple interconnected systems: TradingView charts and real-time data feeds, accurate volume reporting from exchanges, Quantify Trading Model integration, and stable platform connectivity. Any interruption or malfunction in these systems may result in incorrect bias signals, missed transitions, or unexpected analytical behavior.

Users acknowledge that neither Fractalyst nor the creator has control over third-party data providers, exchange volume reporting accuracy, or TradingView platform stability, and cannot guarantee data accuracy, service availability, or analytical performance. Market microstructure changes, volume reporting delays, exchange outages, and technical factors may significantly affect bias detection accuracy compared to theoretical or backtested performance.

Intellectual Property Protection

The VWAP/VOL Extension, including all proprietary algorithms, volume classification methodologies, three-state bias detection systems, and integration protocols, constitutes the exclusive intellectual property of Fractalyst. Unauthorized reproduction, reverse engineering, modification, or commercial exploitation of these proprietary technologies is strictly prohibited and may result in legal action.

Liability Limitation

By utilizing this extension, users acknowledge and agree that they assume full responsibility and liability for all trading decisions, financial outcomes, and potential losses resulting from reliance on the extension's bias detection signals. Fractalyst shall not be liable for any unfavorable outcomes, financial losses, missed opportunities, or damages resulting from the development, use, malfunction, or performance of this extension.

Past performance of bias detection accuracy, volume classification effectiveness, or integration with Quantify Trading Model does not guarantee future results. Trading outcomes depend on numerous factors including market regime changes, volume pattern evolution, institutional behavior shifts, and proper system configuration, all of which are beyond the control of Fractalyst.

User Responsibility Statement

Users are solely responsible for understanding the risks associated with algorithmic bias detection, properly configuring system parameters, maintaining appropriate risk management protocols, and regularly monitoring extension performance. Users should thoroughly validate the extension's bias signals through comprehensive backtesting before live implementation and should never base trading decisions solely on automated bias detection.

This extension is designed to provide systematic institutional flow analysis but does not replace the need for proper market understanding, risk management discipline, and comprehensive trading methodology. Users should maintain active oversight of bias detection accuracy and be prepared to implement manual overrides when market conditions invalidate volume-based analysis assumptions.

Terms of Service Acceptance

Continued use of the VWAP/VOL Extension constitutes acceptance of these terms, acknowledgment of associated risks, and agreement to respect all intellectual property protections. Users assume full responsibility for compliance with applicable laws and regulations governing automated trading system usage in their jurisdiction.

Bear Market Defender [QuantraSystems]Bear Market Defender

A system to short Altcoins when BTC is ranging or falling - benefit from Altcoin bleed or collapse .

QuantraSystems guarantees that the information created and published within this document and on the TradingView platform is fully compliant with applicable regulations, does not constitute investment advice, and is not exclusively intended for qualified investors.

Important Note!

The system equity curve presented here has been generated as part of the process of testing and verifying the methodology behind this script.

Crucially, it was developed after the system was conceptualized, designed, and created, which helps to mitigate the risk of overfitting to historical data. In other words, the system was built for robustness, not for simply optimizing past performance.

This ensures that the system is less likely to degrade in performance over time, compared to hyper-optimized systems that are tailored to past data. No tweaks or optimizations were made to this system post-backtest.

Even More Important Note!!

The nature of markets is that they change quickly and unpredictably. Past performance does not guarantee future results - this is a fundamental rule in trading and investing.

While this system is designed with broad, flexible conditions to adapt quickly to a range of market environments, it is essential to understand that no assumptions should be made about future returns based on historical data. Markets are inherently uncertain, and this system - like all trading systems - cannot predict future outcomes.

INTRODUCTION TO THE STAR FRAMEWORK

The STAR Framework – an abbreviation for Strategic Trading with Adaptive Risk - is a bespoke portfolio-level infrastructure for dynamic, multi-asset crypto trading systems. It combines systematic position management, adaptive sizing, and “intra-system” diversification, all built on a rigorous foundation of Risk-based position sizing .

At its core, STAR is designed to facilitate:

Adaptive position sizing based on user-defined maximum portfolio risk

Capital allocation across multiple assets with dynamic weight adjustment

Execution-aware trading with robust fee and slippage adjustment

Realistic equity curve logic based on a compounding realized PnL and additive unrealized PnL

The STAR Framework is intended for use as both a standalone portfolio system or preferred as a modular component within a broader trading “global portfolio” - delivering a balance of robustness and scalability across strategy types, timeframes, and market regimes.

RISK ALLOCATION VIA "R" CALCULATIONS

The foundational concept behind STAR is the use of the R unit - a dynamic representation of risk per trade. R is defined by the distance between a trade's entry and its stoploss, making it an intuitive and universally adaptive sizing unit across any token, timeframe, or market.

Example: Suppose the entry price is $100, and the stoploss is $95. A $5 move against the position represents a 1R loss. A 15% price increase to $115 would equal a +3R gain.

This makes R-based systems highly flexible: the user defines the percentage of capital that is put at risk per R and all positions are scaled accordingly - whether the token is volatile, illiquid, or slow-moving.

R is an advantageous method for determine position sizing - instead of being tied to complex value at risk mechanisms with having layered exit criteria, or continuous volatility-based sizing criteria that need to be adjusted while in an open trade, R allows for very straightforward sizing, invalidation and especially risk control – which is the most fundamental.

REALIZED BALANCE, FEES & SLIPPAGE ACCOUNTING

All position sizing, risk metrics, and the base equity curve within STAR are calculated based on realized balance only .

This means:

No sizing adjustments are made based on unrealized profit and loss ✅

No active positions are included in the system's realized equity until fully closed ✅

Every trade is sized precisely according to current locked-in realized portfolio balance ✅

This creates the safest risk profile - especially when multiple trades are open. Unrealized gains are not used to inflate sizing, ensuring margin safety across all assets.

All calculations also incorporate slippage and fees, based on user-defined estimates – which can and should be based upon user-collected data - and updated frequently forwards in time. These are not cosmetic, or simply applied to the final equity curve - they are fully integrated into the dynamic position sizing and equity performance , ensuring:

Stoploss hits result in exactly a −1R loss, even after slippage and fees ✅

Winners are discounted based on realistic execution costs ✅

No trade is oversized due to unaccounted execution costs ✅

Example - Slippage in R Units:

Let R be defined as the distance from entry to stoploss.

Suppose that distance is $1, and the trade is closed at a win of +$2.

If execution slippage leads to a 50 cent worse entry and a 50 cent worse exit, you’ve lost $1 extra - which is an additional 1R in execution slippage. This makes the effective return 1.0R instead of the intended 2.0R.

This is equivalent to a slippage value of 50%.

Thus, slippage in STAR is tracked and modelled on an R-adjusted basis , enabling more accurate long-term performance modelling.

MULTI-ASSET, LONG/SHORT SUPPORT

STAR supports concurrent long and short positions across multiple tokens. This can sometimes result in partially hedged exposure - for example, being long one asset and short another.

This structure has key benefits:

Diversifies idiosyncratic risk by distributing exposure across multiple tokens

Allows simultaneous exploitation of relative strength and weakness

Reduces portfolio volatility via natural hedging during reduced trending periods

Even in a highly correlated market like crypto, short-term momentum behaviour often varies between tokens - making diversified, multi-directional exposure a strategic advantage .

EQUITY CURVE

The STAR framework only updates the underlying realized equity when a position is closed, and the trade outcome is known. This approach ensures:

True representation of actual capital available for trading

No exposure distortion due to unrealized gains

Risk remains tightly linked to realized results

This trade-to-trade basis for realized equity modelling eliminates the common pitfall of overallocation based on unrealized profits.

The visual equity curve represents an accurate visualization of the Total Equity however, which is equivalent to what would be the realized equity if all trades were closed on the prior bar close.

TIMEFRAME CONSIDERATIONS

Lower timeframes typically yield better performance for STAR due to:

Greater data density per day - more observations = better statistical inference

Faster compounding - more trades per week = faster capital rotation

However, lower timeframes also suffer from increased slippage and fees. STAR's execution-aware structure helps mitigate this, but users must still choose timeframes appropriate to their liquidity, costs, and operational availability.

INPUT OPTIONS

Fees (direct trading costs - the percentage of capital removed from the initial position size)

Slippage (execution delay, as a percentage. In practice, the fill price is often worse than the signal price. This directly affects R and hence position sizing)

Risk % ( Please note : this is the risk level if every position is opened at once. 5% risk for 5 assets is 1% risk per position)

System Start date

Float Precision value of displayed numbers

Table visualization - positioning and table sizes

Adjustable color options

VISUAL SIMPLICITY

To avoid usual unnecessary complexity and empower fast at-a-glance action taking, as well as enable mobile compatibility, only the most relevant information is presented.

This includes all information required to open positions in one table.

As well as a quick and straightforward overview for the system stats

Lastly, there is an optional table that can be enabled

displaying more detailed information if desired:

USAGE GUIDELINES

To use STAR effectively:

Input your average slippage and fees %

Input your maximum portfolio risk % (this controls overall leverage and is equivalent to the maximum loss that the allocation to STAR would bring if ALL positions are allocated AND hit their stop loss at the same time)

Wait for signal alerts with entry, stop, and size details

STAR will dynamically calculate sizing, risk exposure, and portfolio allocation on your behalf. Position multipliers, stop placement, and asset-specific risk are all embedded in the system logic.

Note: Leverage must be manually set to ISOLATED on your exchange platform to prevent unwanted position linking.

ABOUT THE BEAR MARKET DEFENDER STRATEGY

The first strategy to launch on the STAR Framework is the BEAR MARKET DEFENDER (BMD) - a fast-acting, trend following system based upon the Trend Titan NEUTRONSTAR. For the details of the logic behind NEUTRONSTAR, please refer to the methodology and trend aggregation section of the following indicator:

The BMD ’s short side exit calculation methodology is slightly improved compared to NEUTRONSTAR, to capture downtrends more consistently and also cut positions faster – which is crucial when considering general jump risk in the Crypto space.

Accordingly, the only focus of the BMD is to capture trends to the short side, providing the benefit of being in a spectrum from no correlation to being negatively correlated in risk and return behavior to classical Crypto long exposure.

More precisely, Crypto behavior showcases that when Bitcoin is in a ranging/mean reverting environment, most tokens that don’t fall into the “Blue-Chip” category tend to find themselves in a trend towards 0.

Typically during this period most Crypto portfolios suffer heavily due to a “Crypto-long” biased exposure.

The Bear Market Defender thrives in these chaotic, high volatility markets where most coins trend towards zero while the traditional Crypto long exposure is either flat or in a drawdown, therefore the BMD adds a source of uncorrelated risk and returns to hedge typical long exposure and bolster portfolio volatility.

Because of the BMD's short-only exposure, it will often suffer small losses during strong uptrends. During these periods, long exposure performs the best and the goal is to outperform the temporary underperformance in the BMD .

To take advantage of the abovementioned behavior of most tokens trending to zero, assets traded in the BMD are systematically updated on a quarterly basis with available liquidity being an important consideration for the tokens to be eligible for selection.

FINAL SUMMARY

The STAR Framework represents a new generation of portfolio grade trading infrastructure, built around disciplined execution, realized equity, and adaptive position sizing. It is designed to support any number of future methodologies - beginning with BMD .

The Bear Market Defender is here to hedge out commonly long biased portfolio allocations in the Crypto market, specializing in bringing uncorrelated returns during periods of sideways price action on Bitcoin, or whole-market downturns.

Together, STAR + BMD deliver a scalable, volatility tuned system that prioritizes capital preservation, signal accuracy, and adaptive risk allocation. Whether deployed standalone or within a broader portfolio, this framework is engineered for high performance, longevity, and adaptability in the ever-evolving crypto landscape.

Position Size Calculator v206/17/2025 - Updated to add MGC to list of instruments

Position Size Calculator for Futures Trading

A professional position sizing tool designed specifically for futures traders who want to maintain disciplined risk management. This indicator calculates the optimal number of contracts based on your predefined risk amount and provides instant visual feedback.

Key Features:

• Interactive price selection - simply click on the chart to set entry, stop loss, and take profit levels

• Supports all major futures contracts: ES, NQ, GC, RTY, YM, MNQ, MES with accurate contract specifications

• Customizable risk amount (defaults to $500 but fully adjustable)

• Real-time position size calculations that never exceed your risk tolerance

• Visual risk validation with color-coded header (green = valid risk, red = excessive risk)

• Automatic 2:1 risk/reward ratio calculations

• Compact, non-intrusive table display in top-right corner

• Clean interface with no chart clutter

How to Use:

Select your futures instrument from the dropdown

Set your maximum risk amount (default $500)

Click on the chart to set your Entry Price

Click on the chart to set your Stop Loss Price

Optionally click to set your Take Profit Price

The calculator instantly shows maximum contracts, actual risk, expected profit, and R/R ratio

Risk Management:

The indicator enforces strict risk management by calculating the maximum number of contracts you can trade while staying within your specified risk limit. The header turns green when your trade is within acceptable risk parameters and red when the risk is too high, providing instant visual feedback.

Perfect for day traders, swing traders, and anyone trading futures who wants to maintain consistent position sizing and risk management discipline.

SAFE Leverage Pro x50Safe Leverage Pro x50 — Safe leverage based on timeframes

Description:

Safe Leverage Pro x50 is an indicator designed to help traders choose prudent and realistic leverage, tailored to the timeframe being traded and the asset chosen.

Based on rigorous statistical research, this indicator provides a visual recommendation of the maximum typical leverage by timeframe and automatically suggests a more conservative value (by default, half) for trading with greater peace of mind and risk control.

* The goal is not for the indicator to make decisions for you, but rather to support your pre-defined entry strategies, allowing you to clearly understand how much leverage you can use without compromising your account against normal price fluctuations.

*The indicator does not calculate based on real-time volatility or ATR, but rather relies on statistical historical patterns obtained by analyzing price behavior after entry, differentiating between average movements in long and short entries by timeframe.

Important: Before following the recommendations of this indicator, check the maximum leverage your broker or exchange allows for the asset you are trading, as it can vary significantly between platforms.

* Philosophy behind the indicator:

This project arises as a response to the simplistic discourse that condemns leverage without distinguishing nuances.

Leverage is not intrinsically bad. What is dangerous is leveraging without method, without awareness, and without risk management.

Safe Leverage Pro x50 is designed to change that narrative:

** It's not about whether or not to use leverage, but when, how much, and how to use it intelligently.

Adaptive Momentum Deviation Oscillator | QuantMACAdaptive Momentum Deviation Oscillator | QuantMAC 📊

Overview 🎯

The Adaptive Momentum Deviation Oscillator (AMDO) is an advanced technical analysis indicator that combines the power of Bollinger Bands with adaptive momentum calculations to identify optimal entry and exit points in financial markets. This sophisticated oscillator creates dynamic bands that adapt to market volatility while providing clear visual signals for both trending and ranging market conditions.

How It Works 🔧

Core Methodology

The AMDO employs a sophisticated multi-layered approach to market analysis through four distinct phases:

Bollinger Band Foundation : The indicator begins by establishing a volatility baseline using traditional Bollinger Bands. These bands are calculated using a simple moving average as the center line, with upper and lower bands positioned at a specific number of standard deviations away from this centerline. The distance between these bands expands and contracts based on market volatility, creating a dynamic envelope around price action.

BB% Normalization Process : The raw price data is then transformed into a normalized percentage format that represents where the current price sits within the Bollinger Band envelope. When price is at the lower band, this percentage reads 0%; at the upper band, it reads 100%. This normalization allows for consistent comparison across different timeframes and price levels, creating a standardized oscillator that oscillates between extreme values.

Adaptive Momentum Band Construction : The normalized BB% values undergo a secondary volatility analysis where their own standard deviation is calculated over a specified period. This creates "bands around the bands" - upper and lower boundaries that adapt to the volatility of the normalized price position itself. These adaptive bands expand during periods of high momentum volatility and contract during consolidation phases.

Intelligent Signal Synthesis : The final layer combines the adaptive momentum bands with user-defined threshold levels to create a sophisticated trigger system. The indicator monitors when the dynamic bands cross above or below these thresholds, filtering out noise while capturing significant momentum shifts. This creates a dual-confirmation system where both volatility adaptation and threshold breaches must align for signal generation.

Key Components 🛠️

Adaptive Momentum Bands 📈

Dynamic Volatility Response : These bands automatically widen during periods of high momentum volatility and narrow during consolidation phases. Unlike fixed oscillator boundaries, they continuously recalibrate based on recent price behavior within the Bollinger Band framework.

Dual-Layer Calculation : The bands are derived from the volatility of the normalized price position itself, creating a "volatility of volatility" measurement. This provides early warning signals when momentum characteristics are changing, even before price breakouts occur.

State-Aware Visualization : The bands employ intelligent color coding that transitions between active and neutral states based on their interaction with threshold levels. Active states indicate high-probability momentum conditions, while neutral states suggest consolidation or indecision.

Momentum Persistence Tracking : The bands maintain memory of recent momentum characteristics, allowing them to distinguish between genuine momentum shifts and temporary price spikes or dips.

Threshold Levels 🎚️

Statistical Significance Boundaries : The threshold levels (default 83 for long, 40 for short) are positioned to capture statistically significant momentum events while filtering out market noise. These levels represent points where momentum probability shifts meaningfully in favor of directional moves.

Asymmetric Design Philosophy : The intentional asymmetry between long and short thresholds (83 vs 40) reflects the natural upward bias of many financial markets and the different risk/reward profiles of long versus short positions.

Contextual Sensitivity : The thresholds work in conjunction with the adaptive bands to create context-sensitive triggers. A threshold breach is only meaningful when it occurs in the proper sequence with band interactions.

Risk-Adjusted Positioning : The threshold levels are calibrated to provide favorable risk-adjusted entry points, considering both the probability of success and the potential magnitude of subsequent moves.

Bollinger Bands Overlay 📊

Multi-Timeframe Context : The price chart overlay provides essential context by showing traditional Bollinger Bands alongside the oscillator. This dual perspective allows traders to see both the absolute price position and the momentum characteristics simultaneously.

Support/Resistance Identification : The filled band area creates a visual representation of dynamic support and resistance levels. Price interaction with these bands provides additional confirmation for oscillator signals.

Volatility Environment Assessment : The width and slope of the bands offer immediate visual feedback about the current volatility environment, helping traders adjust their expectations and risk management accordingly.

Confluence Analysis : The overlay enables traders to identify confluence between price action at Bollinger Band levels and oscillator signals, creating higher-probability trade setups.

Signal Generation ⚡

The AMDO generates signals through precise mathematical crossover events:

Long Signals 🟢

Momentum Accumulation Detection : Long signals are generated when the lower adaptive momentum band crosses above the 83 threshold, indicating that downside momentum has exhausted and bullish momentum is beginning to accumulate. This represents a shift from defensive to offensive market posture.

Statistical Edge Confirmation : The crossing event occurs only when momentum characteristics have shifted sufficiently to provide a statistical edge for long positions. The adaptive nature ensures the signal quality remains consistent across different market volatility regimes.

Visual State Synchronization : Upon signal generation, the entire indicator ecosystem shifts to a bullish state - bar colors change, band states update, and the visual hierarchy emphasizes the long bias until conditions change.

Momentum Persistence Validation : The signal incorporates momentum persistence analysis to distinguish between genuine trend starts and false breakouts, reducing whipsaw trades in choppy market conditions.

Short Signals 🔴

Momentum Exhaustion Recognition : Short signals trigger when the upper adaptive momentum band crosses below the 40 threshold, signaling that bullish momentum has peaked and bearish momentum is emerging. This asymmetric threshold reflects the different dynamics of bullish versus bearish market phases.

Volatility-Adjusted Timing : The adaptive band system ensures that short signals are generated with appropriate timing regardless of the underlying volatility environment, maintaining signal quality in both high and low volatility conditions.

Regime-Aware Activation : Short signals are only active in Long/Short trading mode, recognizing that not all trading strategies benefit from short positions. The indicator adapts its behavior based on the selected trading approach.

Risk-Calibrated Thresholds : The 40 threshold is specifically calibrated to capture meaningful bearish momentum shifts while accounting for the higher risk typically associated with short positions.

Cash Signals 💰

Defensive Positioning Logic : In Long/Cash mode, cash signals are generated when short conditions are met, allowing traders to move to a defensive cash position rather than taking on short exposure. This preserves capital during unfavorable market conditions.

Risk Mitigation Strategy : Cash signals represent a risk-off approach that removes market exposure when momentum conditions favor the short side, protecting long-biased portfolios from adverse market movements.

Opportunity Cost Optimization : The cash position allows traders to avoid negative returns while maintaining flexibility to re-enter long positions when momentum conditions improve, optimizing the risk-adjusted return profile.

Features & Customization ⚙️

Color Schemes 🎨

9 pre-built color schemes (Classic through Classic9)

Custom color override option

Dynamic color changes based on signal states

Trading Modes 📈

Long/Short : Full bidirectional trading capability

Long/Cash : Long-only strategy with cash positions

Performance Metrics 📊

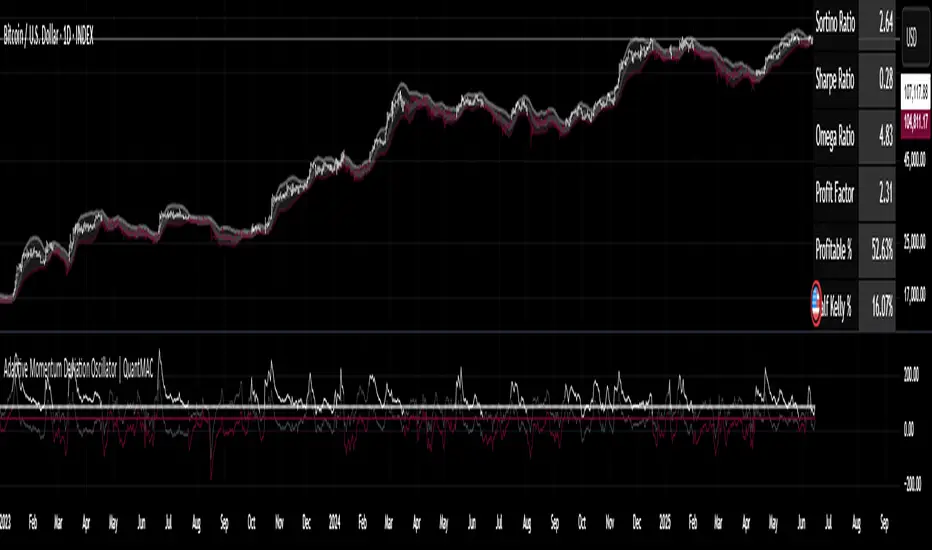

The indicator includes a comprehensive suite of advanced performance analytics that provide deep insights into strategy effectiveness:

Risk-Adjusted Return Metrics

Sortino Ratio : Measures returns relative to downside deviation only, providing a more accurate assessment of risk-adjusted performance by focusing on harmful volatility rather than total volatility. This metric is particularly valuable for asymmetric return distributions.

Sharpe Ratio : Calculates excess return per unit of total risk, offering a standardized measure of risk-adjusted performance that allows for comparison across different strategies and timeframes.

Omega Ratio : Employs probability-weighted analysis to compare the likelihood and magnitude of gains versus losses, providing insights into the overall shape of the return distribution and tail risk characteristics.

Drawdown and Risk Analysis

Maximum Drawdown : Tracks the largest peak-to-trough equity decline, providing crucial information about the worst-case scenario and helping traders understand the emotional and financial stress they might encounter.

Dynamic Drawdown Monitoring : Continuously updates drawdown calculations in real-time, allowing traders to monitor current drawdown levels relative to historical maximums.

Trade Statistics and Profitability

Profit Factor Analysis : Compares gross profits to gross losses, revealing the efficiency of the trading approach and the relationship between winning and losing trades.

Win Rate Calculation : Provides the percentage of profitable trades, which must be interpreted in conjunction with profit factor and average trade size for meaningful analysis.

Trade Frequency Tracking : Monitors total trade count to assess strategy turnover and transaction cost implications.

Position Sizing Guidance

Half Kelly Percentage : Calculates optimal position sizing based on Kelly Criterion methodology, then applies a conservative 50% reduction to account for parameter uncertainty and reduce volatility. This provides mathematically-based position sizing guidance that balances growth with risk management.

Parameters & Settings 🔧

BMD Settings

- Base Length : Period for Bollinger Band calculation (default: 10)

- Source : Price data source (default: close)

- Standard Deviation Length : Period for volatility calculation (default: 35)

- SD Multiplier : Bollinger Band width multiplier (default: 1.0)

- BB% Multiplier : Scaling factor for BB% calculation (default: 100)

BMD Settings

Base Length : Period for Bollinger Band calculation (default: 10)

Source : Price data source (default: close)

Standard Deviation Length : Period for volatility calculation (default: 35)

SD Multiplier : Bollinger Band width multiplier (default: 1.0)

BB% Multiplier : Scaling factor for BB% calculation (default: 100)

Signal Thresholds 🎯

Long Threshold : Trigger level for long signals (default: 83)

Short Threshold : Trigger level for short signals (default: 40)

Display Options 🖥️

Toggleable metrics table with 6 position options

Customizable date range limiter

Multiple visual elements for comprehensive analysis

Use Cases & Applications 💡

Trend Following

Identifies momentum shifts in trending markets

Provides early entry signals during trend continuations

Adaptive bands adjust to changing volatility conditions

Mean Reversion

Detects oversold/overbought conditions

Signals potential reversal points

Works effectively in ranging markets

Risk Management

Built-in performance metrics for strategy evaluation

Half Kelly percentage for position sizing guidance

Maximum drawdown monitoring

Advantages ✅

Adaptive Nature : Automatically adjusts to market volatility

Dual Display : Oscillator and price chart components work together

Comprehensive Metrics : Built-in performance analysis

Flexible Trading Modes : Supports different trading strategies

Visual Clarity : Color-coded signals and states

Customizable : Extensive parameter adjustment options

Important Considerations ⚠️

This indicator is designed for educational and analysis purposes

Should be used in conjunction with other technical analysis tools

Proper risk management is essential when trading

Backtest thoroughly before implementing in live trading

Market conditions can change rapidly, affecting indicator performance

Disclaimer ⚠️

Past performance is not indicative of future results. Trading involves substantial risk of loss and is not suitable for all investors. The information provided by this indicator should not be considered as financial advice. Always conduct your own research.

No indicator guarantees profitable trades - Always use proper risk management! 🛡️

Luma DCA Simulator (BTC only)Luma DCA Simulator – Guide

What is the Luma DCA Simulator?

The Luma DCA Tracker shows how regular Bitcoin investments (Dollar Cost Averaging) would have developed over a freely selectable period – directly in the chart, transparent and easy to follow.

Settings Overview

1. Investment amount per interval

Specifies how much capital is invested at each purchase (e.g. 100).

2. Start date

Defines the point in time from which the simulation begins – e.g. 01.01.2020.

3. Investment interval

Determines how frequently investments are made:

– Daily

– Weekly

– Every 14 days

– Monthly

4. Language

Switches the info box display between English and German.

5. Show investment data (optional)

If activated, the chart will display additional values such as total invested capital, BTC amount, current value, and profit/loss.

What the Chart Displays

Entry points: Each DCA purchase is marked as a point in the price chart.

Average entry price: An orange line visualizes the evolving DCA average.

Info box (bottom left) with a live summary of:

– Total invested capital

– Total BTC acquired

– Average entry price

– Current portfolio value

– Profit/loss in absolute terms and percentage

Note on Accuracy

This simulation is for illustrative purposes only.

Spreads, slippage, fees, and tax effects are not included.

Actual results may vary.

Technical Note

For daily or weekly intervals, the chart timeframe should be set to 1 day or lower to ensure all purchases are accurately included.

Larger timeframes (e.g. weekly or monthly charts) may result in missed investments.

Currency Handling

All calculations are based on the selected chart symbol (e.g. BTCUSD, BTCEUR, BTCUSDT).

The displayed currency is automatically determined by the chart used.

Luma DCA Tracker (BTC)Luma DCA Tracker (BTC) – User Guide

Function

This indicator simulates a regular Bitcoin investment strategy (Dollar Cost Averaging). It calculates and visualizes:

Accumulated BTC amount

Average entry price

Total amount invested

Current portfolio value

Profit/loss in absolute and percentage terms

Settings

Investment per interval

Fixed amount to be invested at each interval (e.g., 100 USD)

Start date

The date when DCA simulation begins

Investment interval

Choose between:

daily, weekly, every 14 days, or monthly

Show investment data

Displays additional chart lines (total invested, value, profit, etc.)

Chart Elements

Orange line: Average DCA entry price

Grey dots: Entry points based on selected interval

Info box (bottom left): Live summary of all key values

Notes

Purchases are simulated at the closing price of each interval

No fees, slippage, or taxes are included

The indicator is a simulation only and not linked to an actual portfolio

X-Day Capital Efficiency ScoreThis indicator helps identify the Most Profitable Movers for Your fixed Capital (ie, which assets offer the best average intraday profit potential for a fixed capital).

Unlike traditional volatility indicators (like ATR or % change), this script calculates how much real dollar profit you could have made each day over a custom lookback period — assuming you deployed your full capital into that ticker daily.

How it works:

Calculates the daily intraday range (high − low)

Filters for clean candles (where body > 60% of the candle range)

Assumes you invested the full amount of capital ($100K set as default) on each valid day

Computes an average daily profit score based on price action over the selected period (default set to 20 days)

Plots the score in dollars — higher = more efficient use of capital

Why It’s Useful:

Compare tickers based on real dollar return potential — not just % volatility

Spot low-priced, high-volatility stocks that are better suited for intraday or momentum trading

Inputs:

Capital ($): Amount you're hypothetically deploying (e.g., 100,000)

Look Back Period: Number of past days to average over (e.g., 20)

Futures Margin Lookup TableThis script applies a table to your chart, which provides the intraday and overnight margin requirements of the currently selected symbol.

In this indicator the user must provide the broker data in the form of specifically formatted text blocks. The data for which should be found on the broker website under futures margin requirements.

The purpose for it's creation is due to the non-standard way each individual broker may price their margins and lack of information within TradingView when connected to some (maybe all) brokers, including during paper trading, as the flat percentage rule is not accurate.

An example of information could look like this

MES;Micro S&P;$50;$2406

ES;E-Mini S&P;$500;$24,053

GC;Gold;$500;$16500

NQ;E-Mini Nasdaq;$1,000;$34,810

FDAX;Dax Index;€2,000;€44,311

Each symbol begins a new line, and the values on that line are separated by semicolons (;)

Each line consists of the following...

SYMBOL : Search string used to match to the beginning of the current chart symbol.

NAME: Human readable name

INTRA: Intraday trading margin requirement per contract

OVERNIGHT: Overnight trading margin requirement per contract

The script simply finds a matching line within your provided information using the current chart symbol.

So for example the continuous chart for

NQ1!

would match to the user specified line starting with NQ... as would the individual contract dates such as NQM2025, NQK2025, etc.

NOTES:

There is a possibility that symbols with similar starting characters could match. If this is the case put the longer symbol higher in the list.

There is also a line / character limit to the text input fields within pinescript. Ensure the text you enter / paste into them is not truncated. If so there are 3 input fields for just this purpose. Find the last complete line and continue the remaining symbol lines on the subsequent inputs.

MÈGAS ALGO : MÈGAS Engine [STRATEGY]Overview

The MÈGAS Engine is an advanced algorithmic trading system that integrates a range of technical analysis tools to pinpoint high-probability opportunities in the market.

Key Features

Core Signal Generation:

-Structure Break Detection: Advanced breakout identification with adjustable

sensitivity controls

-Dual-Direction Analysis: Separate bullish and bearish signal parameters with customizable delta

thresholds and depth settings

-Dynamic Parameter Management: OverfitShield technology with pulsewave parameter cycling

to reduce overfitting risks

Filtering Alghoritm:

-Volatility Filter: Rogers-Satchell volatility estimation with RSI-based normalization to avoid

trading in unfavorable market conditions

-Volume Confirmation: Cumulative volume analysis ensuring adequate liquidity support for trade

entries

OverfitShield Method:

OverfitShield is a built-in function within the trading strategy designed to reduce overfitting bias by introducing parameter variability during execution. When the "variable" mode is activated, instead of relying on fixed values for key strategy parameters the system dynamically selects values from customizable ranges.

This approach mimics real-world market uncertainty and ensures that the strategy does not become overly dependent on a single optimal value found during backtesting — making it more robust across different market conditions and time periods.

Position Management

-Customizable Exit Set-up

The exit logic can be customized to 'CONTINUE', 'TAKE PROFIT', or 'TRAILING PROFIT' to suit

your trading approach and maximize performance.

-CONTINUE Mode:

This mode does not use predefined take profit levels. Instead, it remains in the market as long as the trend persists. By avoiding fixed exit points, this approach is often the most effective in backtesting, as it allows positions to run in favorable trends for longer periods.

-TAKE PROFIT Mode:

This mode allows you to set multiple grid-like take profit levels at different price points, effectively creating a multi-tier exit strategy. You can specify the number of profit levels you want, along with the percentage step between each level. This structured approach can be beneficial for capturing incremental profits in a trending market while allowing for more flexibility in trade management.

-TRAILING PROFIT Mode:

Similar to the Take Profit mode, this option allows you to set the trailing stop levels. The trailing stop moves with the market, ensuring that you lock in profits as the price continues to move in your favor. Once a profit level is hit, the trailing stop "follows" the price movement, adjusting dynamically to safeguard profits as the trade progresses.

3. Customizable Insight Alerts

Traders can configure personalized alert messages for every strategy action, including entries, exits, and profit targets. These alerts are fully compatible with TradingView's webhook system.

Advantages

Customization: Fully customizable exit set-up and alerts allow traders to tailor the strategy to their personal trading objectives.

How It Works — Step by Step

Step 1: Apply the Strategy

Open the chart for your selected symbol and timeframe. Add the MÈGAS Engine to the chart.

Step 2:Backtesting and Optimization

Run a full backtest and optimize the strategy parameters across the chosen trading pairs to:

Identify robust settings that perform consistently well

Avoid overfitting through validation techniques

Select the most profitable and stable configuration for live or forward testing.

Step 3: Review Results and Alerts

Check the backtest results on the chart and confirm that the custom alert messages are displaying as expected. This helps verify that everything is functioning correctly before moving forward.

Step 4: Configure Portfolio Management

Set up the exit logic based on your specific requirements. Tailor the exit strategy to match your trading approach, whether you prefer predefined take profit levels, trailing stops, or a trend-following method. This flexibility ensures the exit logic aligns with your overall strategy for optimal performance.

Open the strategy settings window. In the dedicated portfolio management section, choose your preferred capital allocation method based on your trading style and risk preferences. Once set, save the configuration as the default.

Step 5: Set Up Alerts

Click "Add Alert" on the strategy

-In the message field, use: {{strategy.order.comment}}

Under the Notifications tab:

-Enable Webhook URL

-Enter your external webhook address

-Click 'Create' to activate alerts for your strategy

Please Note:

The results and visualizations presented are derived from optimized backtesting iterations using historical and paid real-time market data sourced via TradingView. While these results are intended to demonstrate potential performance, they do not guarantee future outcomes or accuracy. Past performance is not indicative of future results, and all trading involves risk.

We strongly recommend that users review and adjust the Properties within the script settings to align with their specific account configurations and preferred trading platforms. This ensures that the strategy outputs are reflective of real-world conditions and enhances the reliability of the results obtained. Use this tool responsibly and at your own risk.

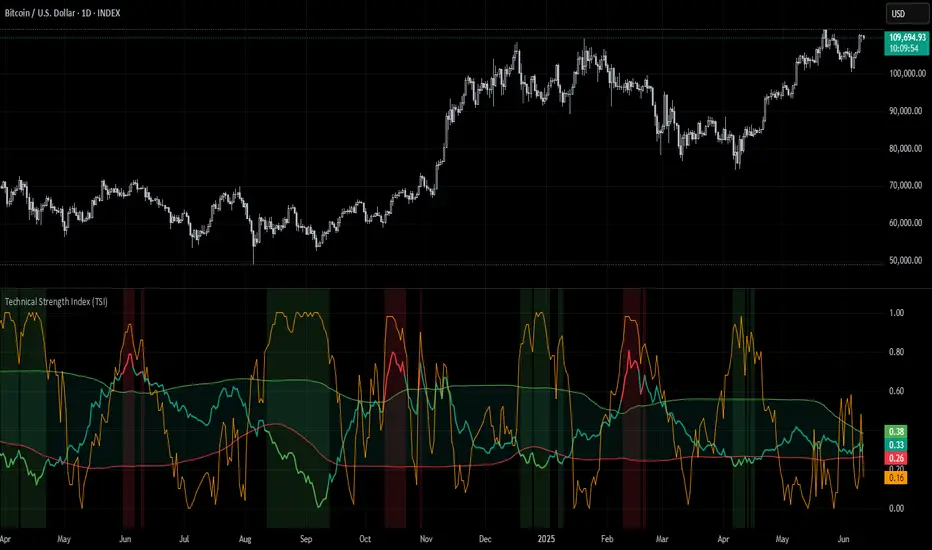

Technical Strength Index (TSI)📘 TSI with Dynamic Bands – Technical Strength Index

The TSI with Dynamic Bands is a multi-factor indicator designed to measure the statistical strength and structure of a trend. It combines several quantitative metrics into a single, normalized score between 0 and 1, allowing traders to assess the technical quality of market moves and detect overbought/oversold conditions with adaptive precision.

🧠 Core Components

This indicator draws from the StatMetrics library, blending:

📈 Trend Persistence: via the Hurst exponent, indicating whether price action is mean-reverting or trending.

📉 Risk-Adjusted Volatility: via the inverted , rewarding smoother, less erratic price movement.

🚀 Momentum Strength: using a combination of directional momentum and Z-score–normalized returns.

These components are normalized and averaged into the TSI line.

🎯 Features

TSI Line: Composite score of trend quality (0 = weak/noise, 1 = strong/structured).

Dynamic Bands: Mean ± 1 standard deviation envelopes provide adaptive context.

Overbought/Oversold Detection: Based on a rolling quantile (e.g. 90th/10th percentile of TSI history).

Signal Strength Bar (optional): Measures how statistically extreme the current TSI value is, helping validate confidence in trade setups.

Dynamic Color Cues: Background and bar gradients help visually identify statistically significant zones.

📈 How to Use

Look for overbought (red background) or oversold (green background) conditions as potential reversal zones.

Confirm trend strength with the optional signal strength bar — stronger values suggest higher signal confidence.

Use the TSI line and context bands to filter out noisy ranges and focus on structured price moves.

⚙️ Inputs

Lookback Period: Controls the smoothing and window size for statistical calculations.

Overbought/Oversold Quantiles: Adjust the thresholds for signal zones.

Plot Signal Strength: Enable or disable the signal confidence bar.

Overlay Signal Strength: Show signal strength in the same panel (compact) or not (cleaner TSI-only view).

🛠 Example Use Cases

Mean reversion traders identifying reversal zones with statistical backing

Momentum/Trend traders confirming structure before entries

Quantitative dashboards or multi-asset screening tools

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any financial instrument.

This AI is not a financial advisor; please consult your financial advisor for personalized advice.

Zuper Custom Index (Up to 40 Stocks)Description:

This indicator empowers you to create your own custom index from up to 40 stocks, with full control over the weight of each component. Whether you want to track a sector, a basket of favourites, or build your own benchmark, this tool gives you the flexibility and visualisation you need—all directly on your TradingView chart.

Key Features:

Supports Up to 40 Stocks:

Combine up to 40 different symbols into a single, custom index.

Flexible Weighting:

Assign a custom percentage weight to each stock. The script automatically normalizes your weights to ensure the index always sums to 100%.

Candlestick or Line Chart Display:

Choose between a candlestick chart (showing open, high, low, close of the index) or a simple line chart (close only) for your custom index.

Dynamic Rebalancing:

Change weights or symbols at any time; the index recalculates instantly.

Easy Symbol Input:

Add or remove stocks with simple input fields—no code editing required.

Perfect for Sector Analysis & Custom Baskets:

Track sectors, strategies, or any group of assets you care about.

How to Use:

Add the Indicator to Your Chart.

Enter Up to 40 Stock Symbols in the input fields.

Assign Weights (as percentages) to each symbol.

If all weights are left at zero, the index will use equal weighting.

If you enter custom weights, they will be automatically normalized.

Choose Your Display Type:

Select between a candlestick or line chart for your index.

Analyze Your Custom Index!

Use Cases:

Build your own sector or thematic index.

Track a custom ETF or fund composition.

Compare your portfolio’s performance as a single chart.

Visualize the impact of different weightings on a basket of stocks.

Notes:

The indicator uses TradingView’s latest Pine Script version for maximum performance and flexibility.

You can use any valid TradingView symbol (stocks, ETFs, indices, etc.).

For best results, ensure all symbols are available on your selected timeframe and exchange.

Create, visualize, and analyze your own custom indices—right on your TradingView chart!

SmartPhase Analyzer📝 SmartPhase Analyzer – Composite Market Regime Classifier

SmartPhase Analyzer is an adaptive regime classification tool that scores market conditions using a customizable set of statistical indicators. It blends multiple normalized metrics into a composite score, which is dynamically evaluated against rolling statistical thresholds to determine the current market regime.

✅ Features:

Composite score calculated from 13+ toggleable statistical indicators:

Sharpe, Sortino, Omega, Alpha, Beta, CV, R², Entropy, Drawdown, Z-Score, PLF, SRI, and Momentum Rank

Uses dynamic thresholds (mean ± std deviation) to classify regime states:

🟢 BULL – Strongly bullish

🟩 ACCUM – Mildly bullish

⚪ NEUTRAL – Sideways

🟧 DISTRIB – Mildly bearish

🔴 BEAR – Strongly bearish

Color-coded histogram for composite score clarity

Real-time regime label plotted on chart

Benchmark-aware metrics (Alpha, Beta, etc.)

Modular design using the StatMetrics library by RWCS_LTD

🧠 How to Use:

Enable/disable metrics in the settings panel to customize your composite model

Use the composite histogram and regime background for discretionary or systematic analysis

⚠️ Disclaimer: